Assessing Australian Banking's Impact on Economic Growth: CBA Study

VerifiedAdded on 2020/10/22

|13

|4214

|59

Report

AI Summary

This research project investigates the influence of the Australian banking sector on economic growth, with a specific focus on the Commonwealth Bank of Australia (CBA). The report begins with an introduction and background, highlighting the dominance of major banks in Australia and the role of banking in a modern service-based economy. It outlines the project's objectives, including determining the role of the financial system, assessing the impact of exchange rate fluctuations and interest rates, and evaluating the role of the Reserve Bank's monetary policy. The literature review explores the role of financial systems and banks, emphasizing financial intermediation and banking regulations. It also examines the impact of exchange rate fluctuations and interest rates on the banking sector. The report discusses currency risk management and its importance, as well as the effects of interest rate alterations on the financial system. The project aims to provide insights into the critical role banks play in capital formation and economic growth, emphasizing their influence on various aspects of the economy.

RESEARCH PROJECT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Topic: To assess influence of Australian banking sector on economic growth- A study on

Commonwealth bank of Australia..........................................................................................1

INTRODUCTION...........................................................................................................................1

Background of study...............................................................................................................1

PROJECT OBJECTIVE..................................................................................................................2

Aims and Objective................................................................................................................2

PROJECT SCOPE...........................................................................................................................3

LITERATURE REVIEW................................................................................................................3

Role of financial system (banks) on economy.......................................................................3

Impact of fluctuations in exchange rate on banking sector....................................................4

Impact of interest rate on banking sector...............................................................................6

Role of reserve bank monetary policy on economic growth..................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Topic: To assess influence of Australian banking sector on economic growth- A study on

Commonwealth bank of Australia..........................................................................................1

INTRODUCTION...........................................................................................................................1

Background of study...............................................................................................................1

PROJECT OBJECTIVE..................................................................................................................2

Aims and Objective................................................................................................................2

PROJECT SCOPE...........................................................................................................................3

LITERATURE REVIEW................................................................................................................3

Role of financial system (banks) on economy.......................................................................3

Impact of fluctuations in exchange rate on banking sector....................................................4

Impact of interest rate on banking sector...............................................................................6

Role of reserve bank monetary policy on economic growth..................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

Topic: To assess influence of Australian banking sector on economic growth- A study on

Commonwealth bank of Australia

INTRODUCTION

Banking is referred as financial institution which is engaged in lending and borrowing

money. The present report will briefly discuss about Australian banking sector and how it is

influencing economic growth with reference to Commonwealth bank of Australia. In the same

series, it will be stating project objectives, scope and literature review with appropriate

conclusion.

Background of study

Banking in Australia is highly dominated through four major banks such as Westpac

banking corporation, Commonwealth Bank of Australia, national Australia bank and New

Zealand banking group. These banks have AA ratings where trade finance liquidity is issue in

rest of the world. The banking system in Australia is highly transparent and reliable as its

operational and structural differences through American system (Banking in Australia, 2019). On

historic basis, Australian banks have not operated with reference to restrictions which limited US

bank operation in 1933. The Australian banking system has undergone with progressive

deregulation along with privatization as well. In this aspect, foreign banks are allowed for

entering financial market and retail banks give wide range of financial services like general and

life insurance, security underwriting and stock brokering to its retail consumers for creating

consumer and corporate loans as it forms competition through merchant banks and brokerage

houses.

1

Commonwealth bank of Australia

INTRODUCTION

Banking is referred as financial institution which is engaged in lending and borrowing

money. The present report will briefly discuss about Australian banking sector and how it is

influencing economic growth with reference to Commonwealth bank of Australia. In the same

series, it will be stating project objectives, scope and literature review with appropriate

conclusion.

Background of study

Banking in Australia is highly dominated through four major banks such as Westpac

banking corporation, Commonwealth Bank of Australia, national Australia bank and New

Zealand banking group. These banks have AA ratings where trade finance liquidity is issue in

rest of the world. The banking system in Australia is highly transparent and reliable as its

operational and structural differences through American system (Banking in Australia, 2019). On

historic basis, Australian banks have not operated with reference to restrictions which limited US

bank operation in 1933. The Australian banking system has undergone with progressive

deregulation along with privatization as well. In this aspect, foreign banks are allowed for

entering financial market and retail banks give wide range of financial services like general and

life insurance, security underwriting and stock brokering to its retail consumers for creating

consumer and corporate loans as it forms competition through merchant banks and brokerage

houses.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

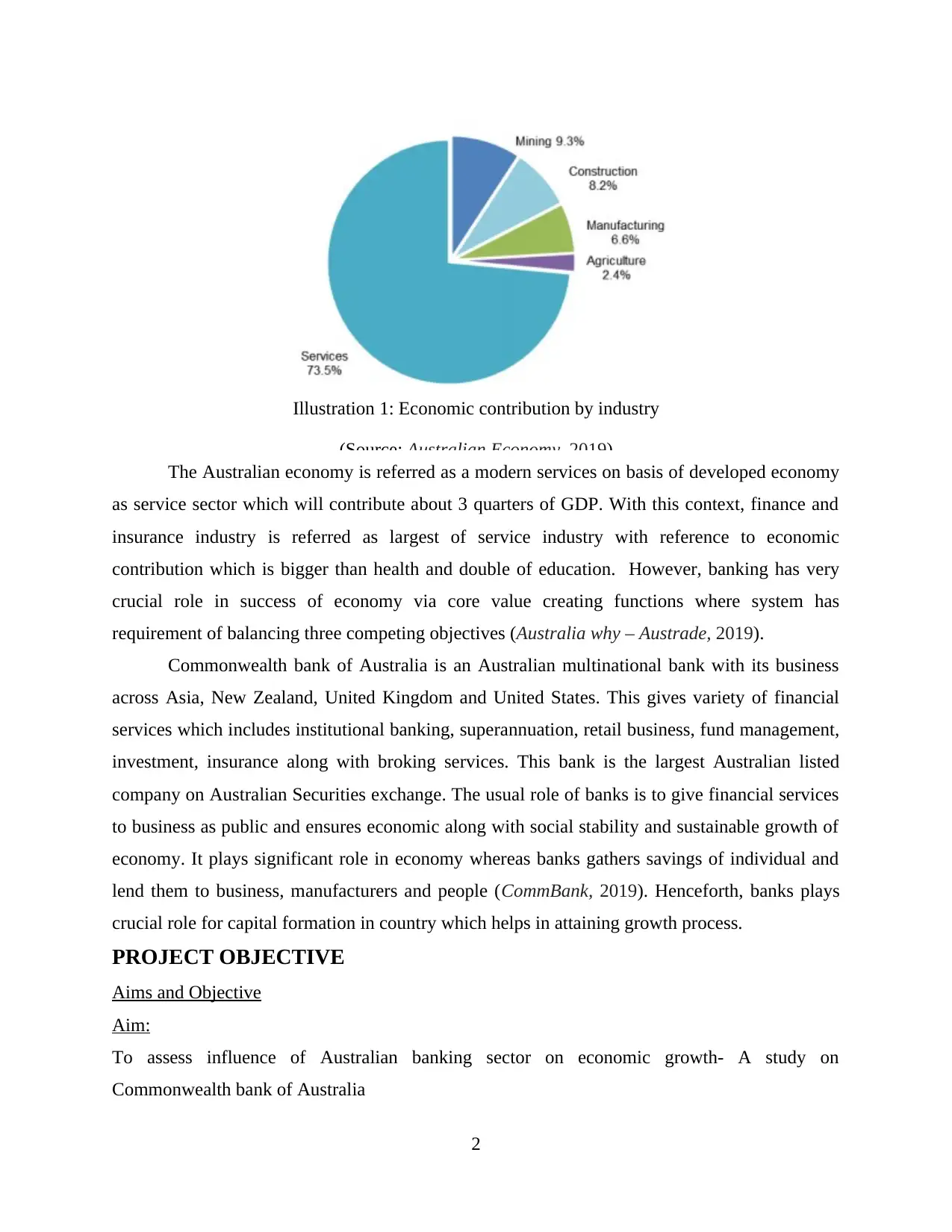

Illustration 1: Economic contribution by industry

(Source: Australian Economy, 2019)

The Australian economy is referred as a modern services on basis of developed economy

as service sector which will contribute about 3 quarters of GDP. With this context, finance and

insurance industry is referred as largest of service industry with reference to economic

contribution which is bigger than health and double of education. However, banking has very

crucial role in success of economy via core value creating functions where system has

requirement of balancing three competing objectives (Australia why – Austrade, 2019).

Commonwealth bank of Australia is an Australian multinational bank with its business

across Asia, New Zealand, United Kingdom and United States. This gives variety of financial

services which includes institutional banking, superannuation, retail business, fund management,

investment, insurance along with broking services. This bank is the largest Australian listed

company on Australian Securities exchange. The usual role of banks is to give financial services

to business as public and ensures economic along with social stability and sustainable growth of

economy. It plays significant role in economy whereas banks gathers savings of individual and

lend them to business, manufacturers and people (CommBank, 2019). Henceforth, banks plays

crucial role for capital formation in country which helps in attaining growth process.

PROJECT OBJECTIVE

Aims and Objective

Aim:

To assess influence of Australian banking sector on economic growth- A study on

Commonwealth bank of Australia

2

(Source: Australian Economy, 2019)

The Australian economy is referred as a modern services on basis of developed economy

as service sector which will contribute about 3 quarters of GDP. With this context, finance and

insurance industry is referred as largest of service industry with reference to economic

contribution which is bigger than health and double of education. However, banking has very

crucial role in success of economy via core value creating functions where system has

requirement of balancing three competing objectives (Australia why – Austrade, 2019).

Commonwealth bank of Australia is an Australian multinational bank with its business

across Asia, New Zealand, United Kingdom and United States. This gives variety of financial

services which includes institutional banking, superannuation, retail business, fund management,

investment, insurance along with broking services. This bank is the largest Australian listed

company on Australian Securities exchange. The usual role of banks is to give financial services

to business as public and ensures economic along with social stability and sustainable growth of

economy. It plays significant role in economy whereas banks gathers savings of individual and

lend them to business, manufacturers and people (CommBank, 2019). Henceforth, banks plays

crucial role for capital formation in country which helps in attaining growth process.

PROJECT OBJECTIVE

Aims and Objective

Aim:

To assess influence of Australian banking sector on economic growth- A study on

Commonwealth bank of Australia

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Objectives

To determine role of financial system (banks) on economy

To assess impact of fluctuations in exchange rate risk on banking sector.

To identify impact of interest rate on banking sector.

To assess role of reserve bank monetary policy for economic growth.

PROJECT SCOPE

In this study, topic of project has been decided with context of Australian banking sector

as in first part, brief overview of entire project has been given. Furthermore, background of the

study has been designed with context of Commonwealth bank of Australia and then project

objective and aim has been framed. In the similar aspect, themes has been framed with each

objective and literature review is performed and then entire research project is concluded.

LITERATURE REVIEW

Role of financial system (banks) on economy

According to Geddes, Schmidt and Steffen (2018), banks accepts deposits and forms loan

and profit margin has been derived with variation in interest rate paid and charged to depositors

and borrowers on respective aspect. The procedure performed through banks of taking funds

through depositor and then lending to any borrower is termed as financial intermediation.

However, Auer and et.al., (2019) states that procedure of this financial intermediation in which

certain assets are conversed into multiple liabilities or assets. The financial intermediaries

channel funds by the one who have surplus savings or extra money to one who does not have

enough money for carrying desired activity.

As per views of Ouenniche and Carrales (2018), banking thrive with context of financial

intermediation with capabilities of financial institutions who directly allows for lending and

receiving money on deposit. The bank is replicated as very important financial intermediary with

context to economy along with connecting it to deficit and surplus economic agents. Its main role

is to give safe place for keeping money and opportunity as well for earning interest on deposits.

On the contrary, Pacheco Pardo, Knoerich and Li (2018) had critiqued that combination of

investment and commercial banking could be outcome of conflict of interest. Some might

provide importance to single type of bankings which provides less significant to other banking

type which does not create commercial sense. Services such as savings and current account give

convenient aspect for repaying bills with absence of hustle of inapplicable cash. On the similar

3

To determine role of financial system (banks) on economy

To assess impact of fluctuations in exchange rate risk on banking sector.

To identify impact of interest rate on banking sector.

To assess role of reserve bank monetary policy for economic growth.

PROJECT SCOPE

In this study, topic of project has been decided with context of Australian banking sector

as in first part, brief overview of entire project has been given. Furthermore, background of the

study has been designed with context of Commonwealth bank of Australia and then project

objective and aim has been framed. In the similar aspect, themes has been framed with each

objective and literature review is performed and then entire research project is concluded.

LITERATURE REVIEW

Role of financial system (banks) on economy

According to Geddes, Schmidt and Steffen (2018), banks accepts deposits and forms loan

and profit margin has been derived with variation in interest rate paid and charged to depositors

and borrowers on respective aspect. The procedure performed through banks of taking funds

through depositor and then lending to any borrower is termed as financial intermediation.

However, Auer and et.al., (2019) states that procedure of this financial intermediation in which

certain assets are conversed into multiple liabilities or assets. The financial intermediaries

channel funds by the one who have surplus savings or extra money to one who does not have

enough money for carrying desired activity.

As per views of Ouenniche and Carrales (2018), banking thrive with context of financial

intermediation with capabilities of financial institutions who directly allows for lending and

receiving money on deposit. The bank is replicated as very important financial intermediary with

context to economy along with connecting it to deficit and surplus economic agents. Its main role

is to give safe place for keeping money and opportunity as well for earning interest on deposits.

On the contrary, Pacheco Pardo, Knoerich and Li (2018) had critiqued that combination of

investment and commercial banking could be outcome of conflict of interest. Some might

provide importance to single type of bankings which provides less significant to other banking

type which does not create commercial sense. Services such as savings and current account give

convenient aspect for repaying bills with absence of hustle of inapplicable cash. On the similar

3

note Auer and et.al., (2019), stated that when one runs short of liquidity then bank is capable for

giving advance for recouping shortfall via other funds of depositories.

Ouenniche and Carrales (2018) stated that, regulations of banks helps for building

confidence in public and forming trust in country's banking system and ensure about safety of

public savings and mandatory for protecting public deposit. In the same series, credit control is

crucial aspect of banking regulation and prevents excess creation of credit through controlling

investments and loans. Banks ensure about fairness with context to financial services to every

customers with absence of discrimination related to sex, race, religion etc. whereas government

policy should be implemented on appropriate aspect for assisting nation's economic policy. On

the contrary, Geddes, Schmidt and Steffen (2018) has argued that there is presence of

unnecessary control along with heavy regulation might restricts banks for performing task on

freely basis so, banks are not capable for earning adequate margin. The regulations of banking

might control every unnecessary task but could not prevent to unnecessary failure as these are

very expensive and time consuming procedure.

As per views of Pardo, Knoerich and Li (2018), banks are referred as vital institutions in

society has significantly contributed for economic development via business facilitation. The

development of saving plans has been facilitated along with instrument of monetary strategy of

government through others. Clemens and Auer and et.al., (2019) has stated that, banks had made

availability of loans for various periods to trade, agriculture and industry which forms direct

investment in industrial sectors. They give agricultural, commercial and industrial consultancy

which facilitate procedure of economic development.

Impact of fluctuations in exchange rate on banking sector

According to Okoye and et.al., (2018), foreign exchange rate fluctuations impact banks in

direct and indirect manner. Its direct impact emerges from asset or liabilities holdings through

bank with reference to net payment streams denominated in foreign currency. The fluctuations in

foreign exchange rate changes values of domestic currency like assets as explicit source of risk

of foreign exchange are easiest for determining and could be hedged. On the contrary, Edwards

(2018) has stated that indirect source of risk are subtle and important and bank with absence of

foreign assets and liabilities could be exposed related to currency risk due of exchange rate

impact profitability of operations of domestic banking.

4

giving advance for recouping shortfall via other funds of depositories.

Ouenniche and Carrales (2018) stated that, regulations of banks helps for building

confidence in public and forming trust in country's banking system and ensure about safety of

public savings and mandatory for protecting public deposit. In the same series, credit control is

crucial aspect of banking regulation and prevents excess creation of credit through controlling

investments and loans. Banks ensure about fairness with context to financial services to every

customers with absence of discrimination related to sex, race, religion etc. whereas government

policy should be implemented on appropriate aspect for assisting nation's economic policy. On

the contrary, Geddes, Schmidt and Steffen (2018) has argued that there is presence of

unnecessary control along with heavy regulation might restricts banks for performing task on

freely basis so, banks are not capable for earning adequate margin. The regulations of banking

might control every unnecessary task but could not prevent to unnecessary failure as these are

very expensive and time consuming procedure.

As per views of Pardo, Knoerich and Li (2018), banks are referred as vital institutions in

society has significantly contributed for economic development via business facilitation. The

development of saving plans has been facilitated along with instrument of monetary strategy of

government through others. Clemens and Auer and et.al., (2019) has stated that, banks had made

availability of loans for various periods to trade, agriculture and industry which forms direct

investment in industrial sectors. They give agricultural, commercial and industrial consultancy

which facilitate procedure of economic development.

Impact of fluctuations in exchange rate on banking sector

According to Okoye and et.al., (2018), foreign exchange rate fluctuations impact banks in

direct and indirect manner. Its direct impact emerges from asset or liabilities holdings through

bank with reference to net payment streams denominated in foreign currency. The fluctuations in

foreign exchange rate changes values of domestic currency like assets as explicit source of risk

of foreign exchange are easiest for determining and could be hedged. On the contrary, Edwards

(2018) has stated that indirect source of risk are subtle and important and bank with absence of

foreign assets and liabilities could be exposed related to currency risk due of exchange rate

impact profitability of operations of domestic banking.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per views of Ibrahim, Belal and Ahmed (2018), maintaining the exchange risk

management as integral part of decision of every firm related to foreign currency exposure.

Currency risks has need of appropriate understanding of economic techniques and agents for

dealing with implication of consequent risk. Choosing proper degree of exposure of risk and

decision which is ought to be recouped. This is referred as critical problem which is referred as

focus of business unit. Mrabet and Alsamara (2018) has argued that, required of currency risk

management has acquired prominence in world around year 1973, after break down of Bre-Hon

woods system when US dollar was directly pegged to gold. The problem of management of

currency risk with context of non financial firms who are independent through core business is

dealt through corporate treasuries. Multiple banks have risk committees for observing treasury

strategy for managing interest and exchange rate which replicates significance of firm which

attaches risk techniques and issues.

Edwards (2018) stated that, sensitivity of bank profits and returns it exerts huge influence

on exchange and interest rate risks via traditional on-balance sheet operations of banking. Okoye

and et.al., (2018) posits that its international investors had managed risk of exchange rate on

internal aspect through perspective of assets and liabilities. On basis of this fact, exposure of

currency is on basis of transaction risk on its liabilities and assets denominated in foreign

currencies which tend for considering currencies as different asset class with mandate of overlay

currency. The foreign currency's price with context of local currency with significance of

understanding growth of every country throughout the world. The consequences of

misalignments of exchange rate lead to contraction of result and extensive economic hardships.

However, Edwards (2018) stated that there is presence of reasonably very strong evidence where

alignment of exchange rate has provided critical impact on rate of growth of per capital output

especially in countries of low income.

According to Mrabet and Alsamara (2018), exchange rate is referred as value of single

currency in term of any other currency as it matter to economy of Australia due to influence on

financial and trade flows among Australia and rest of the world. Alterations in exchange rate

impact Australian economy in two aspects such as direct impact on prices of services and goods

generated in Australia relative to price of services and goods produced overseas. Similarly,

indirect impact on inflation and economic activity as change in relative price of services and

goods generated domestically and overseas influences decision making on basis of consumption

5

management as integral part of decision of every firm related to foreign currency exposure.

Currency risks has need of appropriate understanding of economic techniques and agents for

dealing with implication of consequent risk. Choosing proper degree of exposure of risk and

decision which is ought to be recouped. This is referred as critical problem which is referred as

focus of business unit. Mrabet and Alsamara (2018) has argued that, required of currency risk

management has acquired prominence in world around year 1973, after break down of Bre-Hon

woods system when US dollar was directly pegged to gold. The problem of management of

currency risk with context of non financial firms who are independent through core business is

dealt through corporate treasuries. Multiple banks have risk committees for observing treasury

strategy for managing interest and exchange rate which replicates significance of firm which

attaches risk techniques and issues.

Edwards (2018) stated that, sensitivity of bank profits and returns it exerts huge influence

on exchange and interest rate risks via traditional on-balance sheet operations of banking. Okoye

and et.al., (2018) posits that its international investors had managed risk of exchange rate on

internal aspect through perspective of assets and liabilities. On basis of this fact, exposure of

currency is on basis of transaction risk on its liabilities and assets denominated in foreign

currencies which tend for considering currencies as different asset class with mandate of overlay

currency. The foreign currency's price with context of local currency with significance of

understanding growth of every country throughout the world. The consequences of

misalignments of exchange rate lead to contraction of result and extensive economic hardships.

However, Edwards (2018) stated that there is presence of reasonably very strong evidence where

alignment of exchange rate has provided critical impact on rate of growth of per capital output

especially in countries of low income.

According to Mrabet and Alsamara (2018), exchange rate is referred as value of single

currency in term of any other currency as it matter to economy of Australia due to influence on

financial and trade flows among Australia and rest of the world. Alterations in exchange rate

impact Australian economy in two aspects such as direct impact on prices of services and goods

generated in Australia relative to price of services and goods produced overseas. Similarly,

indirect impact on inflation and economic activity as change in relative price of services and

goods generated domestically and overseas influences decision making on basis of consumption

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and production. On the contrary, Ibrahim, Belal and Ahmed (2018) stated that by considering

both effects have presence of implications for purpose of balance of payments. The effects of

movement of exchange rate highlights main channel via these changes give direct impact on

Australian economy. For instance, if exchange rate among Australian and US dollar is 0.75 then

one AUD is transformed in US75c. Any increment in value of AUD is referred as appreciation

and decrement in value of AUD is known as depreciation.

Impact of interest rate on banking sector

As per views of Devarajan (2018), alterations in interest rates forms ripple effect via

financial system and impacting in various aspects. Increment in cash price is good for banks and

businesses of Australia but rise in rate of interest signifies rise in repayment for other loans and

mortgages as well. There are various Australians, extracts borrowing money harder whereas

personal finances are very expensive which doesn't bode time of reduced spending. However,

Drechsler, Savov and Schnabl (2018) said that, official cash rate is referred as lowest rate of

interest on which banks borrow through other banks. In simple words, rise in rate of interest rate

shows that it is very expensive for purpose of banks to borrow money and leading to specific

banks along with increment in rates to keep up.

According to Prabhakaran and Karthika (2018), banking sector has contributed

commendable role in sustaining and fuelling growth with context of economy. The saving of

nation could be mobilized and channelling with priorities of high investment and optimum

utilization of availability of resources. The risk related to interest rate is referred as exposure of

financial condition of bank till adverse movements in interest rate. The acceptance of this risk is

very normal for perspective of banking and could be referred as important source of shareholder

value and profitability. Conversely, Wilms, Swank and de Haan (2018) stated that excessive risk

of interest rate could pose significant threat to capital base and earnings of bank. Fluctuations in

interest rate impact earnings of bank through altering its net interest income along with level of

other interest sensitive income and operating expenses as well. In the similar aspect, it will also

impact underlying value of assets and liabilities of bank along with off balance sheet instruments

due to present value of future cash flows alters along with interest rate.

Drechsler, Savov and Schnabl (2018) stated that high real interest rates tends for

encouraging savings as it also identifies investment. Liberalization has been rated with lending

and low inflation promotes capital accumulation and economic growth in developing countries.

6

both effects have presence of implications for purpose of balance of payments. The effects of

movement of exchange rate highlights main channel via these changes give direct impact on

Australian economy. For instance, if exchange rate among Australian and US dollar is 0.75 then

one AUD is transformed in US75c. Any increment in value of AUD is referred as appreciation

and decrement in value of AUD is known as depreciation.

Impact of interest rate on banking sector

As per views of Devarajan (2018), alterations in interest rates forms ripple effect via

financial system and impacting in various aspects. Increment in cash price is good for banks and

businesses of Australia but rise in rate of interest signifies rise in repayment for other loans and

mortgages as well. There are various Australians, extracts borrowing money harder whereas

personal finances are very expensive which doesn't bode time of reduced spending. However,

Drechsler, Savov and Schnabl (2018) said that, official cash rate is referred as lowest rate of

interest on which banks borrow through other banks. In simple words, rise in rate of interest rate

shows that it is very expensive for purpose of banks to borrow money and leading to specific

banks along with increment in rates to keep up.

According to Prabhakaran and Karthika (2018), banking sector has contributed

commendable role in sustaining and fuelling growth with context of economy. The saving of

nation could be mobilized and channelling with priorities of high investment and optimum

utilization of availability of resources. The risk related to interest rate is referred as exposure of

financial condition of bank till adverse movements in interest rate. The acceptance of this risk is

very normal for perspective of banking and could be referred as important source of shareholder

value and profitability. Conversely, Wilms, Swank and de Haan (2018) stated that excessive risk

of interest rate could pose significant threat to capital base and earnings of bank. Fluctuations in

interest rate impact earnings of bank through altering its net interest income along with level of

other interest sensitive income and operating expenses as well. In the similar aspect, it will also

impact underlying value of assets and liabilities of bank along with off balance sheet instruments

due to present value of future cash flows alters along with interest rate.

Drechsler, Savov and Schnabl (2018) stated that high real interest rates tends for

encouraging savings as it also identifies investment. Liberalization has been rated with lending

and low inflation promotes capital accumulation and economic growth in developing countries.

6

There are various commercial banks which had raised holdings of its long term assets and

liabilities as their values are sensitive to changes in rate. These changes signify that managing the

lending interest rate risk is complex and important. On the contrary, Devarajan (2018) stated that

nature of business activity of bank along with overall risk level must be identified about

sophisticated management of interest must be managed. It would have process which enables

management of bank to determine, monitor, control and measure interest risk on timely aspect.

As per views of Drechsler, Savov and Schnabl (2018), profitability of banking sector

raise with hike in interest rate. There are various institutions in this banking sector like

commercial and retail banks, insurance organizations, investment banks along with brokerage

have massive cash holdings due to business activities and customer balances. The rise in interest

rate will directly impact on raising yield on cash and proceeds directly to earnings. However,

Prabhakaran and Karthika (2018) states that benefit of higher interest rate is notable for

commercial and regional banks and brokerage as well. The organization which holds cash of

customer in accounts which pay out set interest rate is below short term rates. Further profit off

of marginal variation among yield which is generated with invested cash in short term notes

along with interest paid out to consumers. If there is raise in rate then spread increases along with

extra income to earnings.

According to Wilms, Swank and de Haan (2018), indirect method with hike of interest

rate raises profitability for banking sector which tends to incur in environment where economic

growth is strong and increment in bond yields. With these conditions, business and consumer

demand for loans spike would directly augment bank's earnings. However, Prabhakaran and

Karthika (2018) stated that rise in interest rate would raise profitability on loan with presence of

huge spread among federal fund rate and bank charges to its specific customers. The spread

among short term and long term rate will expand with hike of interest rate due to long term rates

tend to increase faster compared to short term rates. It is very true for rate hike as it shows

underlying conditions along with inflationary pressures which directly tends for prompting

increment in interest rate as it is optimal confluence for bank events which borrow on short term

aspect and lend with perspective of long term basis.

Role of reserve bank monetary policy on economic growth

According to Gambacorta and Shin (2018), reserve bank of Australia is central bank as it

conducts monetary policy and works for maintaining strong financial system and issues currency

7

liabilities as their values are sensitive to changes in rate. These changes signify that managing the

lending interest rate risk is complex and important. On the contrary, Devarajan (2018) stated that

nature of business activity of bank along with overall risk level must be identified about

sophisticated management of interest must be managed. It would have process which enables

management of bank to determine, monitor, control and measure interest risk on timely aspect.

As per views of Drechsler, Savov and Schnabl (2018), profitability of banking sector

raise with hike in interest rate. There are various institutions in this banking sector like

commercial and retail banks, insurance organizations, investment banks along with brokerage

have massive cash holdings due to business activities and customer balances. The rise in interest

rate will directly impact on raising yield on cash and proceeds directly to earnings. However,

Prabhakaran and Karthika (2018) states that benefit of higher interest rate is notable for

commercial and regional banks and brokerage as well. The organization which holds cash of

customer in accounts which pay out set interest rate is below short term rates. Further profit off

of marginal variation among yield which is generated with invested cash in short term notes

along with interest paid out to consumers. If there is raise in rate then spread increases along with

extra income to earnings.

According to Wilms, Swank and de Haan (2018), indirect method with hike of interest

rate raises profitability for banking sector which tends to incur in environment where economic

growth is strong and increment in bond yields. With these conditions, business and consumer

demand for loans spike would directly augment bank's earnings. However, Prabhakaran and

Karthika (2018) stated that rise in interest rate would raise profitability on loan with presence of

huge spread among federal fund rate and bank charges to its specific customers. The spread

among short term and long term rate will expand with hike of interest rate due to long term rates

tend to increase faster compared to short term rates. It is very true for rate hike as it shows

underlying conditions along with inflationary pressures which directly tends for prompting

increment in interest rate as it is optimal confluence for bank events which borrow on short term

aspect and lend with perspective of long term basis.

Role of reserve bank monetary policy on economic growth

According to Gambacorta and Shin (2018), reserve bank of Australia is central bank as it

conducts monetary policy and works for maintaining strong financial system and issues currency

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of nation. With well being of policy making body, reserve bank gives services of banking and

registry to particular range of agencies of government till number of overseas official institutions

and central banks. In the similar aspect, it manages gold and foreign exchange reserves of

Australia. On the contrary, Su and et.al., (2018) has stated that functions and role of reserve bank

in underpinned with different pieces of legislation. The bank is referred as statutory authority

which established act of parliament, reserve bank act 1959 which had provided specific

obligations and powers. With context of this act boards are categorised in two types which are

reserve bank board and payments system board.

As per views of Groenewold (2018), monetary policy is conducted for attaining its

objectives of board of reserve bank. It is referred as board responsibility for setting interest rate

in such aspect that directly contribute to currency's stability, economic prosperity, full

employment and welfare of Australia people. However, Hamza and Saadaoui (2018) states that

to attain price stability, reserve bank implies flexible medium term target inflation with objective

of inflation in 2 and 3%. In the similar aspect, cash rate is set for purpose of influencing

economic activity for attaining goal.

Su and et.al., (2018) states that, price stability is maintained by controlling level of

money supply as it plays stabilizing role for purpose of influencing economic growth via

numerous channels. Consequently, scope of this role might be limited with concurrent pursuit of

various other primary objectives of monetary policy with its nature and transmission mechanism.

The other factors such as uncertainty faced through policy makers along with stance of economic

policies and concurrent target of its intermediate objectives might have implications for attaining

ultimate objective to gain sustainable growth.

On the contrary, Gambacorta and Shin (2018) argued that decision of monetary policy

cuts interest rate for instance, lowering borrowing cost, outcome of higher investment activity

and buying various other consumer durables. The expectation related to economic activity would

strengthen and might prompt banks for ease of lending policy and enables households and

business for boost spending. With reference to low interest rate regime, stocks are attractive to

purchase along with increment in household financial assets. This might contribute for huge

consumer spending and organization's investment project are highly attractive. Lower rate of

interest tends for cause of depreciating in currency due to high demand for domestic goods

8

registry to particular range of agencies of government till number of overseas official institutions

and central banks. In the similar aspect, it manages gold and foreign exchange reserves of

Australia. On the contrary, Su and et.al., (2018) has stated that functions and role of reserve bank

in underpinned with different pieces of legislation. The bank is referred as statutory authority

which established act of parliament, reserve bank act 1959 which had provided specific

obligations and powers. With context of this act boards are categorised in two types which are

reserve bank board and payments system board.

As per views of Groenewold (2018), monetary policy is conducted for attaining its

objectives of board of reserve bank. It is referred as board responsibility for setting interest rate

in such aspect that directly contribute to currency's stability, economic prosperity, full

employment and welfare of Australia people. However, Hamza and Saadaoui (2018) states that

to attain price stability, reserve bank implies flexible medium term target inflation with objective

of inflation in 2 and 3%. In the similar aspect, cash rate is set for purpose of influencing

economic activity for attaining goal.

Su and et.al., (2018) states that, price stability is maintained by controlling level of

money supply as it plays stabilizing role for purpose of influencing economic growth via

numerous channels. Consequently, scope of this role might be limited with concurrent pursuit of

various other primary objectives of monetary policy with its nature and transmission mechanism.

The other factors such as uncertainty faced through policy makers along with stance of economic

policies and concurrent target of its intermediate objectives might have implications for attaining

ultimate objective to gain sustainable growth.

On the contrary, Gambacorta and Shin (2018) argued that decision of monetary policy

cuts interest rate for instance, lowering borrowing cost, outcome of higher investment activity

and buying various other consumer durables. The expectation related to economic activity would

strengthen and might prompt banks for ease of lending policy and enables households and

business for boost spending. With reference to low interest rate regime, stocks are attractive to

purchase along with increment in household financial assets. This might contribute for huge

consumer spending and organization's investment project are highly attractive. Lower rate of

interest tends for cause of depreciating in currency due to high demand for domestic goods

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

where imported goods are very expensive. Furthermore, combination of these particular factor

increases result along with employment, consumer spending and investment as well.

CONCLUSION

On basis of above report it could be concluded that Australian banking sector influence

economic growth on both positive and negative aspect. It had shown that financial system plays

very important role in economy as it thrives for financial intermediation with its capabilities of

financial instruments as they allow for lending and gaining money on deposit. In the similar

context, it had reflected that fluctuations in exchange rate affects entire banking industry in both

direct and indirect manner as it is integral part of firm's decision on basis of exposure of foreign

currency. Thus, interest rate plays very significant role in banking sector as it forms ripple effect

by financial system. Henceforth, it had shown that most important is role of reserve bank

monetary policy affected economic growth as it helps in attaining objectives of reserve bank

board.

9

increases result along with employment, consumer spending and investment as well.

CONCLUSION

On basis of above report it could be concluded that Australian banking sector influence

economic growth on both positive and negative aspect. It had shown that financial system plays

very important role in economy as it thrives for financial intermediation with its capabilities of

financial instruments as they allow for lending and gaining money on deposit. In the similar

context, it had reflected that fluctuations in exchange rate affects entire banking industry in both

direct and indirect manner as it is integral part of firm's decision on basis of exposure of foreign

currency. Thus, interest rate plays very significant role in banking sector as it forms ripple effect

by financial system. Henceforth, it had shown that most important is role of reserve bank

monetary policy affected economic growth as it helps in attaining objectives of reserve bank

board.

9

REFERENCES

Books and Journals

Auer, S. and et.al., 2019. International monetary policy transmission through banks in small open

economies. Journal of International Money and Finance. 90. pp.34-53.

Devarajan, S., 2018. The impact of macroeconomic variables on the profitability of public and

private sector banks in India; A structural equation modeling approach. ACADEMICIA: An

International Multidisciplinary Research Journal. 8(1). pp.44-77.

Drechsler, I., Savov, A. and Schnabl, P., 2018. Banking on deposits: Maturity transformation

without interest rate risk(No. w24582). National Bureau of Economic Research.

Edwards, S., 2018. Exchange rate puzzles and dilemmas: how can policymakers

respond?. Contributed Papers (cont). p.144.

Gambacorta, L. and Shin, H. S., 2018. Why bank capital matters for monetary policy. Journal of

Financial Intermediation. 35. pp.17-29.

Geddes, A., Schmidt, T. S. and Steffen, B., 2018. The multiple roles of state investment banks in

low-carbon energy finance: An analysis of Australia, the UK and Germany. Energy

Policy. 115. pp.158-170.

Groenewold, N., 2018. Australia saved from the financial crisis by policy or by exports?. Journal

of Policy Modeling. 40(1). pp.118-135.

Hamza, H. and Saadaoui, Z., 2018. Monetary transmission through the debt financing channel of

Islamic banks: Does PSIA play a role?. Research in International Business and

Finance. 45. pp.557-570.

Ibrahim, A., Belal, M. and Ahmed, S. A. K., 2018. Impact Of Fiscal Policy Shocks On Official

Versus Parallel Exchange Rate Of Sudan: Under Long-Term Economic Sanction And

South Sudan Reverondum (1997-2017). ABC Research Alert. 6(1).

Mrabet, Z. and Alsamara, M., 2018. The impact of parallel market exchange rate volatility and

oil exports on real GDP in Syria: Evidence from the ARDL approach. The Journal of

International Trade & Economic Development. 27(3). pp.333-349.

Okoye, L. U. and et.al., 2018. EXAMINATION OF CAUSAL RELATIONSHIP BETWEEN

TRADE OPENNESS, EXCHANGE RATE CHANGES AND MANUFACTURING

CAPACITY UTILIZATION. DUTSE. JOURNAL OF ECONOMICS AND

DEVELOPMENT STUDIES (DUJEDS). 4(2).

Ouenniche, J. and Carrales, S., 2018. Assessing efficiency profiles of UK commercial banks: a

DEA analysis with regression-based feedback. Annals of Operations Research. 266(1-2).

pp.551-587.

Pacheco Pardo, R., Knoerich, J. and Li, Y., 2018. The Role of London and Frankfurt in

Supporting the Internationalisation of the Chinese Renminbi. New Political Economy,

pp.1-16.

Prabhakaran, K. and Karthika, P., 2018. Impact of Oil Price and Macroeconomic Variables on

the Profitability-A Study on Bank Muscat, Sultanate of Oman. International Journal on

Global Business Management & Research. 7(2). pp.28-38.

10

Books and Journals

Auer, S. and et.al., 2019. International monetary policy transmission through banks in small open

economies. Journal of International Money and Finance. 90. pp.34-53.

Devarajan, S., 2018. The impact of macroeconomic variables on the profitability of public and

private sector banks in India; A structural equation modeling approach. ACADEMICIA: An

International Multidisciplinary Research Journal. 8(1). pp.44-77.

Drechsler, I., Savov, A. and Schnabl, P., 2018. Banking on deposits: Maturity transformation

without interest rate risk(No. w24582). National Bureau of Economic Research.

Edwards, S., 2018. Exchange rate puzzles and dilemmas: how can policymakers

respond?. Contributed Papers (cont). p.144.

Gambacorta, L. and Shin, H. S., 2018. Why bank capital matters for monetary policy. Journal of

Financial Intermediation. 35. pp.17-29.

Geddes, A., Schmidt, T. S. and Steffen, B., 2018. The multiple roles of state investment banks in

low-carbon energy finance: An analysis of Australia, the UK and Germany. Energy

Policy. 115. pp.158-170.

Groenewold, N., 2018. Australia saved from the financial crisis by policy or by exports?. Journal

of Policy Modeling. 40(1). pp.118-135.

Hamza, H. and Saadaoui, Z., 2018. Monetary transmission through the debt financing channel of

Islamic banks: Does PSIA play a role?. Research in International Business and

Finance. 45. pp.557-570.

Ibrahim, A., Belal, M. and Ahmed, S. A. K., 2018. Impact Of Fiscal Policy Shocks On Official

Versus Parallel Exchange Rate Of Sudan: Under Long-Term Economic Sanction And

South Sudan Reverondum (1997-2017). ABC Research Alert. 6(1).

Mrabet, Z. and Alsamara, M., 2018. The impact of parallel market exchange rate volatility and

oil exports on real GDP in Syria: Evidence from the ARDL approach. The Journal of

International Trade & Economic Development. 27(3). pp.333-349.

Okoye, L. U. and et.al., 2018. EXAMINATION OF CAUSAL RELATIONSHIP BETWEEN

TRADE OPENNESS, EXCHANGE RATE CHANGES AND MANUFACTURING

CAPACITY UTILIZATION. DUTSE. JOURNAL OF ECONOMICS AND

DEVELOPMENT STUDIES (DUJEDS). 4(2).

Ouenniche, J. and Carrales, S., 2018. Assessing efficiency profiles of UK commercial banks: a

DEA analysis with regression-based feedback. Annals of Operations Research. 266(1-2).

pp.551-587.

Pacheco Pardo, R., Knoerich, J. and Li, Y., 2018. The Role of London and Frankfurt in

Supporting the Internationalisation of the Chinese Renminbi. New Political Economy,

pp.1-16.

Prabhakaran, K. and Karthika, P., 2018. Impact of Oil Price and Macroeconomic Variables on

the Profitability-A Study on Bank Muscat, Sultanate of Oman. International Journal on

Global Business Management & Research. 7(2). pp.28-38.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.