Taxation Law Assignment: Australia, Masters Level, T3 2018

VerifiedAdded on 2023/01/19

|13

|1827

|72

Homework Assignment

AI Summary

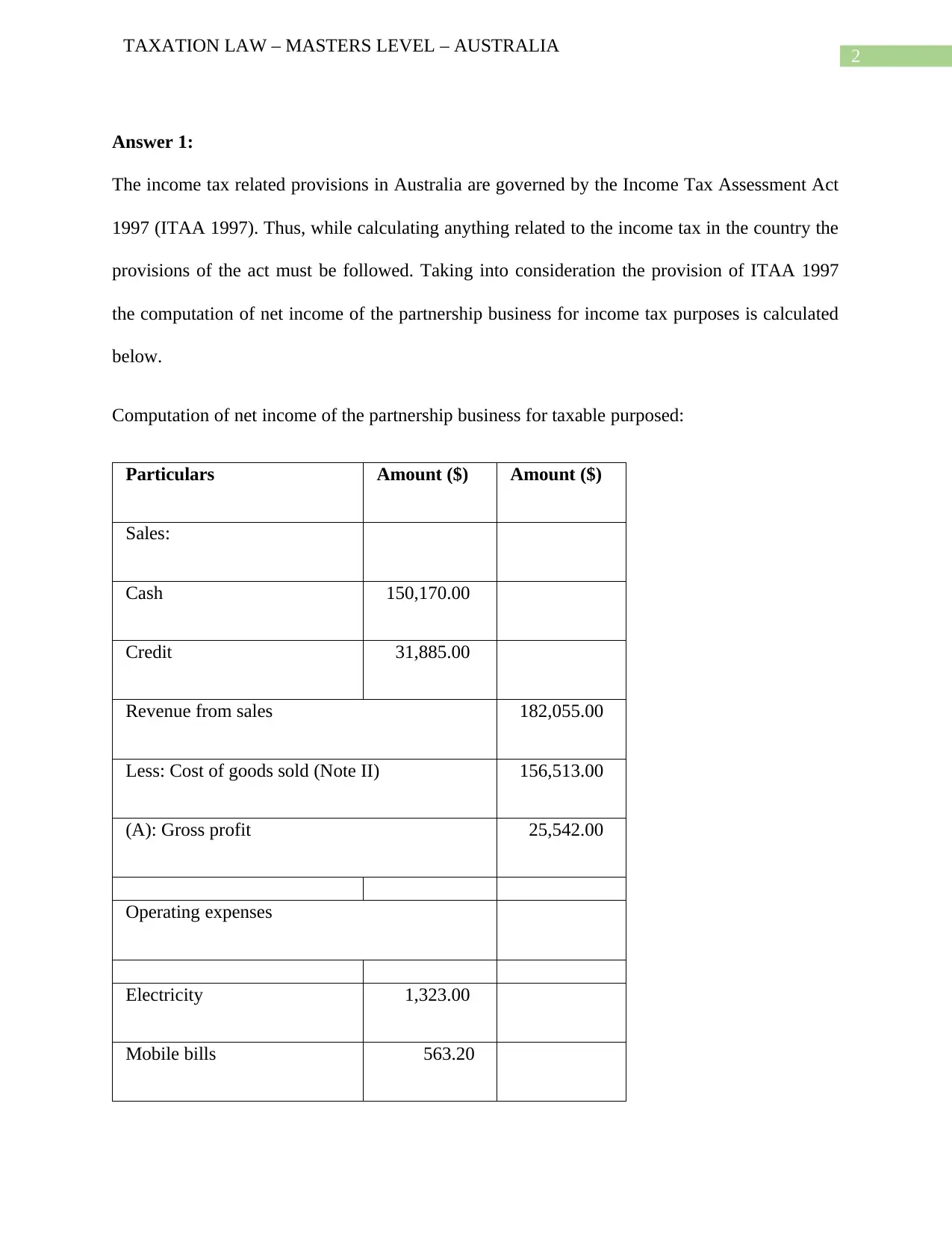

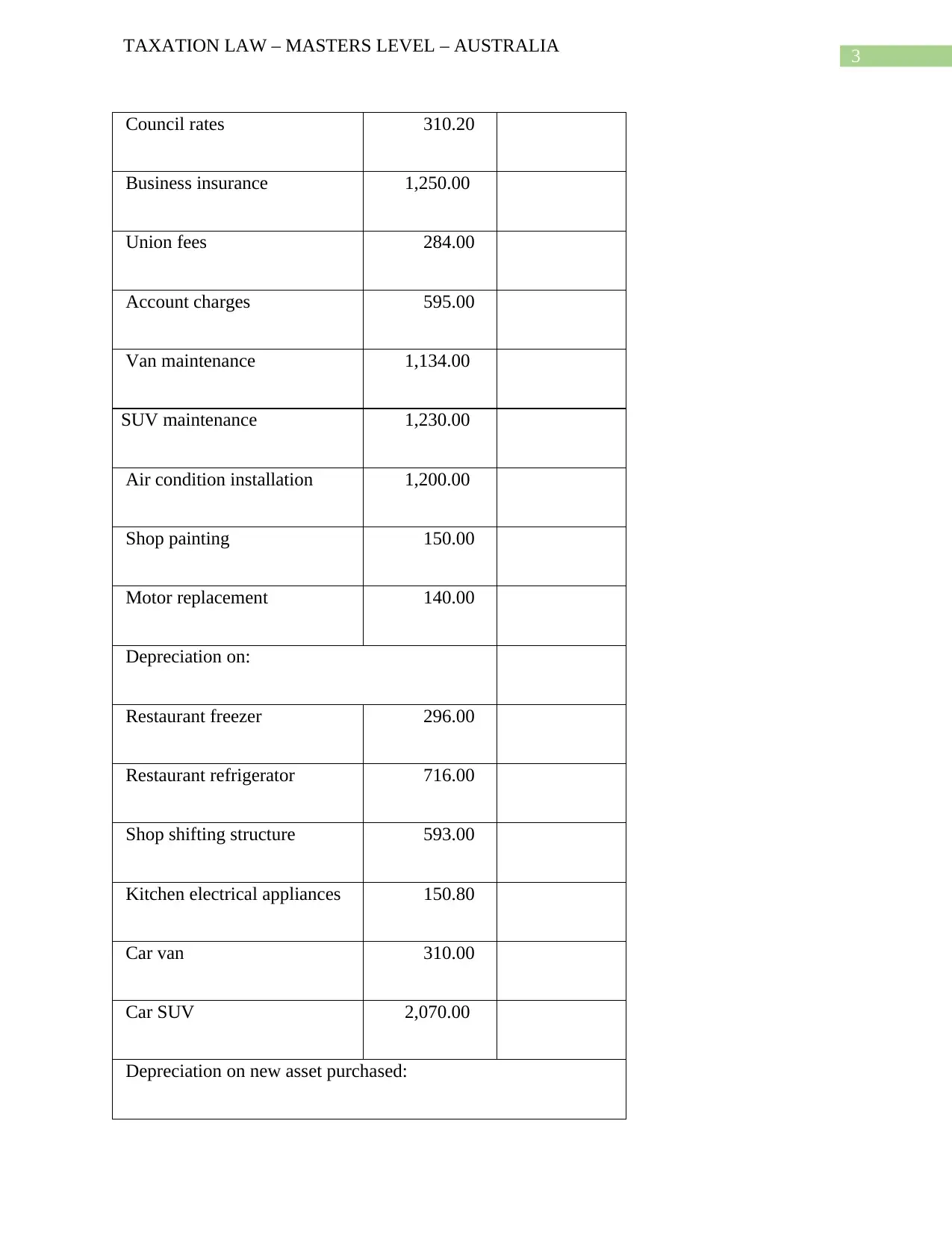

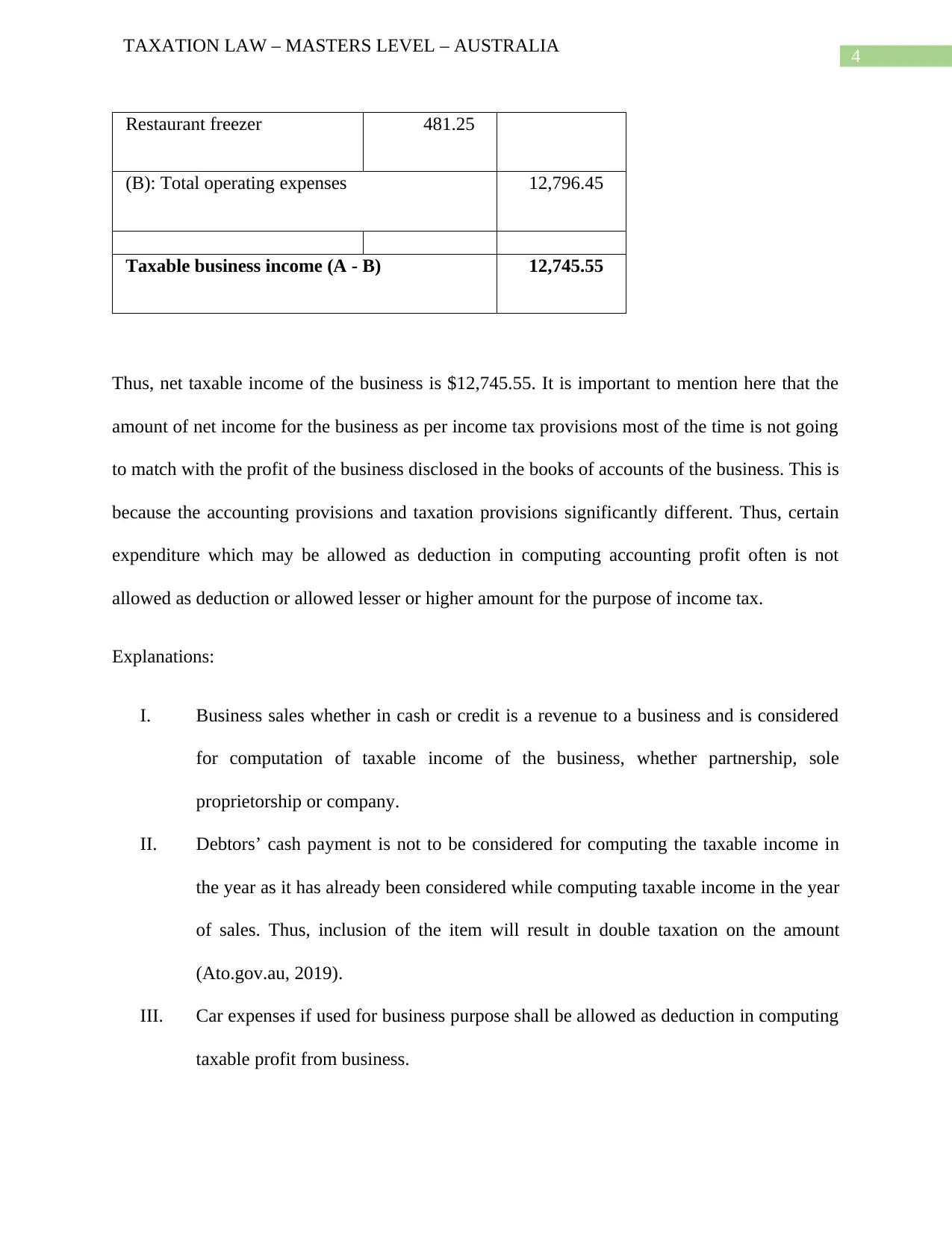

This assignment solution addresses two key areas of Australian taxation law at the Masters level. Answer 1 focuses on calculating the net taxable income of a partnership business, Brekkie and Lunch and OZ Bottle Shop, detailing the inclusion and exclusion of various revenue and expense items based on the Income Tax Assessment Act 1997 (ITAA 1997). It provides a comprehensive breakdown of sales, cost of goods sold, operating expenses, and depreciation, culminating in the determination of taxable business income. Answer 2 examines Fringe Benefits Tax (FBT), specifically addressing whether payments made by an employer for an employee's child's private school fees and concessional rent attract FBT. It explains the relevant provisions of the Fringe Benefits Tax Act 1986 and applies them to the case facts, concluding that the employer is liable for FBT on both benefits. The solution includes detailed calculations of fringe benefits and references to relevant Australian Taxation Office (ATO) and legislation resources.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.