EFN405 Applied Economics: Analyzing Economic Growth in Australia

VerifiedAdded on 2023/06/11

|8

|2123

|398

Homework Assignment

AI Summary

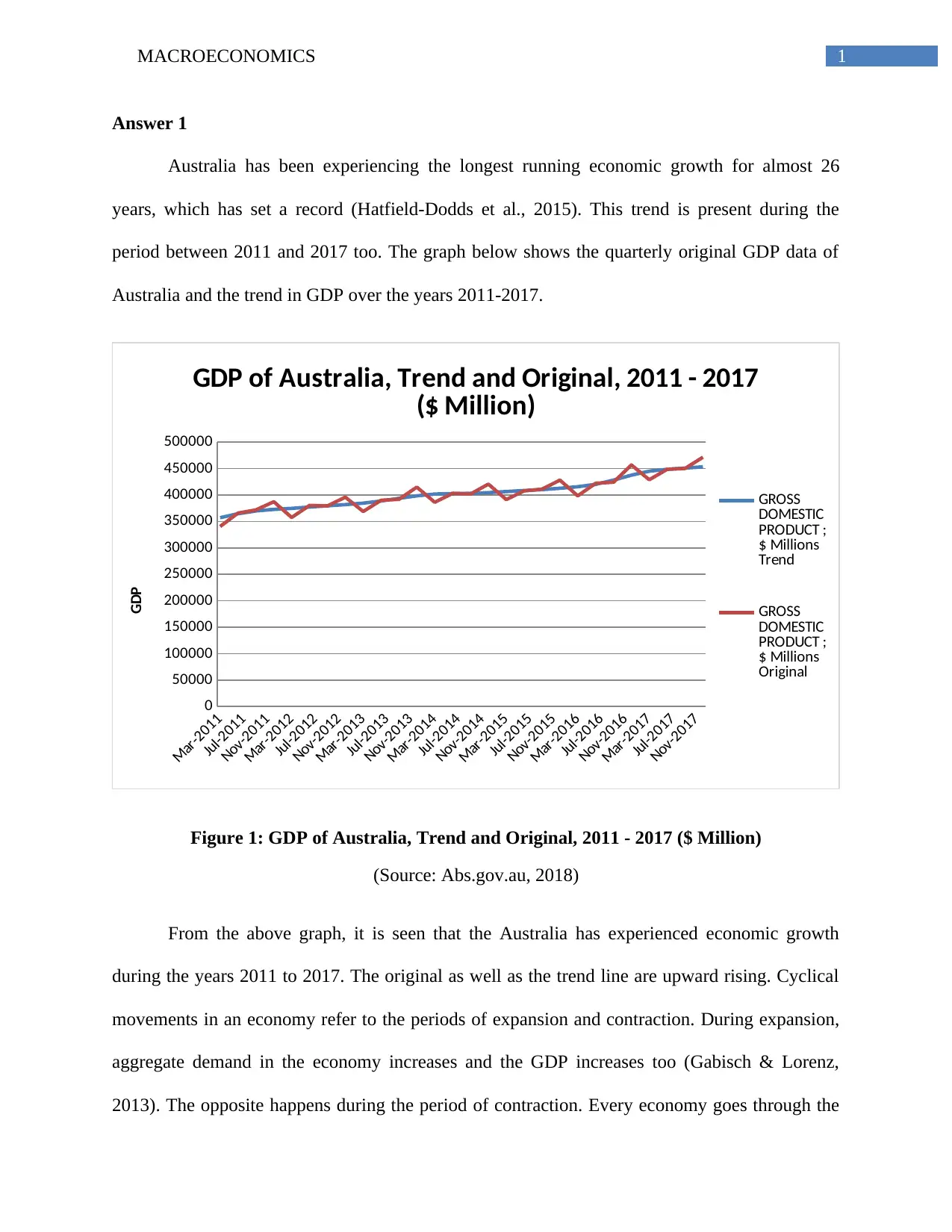

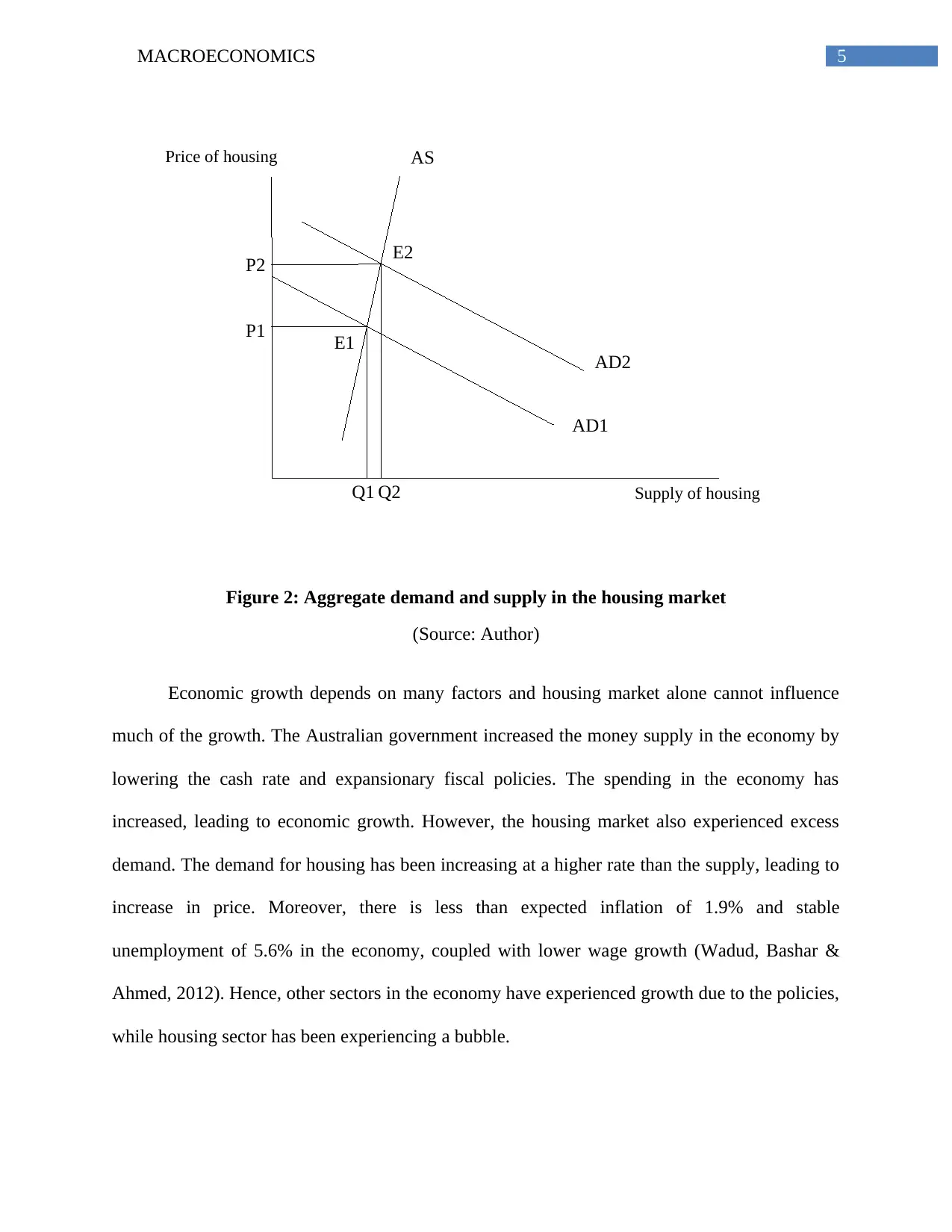

This assignment provides an analysis of Australia's macroeconomic performance between 2011 and 2017, focusing on economic growth, cyclical movements, and the impact of fiscal and monetary policies. It examines the structural shift in the Australian economy from manufacturing and agriculture to the service and mining sectors, highlighting the influence of global events like the financial crisis and increasing demand from China. The analysis also covers the housing market bubble, the effects of tax policies, and the role of the Reserve Bank of Australia (RBA) in managing inflation and unemployment. The assignment concludes that while government policies have contributed to overall economic growth, the housing sector has experienced excessive demand and price increases, leading to a housing bubble.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.