Taxation Law of Australia Individual Assignment LAWS20060

VerifiedAdded on 2023/01/18

|12

|3720

|85

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment, addressing various aspects of Australian taxation. The assignment covers key topics such as depreciating assets, tax offsets, and marginal tax rates. It delves into specific sections of the Income Tax Assessment Act 1997 (ITAA 1997), including Division 17, s. 118-52, s. 104-15, and s. 4-10(3). The solution analyzes relevant case law, including FC of T v Day 2008 ATC 20-064, focusing on the deductibility of legal expenses. Furthermore, the assignment explores consumption taxes and their impact on consumer behavior. The solution provides practical examples of general deductions under s. 8-1 ITAA 1997, and discusses the tax treatment of various expenses, including loan interest, mobile phone charges, childcare costs, stolen business items, and election-related expenditures. The assignment also analyzes CGT events, including the granting of leases, options, and the sale of shares, and determines the applicability of the discount method. Finally, it examines the taxability of prize money and the difference between allowances and reimbursements for employee business expenses.

TAXATION LAW

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

a) TR 2018/4 deals with the depreciating assets effective life with regards to income tax1.

b) The relevant division dealing with tax offsets is Division 17 ITAA 1997.

c) Resident taxpayer would attract a top tax rate to the extent of 45% for the tax year

2018/2019.

d) An instance of an asset which is exempt from capital gains tax is car which has been

indicated as per s. 118-52.

e) CGT event B1 s104-15 deals with the tax treatment of asset enjoyment without

possessing the legal ownership of the asset.

f) The underlying formula that has been outlined in s. 4-10(3) pertains to the income tax

liability computation. It highlights that that the first step in this regards is to multiple the

tax rate (as per applicable tax slabs) with the taxable income after requisite deduction.

However, it is possible that the actual tax liability is lower than the above amount as tax

offsets would be deducted3.

g) The FC of T v Day 2008 ATC 20-064 is a case whose significance pertains to the

deduction that may be availed by the taxpayer under s. 8-1.The key legal issue in the

given case was whether the legal expenses incurred by the taxpayer would provide

deduction or not. The Tax Commissioner denied the same but the High Court allowed the

same. The key principle indicated was that it is essential to consider whether the legal

expenses incurred are with regards to assessable income derivation. This was true in the

given case as the legal services were hired by a custom officer so as to defend against

charges levied in regards to professional conduct. The charges could impact the

professional career of the taxpayer and thereby the expenses were incurred in order to

ensure that assessable income remains intact4.

h) The tax rate which would be levied on the last dollar of the taxable income for the

taxpayer would be referred to as marginal tax. Most countries tend to have a progressive

income tax system whereby the tax slabs tend to progressively increase and thereby a

1ATO, Taxable Ruling TR 2018/4, https://www.ato.gov.au/law/view/document?DocID=TXR%2FTR20184%2FNAT

%2FATO%2F00001

2ATO, Income Tax Assessment Act 1997 – SECT 118.5, http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s118.5.html

3 Austlii, INCOME TAX ASSESSMENT ACT 1997 - SECT 4.10 How to work out how much income tax you must pay, <

http://www6.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s4.10.html>

4 High Court of Australia, COMMISSIONER OF TAXATION v SHANE DAY <

http://www.hcourt.gov.au/assets/publications/judgment-summaries/2008/hca53-2008-11-12.pdf>

2

a) TR 2018/4 deals with the depreciating assets effective life with regards to income tax1.

b) The relevant division dealing with tax offsets is Division 17 ITAA 1997.

c) Resident taxpayer would attract a top tax rate to the extent of 45% for the tax year

2018/2019.

d) An instance of an asset which is exempt from capital gains tax is car which has been

indicated as per s. 118-52.

e) CGT event B1 s104-15 deals with the tax treatment of asset enjoyment without

possessing the legal ownership of the asset.

f) The underlying formula that has been outlined in s. 4-10(3) pertains to the income tax

liability computation. It highlights that that the first step in this regards is to multiple the

tax rate (as per applicable tax slabs) with the taxable income after requisite deduction.

However, it is possible that the actual tax liability is lower than the above amount as tax

offsets would be deducted3.

g) The FC of T v Day 2008 ATC 20-064 is a case whose significance pertains to the

deduction that may be availed by the taxpayer under s. 8-1.The key legal issue in the

given case was whether the legal expenses incurred by the taxpayer would provide

deduction or not. The Tax Commissioner denied the same but the High Court allowed the

same. The key principle indicated was that it is essential to consider whether the legal

expenses incurred are with regards to assessable income derivation. This was true in the

given case as the legal services were hired by a custom officer so as to defend against

charges levied in regards to professional conduct. The charges could impact the

professional career of the taxpayer and thereby the expenses were incurred in order to

ensure that assessable income remains intact4.

h) The tax rate which would be levied on the last dollar of the taxable income for the

taxpayer would be referred to as marginal tax. Most countries tend to have a progressive

income tax system whereby the tax slabs tend to progressively increase and thereby a

1ATO, Taxable Ruling TR 2018/4, https://www.ato.gov.au/law/view/document?DocID=TXR%2FTR20184%2FNAT

%2FATO%2F00001

2ATO, Income Tax Assessment Act 1997 – SECT 118.5, http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s118.5.html

3 Austlii, INCOME TAX ASSESSMENT ACT 1997 - SECT 4.10 How to work out how much income tax you must pay, <

http://www6.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s4.10.html>

4 High Court of Australia, COMMISSIONER OF TAXATION v SHANE DAY <

http://www.hcourt.gov.au/assets/publications/judgment-summaries/2008/hca53-2008-11-12.pdf>

2

higher marginal tax may be applicable for income above a certain threshold. The average

rate of taxation which is levied on each of each dollar of taxable income would refer to

the average tax rate. For enhanced clarity in this regards, the working using actual

numerical values is exhibited below.

Let the net taxable income for the resident taxpayer be $ 110,000 for 2018-2019. Any taxable

income lying in the bracket of $ 90,000- $180,000 attracts a marginal tax rate of 37% which

would be the marginal tax rate for the taxpayer. The total tax liability in accordance with the

personal income tax slabs can be computed as shown below.

Income tax liability = 20797 + 0.37*(110,000-90,000) = $28,197

Average tax rate = ($28197,/ $110,000) = 25.63%

i) The consumption tax is levied by the government with the underlying intention to bring

about a change in the consumption pattern of consumers. This is required since there are

certain products which are harmful for the health of people and lead to the negative

externality of higher strain on public health infrastructure and lower productivity of

people. This negative externality is not built in the prices owing to which the

consumption of this products is in excess to the socially efficient level. For correcting this

mismatch, consumption tax is levied so that higher cost would act as a deterrent for

consumption and thereby reduce consumption. Some of the examples of these taxes

levied by various nations in the developed world are sugar tax, soda tax and fat tax. The

name itself suggests the underlying items on which these taxes would be applicable.

Ideally, the government should use the revenue collected from this tax to subsidise the

purchase of healthy substitutes which would bring about real change but this is seldom

done.

Question 2

(a) Outgoings which are pivotal for assessable income generation by the taxpayer will be

claimed as general deduction under s. 8-1 ITAA 1997. Further, the deduction will not be

claimed for the outgoings under ss. 8-1(2) ITAA 1997 which have realised for the

generation of non-assessable income, private or capital in nature. Brett has taken loan so

that he can pay employee wages which refers that he has realised the loan payment in

regards to generation of assessable income as non payment of salary would potential shut

3

rate of taxation which is levied on each of each dollar of taxable income would refer to

the average tax rate. For enhanced clarity in this regards, the working using actual

numerical values is exhibited below.

Let the net taxable income for the resident taxpayer be $ 110,000 for 2018-2019. Any taxable

income lying in the bracket of $ 90,000- $180,000 attracts a marginal tax rate of 37% which

would be the marginal tax rate for the taxpayer. The total tax liability in accordance with the

personal income tax slabs can be computed as shown below.

Income tax liability = 20797 + 0.37*(110,000-90,000) = $28,197

Average tax rate = ($28197,/ $110,000) = 25.63%

i) The consumption tax is levied by the government with the underlying intention to bring

about a change in the consumption pattern of consumers. This is required since there are

certain products which are harmful for the health of people and lead to the negative

externality of higher strain on public health infrastructure and lower productivity of

people. This negative externality is not built in the prices owing to which the

consumption of this products is in excess to the socially efficient level. For correcting this

mismatch, consumption tax is levied so that higher cost would act as a deterrent for

consumption and thereby reduce consumption. Some of the examples of these taxes

levied by various nations in the developed world are sugar tax, soda tax and fat tax. The

name itself suggests the underlying items on which these taxes would be applicable.

Ideally, the government should use the revenue collected from this tax to subsidise the

purchase of healthy substitutes which would bring about real change but this is seldom

done.

Question 2

(a) Outgoings which are pivotal for assessable income generation by the taxpayer will be

claimed as general deduction under s. 8-1 ITAA 1997. Further, the deduction will not be

claimed for the outgoings under ss. 8-1(2) ITAA 1997 which have realised for the

generation of non-assessable income, private or capital in nature. Brett has taken loan so

that he can pay employee wages which refers that he has realised the loan payment in

regards to generation of assessable income as non payment of salary would potential shut

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

down business. Thereby, the interest payment against loan will be deducted under the s.

8-1 ITAA 19975.

(b) As discussed above, any expenses which are personal expense of the taxpayer will not be

deductible. Further, if a portion of the expenses has been realised for production of the

assessable income then that amount will be available for deduction. In given case, Julie

has an expense of $500 on her mobile phone charge which might be considered a private

expense. However, the use is not entirely private as 60% of the total calls are work

related. This indicates that only 60% of $500 will be taken for deduction. Thus, the

deduction is available for $300 only.

(c) As per TR 95/9, the expenses in the form of child care will not be considered for

deduction because it belongs to the category of private expenses of the taxpayer. The

ruling of Lodge v. FC of T6case also supports this observation. In given scenario, Sally

has paid $1200 to babysitter for taking care of her child. Thereby, this private expense of

Sally will not be considered for deduction despite this payment being necessary for her to

attend work.

(d) Losses which are borne by business in the form of stolen items are business related

expenses which take place in normal course of business and hene considered to be

deductible under general deduction as clarified in the verdict of Charles Moore & Co

(WA) Pty Ltd v. Federal Commissioner of Taxation7 case. Thus, the loss in terms of stolen

goods of monetary worth $20,000 will be deductible as the goods were part of the

business of Jerry and would have derived assessable income for him.

(e) The expenditure which is related to assessable income derivation but are of capital in

nature would not be considered for deduction under ss. 8-1(2) ITAA 1997. The

expenditure of $5000 for contesting the local election belong to capital expenditure as

they donot relate to discharging of duties of elected representative and thus, no deduction

5 Austlii, Income Tax Assessment Act 1997- SECT 8.1, http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s8.1.html

6 Lodge v. FC of T (1972) 128 CLR 171

7 Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

4

8-1 ITAA 19975.

(b) As discussed above, any expenses which are personal expense of the taxpayer will not be

deductible. Further, if a portion of the expenses has been realised for production of the

assessable income then that amount will be available for deduction. In given case, Julie

has an expense of $500 on her mobile phone charge which might be considered a private

expense. However, the use is not entirely private as 60% of the total calls are work

related. This indicates that only 60% of $500 will be taken for deduction. Thus, the

deduction is available for $300 only.

(c) As per TR 95/9, the expenses in the form of child care will not be considered for

deduction because it belongs to the category of private expenses of the taxpayer. The

ruling of Lodge v. FC of T6case also supports this observation. In given scenario, Sally

has paid $1200 to babysitter for taking care of her child. Thereby, this private expense of

Sally will not be considered for deduction despite this payment being necessary for her to

attend work.

(d) Losses which are borne by business in the form of stolen items are business related

expenses which take place in normal course of business and hene considered to be

deductible under general deduction as clarified in the verdict of Charles Moore & Co

(WA) Pty Ltd v. Federal Commissioner of Taxation7 case. Thus, the loss in terms of stolen

goods of monetary worth $20,000 will be deductible as the goods were part of the

business of Jerry and would have derived assessable income for him.

(e) The expenditure which is related to assessable income derivation but are of capital in

nature would not be considered for deduction under ss. 8-1(2) ITAA 1997. The

expenditure of $5000 for contesting the local election belong to capital expenditure as

they donot relate to discharging of duties of elected representative and thus, no deduction

5 Austlii, Income Tax Assessment Act 1997- SECT 8.1, http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s8.1.html

6 Lodge v. FC of T (1972) 128 CLR 171

7 Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will be applied under s.8-1 ITAA 1997 despite the fact that the amount has realised in

relation to the assessable income generation. Further, s. 40-664 ITAA 1997 would not be

held as the expenditure is not business linked8.

Question 3

(a) Granting of lease @ premium of $5000

Type of transaction: The transaction of granting of new lease or an act of renewal of the

previous existing lease at premium is termed as Type F1 CGT event under ss. 115-59

Capital gains: Total incidental cost incurred on the transaction for lease granting or renewal

and the derived premium are the two main factors which are used to compute the capital

gains as per the statutory formula given in ss. 104-110 ITAA 1997.

Capital gains = Derived premium – Total incidental cost.

Andy purchased a land and granted lease to Brian. Here, there is no incidental cost on lease

and the derived premium is $5,000 then, the capital gains are computed as Capital gains =

$5,000 - $0 = $5,000

Applicable method: The discount method is not applicable for derived capital gains for Type

F1 CGT event.

(b) Granting option to purchase the 100-acre farm of John to Farm Ltd against the sum of

$40,000

Type of transaction: The transaction to grant an option to other party to purchase the asset in

the exchange of asset belongs to D2 CGT event10.

Capital gains: Total incidental cost incurred on the transaction of granting option and the

derived income from granting option are the two main factors which are used to compute the

capital gains as per the statutory formula given in ss. 104-40 ITAA 1997.

8 Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

9 Austlii, Section 115-5<http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.5.html>

10 Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press Australia, 2017)

5

relation to the assessable income generation. Further, s. 40-664 ITAA 1997 would not be

held as the expenditure is not business linked8.

Question 3

(a) Granting of lease @ premium of $5000

Type of transaction: The transaction of granting of new lease or an act of renewal of the

previous existing lease at premium is termed as Type F1 CGT event under ss. 115-59

Capital gains: Total incidental cost incurred on the transaction for lease granting or renewal

and the derived premium are the two main factors which are used to compute the capital

gains as per the statutory formula given in ss. 104-110 ITAA 1997.

Capital gains = Derived premium – Total incidental cost.

Andy purchased a land and granted lease to Brian. Here, there is no incidental cost on lease

and the derived premium is $5,000 then, the capital gains are computed as Capital gains =

$5,000 - $0 = $5,000

Applicable method: The discount method is not applicable for derived capital gains for Type

F1 CGT event.

(b) Granting option to purchase the 100-acre farm of John to Farm Ltd against the sum of

$40,000

Type of transaction: The transaction to grant an option to other party to purchase the asset in

the exchange of asset belongs to D2 CGT event10.

Capital gains: Total incidental cost incurred on the transaction of granting option and the

derived income from granting option are the two main factors which are used to compute the

capital gains as per the statutory formula given in ss. 104-40 ITAA 1997.

8 Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

9 Austlii, Section 115-5<http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.5.html>

10 Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press Australia, 2017)

5

Capital gains = Income from granting option – Total incidental cost.

John purchased a land 10 years ago and granted the same to Farm ltd for $40,000. Here, there

is no incidental cost then, the capital gains are computed as Capital gains = $40,000 - $0 =

$40,000

Applicable method: The discount method is not applicable for derived capital gains for Type

D2 CGT event.

(c) Main residence

Type of transaction:In such cases where the capital gains has been derived from the sale of

the main residence of the asset, then is essential to determine whether the dwelling is main

residence of taxpayer or not. This is because under the exemption clause of Subdivision 118-

B, the capital gains will not be taxed when it has derived from the sale of main residence.

Further, the taxpayer has the legal position to treat their dwelling as main residence even

when they have not stayed for a max period of 6 years provided main residence does not exsit

elsewhere. In present case as well, Jamie and Olivia have purchased a home but not lived for

2 years whereas their main residence place has not shifted to alternative location. This

indicates the house will be classified as their main residence.

Capital gains:Under Subdivision 118-B, capital gains tax liabilities will not be raised on the

capital gains generated from the liquidation of the main residence of the taxpayer11.

Applicable method:The discount method would be applicable for derived capital gains (if

any) as the holding period of asset is more than 1 year.

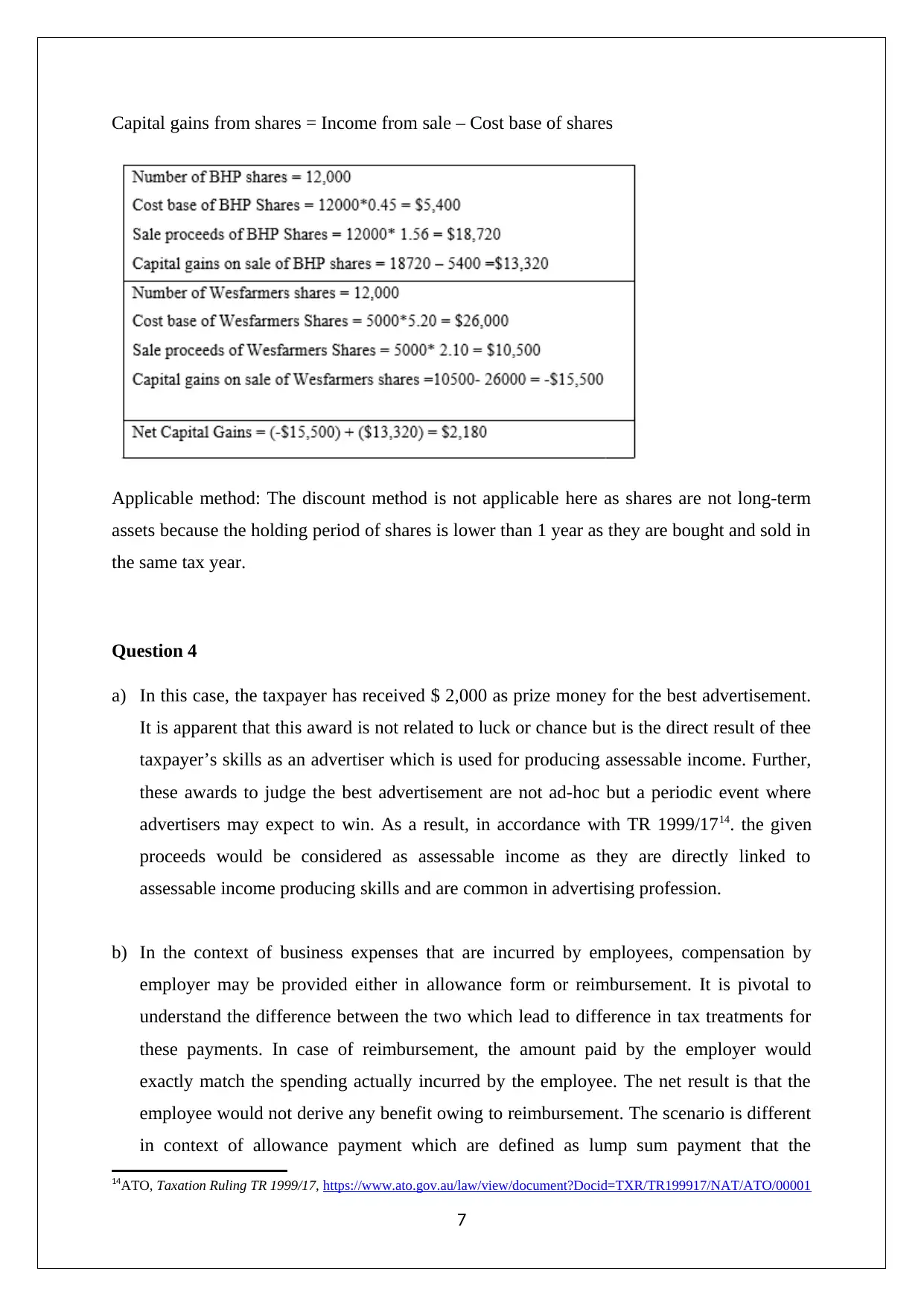

(d) Shares

Type of transaction:The transaction for sale of shares belongs to Type A1 CGT event. This

is because the shares are considered as CGT asset of taxpayer12.

Capital gains: Under ss.104-10 ITAA 1997, sale price of shares and the net cost base of

assets would be used for determining the capital gains of shares13.

11 CCH, Subdivision II8B <https://iknow.cch.com.au/topic/tlp104/overview/main-residence>

12 Ibid, 10. 654

13 Austlii, Income Tax Assessment Act 1997 – SECT 104.10,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.10.html

6

John purchased a land 10 years ago and granted the same to Farm ltd for $40,000. Here, there

is no incidental cost then, the capital gains are computed as Capital gains = $40,000 - $0 =

$40,000

Applicable method: The discount method is not applicable for derived capital gains for Type

D2 CGT event.

(c) Main residence

Type of transaction:In such cases where the capital gains has been derived from the sale of

the main residence of the asset, then is essential to determine whether the dwelling is main

residence of taxpayer or not. This is because under the exemption clause of Subdivision 118-

B, the capital gains will not be taxed when it has derived from the sale of main residence.

Further, the taxpayer has the legal position to treat their dwelling as main residence even

when they have not stayed for a max period of 6 years provided main residence does not exsit

elsewhere. In present case as well, Jamie and Olivia have purchased a home but not lived for

2 years whereas their main residence place has not shifted to alternative location. This

indicates the house will be classified as their main residence.

Capital gains:Under Subdivision 118-B, capital gains tax liabilities will not be raised on the

capital gains generated from the liquidation of the main residence of the taxpayer11.

Applicable method:The discount method would be applicable for derived capital gains (if

any) as the holding period of asset is more than 1 year.

(d) Shares

Type of transaction:The transaction for sale of shares belongs to Type A1 CGT event. This

is because the shares are considered as CGT asset of taxpayer12.

Capital gains: Under ss.104-10 ITAA 1997, sale price of shares and the net cost base of

assets would be used for determining the capital gains of shares13.

11 CCH, Subdivision II8B <https://iknow.cch.com.au/topic/tlp104/overview/main-residence>

12 Ibid, 10. 654

13 Austlii, Income Tax Assessment Act 1997 – SECT 104.10,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.10.html

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Capital gains from shares = Income from sale – Cost base of shares

Applicable method: The discount method is not applicable here as shares are not long-term

assets because the holding period of shares is lower than 1 year as they are bought and sold in

the same tax year.

Question 4

a) In this case, the taxpayer has received $ 2,000 as prize money for the best advertisement.

It is apparent that this award is not related to luck or chance but is the direct result of thee

taxpayer’s skills as an advertiser which is used for producing assessable income. Further,

these awards to judge the best advertisement are not ad-hoc but a periodic event where

advertisers may expect to win. As a result, in accordance with TR 1999/1714. the given

proceeds would be considered as assessable income as they are directly linked to

assessable income producing skills and are common in advertising profession.

b) In the context of business expenses that are incurred by employees, compensation by

employer may be provided either in allowance form or reimbursement. It is pivotal to

understand the difference between the two which lead to difference in tax treatments for

these payments. In case of reimbursement, the amount paid by the employer would

exactly match the spending actually incurred by the employee. The net result is that the

employee would not derive any benefit owing to reimbursement. The scenario is different

in context of allowance payment which are defined as lump sum payment that the

14ATO, Taxation Ruling TR 1999/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR199917/NAT/ATO/00001

7

Applicable method: The discount method is not applicable here as shares are not long-term

assets because the holding period of shares is lower than 1 year as they are bought and sold in

the same tax year.

Question 4

a) In this case, the taxpayer has received $ 2,000 as prize money for the best advertisement.

It is apparent that this award is not related to luck or chance but is the direct result of thee

taxpayer’s skills as an advertiser which is used for producing assessable income. Further,

these awards to judge the best advertisement are not ad-hoc but a periodic event where

advertisers may expect to win. As a result, in accordance with TR 1999/1714. the given

proceeds would be considered as assessable income as they are directly linked to

assessable income producing skills and are common in advertising profession.

b) In the context of business expenses that are incurred by employees, compensation by

employer may be provided either in allowance form or reimbursement. It is pivotal to

understand the difference between the two which lead to difference in tax treatments for

these payments. In case of reimbursement, the amount paid by the employer would

exactly match the spending actually incurred by the employee. The net result is that the

employee would not derive any benefit owing to reimbursement. The scenario is different

in context of allowance payment which are defined as lump sum payment that the

14ATO, Taxation Ruling TR 1999/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR199917/NAT/ATO/00001

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

employer provides employee for a particular item. The actual expenditure on the same

may be zero by the employee but the amount would still be given to the employee leading

to employee extracting economic benefits. As a result allowance payments contribute to

assessable income15. For the taxpayer (employee), an allowance of $ 500 is given by

employer for the Sydney trip as this amount is not dependent on the actual expenses and

no records need to be produced by the employee. Hence, this would be reflected as

assessable income.

c) The client has presented the taxpayer with an iPhone. It would not be treated as assessable

income only if it is a gift. There are various conditions outlined in TR 2005/13 to

highlight the same16. However, considering that the relationship between taxpayer and

client is professional, hence it is quite unlikely that the phone was given without

expectation of any material benefit. Also, it is likely that the phone may have been owing

to services offered in the past. Either ways, it is evident that the giving of iPhone to

taxpayer is on account of the professional relationship between the two and not on

grounds of personal association. Therefore, the given Iphone would contribute to

statutory income which as per s. 6-1017 would be termed as assessable income.

d) Based on the given facts, it is evident that the key objective is to outline if the

compensation payments to the tnne of $ 2,000 would be assessable income or not. A

fundamental principle with regards to determination of tax assessability of these

payments has been indicated in TD 93/5818. This highlights that the payments which are

compensatory would contribute to assessable income only if they are provided as

compensation for assessable income which has been lost. In the facts presented, it comes

to light that the compensation receipts are related to personal injury and thereby these

would not be taxed.

e) The computation of capital gains/losses is carried out only when a CGT event is

triggered. There are a host of CGT events to deal with various situations. However, in

15 ATO, TR 92/15 <https://www.ato.gov.au/law/view/document?docid=txr/tr9215/nat/ato/00001>

16 ATO TR 2005/13, <https://www.ato.gov.au/law/view/document?DocID=TXR/TR200513/NAT/ATO/00001>

17 ITAA 1997

18 Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company, 2017)

8

may be zero by the employee but the amount would still be given to the employee leading

to employee extracting economic benefits. As a result allowance payments contribute to

assessable income15. For the taxpayer (employee), an allowance of $ 500 is given by

employer for the Sydney trip as this amount is not dependent on the actual expenses and

no records need to be produced by the employee. Hence, this would be reflected as

assessable income.

c) The client has presented the taxpayer with an iPhone. It would not be treated as assessable

income only if it is a gift. There are various conditions outlined in TR 2005/13 to

highlight the same16. However, considering that the relationship between taxpayer and

client is professional, hence it is quite unlikely that the phone was given without

expectation of any material benefit. Also, it is likely that the phone may have been owing

to services offered in the past. Either ways, it is evident that the giving of iPhone to

taxpayer is on account of the professional relationship between the two and not on

grounds of personal association. Therefore, the given Iphone would contribute to

statutory income which as per s. 6-1017 would be termed as assessable income.

d) Based on the given facts, it is evident that the key objective is to outline if the

compensation payments to the tnne of $ 2,000 would be assessable income or not. A

fundamental principle with regards to determination of tax assessability of these

payments has been indicated in TD 93/5818. This highlights that the payments which are

compensatory would contribute to assessable income only if they are provided as

compensation for assessable income which has been lost. In the facts presented, it comes

to light that the compensation receipts are related to personal injury and thereby these

would not be taxed.

e) The computation of capital gains/losses is carried out only when a CGT event is

triggered. There are a host of CGT events to deal with various situations. However, in

15 ATO, TR 92/15 <https://www.ato.gov.au/law/view/document?docid=txr/tr9215/nat/ato/00001>

16 ATO TR 2005/13, <https://www.ato.gov.au/law/view/document?DocID=TXR/TR200513/NAT/ATO/00001>

17 ITAA 1997

18 Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company, 2017)

8

relation to capital gains or losses with regards to a CGT asset, the requisite CGT event is

A1 which refers to the disposal of asset, Only when the underlying asset is liquidated

would be computation of gains or losses be performed. Considering the facts provided, it

is apparent that the value of shares has appreciated but this gain is notional and cannot be

realised till the time asset sale happens.

Question 5

The tax residency of Nepal resident Nisu ought to be determined for 2018/2019 using the

relevant statutes and underlying tests. The key section which outlines the tax residency and

general approach is ss. 6-1 ITAA 1936. However, the tests available for ascertaining the tax

residency of individual taxpayers have been clearly outlined in tax ruling TR 98/1719. The

determination of tax residency is pivotal as the tax treatment extended to Australian residents

and foreign residents in terms of tax slabs, concessions, sources of income included and

allowable deductions tend to be different. The key tests available for tax residency

determination of individuals are outlined as follows.

1) !83 day test – This is applicable for foreign residents who are staying in Australia.

2) Domicile Test – This is applicable for Australian residents who are outside Australia for

work or personal reasons.

3) Commonwealth Superannuation Test –This is applicable for those taxpayers who are

employees of Federal government and are stationed outside Australia in professional

capacity.

4) Ordinary Residency Test – This is applicable for foreign residents who are staying in

Australia.

It is given that Nisu belongs to Nepal and thereby would be a foreign resident in Australia.

Considering the description given above for the tests, it is apparent that only two tests namely

183 day and ordinary residency test could potentially apply for Nisu.

183 Day Test

The passing of this test would require that the taxpayer should have spent a minimum of 183

days in Australia during the tax year under consideration. Also, it is essential that the Tax

19ATO, Taxation Ruling TR 98/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

9

A1 which refers to the disposal of asset, Only when the underlying asset is liquidated

would be computation of gains or losses be performed. Considering the facts provided, it

is apparent that the value of shares has appreciated but this gain is notional and cannot be

realised till the time asset sale happens.

Question 5

The tax residency of Nepal resident Nisu ought to be determined for 2018/2019 using the

relevant statutes and underlying tests. The key section which outlines the tax residency and

general approach is ss. 6-1 ITAA 1936. However, the tests available for ascertaining the tax

residency of individual taxpayers have been clearly outlined in tax ruling TR 98/1719. The

determination of tax residency is pivotal as the tax treatment extended to Australian residents

and foreign residents in terms of tax slabs, concessions, sources of income included and

allowable deductions tend to be different. The key tests available for tax residency

determination of individuals are outlined as follows.

1) !83 day test – This is applicable for foreign residents who are staying in Australia.

2) Domicile Test – This is applicable for Australian residents who are outside Australia for

work or personal reasons.

3) Commonwealth Superannuation Test –This is applicable for those taxpayers who are

employees of Federal government and are stationed outside Australia in professional

capacity.

4) Ordinary Residency Test – This is applicable for foreign residents who are staying in

Australia.

It is given that Nisu belongs to Nepal and thereby would be a foreign resident in Australia.

Considering the description given above for the tests, it is apparent that only two tests namely

183 day and ordinary residency test could potentially apply for Nisu.

183 Day Test

The passing of this test would require that the taxpayer should have spent a minimum of 183

days in Australia during the tax year under consideration. Also, it is essential that the Tax

19ATO, Taxation Ruling TR 98/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Commissioner must not have any suspicion in regards to taxpayer having plans to live in

Australia over the long run.

The relevant dates for Nisu are captured below

Date of arrival = 30 December 2018

Date of departure =30 June 2019

The total days of stay in Australia come out as 183 days for tax year 2018/2019. But despite

fulfilling this condition, Nisu would not be an Australian tax resident as per this test as he has

left Australian permanently owing to which it is evident that he would not settle or live in

Australia over long term.

Ordinary Residency Test

Owing to lack of clarity with regards to residency concept in Australian context, the

following factors are jointly considered to determine tax residency20.

Reason for visit to Australia – Significant causes related to long term employment and

study would lead to Australian tax residency unlike tourist which is casual purpose.

The nature and extent of ties in Australia – It considers both personal and professional

ties and draws comparison between Australia and country of origin21

Social arrangements while in Australia – The leading of a normal social life similar to

that in country of origin would enhance chances of Australian tax residency.

Considering the above factors, the applicability of the same for Nisu is discussed below.

He has come to Australia for a three year period for studying and hence the prupose

is very significant.

Also, he has got a part time job in Australia, education in Australia and has friends in

Australia thereby referring to sizable ties in Australia.

During his brief stay, his social life seemed very normal considering that he had

joined the football club and had quite a few friends.

Considering the above aspects, it would be appropriate to conclude that Nisu would be a tax

resident of Australia for 2018/2019 as per residency test.

20 Ibid, 10, 782

21Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

10

Australia over the long run.

The relevant dates for Nisu are captured below

Date of arrival = 30 December 2018

Date of departure =30 June 2019

The total days of stay in Australia come out as 183 days for tax year 2018/2019. But despite

fulfilling this condition, Nisu would not be an Australian tax resident as per this test as he has

left Australian permanently owing to which it is evident that he would not settle or live in

Australia over long term.

Ordinary Residency Test

Owing to lack of clarity with regards to residency concept in Australian context, the

following factors are jointly considered to determine tax residency20.

Reason for visit to Australia – Significant causes related to long term employment and

study would lead to Australian tax residency unlike tourist which is casual purpose.

The nature and extent of ties in Australia – It considers both personal and professional

ties and draws comparison between Australia and country of origin21

Social arrangements while in Australia – The leading of a normal social life similar to

that in country of origin would enhance chances of Australian tax residency.

Considering the above factors, the applicability of the same for Nisu is discussed below.

He has come to Australia for a three year period for studying and hence the prupose

is very significant.

Also, he has got a part time job in Australia, education in Australia and has friends in

Australia thereby referring to sizable ties in Australia.

During his brief stay, his social life seemed very normal considering that he had

joined the football club and had quite a few friends.

Considering the above aspects, it would be appropriate to conclude that Nisu would be a tax

resident of Australia for 2018/2019 as per residency test.

20 Ibid, 10, 782

21Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bibliography

ATO, Income Tax Assessment Act 1997 – SECT 118.5,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s118.5.html

11

ATO, Income Tax Assessment Act 1997 – SECT 118.5,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s118.5.html

11

ATO, Taxable Ruling TR 2018/4, https://www.ato.gov.au/law/view/document?DocID=TXR

%2FTR20184%2FNAT%2FATO%2F00001

ATO, Taxation Ruling TR 1999/17, https://www.ato.gov.au/law/view/document?

Docid=TXR/TR199917/NAT/ATO/00001

ATO, Taxation Ruling TR 98/17,

https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

Austlii, Income Tax Assessment Act 1936 – SECT 6,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s6.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.10,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.10.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.5,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html

Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press

Australia, 2017)

Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

FC of T v. Pechey75 ATC 4083

Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company,

2017)

Lodge v. FC of T (1972) 128 CLR 171

Mc Laurin v. FC of T (1961) 104 CLR 381

Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

12

%2FTR20184%2FNAT%2FATO%2F00001

ATO, Taxation Ruling TR 1999/17, https://www.ato.gov.au/law/view/document?

Docid=TXR/TR199917/NAT/ATO/00001

ATO, Taxation Ruling TR 98/17,

https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

Austlii, Income Tax Assessment Act 1936 – SECT 6,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s6.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.10,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.10.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.5,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html

Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press

Australia, 2017)

Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

FC of T v. Pechey75 ATC 4083

Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company,

2017)

Lodge v. FC of T (1972) 128 CLR 171

Mc Laurin v. FC of T (1961) 104 CLR 381

Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.