Industry/Micro Environment Report: Australian Activewear

VerifiedAdded on 2021/01/19

|28

|7443

|159

Report

AI Summary

This comprehensive report by Group 4 – Fantastic Four provides an in-depth analysis of the Australian activewear industry. It begins with an executive summary highlighting the industry's growth, driven by the athleisure trend and consumer demand for sustainable products. The report then delves into a detailed industry overview, followed by a PESTEL analysis, examining political, economic, legal, demographic, social, environmental, and technological factors impacting the market. Further sections include competitor and collaborator analyses, customer analysis, and key success factors. The report emphasizes the importance of eco-friendly practices and personalized customer service for future growth, projecting significant revenue increases by 2024. The report uses figures, tables, and analysis to provide a thorough understanding of the market, its challenges, and opportunities, making it a valuable resource for anyone interested in the Australian activewear sector.

1

Industry/Micro Environment

Report

By: Group 4 – Fantastic Four

Industry/Micro Environment

Report

By: Group 4 – Fantastic Four

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The Australian Activewear industry has experienced record growth in recent years, and is

expected to continue to thrive in coming years.

In 2019 alone, sales are expected to grow by 3.3%, an increase which is fuelled by the

popular athleisure trend; consumers are becoming more inclined to wear comfortable and

fashionable sportswear in day-to-day activities than ever before. This trend, along with

greater demand for luxury activewear items, has greatly driven sales within the industry, and

is highlighted through the success of brands such as Lululemon Athletica who offer high-

quality garments that are stylish, comfortable and flexible (Euromonitor, 2017).

Consumer attitudes favouring ethical and environmentally-conscious companies are also

increasing demand for products made with bamboo-fibre, which is considered a sustainable

and eco-friendly material (Imadi, Mahood, & Kazi, 2014).

Strong competitors in this industry include Nike (8.5% of market share) and Adidas (7.1% of

market share) who provide technologically superior products. Nike is considered a market

leader, while Adidas is considered a market challenger through their focus on the experiential

value of sportswear products (Euromonitor, 2019).

Increased online sales suggest offering activewear products from online-platforms, especially

through intermediaries such as eBay, can promote brand awareness and increase sales for

smaller activewear companies, who are attempting to compete with larger, well-established

brands such as Nike.

While the 35-54 year-old age group has generally dominated sales in this industry, consumers

within the 15-34 year old age group are becoming the main target group for activewear

companies as consumers from this demographic generally drive fashion trends and are

considered early-adopters of new styles entering the market. Promotion through social media

campaigns proves a highly effective way of targeting this audience (Still, 2014).

If companies new to the industry can harness the power of eco-friendly and sustainable fabric

options (bamboo) and provide personalised customer service they will engender a large

following from environmentally and health-conscious consumers (Business Insider, 2019)

and will be able to differentiate themselves in the market (McCann, 2015). Companies with

such positioning are expected to maintain steady future growth and benefit from overall

industry revenue growth, which is estimated to reach $2.4 billion in 2024 (Do, 2018).

Executive Summary

The Australian Activewear industry has experienced record growth in recent years, and is

expected to continue to thrive in coming years.

In 2019 alone, sales are expected to grow by 3.3%, an increase which is fuelled by the

popular athleisure trend; consumers are becoming more inclined to wear comfortable and

fashionable sportswear in day-to-day activities than ever before. This trend, along with

greater demand for luxury activewear items, has greatly driven sales within the industry, and

is highlighted through the success of brands such as Lululemon Athletica who offer high-

quality garments that are stylish, comfortable and flexible (Euromonitor, 2017).

Consumer attitudes favouring ethical and environmentally-conscious companies are also

increasing demand for products made with bamboo-fibre, which is considered a sustainable

and eco-friendly material (Imadi, Mahood, & Kazi, 2014).

Strong competitors in this industry include Nike (8.5% of market share) and Adidas (7.1% of

market share) who provide technologically superior products. Nike is considered a market

leader, while Adidas is considered a market challenger through their focus on the experiential

value of sportswear products (Euromonitor, 2019).

Increased online sales suggest offering activewear products from online-platforms, especially

through intermediaries such as eBay, can promote brand awareness and increase sales for

smaller activewear companies, who are attempting to compete with larger, well-established

brands such as Nike.

While the 35-54 year-old age group has generally dominated sales in this industry, consumers

within the 15-34 year old age group are becoming the main target group for activewear

companies as consumers from this demographic generally drive fashion trends and are

considered early-adopters of new styles entering the market. Promotion through social media

campaigns proves a highly effective way of targeting this audience (Still, 2014).

If companies new to the industry can harness the power of eco-friendly and sustainable fabric

options (bamboo) and provide personalised customer service they will engender a large

following from environmentally and health-conscious consumers (Business Insider, 2019)

and will be able to differentiate themselves in the market (McCann, 2015). Companies with

such positioning are expected to maintain steady future growth and benefit from overall

industry revenue growth, which is estimated to reach $2.4 billion in 2024 (Do, 2018).

3

Contents

Industry Overview: ............................................................................................................................. 4

PESTEL Factors: ................................................................................................................................ 5

Political: ....................................................................................................................................... 5

Economic: .................................................................................................................................... 6

Legal: ........................................................................................................................................... 7

Demographic: .............................................................................................................................. 8

Social: ......................................................................................................................................... 10

Environmental: ......................................................................................................................... 11

Technological: ........................................................................................................................... 12

Competitor Analysis: ........................................................................................................................ 13

Collaborator Analysis:...................................................................................................................... 17

Customer Analysis: ........................................................................................................................... 22

Key Success Factors: ........................................................................................................................ 24

Reference List: .................................................................................................................................. 25

Contents

Industry Overview: ............................................................................................................................. 4

PESTEL Factors: ................................................................................................................................ 5

Political: ....................................................................................................................................... 5

Economic: .................................................................................................................................... 6

Legal: ........................................................................................................................................... 7

Demographic: .............................................................................................................................. 8

Social: ......................................................................................................................................... 10

Environmental: ......................................................................................................................... 11

Technological: ........................................................................................................................... 12

Competitor Analysis: ........................................................................................................................ 13

Collaborator Analysis:...................................................................................................................... 17

Customer Analysis: ........................................................................................................................... 22

Key Success Factors: ........................................................................................................................ 24

Reference List: .................................................................................................................................. 25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

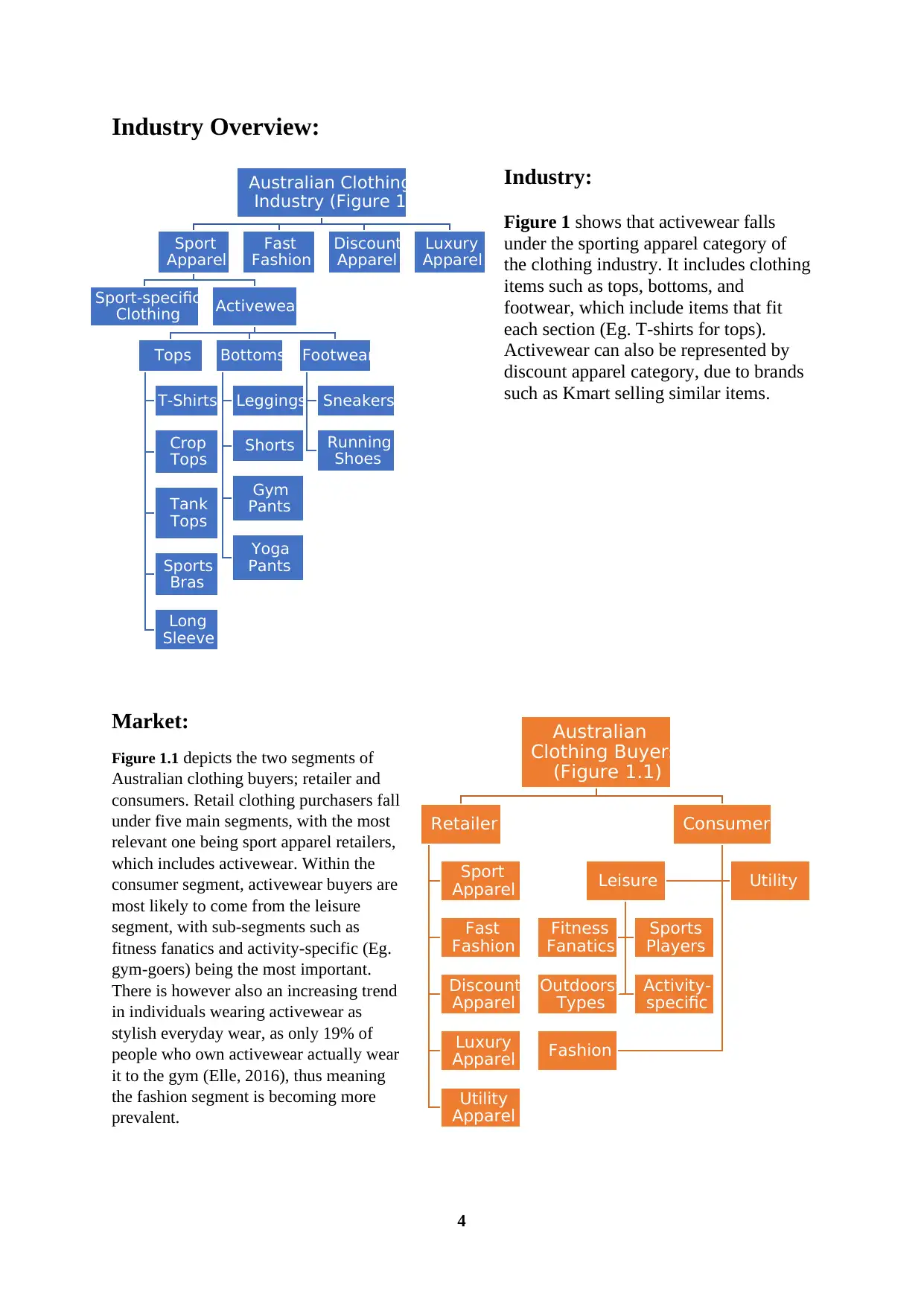

Industry Overview:

Industry:

Figure 1 shows that activewear falls

under the sporting apparel category of

the clothing industry. It includes clothing

items such as tops, bottoms, and

footwear, which include items that fit

each section (Eg. T-shirts for tops).

Activewear can also be represented by

discount apparel category, due to brands

such as Kmart selling similar items.

Market:

Figure 1.1 depicts the two segments of

Australian clothing buyers; retailer and

consumers. Retail clothing purchasers fall

under five main segments, with the most

relevant one being sport apparel retailers,

which includes activewear. Within the

consumer segment, activewear buyers are

most likely to come from the leisure

segment, with sub-segments such as

fitness fanatics and activity-specific (Eg.

gym-goers) being the most important.

There is however also an increasing trend

in individuals wearing activewear as

stylish everyday wear, as only 19% of

people who own activewear actually wear

it to the gym (Elle, 2016), thus meaning

the fashion segment is becoming more

prevalent.

Australian Clothing

Industry (Figure 1)

Sport

Apparel

Sport-specific

Clothing Activewear

Tops

T-Shirts

Crop

Tops

Tank

Tops

Sports

Bras

Long

Sleeve

Bottoms

Leggings

Shorts

Gym

Pants

Yoga

Pants

Footwear

Sneakers

Running

Shoes

Fast

Fashion

Discount

Apparel

Luxury

Apparel

Australian

Clothing Buyers

(Figure 1.1)

Retailer

Sport

Apparel

Fast

Fashion

Discount

Apparel

Luxury

Apparel

Utility

Apparel

Consumer

Leisure

Fitness

Fanatics

Sports

Players

Outdoorsy

Types

Activity-

specific

Utility

Fashion

Industry Overview:

Industry:

Figure 1 shows that activewear falls

under the sporting apparel category of

the clothing industry. It includes clothing

items such as tops, bottoms, and

footwear, which include items that fit

each section (Eg. T-shirts for tops).

Activewear can also be represented by

discount apparel category, due to brands

such as Kmart selling similar items.

Market:

Figure 1.1 depicts the two segments of

Australian clothing buyers; retailer and

consumers. Retail clothing purchasers fall

under five main segments, with the most

relevant one being sport apparel retailers,

which includes activewear. Within the

consumer segment, activewear buyers are

most likely to come from the leisure

segment, with sub-segments such as

fitness fanatics and activity-specific (Eg.

gym-goers) being the most important.

There is however also an increasing trend

in individuals wearing activewear as

stylish everyday wear, as only 19% of

people who own activewear actually wear

it to the gym (Elle, 2016), thus meaning

the fashion segment is becoming more

prevalent.

Australian Clothing

Industry (Figure 1)

Sport

Apparel

Sport-specific

Clothing Activewear

Tops

T-Shirts

Crop

Tops

Tank

Tops

Sports

Bras

Long

Sleeve

Bottoms

Leggings

Shorts

Gym

Pants

Yoga

Pants

Footwear

Sneakers

Running

Shoes

Fast

Fashion

Discount

Apparel

Luxury

Apparel

Australian

Clothing Buyers

(Figure 1.1)

Retailer

Sport

Apparel

Fast

Fashion

Discount

Apparel

Luxury

Apparel

Utility

Apparel

Consumer

Leisure

Fitness

Fanatics

Sports

Players

Outdoorsy

Types

Activity-

specific

Utility

Fashion

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

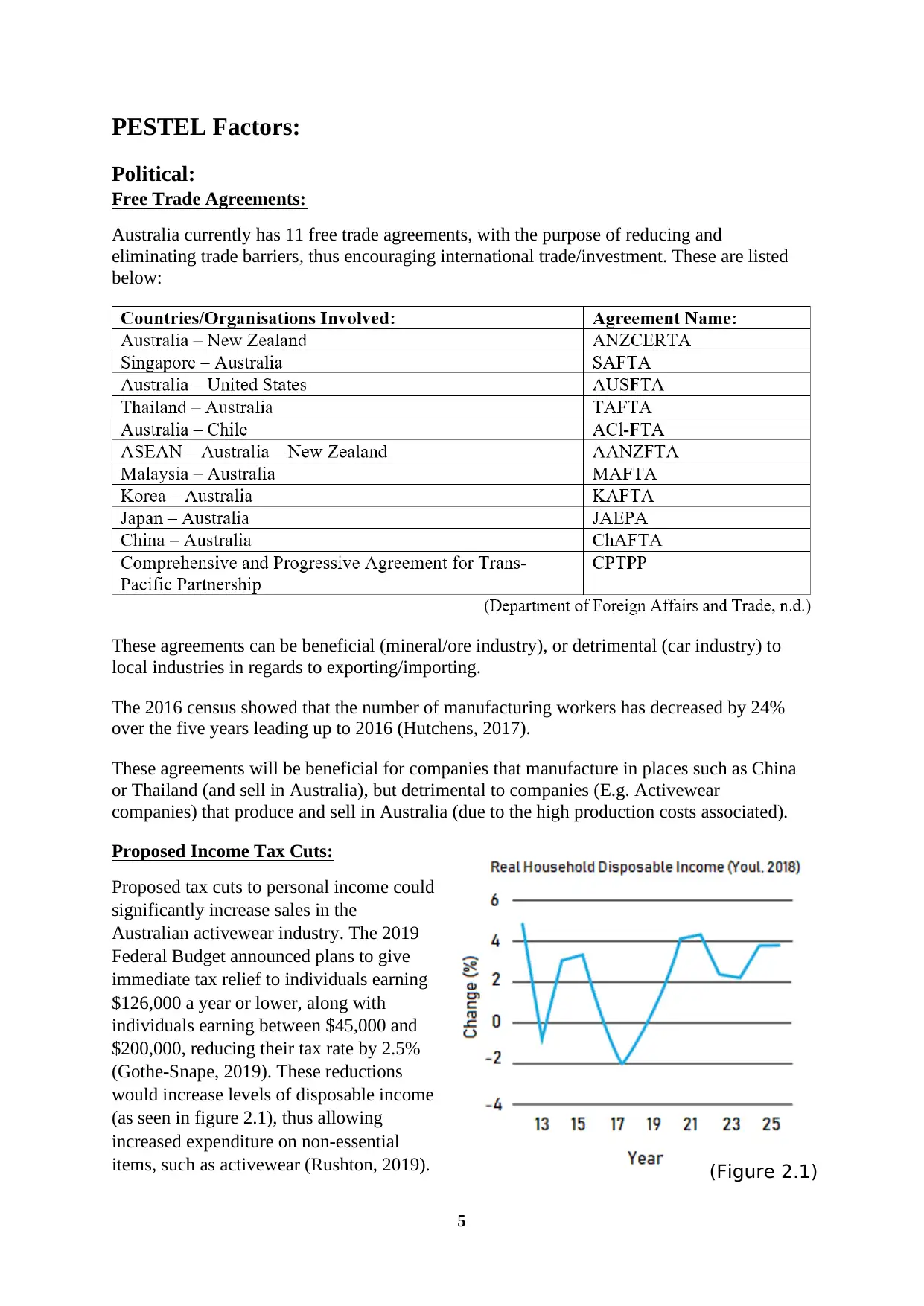

PESTEL Factors:

Political:

Free Trade Agreements:

Australia currently has 11 free trade agreements, with the purpose of reducing and

eliminating trade barriers, thus encouraging international trade/investment. These are listed

below:

These agreements can be beneficial (mineral/ore industry), or detrimental (car industry) to

local industries in regards to exporting/importing.

The 2016 census showed that the number of manufacturing workers has decreased by 24%

over the five years leading up to 2016 (Hutchens, 2017).

These agreements will be beneficial for companies that manufacture in places such as China

or Thailand (and sell in Australia), but detrimental to companies (E.g. Activewear

companies) that produce and sell in Australia (due to the high production costs associated).

Proposed Income Tax Cuts:

Proposed tax cuts to personal income could

significantly increase sales in the

Australian activewear industry. The 2019

Federal Budget announced plans to give

immediate tax relief to individuals earning

$126,000 a year or lower, along with

individuals earning between $45,000 and

$200,000, reducing their tax rate by 2.5%

(Gothe-Snape, 2019). These reductions

would increase levels of disposable income

(as seen in figure 2.1), thus allowing

increased expenditure on non-essential

items, such as activewear (Rushton, 2019). (Figure 2.1)

PESTEL Factors:

Political:

Free Trade Agreements:

Australia currently has 11 free trade agreements, with the purpose of reducing and

eliminating trade barriers, thus encouraging international trade/investment. These are listed

below:

These agreements can be beneficial (mineral/ore industry), or detrimental (car industry) to

local industries in regards to exporting/importing.

The 2016 census showed that the number of manufacturing workers has decreased by 24%

over the five years leading up to 2016 (Hutchens, 2017).

These agreements will be beneficial for companies that manufacture in places such as China

or Thailand (and sell in Australia), but detrimental to companies (E.g. Activewear

companies) that produce and sell in Australia (due to the high production costs associated).

Proposed Income Tax Cuts:

Proposed tax cuts to personal income could

significantly increase sales in the

Australian activewear industry. The 2019

Federal Budget announced plans to give

immediate tax relief to individuals earning

$126,000 a year or lower, along with

individuals earning between $45,000 and

$200,000, reducing their tax rate by 2.5%

(Gothe-Snape, 2019). These reductions

would increase levels of disposable income

(as seen in figure 2.1), thus allowing

increased expenditure on non-essential

items, such as activewear (Rushton, 2019). (Figure 2.1)

6

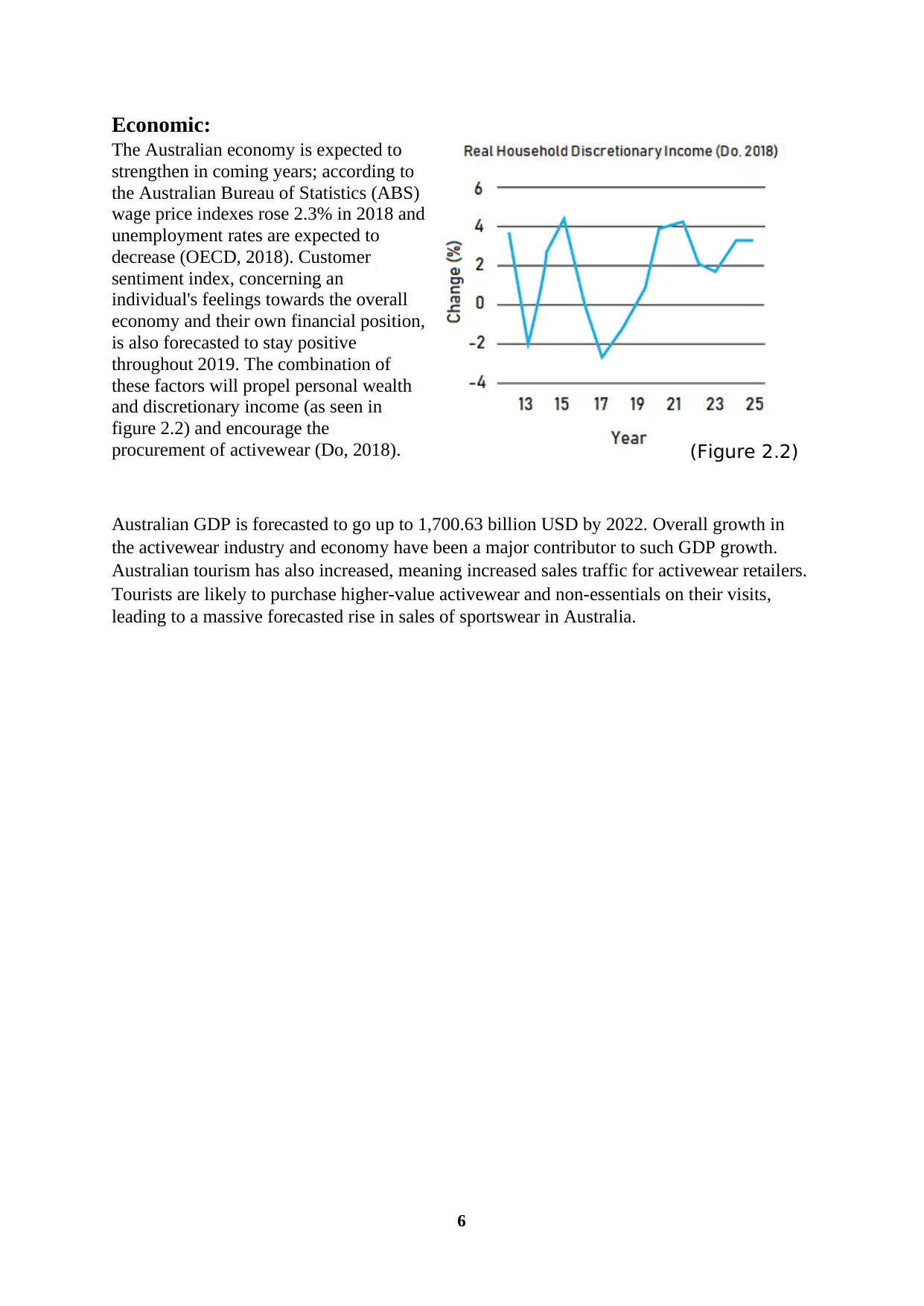

Economic:

The Australian economy is expected to

strengthen in coming years; according to

the Australian Bureau of Statistics (ABS)

wage price indexes rose 2.3% in 2018 and

unemployment rates are expected to

decrease (OECD, 2018). Customer

sentiment index, concerning an

individual's feelings towards the overall

economy and their own financial position,

is also forecasted to stay positive

throughout 2019. The combination of

these factors will propel personal wealth

and discretionary income (as seen in

figure 2.2) and encourage the

procurement of activewear (Do, 2018).

Australian GDP is forecasted to go up to 1,700.63 billion USD by 2022. Overall growth in

the activewear industry and economy have been a major contributor to such GDP growth.

Australian tourism has also increased, meaning increased sales traffic for activewear retailers.

Tourists are likely to purchase higher-value activewear and non-essentials on their visits,

leading to a massive forecasted rise in sales of sportswear in Australia.

(Figure 2.2)

Economic:

The Australian economy is expected to

strengthen in coming years; according to

the Australian Bureau of Statistics (ABS)

wage price indexes rose 2.3% in 2018 and

unemployment rates are expected to

decrease (OECD, 2018). Customer

sentiment index, concerning an

individual's feelings towards the overall

economy and their own financial position,

is also forecasted to stay positive

throughout 2019. The combination of

these factors will propel personal wealth

and discretionary income (as seen in

figure 2.2) and encourage the

procurement of activewear (Do, 2018).

Australian GDP is forecasted to go up to 1,700.63 billion USD by 2022. Overall growth in

the activewear industry and economy have been a major contributor to such GDP growth.

Australian tourism has also increased, meaning increased sales traffic for activewear retailers.

Tourists are likely to purchase higher-value activewear and non-essentials on their visits,

leading to a massive forecasted rise in sales of sportswear in Australia.

(Figure 2.2)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Legal:

Penalty Rates:

From the 1st of November 2018, increases in the General Retail Industry award rate were

implemented. This means an increase of 15% pay for work performed on Saturday, and a 5%

increase in pay for work that is performed after 6pm on weekdays (Elmas, 2018).

By 2020, there will be a 25% penalty rate implemented on Saturdays, and an extra 15%

loading rate after 6pm on weekdays (Elmas, 2018).

The implication of such an increase in penalty rates on the retail sector will mean that it is

more costly to have operate retail stores during Saturdays and weekdays (after 6pm). This

will discourage retail stores from staying open past 6pm, or for long periods on Saturdays. If

they do decide to stay open during these times, they will incur a higher cost of operating each

store. This may lead to an increase in prices or a reduction in the price margins of products,

which will discourage current and prospective brands from becoming part of the Australian

retail sector.

GST on low value imported goods:

The Federal Parliament implemented a law on the 1st of July 2018 intending to extend the

goods and services tax (10%) to goods that are imported by consumers (valued at $1,000 or

under) (Australian Taxation Office, 2018).

The law will positively impact the whole industry, including the activewear aspect of the

sportswear/clothing industry. It will cause importers of activewear (on marketplaces like

eBay) to increase their prices or reduce their margins when selling their clothing in Australia,

giving the local competitors an advantage (Youl, 2018)

Retail Regulations:

The Competition and Consumer Act 2010 covers largely all parts of the market (suppliers,

retailers, consumers, etc.); and laws on product safety and labelling, unfair market practices,

price monitoring, industry codes, industry regulation – airports, electricity, gas,

telecommunications, mergers and acquisitions (ACCC, 2010).

Thus, activewear businesses can’t create their own monopoly to surge prices, put smaller

businesses out of business, perform under-the-table deals which intermediaries and be unfair

to customers.

Store trading hours regulation are also established to protect smaller players in the activewear

market. However, the government are becoming more lenient towards the law as it does

constrain growth and activity.

Legal:

Penalty Rates:

From the 1st of November 2018, increases in the General Retail Industry award rate were

implemented. This means an increase of 15% pay for work performed on Saturday, and a 5%

increase in pay for work that is performed after 6pm on weekdays (Elmas, 2018).

By 2020, there will be a 25% penalty rate implemented on Saturdays, and an extra 15%

loading rate after 6pm on weekdays (Elmas, 2018).

The implication of such an increase in penalty rates on the retail sector will mean that it is

more costly to have operate retail stores during Saturdays and weekdays (after 6pm). This

will discourage retail stores from staying open past 6pm, or for long periods on Saturdays. If

they do decide to stay open during these times, they will incur a higher cost of operating each

store. This may lead to an increase in prices or a reduction in the price margins of products,

which will discourage current and prospective brands from becoming part of the Australian

retail sector.

GST on low value imported goods:

The Federal Parliament implemented a law on the 1st of July 2018 intending to extend the

goods and services tax (10%) to goods that are imported by consumers (valued at $1,000 or

under) (Australian Taxation Office, 2018).

The law will positively impact the whole industry, including the activewear aspect of the

sportswear/clothing industry. It will cause importers of activewear (on marketplaces like

eBay) to increase their prices or reduce their margins when selling their clothing in Australia,

giving the local competitors an advantage (Youl, 2018)

Retail Regulations:

The Competition and Consumer Act 2010 covers largely all parts of the market (suppliers,

retailers, consumers, etc.); and laws on product safety and labelling, unfair market practices,

price monitoring, industry codes, industry regulation – airports, electricity, gas,

telecommunications, mergers and acquisitions (ACCC, 2010).

Thus, activewear businesses can’t create their own monopoly to surge prices, put smaller

businesses out of business, perform under-the-table deals which intermediaries and be unfair

to customers.

Store trading hours regulation are also established to protect smaller players in the activewear

market. However, the government are becoming more lenient towards the law as it does

constrain growth and activity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

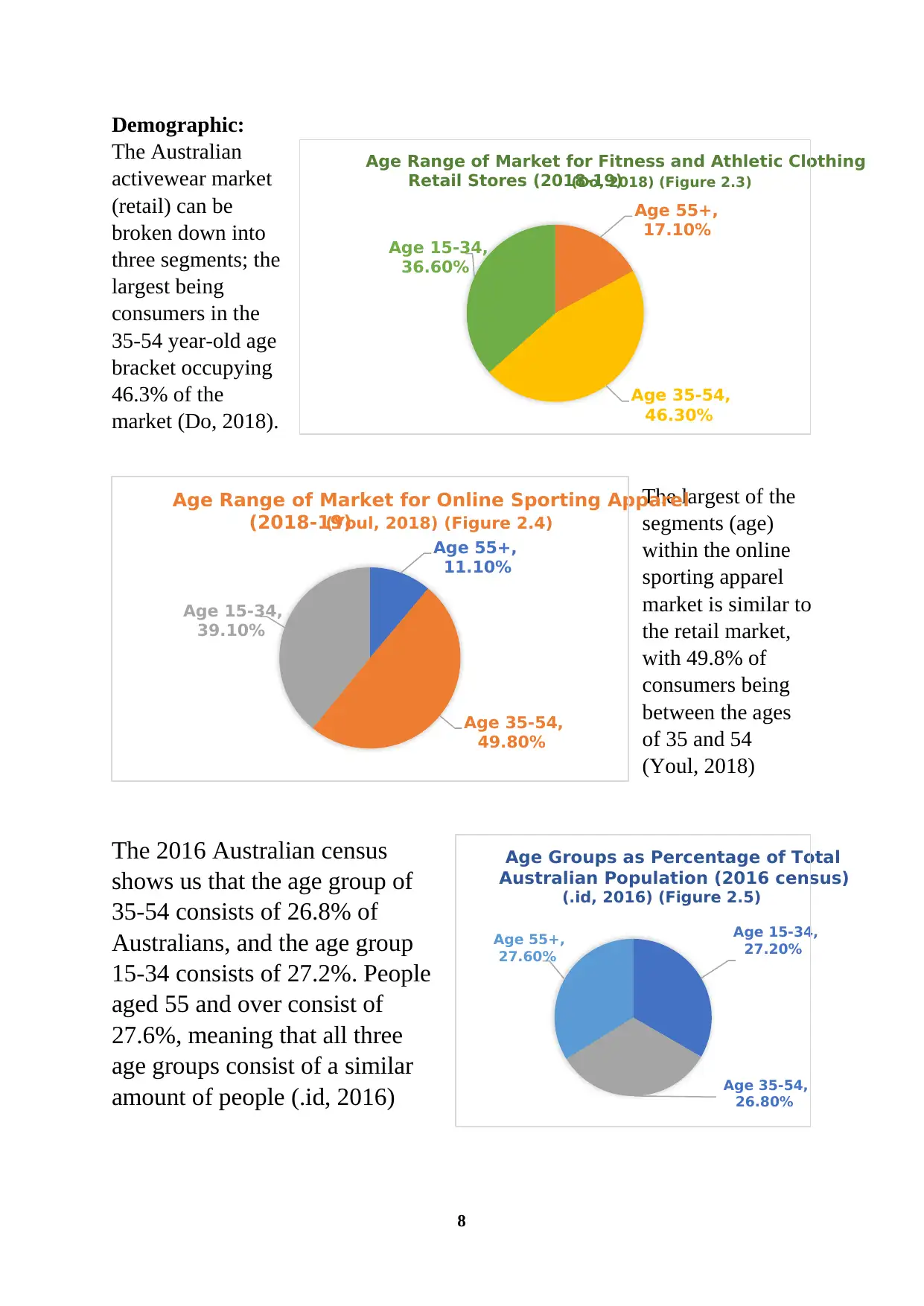

Demographic:

The Australian

activewear market

(retail) can be

broken down into

three segments; the

largest being

consumers in the

35-54 year-old age

bracket occupying

46.3% of the

market (Do, 2018).

The largest of the

segments (age)

within the online

sporting apparel

market is similar to

the retail market,

with 49.8% of

consumers being

between the ages

of 35 and 54

(Youl, 2018)

The 2016 Australian census

shows us that the age group of

35-54 consists of 26.8% of

Australians, and the age group

15-34 consists of 27.2%. People

aged 55 and over consist of

27.6%, meaning that all three

age groups consist of a similar

amount of people (.id, 2016)

Age 55+,

17.10%

Age 35-54,

46.30%

Age 15-34,

36.60%

Age Range of Market for Fitness and Athletic Clothing

Retail Stores (2018-19)(Do, 2018) (Figure 2.3)

Age 55+,

11.10%

Age 35-54,

49.80%

Age 15-34,

39.10%

Age Range of Market for Online Sporting Apparel

(2018-19)(Youl, 2018) (Figure 2.4)

Age 15-34,

27.20%

Age 35-54,

26.80%

Age 55+,

27.60%

Age Groups as Percentage of Total

Australian Population (2016 census)

(.id, 2016) (Figure 2.5)

Demographic:

The Australian

activewear market

(retail) can be

broken down into

three segments; the

largest being

consumers in the

35-54 year-old age

bracket occupying

46.3% of the

market (Do, 2018).

The largest of the

segments (age)

within the online

sporting apparel

market is similar to

the retail market,

with 49.8% of

consumers being

between the ages

of 35 and 54

(Youl, 2018)

The 2016 Australian census

shows us that the age group of

35-54 consists of 26.8% of

Australians, and the age group

15-34 consists of 27.2%. People

aged 55 and over consist of

27.6%, meaning that all three

age groups consist of a similar

amount of people (.id, 2016)

Age 55+,

17.10%

Age 35-54,

46.30%

Age 15-34,

36.60%

Age Range of Market for Fitness and Athletic Clothing

Retail Stores (2018-19)(Do, 2018) (Figure 2.3)

Age 55+,

11.10%

Age 35-54,

49.80%

Age 15-34,

39.10%

Age Range of Market for Online Sporting Apparel

(2018-19)(Youl, 2018) (Figure 2.4)

Age 15-34,

27.20%

Age 35-54,

26.80%

Age 55+,

27.60%

Age Groups as Percentage of Total

Australian Population (2016 census)

(.id, 2016) (Figure 2.5)

9

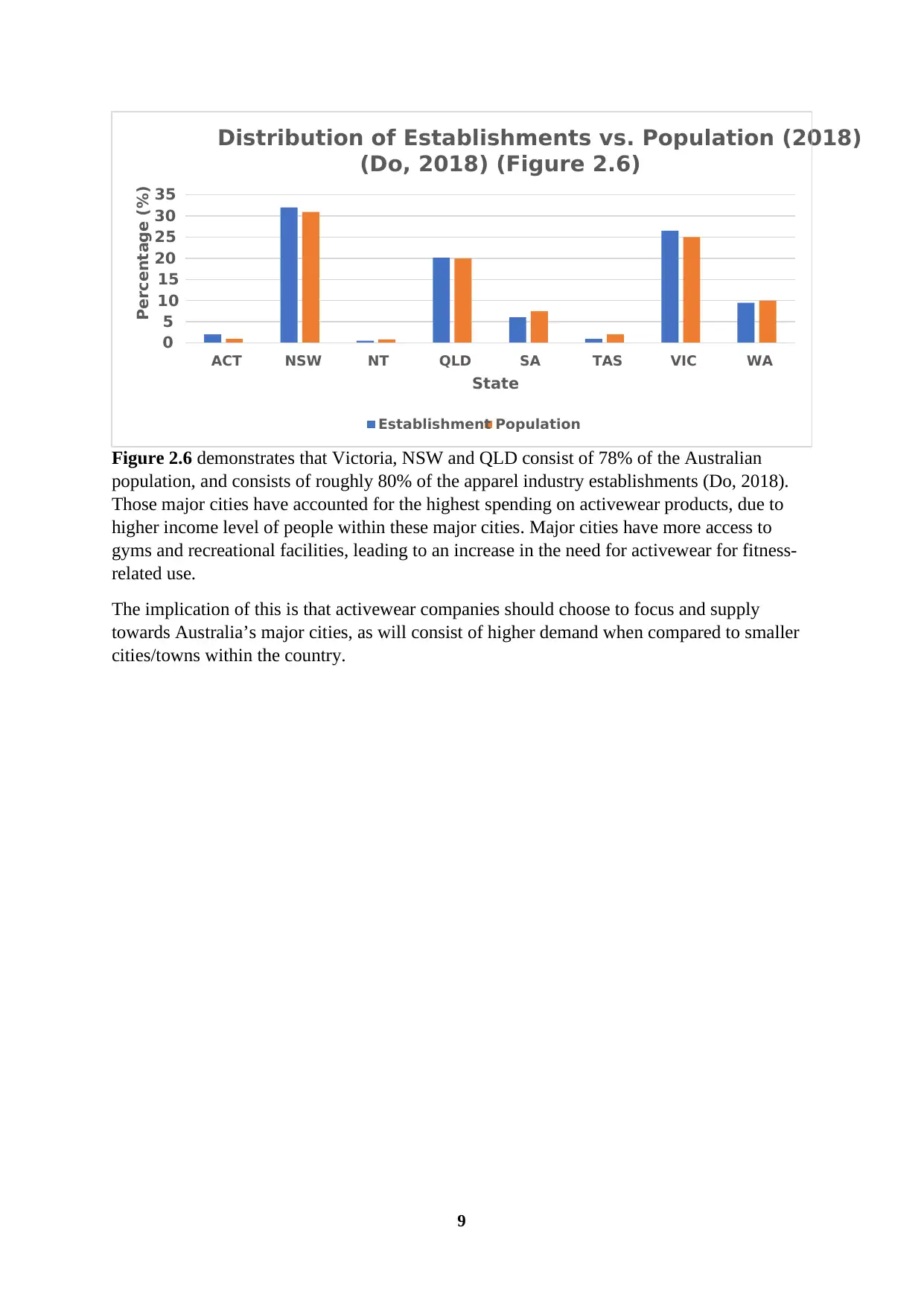

Figure 2.6 demonstrates that Victoria, NSW and QLD consist of 78% of the Australian

population, and consists of roughly 80% of the apparel industry establishments (Do, 2018).

Those major cities have accounted for the highest spending on activewear products, due to

higher income level of people within these major cities. Major cities have more access to

gyms and recreational facilities, leading to an increase in the need for activewear for fitness-

related use.

The implication of this is that activewear companies should choose to focus and supply

towards Australia’s major cities, as will consist of higher demand when compared to smaller

cities/towns within the country.

0

5

10

15

20

25

30

35

ACT NSW NT QLD SA TAS VIC WA

Percentage (%)

State

Distribution of Establishments vs. Population (2018)

(Do, 2018) (Figure 2.6)

Establishment Population

Figure 2.6 demonstrates that Victoria, NSW and QLD consist of 78% of the Australian

population, and consists of roughly 80% of the apparel industry establishments (Do, 2018).

Those major cities have accounted for the highest spending on activewear products, due to

higher income level of people within these major cities. Major cities have more access to

gyms and recreational facilities, leading to an increase in the need for activewear for fitness-

related use.

The implication of this is that activewear companies should choose to focus and supply

towards Australia’s major cities, as will consist of higher demand when compared to smaller

cities/towns within the country.

0

5

10

15

20

25

30

35

ACT NSW NT QLD SA TAS VIC WA

Percentage (%)

State

Distribution of Establishments vs. Population (2018)

(Do, 2018) (Figure 2.6)

Establishment Population

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Social:

Athleisure Trend:

Consumers are increasingly choosing luxury sportswear products that can be worn during

exercise and casually too. According to Cheng (2018) sales of specialised performance

activewear are declining in comparison to ‘sports leisure’ products. Industry players must

take note of this trend and consider expanding their product into the ‘Athleisure’ market.

Social trends:

Consumers are also becoming more environmentally conscious; over 90% of Australians are

concerned about sustainability and the environment. This trend which is propelled by social

media marketing campaigns, such as Greenpeace’s, which campaigns for retail companies to

omit hazardous chemicals in their production process (Still, 2014). Companies which are

recognised as acting in an ethical and socially-responsible manner are preferred by consumers

and thus attract more sales and profits (Retail Insight Network, 2018).

Social:

Athleisure Trend:

Consumers are increasingly choosing luxury sportswear products that can be worn during

exercise and casually too. According to Cheng (2018) sales of specialised performance

activewear are declining in comparison to ‘sports leisure’ products. Industry players must

take note of this trend and consider expanding their product into the ‘Athleisure’ market.

Social trends:

Consumers are also becoming more environmentally conscious; over 90% of Australians are

concerned about sustainability and the environment. This trend which is propelled by social

media marketing campaigns, such as Greenpeace’s, which campaigns for retail companies to

omit hazardous chemicals in their production process (Still, 2014). Companies which are

recognised as acting in an ethical and socially-responsible manner are preferred by consumers

and thus attract more sales and profits (Retail Insight Network, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

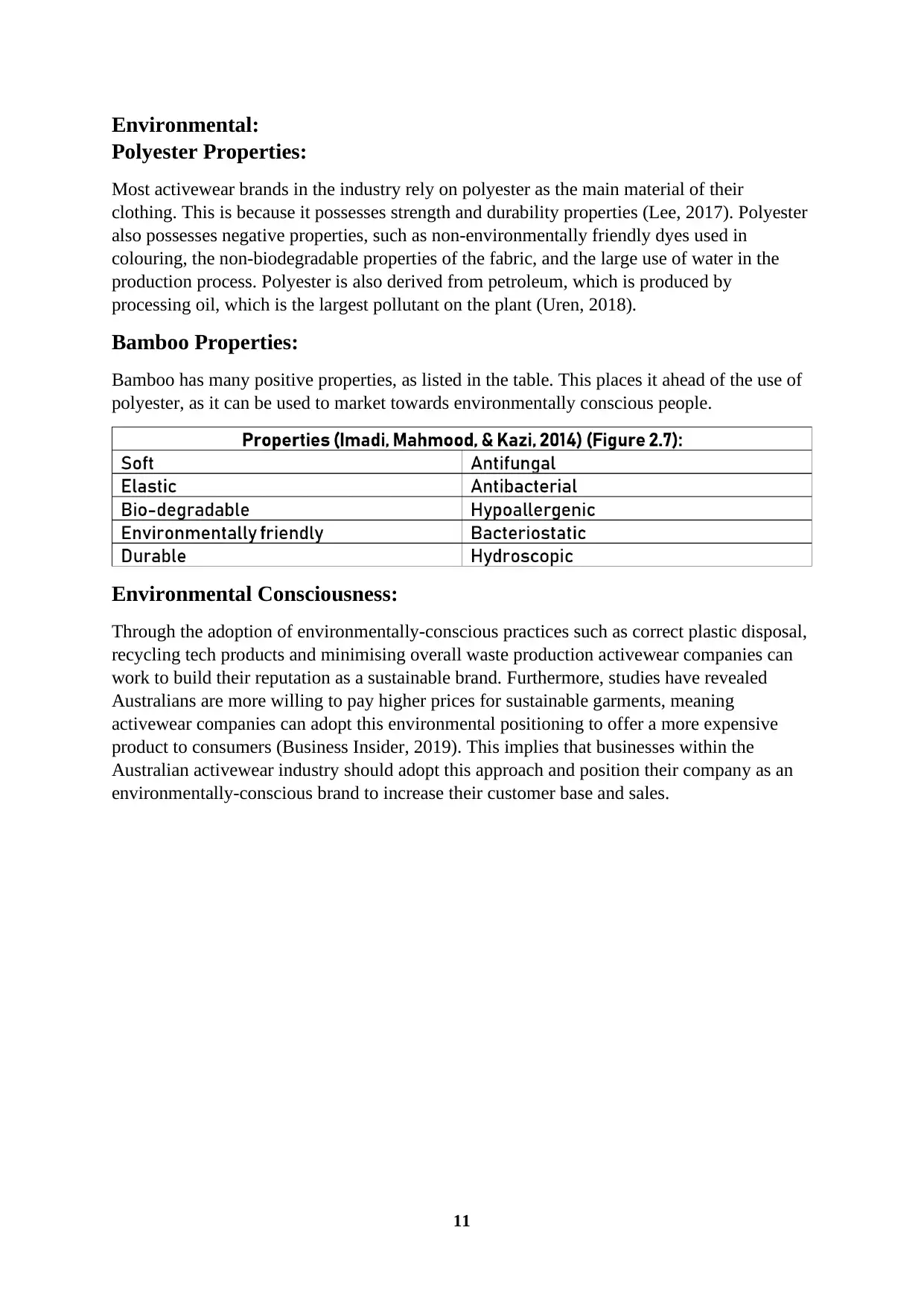

Environmental:

Polyester Properties:

Most activewear brands in the industry rely on polyester as the main material of their

clothing. This is because it possesses strength and durability properties (Lee, 2017). Polyester

also possesses negative properties, such as non-environmentally friendly dyes used in

colouring, the non-biodegradable properties of the fabric, and the large use of water in the

production process. Polyester is also derived from petroleum, which is produced by

processing oil, which is the largest pollutant on the plant (Uren, 2018).

Bamboo Properties:

Bamboo has many positive properties, as listed in the table. This places it ahead of the use of

polyester, as it can be used to market towards environmentally conscious people.

Environmental Consciousness:

Through the adoption of environmentally-conscious practices such as correct plastic disposal,

recycling tech products and minimising overall waste production activewear companies can

work to build their reputation as a sustainable brand. Furthermore, studies have revealed

Australians are more willing to pay higher prices for sustainable garments, meaning

activewear companies can adopt this environmental positioning to offer a more expensive

product to consumers (Business Insider, 2019). This implies that businesses within the

Australian activewear industry should adopt this approach and position their company as an

environmentally-conscious brand to increase their customer base and sales.

Environmental:

Polyester Properties:

Most activewear brands in the industry rely on polyester as the main material of their

clothing. This is because it possesses strength and durability properties (Lee, 2017). Polyester

also possesses negative properties, such as non-environmentally friendly dyes used in

colouring, the non-biodegradable properties of the fabric, and the large use of water in the

production process. Polyester is also derived from petroleum, which is produced by

processing oil, which is the largest pollutant on the plant (Uren, 2018).

Bamboo Properties:

Bamboo has many positive properties, as listed in the table. This places it ahead of the use of

polyester, as it can be used to market towards environmentally conscious people.

Environmental Consciousness:

Through the adoption of environmentally-conscious practices such as correct plastic disposal,

recycling tech products and minimising overall waste production activewear companies can

work to build their reputation as a sustainable brand. Furthermore, studies have revealed

Australians are more willing to pay higher prices for sustainable garments, meaning

activewear companies can adopt this environmental positioning to offer a more expensive

product to consumers (Business Insider, 2019). This implies that businesses within the

Australian activewear industry should adopt this approach and position their company as an

environmentally-conscious brand to increase their customer base and sales.

12

Technological:

Online Shopping:

Online shopping has dramatically increased accessibility to activewear garments through e-

commerce development and represents an increasing sales trend in the fashion industry.

AusPost Industry report stated 35.6% of sales have been online fashion-apparel purchases,

including an 11.7% increase in sales in the activewear sector compared to the previous year

(Yip, Lieu & Foo, 2018).

This implies sellers could greatly benefit from developing an online platform for their brand

as online apparel purchases are on the rise. Moreover, online retailing saves organisation

costs through the reduction of staff wages and allows them to process sales transactions at

any time of day or night.

Buy Now Pay Later:

One considerable e-commerce development has been the introduction of “buy now, pay later”

options such as Afterpay and ZipPay, which offer customers interest-free payment plans on

purchases via regular weekly, fortnightly or monthly instalments. This new innovation has

resulted in a 289% surge in online sales between 2017 and 2018, concluding a total of $2.2

billion Afterpay sales, 25% of which was from the fashion retail industry alone (Wu, 2018).

Offering payment options such as Afterpay is an effective way to increase activewear sales

from younger, lower-income demographics. 60% of Afterpay users are aged between 18 and

34 years, demonstrating these services lower the price barrier many young people face when

purchasing expensive activewear products (Wu, 2018). Therefore, activewear companies

should consider adopting such payments plans to increase sales from younger demographics

who largely drive fashion trends.

Technological:

Online Shopping:

Online shopping has dramatically increased accessibility to activewear garments through e-

commerce development and represents an increasing sales trend in the fashion industry.

AusPost Industry report stated 35.6% of sales have been online fashion-apparel purchases,

including an 11.7% increase in sales in the activewear sector compared to the previous year

(Yip, Lieu & Foo, 2018).

This implies sellers could greatly benefit from developing an online platform for their brand

as online apparel purchases are on the rise. Moreover, online retailing saves organisation

costs through the reduction of staff wages and allows them to process sales transactions at

any time of day or night.

Buy Now Pay Later:

One considerable e-commerce development has been the introduction of “buy now, pay later”

options such as Afterpay and ZipPay, which offer customers interest-free payment plans on

purchases via regular weekly, fortnightly or monthly instalments. This new innovation has

resulted in a 289% surge in online sales between 2017 and 2018, concluding a total of $2.2

billion Afterpay sales, 25% of which was from the fashion retail industry alone (Wu, 2018).

Offering payment options such as Afterpay is an effective way to increase activewear sales

from younger, lower-income demographics. 60% of Afterpay users are aged between 18 and

34 years, demonstrating these services lower the price barrier many young people face when

purchasing expensive activewear products (Wu, 2018). Therefore, activewear companies

should consider adopting such payments plans to increase sales from younger demographics

who largely drive fashion trends.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.