Porter's Five Forces Analysis of Australian Banking Industry

VerifiedAdded on 2022/09/08

|24

|5554

|76

Report

AI Summary

This report provides a comprehensive analysis of the Australian banking industry, focusing on the application of Porter's Five Forces framework. The analysis examines the industry's competitive environment, including the threats of new entrants, substitutes, and the bargaining power of suppliers and customers, as well as the rivalry among existing competitors. The report highlights the dominance of the four major banks in Australia and discusses the impact of government regulations and market dynamics on the industry's profitability and competitiveness. The study also explores the external environment influencing the banking sector and concludes with recommendations for strategic positioning. The report aims to understand the key variables within the external environment that influence the banking industry and to provide insights into the macro-environmental variables that might influence the performance of the financial industry. The report is contributed by a student and is available on Desklib.

Running head: ORGANISATIONAL STRATEGY

'Porter's Five Forces' analysis for Banking Industry of Australia

Name of the Student:

Name of the University:

Author note:

'Porter's Five Forces' analysis for Banking Industry of Australia

Name of the Student:

Name of the University:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ORGANISATIONAL STRATEGY

Table of Contents

1.0 Introduction................................................................................................................................2

2.0 Environment analysis of banking industry and profitability.....................................................3

2.1 Porter’s five forces.................................................................................................................3

2.2 Porter’s five forces analysis of Australian banking industry.................................................6

2.2.1 Threats of New Entrants.................................................................................................6

2.2.2 Threat of substitutes........................................................................................................7

2.2.3 Bargaining power of the suppliers..................................................................................8

2.2.4 Bargaining power of the consumers...............................................................................9

2.2.5 Rivalry within industry...................................................................................................9

2.3 External environment...........................................................................................................11

2.4 Profitability..........................................................................................................................14

3.0 Conclusion and recommendations...........................................................................................17

References......................................................................................................................................19

Appendix........................................................................................................................................23

Table of Contents

1.0 Introduction................................................................................................................................2

2.0 Environment analysis of banking industry and profitability.....................................................3

2.1 Porter’s five forces.................................................................................................................3

2.2 Porter’s five forces analysis of Australian banking industry.................................................6

2.2.1 Threats of New Entrants.................................................................................................6

2.2.2 Threat of substitutes........................................................................................................7

2.2.3 Bargaining power of the suppliers..................................................................................8

2.2.4 Bargaining power of the consumers...............................................................................9

2.2.5 Rivalry within industry...................................................................................................9

2.3 External environment...........................................................................................................11

2.4 Profitability..........................................................................................................................14

3.0 Conclusion and recommendations...........................................................................................17

References......................................................................................................................................19

Appendix........................................................................................................................................23

2ORGANISATIONAL STRATEGY

1.0 Introduction

Banking industry of Australia is one of the largest sectors of the economy. The industry is

dominated by four major banks, namely, Commonwealth Bank of Australia (CBA), Australia

and New Zealand Banking Group (ANZ), National Australia Bank (NAB) and Westpac Banking

Corporation (Walton 2020). There are some other smaller and regional banks also throughout the

nation and various different types of financial institutions. All the commercial retail banking and

financial institutions are controlled and regulated by the central bank, that is, Reserve Bank of

Australia (RBA). In Australia, there are 53 banks, among which 14 are owned by the Australian

government. All the four primary banks of Australia had cash earnings of $26.9 billion in total in

2019, with a net interest margin of 1.94% (Dring 2019). Thus, it can be said that the banking and

finance industry of Australia has been a major contributor to the GDP over the decades and due

to RBA’s appropriate regulatory policies, Australia has managed to experience a record

continuous economic growth for more than two decades. It can also be inferred that similar to

any other industry, the banking sector has been facing certain challenges as well as opportunities

over the years, which have influenced the performances of the industry, whether positively or

negatively. To understand the challenges, opportunities, and competitive position of the banking

industry, Porter’s five forces analysis is performed in this report. The aim of the report is to

analyse the key variables within the external environment which have a direct impact on the

banking industry and macro-environmental variables that might influence the current and future

performance of the financial industry. It is important to understand the environmental variables

and their relative strengths as that would help the banking industry to design policies accordingly

and mitigate the effects of challenges for keeping the economy stable. Hence, a thorough

discussion has been made in this report to highlight different aspects of the Porter’s five forces

1.0 Introduction

Banking industry of Australia is one of the largest sectors of the economy. The industry is

dominated by four major banks, namely, Commonwealth Bank of Australia (CBA), Australia

and New Zealand Banking Group (ANZ), National Australia Bank (NAB) and Westpac Banking

Corporation (Walton 2020). There are some other smaller and regional banks also throughout the

nation and various different types of financial institutions. All the commercial retail banking and

financial institutions are controlled and regulated by the central bank, that is, Reserve Bank of

Australia (RBA). In Australia, there are 53 banks, among which 14 are owned by the Australian

government. All the four primary banks of Australia had cash earnings of $26.9 billion in total in

2019, with a net interest margin of 1.94% (Dring 2019). Thus, it can be said that the banking and

finance industry of Australia has been a major contributor to the GDP over the decades and due

to RBA’s appropriate regulatory policies, Australia has managed to experience a record

continuous economic growth for more than two decades. It can also be inferred that similar to

any other industry, the banking sector has been facing certain challenges as well as opportunities

over the years, which have influenced the performances of the industry, whether positively or

negatively. To understand the challenges, opportunities, and competitive position of the banking

industry, Porter’s five forces analysis is performed in this report. The aim of the report is to

analyse the key variables within the external environment which have a direct impact on the

banking industry and macro-environmental variables that might influence the current and future

performance of the financial industry. It is important to understand the environmental variables

and their relative strengths as that would help the banking industry to design policies accordingly

and mitigate the effects of challenges for keeping the economy stable. Hence, a thorough

discussion has been made in this report to highlight different aspects of the Porter’s five forces

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ORGANISATIONAL STRATEGY

model, supported by academic theories, for evaluating the competitive position of the Australian

banking industry within the economy.

2.0 Environment analysis of banking industry and profitability

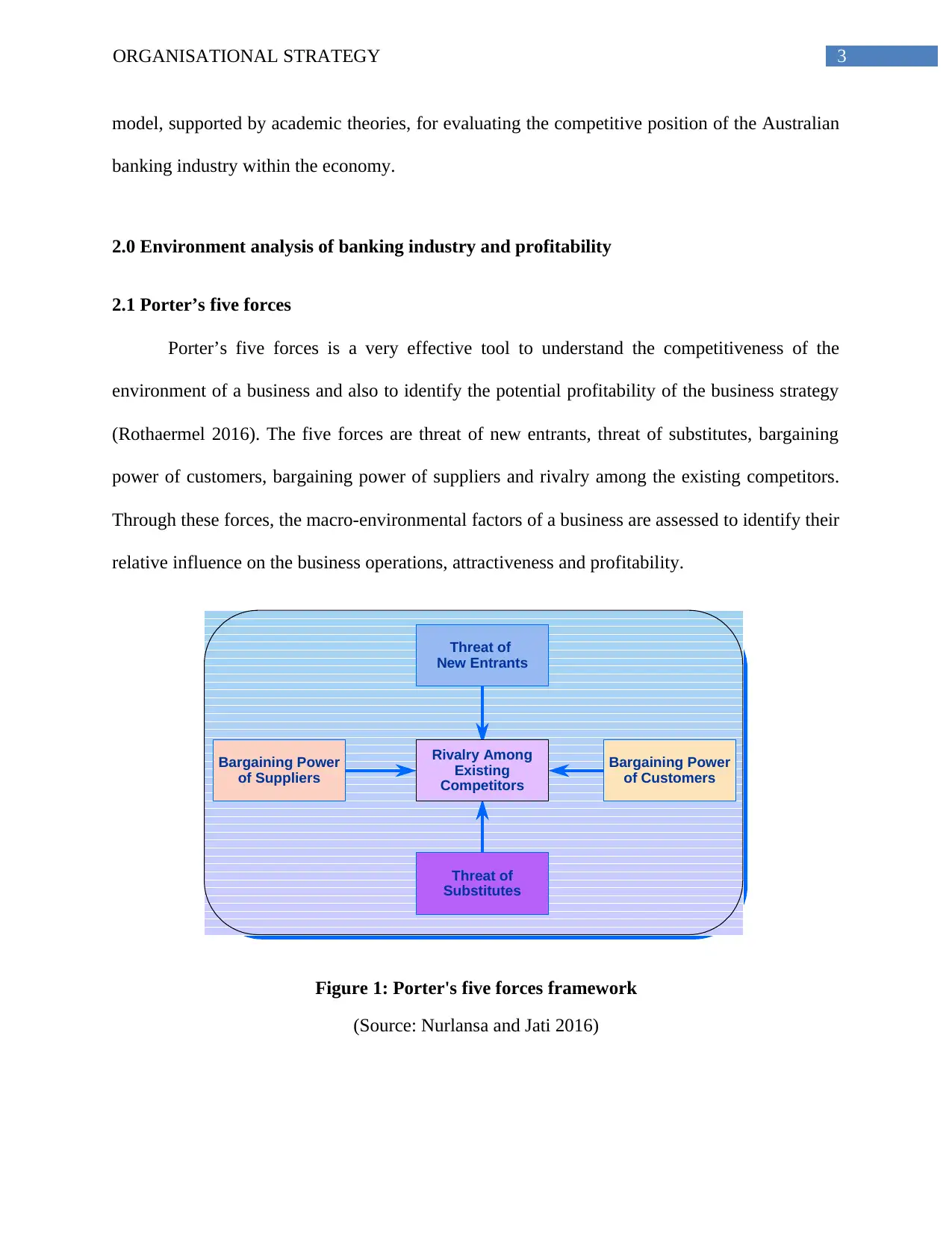

2.1 Porter’s five forces

Porter’s five forces is a very effective tool to understand the competitiveness of the

environment of a business and also to identify the potential profitability of the business strategy

(Rothaermel 2016). The five forces are threat of new entrants, threat of substitutes, bargaining

power of customers, bargaining power of suppliers and rivalry among the existing competitors.

Through these forces, the macro-environmental factors of a business are assessed to identify their

relative influence on the business operations, attractiveness and profitability.

Threat of

Substitutes

Threat of

Substitutes

Threat of

New Entrants

Threat of

New Entrants

Bargaining Power

of Customers

Bargaining Power

of Customers

Bargaining Power

of Suppliers

Bargaining Power

of Suppliers

Rivalry Among

Existing

Competitors

Figure 1: Porter's five forces framework

(Source: Nurlansa and Jati 2016)

model, supported by academic theories, for evaluating the competitive position of the Australian

banking industry within the economy.

2.0 Environment analysis of banking industry and profitability

2.1 Porter’s five forces

Porter’s five forces is a very effective tool to understand the competitiveness of the

environment of a business and also to identify the potential profitability of the business strategy

(Rothaermel 2016). The five forces are threat of new entrants, threat of substitutes, bargaining

power of customers, bargaining power of suppliers and rivalry among the existing competitors.

Through these forces, the macro-environmental factors of a business are assessed to identify their

relative influence on the business operations, attractiveness and profitability.

Threat of

Substitutes

Threat of

Substitutes

Threat of

New Entrants

Threat of

New Entrants

Bargaining Power

of Customers

Bargaining Power

of Customers

Bargaining Power

of Suppliers

Bargaining Power

of Suppliers

Rivalry Among

Existing

Competitors

Figure 1: Porter's five forces framework

(Source: Nurlansa and Jati 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ORGANISATIONAL STRATEGY

As explained by Rothaermel (2016), there are many factors that influence these forces to

assess the competitiveness of the businesses, such as, the threat of new entrants is influenced

by economies of scale, proprietary product differences, brand identity, capital requirements,

access to distribution, absolute cost advantages, government policies, expected retaliation, and

switching costs of the customers. When a business has lower economies of scale, loses brand

identity, or has high requirement for funding, low switching cost, low absolute cost advantage or

loses distribution access, then the threat of new entrants becomes high and lowers its

competitiveness in the market.

Threat of substitutes implies the availability of substitute, that is, goods or services that

are similar and can satisfy the similar needs of the consumers. The influencing factors are

relative price and performance of the substitutes, switching costs and buyers’ propensity to

substitute the product or service of a particular industry (Nurlansa and Jati 2016). When the

threat of substitute is high for an industry, its competitiveness reduces.

Bargaining power of the suppliers indicates the convenience of the suppliers to increase

their prices. Number of suppliers, uniqueness of their supplies, the switching cost from one

supplier or firm to another, presence of the substitute inputs, concentration of the suppliers

relative to the industry suppliers, cost of production or operation relative to the total purchase in

the industry, impact of the supplies on production cost or differentiation, extent of information

about the supply, profitability of the suppliers, incentives of the decision makers and threat of

forward integration are the major elements that can give an edge to the suppliers and when the

industry is profitable when the bargaining power of the suppliers is low (Varelas and

Georgopoulos 2017).

As explained by Rothaermel (2016), there are many factors that influence these forces to

assess the competitiveness of the businesses, such as, the threat of new entrants is influenced

by economies of scale, proprietary product differences, brand identity, capital requirements,

access to distribution, absolute cost advantages, government policies, expected retaliation, and

switching costs of the customers. When a business has lower economies of scale, loses brand

identity, or has high requirement for funding, low switching cost, low absolute cost advantage or

loses distribution access, then the threat of new entrants becomes high and lowers its

competitiveness in the market.

Threat of substitutes implies the availability of substitute, that is, goods or services that

are similar and can satisfy the similar needs of the consumers. The influencing factors are

relative price and performance of the substitutes, switching costs and buyers’ propensity to

substitute the product or service of a particular industry (Nurlansa and Jati 2016). When the

threat of substitute is high for an industry, its competitiveness reduces.

Bargaining power of the suppliers indicates the convenience of the suppliers to increase

their prices. Number of suppliers, uniqueness of their supplies, the switching cost from one

supplier or firm to another, presence of the substitute inputs, concentration of the suppliers

relative to the industry suppliers, cost of production or operation relative to the total purchase in

the industry, impact of the supplies on production cost or differentiation, extent of information

about the supply, profitability of the suppliers, incentives of the decision makers and threat of

forward integration are the major elements that can give an edge to the suppliers and when the

industry is profitable when the bargaining power of the suppliers is low (Varelas and

Georgopoulos 2017).

5ORGANISATIONAL STRATEGY

Bargaining power of customers represents the influential power of the customers to

drive down the prices of the industry. The profitability of an industry or a business considerably

depends on the volume of customers and their preferences. The more the number of buyers, the

higher is the industry competiveness and profitability. As stated by Nurlansa and Jati (2016), the

important elements that should be considered while assessing the power of the customers are the

output differentiation, availability of substitutes, switching cost of the consumers, concentration

of industries relative to that for the buyers, cost of operation and production in relation to total

buyer purchase, consumers’ profitability, information to the buyers about industry output,

incentives of the decision makers, effect of the production on the cost or differentiation of the

buyers, and threats of the backward integration are the most important aspects that influence the

bargaining power of the customers and that affects the profitability of the industry.

Lastly, the rivalry among existing competitors represents the aspects like growth rate of

the industry, high fixed cost, brand image and identity, production potential or intermittent over-

capacity, product differentiation, informational complexity, corporate stakes, exit barriers,

balance and concentration and diversity of the competitors, which determine the attractiveness

and profitability of an industry (Varelas and Georgopoulos 2017). The more is internal rivalry,

the lower is the profitability of the industry. Thus, it can be said that, the profitability and

competitiveness of an industry depends on all the above factors and these aspects, combined with

the dynamic conditions, have changes in their nature and strength of influence on the industry

attractiveness.

Bargaining power of customers represents the influential power of the customers to

drive down the prices of the industry. The profitability of an industry or a business considerably

depends on the volume of customers and their preferences. The more the number of buyers, the

higher is the industry competiveness and profitability. As stated by Nurlansa and Jati (2016), the

important elements that should be considered while assessing the power of the customers are the

output differentiation, availability of substitutes, switching cost of the consumers, concentration

of industries relative to that for the buyers, cost of operation and production in relation to total

buyer purchase, consumers’ profitability, information to the buyers about industry output,

incentives of the decision makers, effect of the production on the cost or differentiation of the

buyers, and threats of the backward integration are the most important aspects that influence the

bargaining power of the customers and that affects the profitability of the industry.

Lastly, the rivalry among existing competitors represents the aspects like growth rate of

the industry, high fixed cost, brand image and identity, production potential or intermittent over-

capacity, product differentiation, informational complexity, corporate stakes, exit barriers,

balance and concentration and diversity of the competitors, which determine the attractiveness

and profitability of an industry (Varelas and Georgopoulos 2017). The more is internal rivalry,

the lower is the profitability of the industry. Thus, it can be said that, the profitability and

competitiveness of an industry depends on all the above factors and these aspects, combined with

the dynamic conditions, have changes in their nature and strength of influence on the industry

attractiveness.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ORGANISATIONAL STRATEGY

2.2 Porter’s five forces analysis of Australian banking industry

2.2.1 Threats of New Entrants

The banking industry of Australia is majorly dominated by the four large banks. The

industry follows an oligopoly structure, where very few service providers control large number

of consumers and provide slightly differentiated products and services, where the barriers to

entry are high with high fixed cost. The major banks act as a group, where price change by one

bank is responded accordingly and almost immediately by the other banks (Afrin 2020). The

Australian banking industry has successfully created a strong brand image by supporting the

positive economic growth for more than two decades. However, in this sector, a new entrant can

bring innovation in the goods and services provided, new operation techniques and lower pricing

strategy, and a higher value proposition for the customers.

The banking sector in Australia is quite stable in terms of products and services provided.

The banks not only provide traditional banking services but also new type of products and

services, such as digital banking technology and various new products in terms of schemes are

provided. These established banks have access to maximum of the capital deposits of the nation

due to their reputation and brand image. Hence, they also have the absolute cost advantage in the

market, in comparison to the smaller financial and non-financial institutions like some regional

banks. These banks provide their products and services at an affordable prices due to their large

economies of scale. The new entrants in the banking sector will face challenge in economies of

scale of learning as well as providing service at a lower price because these new banks or

financial institutions will need more time in learning and understanding the market trends and the

needs of the customers and they will also need more resources for setting up (Dring 2019). Thus,

2.2 Porter’s five forces analysis of Australian banking industry

2.2.1 Threats of New Entrants

The banking industry of Australia is majorly dominated by the four large banks. The

industry follows an oligopoly structure, where very few service providers control large number

of consumers and provide slightly differentiated products and services, where the barriers to

entry are high with high fixed cost. The major banks act as a group, where price change by one

bank is responded accordingly and almost immediately by the other banks (Afrin 2020). The

Australian banking industry has successfully created a strong brand image by supporting the

positive economic growth for more than two decades. However, in this sector, a new entrant can

bring innovation in the goods and services provided, new operation techniques and lower pricing

strategy, and a higher value proposition for the customers.

The banking sector in Australia is quite stable in terms of products and services provided.

The banks not only provide traditional banking services but also new type of products and

services, such as digital banking technology and various new products in terms of schemes are

provided. These established banks have access to maximum of the capital deposits of the nation

due to their reputation and brand image. Hence, they also have the absolute cost advantage in the

market, in comparison to the smaller financial and non-financial institutions like some regional

banks. These banks provide their products and services at an affordable prices due to their large

economies of scale. The new entrants in the banking sector will face challenge in economies of

scale of learning as well as providing service at a lower price because these new banks or

financial institutions will need more time in learning and understanding the market trends and the

needs of the customers and they will also need more resources for setting up (Dring 2019). Thus,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ORGANISATIONAL STRATEGY

due to all these factors, under the oligopoly market structure, the barriers to entry are quite high

in the banking industry of Australia.

Furthermore, the government regulation and initial capital requirement determined by

APRA while establishment of credibility and switching costs are also considered as important

barriers to entry for the new entrants in the banking sector. APRA has determined that all the

locally incorporated banks must hold total capital of minimum 8% of the risk weighted assets,

and minimum half of their total capital has to be better quality under Tier 1, with a minimum

Tier 1 ratio of 4% (Walton 2020). This is a large amount for a new bank while setting up. RBA

(2020) mentioned about the switching costs. The larger the switching cost for the customers, the

harder it will be for the new entrants to gain customers in the banking sector. Therefore, due to

all the above-mentioned factors along with the strong brand reputation of the existing banks, the

threat of new entry is very low for the banking industry of Australia.

2.2.2 Threat of substitutes

In the banking industry, the market players offer similar product and services. Those are

close substitutes of each other, if not perfect substitutes. After the financial deregulation in

Australia in the 1980s, wide range of substitute products and services emerged in the commercial

banking sector. Apart from the commercial banks, variety of financial institutions exist in the

market that provide loans or takes deposits from customers, such as, credit unions, investment

banks, money market corporations, and private investors. The banks act as a group and any price

changes is matched by appropriate responses, which makes the customers less sensitive to price

changes (Afrin 2020). However, in this industry, credibility or trust factor is a very crucial

element for the banks to gain new customers and retain existing customers. Therefore, even

though there are substitute products and services, the customers must gain trust on the providers

due to all these factors, under the oligopoly market structure, the barriers to entry are quite high

in the banking industry of Australia.

Furthermore, the government regulation and initial capital requirement determined by

APRA while establishment of credibility and switching costs are also considered as important

barriers to entry for the new entrants in the banking sector. APRA has determined that all the

locally incorporated banks must hold total capital of minimum 8% of the risk weighted assets,

and minimum half of their total capital has to be better quality under Tier 1, with a minimum

Tier 1 ratio of 4% (Walton 2020). This is a large amount for a new bank while setting up. RBA

(2020) mentioned about the switching costs. The larger the switching cost for the customers, the

harder it will be for the new entrants to gain customers in the banking sector. Therefore, due to

all the above-mentioned factors along with the strong brand reputation of the existing banks, the

threat of new entry is very low for the banking industry of Australia.

2.2.2 Threat of substitutes

In the banking industry, the market players offer similar product and services. Those are

close substitutes of each other, if not perfect substitutes. After the financial deregulation in

Australia in the 1980s, wide range of substitute products and services emerged in the commercial

banking sector. Apart from the commercial banks, variety of financial institutions exist in the

market that provide loans or takes deposits from customers, such as, credit unions, investment

banks, money market corporations, and private investors. The banks act as a group and any price

changes is matched by appropriate responses, which makes the customers less sensitive to price

changes (Afrin 2020). However, in this industry, credibility or trust factor is a very crucial

element for the banks to gain new customers and retain existing customers. Therefore, even

though there are substitute products and services, the customers must gain trust on the providers

8ORGANISATIONAL STRATEGY

before depositing large amount of money with them or to avail any type of banking services

(Muigai and Gitau 2018). The relative prices and performance of the substitutes in this sector are

also important, however, the substitute products and services are provided by smaller financial

institutions and the propensity to substitute of the buyers is higher for the large four banks in the

sector. Therefore, the threat of substitutes is average for the Australian banking industry.

2.2.3 Bargaining power of the suppliers

The major suppliers of the baking sector are the depositors, legal service providers,

accounting service providers and the financial markets (Miller and Herzog 2017). For the entire

operations of the banks, they require all the above mentioned services. While the legal service

providers are required for legal operations for the contracts with the clients and other several

legal issues, the accounting services, such as, the financial statement preparation, annual tax

audit and all other types accounting jobs are provided by the accounting firms. In the Australian

banking industry, the major banks have options for switching their legal and accounting service

providers in case they are not satisfied with their quality of services or prices. However, the

smaller financial institutions do not have that much choices. Hence, bargaining power of those

suppliers are low for the larger banks and high for the smaller and regional banks and financial

institutions.

According to Kessey (2019), the composition of funding differs from one bank to

another. The four large banks of Australia get their funding from the customers’ deposits and

from the wholesale debt. The regional banks also get local funds, offshore funding, and through

‘securitisation’. Since the foreign banks have lower level of deposits than the domestic banks,

these have to rely on the offshore capital. Hence, the major supply of fund in the market goes to

the four primary banks in the industry and the banking industry has been in a better position in

before depositing large amount of money with them or to avail any type of banking services

(Muigai and Gitau 2018). The relative prices and performance of the substitutes in this sector are

also important, however, the substitute products and services are provided by smaller financial

institutions and the propensity to substitute of the buyers is higher for the large four banks in the

sector. Therefore, the threat of substitutes is average for the Australian banking industry.

2.2.3 Bargaining power of the suppliers

The major suppliers of the baking sector are the depositors, legal service providers,

accounting service providers and the financial markets (Miller and Herzog 2017). For the entire

operations of the banks, they require all the above mentioned services. While the legal service

providers are required for legal operations for the contracts with the clients and other several

legal issues, the accounting services, such as, the financial statement preparation, annual tax

audit and all other types accounting jobs are provided by the accounting firms. In the Australian

banking industry, the major banks have options for switching their legal and accounting service

providers in case they are not satisfied with their quality of services or prices. However, the

smaller financial institutions do not have that much choices. Hence, bargaining power of those

suppliers are low for the larger banks and high for the smaller and regional banks and financial

institutions.

According to Kessey (2019), the composition of funding differs from one bank to

another. The four large banks of Australia get their funding from the customers’ deposits and

from the wholesale debt. The regional banks also get local funds, offshore funding, and through

‘securitisation’. Since the foreign banks have lower level of deposits than the domestic banks,

these have to rely on the offshore capital. Hence, the major supply of fund in the market goes to

the four primary banks in the industry and the banking industry has been in a better position in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ORGANISATIONAL STRATEGY

terms of bargaining with the fund suppliers. At the same time, the sector also experiences

competitive price pressure to maintain their flow of funding and that is a challenge for the

smaller players in the market. The larger banks can provide higher interest rate on the deposits

and capture the maximum fund supply, however, this practice has lowered the net interest margin

quite drastically for the industry. Moreover, supplier concentration is less relative to industry

concentration. Lastly, the banking industry collects information about the suppliers as part of

regulations, which is beneficial for having a power over the suppliers. Thus, it can be said that

the bargaining power of the suppliers is moderate for the Australian banking industry.

2.2.4 Bargaining power of the consumers

The buyers of the banking industry are the customers, which includes individuals and the

households for the retail banking and mortgage and businesses for corporate banking. The

bargaining power of the consumers in the banking industry comes from the availability of the

substitute products and service providers and this makes all the players in the industry to engage

in a price competition for attracting more customers. As per the interest rate set by the RBA, the

commercial banks set competitive interest rate that affected the net interest margin considerably

in 2013. Moreover, all the banks in the industry must maintain customer satisfaction through

their product and service and hence, the competition is high. At the same time, the banks also

impose some prices for the services to maintain minimum profit from the operations (Afolabi,

Ezenwoke and Ayo 2017). Thus, it can be said that the bargaining power of the consumers is

average in Australian banking industry.

2.2.5 Rivalry within industry

In the banking sector of Australia, the industry rivalry is quite intense. CBA, ANZ, NAB

and Westpac are the dominant players in the commercial banking. The other banks and financial

terms of bargaining with the fund suppliers. At the same time, the sector also experiences

competitive price pressure to maintain their flow of funding and that is a challenge for the

smaller players in the market. The larger banks can provide higher interest rate on the deposits

and capture the maximum fund supply, however, this practice has lowered the net interest margin

quite drastically for the industry. Moreover, supplier concentration is less relative to industry

concentration. Lastly, the banking industry collects information about the suppliers as part of

regulations, which is beneficial for having a power over the suppliers. Thus, it can be said that

the bargaining power of the suppliers is moderate for the Australian banking industry.

2.2.4 Bargaining power of the consumers

The buyers of the banking industry are the customers, which includes individuals and the

households for the retail banking and mortgage and businesses for corporate banking. The

bargaining power of the consumers in the banking industry comes from the availability of the

substitute products and service providers and this makes all the players in the industry to engage

in a price competition for attracting more customers. As per the interest rate set by the RBA, the

commercial banks set competitive interest rate that affected the net interest margin considerably

in 2013. Moreover, all the banks in the industry must maintain customer satisfaction through

their product and service and hence, the competition is high. At the same time, the banks also

impose some prices for the services to maintain minimum profit from the operations (Afolabi,

Ezenwoke and Ayo 2017). Thus, it can be said that the bargaining power of the consumers is

average in Australian banking industry.

2.2.5 Rivalry within industry

In the banking sector of Australia, the industry rivalry is quite intense. CBA, ANZ, NAB

and Westpac are the dominant players in the commercial banking. The other banks and financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ORGANISATIONAL STRATEGY

institutions are smaller players, who not have much market influential power. The Customer

Owned Banking Association represents an industry body which includes over 100 credit unions,

mutual banks and building societies constituting the cooperative banking sector (Sathye 2020).

All types of financial actions are regulated by RBA. While the banking sector has high level of

entry barriers for potential entrants, the four major banks also have competition among

themselves. The level of competition is quite high for not only traditional banking activities, but

also with new age product and services, such as, internet banking, credit card, various deposit

schemes for different time period and many more.

Deloitte Australia (2020) highlighted that the internal industry rivalry is primarily based

on the product and the prices. The major banks compete with each other on the basis of the

interest rate under the current cash rate determined by RBA. On the other hand, the smaller

banks can lower their prices due to their low cost operation and size. As a result of this internal

competition, the overall price in the industry is low and that lowers the revenues and profits for

the entire industry. Secondly, the variety of product and services are more in the major banks

than in the smaller banks. In terms of quality and innovation, the major players dominate the

market. In case of smaller financial institutions, the level of innovation and quality remains

limited to one or two products or services, while the four big players can invest more in

technology and R&D programs for providing better experience and higher value additions to the

customers. The outcome can be seen from the market share of the four big banks (Walton 2020).

Finally it can be said that, the internal competition among the four major banks is quite high in

the banking industry, however, when the overall picture is considered, the level of industry

rivalry can be regarded as average.

institutions are smaller players, who not have much market influential power. The Customer

Owned Banking Association represents an industry body which includes over 100 credit unions,

mutual banks and building societies constituting the cooperative banking sector (Sathye 2020).

All types of financial actions are regulated by RBA. While the banking sector has high level of

entry barriers for potential entrants, the four major banks also have competition among

themselves. The level of competition is quite high for not only traditional banking activities, but

also with new age product and services, such as, internet banking, credit card, various deposit

schemes for different time period and many more.

Deloitte Australia (2020) highlighted that the internal industry rivalry is primarily based

on the product and the prices. The major banks compete with each other on the basis of the

interest rate under the current cash rate determined by RBA. On the other hand, the smaller

banks can lower their prices due to their low cost operation and size. As a result of this internal

competition, the overall price in the industry is low and that lowers the revenues and profits for

the entire industry. Secondly, the variety of product and services are more in the major banks

than in the smaller banks. In terms of quality and innovation, the major players dominate the

market. In case of smaller financial institutions, the level of innovation and quality remains

limited to one or two products or services, while the four big players can invest more in

technology and R&D programs for providing better experience and higher value additions to the

customers. The outcome can be seen from the market share of the four big banks (Walton 2020).

Finally it can be said that, the internal competition among the four major banks is quite high in

the banking industry, however, when the overall picture is considered, the level of industry

rivalry can be regarded as average.

11ORGANISATIONAL STRATEGY

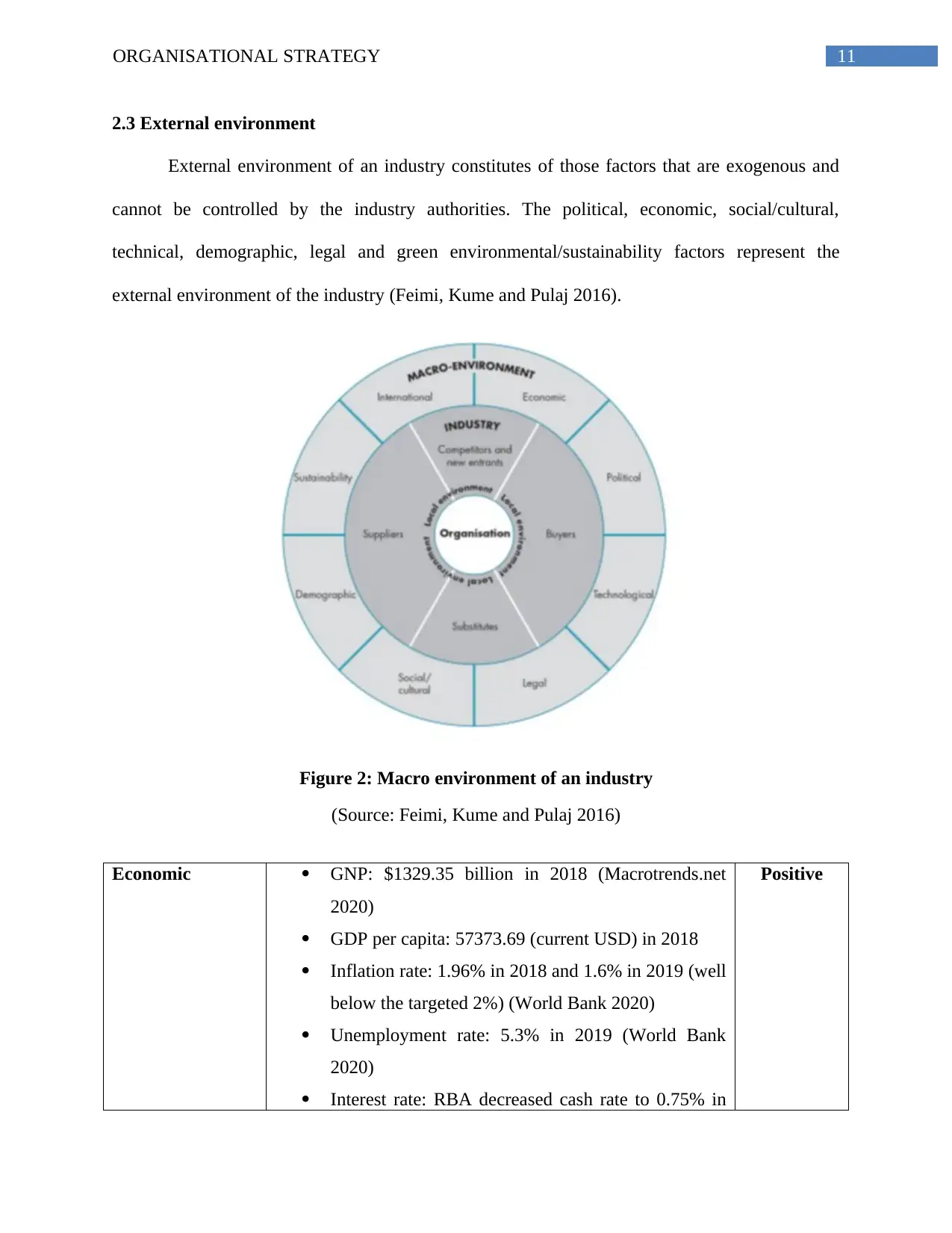

2.3 External environment

External environment of an industry constitutes of those factors that are exogenous and

cannot be controlled by the industry authorities. The political, economic, social/cultural,

technical, demographic, legal and green environmental/sustainability factors represent the

external environment of the industry (Feimi, Kume and Pulaj 2016).

Figure 2: Macro environment of an industry

(Source: Feimi, Kume and Pulaj 2016)

Economic GNP: $1329.35 billion in 2018 (Macrotrends.net

2020)

GDP per capita: 57373.69 (current USD) in 2018

Inflation rate: 1.96% in 2018 and 1.6% in 2019 (well

below the targeted 2%) (World Bank 2020)

Unemployment rate: 5.3% in 2019 (World Bank

2020)

Interest rate: RBA decreased cash rate to 0.75% in

Positive

2.3 External environment

External environment of an industry constitutes of those factors that are exogenous and

cannot be controlled by the industry authorities. The political, economic, social/cultural,

technical, demographic, legal and green environmental/sustainability factors represent the

external environment of the industry (Feimi, Kume and Pulaj 2016).

Figure 2: Macro environment of an industry

(Source: Feimi, Kume and Pulaj 2016)

Economic GNP: $1329.35 billion in 2018 (Macrotrends.net

2020)

GDP per capita: 57373.69 (current USD) in 2018

Inflation rate: 1.96% in 2018 and 1.6% in 2019 (well

below the targeted 2%) (World Bank 2020)

Unemployment rate: 5.3% in 2019 (World Bank

2020)

Interest rate: RBA decreased cash rate to 0.75% in

Positive

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.