Taxation Law Report: Australia's Dividend Imputation System Analysis

VerifiedAdded on 2021/05/31

|14

|3517

|326

Report

AI Summary

This report offers a comprehensive analysis of Australia's dividend imputation system, exploring its core functions and historical context. It delves into the reasons behind the system's introduction, primarily to address the double taxation of corporate profits, and details how franking credits operate to offset shareholder tax liabilities. The report examines the proposed reforms by the Labour party, focusing on the removal of imputation credit refunds for individuals and superannuation funds, and discusses the potential advantages and disadvantages of these policies. It further analyzes the attributes of a good tax system, evaluating the Labour party's proposals in terms of fiscal adequacy, economic growth, and fairness. The report concludes by assessing the overall impact of these policies on various stakeholders, including investors, charities, and the broader Australian economy.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Task A:.....................................................................................................................2

Current system of Dividend Imputation Functions:...............................................................2

Motive for Presenting Dividend Imputation in 1980:............................................................3

Proposed labour reformation to the dividend imputation system:.........................................4

Answer to task B:.......................................................................................................................5

Labour Policies Advantages and Disadvantages:..................................................................5

The advantages of labour Policy:...........................................................................................6

Removing imputation credit refunds:.....................................................................................6

Attributes of good tax policies:..............................................................................................7

Answer to Task C:......................................................................................................................8

Answer to question 1:.............................................................................................................8

Answer to question 2:.............................................................................................................8

Answer to question 3:.............................................................................................................8

Answer to question 4:.............................................................................................................9

Answer to question 5:.............................................................................................................9

Reference List:.........................................................................................................................11

Table of Contents

Answer to Task A:.....................................................................................................................2

Current system of Dividend Imputation Functions:...............................................................2

Motive for Presenting Dividend Imputation in 1980:............................................................3

Proposed labour reformation to the dividend imputation system:.........................................4

Answer to task B:.......................................................................................................................5

Labour Policies Advantages and Disadvantages:..................................................................5

The advantages of labour Policy:...........................................................................................6

Removing imputation credit refunds:.....................................................................................6

Attributes of good tax policies:..............................................................................................7

Answer to Task C:......................................................................................................................8

Answer to question 1:.............................................................................................................8

Answer to question 2:.............................................................................................................8

Answer to question 3:.............................................................................................................8

Answer to question 4:.............................................................................................................9

Answer to question 5:.............................................................................................................9

Reference List:.........................................................................................................................11

2TAXATION LAW

Answer to Task A:

Introduction:

The current report would be highlighting the present system of dividend imputation in

Australia. the report would seek to address the primary reason for introducing the dividend

imputation system and the process involved in the administering of the dividend imputation

system. The study would take into the consideration the proposal made by the labour policies

to the current system of dividends along with the advantages and disadvantages surrounding

the dividend imputation system. The report would be highlighting the attributes that is

required in the good in the tax system with appropriate reference to current proposal of the

dividend imputation made by the labour.

Current system of Dividend Imputation Functions:

Australian is viewed one of the few OECD countries that operate the system of full

dividend imputation (Barkoczy, 2014). The history of Australia’s imputation tax system

spans more that decades. While only some of the countries makes the use of dividend

imputation system, majority of the nations have certain structure to administer the issue

relating to the double taxation. There are other options that are commonly used namely the

rebates or the concessional mode of taxing the dividend income.

There are number of nations that does not consider dividend imputation in the

personal assessable income. The major reformations that was made in the dividend

imputation system operation includes the provision of rebate, where the allowable rebates

associated to franking credits before 1st July 2000 was capped in terms of the tax obligation of

the taxpayer with extra imputation credit was vanished (Coleman & Sadiq, 2013). During the

year 2000 in July a new system was introduced where the entire sum of franking credits was

refunded to the taxpayer even though the franking credit goes past the tax obligations.

Answer to Task A:

Introduction:

The current report would be highlighting the present system of dividend imputation in

Australia. the report would seek to address the primary reason for introducing the dividend

imputation system and the process involved in the administering of the dividend imputation

system. The study would take into the consideration the proposal made by the labour policies

to the current system of dividends along with the advantages and disadvantages surrounding

the dividend imputation system. The report would be highlighting the attributes that is

required in the good in the tax system with appropriate reference to current proposal of the

dividend imputation made by the labour.

Current system of Dividend Imputation Functions:

Australian is viewed one of the few OECD countries that operate the system of full

dividend imputation (Barkoczy, 2014). The history of Australia’s imputation tax system

spans more that decades. While only some of the countries makes the use of dividend

imputation system, majority of the nations have certain structure to administer the issue

relating to the double taxation. There are other options that are commonly used namely the

rebates or the concessional mode of taxing the dividend income.

There are number of nations that does not consider dividend imputation in the

personal assessable income. The major reformations that was made in the dividend

imputation system operation includes the provision of rebate, where the allowable rebates

associated to franking credits before 1st July 2000 was capped in terms of the tax obligation of

the taxpayer with extra imputation credit was vanished (Coleman & Sadiq, 2013). During the

year 2000 in July a new system was introduced where the entire sum of franking credits was

refunded to the taxpayer even though the franking credit goes past the tax obligations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Consequently, the shareholders did not have to shoulder the wastage of additional sum of

franking credit with the amount of imputation is retained by the taxpayer leading to marginal

personal tax rate lower than the legal corporation tax rate.

In Australia the system of dividend imputation requires a company to preserve the

records of franking credit which keeps the track of records associated to franking account

along with the record of income tax payment made to ATO (Grange et al., 2014). As evident

in the company’s franking account the balance of maximum franking amount credits is

reflected that is distributable to the shareholders. As an alternative a corporation is prohibited

from franking the dividends and the imputation credits attached to the dividends. A business

is prohibited from franking the dividends greater than the sum of corporation tax that is paid.

When an Australian resident company pays tax lower than the statutory rate of tax an

insufficient amount of franking credits would be reflected in the corporations franking credit

account in order to make the dividends completely franked (James, 2014). Likewise, where

the companies do not pay any sum of tax on income after applying the applicable tax offsets

the distributed amount of dividends must be unfranked. In Australia, the current dividend

system is viewed as the prepayment of tax in respect of the corporate profits since the

domestic shareholders usually pay taxes on the distributed company profits based on the

applicable marginal tax rates. It is worth mentioning that this view is applied on companies

where all the company’s shareholder is held as Australian resident for assessment purpose.

The dividend imputation system functions by providing the Australian corporations

with the facilities of issuing franked dividends to shareholders (Jover-Ledesma, 2014). This

constitutes dividends which is paid following tax resulting the shareholders to obtain the after

tax dividends together with franking credits signifying the tax of corporation that are paid on

incomes. In the current dividend imputation system, franking credits can be offset against the

Consequently, the shareholders did not have to shoulder the wastage of additional sum of

franking credit with the amount of imputation is retained by the taxpayer leading to marginal

personal tax rate lower than the legal corporation tax rate.

In Australia the system of dividend imputation requires a company to preserve the

records of franking credit which keeps the track of records associated to franking account

along with the record of income tax payment made to ATO (Grange et al., 2014). As evident

in the company’s franking account the balance of maximum franking amount credits is

reflected that is distributable to the shareholders. As an alternative a corporation is prohibited

from franking the dividends and the imputation credits attached to the dividends. A business

is prohibited from franking the dividends greater than the sum of corporation tax that is paid.

When an Australian resident company pays tax lower than the statutory rate of tax an

insufficient amount of franking credits would be reflected in the corporations franking credit

account in order to make the dividends completely franked (James, 2014). Likewise, where

the companies do not pay any sum of tax on income after applying the applicable tax offsets

the distributed amount of dividends must be unfranked. In Australia, the current dividend

system is viewed as the prepayment of tax in respect of the corporate profits since the

domestic shareholders usually pay taxes on the distributed company profits based on the

applicable marginal tax rates. It is worth mentioning that this view is applied on companies

where all the company’s shareholder is held as Australian resident for assessment purpose.

The dividend imputation system functions by providing the Australian corporations

with the facilities of issuing franked dividends to shareholders (Jover-Ledesma, 2014). This

constitutes dividends which is paid following tax resulting the shareholders to obtain the after

tax dividends together with franking credits signifying the tax of corporation that are paid on

incomes. In the current dividend imputation system, franking credits can be offset against the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

shareholder’s tax liability. Alternatively, if the liability to tax is exhausted dividends can be

redeemed in cash from ATO (Kenny, 2013). The functions of dividend imputation system is

reliant on the fundamentals of return on equity where income that are received from

corporations in the form of dividends must be taxed along with income based on taxpayers

marginal income tax.

Motive for Presenting Dividend Imputation in 1980:

The primary reason for introducing the dividend imputation was to manage the

problem of double taxation of organizations profits in comparison to the tax of

unincorporated enterprise (Krever, 2013). The dividend imputation system offers the

shareholders with the franking credits that can be counterbalanced alongside the individual

earnings tax obligations. However, upon the non-presence of the dividend imputation system

the profits of the corporations that is allocated to the shareholders of Australia would be

subjected to double taxation. This includes once at the company level and once at the

personal level.

The introduction of dividend imputation system has resulted in removal of previously

present distortion that offered incentives for financing debt. Interest is subtracted from the

company profits and taxes are levied once at the personal level.

Proposed labour reformation to the dividend imputation system:

The labour party announced a plan relating to the reformation of the dividend

imputation system in Australia (Morgan et al., 2013). In the current dividend imputation

system when a company pay dividends to its shareholders it has the choice of passing on the

credits to any sum of tax paid by the corporates on its profits. Under the current system if the

dividend imputation credit surpasses the tax liability of shareholders, the extra amount is

eligible for cash refund.

shareholder’s tax liability. Alternatively, if the liability to tax is exhausted dividends can be

redeemed in cash from ATO (Kenny, 2013). The functions of dividend imputation system is

reliant on the fundamentals of return on equity where income that are received from

corporations in the form of dividends must be taxed along with income based on taxpayers

marginal income tax.

Motive for Presenting Dividend Imputation in 1980:

The primary reason for introducing the dividend imputation was to manage the

problem of double taxation of organizations profits in comparison to the tax of

unincorporated enterprise (Krever, 2013). The dividend imputation system offers the

shareholders with the franking credits that can be counterbalanced alongside the individual

earnings tax obligations. However, upon the non-presence of the dividend imputation system

the profits of the corporations that is allocated to the shareholders of Australia would be

subjected to double taxation. This includes once at the company level and once at the

personal level.

The introduction of dividend imputation system has resulted in removal of previously

present distortion that offered incentives for financing debt. Interest is subtracted from the

company profits and taxes are levied once at the personal level.

Proposed labour reformation to the dividend imputation system:

The labour party announced a plan relating to the reformation of the dividend

imputation system in Australia (Morgan et al., 2013). In the current dividend imputation

system when a company pay dividends to its shareholders it has the choice of passing on the

credits to any sum of tax paid by the corporates on its profits. Under the current system if the

dividend imputation credit surpasses the tax liability of shareholders, the extra amount is

eligible for cash refund.

5TAXATION LAW

The proposal made by labour aims to remove the individual’s ability and

superannuation funds so that it can get the extra sum of imputation credits from 1st July 2019

that makes the imputation credits a non-refundable tax offsets (Woellner, 2013). However,

the reformation is not in the direction of charities and non-for profit entities. Another

proposal of labour includes the inclusion of self-managed super funds based on pension

mode. This includes turning into cash the whole sum of Australian shareholdings which can

be tax free and rolling over of cash would assist in freeing up the superannuation account

with large funds by allowing Australian shares as the favoured class of assets.

The proposal of labour also includes the new arrangement of the depreciation which

would held in rewarding the business to make investment in generous write off provision.

Such proposal would help the shareholders in 20% immediate reduction for new eligible

assets that has the worth of more than $20,000 (Woellner et al., 2014). The proposal made by

labour would held in reversing the change which is made to the policy as it would assist in

assuring that the individuals and the super funds would be able to claim refunds relating to

any sum of extra imputations credits which is not used in offsetting the tax obligations.

Answer to task B:

Labour Policies Advantages and Disadvantages:

The policies of labour suffers from disadvantages since it negatively creates an effect

on the cash refunds of the wealthy investors. There are policies that are viewed as bold and

probably held as unsafe since it results in negative effect on those people that are retired. The

policies of labour have been criticized because the policies have not been successful in

keeping with the negative gearing and capital gains tax (Pinto, 2013). Among the major

disadvantages of the labour policies is the objective of thrusting large sum of money in the

direction of older people that hardly has any need for it. These labour policies not only

The proposal made by labour aims to remove the individual’s ability and

superannuation funds so that it can get the extra sum of imputation credits from 1st July 2019

that makes the imputation credits a non-refundable tax offsets (Woellner, 2013). However,

the reformation is not in the direction of charities and non-for profit entities. Another

proposal of labour includes the inclusion of self-managed super funds based on pension

mode. This includes turning into cash the whole sum of Australian shareholdings which can

be tax free and rolling over of cash would assist in freeing up the superannuation account

with large funds by allowing Australian shares as the favoured class of assets.

The proposal of labour also includes the new arrangement of the depreciation which

would held in rewarding the business to make investment in generous write off provision.

Such proposal would help the shareholders in 20% immediate reduction for new eligible

assets that has the worth of more than $20,000 (Woellner et al., 2014). The proposal made by

labour would held in reversing the change which is made to the policy as it would assist in

assuring that the individuals and the super funds would be able to claim refunds relating to

any sum of extra imputations credits which is not used in offsetting the tax obligations.

Answer to task B:

Labour Policies Advantages and Disadvantages:

The policies of labour suffers from disadvantages since it negatively creates an effect

on the cash refunds of the wealthy investors. There are policies that are viewed as bold and

probably held as unsafe since it results in negative effect on those people that are retired. The

policies of labour have been criticized because the policies have not been successful in

keeping with the negative gearing and capital gains tax (Pinto, 2013). Among the major

disadvantages of the labour policies is the objective of thrusting large sum of money in the

direction of older people that hardly has any need for it. These labour policies not only

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

pushes the money out of the budget but also makes sure that the problems would remain long

after the conclusion of the party-political times.

The policy of the labour serves to remove the disparity of wealth among the peoples.

The policies of the labour regularly attracts the attention. The policies of the labour is been

under criticism and suffers from the disadvantage of inequality among the wealth in large

quantity since the labour policies introduces the intergenerational differences (Bankman et al.

2017). A widespread criticism has attracted the policies of labour as most of the rich

Australian are found to hold 40% of their national income however 65% of the Australian

health is held by those that are beyond the age of 55 years. The policies of labour has

attracted criticism in the areas of self-administered superfunds for pensions which might

result the holding members to loss the additional amount of franking credits.

Several researchers have stated that a question of fairness is bought forward in the

imputation credit that the labour has proposed. The proposed of making an effective

distribution of the assets of the deceased person resulting the other party to retain most of the

assets in the form of pension leading to the questions of imputation credit (McDaniel, 2017).

The policies of the labour have been criticized for hurrying towards revenue because it has

lost the regulation on expenditure and the measures of dividend imputation have merely

overlooked the fairness and was later categorized as the cruel tax grab.

The advantages of labour Policy:

Removing imputation credit refunds:

Apart from the disadvantages of the labour policies there are certain advantages of the

labour policies. The labour policies is advantageous in the direction that the imputation

credits and the superannuation funds is not anymore held as the refundable tax offset

(Schenk, 2017). This constitutes that the imputation credits can be used to reduce the

pushes the money out of the budget but also makes sure that the problems would remain long

after the conclusion of the party-political times.

The policy of the labour serves to remove the disparity of wealth among the peoples.

The policies of the labour regularly attracts the attention. The policies of the labour is been

under criticism and suffers from the disadvantage of inequality among the wealth in large

quantity since the labour policies introduces the intergenerational differences (Bankman et al.

2017). A widespread criticism has attracted the policies of labour as most of the rich

Australian are found to hold 40% of their national income however 65% of the Australian

health is held by those that are beyond the age of 55 years. The policies of labour has

attracted criticism in the areas of self-administered superfunds for pensions which might

result the holding members to loss the additional amount of franking credits.

Several researchers have stated that a question of fairness is bought forward in the

imputation credit that the labour has proposed. The proposed of making an effective

distribution of the assets of the deceased person resulting the other party to retain most of the

assets in the form of pension leading to the questions of imputation credit (McDaniel, 2017).

The policies of the labour have been criticized for hurrying towards revenue because it has

lost the regulation on expenditure and the measures of dividend imputation have merely

overlooked the fairness and was later categorized as the cruel tax grab.

The advantages of labour Policy:

Removing imputation credit refunds:

Apart from the disadvantages of the labour policies there are certain advantages of the

labour policies. The labour policies is advantageous in the direction that the imputation

credits and the superannuation funds is not anymore held as the refundable tax offset

(Schenk, 2017). This constitutes that the imputation credits can be used to reduce the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

payment of the tax nevertheless the taxpayers are unable to get the refunds relating to the

extra amount of the imputation credits. The labour policies would help the government in

saving a large chunk from their budget sum of $11.4 billion in the span of four years with $59

billion in the next decade.

The policies of the labour is only applicable for the superannuation funds and the

individuals. The policies of labour can be held as advantageous because income tax

exemption of charities and the non-for-profit institutes would be able to get the refunds

relating to the deductions of the gifts (Murphy & Higgins, 2016). An important reason for

justifying the policies of labour is that the principles of cost to budget as this is beneficial for

the present refunds. Furthermore, there are taxpayers that have higher amount of wealth and

the self-administered superfunds would help in recreating the matters of taxation. The

policies of the labour can appreciated in the advantageous manner as it helps in making sure

that both the parties gain from the superannuation as this would help the tax to remain stable

for short to medium term.

Attributes of good tax policies:

The taxation system should be in a way that it helps in meeting the requirements of

the increasing the activities of the state and achieving the purpose of the community. The

labour policies is held as productive in nature based on the fiscal adequacy (Schmalbeck et

al., 2015). The attributes of good tax system is to review complete growth of the country with

adequate sum of government in enhancing the development and welfare of the Australia. The

proposal of the labour in eliminating system of imputation credits refunds targets to lower the

payment of the tax with overall growth of the economy.

An attributes of the good tax system is under obligations of following the ideologies

of diversity. This constitutes that there should not be a single system of imposing taxes in

payment of the tax nevertheless the taxpayers are unable to get the refunds relating to the

extra amount of the imputation credits. The labour policies would help the government in

saving a large chunk from their budget sum of $11.4 billion in the span of four years with $59

billion in the next decade.

The policies of the labour is only applicable for the superannuation funds and the

individuals. The policies of labour can be held as advantageous because income tax

exemption of charities and the non-for-profit institutes would be able to get the refunds

relating to the deductions of the gifts (Murphy & Higgins, 2016). An important reason for

justifying the policies of labour is that the principles of cost to budget as this is beneficial for

the present refunds. Furthermore, there are taxpayers that have higher amount of wealth and

the self-administered superfunds would help in recreating the matters of taxation. The

policies of the labour can appreciated in the advantageous manner as it helps in making sure

that both the parties gain from the superannuation as this would help the tax to remain stable

for short to medium term.

Attributes of good tax policies:

The taxation system should be in a way that it helps in meeting the requirements of

the increasing the activities of the state and achieving the purpose of the community. The

labour policies is held as productive in nature based on the fiscal adequacy (Schmalbeck et

al., 2015). The attributes of good tax system is to review complete growth of the country with

adequate sum of government in enhancing the development and welfare of the Australia. The

proposal of the labour in eliminating system of imputation credits refunds targets to lower the

payment of the tax with overall growth of the economy.

An attributes of the good tax system is under obligations of following the ideologies

of diversity. This constitutes that there should not be a single system of imposing taxes in

8TAXATION LAW

order to fund for the government (Robin & Barkoczy, 2018). The policies of the labour is

held as having the attributes of good tax system because the rate of tax is created in a way

which would yield revenues for the government as well as it would also result in savings for

the government by $11.4 billion in a time of four years and $59 billion in the forthcoming

decade. It is largely found that the negative gearing, CGT discounts and the cost involved in

managing the matters of taxation continuously contained two wings of tax suggestion.

The taxation policies of labour is held as the good system of taxation because it

comprises of contributions made in the areas of government and the public revenue. With

varied amount of principles that is present in policies of labour represents the fiscal adequacy

principles with better satisfactions of the principles of equity (Robin, 2017). The policies of

the labour lowers the higher sum of dependence on one sole base to avoid opposing effect on

economy. The policies of labour acts as the tool for promoting economic expansion and

promotes capital formation. The policies of the labour are regarded a progressive tax system

with higher amount of taxes is imposed on those that generates higher income (Roe, 2017).

The labour philosophy behind progressive taxes is that people with higher income are

anticipated to contribute a wider share of public servants than those that are able to pay less

amount of tax.

Answer to Task C:

Answer to question 1:

For the financial year of 2015-16 and the rate of corporate tax for Sigma Pty Ltd

stands 30%. The primary reason for considering a corporate tax rate of 30% on Sigma Pty

Ltd is because the company has surpassed the annual turnover threshold limit of $10 million.

In the subsequent year of 2016/17 the Australian taxation office has defined that the form the

2016-17 income year the lower company tax rate is 27.5% (Blakelock & King, 2017). The

order to fund for the government (Robin & Barkoczy, 2018). The policies of the labour is

held as having the attributes of good tax system because the rate of tax is created in a way

which would yield revenues for the government as well as it would also result in savings for

the government by $11.4 billion in a time of four years and $59 billion in the forthcoming

decade. It is largely found that the negative gearing, CGT discounts and the cost involved in

managing the matters of taxation continuously contained two wings of tax suggestion.

The taxation policies of labour is held as the good system of taxation because it

comprises of contributions made in the areas of government and the public revenue. With

varied amount of principles that is present in policies of labour represents the fiscal adequacy

principles with better satisfactions of the principles of equity (Robin, 2017). The policies of

the labour lowers the higher sum of dependence on one sole base to avoid opposing effect on

economy. The policies of labour acts as the tool for promoting economic expansion and

promotes capital formation. The policies of the labour are regarded a progressive tax system

with higher amount of taxes is imposed on those that generates higher income (Roe, 2017).

The labour philosophy behind progressive taxes is that people with higher income are

anticipated to contribute a wider share of public servants than those that are able to pay less

amount of tax.

Answer to Task C:

Answer to question 1:

For the financial year of 2015-16 and the rate of corporate tax for Sigma Pty Ltd

stands 30%. The primary reason for considering a corporate tax rate of 30% on Sigma Pty

Ltd is because the company has surpassed the annual turnover threshold limit of $10 million.

In the subsequent year of 2016/17 the Australian taxation office has defined that the form the

2016-17 income year the lower company tax rate is 27.5% (Blakelock & King, 2017). The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

lower company tax rate of 27.5% is applicable for Sigma Pty Ltd because the annual turnover

for the company during the income year stood $9 million which is less than $10 million

threshold for small company.

Answer to question 2:

As per the Australian taxation office an Australian resident company that has decided

to join the dividend imputation system in Australia may be required to pay the franked

dividend. Taking into the consideration the current situation of Sigma Pty Ltd for every

financial year the imputation credits relating to the corporate tax rates for the financial year of

2016 and for the financial year of 2017 stands 27.5 per cent.

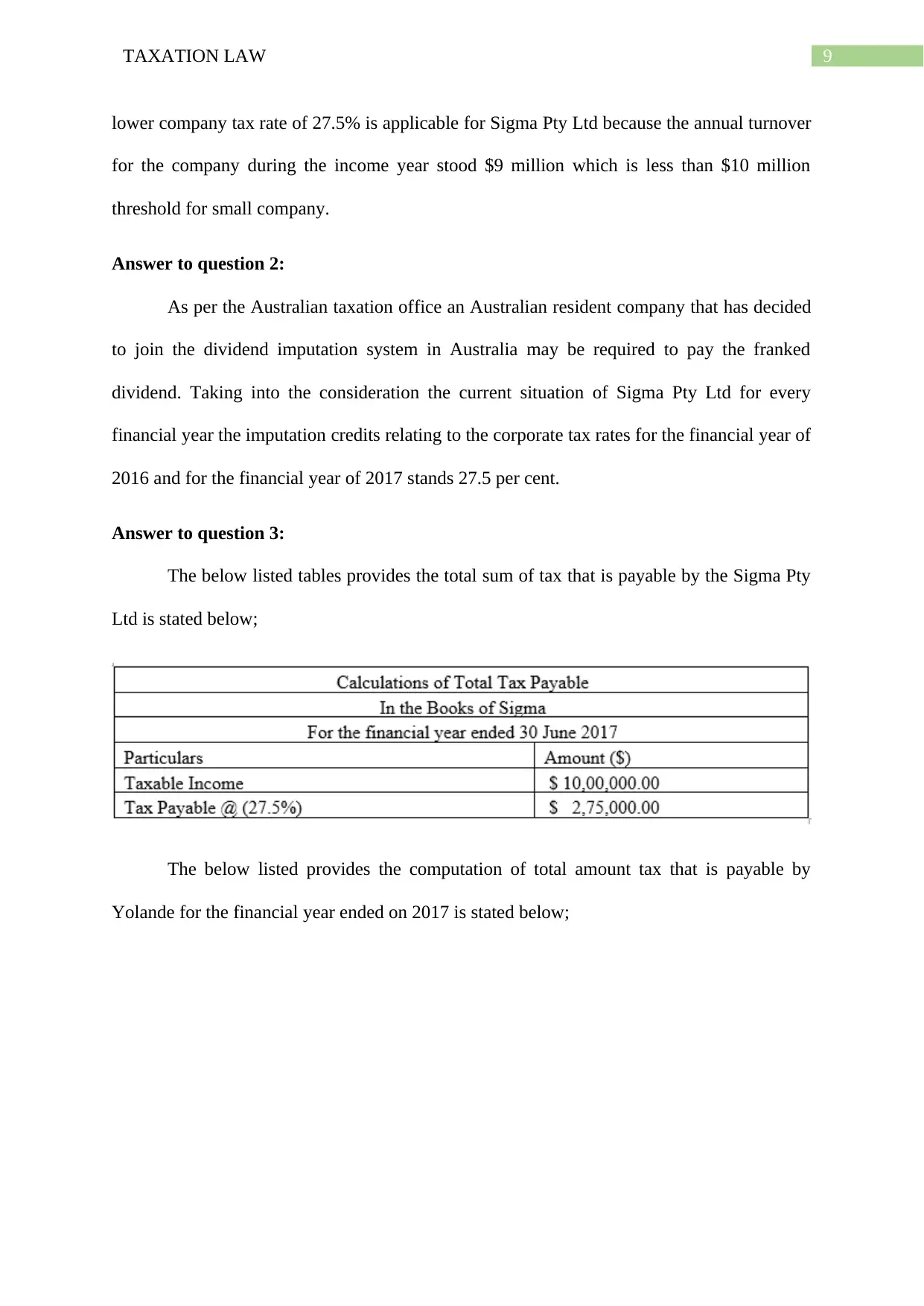

Answer to question 3:

The below listed tables provides the total sum of tax that is payable by the Sigma Pty

Ltd is stated below;

The below listed provides the computation of total amount tax that is payable by

Yolande for the financial year ended on 2017 is stated below;

lower company tax rate of 27.5% is applicable for Sigma Pty Ltd because the annual turnover

for the company during the income year stood $9 million which is less than $10 million

threshold for small company.

Answer to question 2:

As per the Australian taxation office an Australian resident company that has decided

to join the dividend imputation system in Australia may be required to pay the franked

dividend. Taking into the consideration the current situation of Sigma Pty Ltd for every

financial year the imputation credits relating to the corporate tax rates for the financial year of

2016 and for the financial year of 2017 stands 27.5 per cent.

Answer to question 3:

The below listed tables provides the total sum of tax that is payable by the Sigma Pty

Ltd is stated below;

The below listed provides the computation of total amount tax that is payable by

Yolande for the financial year ended on 2017 is stated below;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Answer to question 4:

Based on the tax rate the answer is “No”. The primary reason is that the answer would

not be held different given the purchase of shares were made by the Yolande during the 30th

May 2017. Another important factor involved in the static tax rate is because the tax rate

based on the imputation would remain to 27.5 and the same is applied in case of both the

Sigma Pty Ltd and for Yolande as well. The rate of corporate tax during the financial year

ended 2016-17 stands 27.5 for the Sigma Pty Ltd this is because the annual turnover limit of

the company stood less than the small company turnover threshold limit of $10 million.

Answer to question 5:

The rate of corporate tax for Sigma Pty Ltd and for Yolade would remain different.

The reason for this is that the aggregate sum of the total turnover threshold have gone past the

$10 million limit and this results in different amount of tax payment for both the Yolande and

the Sigma Pty Ltd during the year 2016-17. A tabular representation of the total amount of

tax that is payable for both is stated below;

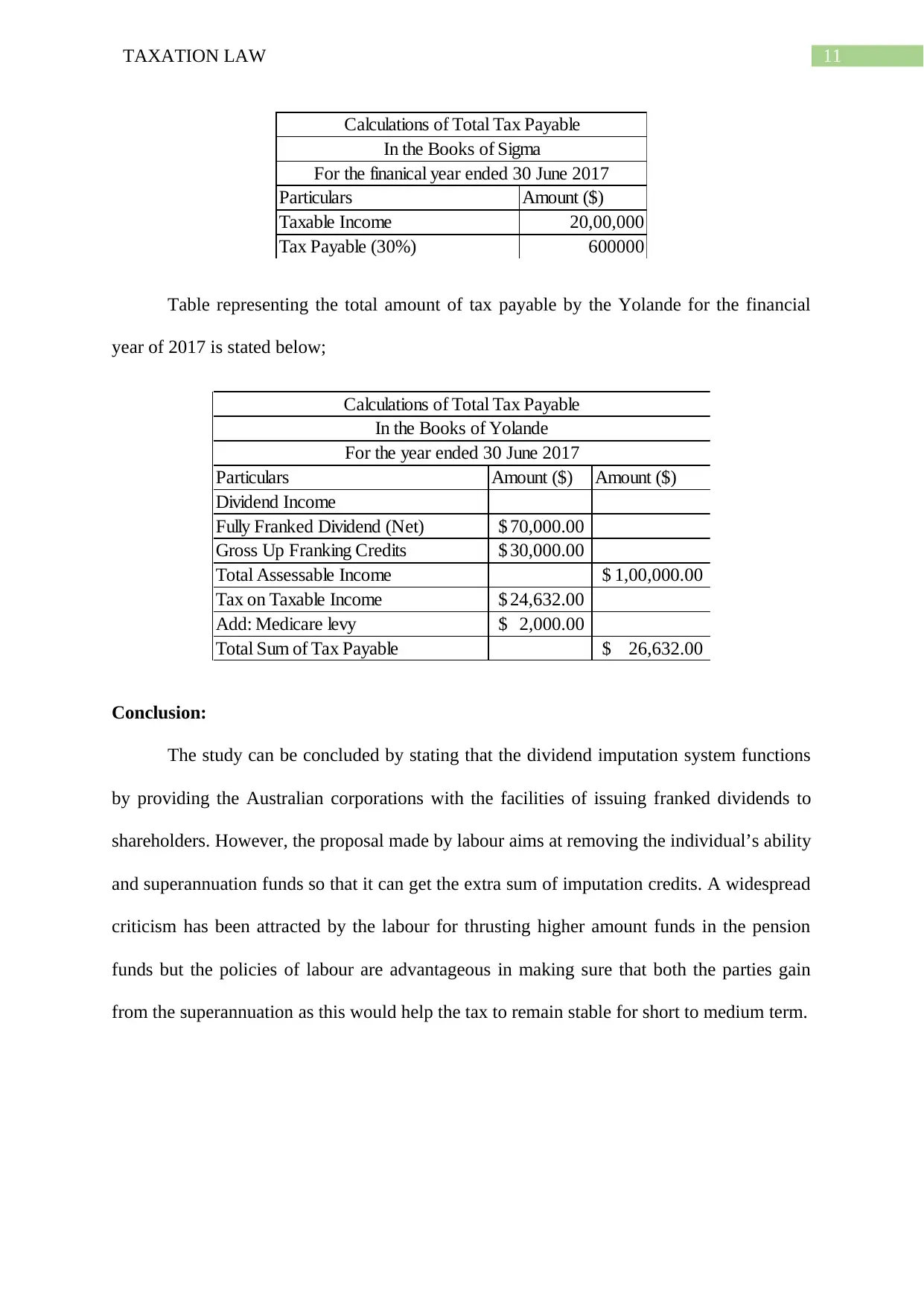

Table representing Computation of Tax Payable by the Sigma Pty Ltd is stated below;

Answer to question 4:

Based on the tax rate the answer is “No”. The primary reason is that the answer would

not be held different given the purchase of shares were made by the Yolande during the 30th

May 2017. Another important factor involved in the static tax rate is because the tax rate

based on the imputation would remain to 27.5 and the same is applied in case of both the

Sigma Pty Ltd and for Yolande as well. The rate of corporate tax during the financial year

ended 2016-17 stands 27.5 for the Sigma Pty Ltd this is because the annual turnover limit of

the company stood less than the small company turnover threshold limit of $10 million.

Answer to question 5:

The rate of corporate tax for Sigma Pty Ltd and for Yolade would remain different.

The reason for this is that the aggregate sum of the total turnover threshold have gone past the

$10 million limit and this results in different amount of tax payment for both the Yolande and

the Sigma Pty Ltd during the year 2016-17. A tabular representation of the total amount of

tax that is payable for both is stated below;

Table representing Computation of Tax Payable by the Sigma Pty Ltd is stated below;

11TAXATION LAW

Particulars Amount ($)

Taxable Income 20,00,000

Tax Payable (30%) 600000

Calculations of Total Tax Payable

In the Books of Sigma

For the finanical year ended 30 June 2017

Table representing the total amount of tax payable by the Yolande for the financial

year of 2017 is stated below;

Particulars Amount ($) Amount ($)

Dividend Income

Fully Franked Dividend (Net) 70,000.00$

Gross Up Franking Credits 30,000.00$

Total Assessable Income 1,00,000.00$

Tax on Taxable Income 24,632.00$

Add: Medicare levy 2,000.00$

Total Sum of Tax Payable 26,632.00$

For the year ended 30 June 2017

Calculations of Total Tax Payable

In the Books of Yolande

Conclusion:

The study can be concluded by stating that the dividend imputation system functions

by providing the Australian corporations with the facilities of issuing franked dividends to

shareholders. However, the proposal made by labour aims at removing the individual’s ability

and superannuation funds so that it can get the extra sum of imputation credits. A widespread

criticism has been attracted by the labour for thrusting higher amount funds in the pension

funds but the policies of labour are advantageous in making sure that both the parties gain

from the superannuation as this would help the tax to remain stable for short to medium term.

Particulars Amount ($)

Taxable Income 20,00,000

Tax Payable (30%) 600000

Calculations of Total Tax Payable

In the Books of Sigma

For the finanical year ended 30 June 2017

Table representing the total amount of tax payable by the Yolande for the financial

year of 2017 is stated below;

Particulars Amount ($) Amount ($)

Dividend Income

Fully Franked Dividend (Net) 70,000.00$

Gross Up Franking Credits 30,000.00$

Total Assessable Income 1,00,000.00$

Tax on Taxable Income 24,632.00$

Add: Medicare levy 2,000.00$

Total Sum of Tax Payable 26,632.00$

For the year ended 30 June 2017

Calculations of Total Tax Payable

In the Books of Yolande

Conclusion:

The study can be concluded by stating that the dividend imputation system functions

by providing the Australian corporations with the facilities of issuing franked dividends to

shareholders. However, the proposal made by labour aims at removing the individual’s ability

and superannuation funds so that it can get the extra sum of imputation credits. A widespread

criticism has been attracted by the labour for thrusting higher amount funds in the pension

funds but the policies of labour are advantageous in making sure that both the parties gain

from the superannuation as this would help the tax to remain stable for short to medium term.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.