CPA Australia Advanced Taxation: International Tax & Super Solution

VerifiedAdded on 2023/04/24

|11

|2716

|405

Case Study

AI Summary

This CPA Australia Advanced Taxation assignment presents a case study involving Dr. Peter Wong, an Australian pathologist working abroad, and Joseph Conti, an Australian resident receiving a superannuation lump sum. The solution analyzes Dr. Wong's residency status between 2015 and 2018, calculating his Australian assessable income for those years based on salary, dividends, interest, and rental income. It applies relevant legislation and case law to determine his residency under the ITAA 1936. Furthermore, the assignment calculates Joseph Conti's maximum tax payable on his superannuation lump sum benefit, considering his age, pre-July 1983 component, and undeducted contributions, while excluding the Medicare Levy. The analysis references relevant sections of tax legislation to support the calculations and conclusions.

CPA AUSTRALIA

ADVANCED TAXATION SUPPLEMENT

ASSESSMENT TEMPLATE

CPA Australia ID:

Candidate name:

Assessment due date:

ASSESSOR USE ONLY

First Attempt Written assessment (final grade): Pass / Fail

Grade:

Second Attempt Written assessment (final grade): Pass / Fail

Grade:

Any additional comments:

Participant Outcome: Pass / Fail

(Please circle one)

(Note: Participant is only competent when all competencies have been covered.)

Date:

Assessor name: Assessor signature:

By submitting my written assessment for marking, I authorise CPA Australia to release a copy

of this work to external parties for the purpose of assessment. I also certify that the attached

work is my own except where I have made due reference to external sources. I confirm that the

work contains no plagiarism and that I have kept a copy of this assignment for my records.

ADVANCED TAXATION SUPPLEMENT

ASSESSMENT TEMPLATE

CPA Australia ID:

Candidate name:

Assessment due date:

ASSESSOR USE ONLY

First Attempt Written assessment (final grade): Pass / Fail

Grade:

Second Attempt Written assessment (final grade): Pass / Fail

Grade:

Any additional comments:

Participant Outcome: Pass / Fail

(Please circle one)

(Note: Participant is only competent when all competencies have been covered.)

Date:

Assessor name: Assessor signature:

By submitting my written assessment for marking, I authorise CPA Australia to release a copy

of this work to external parties for the purpose of assessment. I also certify that the attached

work is my own except where I have made due reference to external sources. I confirm that the

work contains no plagiarism and that I have kept a copy of this assignment for my records.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advanced Taxation Supplement - 2018

INTERNATIONAL TAX FUNDAMENTALS

Case Study

Dr Peter Wong is an Australian pathologist employed by Apex Laboratories Ltd (Apex) in Sydney since

2010. In June 2015 he accepted a 2-year research fellowship at a New York university, starting from

01 July 2015.

Willing to keep Dr Wong as an employee during his time overseas, Apex offered him a part-time

position, working remotely from New York and requiring him to travel to Sydney for project

meetings every 8 weeks.

After accepting the new work conditions, Dr Wong leased his Sydney apartment, sold his car and

moved to New York on 1 July 2015. Since then, his income consisted of the following:

- Salaries of $50,000 per year paid by Apex into his Australian bank account on a monthly

basis;

- Dividends of $3,000 from a US company, received on 1 October 2015 (no withholding tax was

applied in the US);

- Interest on his US bank deposits amounting to $180 (net of 10% US withholding tax);

received on 1 September 2015;

- Fully-franked dividends of $2,000 from an Australian company, received on 1 October 2017;

and

- Rents of $20,000 per year from his Sydney apartment paid in monthly instalments into his

Australian bank account.

In December 2015, the New York university offered Dr Wong a full time research position with an

annual salary of $100,000 plus travel allowance of $10,000 paid in January each year, as well as

sponsorship for a permanent residency visa. Dr Wong accepted the offer and on 1 January 2016 he

resigned from Apex. His Sydney apartment remained rented at the same price on a continuous basis

until 30 June 2018.

© CPA Australia Ltd 2018 1

INTERNATIONAL TAX FUNDAMENTALS

Case Study

Dr Peter Wong is an Australian pathologist employed by Apex Laboratories Ltd (Apex) in Sydney since

2010. In June 2015 he accepted a 2-year research fellowship at a New York university, starting from

01 July 2015.

Willing to keep Dr Wong as an employee during his time overseas, Apex offered him a part-time

position, working remotely from New York and requiring him to travel to Sydney for project

meetings every 8 weeks.

After accepting the new work conditions, Dr Wong leased his Sydney apartment, sold his car and

moved to New York on 1 July 2015. Since then, his income consisted of the following:

- Salaries of $50,000 per year paid by Apex into his Australian bank account on a monthly

basis;

- Dividends of $3,000 from a US company, received on 1 October 2015 (no withholding tax was

applied in the US);

- Interest on his US bank deposits amounting to $180 (net of 10% US withholding tax);

received on 1 September 2015;

- Fully-franked dividends of $2,000 from an Australian company, received on 1 October 2017;

and

- Rents of $20,000 per year from his Sydney apartment paid in monthly instalments into his

Australian bank account.

In December 2015, the New York university offered Dr Wong a full time research position with an

annual salary of $100,000 plus travel allowance of $10,000 paid in January each year, as well as

sponsorship for a permanent residency visa. Dr Wong accepted the offer and on 1 January 2016 he

resigned from Apex. His Sydney apartment remained rented at the same price on a continuous basis

until 30 June 2018.

© CPA Australia Ltd 2018 1

Advanced Taxation Supplement - 2018

QUESTION A

(a) Considering the facts above, advise Dr Wong on his residency status for the period between

1 July 2015 and 30 June 2018, applying legislation, case law and relevant tax rulings to

support your answer.

(12 marks)

Type your answer here. Ensure you answer all parts of the question.

Answer:

Issues:

Is the taxpayer would be treated as Australian resident under the definition of “section 6 (1)

of the ITAA 1997”?

Laws:

As defined under “section 6 (1) of the ITAA 1936” the Australian resident are those people

that are having their domicile in Australia, except when the commissioner is content that an individual’s

permanent place of residence is out of Australian. It includes those people that are actually living in

Australia, constantly or intermittently for more than of the income year, except when the taxation

commissioner is content that the usual place of residence of the taxpayer is out of Australia and the

taxpayer has no intention of takin up the Australian residency. To determine the residency status there

are some alternative test that are performed.

Resides Test

The first test is the Resides Test which is also known as the common law test. An individual

would be treated as the Australian resident for the purpose of taxation if a person is actually living in

Australia, irrespective of the nationality, citizenship or their location of the permanent home. As held in

“Applegate v FCT (1979)” the word reside signifies to dwell on permanent basis or for the

considerable period of time at particular period. The case provides the factors that are treated as

indicative of whether or not a person is living in Australia including the term of employment or

appointment. As held in “Sneddon v FCT (2012)” the court of law held that the taxpayer to be the

Australian resident since he maintained his home in Australia. Similarly, in “Murray v FCT (2012)” the

fact that the taxpayer has bought a residential property in the overseas was not treated as sufficient to

establish that the taxpayer was not the Australian resident.

The Domicile Test:

According to the “section 6 (1)” an individual would be considered as the Australian citizen if

an individual has their place of residence in Australia and they can prove that they have not

established a permanent place of residence out of Australia. The intention of an individual to stay

permanently instead of their stay being transitory is considered as important but cannot be treated as

the only factor that should be taken into the consideration. As per the IT 2650 factors such as actual

2 © CPA Australia Ltd 2018

QUESTION A

(a) Considering the facts above, advise Dr Wong on his residency status for the period between

1 July 2015 and 30 June 2018, applying legislation, case law and relevant tax rulings to

support your answer.

(12 marks)

Type your answer here. Ensure you answer all parts of the question.

Answer:

Issues:

Is the taxpayer would be treated as Australian resident under the definition of “section 6 (1)

of the ITAA 1997”?

Laws:

As defined under “section 6 (1) of the ITAA 1936” the Australian resident are those people

that are having their domicile in Australia, except when the commissioner is content that an individual’s

permanent place of residence is out of Australian. It includes those people that are actually living in

Australia, constantly or intermittently for more than of the income year, except when the taxation

commissioner is content that the usual place of residence of the taxpayer is out of Australia and the

taxpayer has no intention of takin up the Australian residency. To determine the residency status there

are some alternative test that are performed.

Resides Test

The first test is the Resides Test which is also known as the common law test. An individual

would be treated as the Australian resident for the purpose of taxation if a person is actually living in

Australia, irrespective of the nationality, citizenship or their location of the permanent home. As held in

“Applegate v FCT (1979)” the word reside signifies to dwell on permanent basis or for the

considerable period of time at particular period. The case provides the factors that are treated as

indicative of whether or not a person is living in Australia including the term of employment or

appointment. As held in “Sneddon v FCT (2012)” the court of law held that the taxpayer to be the

Australian resident since he maintained his home in Australia. Similarly, in “Murray v FCT (2012)” the

fact that the taxpayer has bought a residential property in the overseas was not treated as sufficient to

establish that the taxpayer was not the Australian resident.

The Domicile Test:

According to the “section 6 (1)” an individual would be considered as the Australian citizen if

an individual has their place of residence in Australia and they can prove that they have not

established a permanent place of residence out of Australia. The intention of an individual to stay

permanently instead of their stay being transitory is considered as important but cannot be treated as

the only factor that should be taken into the consideration. As per the IT 2650 factors such as actual

2 © CPA Australia Ltd 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advanced Taxation Supplement - 2018

and the intended length of overseas stay, whether any fixed homes has been established out of

Australia and the durability of a person’s relation with the place in Australia are also vital. Similarly, in

“Boer v FCT (2012)” and “Sully v FCT (2012)” the taxpayer was treated as Australian resident all

through their stay in abroad because they did not establish any permanent place of residence out of

Australia.

The 183 days’ test:

Under this test, a taxpayer is treated as Australian resident if the taxpayer during a relevant

income year spends more than one half of the income year in Australia and does not intends to take

up the residency out of Australia.

Application:

As evident in the current case Dr Peter Wong accepted the offer two-year research fellowship

in US. Prior to moving US he maintained his home in Australia by renting out the same. Dr Peter

Wong will be treated as Australian resident for the year 2015 under the Resides Test because he

maintained his home in Australia and the bank account. He also maintained his Australian bank

account where his salaries were paid. While from the year 2016 to 2018 Dr Peter Wong will not be

treated as Australian resident because he accepted the permanent visa that was offered by his

employer. Therefore, Dr Peter Wong is only resident of Australia for the year 2015 while from 2016

to 2018 he will be treated as non-resident of Australia.

On the other hand, the Domicile Test has been referred in the situation of Dr Peter Wong to

ascertain the residency position. With respect to “section 6 (1) of the ITAA 1936” for the year ended

2015, Dr Peter Wong have possessed the Australian domicile however following the acceptance of the

permanent visa in 2016 Dr Peter Wong ceases to be an Australian resident. With respect to the rule of

Thumb, Dr Peter Wong has established a fixed home out of Australia which reflected a durability and

endurance with his fixed place of abode outside Australia. Therefore, Dr Peter Wong is a non-resident

of Australia for the year 2016 to 2018.

Under the 183 day’s test Dr Peter Wong cannot be treated as Australian citizen because for

the year 2015 to 2018 he did not reside in Australia and hence he also took up the permanent place of

abode out of Australia. Therefore, Dr Peter Wong ceases to be an Australian resident.

Conclusion:

On a conclusive note Dr Peter Wong will be only treated as Australian resident under

“section 6 (1) of the ITAA 1936” for the year 2015. However, from the year 2016 onwards Dr Peter

Wong will be treated as non-resident of Australia because he has established a fixed or permanent

home out of Australia.

© CPA Australia Ltd 2018 3

and the intended length of overseas stay, whether any fixed homes has been established out of

Australia and the durability of a person’s relation with the place in Australia are also vital. Similarly, in

“Boer v FCT (2012)” and “Sully v FCT (2012)” the taxpayer was treated as Australian resident all

through their stay in abroad because they did not establish any permanent place of residence out of

Australia.

The 183 days’ test:

Under this test, a taxpayer is treated as Australian resident if the taxpayer during a relevant

income year spends more than one half of the income year in Australia and does not intends to take

up the residency out of Australia.

Application:

As evident in the current case Dr Peter Wong accepted the offer two-year research fellowship

in US. Prior to moving US he maintained his home in Australia by renting out the same. Dr Peter

Wong will be treated as Australian resident for the year 2015 under the Resides Test because he

maintained his home in Australia and the bank account. He also maintained his Australian bank

account where his salaries were paid. While from the year 2016 to 2018 Dr Peter Wong will not be

treated as Australian resident because he accepted the permanent visa that was offered by his

employer. Therefore, Dr Peter Wong is only resident of Australia for the year 2015 while from 2016

to 2018 he will be treated as non-resident of Australia.

On the other hand, the Domicile Test has been referred in the situation of Dr Peter Wong to

ascertain the residency position. With respect to “section 6 (1) of the ITAA 1936” for the year ended

2015, Dr Peter Wong have possessed the Australian domicile however following the acceptance of the

permanent visa in 2016 Dr Peter Wong ceases to be an Australian resident. With respect to the rule of

Thumb, Dr Peter Wong has established a fixed home out of Australia which reflected a durability and

endurance with his fixed place of abode outside Australia. Therefore, Dr Peter Wong is a non-resident

of Australia for the year 2016 to 2018.

Under the 183 day’s test Dr Peter Wong cannot be treated as Australian citizen because for

the year 2015 to 2018 he did not reside in Australia and hence he also took up the permanent place of

abode out of Australia. Therefore, Dr Peter Wong ceases to be an Australian resident.

Conclusion:

On a conclusive note Dr Peter Wong will be only treated as Australian resident under

“section 6 (1) of the ITAA 1936” for the year 2015. However, from the year 2016 onwards Dr Peter

Wong will be treated as non-resident of Australia because he has established a fixed or permanent

home out of Australia.

© CPA Australia Ltd 2018 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advanced Taxation Supplement - 2018

Assessor comments Grade

First Attempt

/ 12

Second Attempt

/ 12

4 © CPA Australia Ltd 2018

Assessor comments Grade

First Attempt

/ 12

Second Attempt

/ 12

4 © CPA Australia Ltd 2018

Advanced Taxation Supplement - 2018

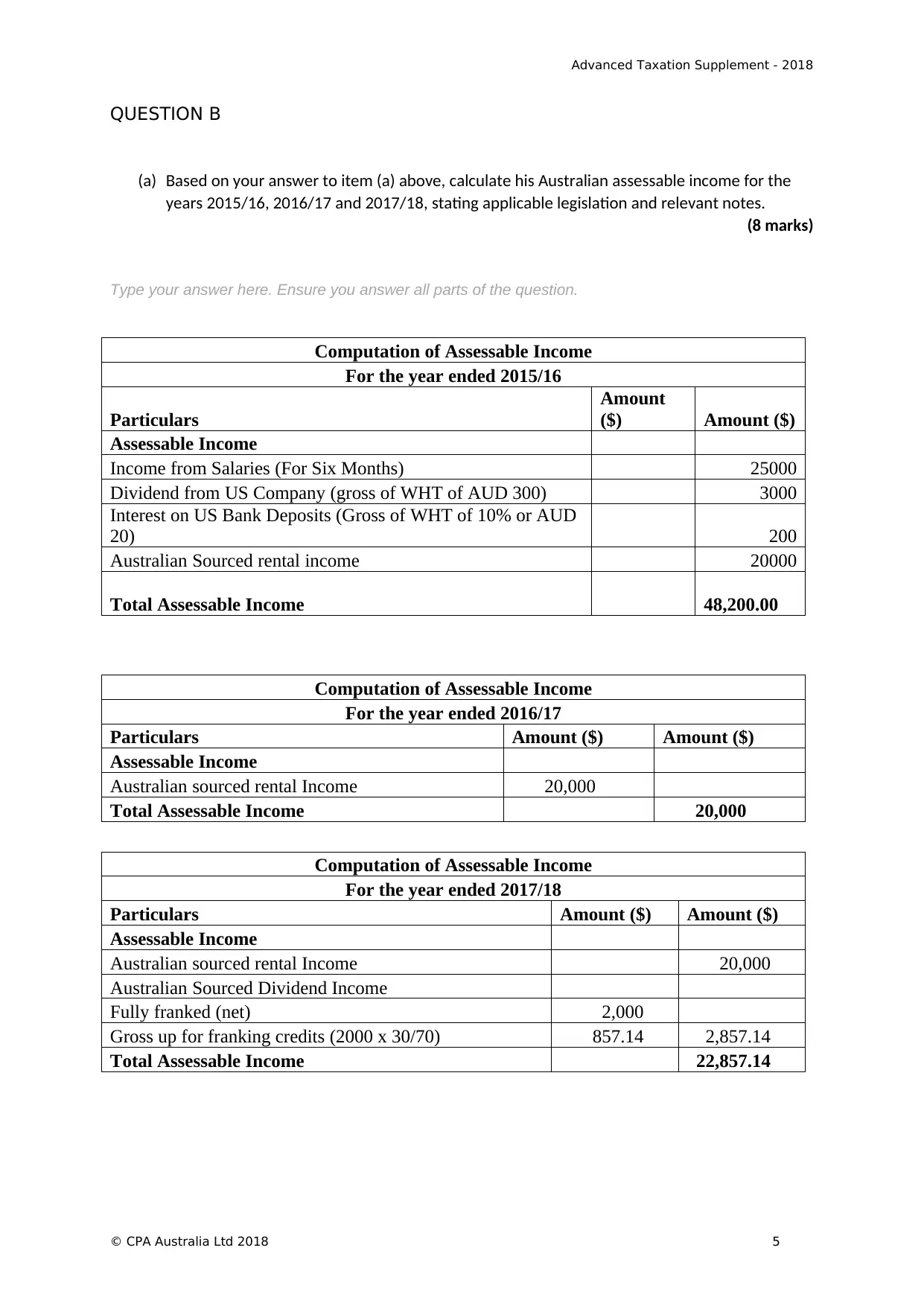

QUESTION B

(a) Based on your answer to item (a) above, calculate his Australian assessable income for the

years 2015/16, 2016/17 and 2017/18, stating applicable legislation and relevant notes.

(8 marks)

Type your answer here. Ensure you answer all parts of the question.

Computation of Assessable Income

For the year ended 2015/16

Particulars

Amount

($) Amount ($)

Assessable Income

Income from Salaries (For Six Months) 25000

Dividend from US Company (gross of WHT of AUD 300) 3000

Interest on US Bank Deposits (Gross of WHT of 10% or AUD

20) 200

Australian Sourced rental income 20000

Total Assessable Income 48,200.00

Computation of Assessable Income

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian sourced rental Income 20,000

Total Assessable Income 20,000

Computation of Assessable Income

For the year ended 2017/18

Particulars Amount ($) Amount ($)

Assessable Income

Australian sourced rental Income 20,000

Australian Sourced Dividend Income

Fully franked (net) 2,000

Gross up for franking credits (2000 x 30/70) 857.14 2,857.14

Total Assessable Income 22,857.14

© CPA Australia Ltd 2018 5

QUESTION B

(a) Based on your answer to item (a) above, calculate his Australian assessable income for the

years 2015/16, 2016/17 and 2017/18, stating applicable legislation and relevant notes.

(8 marks)

Type your answer here. Ensure you answer all parts of the question.

Computation of Assessable Income

For the year ended 2015/16

Particulars

Amount

($) Amount ($)

Assessable Income

Income from Salaries (For Six Months) 25000

Dividend from US Company (gross of WHT of AUD 300) 3000

Interest on US Bank Deposits (Gross of WHT of 10% or AUD

20) 200

Australian Sourced rental income 20000

Total Assessable Income 48,200.00

Computation of Assessable Income

For the year ended 2016/17

Particulars Amount ($) Amount ($)

Assessable Income

Australian sourced rental Income 20,000

Total Assessable Income 20,000

Computation of Assessable Income

For the year ended 2017/18

Particulars Amount ($) Amount ($)

Assessable Income

Australian sourced rental Income 20,000

Australian Sourced Dividend Income

Fully franked (net) 2,000

Gross up for franking credits (2000 x 30/70) 857.14 2,857.14

Total Assessable Income 22,857.14

© CPA Australia Ltd 2018 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advanced Taxation Supplement - 2018

Assessor comments S

First attempt

/ 8

Second attempt

/ 8

SUPERANNUATION

Case Study

Joseph Conti, an Australian resident, has been employed by Build Ltd, an Australian construction

company, since 1 July 1980. Due to a downturn in the economy, Build Ltd was restructured and

Joseph was offered an early retirement package.

Joseph accepted the package and retired on 30 June 2018, aged 58. Among other benefits, on that

date he received a lump sum payment of $500,000 from his complying taxed superannuation fund.

His latest superannuation account statement showed the following information:

Balance on 30 June 2007: $300,000 (including $33,313 pre-July 1983 component)

Balance on 30 June 2018: $500,000 (including $50,000 undeducted contributions made

between 2010 and 2015)

6 © CPA Australia Ltd 2018

Assessor comments S

First attempt

/ 8

Second attempt

/ 8

SUPERANNUATION

Case Study

Joseph Conti, an Australian resident, has been employed by Build Ltd, an Australian construction

company, since 1 July 1980. Due to a downturn in the economy, Build Ltd was restructured and

Joseph was offered an early retirement package.

Joseph accepted the package and retired on 30 June 2018, aged 58. Among other benefits, on that

date he received a lump sum payment of $500,000 from his complying taxed superannuation fund.

His latest superannuation account statement showed the following information:

Balance on 30 June 2007: $300,000 (including $33,313 pre-July 1983 component)

Balance on 30 June 2018: $500,000 (including $50,000 undeducted contributions made

between 2010 and 2015)

6 © CPA Australia Ltd 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advanced Taxation Supplement - 2018

QUESTION 1

On the basis of the above information, calculate Joseph’s maximum tax payable in relation to his

superannuation lump sum benefit, stating supporting legislation for each step of the calculation and

excluding Medicare Levy.

(10 marks)

Type your answer here. Ensure you answer all parts of the question.

Answer:

According to the Australian Taxation office the taxpayer receives the tax-free component of

the superannuation benefit that have attained their perseveration age but they are below the age of 60

years. These incomes are neither taxable income nor it is exempted income. As stated under the

section 307-215 the taxable component represents the value of the superannuation interest following

the deduction of the tax free component of the interest. As explained under the section 307-275 (1)), it

is noteworthy to denote that the taxable component of the superannuation benefit comprises of the

element that are taxed in the fund or comprises of the element that are untaxed or not taxed under the

super fund. On a wider note the element taxed in the superannuation fund represents the one that has

carried tax in the fund either due to the deductible contributions or because of the income that are

comprising in the fund which is the subject to tax in the fund. The element that are taxed in the fund is

also levied for taxation purpose in the hands of recipient at the lower rate than the element tax is not

taxed in the fund based on the reason that the element carries tax in the fund’s hand.

As stated by the Australian taxation office majority of the super that is held in the fund would

be in the form of preserved benefits. The access to the superannuation benefits is usually restricted to

the members that have attained the age of preservation. An individual’s age of preservation ranges

between the age of 55 years to 60 years depending upon the age of date of birth. As understood in the

current case of Joseph he has attained the preservation age of 58 and hence he is allowed to obtain

the super benefits relating to the lump sum that is received by him from the lump sum payment of

$500,000.

According to the section 301-15 the superannuation benefit might be considered as the lump

sum or superannuation income stream benefit. As per the section 301-20 (2), (3)) up to a certain low

rate limit a low rate cap amount is applied for tax offset. This helps in assuring that the tax rate on that

part of lump sum constitute the element taxed in the fund does not goes past 0%.

In the current case Joseph receives the superannuation lump sum of $500,000. A low rate cap

with respect to section 301-20 (2), (3)) is applied in case of Joseph with the effective tax rate of 15%

excluding the Medicare levy of 2%. Furthermore, the case study provides that the balances in the

superannuation fund during the year ended 30 June 2018 stood 500,000 which also comprised of the

undeducted contributions that was made by Joseph. Additionally, a Pre-July $33,313 component was

© CPA Australia Ltd 2018 7

QUESTION 1

On the basis of the above information, calculate Joseph’s maximum tax payable in relation to his

superannuation lump sum benefit, stating supporting legislation for each step of the calculation and

excluding Medicare Levy.

(10 marks)

Type your answer here. Ensure you answer all parts of the question.

Answer:

According to the Australian Taxation office the taxpayer receives the tax-free component of

the superannuation benefit that have attained their perseveration age but they are below the age of 60

years. These incomes are neither taxable income nor it is exempted income. As stated under the

section 307-215 the taxable component represents the value of the superannuation interest following

the deduction of the tax free component of the interest. As explained under the section 307-275 (1)), it

is noteworthy to denote that the taxable component of the superannuation benefit comprises of the

element that are taxed in the fund or comprises of the element that are untaxed or not taxed under the

super fund. On a wider note the element taxed in the superannuation fund represents the one that has

carried tax in the fund either due to the deductible contributions or because of the income that are

comprising in the fund which is the subject to tax in the fund. The element that are taxed in the fund is

also levied for taxation purpose in the hands of recipient at the lower rate than the element tax is not

taxed in the fund based on the reason that the element carries tax in the fund’s hand.

As stated by the Australian taxation office majority of the super that is held in the fund would

be in the form of preserved benefits. The access to the superannuation benefits is usually restricted to

the members that have attained the age of preservation. An individual’s age of preservation ranges

between the age of 55 years to 60 years depending upon the age of date of birth. As understood in the

current case of Joseph he has attained the preservation age of 58 and hence he is allowed to obtain

the super benefits relating to the lump sum that is received by him from the lump sum payment of

$500,000.

According to the section 301-15 the superannuation benefit might be considered as the lump

sum or superannuation income stream benefit. As per the section 301-20 (2), (3)) up to a certain low

rate limit a low rate cap amount is applied for tax offset. This helps in assuring that the tax rate on that

part of lump sum constitute the element taxed in the fund does not goes past 0%.

In the current case Joseph receives the superannuation lump sum of $500,000. A low rate cap

with respect to section 301-20 (2), (3)) is applied in case of Joseph with the effective tax rate of 15%

excluding the Medicare levy of 2%. Furthermore, the case study provides that the balances in the

superannuation fund during the year ended 30 June 2018 stood 500,000 which also comprised of the

undeducted contributions that was made by Joseph. Additionally, a Pre-July $33,313 component was

© CPA Australia Ltd 2018 7

Advanced Taxation Supplement - 2018

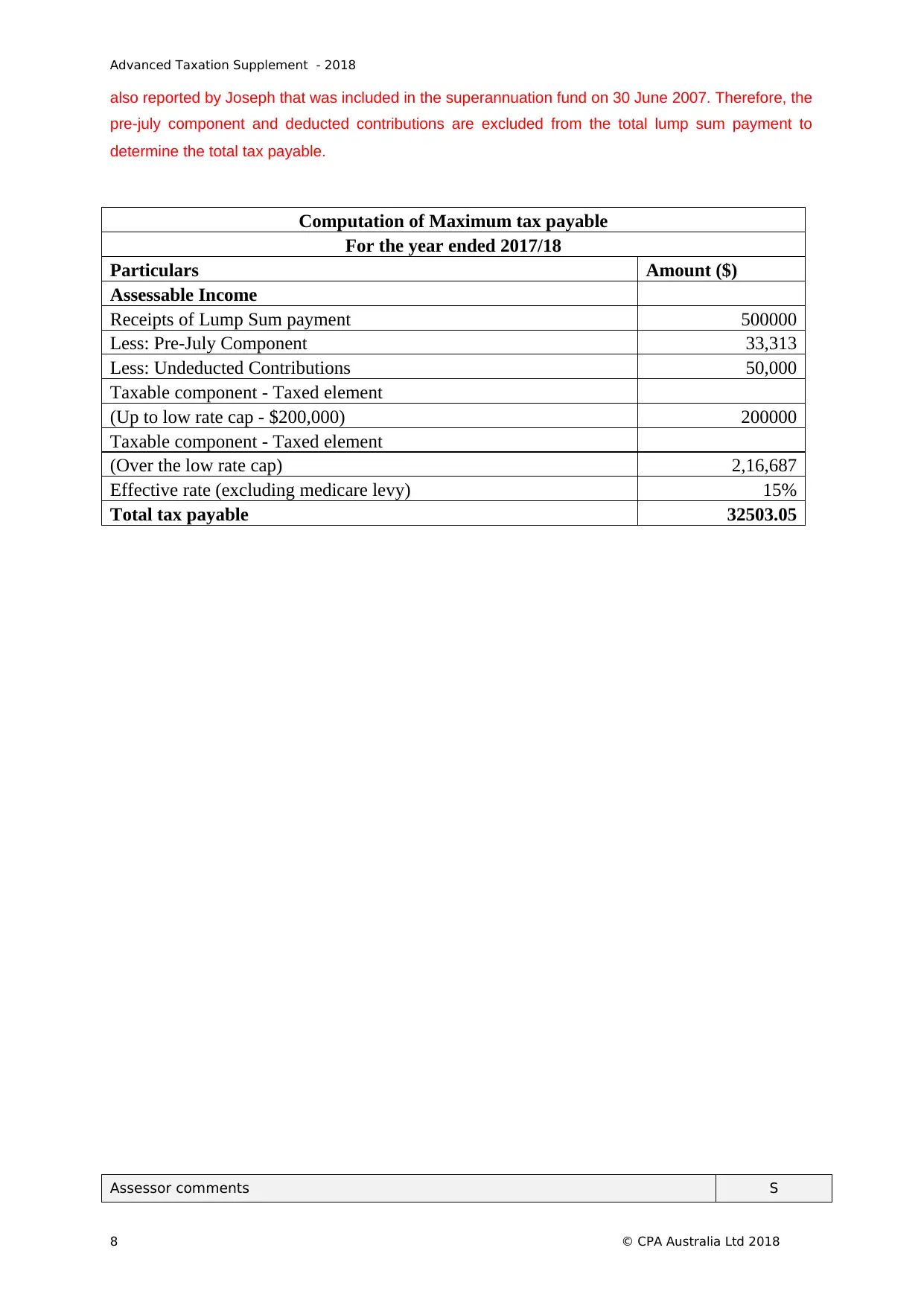

also reported by Joseph that was included in the superannuation fund on 30 June 2007. Therefore, the

pre-july component and deducted contributions are excluded from the total lump sum payment to

determine the total tax payable.

Computation of Maximum tax payable

For the year ended 2017/18

Particulars Amount ($)

Assessable Income

Receipts of Lump Sum payment 500000

Less: Pre-July Component 33,313

Less: Undeducted Contributions 50,000

Taxable component - Taxed element

(Up to low rate cap - $200,000) 200000

Taxable component - Taxed element

(Over the low rate cap) 2,16,687

Effective rate (excluding medicare levy) 15%

Total tax payable 32503.05

Assessor comments S

8 © CPA Australia Ltd 2018

also reported by Joseph that was included in the superannuation fund on 30 June 2007. Therefore, the

pre-july component and deducted contributions are excluded from the total lump sum payment to

determine the total tax payable.

Computation of Maximum tax payable

For the year ended 2017/18

Particulars Amount ($)

Assessable Income

Receipts of Lump Sum payment 500000

Less: Pre-July Component 33,313

Less: Undeducted Contributions 50,000

Taxable component - Taxed element

(Up to low rate cap - $200,000) 200000

Taxable component - Taxed element

(Over the low rate cap) 2,16,687

Effective rate (excluding medicare levy) 15%

Total tax payable 32503.05

Assessor comments S

8 © CPA Australia Ltd 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advanced Taxation Supplement - 2018

First Attempt

/ 10

Second

Attempt

/ 10

© CPA Australia Ltd 2018 9

First Attempt

/ 10

Second

Attempt

/ 10

© CPA Australia Ltd 2018 9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advanced Taxation Supplement - 2018

REFERENCES:

Barkoczy, S., 2016. Foundations of taxation law 2016. Oup catalogue.

Morgan, A., Mortimer, C. And Pinto, D., 2018. A practical introduction to Australian taxation

law 2018.

Sadiq, K., 2018. Australian tax law cases 2018. Thomson Reuters.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. And Pinto, D., 2016. Australian taxation

law 2016. Oup catalogue.

10 © CPA Australia Ltd 2018

REFERENCES:

Barkoczy, S., 2016. Foundations of taxation law 2016. Oup catalogue.

Morgan, A., Mortimer, C. And Pinto, D., 2018. A practical introduction to Australian taxation

law 2018.

Sadiq, K., 2018. Australian tax law cases 2018. Thomson Reuters.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. And Pinto, D., 2016. Australian taxation

law 2016. Oup catalogue.

10 © CPA Australia Ltd 2018

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.