Australia Taxation Law Assignment: Deductions, GST, and Income Tax

VerifiedAdded on 2020/04/01

|9

|1196

|57

Homework Assignment

AI Summary

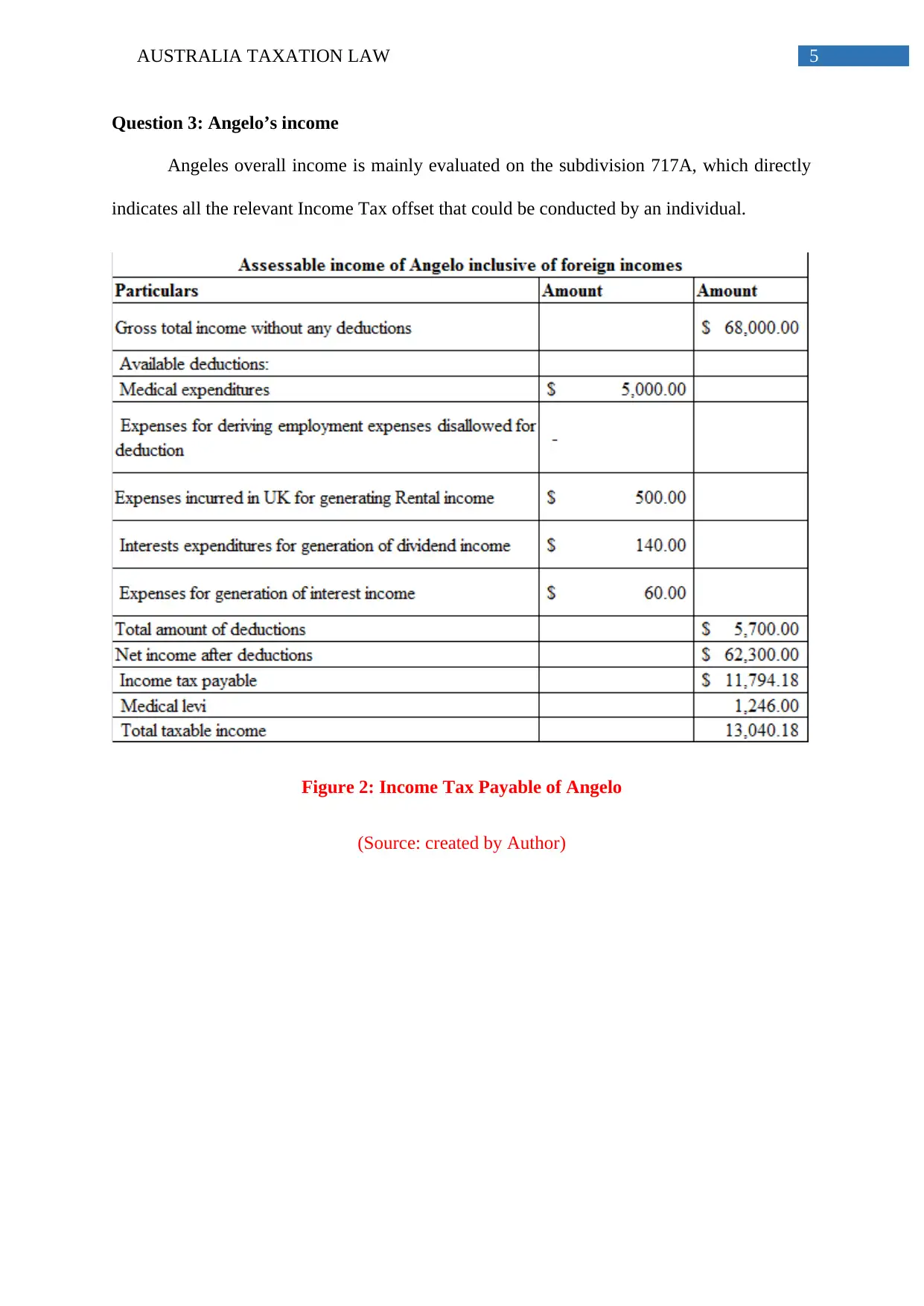

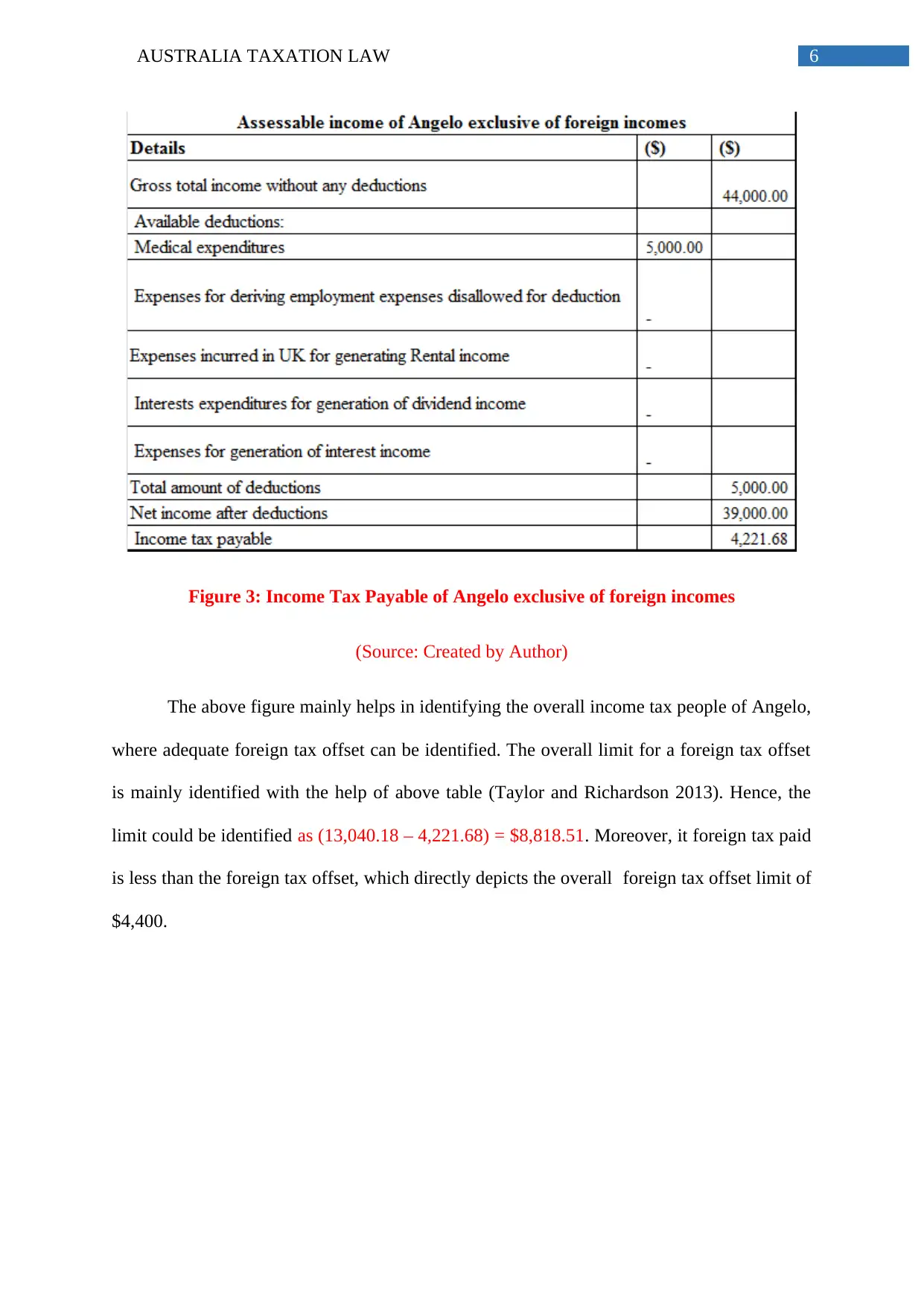

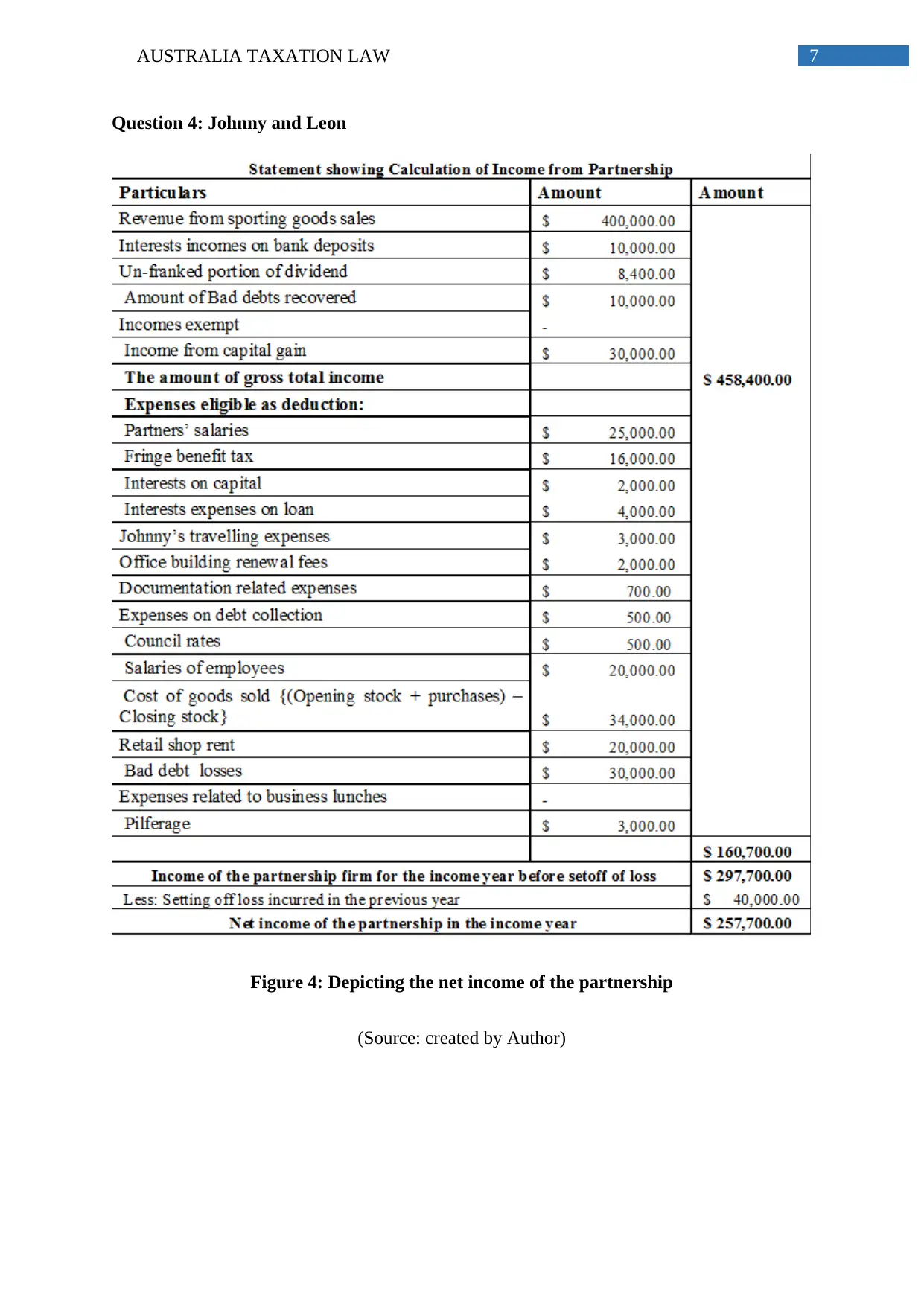

This assignment provides a comprehensive analysis of Australian taxation law, addressing key aspects such as allowable deductions under section 8-1 of the ITAA 1997, the application of GST input credits for businesses like Big Bank Ltd, and the calculation of income tax for individuals including Angelo's income with foreign tax offsets, and partnership income for Johnny and Leon. The assignment examines relevant case studies, financial figures, and legal provisions to illustrate the practical application of tax laws. It covers machinery transfer expenses, GST expenses, revaluation costs, and solicitor expenditures, providing a detailed understanding of tax implications for various business operations and income scenarios. The document includes figures illustrating key financial data, and references to relevant legislation and academic sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.