Australia Taxation Law Assignment - Masters Level Course

VerifiedAdded on 2020/03/28

|11

|2609

|104

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment at the Masters level, focusing on Australian tax law. The assignment addresses five key issues: the tax implications of capital losses, the definition and application of Fringe Benefit Tax (FBT), the allocation of losses from rental properties between co-owners, principles of tax avoidance, and the determination of assessable income from the sale of timber. The solution analyzes relevant legislation, including the Income Tax Assessment Act 1997 and the Fringe Benefit Tax Assessment Act 1986, along with taxation rulings like TR 93/6 and TR 93/32, and relevant case law such as IRC v Duke of Westminster and McCauley v. The Federal Commissioner of Taxation. The analysis covers topics like capital gains and losses, interest-offset arrangements, co-ownership of rental properties, tax avoidance strategies, and the definition of a primary producer. The solution provides detailed explanations and conclusions for each issue, offering insights into the application of tax laws in specific scenarios.

Running head: TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Taxation Law - Masters Level - Australia

Student’s Name

Course Code

Taxation Law - Masters Level - Australia

Student’s Name

Course Code

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

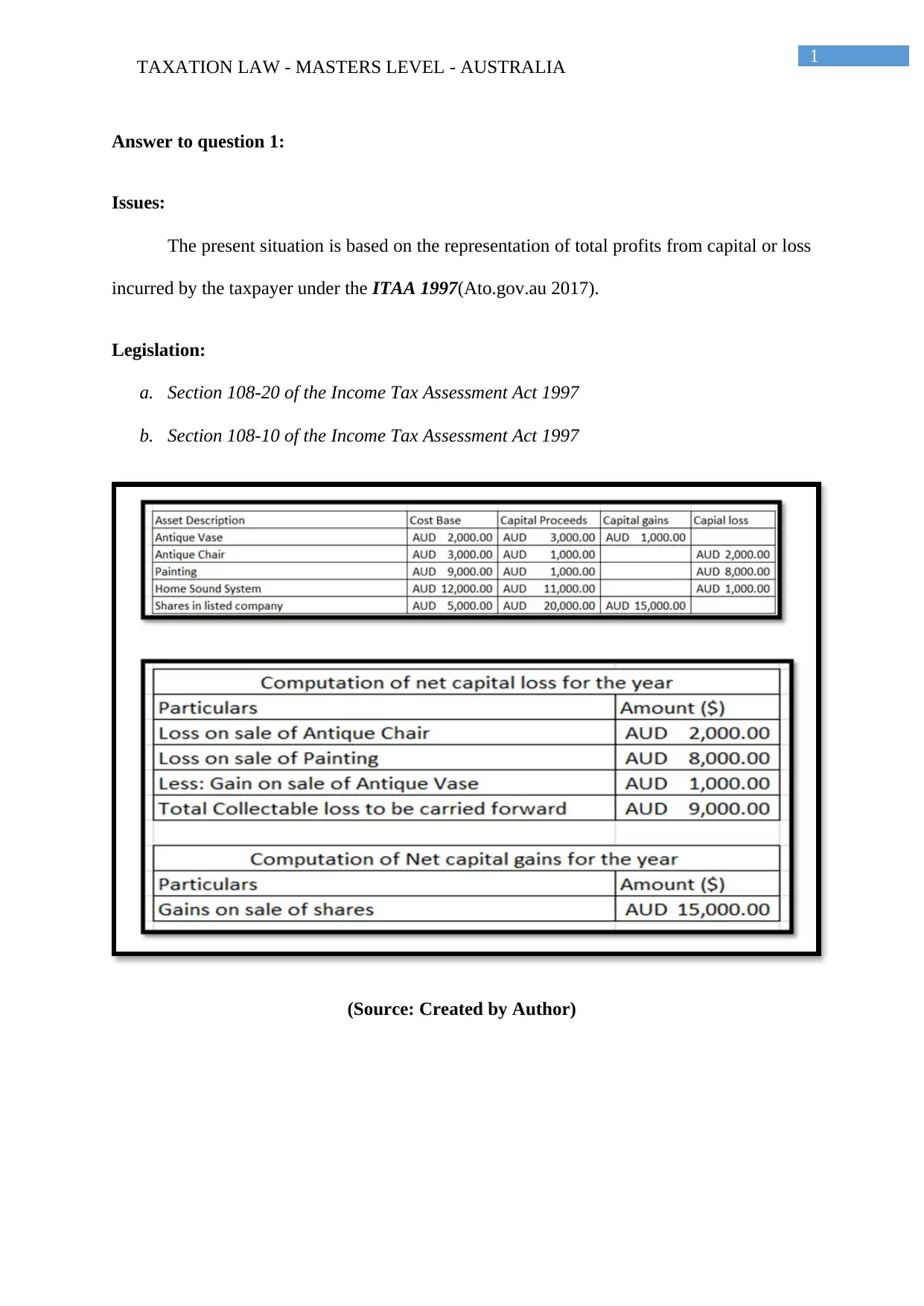

Answer to question 1:

Issues:

The present situation is based on the representation of total profits from capital or loss

incurred by the taxpayer under the ITAA 1997(Ato.gov.au 2017).

Legislation:

a. Section 108-20 of the Income Tax Assessment Act 1997

b. Section 108-10 of the Income Tax Assessment Act 1997

(Source: Created by Author)

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Answer to question 1:

Issues:

The present situation is based on the representation of total profits from capital or loss

incurred by the taxpayer under the ITAA 1997(Ato.gov.au 2017).

Legislation:

a. Section 108-20 of the Income Tax Assessment Act 1997

b. Section 108-10 of the Income Tax Assessment Act 1997

(Source: Created by Author)

2

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Applications:

a. Loss of $1,000 incurred by selling home theatre system are not permissible for set off

as no losses are acceptable on disposal of assets used for personal reasons section

108-20 of the ITAA 1997(Ato.gov.au 2017).

b. According to the section, 108-10 of the ITAA 1997 collective damages are not to be

considered against normal gains by selling shares and are balanced only against the

collective gains under section 108-10 of the ITAA 1997 (Ato.gov.au 2017).

c. Since Eric has earned gains on the disposal of regular assets and there is no present

ordinary capital or any type of appropriate discounts the net capital gain for Eric for

the current year stands $15,000.

Conclusion:

It can be concluded that, no loss will be permitted for balancing from the disposal of

assets, which is used for private purpose. Hence, Eric has made profits from the sale of

ordinary assets.

Answer to question 2:

Issue:

The current problem is related with the definition of Fringe Benefit Tax of the

taxpayer defined under the Fringe Benefit Act 1986 (Ato.gov.au 2017).

Legislation:

a. Taxation rulings of TR 93/6

b. Fringe Benefit Tax Assessment Act 1986

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Applications:

a. Loss of $1,000 incurred by selling home theatre system are not permissible for set off

as no losses are acceptable on disposal of assets used for personal reasons section

108-20 of the ITAA 1997(Ato.gov.au 2017).

b. According to the section, 108-10 of the ITAA 1997 collective damages are not to be

considered against normal gains by selling shares and are balanced only against the

collective gains under section 108-10 of the ITAA 1997 (Ato.gov.au 2017).

c. Since Eric has earned gains on the disposal of regular assets and there is no present

ordinary capital or any type of appropriate discounts the net capital gain for Eric for

the current year stands $15,000.

Conclusion:

It can be concluded that, no loss will be permitted for balancing from the disposal of

assets, which is used for private purpose. Hence, Eric has made profits from the sale of

ordinary assets.

Answer to question 2:

Issue:

The current problem is related with the definition of Fringe Benefit Tax of the

taxpayer defined under the Fringe Benefit Act 1986 (Ato.gov.au 2017).

Legislation:

a. Taxation rulings of TR 93/6

b. Fringe Benefit Tax Assessment Act 1986

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

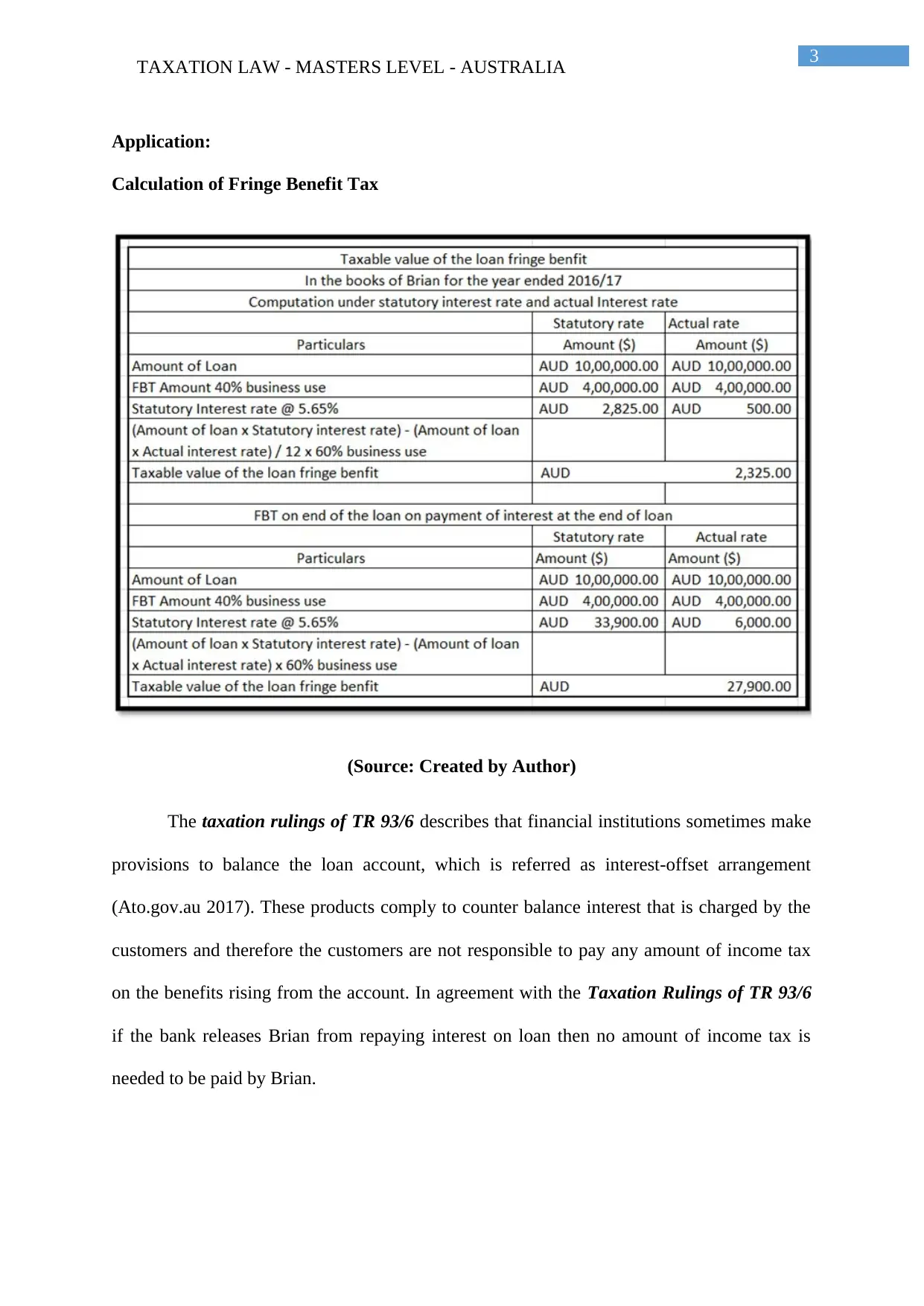

Application:

Calculation of Fringe Benefit Tax

(Source: Created by Author)

The taxation rulings of TR 93/6 describes that financial institutions sometimes make

provisions to balance the loan account, which is referred as interest-offset arrangement

(Ato.gov.au 2017). These products comply to counter balance interest that is charged by the

customers and therefore the customers are not responsible to pay any amount of income tax

on the benefits rising from the account. In agreement with the Taxation Rulings of TR 93/6

if the bank releases Brian from repaying interest on loan then no amount of income tax is

needed to be paid by Brian.

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Application:

Calculation of Fringe Benefit Tax

(Source: Created by Author)

The taxation rulings of TR 93/6 describes that financial institutions sometimes make

provisions to balance the loan account, which is referred as interest-offset arrangement

(Ato.gov.au 2017). These products comply to counter balance interest that is charged by the

customers and therefore the customers are not responsible to pay any amount of income tax

on the benefits rising from the account. In agreement with the Taxation Rulings of TR 93/6

if the bank releases Brian from repaying interest on loan then no amount of income tax is

needed to be paid by Brian.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Conclusion:

To conclude from the above application based on prescribed laws and regulations

there are no liabilities of tax payments. Given the fact for the release of Brian by financial

institutions, the acquired payment for interests liable to him is assisted by the counterbalance

interest is given by proper procedure.

Answer to question 3:

Issue:

The existing subject is related to the procuring a taxable position of loss suffered by

the Jack and Jill from the rental property.

Legislation:

a. Taxation rulings of TR 93/32

b. F.C. of T. v McDonald (1987) 18 ATR 957

c. Section 51 of the ITAA 1997

Application:

The taxation ruling of TR 93/32 is described as the clarification of splitting up net

income or loss produced from the rental property between the shareholders of the property

(Ato.gov.au 2017). The ruling is concerned with the assessment of taxable position of the Co-

owners whose actions are irrelevant for running a business. The current situation of Jack and

his wife Jill is apprehensive to the estimation of taxable situation of the rental property. Both

Jack and Jill enter into the scenario to buy a rental property as a joint tenant with Jack being

authorised to 10% of the profit from the property and Jill is eligible for 90% of profit from

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Conclusion:

To conclude from the above application based on prescribed laws and regulations

there are no liabilities of tax payments. Given the fact for the release of Brian by financial

institutions, the acquired payment for interests liable to him is assisted by the counterbalance

interest is given by proper procedure.

Answer to question 3:

Issue:

The existing subject is related to the procuring a taxable position of loss suffered by

the Jack and Jill from the rental property.

Legislation:

a. Taxation rulings of TR 93/32

b. F.C. of T. v McDonald (1987) 18 ATR 957

c. Section 51 of the ITAA 1997

Application:

The taxation ruling of TR 93/32 is described as the clarification of splitting up net

income or loss produced from the rental property between the shareholders of the property

(Ato.gov.au 2017). The ruling is concerned with the assessment of taxable position of the Co-

owners whose actions are irrelevant for running a business. The current situation of Jack and

his wife Jill is apprehensive to the estimation of taxable situation of the rental property. Both

Jack and Jill enter into the scenario to buy a rental property as a joint tenant with Jack being

authorised to 10% of the profit from the property and Jill is eligible for 90% of profit from

5

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

the property. However, the contract between Jack and Jill described that on the event of

incurring loss from the rental property, Jack shall be responsible to pay 100% of such loss.

According to the Taxation rulings, TR 92/32 Co-ownership of rental property

amounts to a partnership for income tax reasons but it is not a partnership in general law

except the ownership determines running a business (Ato.gov.au 2017). In cases where co-

ownership is in the form of a partnership for income tax purposes only, the profit or loss

coming from the rental property is attributed to the co-ownership of the rental property and

from the distribution of losses or profits made in the partnership. As it is clear from the

existing situation of Jack and Jill the co-ownership of rental property between them is a

partnership to tackle income tax but it cannot be regarded as the partnership in general law.

The taxation rulings of TR 92/32 establishes that co-owners of the rental property are

usually not the partners, when it comes to general law and a partnership agreement either in

the form of oral or written does not affect the sharing of income or loss generated from the

property (Ato.gov.au 2017). Hence, Co-owners of the rental property Jack and Jill will

normally hold the property as the joint tenants or tenants in common. These tenancies are

further classified in the co-owners interest.

As stated in the case of F.C. of T. v McDonald (1987) 18 ATR 957 where the

taxpayer and his wife legally and constructively owned two strata title units as joint tenants

(Ato.gov.au 2017). The agreement between them established that the net profits derived from

the rental property would be distributed as 25 percent to McDonald and 75 percent to Mrs

McDonald. Mr McDonald would incur the whole amount of loss. The question arises that

whether the operating loss on the properties was completely born by the taxpayer or by the

taxpayer and his spouse divided equally. There was no such concern regarding the deduction

of loss amount. It was mentioned that there was no partnership in general law and the only

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

the property. However, the contract between Jack and Jill described that on the event of

incurring loss from the rental property, Jack shall be responsible to pay 100% of such loss.

According to the Taxation rulings, TR 92/32 Co-ownership of rental property

amounts to a partnership for income tax reasons but it is not a partnership in general law

except the ownership determines running a business (Ato.gov.au 2017). In cases where co-

ownership is in the form of a partnership for income tax purposes only, the profit or loss

coming from the rental property is attributed to the co-ownership of the rental property and

from the distribution of losses or profits made in the partnership. As it is clear from the

existing situation of Jack and Jill the co-ownership of rental property between them is a

partnership to tackle income tax but it cannot be regarded as the partnership in general law.

The taxation rulings of TR 92/32 establishes that co-owners of the rental property are

usually not the partners, when it comes to general law and a partnership agreement either in

the form of oral or written does not affect the sharing of income or loss generated from the

property (Ato.gov.au 2017). Hence, Co-owners of the rental property Jack and Jill will

normally hold the property as the joint tenants or tenants in common. These tenancies are

further classified in the co-owners interest.

As stated in the case of F.C. of T. v McDonald (1987) 18 ATR 957 where the

taxpayer and his wife legally and constructively owned two strata title units as joint tenants

(Ato.gov.au 2017). The agreement between them established that the net profits derived from

the rental property would be distributed as 25 percent to McDonald and 75 percent to Mrs

McDonald. Mr McDonald would incur the whole amount of loss. The question arises that

whether the operating loss on the properties was completely born by the taxpayer or by the

taxpayer and his spouse divided equally. There was no such concern regarding the deduction

of loss amount. It was mentioned that there was no partnership in general law and the only

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

noteworthy relationship between the parties was that of the co-ownership. Since the parties

were joint owners in terms of law and justice, the loss suffered for letting the premises should

be shared equally with details that the respondents were also entitled for a deduction

amounting to half of the loss incurred.

In the current case of Jack and Jill, it can be established that the loss should be equally

specified for the purpose of taxation and does not allow a deduction simply by virtue of the

agreement. As the matter of fact, Jack was involved in two significant losses. At the first, he

gave significant portion of his income entitlement and he indemnified his wife Jill against any

type of loss from the investment. The statement of loss compensation was voluntarily made

by Jack and gave shape to a domestic arrangement, where he sought after to advance his

wife’s finance, as section 51 does not permit a deduction simply by virtue of the agreement

(Ato.gov.au 2017).

On the contrary, if Jack and Jill decide to sell the property, the cost base and the

reduced cost based of the property should be included in the amount, which will be paid

together by them along with the incidental cost prevalent at the time of acquisition. Given the

fact, the Jack and Jill are the co-owners of the property, the capital gains or loss will be

accounted as per the ownership interest in the property.

Conclusion:

For drawing conclusion, it is a known fact that there was no kind of partnership

defined under the general law and the loss suffered should be shared equally with the

deduction of half of the loss suffered by Jack and Jill.

Answer to question 4:

IRC v Duke of Westminster [1936] AC 1 was frequently mentioned in the event of

tax avoidance (Ato.gov.au 2017). The case stated a principle that each man is allowed to

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

noteworthy relationship between the parties was that of the co-ownership. Since the parties

were joint owners in terms of law and justice, the loss suffered for letting the premises should

be shared equally with details that the respondents were also entitled for a deduction

amounting to half of the loss incurred.

In the current case of Jack and Jill, it can be established that the loss should be equally

specified for the purpose of taxation and does not allow a deduction simply by virtue of the

agreement. As the matter of fact, Jack was involved in two significant losses. At the first, he

gave significant portion of his income entitlement and he indemnified his wife Jill against any

type of loss from the investment. The statement of loss compensation was voluntarily made

by Jack and gave shape to a domestic arrangement, where he sought after to advance his

wife’s finance, as section 51 does not permit a deduction simply by virtue of the agreement

(Ato.gov.au 2017).

On the contrary, if Jack and Jill decide to sell the property, the cost base and the

reduced cost based of the property should be included in the amount, which will be paid

together by them along with the incidental cost prevalent at the time of acquisition. Given the

fact, the Jack and Jill are the co-owners of the property, the capital gains or loss will be

accounted as per the ownership interest in the property.

Conclusion:

For drawing conclusion, it is a known fact that there was no kind of partnership

defined under the general law and the loss suffered should be shared equally with the

deduction of half of the loss suffered by Jack and Jill.

Answer to question 4:

IRC v Duke of Westminster [1936] AC 1 was frequently mentioned in the event of

tax avoidance (Ato.gov.au 2017). The case stated a principle that each man is allowed to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

order his affairs so that the tax assigned in the fitting Act, will be less. Although it can be

established that this ruling was very effective for others for avoiding tax by lawfully

establishing complex structures, the subsequent cases has been weakened by the courts when

consideration of overall impact is done. Citing an example of the court in the later stages,

more approach that is restrictive was adopted under the WT Ramsay v. IRC principle, which

stated that if a transaction has pre-arranged artificial steps that served no form of commercial

purpose other than saving tax, the appropriate approach was to impose tax to the extent of

entire transaction.

In the current scenario, this principle in Australia, states that if an individual succeeds

in ordering them with the aim of securing a specific result, then, it does not matter how

unappreciative the commissioners of Inland Revenue or the fellow taxpayer might be of their

ingenuity, they cannot be forced to pay any increased amount of tax (Russell 2016). As point

was made by the later decisions, that it permitted the individuals and corporations to

construct the financial contracts with the aim of dropping the tax liability unless the structures

are within the framework of law.

Answer to question 5:

Issues:

The current matter is based on the asserting whether the revenue coming from the sale

of timber will be considered as assessable income for the taxpayer as primary producer or not

under subsection 6 (1) of the Income Tax Assessment Act 1936 (Ato.gov.au 2017).

Legislations:

a. McCauley v. The Federal Commissioner of Taxation (1944) 69 CLR 235

b. Subsection 6 (1) of the Income Tax Assessment Act 1936

c. Subsection 36(1)

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

order his affairs so that the tax assigned in the fitting Act, will be less. Although it can be

established that this ruling was very effective for others for avoiding tax by lawfully

establishing complex structures, the subsequent cases has been weakened by the courts when

consideration of overall impact is done. Citing an example of the court in the later stages,

more approach that is restrictive was adopted under the WT Ramsay v. IRC principle, which

stated that if a transaction has pre-arranged artificial steps that served no form of commercial

purpose other than saving tax, the appropriate approach was to impose tax to the extent of

entire transaction.

In the current scenario, this principle in Australia, states that if an individual succeeds

in ordering them with the aim of securing a specific result, then, it does not matter how

unappreciative the commissioners of Inland Revenue or the fellow taxpayer might be of their

ingenuity, they cannot be forced to pay any increased amount of tax (Russell 2016). As point

was made by the later decisions, that it permitted the individuals and corporations to

construct the financial contracts with the aim of dropping the tax liability unless the structures

are within the framework of law.

Answer to question 5:

Issues:

The current matter is based on the asserting whether the revenue coming from the sale

of timber will be considered as assessable income for the taxpayer as primary producer or not

under subsection 6 (1) of the Income Tax Assessment Act 1936 (Ato.gov.au 2017).

Legislations:

a. McCauley v. The Federal Commissioner of Taxation (1944) 69 CLR 235

b. Subsection 6 (1) of the Income Tax Assessment Act 1936

c. Subsection 36(1)

8

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

d. section 26 (f)

Application:

In the light of current events, it is discovered that Bill owns a large piece of land on

which there are several pine trees. Bill initially intended to use the land for grazing sheep and

wanted to have it cleared. Bill came in agreement with a logging company, which is ready to

pay him $1000 for every 100 meters of timber, which the logging company can harness from

his land. The taxation rulings of TR 95/6 talk about the consequences of income tax arising

from the activities of primary production and forestry (Ato.gov.au 2017).

The ruling states that the relevance of receipts derived from the sale of timber

constitute assessable income irrespective of the fact that taxpayer participated in the activities

of forestry industry. The ruling is usually applicable on the person who practice forest

operations and on people who are not associated with disposal of timber. The ruling states the

consequences of tax on a person, which enters into the business of forest operations. As

stated under subsection 6 (1) of the Income Tax Assessment Act 1936 a taxpayer who is

involved in the forest activities is termed as the primary producer liable for income tax if the

forest activities forms the part of a business (Ato.gov.au 2017).

According to the subsection 6 (1) of the Income Tax Assessment Act 1936 primary

production is usually defined as the planting or tending of tress in a plantation that is made

for felling of tress in a forest (Ato.gov.au 2017). As it can be observed from the case study,

Bill will be considered as the primary producer since he was involved in the activities of

primary production under subsection 6 (1) of the Income Tax Assessment Act 1936 for

felling of trees in a plantation owned by him (Ato.gov.au 2017). Moreover, the forest

activities include felling of trees in a plantation or forest even though the concerned taxpayer

has not planted or tended the trees.

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

d. section 26 (f)

Application:

In the light of current events, it is discovered that Bill owns a large piece of land on

which there are several pine trees. Bill initially intended to use the land for grazing sheep and

wanted to have it cleared. Bill came in agreement with a logging company, which is ready to

pay him $1000 for every 100 meters of timber, which the logging company can harness from

his land. The taxation rulings of TR 95/6 talk about the consequences of income tax arising

from the activities of primary production and forestry (Ato.gov.au 2017).

The ruling states that the relevance of receipts derived from the sale of timber

constitute assessable income irrespective of the fact that taxpayer participated in the activities

of forestry industry. The ruling is usually applicable on the person who practice forest

operations and on people who are not associated with disposal of timber. The ruling states the

consequences of tax on a person, which enters into the business of forest operations. As

stated under subsection 6 (1) of the Income Tax Assessment Act 1936 a taxpayer who is

involved in the forest activities is termed as the primary producer liable for income tax if the

forest activities forms the part of a business (Ato.gov.au 2017).

According to the subsection 6 (1) of the Income Tax Assessment Act 1936 primary

production is usually defined as the planting or tending of tress in a plantation that is made

for felling of tress in a forest (Ato.gov.au 2017). As it can be observed from the case study,

Bill will be considered as the primary producer since he was involved in the activities of

primary production under subsection 6 (1) of the Income Tax Assessment Act 1936 for

felling of trees in a plantation owned by him (Ato.gov.au 2017). Moreover, the forest

activities include felling of trees in a plantation or forest even though the concerned taxpayer

has not planted or tended the trees.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Owning a large chunk of land, Bill has not planted the trees but the total amount of

receipts, which was derived by Bill from the sale of felled timber, makes an assessable

income of the taxpayer in the respective year, during which the sale of timber was done

(Peiros and Smyth 2017). The disposal of existing timber where the taxpayer sold derived

from the trees, which were not necessarily planted by the taxpayer and tended for the purpose

of sale, becomes the part of assessable income. Even though the sales become part of assets

completely or partially of a business, the value of trees will be considered as assessable

income of the taxpayer under subsection 36(1).

On the contrary, if the taxpayer were only paid a lump sum of $50,000 by giving the

rights to remove the timber to the logging company, such receipt of money would constitute

“Royalties”. According to the section 26 (f) receipt of “royalties” by the taxpayer on granting

the right to cut the timber from the land acquired by the taxpayer will establish assessable

income of the assesses during the year of income in which the timber was felled (Ato.gov.au

2017). The royalties received by Bill in the current scenario gives the company right to sell or

remove tress on the land owned by the taxpayer. Under these circumstances, no business

involving forest operations is being done by Bill, given that the taxpayer has not planted the

trees or tended for the purpose of sale. As held in McCauley v. The Federal Commissioner

of Taxation (1944) 69 CLR 235 payments received by the owner for the right to remove or

cut down trees is based on the amount of timber removed under the authority to do so

(Ato.gov.au 2017). The amount received by Bill in the form of royalty constitutes assessable

income under section 26 (f).

Conclusion:

Taking reference of subsection, 36(1) it can be concluded that sale of felled timber

will be considered as assessable income and imposes tax liability on the sum received for

selling the timber.

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

Owning a large chunk of land, Bill has not planted the trees but the total amount of

receipts, which was derived by Bill from the sale of felled timber, makes an assessable

income of the taxpayer in the respective year, during which the sale of timber was done

(Peiros and Smyth 2017). The disposal of existing timber where the taxpayer sold derived

from the trees, which were not necessarily planted by the taxpayer and tended for the purpose

of sale, becomes the part of assessable income. Even though the sales become part of assets

completely or partially of a business, the value of trees will be considered as assessable

income of the taxpayer under subsection 36(1).

On the contrary, if the taxpayer were only paid a lump sum of $50,000 by giving the

rights to remove the timber to the logging company, such receipt of money would constitute

“Royalties”. According to the section 26 (f) receipt of “royalties” by the taxpayer on granting

the right to cut the timber from the land acquired by the taxpayer will establish assessable

income of the assesses during the year of income in which the timber was felled (Ato.gov.au

2017). The royalties received by Bill in the current scenario gives the company right to sell or

remove tress on the land owned by the taxpayer. Under these circumstances, no business

involving forest operations is being done by Bill, given that the taxpayer has not planted the

trees or tended for the purpose of sale. As held in McCauley v. The Federal Commissioner

of Taxation (1944) 69 CLR 235 payments received by the owner for the right to remove or

cut down trees is based on the amount of timber removed under the authority to do so

(Ato.gov.au 2017). The amount received by Bill in the form of royalty constitutes assessable

income under section 26 (f).

Conclusion:

Taking reference of subsection, 36(1) it can be concluded that sale of felled timber

will be considered as assessable income and imposes tax liability on the sum received for

selling the timber.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

References

Ato.gov.au 2017. Home page. [online] Ato.gov.au. Available at: http://www.ato.gov.au

[Accessed 20 Sep. 2017].

Peiros, K., and Smyth, C. 2017. Successful succession: Tax treatment of executor's

commission. Taxation in Australia, 51(7), 394.

Russell, T. 2016. Trust beneficiaries and exemptions from CGT: Reflections on the Oswal

litigation. Taxation in Australia, 51(6), 296.

Taylor, G., and Richardson, G. 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing

and Taxation, 22(1), 12-25.

Woellner, R. H., Barkoczy, S., Murphy, S., Evans, C., and Pinto, D. 2016. Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

TAXATION LAW - MASTERS LEVEL - AUSTRALIA

References

Ato.gov.au 2017. Home page. [online] Ato.gov.au. Available at: http://www.ato.gov.au

[Accessed 20 Sep. 2017].

Peiros, K., and Smyth, C. 2017. Successful succession: Tax treatment of executor's

commission. Taxation in Australia, 51(7), 394.

Russell, T. 2016. Trust beneficiaries and exemptions from CGT: Reflections on the Oswal

litigation. Taxation in Australia, 51(6), 296.

Taylor, G., and Richardson, G. 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing

and Taxation, 22(1), 12-25.

Woellner, R. H., Barkoczy, S., Murphy, S., Evans, C., and Pinto, D. 2016. Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

1 out of 11

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.