Australia's Macroeconomic Policy Brief: ECON1010, Sem 1 2019 Analysis

VerifiedAdded on 2022/10/19

|8

|1693

|454

Report

AI Summary

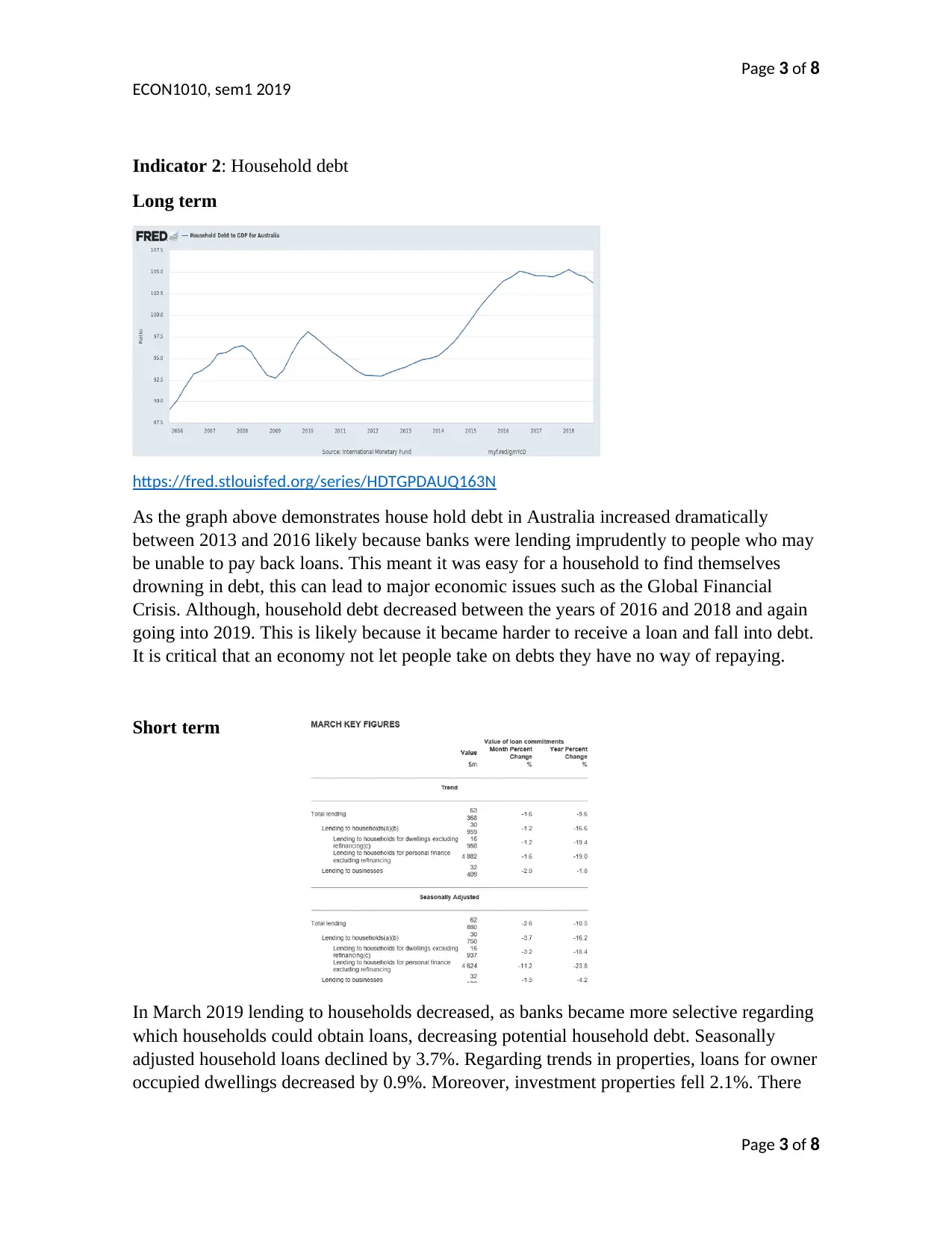

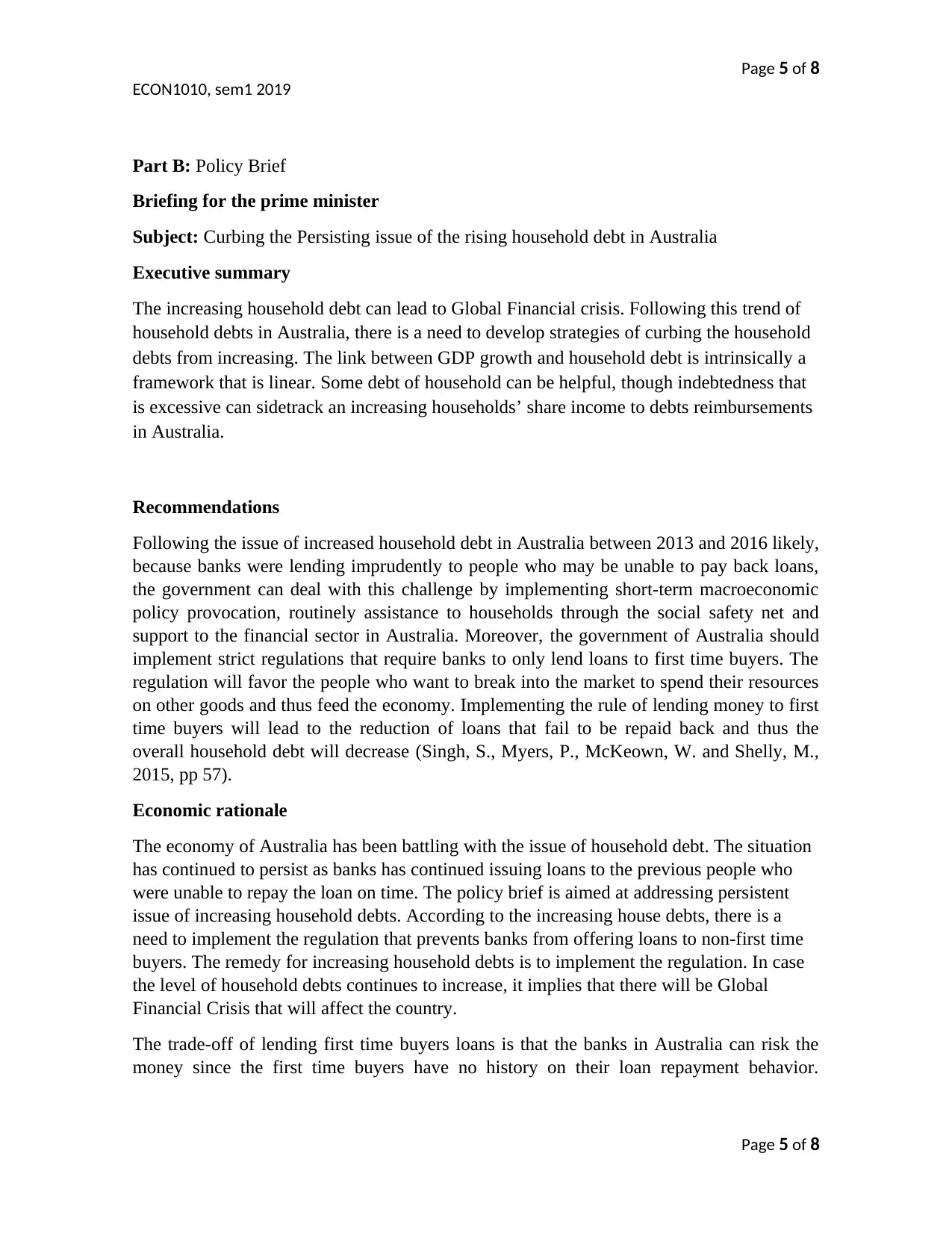

This report provides a comprehensive macroeconomic analysis of Australia, focusing on the Consumer Price Index (CPI) and household debt. The analysis examines long-term and short-term trends in CPI, revealing changes in consumer spending across different sectors and a decreasing inflation rate. It also explores the dramatic increase and subsequent decrease in household debt between 2013 and 2019, attributing the changes to lending practices and government regulations. The policy brief section then addresses the issue of rising household debt, proposing strategies such as short-term macroeconomic policy provocations, routine assistance through a social safety net, and support to the financial sector. The report argues for strict regulations on bank lending, favoring first-time buyers, and highlights the economic rationale behind these recommendations, including the potential for a Global Financial Crisis if household debt continues to increase. The report references relevant academic literature to support its findings and recommendations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.