Economics Assignment: Australia's Macroeconomic Performance Analysis

VerifiedAdded on 2021/06/17

|13

|3611

|62

Report

AI Summary

This economics assignment analyzes the macroeconomic performance of Australia from 1990 to 2016, evaluating key indicators like real GDP growth, inflation, unemployment, exchange rates, net exports, and cash rates. The report investigates the relationships between real GDP growth, inflation, and unemployment, as well as the connection between the cash rate and the Federal Reserve's fund rate. It also examines the relationship between net exports and the real exchange rate. The analysis includes statistical summaries, time series graphs, and discussions of business cycles to provide a comprehensive understanding of the Australian economy's trends and fluctuations over the specified period, offering insights into the country's economic outlook. The report concludes with a brief overview of the future prospects of the Australian economy based on its past performance.

Running Head: ECONOMICS ASSIGNMENT

Economics Assignment

Name of the Student

Name of the University

Course ID

Economics Assignment

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMICS ASSIGNMENT

Executive Summary

The paper sheds light on macroeconomic performance of Australia for a considerably long

period extending from 1990 to 2016. The performance has been evaluated in terms of real GDP

growth rate, inflation, unemployment rate, exchange rate, net export and cash rate. In the

process, the report tries to find whether there exists any relation between trend in real GDP

growth rate and that of inflation and unemployment. The decision regarding cash rate is often

influenced by the movement of interest rate in other nation. In this regard, focus is also given to

trace out any association between cash rate and federal’s fund rate. The movement of grade

balance is examined along with the movement of official exchange rate. Finally, based on the

past performance brief description is given on future outlook of the economy.

Executive Summary

The paper sheds light on macroeconomic performance of Australia for a considerably long

period extending from 1990 to 2016. The performance has been evaluated in terms of real GDP

growth rate, inflation, unemployment rate, exchange rate, net export and cash rate. In the

process, the report tries to find whether there exists any relation between trend in real GDP

growth rate and that of inflation and unemployment. The decision regarding cash rate is often

influenced by the movement of interest rate in other nation. In this regard, focus is also given to

trace out any association between cash rate and federal’s fund rate. The movement of grade

balance is examined along with the movement of official exchange rate. Finally, based on the

past performance brief description is given on future outlook of the economy.

2ECONOMICS ASSIGNMENT

Table of Contents

Introduction......................................................................................................................................3

Relation between real GDP growth and inflation and unemployment rate.....................................3

Real GDP growth and inflation...................................................................................................3

Real GDP growth and unemployment rate..................................................................................4

Relation between net export and real exchange rate between Australia and USA..........................6

Australia’s cash rate and Federal Reserve’s fund rate.....................................................................8

Macroeconomic Outlook for Australia............................................................................................9

Conclusion.......................................................................................................................................9

Reference list.................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

Relation between real GDP growth and inflation and unemployment rate.....................................3

Real GDP growth and inflation...................................................................................................3

Real GDP growth and unemployment rate..................................................................................4

Relation between net export and real exchange rate between Australia and USA..........................6

Australia’s cash rate and Federal Reserve’s fund rate.....................................................................8

Macroeconomic Outlook for Australia............................................................................................9

Conclusion.......................................................................................................................................9

Reference list.................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMICS ASSIGNMENT

Introduction

Australia is the 14th largest economy in the world. The nation in the past few decades

have accounted an outstanding growth and development. Service sector is the most dominating

sector of the economy making the highest contribution in GDP. Australia also has a strong

industrial and agricultural sector. The nation shares international relation with a number of

developed and developing nations. Trade account a significant portion of Australia’s GDP. In the

last few years however Australia has accounted a decline in is economic growth rate (RBA,

2018). The steady performance of Australian economy makes it an interesting area of research.

Relation between real GDP growth and inflation and unemployment rate

One of the most important macroeconomic indicators of a nation is its gross domestic

product. Gross domestic measure is a measure of aggregate output produced in a nation. As GDP

is a representative measure of aggregate valuation of produced goods and services market prices

are used to quantify the volume of output in terms of its market price. In GDP computation use

of current year market price gives nominal GDP while the use of a certain base year market price

provides GDP at constant price. In order to measure economic growth of a nation percentage

change in GDP is taken into consideration (Mankiw, 2014). Use of real GDP growth rate

considers as a more useful measure of economic growth as is free from the effect of inflation.

The growth rare in real GDP thus expected to have a relation with rate of inflation. As a rising

real GDP growth is an indicator of economic expansion it influences unemployment rate through

creation or contraction of job opportunities.

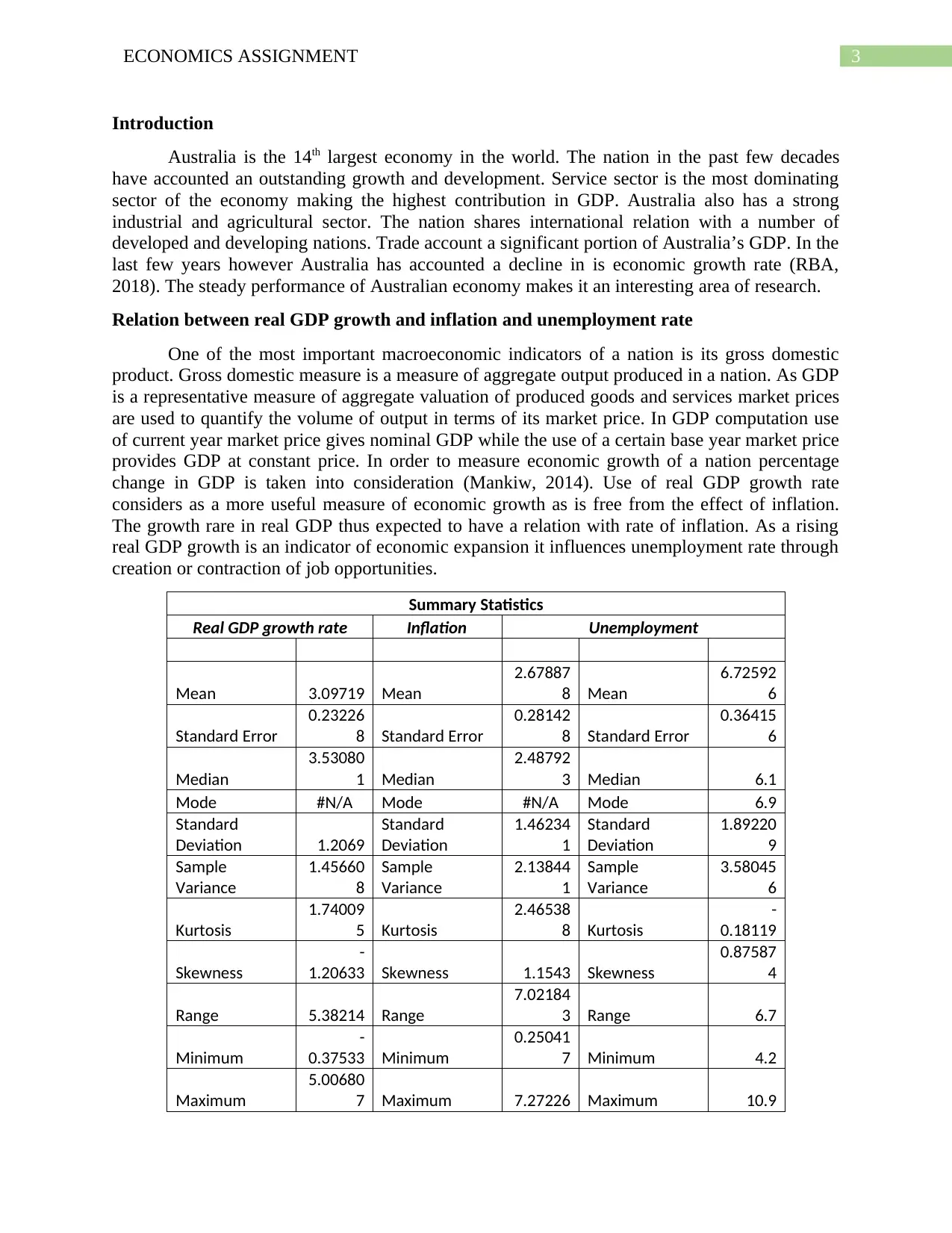

Summary Statistics

Real GDP growth rate Inflation Unemployment

Mean 3.09719 Mean

2.67887

8 Mean

6.72592

6

Standard Error

0.23226

8 Standard Error

0.28142

8 Standard Error

0.36415

6

Median

3.53080

1 Median

2.48792

3 Median 6.1

Mode #N/A Mode #N/A Mode 6.9

Standard

Deviation 1.2069

Standard

Deviation

1.46234

1

Standard

Deviation

1.89220

9

Sample

Variance

1.45660

8

Sample

Variance

2.13844

1

Sample

Variance

3.58045

6

Kurtosis

1.74009

5 Kurtosis

2.46538

8 Kurtosis

-

0.18119

Skewness

-

1.20633 Skewness 1.1543 Skewness

0.87587

4

Range 5.38214 Range

7.02184

3 Range 6.7

Minimum

-

0.37533 Minimum

0.25041

7 Minimum 4.2

Maximum

5.00680

7 Maximum 7.27226 Maximum 10.9

Introduction

Australia is the 14th largest economy in the world. The nation in the past few decades

have accounted an outstanding growth and development. Service sector is the most dominating

sector of the economy making the highest contribution in GDP. Australia also has a strong

industrial and agricultural sector. The nation shares international relation with a number of

developed and developing nations. Trade account a significant portion of Australia’s GDP. In the

last few years however Australia has accounted a decline in is economic growth rate (RBA,

2018). The steady performance of Australian economy makes it an interesting area of research.

Relation between real GDP growth and inflation and unemployment rate

One of the most important macroeconomic indicators of a nation is its gross domestic

product. Gross domestic measure is a measure of aggregate output produced in a nation. As GDP

is a representative measure of aggregate valuation of produced goods and services market prices

are used to quantify the volume of output in terms of its market price. In GDP computation use

of current year market price gives nominal GDP while the use of a certain base year market price

provides GDP at constant price. In order to measure economic growth of a nation percentage

change in GDP is taken into consideration (Mankiw, 2014). Use of real GDP growth rate

considers as a more useful measure of economic growth as is free from the effect of inflation.

The growth rare in real GDP thus expected to have a relation with rate of inflation. As a rising

real GDP growth is an indicator of economic expansion it influences unemployment rate through

creation or contraction of job opportunities.

Summary Statistics

Real GDP growth rate Inflation Unemployment

Mean 3.09719 Mean

2.67887

8 Mean

6.72592

6

Standard Error

0.23226

8 Standard Error

0.28142

8 Standard Error

0.36415

6

Median

3.53080

1 Median

2.48792

3 Median 6.1

Mode #N/A Mode #N/A Mode 6.9

Standard

Deviation 1.2069

Standard

Deviation

1.46234

1

Standard

Deviation

1.89220

9

Sample

Variance

1.45660

8

Sample

Variance

2.13844

1

Sample

Variance

3.58045

6

Kurtosis

1.74009

5 Kurtosis

2.46538

8 Kurtosis

-

0.18119

Skewness

-

1.20633 Skewness 1.1543 Skewness

0.87587

4

Range 5.38214 Range

7.02184

3 Range 6.7

Minimum

-

0.37533 Minimum

0.25041

7 Minimum 4.2

Maximum

5.00680

7 Maximum 7.27226 Maximum 10.9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMICS ASSIGNMENT

Sum

83.6241

4 Sum 72.3297 Sum 181.6

Count 27 Count 27 Count 27

Real GDP growth and inflation

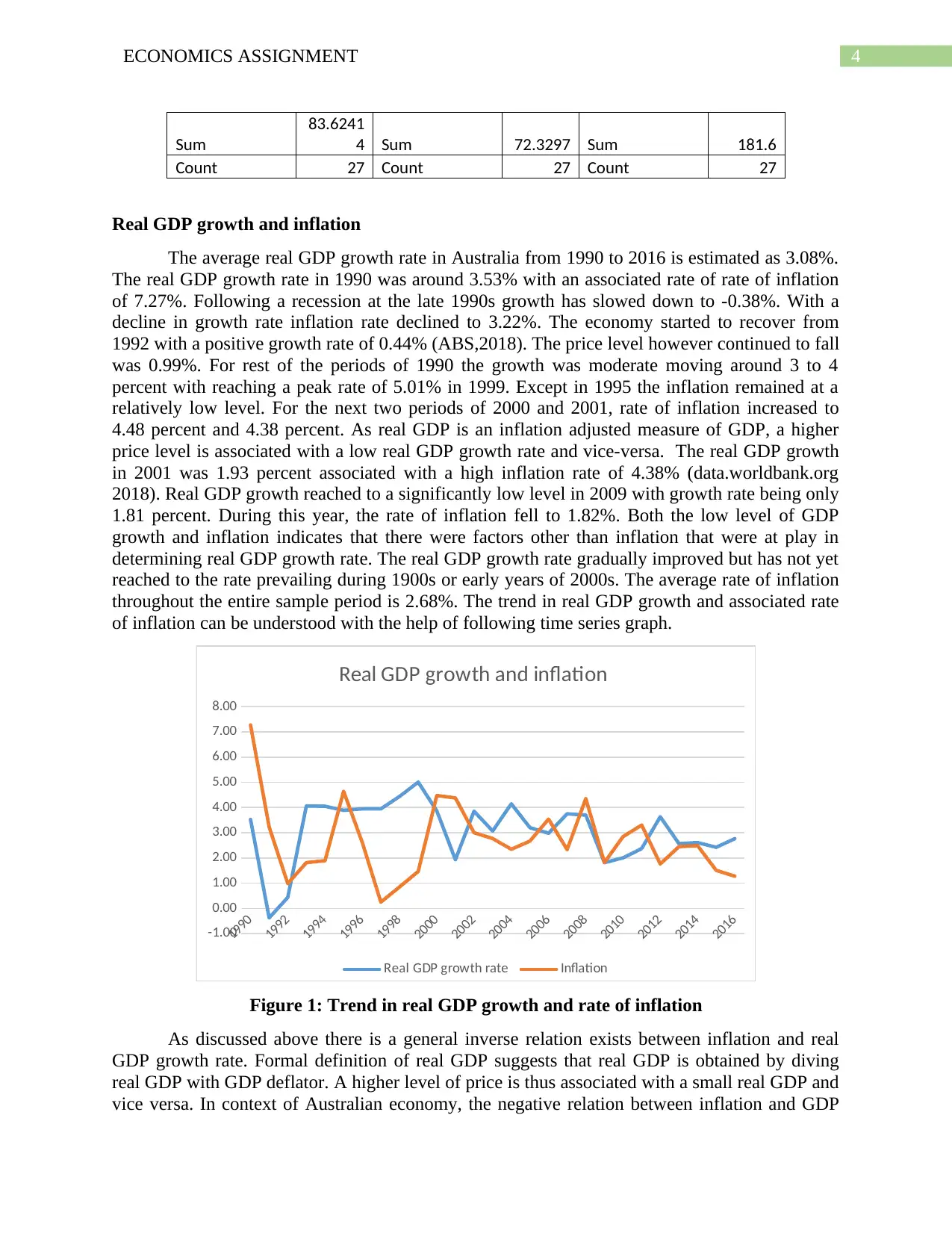

The average real GDP growth rate in Australia from 1990 to 2016 is estimated as 3.08%.

The real GDP growth rate in 1990 was around 3.53% with an associated rate of rate of inflation

of 7.27%. Following a recession at the late 1990s growth has slowed down to -0.38%. With a

decline in growth rate inflation rate declined to 3.22%. The economy started to recover from

1992 with a positive growth rate of 0.44% (ABS,2018). The price level however continued to fall

was 0.99%. For rest of the periods of 1990 the growth was moderate moving around 3 to 4

percent with reaching a peak rate of 5.01% in 1999. Except in 1995 the inflation remained at a

relatively low level. For the next two periods of 2000 and 2001, rate of inflation increased to

4.48 percent and 4.38 percent. As real GDP is an inflation adjusted measure of GDP, a higher

price level is associated with a low real GDP growth rate and vice-versa. The real GDP growth

in 2001 was 1.93 percent associated with a high inflation rate of 4.38% (data.worldbank.org

2018). Real GDP growth reached to a significantly low level in 2009 with growth rate being only

1.81 percent. During this year, the rate of inflation fell to 1.82%. Both the low level of GDP

growth and inflation indicates that there were factors other than inflation that were at play in

determining real GDP growth rate. The real GDP growth rate gradually improved but has not yet

reached to the rate prevailing during 1900s or early years of 2000s. The average rate of inflation

throughout the entire sample period is 2.68%. The trend in real GDP growth and associated rate

of inflation can be understood with the help of following time series graph.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Real GDP growth and inflation

Real GDP growth rate Inflation

Figure 1: Trend in real GDP growth and rate of inflation

As discussed above there is a general inverse relation exists between inflation and real

GDP growth rate. Formal definition of real GDP suggests that real GDP is obtained by diving

real GDP with GDP deflator. A higher level of price is thus associated with a small real GDP and

vice versa. In context of Australian economy, the negative relation between inflation and GDP

Sum

83.6241

4 Sum 72.3297 Sum 181.6

Count 27 Count 27 Count 27

Real GDP growth and inflation

The average real GDP growth rate in Australia from 1990 to 2016 is estimated as 3.08%.

The real GDP growth rate in 1990 was around 3.53% with an associated rate of rate of inflation

of 7.27%. Following a recession at the late 1990s growth has slowed down to -0.38%. With a

decline in growth rate inflation rate declined to 3.22%. The economy started to recover from

1992 with a positive growth rate of 0.44% (ABS,2018). The price level however continued to fall

was 0.99%. For rest of the periods of 1990 the growth was moderate moving around 3 to 4

percent with reaching a peak rate of 5.01% in 1999. Except in 1995 the inflation remained at a

relatively low level. For the next two periods of 2000 and 2001, rate of inflation increased to

4.48 percent and 4.38 percent. As real GDP is an inflation adjusted measure of GDP, a higher

price level is associated with a low real GDP growth rate and vice-versa. The real GDP growth

in 2001 was 1.93 percent associated with a high inflation rate of 4.38% (data.worldbank.org

2018). Real GDP growth reached to a significantly low level in 2009 with growth rate being only

1.81 percent. During this year, the rate of inflation fell to 1.82%. Both the low level of GDP

growth and inflation indicates that there were factors other than inflation that were at play in

determining real GDP growth rate. The real GDP growth rate gradually improved but has not yet

reached to the rate prevailing during 1900s or early years of 2000s. The average rate of inflation

throughout the entire sample period is 2.68%. The trend in real GDP growth and associated rate

of inflation can be understood with the help of following time series graph.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Real GDP growth and inflation

Real GDP growth rate Inflation

Figure 1: Trend in real GDP growth and rate of inflation

As discussed above there is a general inverse relation exists between inflation and real

GDP growth rate. Formal definition of real GDP suggests that real GDP is obtained by diving

real GDP with GDP deflator. A higher level of price is thus associated with a small real GDP and

vice versa. In context of Australian economy, the negative relation between inflation and GDP

5ECONOMICS ASSIGNMENT

growth is found to be valid for most of the years (Svensson, 2015). However, there are some

exception years where both real GDP and inflation declined simultaneously. These are the period

of entire economic slowdown. Such periods include late 1990s to 1991 and in 2009.

Real GDP growth and unemployment rate

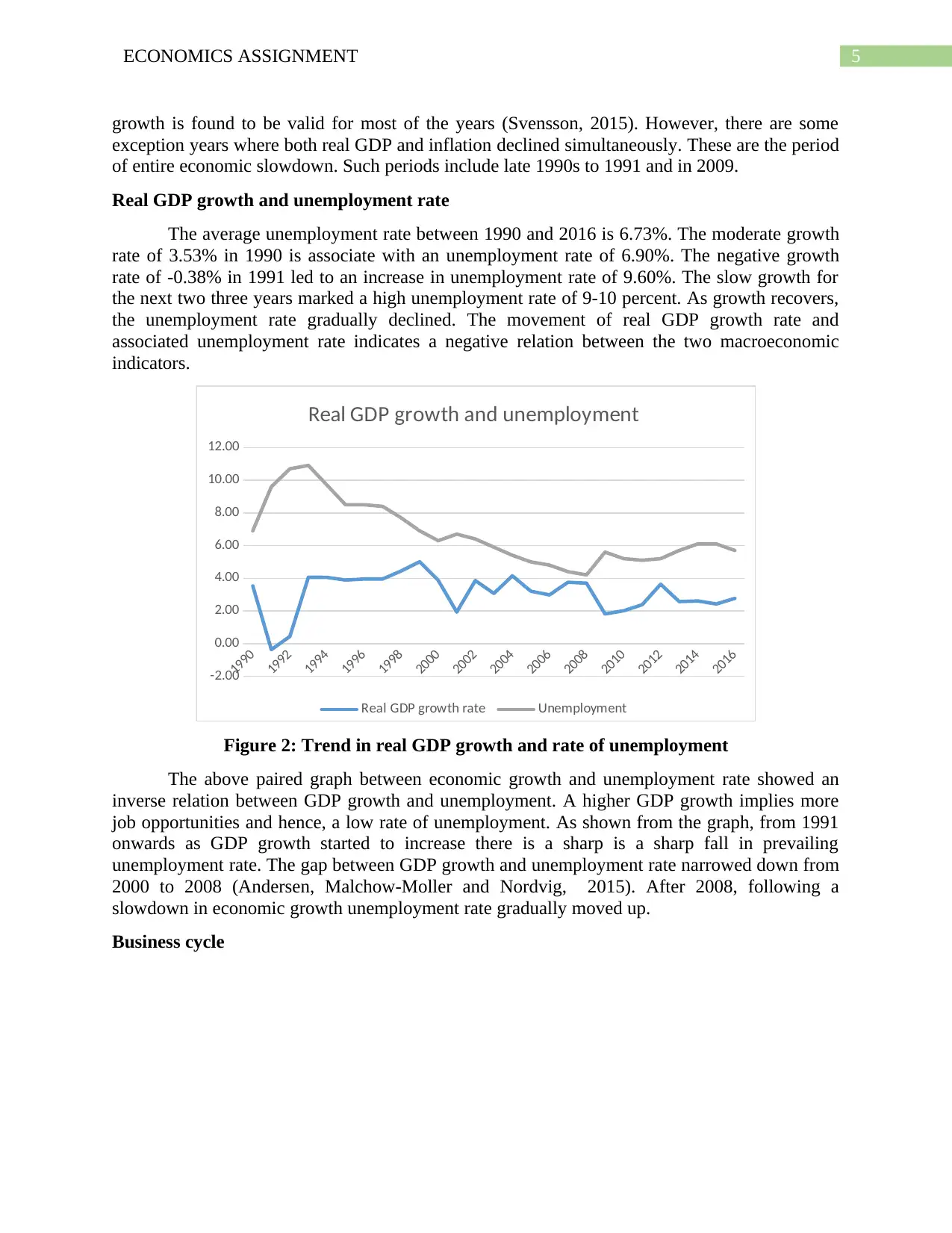

The average unemployment rate between 1990 and 2016 is 6.73%. The moderate growth

rate of 3.53% in 1990 is associate with an unemployment rate of 6.90%. The negative growth

rate of -0.38% in 1991 led to an increase in unemployment rate of 9.60%. The slow growth for

the next two three years marked a high unemployment rate of 9-10 percent. As growth recovers,

the unemployment rate gradually declined. The movement of real GDP growth rate and

associated unemployment rate indicates a negative relation between the two macroeconomic

indicators.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Real GDP growth and unemployment

Real GDP growth rate Unemployment

Figure 2: Trend in real GDP growth and rate of unemployment

The above paired graph between economic growth and unemployment rate showed an

inverse relation between GDP growth and unemployment. A higher GDP growth implies more

job opportunities and hence, a low rate of unemployment. As shown from the graph, from 1991

onwards as GDP growth started to increase there is a sharp is a sharp fall in prevailing

unemployment rate. The gap between GDP growth and unemployment rate narrowed down from

2000 to 2008 (Andersen, Malchow-Moller and Nordvig, 2015). After 2008, following a

slowdown in economic growth unemployment rate gradually moved up.

Business cycle

growth is found to be valid for most of the years (Svensson, 2015). However, there are some

exception years where both real GDP and inflation declined simultaneously. These are the period

of entire economic slowdown. Such periods include late 1990s to 1991 and in 2009.

Real GDP growth and unemployment rate

The average unemployment rate between 1990 and 2016 is 6.73%. The moderate growth

rate of 3.53% in 1990 is associate with an unemployment rate of 6.90%. The negative growth

rate of -0.38% in 1991 led to an increase in unemployment rate of 9.60%. The slow growth for

the next two three years marked a high unemployment rate of 9-10 percent. As growth recovers,

the unemployment rate gradually declined. The movement of real GDP growth rate and

associated unemployment rate indicates a negative relation between the two macroeconomic

indicators.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-2.00

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Real GDP growth and unemployment

Real GDP growth rate Unemployment

Figure 2: Trend in real GDP growth and rate of unemployment

The above paired graph between economic growth and unemployment rate showed an

inverse relation between GDP growth and unemployment. A higher GDP growth implies more

job opportunities and hence, a low rate of unemployment. As shown from the graph, from 1991

onwards as GDP growth started to increase there is a sharp is a sharp fall in prevailing

unemployment rate. The gap between GDP growth and unemployment rate narrowed down from

2000 to 2008 (Andersen, Malchow-Moller and Nordvig, 2015). After 2008, following a

slowdown in economic growth unemployment rate gradually moved up.

Business cycle

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMICS ASSIGNMENT

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Real GDP growth rate

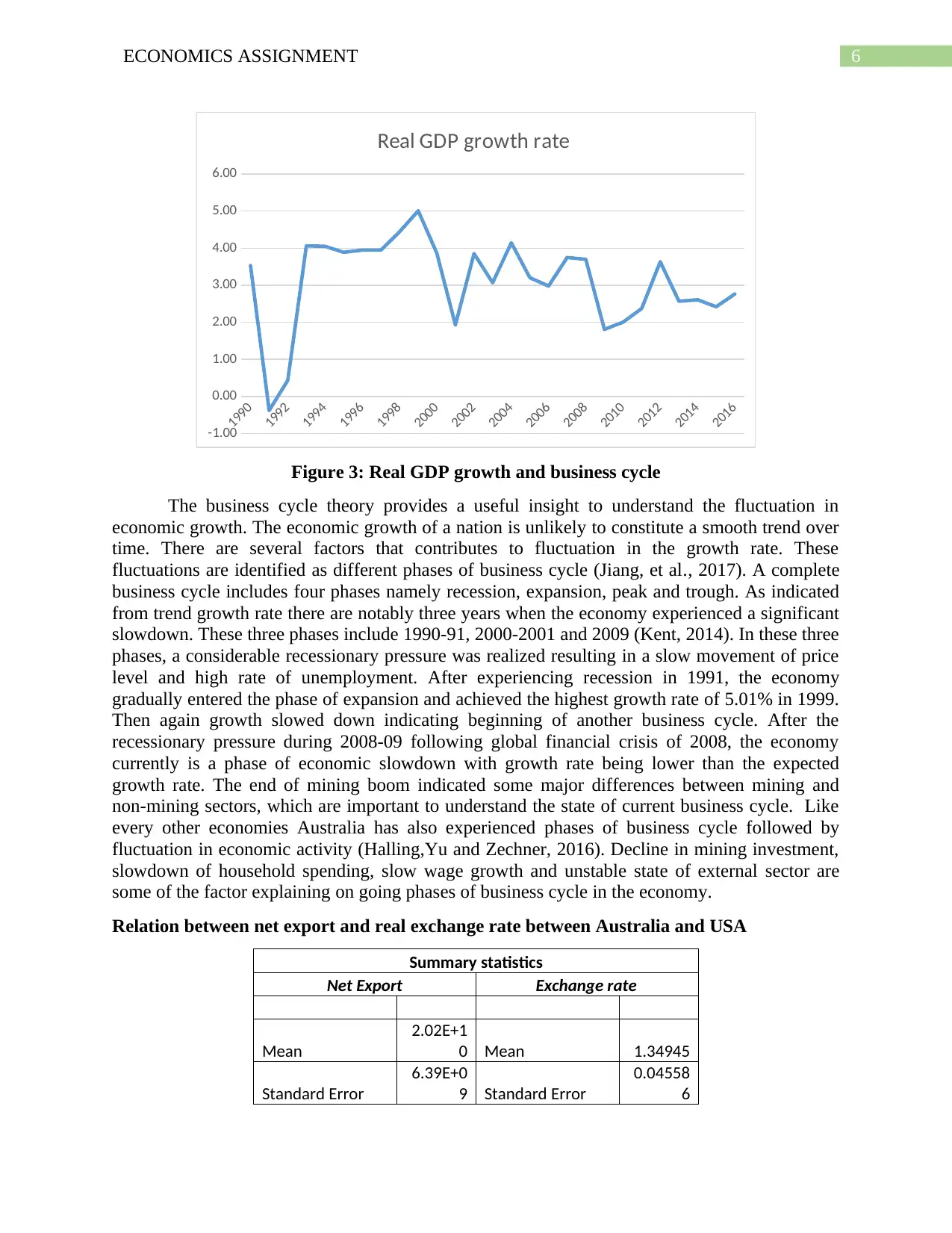

Figure 3: Real GDP growth and business cycle

The business cycle theory provides a useful insight to understand the fluctuation in

economic growth. The economic growth of a nation is unlikely to constitute a smooth trend over

time. There are several factors that contributes to fluctuation in the growth rate. These

fluctuations are identified as different phases of business cycle (Jiang, et al., 2017). A complete

business cycle includes four phases namely recession, expansion, peak and trough. As indicated

from trend growth rate there are notably three years when the economy experienced a significant

slowdown. These three phases include 1990-91, 2000-2001 and 2009 (Kent, 2014). In these three

phases, a considerable recessionary pressure was realized resulting in a slow movement of price

level and high rate of unemployment. After experiencing recession in 1991, the economy

gradually entered the phase of expansion and achieved the highest growth rate of 5.01% in 1999.

Then again growth slowed down indicating beginning of another business cycle. After the

recessionary pressure during 2008-09 following global financial crisis of 2008, the economy

currently is a phase of economic slowdown with growth rate being lower than the expected

growth rate. The end of mining boom indicated some major differences between mining and

non-mining sectors, which are important to understand the state of current business cycle. Like

every other economies Australia has also experienced phases of business cycle followed by

fluctuation in economic activity (Halling,Yu and Zechner, 2016). Decline in mining investment,

slowdown of household spending, slow wage growth and unstable state of external sector are

some of the factor explaining on going phases of business cycle in the economy.

Relation between net export and real exchange rate between Australia and USA

Summary statistics

Net Export Exchange rate

Mean

2.02E+1

0 Mean 1.34945

Standard Error

6.39E+0

9 Standard Error

0.04558

6

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Real GDP growth rate

Figure 3: Real GDP growth and business cycle

The business cycle theory provides a useful insight to understand the fluctuation in

economic growth. The economic growth of a nation is unlikely to constitute a smooth trend over

time. There are several factors that contributes to fluctuation in the growth rate. These

fluctuations are identified as different phases of business cycle (Jiang, et al., 2017). A complete

business cycle includes four phases namely recession, expansion, peak and trough. As indicated

from trend growth rate there are notably three years when the economy experienced a significant

slowdown. These three phases include 1990-91, 2000-2001 and 2009 (Kent, 2014). In these three

phases, a considerable recessionary pressure was realized resulting in a slow movement of price

level and high rate of unemployment. After experiencing recession in 1991, the economy

gradually entered the phase of expansion and achieved the highest growth rate of 5.01% in 1999.

Then again growth slowed down indicating beginning of another business cycle. After the

recessionary pressure during 2008-09 following global financial crisis of 2008, the economy

currently is a phase of economic slowdown with growth rate being lower than the expected

growth rate. The end of mining boom indicated some major differences between mining and

non-mining sectors, which are important to understand the state of current business cycle. Like

every other economies Australia has also experienced phases of business cycle followed by

fluctuation in economic activity (Halling,Yu and Zechner, 2016). Decline in mining investment,

slowdown of household spending, slow wage growth and unstable state of external sector are

some of the factor explaining on going phases of business cycle in the economy.

Relation between net export and real exchange rate between Australia and USA

Summary statistics

Net Export Exchange rate

Mean

2.02E+1

0 Mean 1.34945

Standard Error

6.39E+0

9 Standard Error

0.04558

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMICS ASSIGNMENT

Median

3.05E+1

0 Median 1.33109

Mode #N/A Mode #N/A

Standard

Deviation

3.32E+1

0

Standard

Deviation

0.23687

2

Sample Variance 1.1E+21 Sample Variance

0.05610

8

Kurtosis -0.71044 Kurtosis

0.65764

6

Skewness -0.5941 Skewness

0.68558

1

Range

1.18E+1

1 Range

0.96764

1

Minimum -5.1E+10 Minimum

0.96580

1

Maximum

6.67E+1

0 Maximum

1.93344

3

Sum

5.44E+1

1 Sum

36.4351

4

Count 27 Count 27

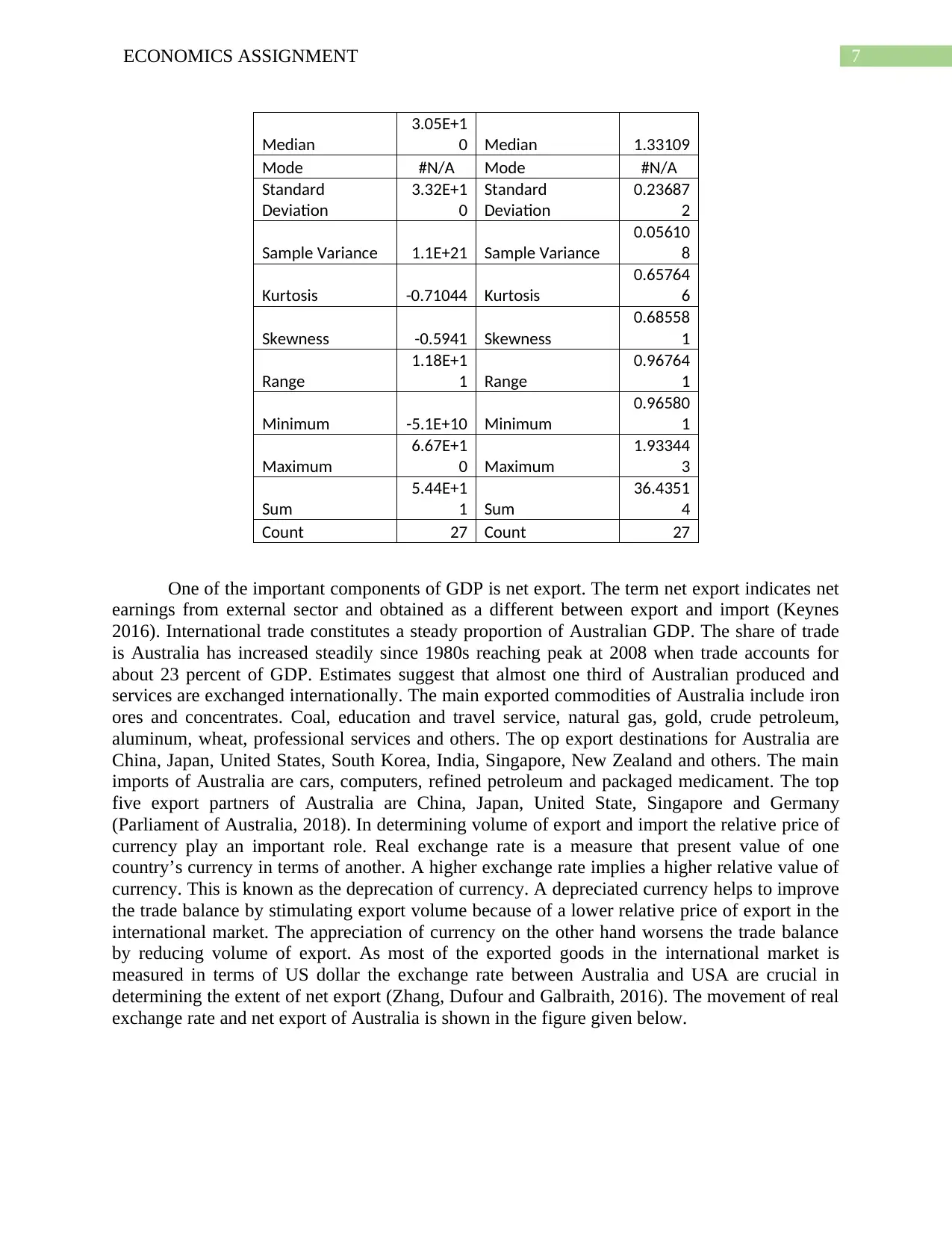

One of the important components of GDP is net export. The term net export indicates net

earnings from external sector and obtained as a different between export and import (Keynes

2016). International trade constitutes a steady proportion of Australian GDP. The share of trade

is Australia has increased steadily since 1980s reaching peak at 2008 when trade accounts for

about 23 percent of GDP. Estimates suggest that almost one third of Australian produced and

services are exchanged internationally. The main exported commodities of Australia include iron

ores and concentrates. Coal, education and travel service, natural gas, gold, crude petroleum,

aluminum, wheat, professional services and others. The op export destinations for Australia are

China, Japan, United States, South Korea, India, Singapore, New Zealand and others. The main

imports of Australia are cars, computers, refined petroleum and packaged medicament. The top

five export partners of Australia are China, Japan, United State, Singapore and Germany

(Parliament of Australia, 2018). In determining volume of export and import the relative price of

currency play an important role. Real exchange rate is a measure that present value of one

country’s currency in terms of another. A higher exchange rate implies a higher relative value of

currency. This is known as the deprecation of currency. A depreciated currency helps to improve

the trade balance by stimulating export volume because of a lower relative price of export in the

international market. The appreciation of currency on the other hand worsens the trade balance

by reducing volume of export. As most of the exported goods in the international market is

measured in terms of US dollar the exchange rate between Australia and USA are crucial in

determining the extent of net export (Zhang, Dufour and Galbraith, 2016). The movement of real

exchange rate and net export of Australia is shown in the figure given below.

Median

3.05E+1

0 Median 1.33109

Mode #N/A Mode #N/A

Standard

Deviation

3.32E+1

0

Standard

Deviation

0.23687

2

Sample Variance 1.1E+21 Sample Variance

0.05610

8

Kurtosis -0.71044 Kurtosis

0.65764

6

Skewness -0.5941 Skewness

0.68558

1

Range

1.18E+1

1 Range

0.96764

1

Minimum -5.1E+10 Minimum

0.96580

1

Maximum

6.67E+1

0 Maximum

1.93344

3

Sum

5.44E+1

1 Sum

36.4351

4

Count 27 Count 27

One of the important components of GDP is net export. The term net export indicates net

earnings from external sector and obtained as a different between export and import (Keynes

2016). International trade constitutes a steady proportion of Australian GDP. The share of trade

is Australia has increased steadily since 1980s reaching peak at 2008 when trade accounts for

about 23 percent of GDP. Estimates suggest that almost one third of Australian produced and

services are exchanged internationally. The main exported commodities of Australia include iron

ores and concentrates. Coal, education and travel service, natural gas, gold, crude petroleum,

aluminum, wheat, professional services and others. The op export destinations for Australia are

China, Japan, United States, South Korea, India, Singapore, New Zealand and others. The main

imports of Australia are cars, computers, refined petroleum and packaged medicament. The top

five export partners of Australia are China, Japan, United State, Singapore and Germany

(Parliament of Australia, 2018). In determining volume of export and import the relative price of

currency play an important role. Real exchange rate is a measure that present value of one

country’s currency in terms of another. A higher exchange rate implies a higher relative value of

currency. This is known as the deprecation of currency. A depreciated currency helps to improve

the trade balance by stimulating export volume because of a lower relative price of export in the

international market. The appreciation of currency on the other hand worsens the trade balance

by reducing volume of export. As most of the exported goods in the international market is

measured in terms of US dollar the exchange rate between Australia and USA are crucial in

determining the extent of net export (Zhang, Dufour and Galbraith, 2016). The movement of real

exchange rate and net export of Australia is shown in the figure given below.

8ECONOMICS ASSIGNMENT

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-60000000000

-40000000000

-20000000000

0

20000000000

40000000000

60000000000

80000000000

0.00

0.50

1.00

1.50

2.00

2.50

Net export and Real exchange rate

Net Export Exchange rate

Figure 4: Movement of net export and real exchange rate

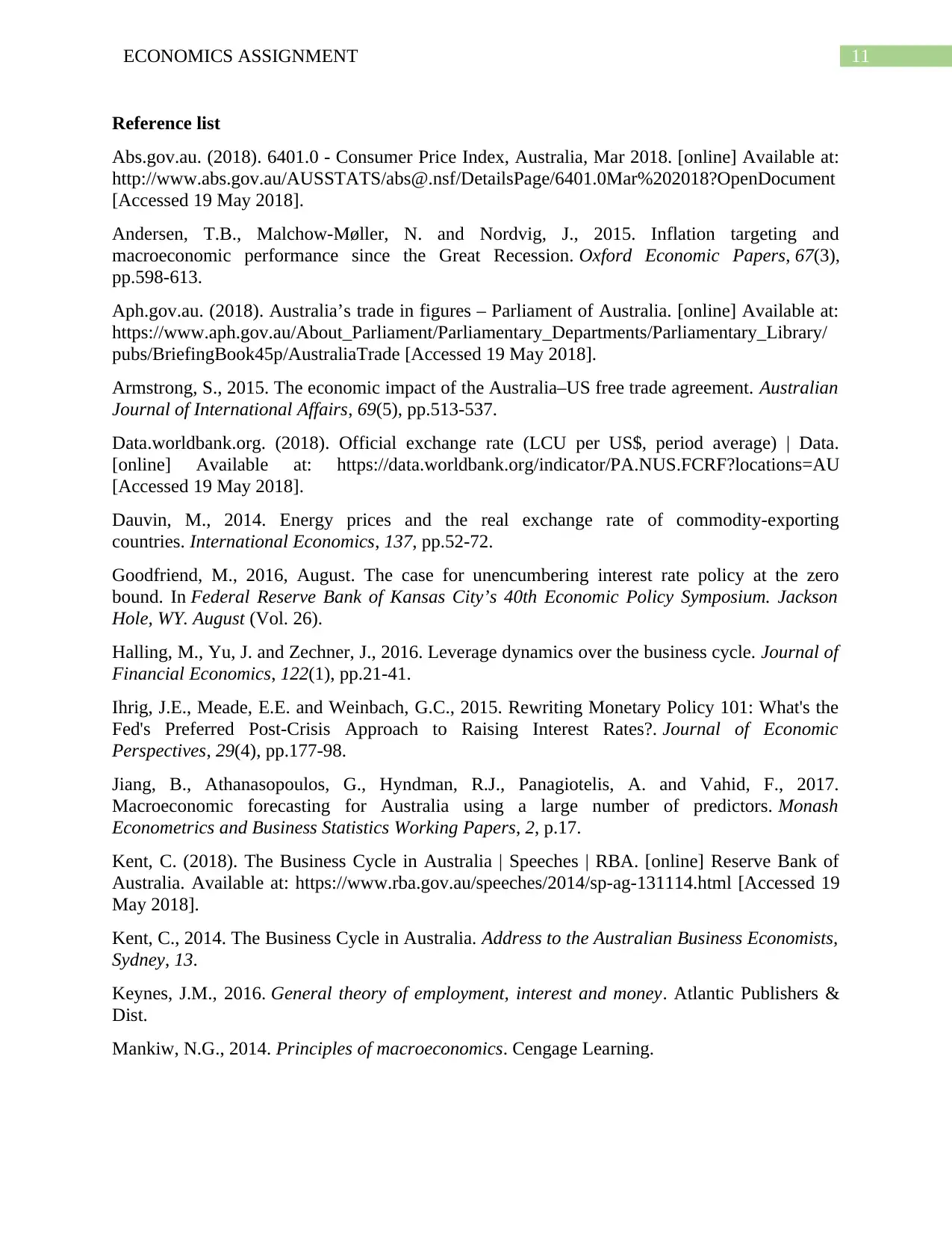

The AUD/US exchange rate during 1990s was 1.28. This implies Australia need to pay

AUD 1.28 to purchase one unit of US dollar. In 1992, the exchange rate rose to 1.36 AUD per

unit of US dollar. This marked a depreciation of Australian dollar. Following a currency

depreciation, the nation experienced a gain in export which resulted in an increases in net export

(Dauvin, 2014). Until 2008, Australia maintained a positive trade balance. In the phase of global

financial crisis, the relative value of US dollar has declined significantly. This caused Australia

dollar to appreciate. The trend decline in exchange rate continued till 2012 with Australia

accounting a sizable trade deficit. The US dollar gradually recovered after overcoming the shock

of financial crisis. In 2016, the recorded exchange rate is 1.35. With this, the external account of

Australia has experienced a trade surplus after a long period of trade deficit.

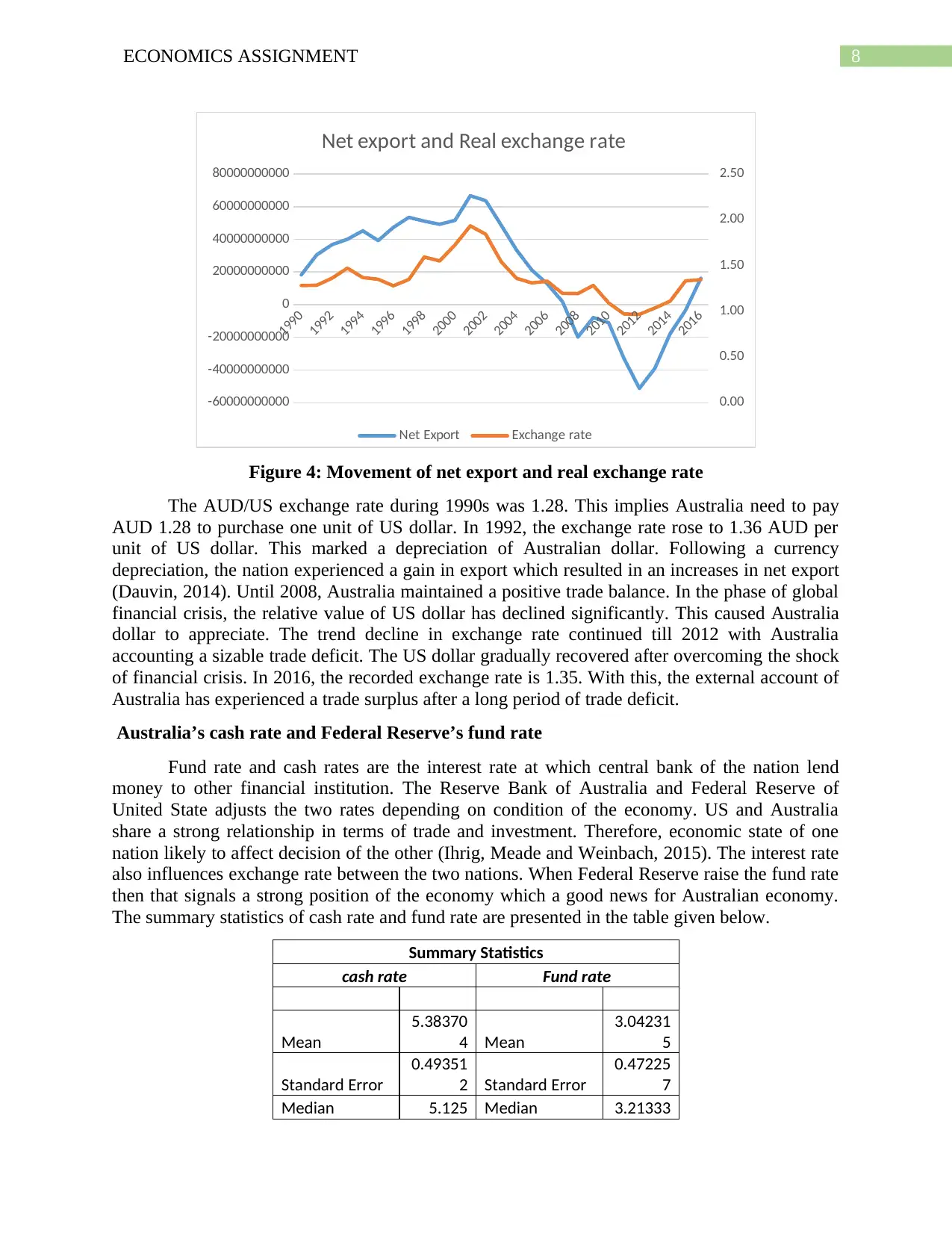

Australia’s cash rate and Federal Reserve’s fund rate

Fund rate and cash rates are the interest rate at which central bank of the nation lend

money to other financial institution. The Reserve Bank of Australia and Federal Reserve of

United State adjusts the two rates depending on condition of the economy. US and Australia

share a strong relationship in terms of trade and investment. Therefore, economic state of one

nation likely to affect decision of the other (Ihrig, Meade and Weinbach, 2015). The interest rate

also influences exchange rate between the two nations. When Federal Reserve raise the fund rate

then that signals a strong position of the economy which a good news for Australian economy.

The summary statistics of cash rate and fund rate are presented in the table given below.

Summary Statistics

cash rate Fund rate

Mean

5.38370

4 Mean

3.04231

5

Standard Error

0.49351

2 Standard Error

0.47225

7

Median 5.125 Median 3.21333

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

-60000000000

-40000000000

-20000000000

0

20000000000

40000000000

60000000000

80000000000

0.00

0.50

1.00

1.50

2.00

2.50

Net export and Real exchange rate

Net Export Exchange rate

Figure 4: Movement of net export and real exchange rate

The AUD/US exchange rate during 1990s was 1.28. This implies Australia need to pay

AUD 1.28 to purchase one unit of US dollar. In 1992, the exchange rate rose to 1.36 AUD per

unit of US dollar. This marked a depreciation of Australian dollar. Following a currency

depreciation, the nation experienced a gain in export which resulted in an increases in net export

(Dauvin, 2014). Until 2008, Australia maintained a positive trade balance. In the phase of global

financial crisis, the relative value of US dollar has declined significantly. This caused Australia

dollar to appreciate. The trend decline in exchange rate continued till 2012 with Australia

accounting a sizable trade deficit. The US dollar gradually recovered after overcoming the shock

of financial crisis. In 2016, the recorded exchange rate is 1.35. With this, the external account of

Australia has experienced a trade surplus after a long period of trade deficit.

Australia’s cash rate and Federal Reserve’s fund rate

Fund rate and cash rates are the interest rate at which central bank of the nation lend

money to other financial institution. The Reserve Bank of Australia and Federal Reserve of

United State adjusts the two rates depending on condition of the economy. US and Australia

share a strong relationship in terms of trade and investment. Therefore, economic state of one

nation likely to affect decision of the other (Ihrig, Meade and Weinbach, 2015). The interest rate

also influences exchange rate between the two nations. When Federal Reserve raise the fund rate

then that signals a strong position of the economy which a good news for Australian economy.

The summary statistics of cash rate and fund rate are presented in the table given below.

Summary Statistics

cash rate Fund rate

Mean

5.38370

4 Mean

3.04231

5

Standard Error

0.49351

2 Standard Error

0.47225

7

Median 5.125 Median 3.21333

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMICS ASSIGNMENT

3

Mode 6.5 Mode #N/A

Standard

Deviation

2.56436

3

Standard

Deviation

2.45391

9

Sample

Variance

6.57595

7

Sample

Variance 6.02172

Kurtosis

6.62617

8 Kurtosis

-

1.26609

Skewness

1.96211

3 Skewness

0.16008

6

Range

13.3333

3 Range 8.01

Minimum 1.5 Minimum

0.08916

7

Maximum

14.8333

3 Maximum

8.09916

7

Sum 145.36 Sum 82.1425

Count 27 Count 27

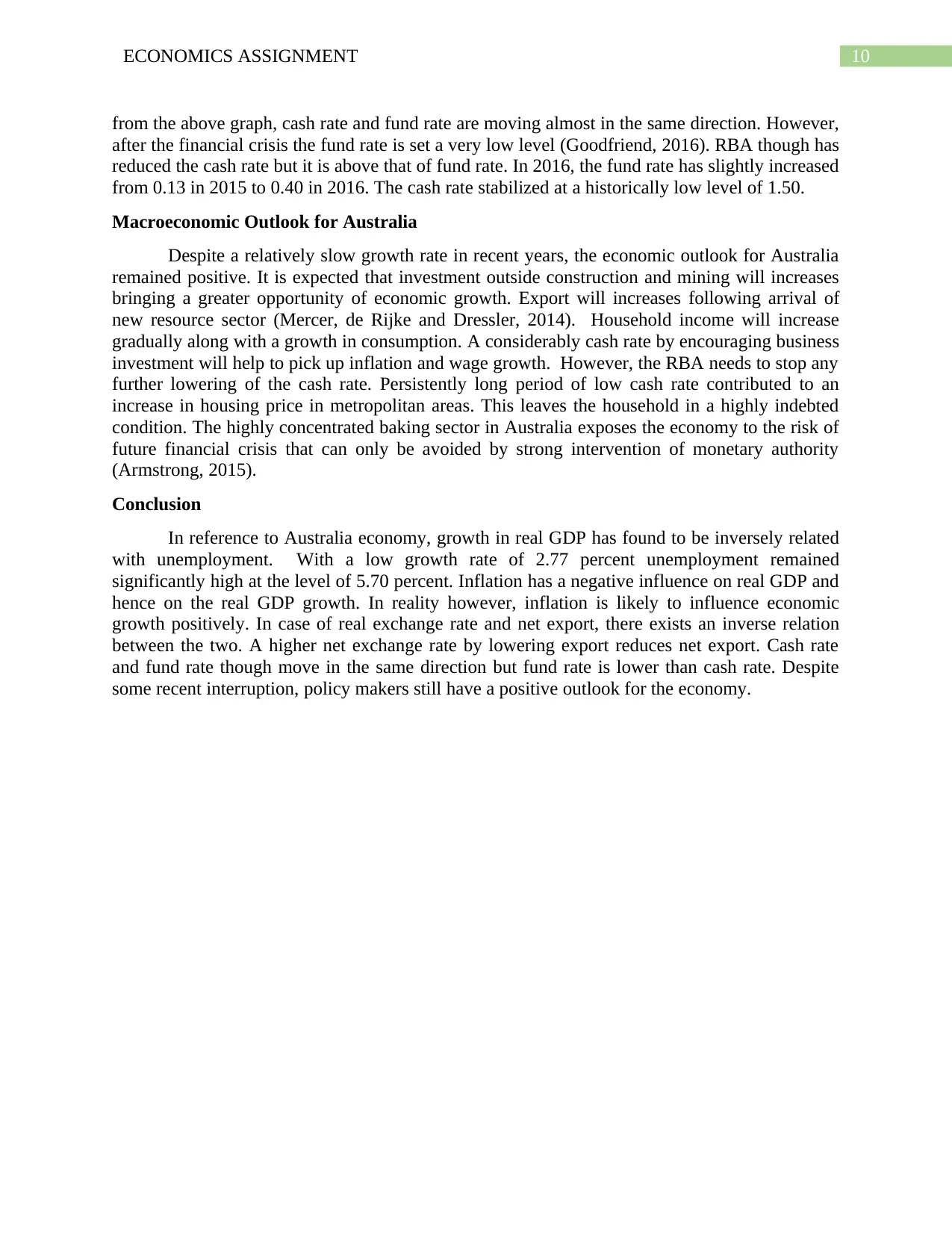

The average fed fund rate is obtained as 3.04 as against the average cash rate of 5.83. The

relatively higher cash rate helps to strengthen Aussie dollar against that of US dollar. The

relatively low average fund rate in US is contributed from continuation of a very low fund rate

especially after the global financial crisis.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Cash rate and Fed fund rate

cash rate Fund rate

Figure 5: Movement of cash rate and Federal fund rate

In 1990, Federal fund rate was 8.10. During this year, corresponding cash rate was 14.83. The

Federal government reduced its fund rate to 5.69. The Reserve Bank of Australia in response to

recessionary shock in 1990 lowered the interest rate to 10 (rba.gov.au 2018). Cash rate reduced

to 5 basis point in 1993. Fed also continued to reduce the cash rate to 3.02 in 1993. As shown

3

Mode 6.5 Mode #N/A

Standard

Deviation

2.56436

3

Standard

Deviation

2.45391

9

Sample

Variance

6.57595

7

Sample

Variance 6.02172

Kurtosis

6.62617

8 Kurtosis

-

1.26609

Skewness

1.96211

3 Skewness

0.16008

6

Range

13.3333

3 Range 8.01

Minimum 1.5 Minimum

0.08916

7

Maximum

14.8333

3 Maximum

8.09916

7

Sum 145.36 Sum 82.1425

Count 27 Count 27

The average fed fund rate is obtained as 3.04 as against the average cash rate of 5.83. The

relatively higher cash rate helps to strengthen Aussie dollar against that of US dollar. The

relatively low average fund rate in US is contributed from continuation of a very low fund rate

especially after the global financial crisis.

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Cash rate and Fed fund rate

cash rate Fund rate

Figure 5: Movement of cash rate and Federal fund rate

In 1990, Federal fund rate was 8.10. During this year, corresponding cash rate was 14.83. The

Federal government reduced its fund rate to 5.69. The Reserve Bank of Australia in response to

recessionary shock in 1990 lowered the interest rate to 10 (rba.gov.au 2018). Cash rate reduced

to 5 basis point in 1993. Fed also continued to reduce the cash rate to 3.02 in 1993. As shown

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMICS ASSIGNMENT

from the above graph, cash rate and fund rate are moving almost in the same direction. However,

after the financial crisis the fund rate is set a very low level (Goodfriend, 2016). RBA though has

reduced the cash rate but it is above that of fund rate. In 2016, the fund rate has slightly increased

from 0.13 in 2015 to 0.40 in 2016. The cash rate stabilized at a historically low level of 1.50.

Macroeconomic Outlook for Australia

Despite a relatively slow growth rate in recent years, the economic outlook for Australia

remained positive. It is expected that investment outside construction and mining will increases

bringing a greater opportunity of economic growth. Export will increases following arrival of

new resource sector (Mercer, de Rijke and Dressler, 2014). Household income will increase

gradually along with a growth in consumption. A considerably cash rate by encouraging business

investment will help to pick up inflation and wage growth. However, the RBA needs to stop any

further lowering of the cash rate. Persistently long period of low cash rate contributed to an

increase in housing price in metropolitan areas. This leaves the household in a highly indebted

condition. The highly concentrated baking sector in Australia exposes the economy to the risk of

future financial crisis that can only be avoided by strong intervention of monetary authority

(Armstrong, 2015).

Conclusion

In reference to Australia economy, growth in real GDP has found to be inversely related

with unemployment. With a low growth rate of 2.77 percent unemployment remained

significantly high at the level of 5.70 percent. Inflation has a negative influence on real GDP and

hence on the real GDP growth. In reality however, inflation is likely to influence economic

growth positively. In case of real exchange rate and net export, there exists an inverse relation

between the two. A higher net exchange rate by lowering export reduces net export. Cash rate

and fund rate though move in the same direction but fund rate is lower than cash rate. Despite

some recent interruption, policy makers still have a positive outlook for the economy.

from the above graph, cash rate and fund rate are moving almost in the same direction. However,

after the financial crisis the fund rate is set a very low level (Goodfriend, 2016). RBA though has

reduced the cash rate but it is above that of fund rate. In 2016, the fund rate has slightly increased

from 0.13 in 2015 to 0.40 in 2016. The cash rate stabilized at a historically low level of 1.50.

Macroeconomic Outlook for Australia

Despite a relatively slow growth rate in recent years, the economic outlook for Australia

remained positive. It is expected that investment outside construction and mining will increases

bringing a greater opportunity of economic growth. Export will increases following arrival of

new resource sector (Mercer, de Rijke and Dressler, 2014). Household income will increase

gradually along with a growth in consumption. A considerably cash rate by encouraging business

investment will help to pick up inflation and wage growth. However, the RBA needs to stop any

further lowering of the cash rate. Persistently long period of low cash rate contributed to an

increase in housing price in metropolitan areas. This leaves the household in a highly indebted

condition. The highly concentrated baking sector in Australia exposes the economy to the risk of

future financial crisis that can only be avoided by strong intervention of monetary authority

(Armstrong, 2015).

Conclusion

In reference to Australia economy, growth in real GDP has found to be inversely related

with unemployment. With a low growth rate of 2.77 percent unemployment remained

significantly high at the level of 5.70 percent. Inflation has a negative influence on real GDP and

hence on the real GDP growth. In reality however, inflation is likely to influence economic

growth positively. In case of real exchange rate and net export, there exists an inverse relation

between the two. A higher net exchange rate by lowering export reduces net export. Cash rate

and fund rate though move in the same direction but fund rate is lower than cash rate. Despite

some recent interruption, policy makers still have a positive outlook for the economy.

11ECONOMICS ASSIGNMENT

Reference list

Abs.gov.au. (2018). 6401.0 - Consumer Price Index, Australia, Mar 2018. [online] Available at:

http://www.abs.gov.au/AUSSTATS/abs@.nsf/DetailsPage/6401.0Mar%202018?OpenDocument

[Accessed 19 May 2018].

Andersen, T.B., Malchow-Møller, N. and Nordvig, J., 2015. Inflation targeting and

macroeconomic performance since the Great Recession. Oxford Economic Papers, 67(3),

pp.598-613.

Aph.gov.au. (2018). Australia’s trade in figures – Parliament of Australia. [online] Available at:

https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/

pubs/BriefingBook45p/AustraliaTrade [Accessed 19 May 2018].

Armstrong, S., 2015. The economic impact of the Australia–US free trade agreement. Australian

Journal of International Affairs, 69(5), pp.513-537.

Data.worldbank.org. (2018). Official exchange rate (LCU per US$, period average) | Data.

[online] Available at: https://data.worldbank.org/indicator/PA.NUS.FCRF?locations=AU

[Accessed 19 May 2018].

Dauvin, M., 2014. Energy prices and the real exchange rate of commodity-exporting

countries. International Economics, 137, pp.52-72.

Goodfriend, M., 2016, August. The case for unencumbering interest rate policy at the zero

bound. In Federal Reserve Bank of Kansas City’s 40th Economic Policy Symposium. Jackson

Hole, WY. August (Vol. 26).

Halling, M., Yu, J. and Zechner, J., 2016. Leverage dynamics over the business cycle. Journal of

Financial Economics, 122(1), pp.21-41.

Ihrig, J.E., Meade, E.E. and Weinbach, G.C., 2015. Rewriting Monetary Policy 101: What's the

Fed's Preferred Post-Crisis Approach to Raising Interest Rates?. Journal of Economic

Perspectives, 29(4), pp.177-98.

Jiang, B., Athanasopoulos, G., Hyndman, R.J., Panagiotelis, A. and Vahid, F., 2017.

Macroeconomic forecasting for Australia using a large number of predictors. Monash

Econometrics and Business Statistics Working Papers, 2, p.17.

Kent, C. (2018). The Business Cycle in Australia | Speeches | RBA. [online] Reserve Bank of

Australia. Available at: https://www.rba.gov.au/speeches/2014/sp-ag-131114.html [Accessed 19

May 2018].

Kent, C., 2014. The Business Cycle in Australia. Address to the Australian Business Economists,

Sydney, 13.

Keynes, J.M., 2016. General theory of employment, interest and money. Atlantic Publishers &

Dist.

Mankiw, N.G., 2014. Principles of macroeconomics. Cengage Learning.

Reference list

Abs.gov.au. (2018). 6401.0 - Consumer Price Index, Australia, Mar 2018. [online] Available at:

http://www.abs.gov.au/AUSSTATS/abs@.nsf/DetailsPage/6401.0Mar%202018?OpenDocument

[Accessed 19 May 2018].

Andersen, T.B., Malchow-Møller, N. and Nordvig, J., 2015. Inflation targeting and

macroeconomic performance since the Great Recession. Oxford Economic Papers, 67(3),

pp.598-613.

Aph.gov.au. (2018). Australia’s trade in figures – Parliament of Australia. [online] Available at:

https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/

pubs/BriefingBook45p/AustraliaTrade [Accessed 19 May 2018].

Armstrong, S., 2015. The economic impact of the Australia–US free trade agreement. Australian

Journal of International Affairs, 69(5), pp.513-537.

Data.worldbank.org. (2018). Official exchange rate (LCU per US$, period average) | Data.

[online] Available at: https://data.worldbank.org/indicator/PA.NUS.FCRF?locations=AU

[Accessed 19 May 2018].

Dauvin, M., 2014. Energy prices and the real exchange rate of commodity-exporting

countries. International Economics, 137, pp.52-72.

Goodfriend, M., 2016, August. The case for unencumbering interest rate policy at the zero

bound. In Federal Reserve Bank of Kansas City’s 40th Economic Policy Symposium. Jackson

Hole, WY. August (Vol. 26).

Halling, M., Yu, J. and Zechner, J., 2016. Leverage dynamics over the business cycle. Journal of

Financial Economics, 122(1), pp.21-41.

Ihrig, J.E., Meade, E.E. and Weinbach, G.C., 2015. Rewriting Monetary Policy 101: What's the

Fed's Preferred Post-Crisis Approach to Raising Interest Rates?. Journal of Economic

Perspectives, 29(4), pp.177-98.

Jiang, B., Athanasopoulos, G., Hyndman, R.J., Panagiotelis, A. and Vahid, F., 2017.

Macroeconomic forecasting for Australia using a large number of predictors. Monash

Econometrics and Business Statistics Working Papers, 2, p.17.

Kent, C. (2018). The Business Cycle in Australia | Speeches | RBA. [online] Reserve Bank of

Australia. Available at: https://www.rba.gov.au/speeches/2014/sp-ag-131114.html [Accessed 19

May 2018].

Kent, C., 2014. The Business Cycle in Australia. Address to the Australian Business Economists,

Sydney, 13.

Keynes, J.M., 2016. General theory of employment, interest and money. Atlantic Publishers &

Dist.

Mankiw, N.G., 2014. Principles of macroeconomics. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.