Australian Economy Report: Interest Rates and Economic Factors

VerifiedAdded on 2021/10/07

|5

|968

|78

Report

AI Summary

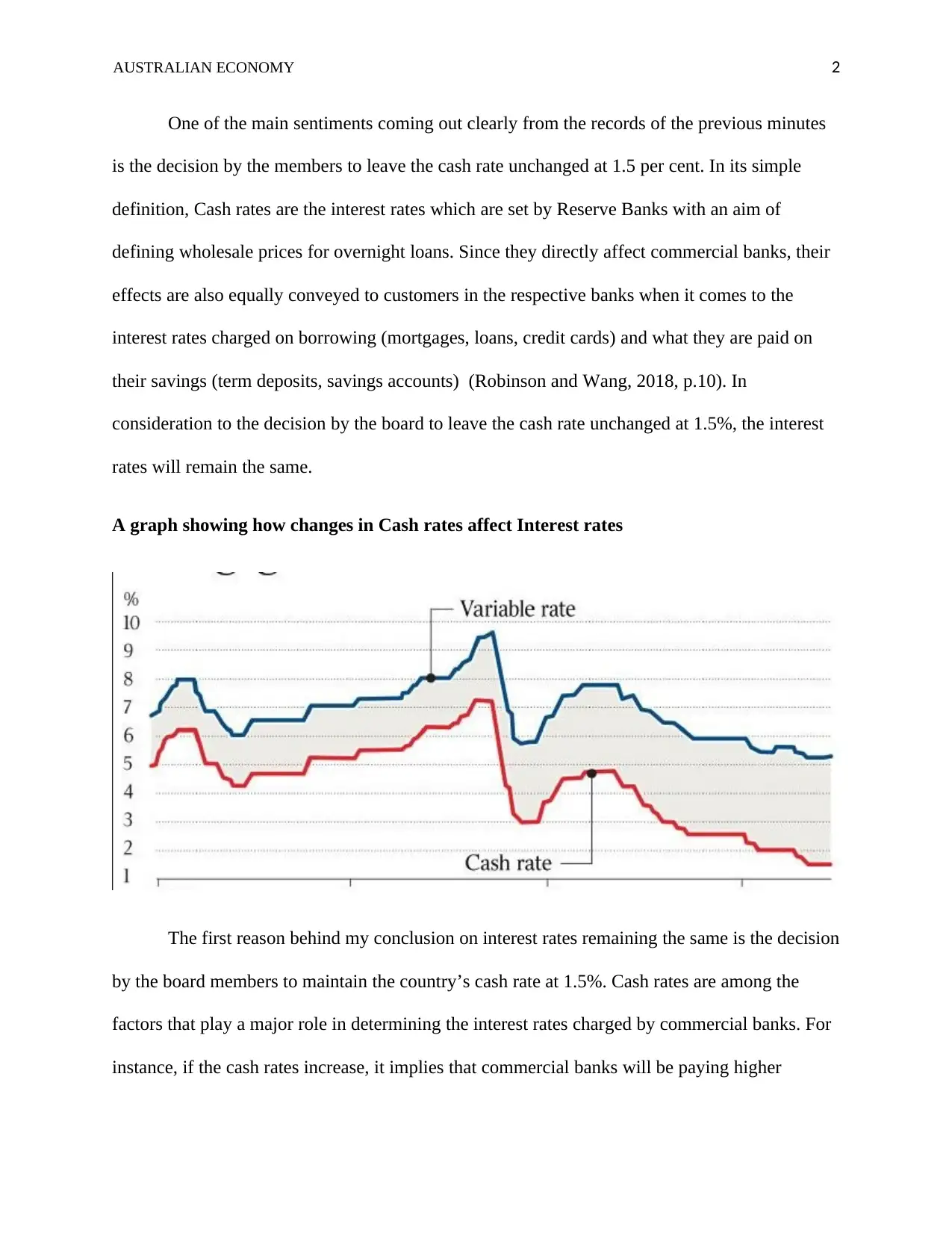

This report provides an analysis of the Australian economy, specifically focusing on the Reserve Bank of Australia's decision to maintain the cash rate at 1.5%. The report examines how cash rates influence interest rates charged by commercial banks on loans and savings, explaining the direct impact on consumers. It argues that because the cash rate remained unchanged, interest rates were also expected to stay the same. The report supports its conclusion by referencing the positive economic activities in Australia, consistent GDP growth forecasts, and the stable global economic conditions that favor the Australian economy. Based on this analysis, the report advises a client to continue their business operations as usual, without adjusting strategies like pricing, as the factors affecting interest rates remain stable. This guidance aims to help the client maintain profitability and manage loan repayments effectively.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.