Financial Conditions in Australia: Interest Rates and Market Analysis

VerifiedAdded on 2023/01/03

|10

|1793

|74

Report

AI Summary

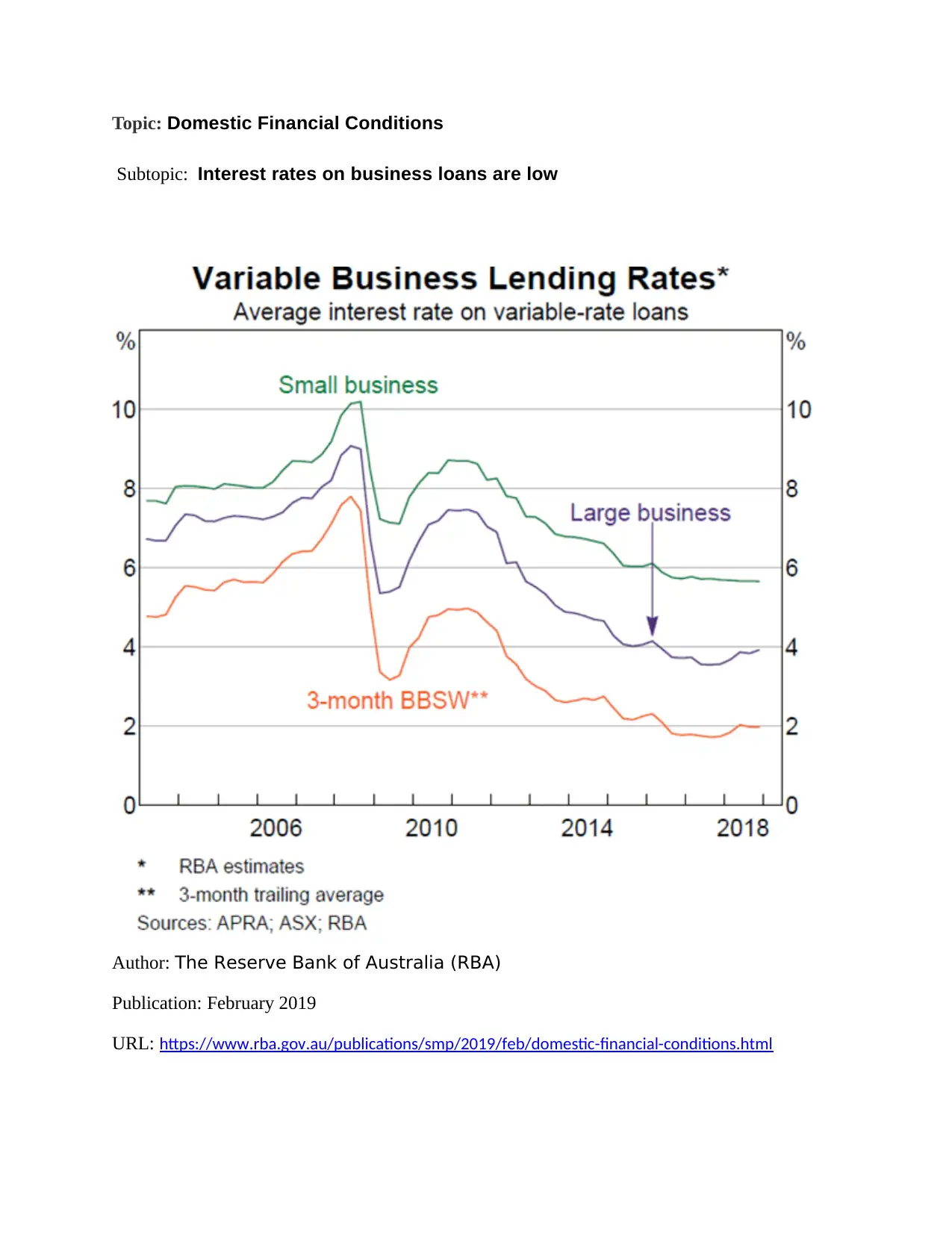

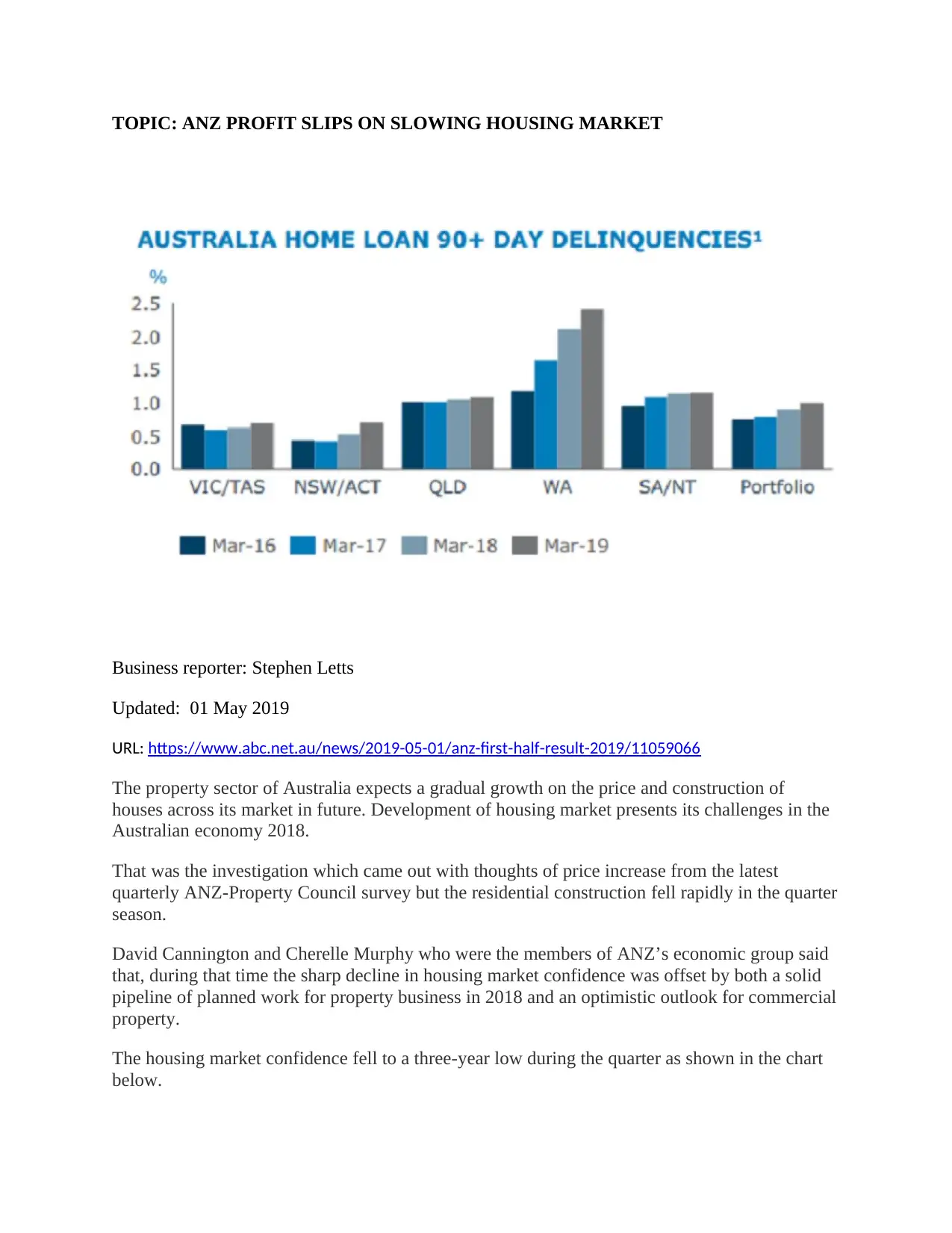

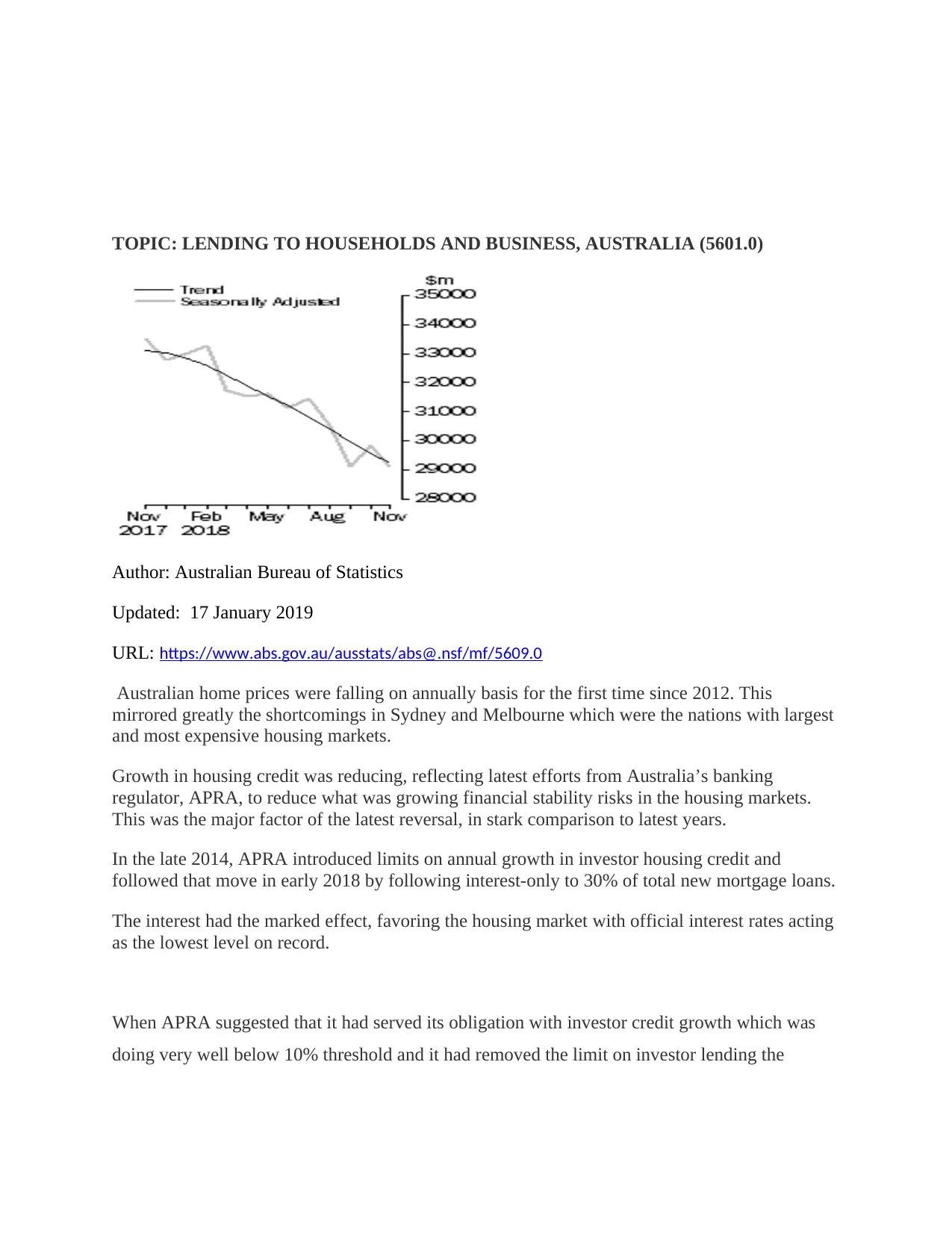

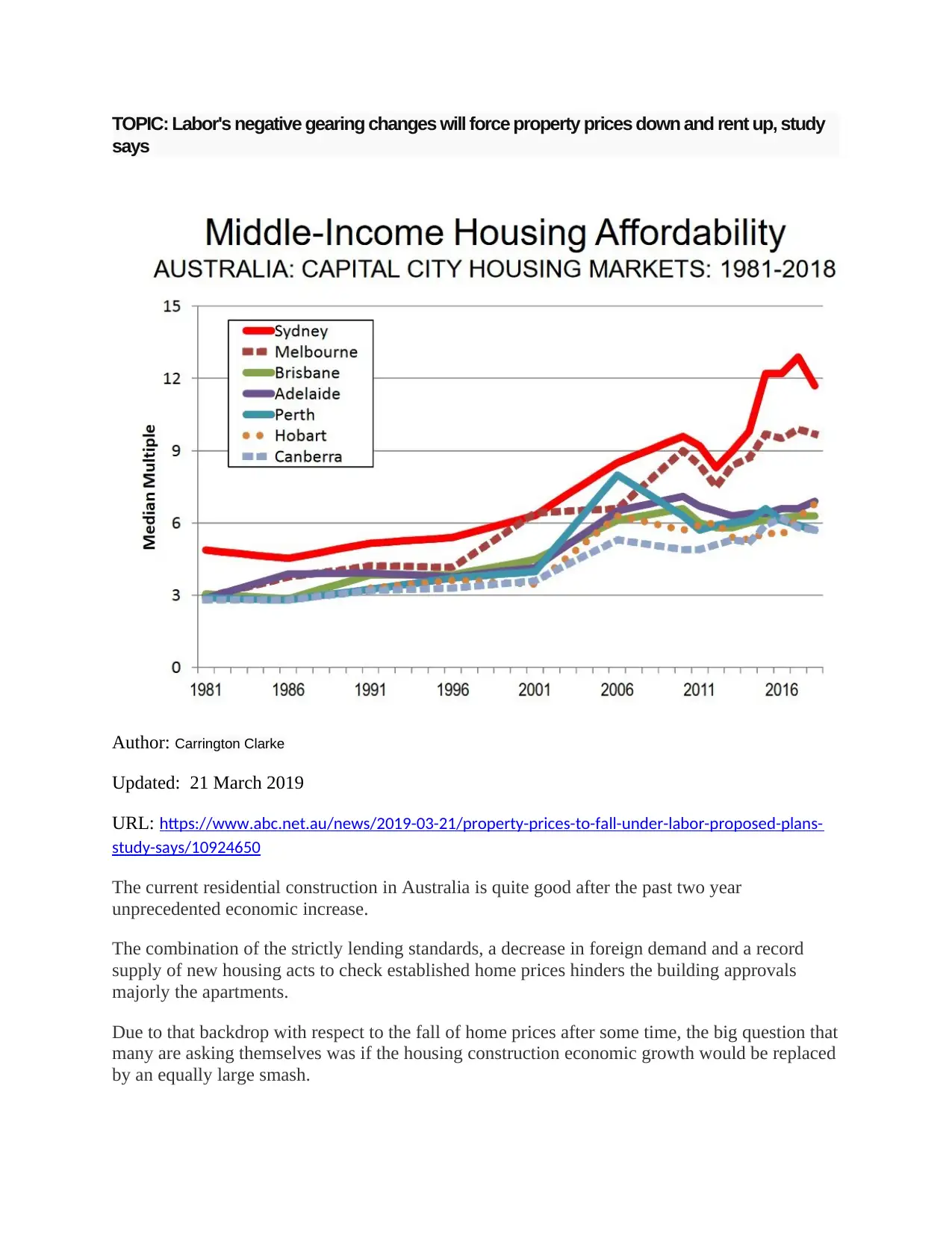

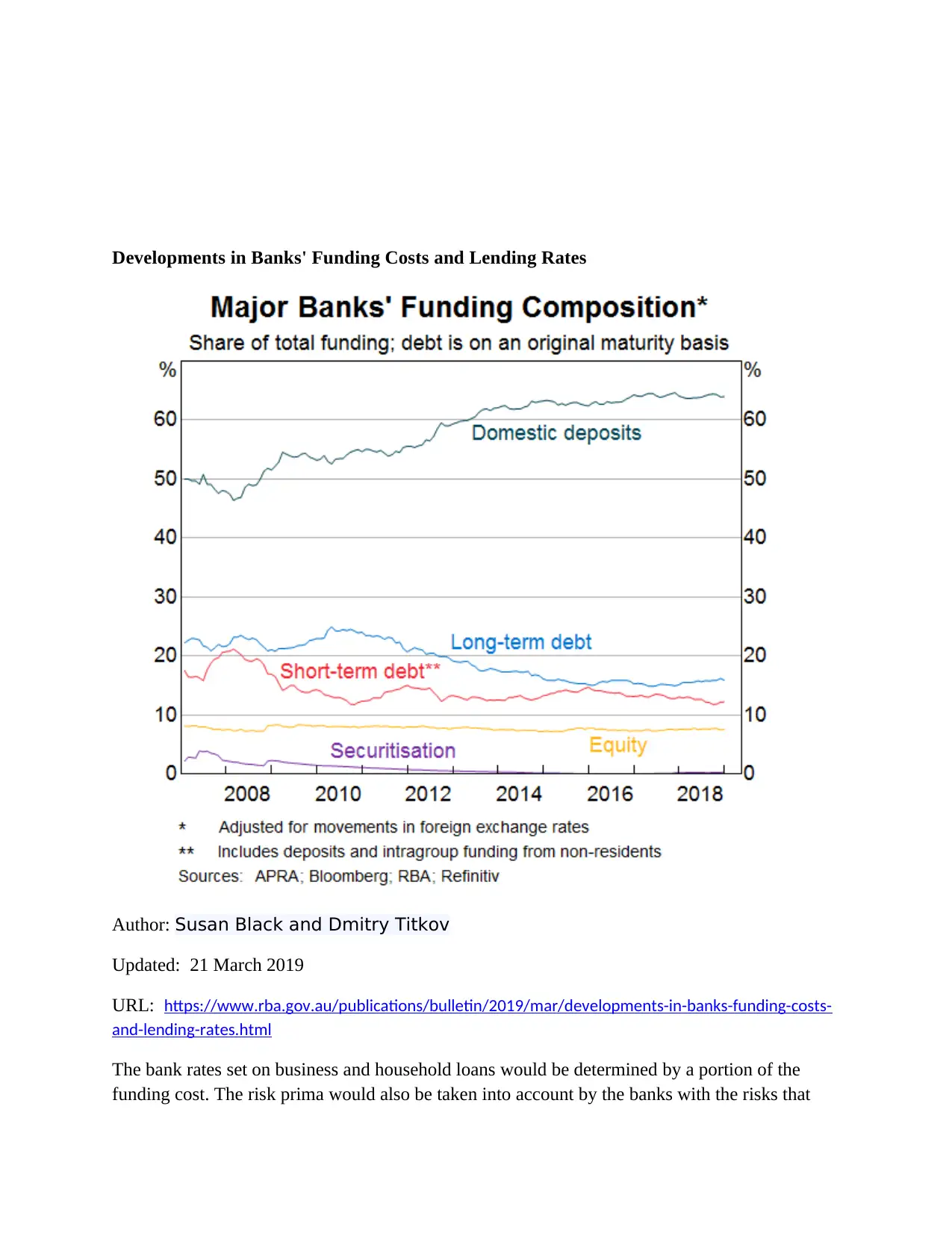

This report provides an analysis of Australia's domestic financial conditions, focusing on the influence of interest rates on business loans and the housing market. It examines the Reserve Bank of Australia (RBA)'s efforts to manage lending risks, including regulatory measures implemented by the Australian Prudential Regulation Authority (APRA) to curb household debt and control investor lending. The report highlights the impact of these policies on housing market confidence, property prices, and lending rates, drawing on data from various sources such as the RBA, ANZ, and the Australian Bureau of Statistics. It explores how factors like lending standards, foreign demand, and housing supply affect the residential construction sector. Furthermore, the report discusses the role of bank funding costs, including deposit levels, bank bonds, and short-term funding, in determining lending rates. It concludes by analyzing how changes in these conditions influence the broader Australian economy, including the impact on household debt, credit growth, and property prices, emphasizing the interplay between regulatory actions and market dynamics.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.