Economics for Managers Report

VerifiedAdded on 2019/11/08

|7

|1449

|151

Report

AI Summary

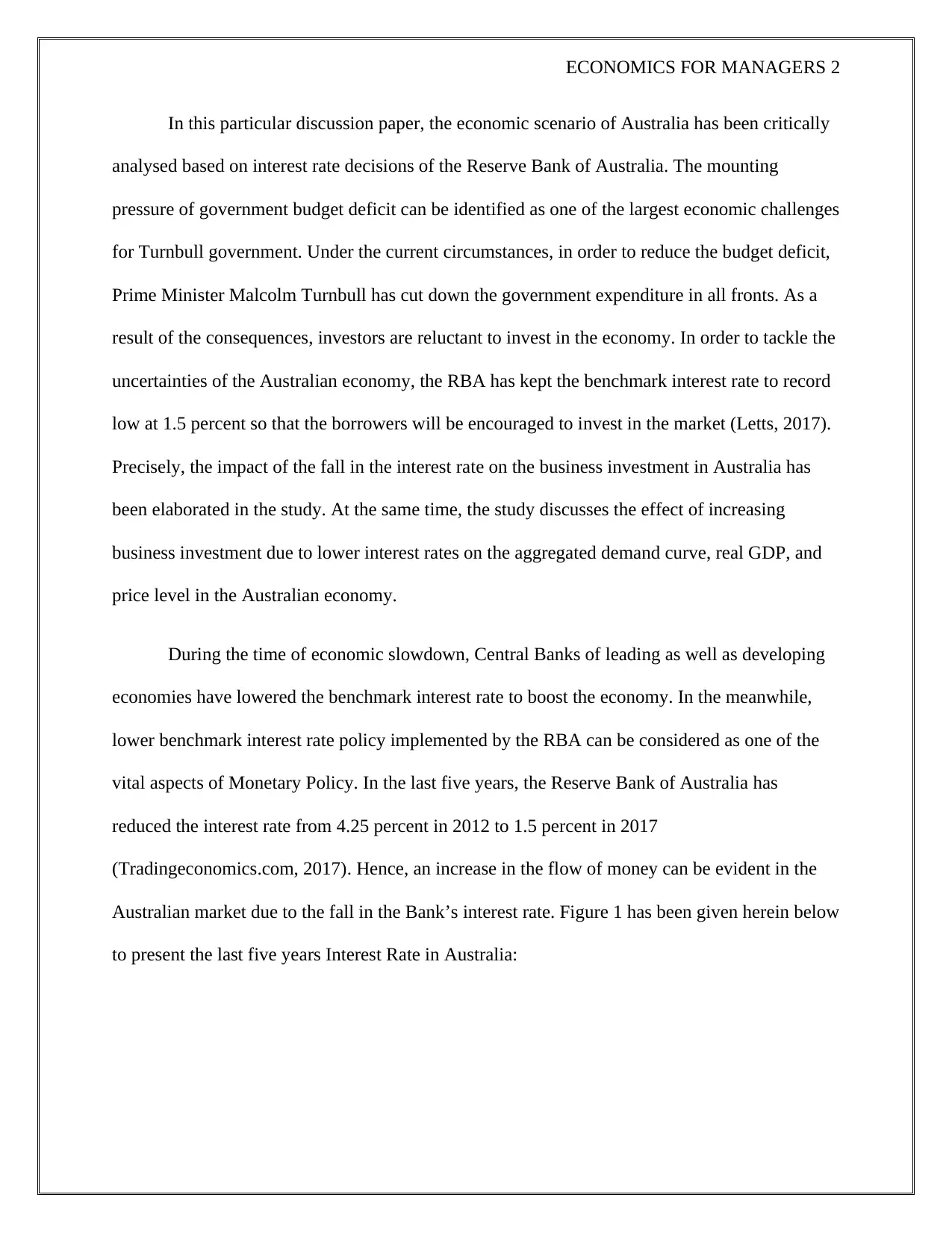

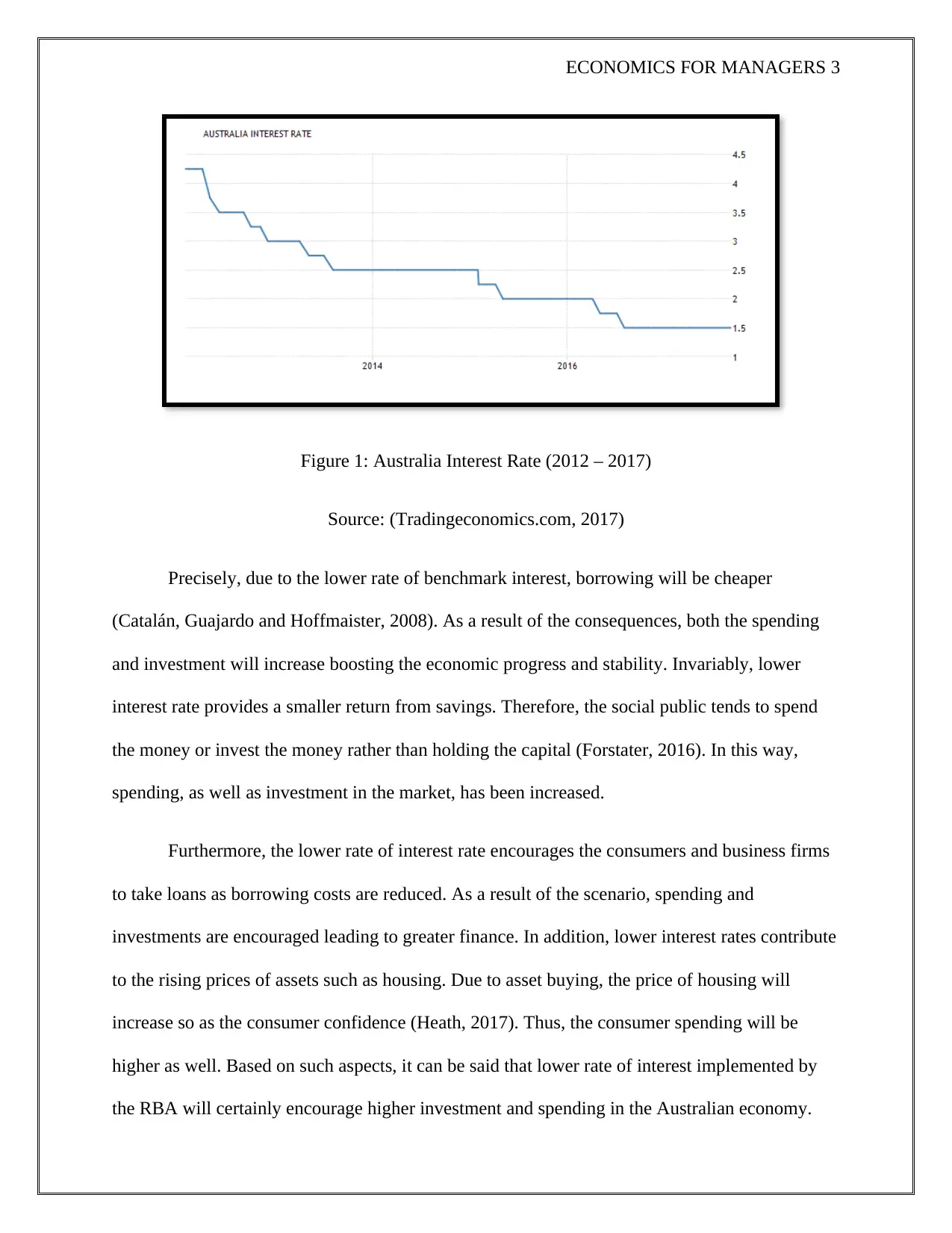

This report examines the effects of the Reserve Bank of Australia's (RBA) interest rate decisions on the Australian economy. It focuses on how the RBA's lowering of interest rates to a record low of 1.5% in 2017, in response to a government budget deficit and investor reluctance, impacts business investment. The report details how lower interest rates encourage borrowing, increase spending and investment, and influence the aggregate demand curve, real GDP, and price levels. Using figures to illustrate the relationship between interest rates, business investment, and macroeconomic indicators, the report concludes that the RBA's policy of lowering interest rates positively impacts the Australian economy by stimulating investment, increasing aggregate demand, and raising real GDP, although it may also lead to inflation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.