Australian Agricultural Company Limited: Integrated Reporting Report

VerifiedAdded on 2020/09/03

|15

|2674

|34

Report

AI Summary

This report provides a comprehensive analysis of the financial statements of Australian Agricultural Company Limited (AAC Limited), focusing on integrated reporting practices. The analysis delves into various financial statement adjustments, including cattle fair value adjustments, property valuations, and the comparison of net profits and comprehensive income. The report examines the classification of livestock under current and non-current assets, the treatment of property, plant, and equipment, and the recording of borrowings under non-current liabilities. It also explores future minimum lease payments, the impact of Australian Accounting Standard AASB 16, other commitments, and contingencies. The report highlights the company's financial performance, discussing increases in cattle fair value, property values, and net profits. The analysis also addresses the impact of market movements, biological transformation, and natural rise on cattle fair value, along with the depreciation, amortization, and revaluation of properties. Furthermore, the report examines the company's borrowings, lease payments, and other commitments, offering insights into its financial position and strategic planning.

INTEGRATED

REPORTING: PROBLEM

SOLVING

REPORTING: PROBLEM

SOLVING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

(i) Cattle fair value adjustments..................................................................................................1

(ii) Adjustments in fair value of property...................................................................................2

(iii) Comparison of net profits and comprehensive income........................................................4

PART B............................................................................................................................................6

(i) Live stock under current and non current assets....................................................................6

(ii) Property, plant and equipment under non current assets.......................................................7

(iii) Borrowings recorded under non current liabilities...............................................................8

PART C............................................................................................................................................9

(i) Future minimum lease payment.............................................................................................9

(ii) Impact of Australian Accounting Standard AASB 16 on the company..............................10

(iii) Other commitments............................................................................................................10

(iv) Contingencies.....................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

(i) Cattle fair value adjustments..................................................................................................1

(ii) Adjustments in fair value of property...................................................................................2

(iii) Comparison of net profits and comprehensive income........................................................4

PART B............................................................................................................................................6

(i) Live stock under current and non current assets....................................................................6

(ii) Property, plant and equipment under non current assets.......................................................7

(iii) Borrowings recorded under non current liabilities...............................................................8

PART C............................................................................................................................................9

(i) Future minimum lease payment.............................................................................................9

(ii) Impact of Australian Accounting Standard AASB 16 on the company..............................10

(iii) Other commitments............................................................................................................10

(iv) Contingencies.....................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Illustration Index

Illustration 1: Comparison of cattle fair value.................................................................................2

Illustration 2: Comparison of values of property, plants and equipments.......................................3

Illustration 3: Comparison of fair value of property........................................................................4

Illustration 4: Comparison of profits................................................................................................5

Illustration 5: Comparison of comprehensive income.....................................................................5

Illustration 6: Fair value of cattle.....................................................................................................7

Illustration 7: Property, plant and equipments.................................................................................8

Illustration 8: Comparison of borrowings........................................................................................9

Illustration 9: Comparison of leased land and building.................................................................10

Index of Tables

Table 1: Increase or decrease in cattle fair value.............................................................................1

Table 2: Fair value of the property..................................................................................................3

Table 3: Profits for 2016 and 2017..................................................................................................4

Table 4: Increase or decrease in comprehensive income.................................................................5

Table 5: Fair value of different type of cattle..................................................................................6

Table 6: Increase or decrease in borrowings....................................................................................8

Table 7: Increase or decrease in operating lease of land and building............................................9

Illustration 1: Comparison of cattle fair value.................................................................................2

Illustration 2: Comparison of values of property, plants and equipments.......................................3

Illustration 3: Comparison of fair value of property........................................................................4

Illustration 4: Comparison of profits................................................................................................5

Illustration 5: Comparison of comprehensive income.....................................................................5

Illustration 6: Fair value of cattle.....................................................................................................7

Illustration 7: Property, plant and equipments.................................................................................8

Illustration 8: Comparison of borrowings........................................................................................9

Illustration 9: Comparison of leased land and building.................................................................10

Index of Tables

Table 1: Increase or decrease in cattle fair value.............................................................................1

Table 2: Fair value of the property..................................................................................................3

Table 3: Profits for 2016 and 2017..................................................................................................4

Table 4: Increase or decrease in comprehensive income.................................................................5

Table 5: Fair value of different type of cattle..................................................................................6

Table 6: Increase or decrease in borrowings....................................................................................8

Table 7: Increase or decrease in operating lease of land and building............................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

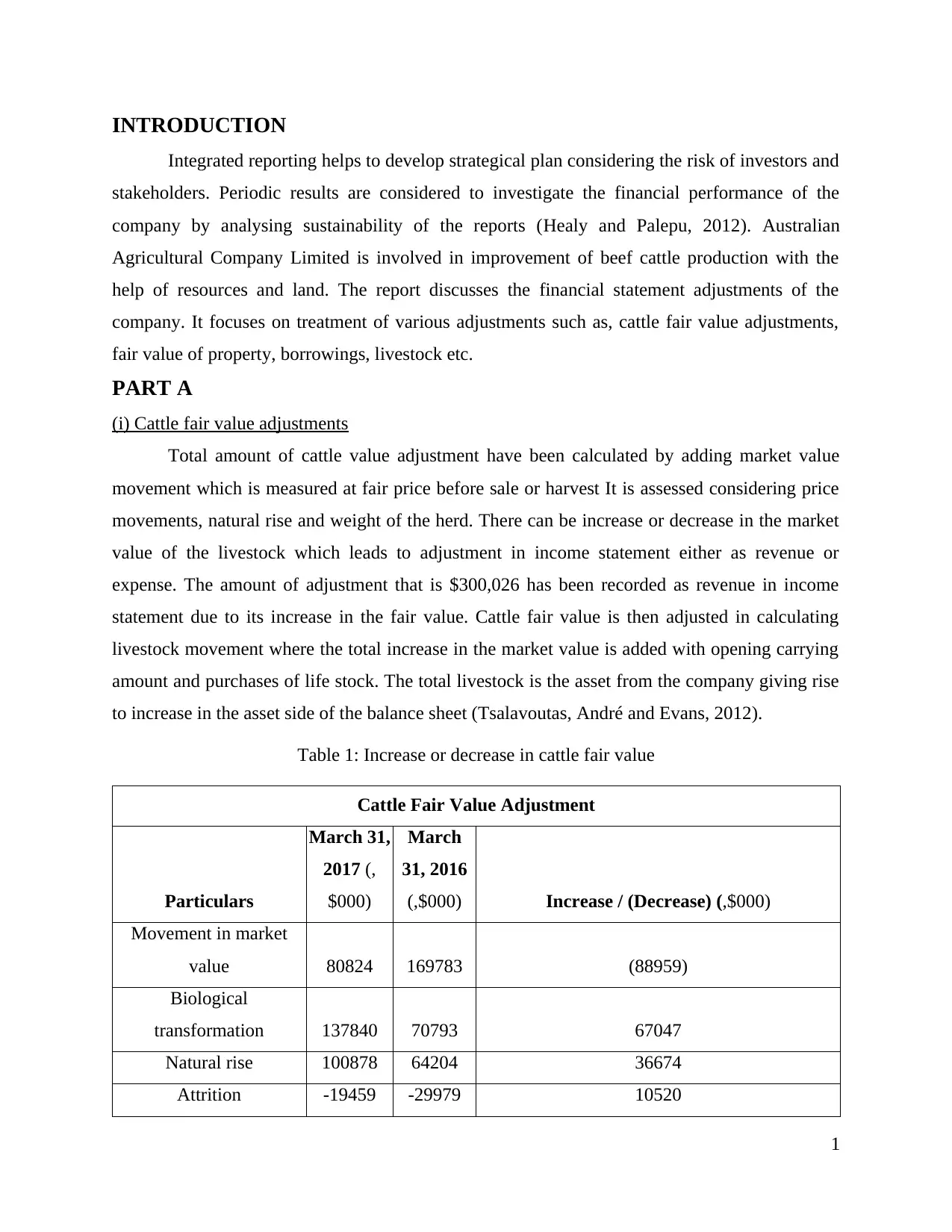

INTRODUCTION

Integrated reporting helps to develop strategical plan considering the risk of investors and

stakeholders. Periodic results are considered to investigate the financial performance of the

company by analysing sustainability of the reports (Healy and Palepu, 2012). Australian

Agricultural Company Limited is involved in improvement of beef cattle production with the

help of resources and land. The report discusses the financial statement adjustments of the

company. It focuses on treatment of various adjustments such as, cattle fair value adjustments,

fair value of property, borrowings, livestock etc.

PART A

(i) Cattle fair value adjustments

Total amount of cattle value adjustment have been calculated by adding market value

movement which is measured at fair price before sale or harvest It is assessed considering price

movements, natural rise and weight of the herd. There can be increase or decrease in the market

value of the livestock which leads to adjustment in income statement either as revenue or

expense. The amount of adjustment that is $300,026 has been recorded as revenue in income

statement due to its increase in the fair value. Cattle fair value is then adjusted in calculating

livestock movement where the total increase in the market value is added with opening carrying

amount and purchases of life stock. The total livestock is the asset from the company giving rise

to increase in the asset side of the balance sheet (Tsalavoutas, André and Evans, 2012).

Table 1: Increase or decrease in cattle fair value

Cattle Fair Value Adjustment

Particulars

March 31,

2017 (,

$000)

March

31, 2016

(,$000) Increase / (Decrease) (,$000)

Movement in market

value 80824 169783 (88959)

Biological

transformation 137840 70793 67047

Natural rise 100878 64204 36674

Attrition -19459 -29979 10520

1

Integrated reporting helps to develop strategical plan considering the risk of investors and

stakeholders. Periodic results are considered to investigate the financial performance of the

company by analysing sustainability of the reports (Healy and Palepu, 2012). Australian

Agricultural Company Limited is involved in improvement of beef cattle production with the

help of resources and land. The report discusses the financial statement adjustments of the

company. It focuses on treatment of various adjustments such as, cattle fair value adjustments,

fair value of property, borrowings, livestock etc.

PART A

(i) Cattle fair value adjustments

Total amount of cattle value adjustment have been calculated by adding market value

movement which is measured at fair price before sale or harvest It is assessed considering price

movements, natural rise and weight of the herd. There can be increase or decrease in the market

value of the livestock which leads to adjustment in income statement either as revenue or

expense. The amount of adjustment that is $300,026 has been recorded as revenue in income

statement due to its increase in the fair value. Cattle fair value is then adjusted in calculating

livestock movement where the total increase in the market value is added with opening carrying

amount and purchases of life stock. The total livestock is the asset from the company giving rise

to increase in the asset side of the balance sheet (Tsalavoutas, André and Evans, 2012).

Table 1: Increase or decrease in cattle fair value

Cattle Fair Value Adjustment

Particulars

March 31,

2017 (,

$000)

March

31, 2016

(,$000) Increase / (Decrease) (,$000)

Movement in market

value 80824 169783 (88959)

Biological

transformation 137840 70793 67047

Natural rise 100878 64204 36674

Attrition -19459 -29979 10520

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Others -57 -223 166

Total cattle fair value

adjustments 300026 274578 25448

There is an increase in cattle fair value which is revenue in nature and has lead to

increase in the assets of the company. It is a beneficial stage where the fair value of the cattle

have been increased.

(ii) Adjustments in fair value of property

Australian agriculture company have calculated the movement of fair value by

considering depreciation, amortisation and disposals. It has led to increase or decrease in fair

value of property for the company (Bodie, 2013). The closing balance of $667,860 have been

calculated considering the adjustment in their price for the year ending March 31, 2017. The

depreciation and amortisation of the property amounting to $19,032,000 are recorded in the

expense side of the income statement. Also, there is an increase in the revaluation price of the

properties amounting to $2,285,000 which are considered as revenue while recording in income

2

Movement in market value

Natural rise

Others-50000

0

50000

100000

150000

200000

250000

300000

350000

March 31, 2017

March 31, 2016

Illustration 1: Comparison of cattle fair value

Total cattle fair value

adjustments 300026 274578 25448

There is an increase in cattle fair value which is revenue in nature and has lead to

increase in the assets of the company. It is a beneficial stage where the fair value of the cattle

have been increased.

(ii) Adjustments in fair value of property

Australian agriculture company have calculated the movement of fair value by

considering depreciation, amortisation and disposals. It has led to increase or decrease in fair

value of property for the company (Bodie, 2013). The closing balance of $667,860 have been

calculated considering the adjustment in their price for the year ending March 31, 2017. The

depreciation and amortisation of the property amounting to $19,032,000 are recorded in the

expense side of the income statement. Also, there is an increase in the revaluation price of the

properties amounting to $2,285,000 which are considered as revenue while recording in income

2

Movement in market value

Natural rise

Others-50000

0

50000

100000

150000

200000

250000

300000

350000

March 31, 2017

March 31, 2016

Illustration 1: Comparison of cattle fair value

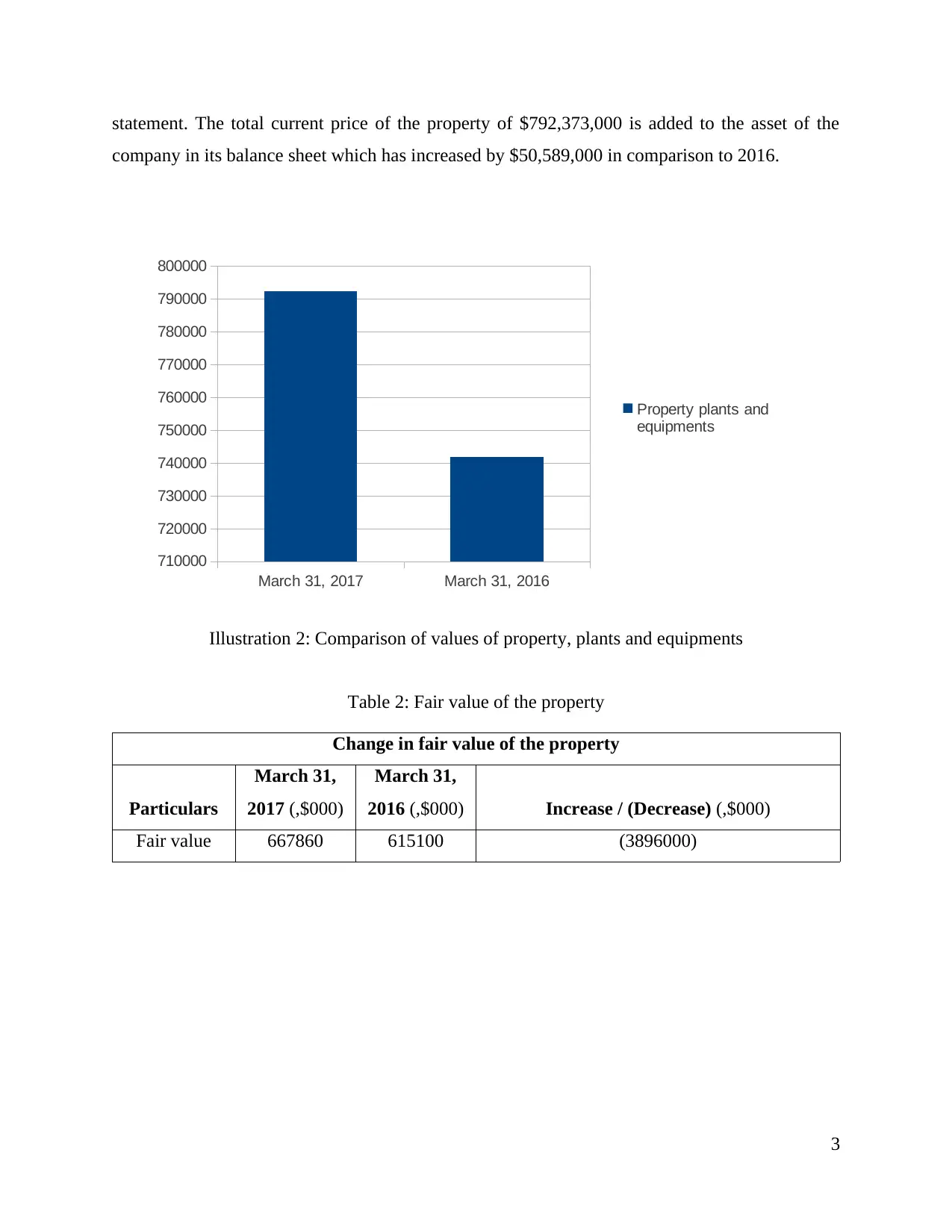

statement. The total current price of the property of $792,373,000 is added to the asset of the

company in its balance sheet which has increased by $50,589,000 in comparison to 2016.

Table 2: Fair value of the property

Change in fair value of the property

Particulars

March 31,

2017 (,$000)

March 31,

2016 (,$000) Increase / (Decrease) (,$000)

Fair value 667860 615100 (3896000)

3

March 31, 2017 March 31, 2016

710000

720000

730000

740000

750000

760000

770000

780000

790000

800000

Property plants and

equipments

Illustration 2: Comparison of values of property, plants and equipments

company in its balance sheet which has increased by $50,589,000 in comparison to 2016.

Table 2: Fair value of the property

Change in fair value of the property

Particulars

March 31,

2017 (,$000)

March 31,

2016 (,$000) Increase / (Decrease) (,$000)

Fair value 667860 615100 (3896000)

3

March 31, 2017 March 31, 2016

710000

720000

730000

740000

750000

760000

770000

780000

790000

800000

Property plants and

equipments

Illustration 2: Comparison of values of property, plants and equipments

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

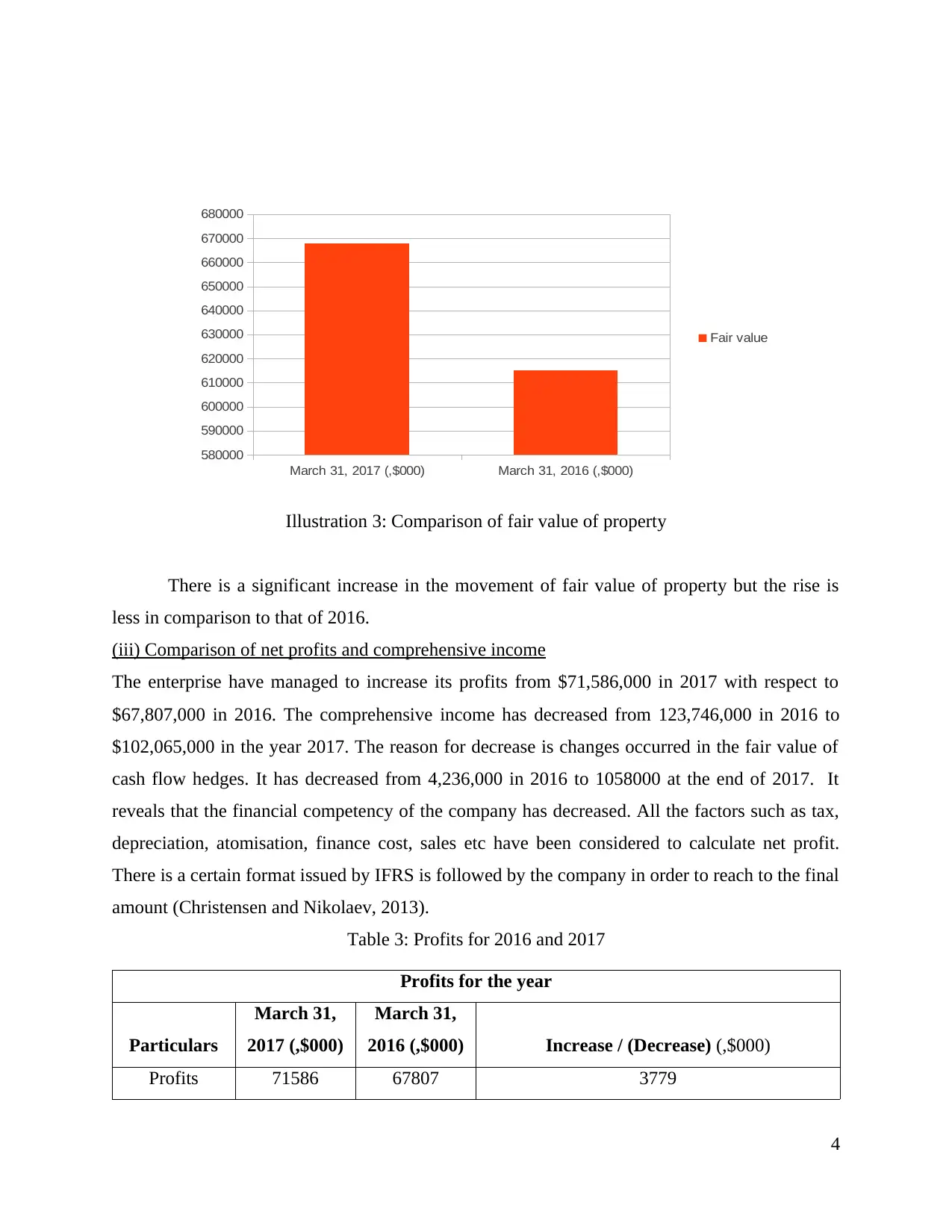

There is a significant increase in the movement of fair value of property but the rise is

less in comparison to that of 2016.

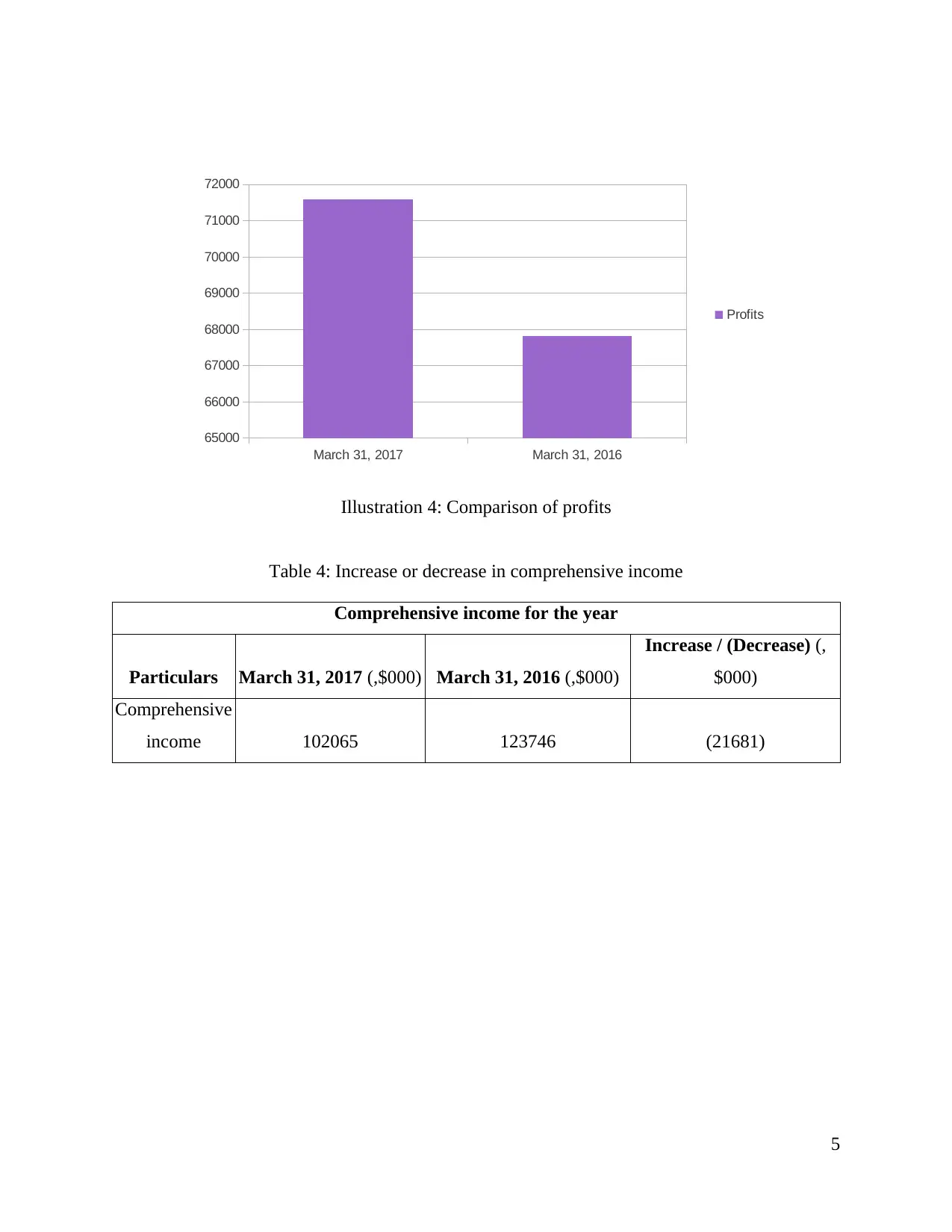

(iii) Comparison of net profits and comprehensive income

The enterprise have managed to increase its profits from $71,586,000 in 2017 with respect to

$67,807,000 in 2016. The comprehensive income has decreased from 123,746,000 in 2016 to

$102,065,000 in the year 2017. The reason for decrease is changes occurred in the fair value of

cash flow hedges. It has decreased from 4,236,000 in 2016 to 1058000 at the end of 2017. It

reveals that the financial competency of the company has decreased. All the factors such as tax,

depreciation, atomisation, finance cost, sales etc have been considered to calculate net profit.

There is a certain format issued by IFRS is followed by the company in order to reach to the final

amount (Christensen and Nikolaev, 2013).

Table 3: Profits for 2016 and 2017

Profits for the year

Particulars

March 31,

2017 (,$000)

March 31,

2016 (,$000) Increase / (Decrease) (,$000)

Profits 71586 67807 3779

4

March 31, 2017 (,$000) March 31, 2016 (,$000)

580000

590000

600000

610000

620000

630000

640000

650000

660000

670000

680000

Fair value

Illustration 3: Comparison of fair value of property

less in comparison to that of 2016.

(iii) Comparison of net profits and comprehensive income

The enterprise have managed to increase its profits from $71,586,000 in 2017 with respect to

$67,807,000 in 2016. The comprehensive income has decreased from 123,746,000 in 2016 to

$102,065,000 in the year 2017. The reason for decrease is changes occurred in the fair value of

cash flow hedges. It has decreased from 4,236,000 in 2016 to 1058000 at the end of 2017. It

reveals that the financial competency of the company has decreased. All the factors such as tax,

depreciation, atomisation, finance cost, sales etc have been considered to calculate net profit.

There is a certain format issued by IFRS is followed by the company in order to reach to the final

amount (Christensen and Nikolaev, 2013).

Table 3: Profits for 2016 and 2017

Profits for the year

Particulars

March 31,

2017 (,$000)

March 31,

2016 (,$000) Increase / (Decrease) (,$000)

Profits 71586 67807 3779

4

March 31, 2017 (,$000) March 31, 2016 (,$000)

580000

590000

600000

610000

620000

630000

640000

650000

660000

670000

680000

Fair value

Illustration 3: Comparison of fair value of property

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

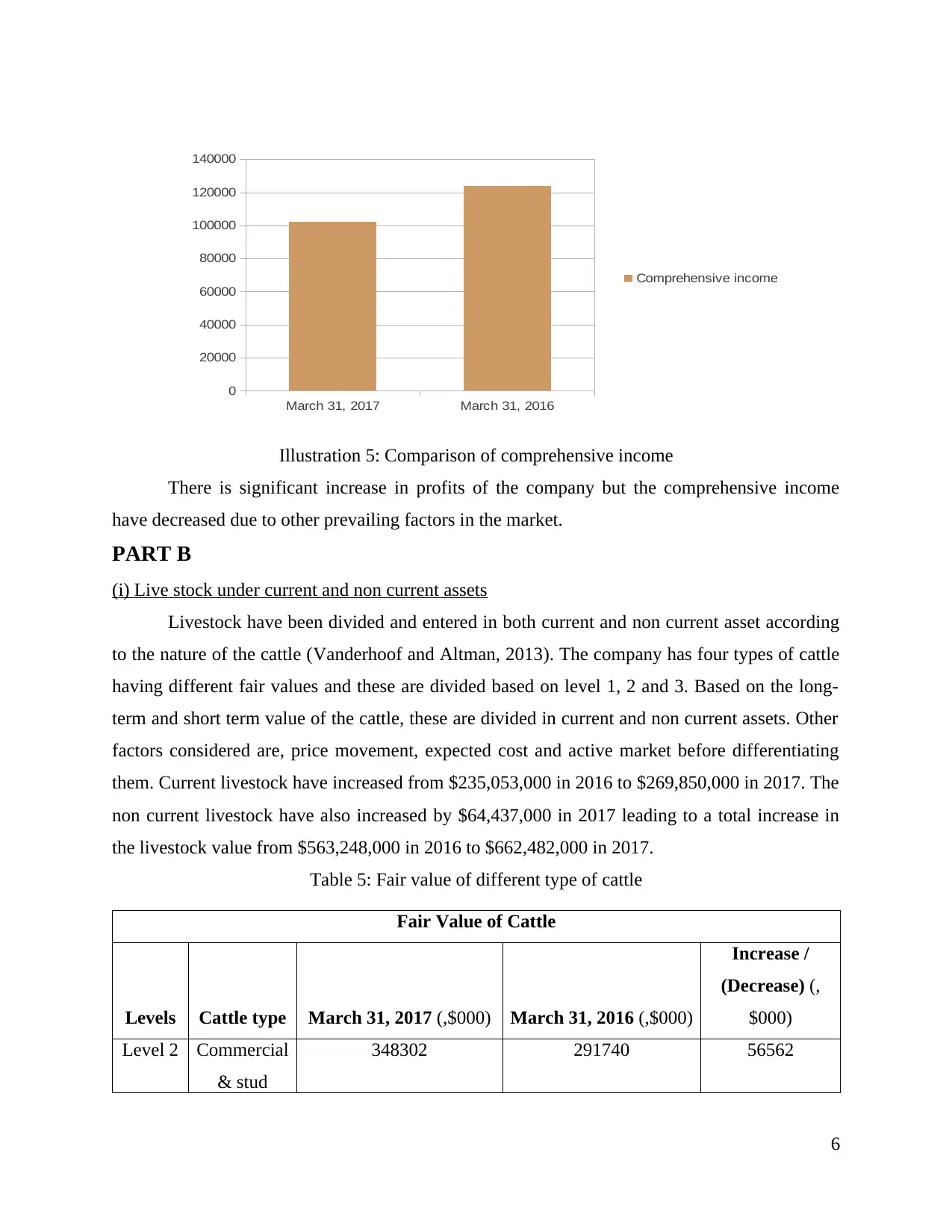

Table 4: Increase or decrease in comprehensive income

Comprehensive income for the year

Particulars March 31, 2017 (,$000) March 31, 2016 (,$000)

Increase / (Decrease) (,

$000)

Comprehensive

income 102065 123746 (21681)

5

March 31, 2017 March 31, 2016

65000

66000

67000

68000

69000

70000

71000

72000

Profits

Illustration 4: Comparison of profits

Comprehensive income for the year

Particulars March 31, 2017 (,$000) March 31, 2016 (,$000)

Increase / (Decrease) (,

$000)

Comprehensive

income 102065 123746 (21681)

5

March 31, 2017 March 31, 2016

65000

66000

67000

68000

69000

70000

71000

72000

Profits

Illustration 4: Comparison of profits

There is significant increase in profits of the company but the comprehensive income

have decreased due to other prevailing factors in the market.

PART B

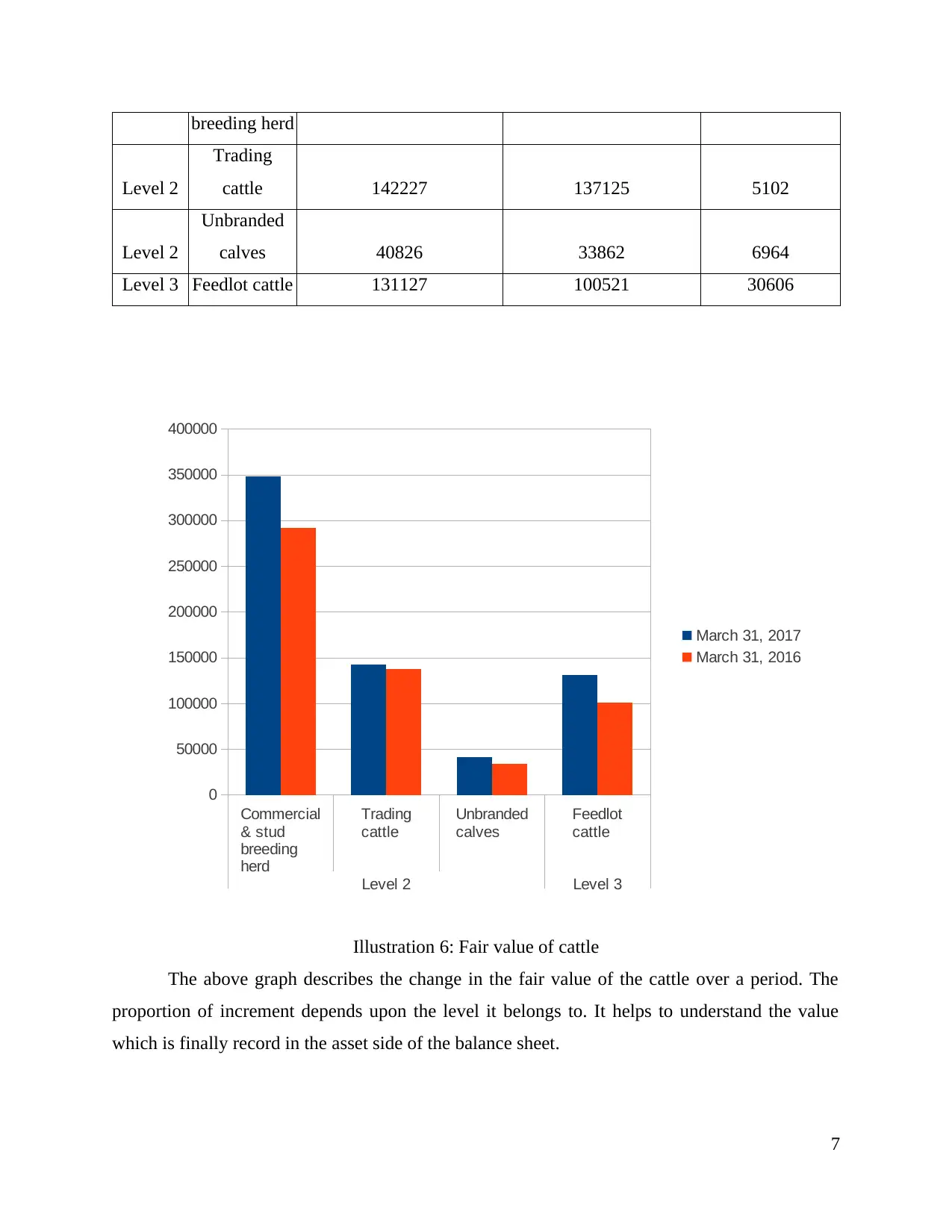

(i) Live stock under current and non current assets

Livestock have been divided and entered in both current and non current asset according

to the nature of the cattle (Vanderhoof and Altman, 2013). The company has four types of cattle

having different fair values and these are divided based on level 1, 2 and 3. Based on the long-

term and short term value of the cattle, these are divided in current and non current assets. Other

factors considered are, price movement, expected cost and active market before differentiating

them. Current livestock have increased from $235,053,000 in 2016 to $269,850,000 in 2017. The

non current livestock have also increased by $64,437,000 in 2017 leading to a total increase in

the livestock value from $563,248,000 in 2016 to $662,482,000 in 2017.

Table 5: Fair value of different type of cattle

Fair Value of Cattle

Levels Cattle type March 31, 2017 (,$000) March 31, 2016 (,$000)

Increase /

(Decrease) (,

$000)

Level 2 Commercial

& stud

348302 291740 56562

6

March 31, 2017 March 31, 2016

0

20000

40000

60000

80000

100000

120000

140000

Comprehensive income

Illustration 5: Comparison of comprehensive income

have decreased due to other prevailing factors in the market.

PART B

(i) Live stock under current and non current assets

Livestock have been divided and entered in both current and non current asset according

to the nature of the cattle (Vanderhoof and Altman, 2013). The company has four types of cattle

having different fair values and these are divided based on level 1, 2 and 3. Based on the long-

term and short term value of the cattle, these are divided in current and non current assets. Other

factors considered are, price movement, expected cost and active market before differentiating

them. Current livestock have increased from $235,053,000 in 2016 to $269,850,000 in 2017. The

non current livestock have also increased by $64,437,000 in 2017 leading to a total increase in

the livestock value from $563,248,000 in 2016 to $662,482,000 in 2017.

Table 5: Fair value of different type of cattle

Fair Value of Cattle

Levels Cattle type March 31, 2017 (,$000) March 31, 2016 (,$000)

Increase /

(Decrease) (,

$000)

Level 2 Commercial

& stud

348302 291740 56562

6

March 31, 2017 March 31, 2016

0

20000

40000

60000

80000

100000

120000

140000

Comprehensive income

Illustration 5: Comparison of comprehensive income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

breeding herd

Level 2

Trading

cattle 142227 137125 5102

Level 2

Unbranded

calves 40826 33862 6964

Level 3 Feedlot cattle 131127 100521 30606

The above graph describes the change in the fair value of the cattle over a period. The

proportion of increment depends upon the level it belongs to. It helps to understand the value

which is finally record in the asset side of the balance sheet.

7

Commercial

& stud

breeding

herd

Trading

cattle

Unbranded

calves

Feedlot

cattle

Level 2 Level 3

0

50000

100000

150000

200000

250000

300000

350000

400000

March 31, 2017

March 31, 2016

Illustration 6: Fair value of cattle

Level 2

Trading

cattle 142227 137125 5102

Level 2

Unbranded

calves 40826 33862 6964

Level 3 Feedlot cattle 131127 100521 30606

The above graph describes the change in the fair value of the cattle over a period. The

proportion of increment depends upon the level it belongs to. It helps to understand the value

which is finally record in the asset side of the balance sheet.

7

Commercial

& stud

breeding

herd

Trading

cattle

Unbranded

calves

Feedlot

cattle

Level 2 Level 3

0

50000

100000

150000

200000

250000

300000

350000

400000

March 31, 2017

March 31, 2016

Illustration 6: Fair value of cattle

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

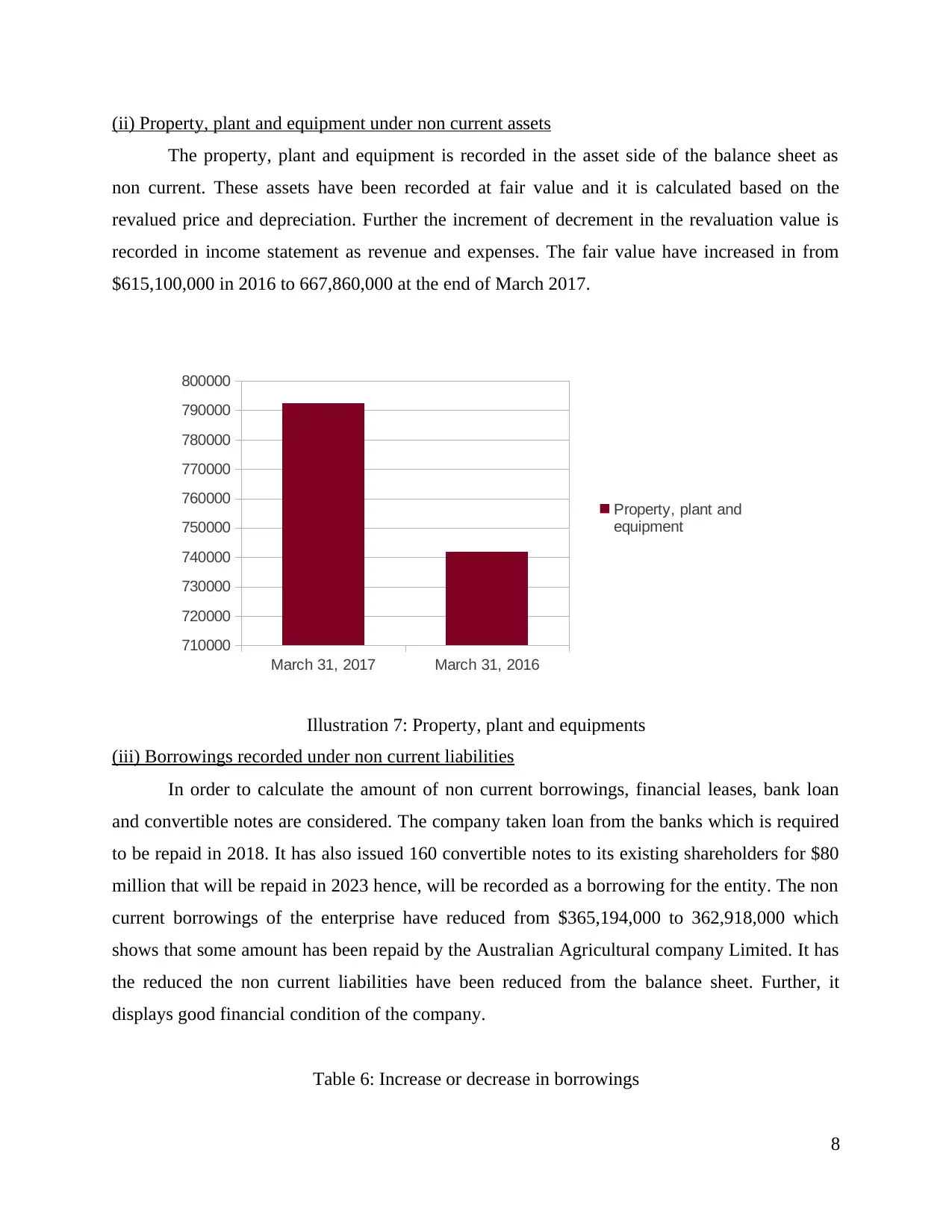

(ii) Property, plant and equipment under non current assets

The property, plant and equipment is recorded in the asset side of the balance sheet as

non current. These assets have been recorded at fair value and it is calculated based on the

revalued price and depreciation. Further the increment of decrement in the revaluation value is

recorded in income statement as revenue and expenses. The fair value have increased in from

$615,100,000 in 2016 to 667,860,000 at the end of March 2017.

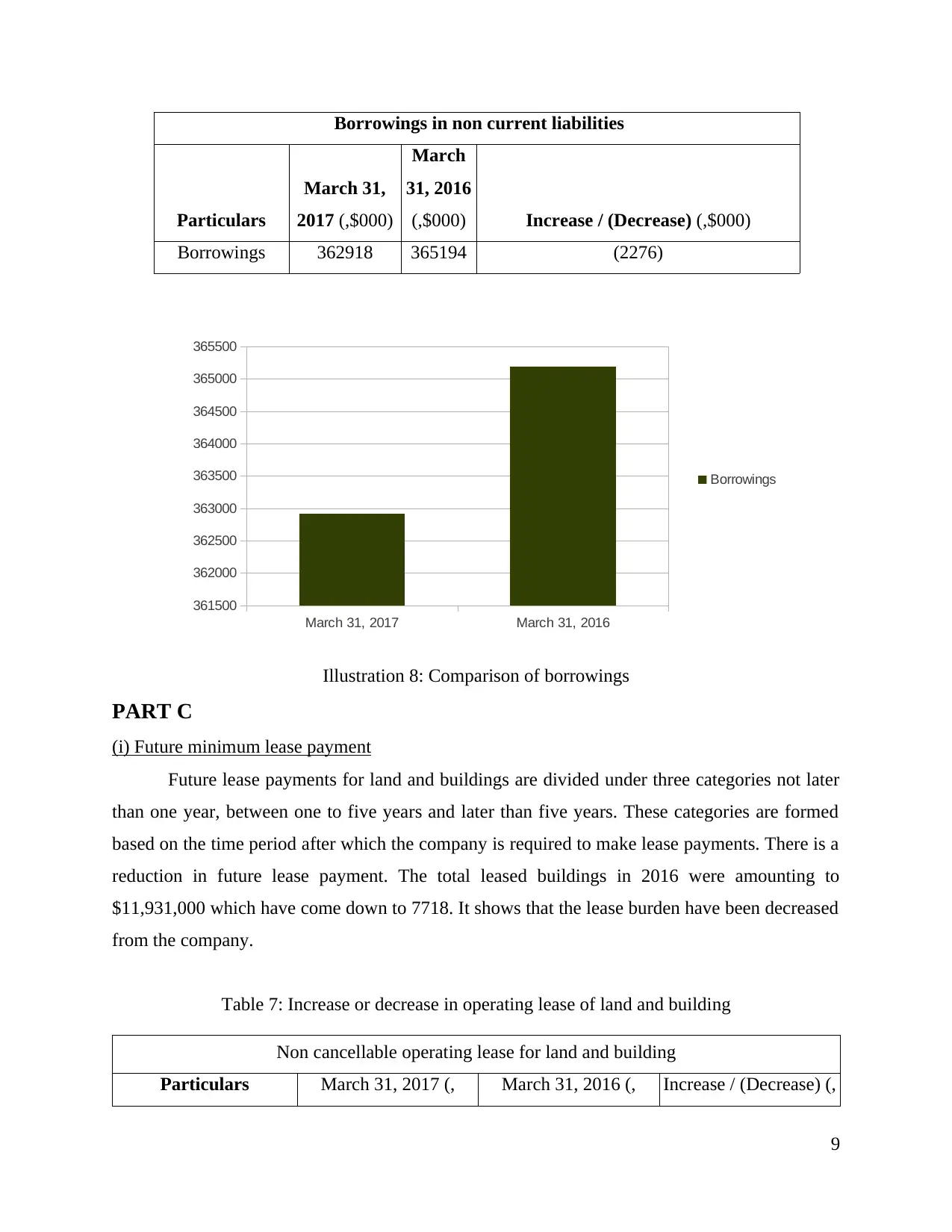

(iii) Borrowings recorded under non current liabilities

In order to calculate the amount of non current borrowings, financial leases, bank loan

and convertible notes are considered. The company taken loan from the banks which is required

to be repaid in 2018. It has also issued 160 convertible notes to its existing shareholders for $80

million that will be repaid in 2023 hence, will be recorded as a borrowing for the entity. The non

current borrowings of the enterprise have reduced from $365,194,000 to 362,918,000 which

shows that some amount has been repaid by the Australian Agricultural company Limited. It has

the reduced the non current liabilities have been reduced from the balance sheet. Further, it

displays good financial condition of the company.

Table 6: Increase or decrease in borrowings

8

March 31, 2017 March 31, 2016

710000

720000

730000

740000

750000

760000

770000

780000

790000

800000

Property, plant and

equipment

Illustration 7: Property, plant and equipments

The property, plant and equipment is recorded in the asset side of the balance sheet as

non current. These assets have been recorded at fair value and it is calculated based on the

revalued price and depreciation. Further the increment of decrement in the revaluation value is

recorded in income statement as revenue and expenses. The fair value have increased in from

$615,100,000 in 2016 to 667,860,000 at the end of March 2017.

(iii) Borrowings recorded under non current liabilities

In order to calculate the amount of non current borrowings, financial leases, bank loan

and convertible notes are considered. The company taken loan from the banks which is required

to be repaid in 2018. It has also issued 160 convertible notes to its existing shareholders for $80

million that will be repaid in 2023 hence, will be recorded as a borrowing for the entity. The non

current borrowings of the enterprise have reduced from $365,194,000 to 362,918,000 which

shows that some amount has been repaid by the Australian Agricultural company Limited. It has

the reduced the non current liabilities have been reduced from the balance sheet. Further, it

displays good financial condition of the company.

Table 6: Increase or decrease in borrowings

8

March 31, 2017 March 31, 2016

710000

720000

730000

740000

750000

760000

770000

780000

790000

800000

Property, plant and

equipment

Illustration 7: Property, plant and equipments

Borrowings in non current liabilities

Particulars

March 31,

2017 (,$000)

March

31, 2016

(,$000) Increase / (Decrease) (,$000)

Borrowings 362918 365194 (2276)

PART C

(i) Future minimum lease payment

Future lease payments for land and buildings are divided under three categories not later

than one year, between one to five years and later than five years. These categories are formed

based on the time period after which the company is required to make lease payments. There is a

reduction in future lease payment. The total leased buildings in 2016 were amounting to

$11,931,000 which have come down to 7718. It shows that the lease burden have been decreased

from the company.

Table 7: Increase or decrease in operating lease of land and building

Non cancellable operating lease for land and building

Particulars March 31, 2017 (, March 31, 2016 (, Increase / (Decrease) (,

9

March 31, 2017 March 31, 2016

361500

362000

362500

363000

363500

364000

364500

365000

365500

Borrowings

Illustration 8: Comparison of borrowings

Particulars

March 31,

2017 (,$000)

March

31, 2016

(,$000) Increase / (Decrease) (,$000)

Borrowings 362918 365194 (2276)

PART C

(i) Future minimum lease payment

Future lease payments for land and buildings are divided under three categories not later

than one year, between one to five years and later than five years. These categories are formed

based on the time period after which the company is required to make lease payments. There is a

reduction in future lease payment. The total leased buildings in 2016 were amounting to

$11,931,000 which have come down to 7718. It shows that the lease burden have been decreased

from the company.

Table 7: Increase or decrease in operating lease of land and building

Non cancellable operating lease for land and building

Particulars March 31, 2017 (, March 31, 2016 (, Increase / (Decrease) (,

9

March 31, 2017 March 31, 2016

361500

362000

362500

363000

363500

364000

364500

365000

365500

Borrowings

Illustration 8: Comparison of borrowings

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.