Australia & New Zealand Tax Law: A Comparative Report for Investors

VerifiedAdded on 2023/06/07

|12

|2554

|97

Report

AI Summary

This report provides a comparative analysis of the taxation laws of Australia and New Zealand, specifically tailored for an international investor residing in Australia. It examines the Income Tax Assessment Act 1997 of Australia and the Income Tax Act 2007 of New Zealand, highlighting the differences in income tax rates, capital gains tax, and fringe benefits tax. The report also discusses the impact of tax treaties, international legislation, and Australian Taxation Office rulings on the investor's tax obligations. Case laws such as Harding v FCT and SARS v Van Kets are referenced to provide context. Ultimately, the report aims to determine which country, Australia or New Zealand, is more advantageous from a taxation perspective, considering the investor's income, investments, and fringe benefits.

Running head: Australia Taxation Law

Australia Taxation Law

Australia Taxation Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australia Taxation Law 1

Executive Summary

Income tax in Australia is levied by the federal government on the taxable income of

corporations and individuals. On the individuals, the income tax is imposed at a progressive rate

while on corporations, it is levied on either of two tax rates. The two legislations under which

income tax is collected are the Income Tax Assessment Act 1936 and Income Tax Assessment

Act 1997. Income Tax Assessment Act 1997 is an act passed by the Australian Parliament. It is

amongst the important legislation which forms the basis of calculation of income tax. It is a

rewritten version of the previous Income Tax Assessment Act 1936.

So, in this report, the various aspects of the Income Tax Assessment Act 1997 would be stated

along with explaining the difference between the taxation law of Australia and New Zealand.As

appointed by the local consultancy service, the various tax treaties, international legislation and

Income tax rulings issued by the Australian Taxation Office shall be described along with the

relevant case laws.

Executive Summary

Income tax in Australia is levied by the federal government on the taxable income of

corporations and individuals. On the individuals, the income tax is imposed at a progressive rate

while on corporations, it is levied on either of two tax rates. The two legislations under which

income tax is collected are the Income Tax Assessment Act 1936 and Income Tax Assessment

Act 1997. Income Tax Assessment Act 1997 is an act passed by the Australian Parliament. It is

amongst the important legislation which forms the basis of calculation of income tax. It is a

rewritten version of the previous Income Tax Assessment Act 1936.

So, in this report, the various aspects of the Income Tax Assessment Act 1997 would be stated

along with explaining the difference between the taxation law of Australia and New Zealand.As

appointed by the local consultancy service, the various tax treaties, international legislation and

Income tax rulings issued by the Australian Taxation Office shall be described along with the

relevant case laws.

Australia Taxation Law 2

Contents

Introduction.................................................................................................................................................3

Income tax and Capital Gain Tax rates for non-resident individuals.........................................................4

Income Tax rulings issued by Australian Taxation Office and International treaties executed by Australia

with various countries..................................................................................................................................6

Taxation Law of New Zealand....................................................................................................................7

Conclusion...................................................................................................................................................9

Bibliography...............................................................................................................................................10

Contents

Introduction.................................................................................................................................................3

Income tax and Capital Gain Tax rates for non-resident individuals.........................................................4

Income Tax rulings issued by Australian Taxation Office and International treaties executed by Australia

with various countries..................................................................................................................................6

Taxation Law of New Zealand....................................................................................................................7

Conclusion...................................................................................................................................................9

Bibliography...............................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australia Taxation Law 3

Introduction

Income Tax in Australia is imposed by the federal government on the income earned by the

individuals and companies. On individuals, the income tax is imposed at progressive rates while

in the case of companies, it is levied on either of two rates prescribed in this behalf. Income tax

is the most significant source of revenue for the government and it is collected by the Australian

Taxation Office.

The Income tax is imposed by Income Tax Assessment Act 1997 which is rewritten from the

previous version Income Tax Assessment Act 1936. There are three categories of assessable

incomes for individual taxpayers viz. personal earnings like salary and wages, capital gains and

business income. The taxable income of individuals is taxed at progressive rates ranging from 0

to 45% along with the Medicare levy of 2%. The income earned by companies is taxable at

27.5% or 30% which is dependent upon the annual turnover. Capital gains are subject to tax at

the point of gain which is decreased by 50% in case if the capital asset was held for 1 year prior

to selling. The financial year runs from 1st July to 30th June of the following year.

So, in this assignment the various aspects of Income Tax Assessment Act 1997 of Australia and

Income Tax Act 2007 of New Zealand would be stated along with explaining the various tax

treaties, International laws and Income tax rulings issued by the Australian Taxation Office in

reference to case laws.

Introduction

Income Tax in Australia is imposed by the federal government on the income earned by the

individuals and companies. On individuals, the income tax is imposed at progressive rates while

in the case of companies, it is levied on either of two rates prescribed in this behalf. Income tax

is the most significant source of revenue for the government and it is collected by the Australian

Taxation Office.

The Income tax is imposed by Income Tax Assessment Act 1997 which is rewritten from the

previous version Income Tax Assessment Act 1936. There are three categories of assessable

incomes for individual taxpayers viz. personal earnings like salary and wages, capital gains and

business income. The taxable income of individuals is taxed at progressive rates ranging from 0

to 45% along with the Medicare levy of 2%. The income earned by companies is taxable at

27.5% or 30% which is dependent upon the annual turnover. Capital gains are subject to tax at

the point of gain which is decreased by 50% in case if the capital asset was held for 1 year prior

to selling. The financial year runs from 1st July to 30th June of the following year.

So, in this assignment the various aspects of Income Tax Assessment Act 1997 of Australia and

Income Tax Act 2007 of New Zealand would be stated along with explaining the various tax

treaties, International laws and Income tax rulings issued by the Australian Taxation Office in

reference to case laws.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australia Taxation Law 4

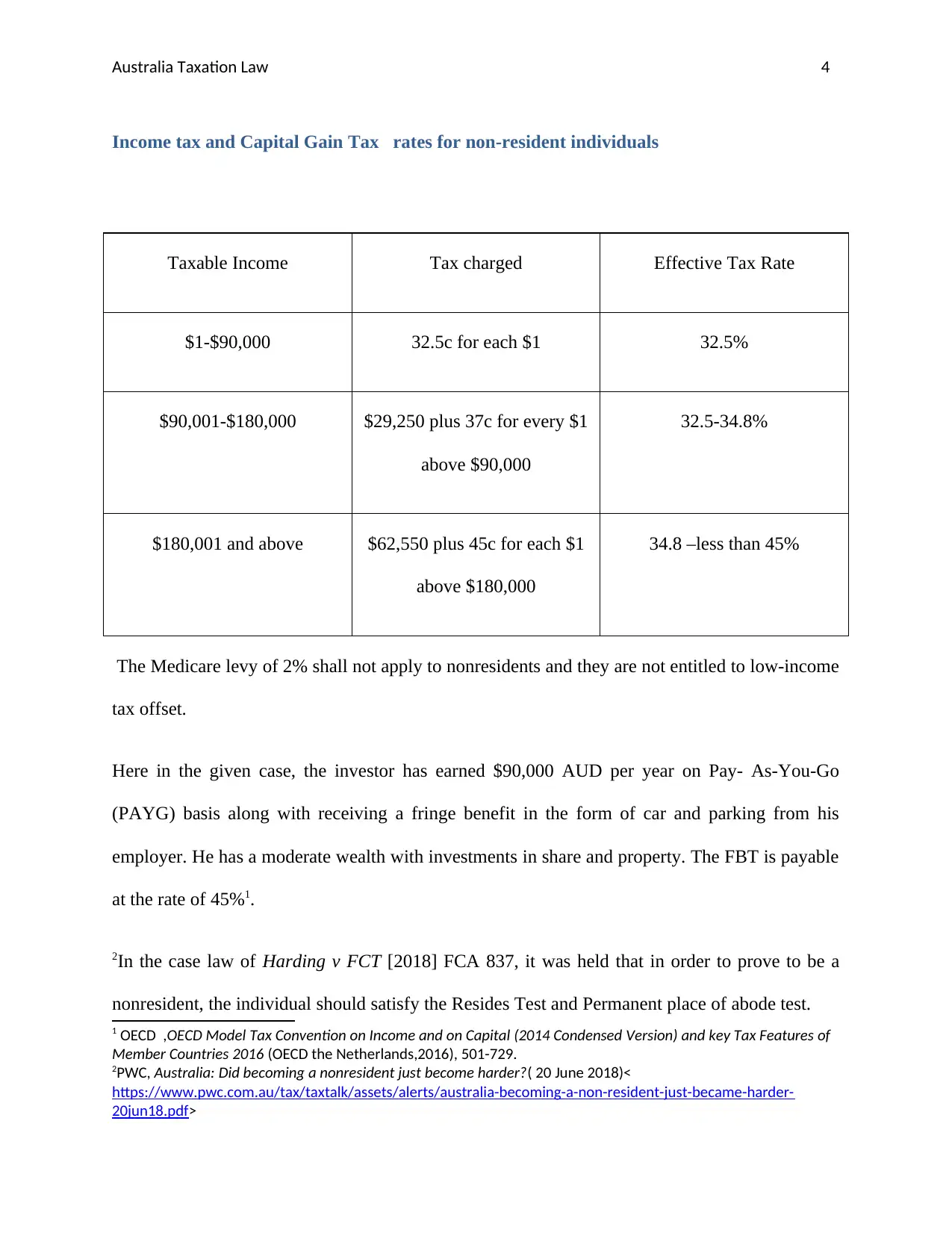

Income tax and Capital Gain Tax rates for non-resident individuals

Taxable Income Tax charged Effective Tax Rate

$1-$90,000 32.5c for each $1 32.5%

$90,001-$180,000 $29,250 plus 37c for every $1

above $90,000

32.5-34.8%

$180,001 and above $62,550 plus 45c for each $1

above $180,000

34.8 –less than 45%

The Medicare levy of 2% shall not apply to nonresidents and they are not entitled to low-income

tax offset.

Here in the given case, the investor has earned $90,000 AUD per year on Pay- As-You-Go

(PAYG) basis along with receiving a fringe benefit in the form of car and parking from his

employer. He has a moderate wealth with investments in share and property. The FBT is payable

at the rate of 45%1.

2In the case law of Harding v FCT [2018] FCA 837, it was held that in order to prove to be a

nonresident, the individual should satisfy the Resides Test and Permanent place of abode test.

1 OECD ,OECD Model Tax Convention on Income and on Capital (2014 Condensed Version) and key Tax Features of

Member Countries 2016 (OECD the Netherlands,2016), 501-729.

2PWC, Australia: Did becoming a nonresident just become harder?( 20 June 2018)<

https://www.pwc.com.au/tax/taxtalk/assets/alerts/australia-becoming-a-non-resident-just-became-harder-

20jun18.pdf>

Income tax and Capital Gain Tax rates for non-resident individuals

Taxable Income Tax charged Effective Tax Rate

$1-$90,000 32.5c for each $1 32.5%

$90,001-$180,000 $29,250 plus 37c for every $1

above $90,000

32.5-34.8%

$180,001 and above $62,550 plus 45c for each $1

above $180,000

34.8 –less than 45%

The Medicare levy of 2% shall not apply to nonresidents and they are not entitled to low-income

tax offset.

Here in the given case, the investor has earned $90,000 AUD per year on Pay- As-You-Go

(PAYG) basis along with receiving a fringe benefit in the form of car and parking from his

employer. He has a moderate wealth with investments in share and property. The FBT is payable

at the rate of 45%1.

2In the case law of Harding v FCT [2018] FCA 837, it was held that in order to prove to be a

nonresident, the individual should satisfy the Resides Test and Permanent place of abode test.

1 OECD ,OECD Model Tax Convention on Income and on Capital (2014 Condensed Version) and key Tax Features of

Member Countries 2016 (OECD the Netherlands,2016), 501-729.

2PWC, Australia: Did becoming a nonresident just become harder?( 20 June 2018)<

https://www.pwc.com.au/tax/taxtalk/assets/alerts/australia-becoming-a-non-resident-just-became-harder-

20jun18.pdf>

Australia Taxation Law 5

3In the case of Applegate v Federal Commissioner of Taxation [1912] VicLawRp 78; (1978) 18

ALR 459, the court decided that the word resides is not a term which denotes and with defined

boundaries.

In Australia, the income tax is collected by withholding tax known as Pay-As-You-Go (PAYG).

For individuals who have a single job, the taxable amount is almost equal to the amount due

before deductions are applied at the end of the year. The inconsistencies and deductions are

declared in the annual tax return and would form a part of the refund which shall follow after the

yearly assessment or amount can also be reduced which is payable after assessment. So he shall

be charged at the rate of 32.5c for each $1 and tax rate would be 32.5%.

Also the net capital gain is included in the taxable income of taxpayer and it is taxed at a

marginal rate in the year the capital gain taxable event arises. Hence the investor, while selling

the asset should take the selling price and deduct the associated costs and original price from it.

The residual amount is capital gain or loss. If the asset is held for more than 12 months, the

deduction of 50% should be applied to the net capital gain provided that the indexation method

does not apply4.

Income Tax rulings issued by Australian Taxation Office and International treaties

executed by Australia with various countries

Tax treaties are bilateral agreements between two countries and Australia has tax treaties with

more than 40 countries including New Zealand. With New Zealand, it has entered International

Tax Agreements Amendment Bill (No 2) 2009 which was in force from 2010.

3 Australian Government :Australian Taxation Office ,Decision Impact Statement(n.d.)<

http://law.ato.gov.au/atolaw/view.htm?docid=%22LIT%2FICD%2F2013%2F4861-2013%2F4862%2F00001%22>

4 NAB, Understanding Capital Gains And Tax( n.d.)< https://www.nab.com.au/personal/learn/managing-your-

debts/capital-gains-tax>

3In the case of Applegate v Federal Commissioner of Taxation [1912] VicLawRp 78; (1978) 18

ALR 459, the court decided that the word resides is not a term which denotes and with defined

boundaries.

In Australia, the income tax is collected by withholding tax known as Pay-As-You-Go (PAYG).

For individuals who have a single job, the taxable amount is almost equal to the amount due

before deductions are applied at the end of the year. The inconsistencies and deductions are

declared in the annual tax return and would form a part of the refund which shall follow after the

yearly assessment or amount can also be reduced which is payable after assessment. So he shall

be charged at the rate of 32.5c for each $1 and tax rate would be 32.5%.

Also the net capital gain is included in the taxable income of taxpayer and it is taxed at a

marginal rate in the year the capital gain taxable event arises. Hence the investor, while selling

the asset should take the selling price and deduct the associated costs and original price from it.

The residual amount is capital gain or loss. If the asset is held for more than 12 months, the

deduction of 50% should be applied to the net capital gain provided that the indexation method

does not apply4.

Income Tax rulings issued by Australian Taxation Office and International treaties

executed by Australia with various countries

Tax treaties are bilateral agreements between two countries and Australia has tax treaties with

more than 40 countries including New Zealand. With New Zealand, it has entered International

Tax Agreements Amendment Bill (No 2) 2009 which was in force from 2010.

3 Australian Government :Australian Taxation Office ,Decision Impact Statement(n.d.)<

http://law.ato.gov.au/atolaw/view.htm?docid=%22LIT%2FICD%2F2013%2F4861-2013%2F4862%2F00001%22>

4 NAB, Understanding Capital Gains And Tax( n.d.)< https://www.nab.com.au/personal/learn/managing-your-

debts/capital-gains-tax>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australia Taxation Law 6

These tax treaties are also referred to as double tax agreements (DTA). They help in preventing

the double taxation and fiscal dodging and assist in fostering cooperation between Australia and

other international tax authorities through the enforcement of respective tax laws.

In the case law of SARS v Van Kets [2012] JOL 28416 (WCC), it was held that the purpose of

exchange of information is to make sure that the resident of Australia does not escape from the

tax which is raised in South Africa.

In A v Commissioner of Inland Revenue [2017] NZTRA 08, it was held that the primary basis for

assessment by the commissioner was income under ordinary concepts. The authority therefore

found that in the given case there were certain isolated transactions of international money

transfers and purchases which had an insufficient link with the disputes , so it disallowed the

amounts.

So, with respect to tax treaties with New Zealand, it would help the investor by reducing the

double taxation caused by overlapping tax jurisdictions. In this case, the income tax and the

fringe benefits tax is levied by the federal law of Australia to the investor who is a nonresident

and originally resides in New Zealand. So, it would help him in resolving the dual claim in

relation to his residential status and source of income.

The Australian Taxation Office publishes its views on the transactions of Commonwealth

taxation laws which can be in the form of authoritative interpretative guidance and rulings and

the decision impact statements on the decisions of the court and tribunal. The system of taxation

rulings permits the commissioner to make the rulings binding which must be honored by the

These tax treaties are also referred to as double tax agreements (DTA). They help in preventing

the double taxation and fiscal dodging and assist in fostering cooperation between Australia and

other international tax authorities through the enforcement of respective tax laws.

In the case law of SARS v Van Kets [2012] JOL 28416 (WCC), it was held that the purpose of

exchange of information is to make sure that the resident of Australia does not escape from the

tax which is raised in South Africa.

In A v Commissioner of Inland Revenue [2017] NZTRA 08, it was held that the primary basis for

assessment by the commissioner was income under ordinary concepts. The authority therefore

found that in the given case there were certain isolated transactions of international money

transfers and purchases which had an insufficient link with the disputes , so it disallowed the

amounts.

So, with respect to tax treaties with New Zealand, it would help the investor by reducing the

double taxation caused by overlapping tax jurisdictions. In this case, the income tax and the

fringe benefits tax is levied by the federal law of Australia to the investor who is a nonresident

and originally resides in New Zealand. So, it would help him in resolving the dual claim in

relation to his residential status and source of income.

The Australian Taxation Office publishes its views on the transactions of Commonwealth

taxation laws which can be in the form of authoritative interpretative guidance and rulings and

the decision impact statements on the decisions of the court and tribunal. The system of taxation

rulings permits the commissioner to make the rulings binding which must be honored by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australia Taxation Law 7

Commissioner. The taxpayer can rely on the ruling and he cannot be penalized by the ATO, even

if later on the views in the rulings are found to be incorrect. The rulings include public and

private rulings. The former includes the advice issued by the ATO for explaining the application

of taxation laws to taxpayers and include- Income Tax Rulings, Taxation rulings etc. while the

latter include advice to a particular taxpayer for specified arrangements5.

Private rulings may be later converted into public rulings to provide guidance to others known as

interpretive decisions. Lastly, oral advice are given on the simple matters related to taxation

affairs of the individual taxpayers6.

Taxation Law of New Zealand

In New Zealand, the prevailing legislation of income tax is the Income Tax Act 2007. The tax

levying authorities are Inland Revenue Department.7 The Tax Administration Act 1994

administers how Inland Revenue Department administers the legislation of tax. In New Zealand,

there is no capital gain tax. Some gains such as profits on the sale of patent rights and

speculation in property transactions are deemed to be income under the capital gain category.

The residents are subjected to tax on income earned internationally . So, the investor would be

taxed on the income earned in Australia but due to Double Taxation Agreements, he would not

be taxed in New Zealand.

8Income tax rates for New Zealand are as follows:

5 Hermione Parker, Instead of the Dole: An Enquiry into Integration of the Tax and Benefit Systems(Routledge

London, 2018) 100

6 Matthew C. Murray and Carole Pateman , Basic Income Worldwide: Horizons of Reform(Palgrave

Macmillan,2012) 100

7 Deloitte ,International Tax New Zealand Highlights 2018(n.d.)<

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-newzealandhighlights-

2018.pdf>

8 PWC, New Zealand Individual - Taxes on personal income(2018)< http://taxsummaries.pwc.com/ID/New-Zealand-

Individual-Taxes-on-personal-income >

Commissioner. The taxpayer can rely on the ruling and he cannot be penalized by the ATO, even

if later on the views in the rulings are found to be incorrect. The rulings include public and

private rulings. The former includes the advice issued by the ATO for explaining the application

of taxation laws to taxpayers and include- Income Tax Rulings, Taxation rulings etc. while the

latter include advice to a particular taxpayer for specified arrangements5.

Private rulings may be later converted into public rulings to provide guidance to others known as

interpretive decisions. Lastly, oral advice are given on the simple matters related to taxation

affairs of the individual taxpayers6.

Taxation Law of New Zealand

In New Zealand, the prevailing legislation of income tax is the Income Tax Act 2007. The tax

levying authorities are Inland Revenue Department.7 The Tax Administration Act 1994

administers how Inland Revenue Department administers the legislation of tax. In New Zealand,

there is no capital gain tax. Some gains such as profits on the sale of patent rights and

speculation in property transactions are deemed to be income under the capital gain category.

The residents are subjected to tax on income earned internationally . So, the investor would be

taxed on the income earned in Australia but due to Double Taxation Agreements, he would not

be taxed in New Zealand.

8Income tax rates for New Zealand are as follows:

5 Hermione Parker, Instead of the Dole: An Enquiry into Integration of the Tax and Benefit Systems(Routledge

London, 2018) 100

6 Matthew C. Murray and Carole Pateman , Basic Income Worldwide: Horizons of Reform(Palgrave

Macmillan,2012) 100

7 Deloitte ,International Tax New Zealand Highlights 2018(n.d.)<

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-newzealandhighlights-

2018.pdf>

8 PWC, New Zealand Individual - Taxes on personal income(2018)< http://taxsummaries.pwc.com/ID/New-Zealand-

Individual-Taxes-on-personal-income >

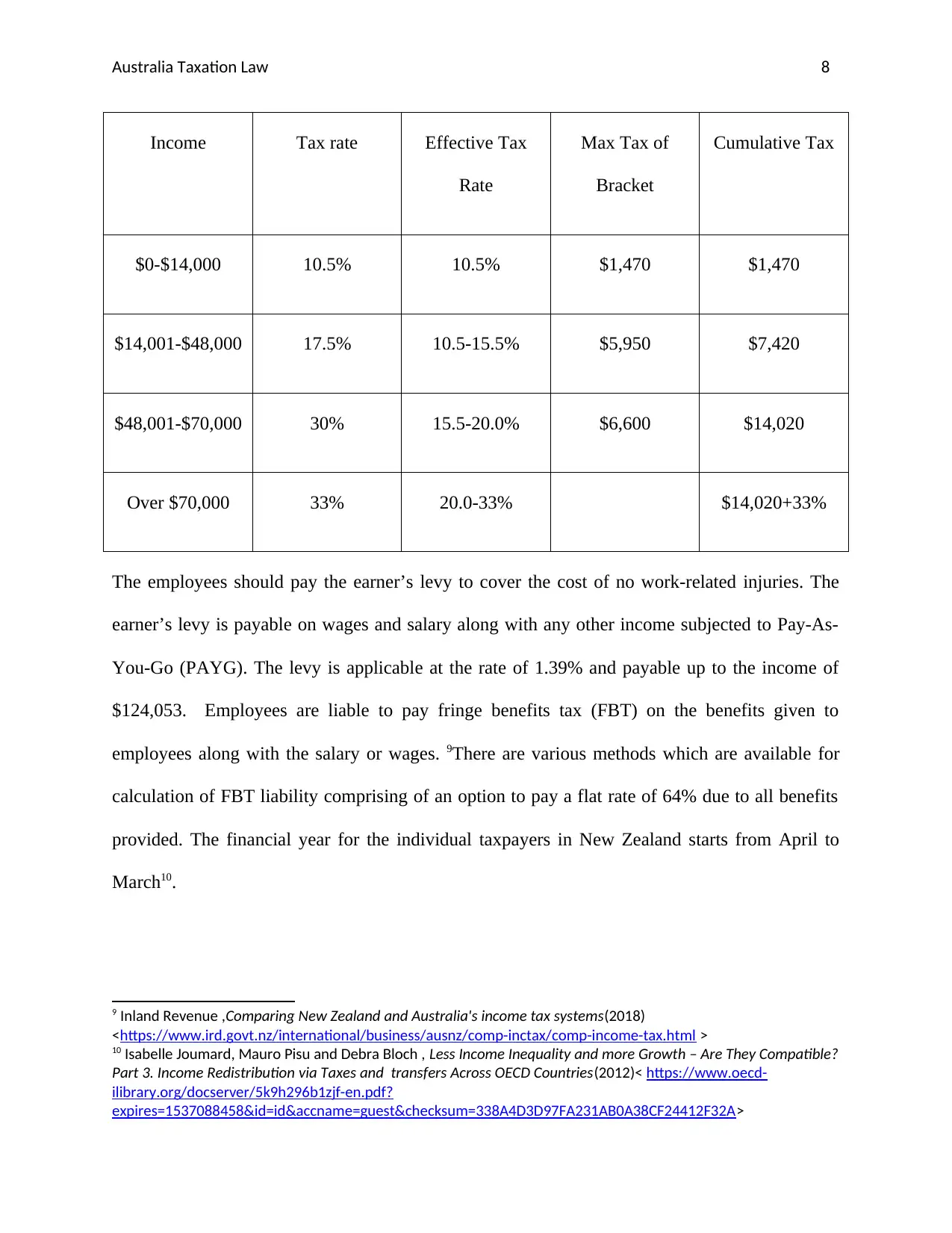

Australia Taxation Law 8

Income Tax rate Effective Tax

Rate

Max Tax of

Bracket

Cumulative Tax

$0-$14,000 10.5% 10.5% $1,470 $1,470

$14,001-$48,000 17.5% 10.5-15.5% $5,950 $7,420

$48,001-$70,000 30% 15.5-20.0% $6,600 $14,020

Over $70,000 33% 20.0-33% $14,020+33%

The employees should pay the earner’s levy to cover the cost of no work-related injuries. The

earner’s levy is payable on wages and salary along with any other income subjected to Pay-As-

You-Go (PAYG). The levy is applicable at the rate of 1.39% and payable up to the income of

$124,053. Employees are liable to pay fringe benefits tax (FBT) on the benefits given to

employees along with the salary or wages. 9There are various methods which are available for

calculation of FBT liability comprising of an option to pay a flat rate of 64% due to all benefits

provided. The financial year for the individual taxpayers in New Zealand starts from April to

March10.

9 Inland Revenue ,Comparing New Zealand and Australia's income tax systems(2018)

<https://www.ird.govt.nz/international/business/ausnz/comp-inctax/comp-income-tax.html >

10 Isabelle Joumard, Mauro Pisu and Debra Bloch , Less Income Inequality and more Growth – Are They Compatible?

Part 3. Income Redistribution via Taxes and transfers Across OECD Countries(2012)< https://www.oecd-

ilibrary.org/docserver/5k9h296b1zjf-en.pdf?

expires=1537088458&id=id&accname=guest&checksum=338A4D3D97FA231AB0A38CF24412F32A>

Income Tax rate Effective Tax

Rate

Max Tax of

Bracket

Cumulative Tax

$0-$14,000 10.5% 10.5% $1,470 $1,470

$14,001-$48,000 17.5% 10.5-15.5% $5,950 $7,420

$48,001-$70,000 30% 15.5-20.0% $6,600 $14,020

Over $70,000 33% 20.0-33% $14,020+33%

The employees should pay the earner’s levy to cover the cost of no work-related injuries. The

earner’s levy is payable on wages and salary along with any other income subjected to Pay-As-

You-Go (PAYG). The levy is applicable at the rate of 1.39% and payable up to the income of

$124,053. Employees are liable to pay fringe benefits tax (FBT) on the benefits given to

employees along with the salary or wages. 9There are various methods which are available for

calculation of FBT liability comprising of an option to pay a flat rate of 64% due to all benefits

provided. The financial year for the individual taxpayers in New Zealand starts from April to

March10.

9 Inland Revenue ,Comparing New Zealand and Australia's income tax systems(2018)

<https://www.ird.govt.nz/international/business/ausnz/comp-inctax/comp-income-tax.html >

10 Isabelle Joumard, Mauro Pisu and Debra Bloch , Less Income Inequality and more Growth – Are They Compatible?

Part 3. Income Redistribution via Taxes and transfers Across OECD Countries(2012)< https://www.oecd-

ilibrary.org/docserver/5k9h296b1zjf-en.pdf?

expires=1537088458&id=id&accname=guest&checksum=338A4D3D97FA231AB0A38CF24412F32A>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australia Taxation Law 9

In Australia, the tax rates are 32.5-34.8% whereas in New Zealand the tax rates are 20-33%, so

the investor should reside in New Zealand. Also, there is a fringe benefits tax of 64% in New

Zealand while it is charged at the rate of 45% in Australia11.

But the investor should reside in his home country i.e. New Zealand because it is much more

beneficial to him as compared to Australia.

Conclusion

Hence to conclude, it can be said that the taxation system of Australia and New Zealand is that in

both of them, the residents are taxed on the income earned worldwide and the nonresidents are

taxed on the income earned in both the countries. The income year in Australia starts from 1 July

to 31 June and in New Zealand, the income year is from 1 April to 31 March.

Although both the countries have similar taxation systems there is a difference between the slab

rates, so the investor should reside in New Zealand from the point of view of taxation levied.

Bibliography

OECD ,OECD Model Tax Convention on Income and on Capital (2014 Condensed Version)

and key Tax Features of Member Countries 2016 (OECD the Netherlands,2016)

PWC, Australia: Did becoming a nonresident just become harder?( 20 June 2018)<

https://www.pwc.com.au/tax/taxtalk/assets/alerts/australia-becoming-a-non-resident-just-

became-harder-20jun18.pdf>

11 Timothy Higgins, Income Contingent Loans: Theory, Practice and Prospects(Routledge London, 2014) 100

In Australia, the tax rates are 32.5-34.8% whereas in New Zealand the tax rates are 20-33%, so

the investor should reside in New Zealand. Also, there is a fringe benefits tax of 64% in New

Zealand while it is charged at the rate of 45% in Australia11.

But the investor should reside in his home country i.e. New Zealand because it is much more

beneficial to him as compared to Australia.

Conclusion

Hence to conclude, it can be said that the taxation system of Australia and New Zealand is that in

both of them, the residents are taxed on the income earned worldwide and the nonresidents are

taxed on the income earned in both the countries. The income year in Australia starts from 1 July

to 31 June and in New Zealand, the income year is from 1 April to 31 March.

Although both the countries have similar taxation systems there is a difference between the slab

rates, so the investor should reside in New Zealand from the point of view of taxation levied.

Bibliography

OECD ,OECD Model Tax Convention on Income and on Capital (2014 Condensed Version)

and key Tax Features of Member Countries 2016 (OECD the Netherlands,2016)

PWC, Australia: Did becoming a nonresident just become harder?( 20 June 2018)<

https://www.pwc.com.au/tax/taxtalk/assets/alerts/australia-becoming-a-non-resident-just-

became-harder-20jun18.pdf>

11 Timothy Higgins, Income Contingent Loans: Theory, Practice and Prospects(Routledge London, 2014) 100

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australia Taxation Law 10

Australian Government :Australian Taxation Office ,Decision Impact Statement(n.d.)<

http://law.ato.gov.au/atolaw/view.htm?docid=%22LIT%2FICD%2F2013%2F4861-

2013%2F4862%2F00001%22>

NAB, Understanding Capital Gains And Tax( n.d.)<

https://www.nab.com.au/personal/learn/managing-your-debts/capital-gains-tax>

Australian Government : The Treasury , Income Tax Treaties(n.d.) < https://treasury.gov.au/tax-

treaties/income-tax-treaties/ >

Parker Hermione , Instead of the Dole: An Enquiry into Integration of the Tax and Benefit

Systems(Routledge London, 2018)

Murray Matthew C. and Pateman Carole , Basic Income Worldwide: Horizons of

Reform(Palgrave Macmillan,2012)

Deloitte ,International Tax New Zealand Highlights 2018(n.d.)<

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

newzealandhighlights-2018.pdf>

PWC, New Zealand Individual - Taxes on personal income(2018)<

http://taxsummaries.pwc.com/ID/New-Zealand-Individual-Taxes-on-personal-income >

Inland Revenue ,Comparing New Zealand and Australia's income tax systems(2018)

<https://www.ird.govt.nz/international/business/ausnz/comp-inctax/comp-income-tax.html >

Joumard Isabelle , Pisu Mauro and Bloch Debra , Less Income Inequality and more Growth –

Are They Compatible? Part 3. Income Redistribution via Taxes and transfers Across OECD

Australian Government :Australian Taxation Office ,Decision Impact Statement(n.d.)<

http://law.ato.gov.au/atolaw/view.htm?docid=%22LIT%2FICD%2F2013%2F4861-

2013%2F4862%2F00001%22>

NAB, Understanding Capital Gains And Tax( n.d.)<

https://www.nab.com.au/personal/learn/managing-your-debts/capital-gains-tax>

Australian Government : The Treasury , Income Tax Treaties(n.d.) < https://treasury.gov.au/tax-

treaties/income-tax-treaties/ >

Parker Hermione , Instead of the Dole: An Enquiry into Integration of the Tax and Benefit

Systems(Routledge London, 2018)

Murray Matthew C. and Pateman Carole , Basic Income Worldwide: Horizons of

Reform(Palgrave Macmillan,2012)

Deloitte ,International Tax New Zealand Highlights 2018(n.d.)<

https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Tax/dttl-tax-

newzealandhighlights-2018.pdf>

PWC, New Zealand Individual - Taxes on personal income(2018)<

http://taxsummaries.pwc.com/ID/New-Zealand-Individual-Taxes-on-personal-income >

Inland Revenue ,Comparing New Zealand and Australia's income tax systems(2018)

<https://www.ird.govt.nz/international/business/ausnz/comp-inctax/comp-income-tax.html >

Joumard Isabelle , Pisu Mauro and Bloch Debra , Less Income Inequality and more Growth –

Are They Compatible? Part 3. Income Redistribution via Taxes and transfers Across OECD

Australia Taxation Law 11

Countries(2012)< https://www.oecd-ilibrary.org/docserver/5k9h296b1zjf-en.pdf?

expires=1537088458&id=id&accname=guest&checksum=338A4D3D97FA231AB0A38CF2441

2F32A>

Higgins Timothy, Income Contingent Loans: Theory, Practice and Prospects (Routledge

London, 2014)

Countries(2012)< https://www.oecd-ilibrary.org/docserver/5k9h296b1zjf-en.pdf?

expires=1537088458&id=id&accname=guest&checksum=338A4D3D97FA231AB0A38CF2441

2F32A>

Higgins Timothy, Income Contingent Loans: Theory, Practice and Prospects (Routledge

London, 2014)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.