ECO511 Economics for Business: Australian Banking Sector Analysis

VerifiedAdded on 2020/09/09

|9

|2459

|41

Essay

AI Summary

This essay, submitted for ECO511, analyzes the Australian banking sector, which is dominated by four major banks, forming an oligopoly. The study explores the issues arising from this market structure, including price rigidity and the potential for anti-competitive practices. The analysis applies the theory of non-collusive oligopoly, specifically the kinked demand curve, to explain price behavior and market dynamics. Evidence from various sources is used to support the arguments. The essay evaluates the current situation, proposing strategies for smaller banks to compete effectively, such as leveraging the open banking system and strategic pricing. The conclusion emphasizes the need to balance the dominance of the big banks with the sustainability of smaller institutions and the benefit of consumers. The essay suggests that a non-collusive oligopoly approach and the open banking system can enhance competition and customer choice within the Australian banking sector. The essay also includes a figure illustrating the non-collusive oligopoly market with a kinked demand curve.

ECO511 - Economics for Business

Assignment 4: Essay Question

Student Name:

Student Id:

Assignment 4: Essay Question

Student Name:

Student Id:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................2

Analysis...........................................................................................................................................3

Theory of non-collusive oligopoly..............................................................................................3

Issues faced in Australian banking sector........................................................................................3

Evidences related to Australian banking sector...............................................................................4

Evaluation of the situation based on theory.....................................................................................5

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

List of figure:

Figure 1: Non-collusive Oligopoly Market (Kinked Demand Curve).............................................6

1

Introduction......................................................................................................................................2

Analysis...........................................................................................................................................3

Theory of non-collusive oligopoly..............................................................................................3

Issues faced in Australian banking sector........................................................................................3

Evidences related to Australian banking sector...............................................................................4

Evaluation of the situation based on theory.....................................................................................5

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

List of figure:

Figure 1: Non-collusive Oligopoly Market (Kinked Demand Curve).............................................6

1

Introduction

The studies have indicated the fact that the four major banks ANZ Bank, Westpac, National

Australia Bank and Commonwealth Bank of Australia are assumed to control around 75% of the

market share. In fact, the banks are also expected to experience lower funding costs as compared

to small rivals (Bakir, 2019). It has also been pointed out that financial technology professionals

have not been mature enough to deal with the issue of competition among the large and small

banks. The power of each of the larger banks needs to be reviewed in order to take control of the

competitive scenario. The situation can be evaluated on the basis of the non-collusive oligopoly

theory and evidence about the situation would be gathered from various media reports (Apergis

& Cooray, 2015). The aim of the research is to suggest a suitable strategy so that the Australian

banks are able to operate as independent entities and they are able to serve large number of

customers. The research also has the scope to relate the theory with that of the scenario so that

the performance of each of the banks can be measured despite the competition.

2

The studies have indicated the fact that the four major banks ANZ Bank, Westpac, National

Australia Bank and Commonwealth Bank of Australia are assumed to control around 75% of the

market share. In fact, the banks are also expected to experience lower funding costs as compared

to small rivals (Bakir, 2019). It has also been pointed out that financial technology professionals

have not been mature enough to deal with the issue of competition among the large and small

banks. The power of each of the larger banks needs to be reviewed in order to take control of the

competitive scenario. The situation can be evaluated on the basis of the non-collusive oligopoly

theory and evidence about the situation would be gathered from various media reports (Apergis

& Cooray, 2015). The aim of the research is to suggest a suitable strategy so that the Australian

banks are able to operate as independent entities and they are able to serve large number of

customers. The research also has the scope to relate the theory with that of the scenario so that

the performance of each of the banks can be measured despite the competition.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis

Theory of non-collusive oligopoly

Selmier (2016) has indicated the fact that one of the most significant features of oligopoly

market is that of price rigidity and so in order to explain this phenomenon kinked demand curve

is used. The concept of kinked demand curve arises as a result of the unconventional behaviour

of the sellers. The situation is that if the seller raises the price of a particular product then the

rival is not expected to follow the seller (Selmier, 2016). On the other hand, Bakir, (2019) argued

that if a particular firm reduces the price of the product then the other firm is likely to follow that

firm. It can be stated that every price level is expected to be matched by an equivalent price

level. As a result, the demand curve is assumed to be kinked. It can be stated that the non-

collusive oligopoly involves entry barriers for the new firms within the market (Bakir, 2019).

Additionally, the firms also choose product banding and differentiation so that they are able to

ensure high customer satisfaction. However, it can be stated that the rival firms are

interdependent on each other while taking important decisions regarding the setting of prices

within the economy (Selmier, 2016). (Taylor & Tyers, 2017) stated that it is expected that the

firms would formulate their own strategies and the rival firms would react to these strategies

appropriately. There would be no collusion among the firms participating in the competition.

Issues faced in the Australian banking sector

The big four Australian banks are expected to dominate over time as they own combined assets

worth $3.6 trillion which is twice the value of economic output of Australia (Financial Times,

2019). Around 80% of the mortgage borrowers are likely to have borrowed from one of the big

four banks and they have also made the financial sector of Australia to be more concentrated

(Financial Times, 2019). Some of the analysts have been pointing out the credit crunch that is

likely to reduce the level of economic growth within Australia and the country might experience

recession (Taylor & Tyers, 2017). The Australian banks are assumed to experience bad debt with

falling house prices in different parts of Australia. The banks may not be able to recover the full

volume of the loans even by selling the homes of the borrowers who have defaulted. The studies

have also indicated that Australian government has encouraged the other banks to challenge the

situation of oligopoly in Australian banking sector after it has been pointed out by the top

3

Theory of non-collusive oligopoly

Selmier (2016) has indicated the fact that one of the most significant features of oligopoly

market is that of price rigidity and so in order to explain this phenomenon kinked demand curve

is used. The concept of kinked demand curve arises as a result of the unconventional behaviour

of the sellers. The situation is that if the seller raises the price of a particular product then the

rival is not expected to follow the seller (Selmier, 2016). On the other hand, Bakir, (2019) argued

that if a particular firm reduces the price of the product then the other firm is likely to follow that

firm. It can be stated that every price level is expected to be matched by an equivalent price

level. As a result, the demand curve is assumed to be kinked. It can be stated that the non-

collusive oligopoly involves entry barriers for the new firms within the market (Bakir, 2019).

Additionally, the firms also choose product banding and differentiation so that they are able to

ensure high customer satisfaction. However, it can be stated that the rival firms are

interdependent on each other while taking important decisions regarding the setting of prices

within the economy (Selmier, 2016). (Taylor & Tyers, 2017) stated that it is expected that the

firms would formulate their own strategies and the rival firms would react to these strategies

appropriately. There would be no collusion among the firms participating in the competition.

Issues faced in the Australian banking sector

The big four Australian banks are expected to dominate over time as they own combined assets

worth $3.6 trillion which is twice the value of economic output of Australia (Financial Times,

2019). Around 80% of the mortgage borrowers are likely to have borrowed from one of the big

four banks and they have also made the financial sector of Australia to be more concentrated

(Financial Times, 2019). Some of the analysts have been pointing out the credit crunch that is

likely to reduce the level of economic growth within Australia and the country might experience

recession (Taylor & Tyers, 2017). The Australian banks are assumed to experience bad debt with

falling house prices in different parts of Australia. The banks may not be able to recover the full

volume of the loans even by selling the homes of the borrowers who have defaulted. The studies

have also indicated that Australian government has encouraged the other banks to challenge the

situation of oligopoly in Australian banking sector after it has been pointed out by the top

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

economic advisor that the market dominance of the big four lenders has been harmful to the

customers (Financial Times, 2019).

The researchers have pointed out the fact that the big four commercial banks have been

constantly exploiting the power they over more than three-quarters of the country’s lending

capacity. The credit card business of the banks has been providing its customers with inferior

products as per the government report that has been released by Productivity Commission. The

banking sector is assumed to experience intense scrutiny by the Royal Commission regarding the

illegal activities that they have been practising overtime (Xu, Gan & Hu, 2015). The big four

banks have the tendency to pass on higher cost towards the customers and also dictate the prices

of the products as per their market power. Additionally, it has also been indicted by the analysts

that the banks have been well-placed so that they are able to offer different products to the

customers at competitive prices (Financial Times, 2019). The lower funding cost, scope and size

have boosted their share so that they are able to gain adequate access to the offshore funding

rates (Xu, Gan & Hu, 2015). The non-bank institutions and the micro-lenders are forced to

follow the prices that are set by the big four banks and there is less competitive threat posed by

the small banks. The increased dominance of the big four banks have forced the small banks to

merge and the banking licenses have plunged during the increase in demand.

Evidence related to the Australian banking sector

Evidences have indicated the fact that the credit rating agencies might play a key role in

increasing the dominance of the Australian banks indicating the possibility of government

bailouts. The studies have indicated that the government is working in this field so as to enable

more market entrants after easing the restrictions on foreign banks (Financial Times, 2019). The

analysts have stated that the big four banks in Australia take customers for granted and charge

high prices for the products. Market competition is also likely to have reduced the power of the

small banks and they were unable to carry out their business appropriately. The customers were

also charged with some of the fees that were never provided to them (Reuters, 2018). The

evidence has been gathered from authentic sources related to the Australian banking sector

which states that the big four banks have been exploiting the customer's overtime by charging

high prices for the products and deviating from the quality of services that are supposed to be

4

customers (Financial Times, 2019).

The researchers have pointed out the fact that the big four commercial banks have been

constantly exploiting the power they over more than three-quarters of the country’s lending

capacity. The credit card business of the banks has been providing its customers with inferior

products as per the government report that has been released by Productivity Commission. The

banking sector is assumed to experience intense scrutiny by the Royal Commission regarding the

illegal activities that they have been practising overtime (Xu, Gan & Hu, 2015). The big four

banks have the tendency to pass on higher cost towards the customers and also dictate the prices

of the products as per their market power. Additionally, it has also been indicted by the analysts

that the banks have been well-placed so that they are able to offer different products to the

customers at competitive prices (Financial Times, 2019). The lower funding cost, scope and size

have boosted their share so that they are able to gain adequate access to the offshore funding

rates (Xu, Gan & Hu, 2015). The non-bank institutions and the micro-lenders are forced to

follow the prices that are set by the big four banks and there is less competitive threat posed by

the small banks. The increased dominance of the big four banks have forced the small banks to

merge and the banking licenses have plunged during the increase in demand.

Evidence related to the Australian banking sector

Evidences have indicated the fact that the credit rating agencies might play a key role in

increasing the dominance of the Australian banks indicating the possibility of government

bailouts. The studies have indicated that the government is working in this field so as to enable

more market entrants after easing the restrictions on foreign banks (Financial Times, 2019). The

analysts have stated that the big four banks in Australia take customers for granted and charge

high prices for the products. Market competition is also likely to have reduced the power of the

small banks and they were unable to carry out their business appropriately. The customers were

also charged with some of the fees that were never provided to them (Reuters, 2018). The

evidence has been gathered from authentic sources related to the Australian banking sector

which states that the big four banks have been exploiting the customer's overtime by charging

high prices for the products and deviating from the quality of services that are supposed to be

4

provided. Critics have also highlighted that the four pillar policy involves government guarantee

to the big four banks regarding the reduction in cost of funding and also control the entry of

small banks within the economy.

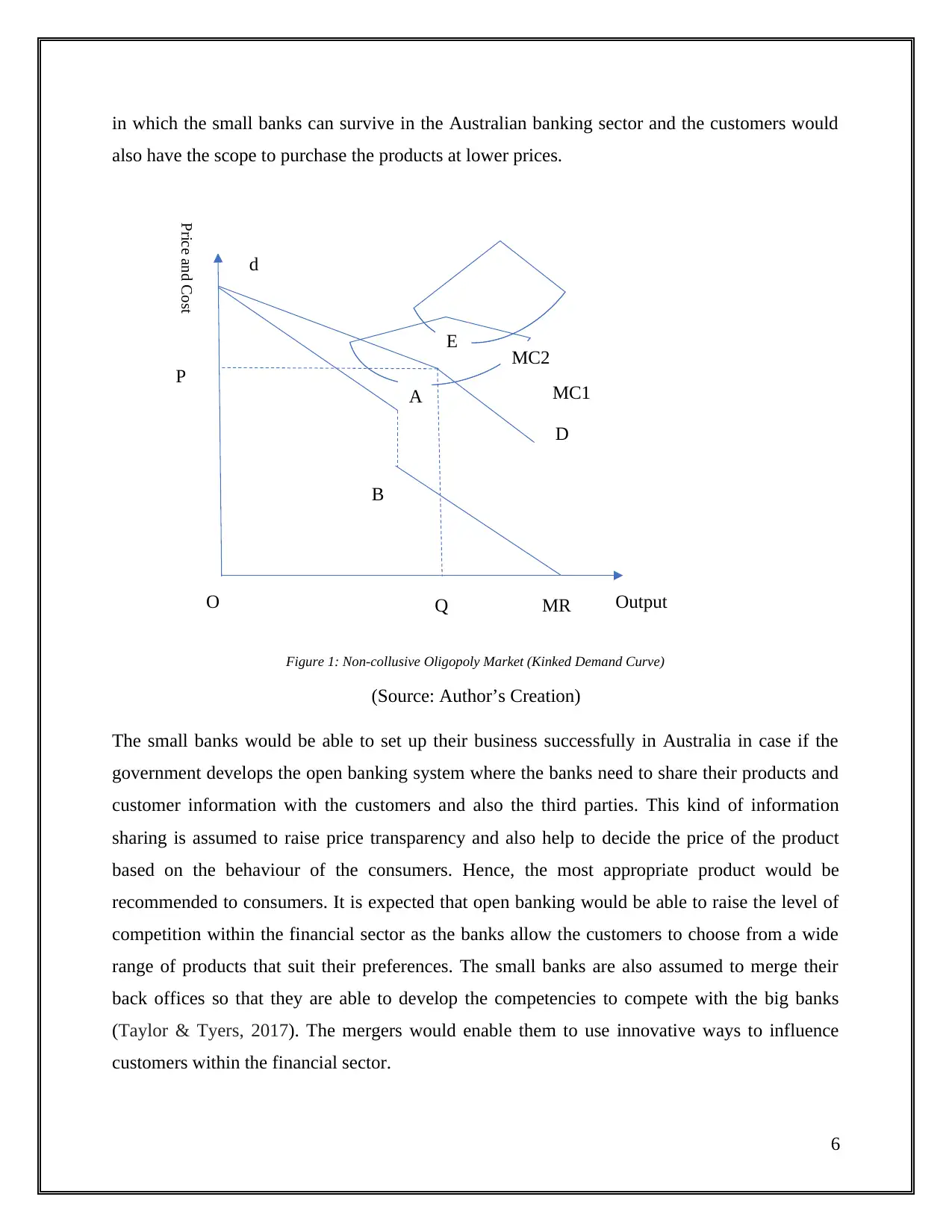

Evaluation of the situation based on theory

The study has indicated the fact that big four banks have formed an oligopoly market structure

within the Australian banking sector which is posing a problem to the local customers. The

market dominance of the big four financial institutions needs to be controlled so that overall

performance of the banking sector can be improved (Financial Times, 2019). There are a series

of initiatives that the small banks need to adopt so as to sustain within the Australian banking

sector despite the healthy competition posed by the big four banks.

For instance, it can be assumed that the prevailing price of the oligopoly product within the

market is OP or QE. In case if one of the big four banks raises the price of the product above OP

then the small banks must not react to the change in price. As a result of the high price charged

by the bank, the customers would automatically deviate to the other products that are offered at

low rates. As a result, the sale of a big bank would reduce considerably (Bakir, 2019). The

demand curve dE is found to be price elastic. On the contrary, if the big bank reduces the price of

the product below QE, then the small banks are expected to reduce the price of the banking

products further. It can be indicated that the demand curve ED is inelastic. By reducing the price

of the banking products, the small banks would be in a profitable position with the increase in

number of customer base. It can further be stated that at an output lower than OQ, the MR curve

dA is likely to be corresponding to dE part of the AR curve. Moreover, if the output is found to

be larger than OQ, then the MR curve BMR would be corresponding to the AR curve ED. It can

be observed that there is a slight discontinuity between the points A and B. It can be inferred that

MR curve is believed to be verticle between these points (Bakir, 2019). The studies depict the

fact that equilibrium can be attained when the MC curve passes through the discontinuous region

of the MR curve. Hence, OQ amount of equilibrium products would be offered at OP price. As

far as the cost is concerned MC curve would shift from MC1 to MC2. The resulting price and the

level of output would remain unchanged. This also indicates the stickiness of the prices as the

oligopoly markets are more stable as compared to the level of cost. This can be an effective way

5

to the big four banks regarding the reduction in cost of funding and also control the entry of

small banks within the economy.

Evaluation of the situation based on theory

The study has indicated the fact that big four banks have formed an oligopoly market structure

within the Australian banking sector which is posing a problem to the local customers. The

market dominance of the big four financial institutions needs to be controlled so that overall

performance of the banking sector can be improved (Financial Times, 2019). There are a series

of initiatives that the small banks need to adopt so as to sustain within the Australian banking

sector despite the healthy competition posed by the big four banks.

For instance, it can be assumed that the prevailing price of the oligopoly product within the

market is OP or QE. In case if one of the big four banks raises the price of the product above OP

then the small banks must not react to the change in price. As a result of the high price charged

by the bank, the customers would automatically deviate to the other products that are offered at

low rates. As a result, the sale of a big bank would reduce considerably (Bakir, 2019). The

demand curve dE is found to be price elastic. On the contrary, if the big bank reduces the price of

the product below QE, then the small banks are expected to reduce the price of the banking

products further. It can be indicated that the demand curve ED is inelastic. By reducing the price

of the banking products, the small banks would be in a profitable position with the increase in

number of customer base. It can further be stated that at an output lower than OQ, the MR curve

dA is likely to be corresponding to dE part of the AR curve. Moreover, if the output is found to

be larger than OQ, then the MR curve BMR would be corresponding to the AR curve ED. It can

be observed that there is a slight discontinuity between the points A and B. It can be inferred that

MR curve is believed to be verticle between these points (Bakir, 2019). The studies depict the

fact that equilibrium can be attained when the MC curve passes through the discontinuous region

of the MR curve. Hence, OQ amount of equilibrium products would be offered at OP price. As

far as the cost is concerned MC curve would shift from MC1 to MC2. The resulting price and the

level of output would remain unchanged. This also indicates the stickiness of the prices as the

oligopoly markets are more stable as compared to the level of cost. This can be an effective way

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Output

Price and Cost

E

D

d

A

B

P

O Q MR

MC2

MC1

in which the small banks can survive in the Australian banking sector and the customers would

also have the scope to purchase the products at lower prices.

Figure 1: Non-collusive Oligopoly Market (Kinked Demand Curve)

(Source: Author’s Creation)

The small banks would be able to set up their business successfully in Australia in case if the

government develops the open banking system where the banks need to share their products and

customer information with the customers and also the third parties. This kind of information

sharing is assumed to raise price transparency and also help to decide the price of the product

based on the behaviour of the consumers. Hence, the most appropriate product would be

recommended to consumers. It is expected that open banking would be able to raise the level of

competition within the financial sector as the banks allow the customers to choose from a wide

range of products that suit their preferences. The small banks are also assumed to merge their

back offices so that they are able to develop the competencies to compete with the big banks

(Taylor & Tyers, 2017). The mergers would enable them to use innovative ways to influence

customers within the financial sector.

6

Price and Cost

E

D

d

A

B

P

O Q MR

MC2

MC1

in which the small banks can survive in the Australian banking sector and the customers would

also have the scope to purchase the products at lower prices.

Figure 1: Non-collusive Oligopoly Market (Kinked Demand Curve)

(Source: Author’s Creation)

The small banks would be able to set up their business successfully in Australia in case if the

government develops the open banking system where the banks need to share their products and

customer information with the customers and also the third parties. This kind of information

sharing is assumed to raise price transparency and also help to decide the price of the product

based on the behaviour of the consumers. Hence, the most appropriate product would be

recommended to consumers. It is expected that open banking would be able to raise the level of

competition within the financial sector as the banks allow the customers to choose from a wide

range of products that suit their preferences. The small banks are also assumed to merge their

back offices so that they are able to develop the competencies to compete with the big banks

(Taylor & Tyers, 2017). The mergers would enable them to use innovative ways to influence

customers within the financial sector.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

The overall study has emphasized on the performance of the big four banks in Australia that has

turned the Australian banking sector into an oligopoly market. The banks have been constantly

dominating in the Australian market which has posed a problem for the small banks to survive.

In fact, the customers are also not satisfied with the prices at which the products are offered by

the big banks. The poor performance of the financial sector has led to entry barriers for the

micro-lenders. Hence, there is a need to control the level of dominance of the big banks and the

small banks must also be able to sustain within the economy. The researchers have suggested a

non-collusive oligopoly strategy for the small banks to take advantage of the market competition.

Moreover, the open banking system to be introduced by the Australian government can also be

an important strategy through which the banks would have the scope to interact with the

customers and offer them with the products and services as per their demand. It can be concluded

that there might be further issues during mergers among the small banks which must be

considered as an effective way to regain the market share.

7

The overall study has emphasized on the performance of the big four banks in Australia that has

turned the Australian banking sector into an oligopoly market. The banks have been constantly

dominating in the Australian market which has posed a problem for the small banks to survive.

In fact, the customers are also not satisfied with the prices at which the products are offered by

the big banks. The poor performance of the financial sector has led to entry barriers for the

micro-lenders. Hence, there is a need to control the level of dominance of the big banks and the

small banks must also be able to sustain within the economy. The researchers have suggested a

non-collusive oligopoly strategy for the small banks to take advantage of the market competition.

Moreover, the open banking system to be introduced by the Australian government can also be

an important strategy through which the banks would have the scope to interact with the

customers and offer them with the products and services as per their demand. It can be concluded

that there might be further issues during mergers among the small banks which must be

considered as an effective way to regain the market share.

7

References

Apergis, N., & Cooray, A. (2015). Asymmetric interest rate pass-through in the US, the UK and

Australia: New evidence from selected individual banks. Journal of Macroeconomics, 45,

155-172.

Bakir, C. (2019). How do mega-bank merger policy and regulations contribute to financial

stability? Evidence from Australia and Canada. Journal of Economic Policy

Reform, 22(1), 1-15.

Financial Times. (2019). Australian regulator vows to tackle ‘cosy oligopoly’ of big banks.

Retrieved 30 August 2019, from https://www.ft.com/content/d940092a-25f2-11e9-8ce6-

5db4543da632

Financial Times. (2019). Foreign banks take aim at Australia’s big four oligopoly. Retrieved

from https://www.ft.com/content/668d60fe-97de-11e9-8cfb-30c211dcd229

Reuters. (2018). Australia's competition watchdog to review banking oligopoly. Retrieved from

https://www.reuters.com/article/australia-banks-competition/australias-competition-

watchdog-to-review-banking-oligopoly-idUSL3N1RN6E8

Selmier, W. T. (2016). Design rules for more resilient banking systems. Policy and

Society, 35(3), 253-267.

Taylor, G., & Tyers, R. (2017). Secular stagnation: Determinants and consequences for

Australia. Economic Record, 93(303), 615-650.

Xu, J., Gan, C., & Hu, B. (2015). An empirical analysis of China’s Big four state-owned banks’

performance: A data envelopment analysis. Journal of Banking Regulation, 16(1), 1-21.

8

Apergis, N., & Cooray, A. (2015). Asymmetric interest rate pass-through in the US, the UK and

Australia: New evidence from selected individual banks. Journal of Macroeconomics, 45,

155-172.

Bakir, C. (2019). How do mega-bank merger policy and regulations contribute to financial

stability? Evidence from Australia and Canada. Journal of Economic Policy

Reform, 22(1), 1-15.

Financial Times. (2019). Australian regulator vows to tackle ‘cosy oligopoly’ of big banks.

Retrieved 30 August 2019, from https://www.ft.com/content/d940092a-25f2-11e9-8ce6-

5db4543da632

Financial Times. (2019). Foreign banks take aim at Australia’s big four oligopoly. Retrieved

from https://www.ft.com/content/668d60fe-97de-11e9-8cfb-30c211dcd229

Reuters. (2018). Australia's competition watchdog to review banking oligopoly. Retrieved from

https://www.reuters.com/article/australia-banks-competition/australias-competition-

watchdog-to-review-banking-oligopoly-idUSL3N1RN6E8

Selmier, W. T. (2016). Design rules for more resilient banking systems. Policy and

Society, 35(3), 253-267.

Taylor, G., & Tyers, R. (2017). Secular stagnation: Determinants and consequences for

Australia. Economic Record, 93(303), 615-650.

Xu, J., Gan, C., & Hu, B. (2015). An empirical analysis of China’s Big four state-owned banks’

performance: A data envelopment analysis. Journal of Banking Regulation, 16(1), 1-21.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.