Analysis of the Australian Construction Industry: HC1072 Report

VerifiedAdded on 2023/01/19

|14

|2705

|36

Report

AI Summary

This report provides a comprehensive analysis of the Australian construction industry. It begins with an introduction highlighting the industry's significance to the Australian economy, its contribution to GDP, and employment figures. The report then delves into the market structure, examining the different sectors (engineering, non-domestic, and domestic building), the dominance of small firms, and the concentration of market power among large contractors. The report further explores factors influencing demand, including government policies, economic conditions, and inflation. Supply-side factors such as urbanization and grants are also considered. Product elasticity within the industry is discussed, followed by an examination of the challenges posed by an aging workforce and skill shortages. The report concludes by emphasizing the importance of industry structure to industrial economics and the implications of the findings.

1

Name

Professor

Institution

Course

Date

Construction Industry in Australia

Name

Professor

Institution

Course

Date

Construction Industry in Australia

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

1.0 Introduction 3

2.0 Market share …………………………………………………………….…………………….4

2.1 market sectors in the construction Industry 6

3.0 Factors That Influence Demand For Construction Products(demand side factors) 8

3.1 Government Policies 9

3.2 Economic Conditions…………..……………….………………………………,,…………9

3.3 Inflation……..………………………………………………………………,……,……….9

4.0 Supply Side Factors………..…….......……………………………………….…….…………9

4.1 Urbanization…..…….……………………………………………………..………………..9

4.2 Grants……..…….…….……………………………………………….……………………9

5.0 Product Elasticity In Construction Industry…………………………………………………10

6.0 Aging workforce and shortages of skills affects the construction Industry…………………11

6.1 Impacts of the aging population…..……………………………………………………….12

7.0 Conclusion…………………………...………………………………………………………13

Table of Contents

1.0 Introduction 3

2.0 Market share …………………………………………………………….…………………….4

2.1 market sectors in the construction Industry 6

3.0 Factors That Influence Demand For Construction Products(demand side factors) 8

3.1 Government Policies 9

3.2 Economic Conditions…………..……………….………………………………,,…………9

3.3 Inflation……..………………………………………………………………,……,……….9

4.0 Supply Side Factors………..…….......……………………………………….…….…………9

4.1 Urbanization…..…….……………………………………………………..………………..9

4.2 Grants……..…….…….……………………………………………….……………………9

5.0 Product Elasticity In Construction Industry…………………………………………………10

6.0 Aging workforce and shortages of skills affects the construction Industry…………………11

6.1 Impacts of the aging population…..……………………………………………………….12

7.0 Conclusion…………………………...………………………………………………………13

3

1. INTRODUCTION

Construction industry in Australia is one of the primary drivers of Australia’s budget. The

industry is Australia’s third contributor after mining and Finance. It generates approximately 8%

of the GDP in its value added terms. The industry is made up of more than 330,000 businesses

around the whole country and has employed more than one million people which is roughly 9%

of the total labor force (Myers, 2016, p. 45). The business is involved in the production of

erections and infrastructure that are indispensable to the setup of all other industries. The

industry also supplements the capital stock of the country and reinforces the developments that

are vital to support the country’s affluence and incomes.

In the financial year 2014/2015, the direct construction output amounted to 7.8% of the

Australia’s total output which was an improvement from 6.6% ten years ago. The latter is what

made the construction industry Australia’s third largest contributor of the country’s GDP as far

as the volume of output is concerned. Only the financial and mining sectors contributed more

than that. The construction industry also supports supply chains both downstream and up stream.

The building industry is the third largest commissioning business in Australia having

recorded 1.05 million employees as of 2015.Most of these workers are employees in the trade

sector. Employment in this industry has been associated with the solid recovery that took place in

2013 and the growth that extended across 2014. The biggest level of building segment is the

building installation services followed by the building completion services and then the other

constructions services follow suit.

1. INTRODUCTION

Construction industry in Australia is one of the primary drivers of Australia’s budget. The

industry is Australia’s third contributor after mining and Finance. It generates approximately 8%

of the GDP in its value added terms. The industry is made up of more than 330,000 businesses

around the whole country and has employed more than one million people which is roughly 9%

of the total labor force (Myers, 2016, p. 45). The business is involved in the production of

erections and infrastructure that are indispensable to the setup of all other industries. The

industry also supplements the capital stock of the country and reinforces the developments that

are vital to support the country’s affluence and incomes.

In the financial year 2014/2015, the direct construction output amounted to 7.8% of the

Australia’s total output which was an improvement from 6.6% ten years ago. The latter is what

made the construction industry Australia’s third largest contributor of the country’s GDP as far

as the volume of output is concerned. Only the financial and mining sectors contributed more

than that. The construction industry also supports supply chains both downstream and up stream.

The building industry is the third largest commissioning business in Australia having

recorded 1.05 million employees as of 2015.Most of these workers are employees in the trade

sector. Employment in this industry has been associated with the solid recovery that took place in

2013 and the growth that extended across 2014. The biggest level of building segment is the

building installation services followed by the building completion services and then the other

constructions services follow suit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

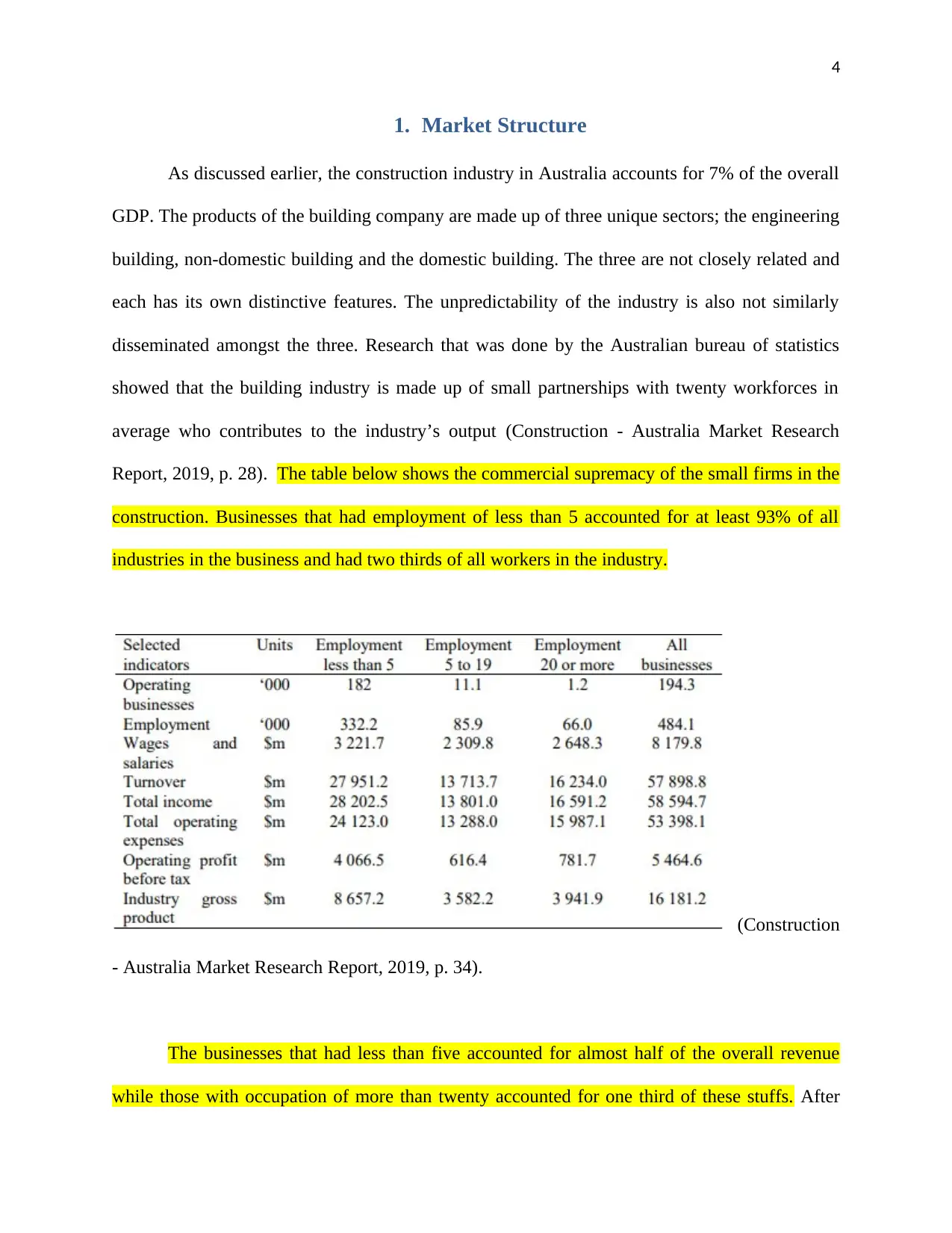

1. Market Structure

As discussed earlier, the construction industry in Australia accounts for 7% of the overall

GDP. The products of the building company are made up of three unique sectors; the engineering

building, non-domestic building and the domestic building. The three are not closely related and

each has its own distinctive features. The unpredictability of the industry is also not similarly

disseminated amongst the three. Research that was done by the Australian bureau of statistics

showed that the building industry is made up of small partnerships with twenty workforces in

average who contributes to the industry’s output (Construction - Australia Market Research

Report, 2019, p. 28). The table below shows the commercial supremacy of the small firms in the

construction. Businesses that had employment of less than 5 accounted for at least 93% of all

industries in the business and had two thirds of all workers in the industry.

(Construction

- Australia Market Research Report, 2019, p. 34).

The businesses that had less than five accounted for almost half of the overall revenue

while those with occupation of more than twenty accounted for one third of these stuffs. After

1. Market Structure

As discussed earlier, the construction industry in Australia accounts for 7% of the overall

GDP. The products of the building company are made up of three unique sectors; the engineering

building, non-domestic building and the domestic building. The three are not closely related and

each has its own distinctive features. The unpredictability of the industry is also not similarly

disseminated amongst the three. Research that was done by the Australian bureau of statistics

showed that the building industry is made up of small partnerships with twenty workforces in

average who contributes to the industry’s output (Construction - Australia Market Research

Report, 2019, p. 28). The table below shows the commercial supremacy of the small firms in the

construction. Businesses that had employment of less than 5 accounted for at least 93% of all

industries in the business and had two thirds of all workers in the industry.

(Construction

- Australia Market Research Report, 2019, p. 34).

The businesses that had less than five accounted for almost half of the overall revenue

while those with occupation of more than twenty accounted for one third of these stuffs. After

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

the data on recital is transformed to percentage, the significance of large firms is identical. Their

13% of employee make 32% of the incomes, and nearly 25% of output. The major free-lancers

belong to the Australian Contractors Association.an industry can from this view be seen as

having high concentration with the major companies accounting for more than half of

manufacturing’s production in the non-housing buildings and engineering building subdivisions.

The principal corporations in the industry therefore lead the business output and also the business

cash flow. The business assembly adopts the form of a pyramid with 20 very large outworkers

and a few large outworkers at the top while numerous minor subcontractors lie in the

bottommost segment.

2.1 Market Sectors in the Construction Industry

Industries are in most cases seen in terms of the number of firms which progress along a

mono flight and these companies contest in the enhancement of the quality of their distinct forms

of the homogenous products. The later view fits the construction company. The products in the

construction industry are close substitutes from the consumption perspective but the technologies

used is different whereby the R & D schemes employed enhance goods in one group and may

form spill overs for goods in some other groups. The complexity of the substitutability has been

in the construction industry for many years (Jason , 2018, p. 45). In a circumstance whereby the

industries are broken down into sub industries in order to address the issue of homogeneity, the

products are differentiated by their companies.

A number of issues come up when we apply the discussion of the existence of variety of

sub markets. The first issue is of course the lack of specialization for the companies in terms of

the products that they produce. The answer to the question of the kind of products a given

the data on recital is transformed to percentage, the significance of large firms is identical. Their

13% of employee make 32% of the incomes, and nearly 25% of output. The major free-lancers

belong to the Australian Contractors Association.an industry can from this view be seen as

having high concentration with the major companies accounting for more than half of

manufacturing’s production in the non-housing buildings and engineering building subdivisions.

The principal corporations in the industry therefore lead the business output and also the business

cash flow. The business assembly adopts the form of a pyramid with 20 very large outworkers

and a few large outworkers at the top while numerous minor subcontractors lie in the

bottommost segment.

2.1 Market Sectors in the Construction Industry

Industries are in most cases seen in terms of the number of firms which progress along a

mono flight and these companies contest in the enhancement of the quality of their distinct forms

of the homogenous products. The later view fits the construction company. The products in the

construction industry are close substitutes from the consumption perspective but the technologies

used is different whereby the R & D schemes employed enhance goods in one group and may

form spill overs for goods in some other groups. The complexity of the substitutability has been

in the construction industry for many years (Jason , 2018, p. 45). In a circumstance whereby the

industries are broken down into sub industries in order to address the issue of homogeneity, the

products are differentiated by their companies.

A number of issues come up when we apply the discussion of the existence of variety of

sub markets. The first issue is of course the lack of specialization for the companies in terms of

the products that they produce. The answer to the question of the kind of products a given

6

business creates varies across the industries. The answers are different since some industries

believe that the industry delivers amenities while others trust that the industries produce

products. The former believes that the key job of the construction is the coordination of the

industry progressions while the latter group believes that the chief duty of the building industry

is the building tasks itself (Lawrence & Nehring, 2015, p. 56).

When the construction business is evaluated in terms of blockades to entry, there comes

up two levels of operations. There exists very limited barriers to entry in the construction market

and these barriers are expected to continue being low given that the industry will maintain the

ongoing practices based on the large number of small and specialized contractors. The number of

contactors who are proficient in handling large schemes is low and the barriers at this level on

the manner of unqualified managers are evident. Due to high risks, the contractor for large

projects is required to show great skills in management and coordination of such works

(McNally, 2017, p. 132).

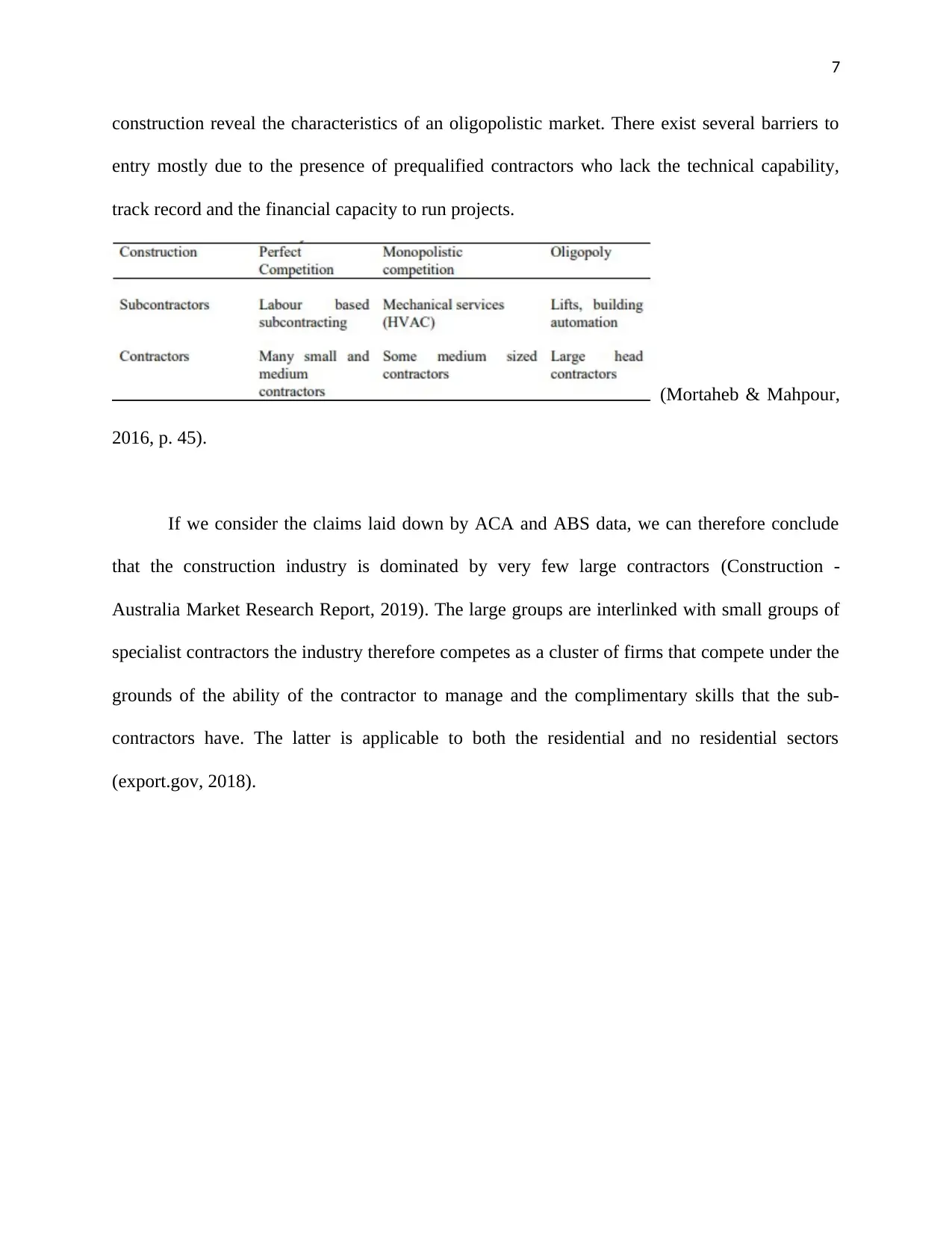

Monopolistic competition is more intensive for the subcontractors in the heating,

ventilation and air conditioning sector. This sector in the construction industry has four major

large firms in Australia and many smaller firms in the local markets the medium firm contractors

who operate with particular types of buildings also have established links with the clients in that

category. Only the small scale firms are ideal for the prefect competition model (Australian

Bureau of Statistics, 2019). The degree of monopoly power exercised by the large firms is

expressed by the use of concentration ratio which basically makes use of the four largest firms in

the industry which are ranked according to the share of their sales expressed in percentage form

accounted by the largest four firms. The large contractors in the engineering and non-residential

business creates varies across the industries. The answers are different since some industries

believe that the industry delivers amenities while others trust that the industries produce

products. The former believes that the key job of the construction is the coordination of the

industry progressions while the latter group believes that the chief duty of the building industry

is the building tasks itself (Lawrence & Nehring, 2015, p. 56).

When the construction business is evaluated in terms of blockades to entry, there comes

up two levels of operations. There exists very limited barriers to entry in the construction market

and these barriers are expected to continue being low given that the industry will maintain the

ongoing practices based on the large number of small and specialized contractors. The number of

contactors who are proficient in handling large schemes is low and the barriers at this level on

the manner of unqualified managers are evident. Due to high risks, the contractor for large

projects is required to show great skills in management and coordination of such works

(McNally, 2017, p. 132).

Monopolistic competition is more intensive for the subcontractors in the heating,

ventilation and air conditioning sector. This sector in the construction industry has four major

large firms in Australia and many smaller firms in the local markets the medium firm contractors

who operate with particular types of buildings also have established links with the clients in that

category. Only the small scale firms are ideal for the prefect competition model (Australian

Bureau of Statistics, 2019). The degree of monopoly power exercised by the large firms is

expressed by the use of concentration ratio which basically makes use of the four largest firms in

the industry which are ranked according to the share of their sales expressed in percentage form

accounted by the largest four firms. The large contractors in the engineering and non-residential

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

construction reveal the characteristics of an oligopolistic market. There exist several barriers to

entry mostly due to the presence of prequalified contractors who lack the technical capability,

track record and the financial capacity to run projects.

(Mortaheb & Mahpour,

2016, p. 45).

If we consider the claims laid down by ACA and ABS data, we can therefore conclude

that the construction industry is dominated by very few large contractors (Construction -

Australia Market Research Report, 2019). The large groups are interlinked with small groups of

specialist contractors the industry therefore competes as a cluster of firms that compete under the

grounds of the ability of the contractor to manage and the complimentary skills that the sub-

contractors have. The latter is applicable to both the residential and no residential sectors

(export.gov, 2018).

construction reveal the characteristics of an oligopolistic market. There exist several barriers to

entry mostly due to the presence of prequalified contractors who lack the technical capability,

track record and the financial capacity to run projects.

(Mortaheb & Mahpour,

2016, p. 45).

If we consider the claims laid down by ACA and ABS data, we can therefore conclude

that the construction industry is dominated by very few large contractors (Construction -

Australia Market Research Report, 2019). The large groups are interlinked with small groups of

specialist contractors the industry therefore competes as a cluster of firms that compete under the

grounds of the ability of the contractor to manage and the complimentary skills that the sub-

contractors have. The latter is applicable to both the residential and no residential sectors

(export.gov, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

3.0 Factors That Influence Demand for Construction Products (Demand Side

Factors)

3.1 Government policies

The Australian government has taken the responsibility to promote the private sector

infrastructure development and telecommunication. The government has introduced the

mandatory participation in infrastructure for development (Joe, 2018, p. 25).

3.2 Economic conditions

Economic growth has focused mainly on the manufacturing sector rather than the

dominant agricultural sector. Growth in construction has been tremendous in the recent past.

3.3 Inflation

Increased cost indices are clear indicators of a rising cost in construction in the domestic

industry. The main reason for the rising cost is inflation. This factor together with the high costs

is expected to affect the construction activities to a large extent (Gerard de , 2017, p. 23).

4.0 Supply Side Factors

4.1 Urbanization

Urban population growth is high in Australia is accelerating. The growth in population

has led to the growth of cities leading to the conversion of marshy areas to suburbs (McNally,

2017, p. 243). The latter has led to an increased demand in apartment construction and pre-

constructed houses since the construction is limited by the land area.

3.0 Factors That Influence Demand for Construction Products (Demand Side

Factors)

3.1 Government policies

The Australian government has taken the responsibility to promote the private sector

infrastructure development and telecommunication. The government has introduced the

mandatory participation in infrastructure for development (Joe, 2018, p. 25).

3.2 Economic conditions

Economic growth has focused mainly on the manufacturing sector rather than the

dominant agricultural sector. Growth in construction has been tremendous in the recent past.

3.3 Inflation

Increased cost indices are clear indicators of a rising cost in construction in the domestic

industry. The main reason for the rising cost is inflation. This factor together with the high costs

is expected to affect the construction activities to a large extent (Gerard de , 2017, p. 23).

4.0 Supply Side Factors

4.1 Urbanization

Urban population growth is high in Australia is accelerating. The growth in population

has led to the growth of cities leading to the conversion of marshy areas to suburbs (McNally,

2017, p. 243). The latter has led to an increased demand in apartment construction and pre-

constructed houses since the construction is limited by the land area.

9

4.2 Grants

Foreign grants are vital for Australia to continue with the desired level of public

investment. Public investment will include the investment in construction sector. Investment in

construction industry will reduce the gap between savings and investment (Myers, 2016, p. 136).

With an increase in the participation of the private sector, there is need for more loans for the

private sectors to mobilize the other resources so as to contribute to the construction industry.

4. Product Elasticity in the Construction Industry

Price elasticity shows that housing prices increase with increase in land price- increasing

the price of inputs increases the price for houses. Supply elasticity of construction industry

products is huge since the response from the buyers is immediate from most markets. The short

term elasticity will tend to dominate as prices are sticky downwards (Lawrence & Nehring, 2015,

p. 476).

The rental market is highly elastic to prices meaning that rents do not rise relative to the

incomes since the renters can easily withdraw. The investors are easily attracted to the increase

in prices (Satyanarayan , 2014, p. 34). On the other hand, research done by ABS show that the

home owners care less about the changes in prices.

5. Aging Workforce and Shortages of Skills Affects the Construction Industry

Australia has been experiencing a housing boom but the aging population experienced

means that there will be fewer workers who will be capable of providing services to the

construction industry (Jason , 2018, p. 4). The industry has tried to curb this issue by utilizing

both the technological and social methods. Ageing population means that people are living

4.2 Grants

Foreign grants are vital for Australia to continue with the desired level of public

investment. Public investment will include the investment in construction sector. Investment in

construction industry will reduce the gap between savings and investment (Myers, 2016, p. 136).

With an increase in the participation of the private sector, there is need for more loans for the

private sectors to mobilize the other resources so as to contribute to the construction industry.

4. Product Elasticity in the Construction Industry

Price elasticity shows that housing prices increase with increase in land price- increasing

the price of inputs increases the price for houses. Supply elasticity of construction industry

products is huge since the response from the buyers is immediate from most markets. The short

term elasticity will tend to dominate as prices are sticky downwards (Lawrence & Nehring, 2015,

p. 476).

The rental market is highly elastic to prices meaning that rents do not rise relative to the

incomes since the renters can easily withdraw. The investors are easily attracted to the increase

in prices (Satyanarayan , 2014, p. 34). On the other hand, research done by ABS show that the

home owners care less about the changes in prices.

5. Aging Workforce and Shortages of Skills Affects the Construction Industry

Australia has been experiencing a housing boom but the aging population experienced

means that there will be fewer workers who will be capable of providing services to the

construction industry (Jason , 2018, p. 4). The industry has tried to curb this issue by utilizing

both the technological and social methods. Ageing population means that people are living

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

longer and few babies are being born and this poses a big problem for the Australian workforce

(Satyanarayan , 2014, p. 1).

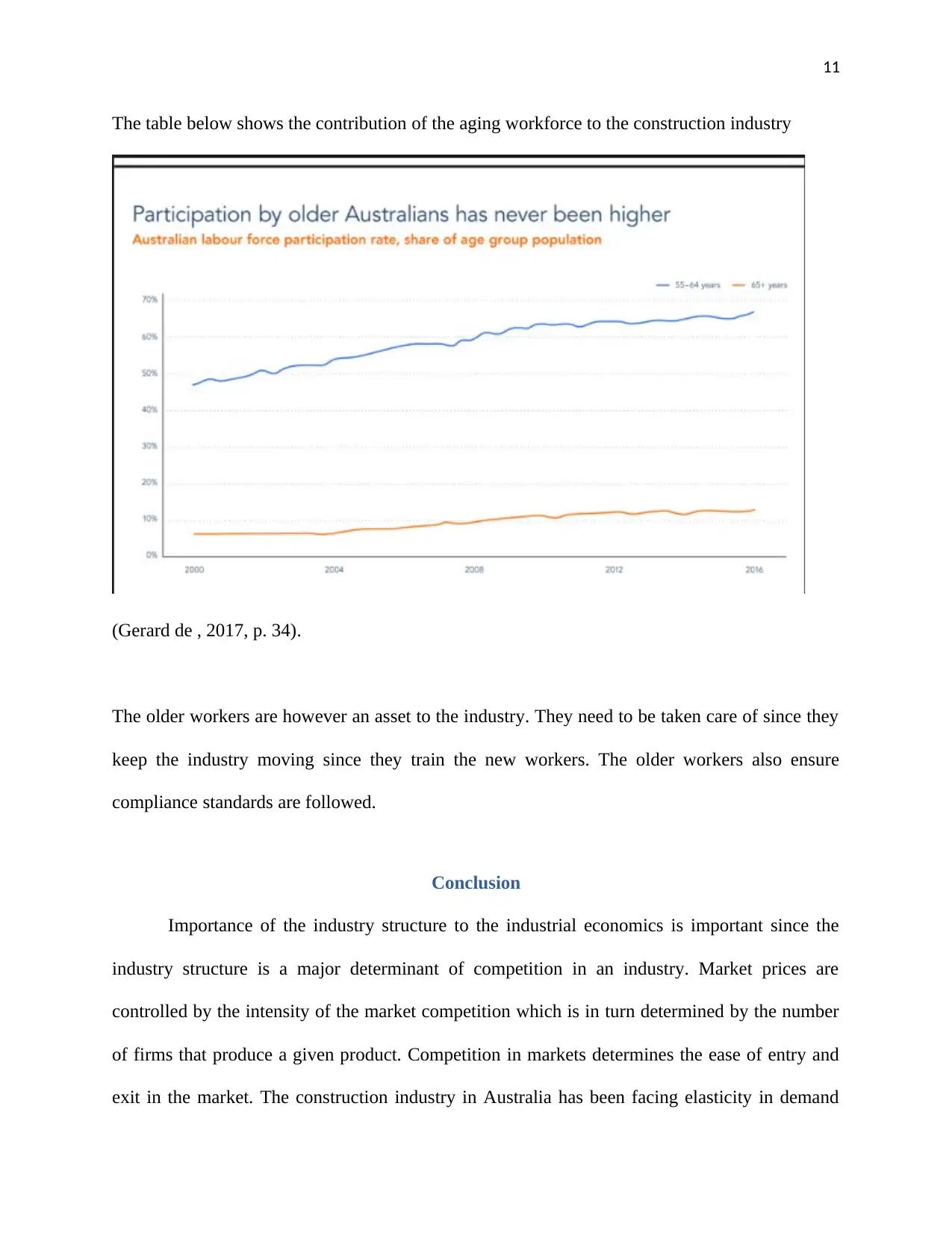

6.1 Impacts of the aging population

Research done by the ABS shows that by the year 2035, more than 20% of the

Australia’s workforce will be above 65 and this will increase tremendously by 2050.there is a

possibility that there will be 3 workers for every persons who are aged above 65 years by

2050.another study carried out by the construction skills queens land found out that over the last

twenty years, the number of workers in the construction industry who were aged above 55 rose

from 8% to 15% and this as a clear representation of a trend running throughout the nation

(Mortaheb & Mahpour, 2016, p. 44). Since there is a trend of retiring later, the older workers will

continue to work in the construction sector. There is a problem since the older people become,

the more they become less flexible and hence their contribution to the labor force diminishes at

an increasing rate.

longer and few babies are being born and this poses a big problem for the Australian workforce

(Satyanarayan , 2014, p. 1).

6.1 Impacts of the aging population

Research done by the ABS shows that by the year 2035, more than 20% of the

Australia’s workforce will be above 65 and this will increase tremendously by 2050.there is a

possibility that there will be 3 workers for every persons who are aged above 65 years by

2050.another study carried out by the construction skills queens land found out that over the last

twenty years, the number of workers in the construction industry who were aged above 55 rose

from 8% to 15% and this as a clear representation of a trend running throughout the nation

(Mortaheb & Mahpour, 2016, p. 44). Since there is a trend of retiring later, the older workers will

continue to work in the construction sector. There is a problem since the older people become,

the more they become less flexible and hence their contribution to the labor force diminishes at

an increasing rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

The table below shows the contribution of the aging workforce to the construction industry

(Gerard de , 2017, p. 34).

The older workers are however an asset to the industry. They need to be taken care of since they

keep the industry moving since they train the new workers. The older workers also ensure

compliance standards are followed.

Conclusion

Importance of the industry structure to the industrial economics is important since the

industry structure is a major determinant of competition in an industry. Market prices are

controlled by the intensity of the market competition which is in turn determined by the number

of firms that produce a given product. Competition in markets determines the ease of entry and

exit in the market. The construction industry in Australia has been facing elasticity in demand

The table below shows the contribution of the aging workforce to the construction industry

(Gerard de , 2017, p. 34).

The older workers are however an asset to the industry. They need to be taken care of since they

keep the industry moving since they train the new workers. The older workers also ensure

compliance standards are followed.

Conclusion

Importance of the industry structure to the industrial economics is important since the

industry structure is a major determinant of competition in an industry. Market prices are

controlled by the intensity of the market competition which is in turn determined by the number

of firms that produce a given product. Competition in markets determines the ease of entry and

exit in the market. The construction industry in Australia has been facing elasticity in demand

12

and supply of construction products and the demand and supply has the distinctive characteristics

that differentiate it from any other market. The industry has monopolistic, perfect and

oligopolistic market structures depending on the level in which the construction industry is

analyzed.

and supply of construction products and the demand and supply has the distinctive characteristics

that differentiate it from any other market. The industry has monopolistic, perfect and

oligopolistic market structures depending on the level in which the construction industry is

analyzed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.