Detailed Examination of BAS, PAYG, and GST: A Finance Assignment

VerifiedAdded on 2020/04/21

|10

|2065

|35

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of Business Activity Statements (BAS), PAYG instalments, and GST regulations. It includes a GST worksheet with calculations for various sales and purchases, a lodgement schedule for BAS with due dates and agent concessions, and a detailed explanation of monthly PAYG instalments, including a weekly net pay calculation and a PAYG instalment summary. The assignment further explores the importance of staying updated with GST legislations, outlining research methods and professional consultations for staying informed about changes in the Australian tax system. The document references relevant literature on tax avoidance, pension reform, and entrepreneurship dynamics, offering a practical understanding of financial reporting and tax compliance.

CARRY OUT BUSINESS

ACTIVITY AND

INSTALMENTS ACTIVITY

TASKS

ACTIVITY AND

INSTALMENTS ACTIVITY

TASKS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1.............................................................................................................................1

GST Worksheet for Business activity statements..................................................................1

Lodgement schedule for BAS................................................................................................3

QUESTION 2.............................................................................................................................5

Monthly PAYG instalment.....................................................................................................5

Lodgement requirements of PAYG section in BAS...............................................................6

QUESTION 3.............................................................................................................................7

How to keep up to date with the changes takes places in the legislations of Goods and

services tax, reporting authority. What kind of research conducted by an individual and

consultation with the professional..........................................................................................7

REFERENCES...........................................................................................................................9

QUESTION 1.............................................................................................................................1

GST Worksheet for Business activity statements..................................................................1

Lodgement schedule for BAS................................................................................................3

QUESTION 2.............................................................................................................................5

Monthly PAYG instalment.....................................................................................................5

Lodgement requirements of PAYG section in BAS...............................................................6

QUESTION 3.............................................................................................................................7

How to keep up to date with the changes takes places in the legislations of Goods and

services tax, reporting authority. What kind of research conducted by an individual and

consultation with the professional..........................................................................................7

REFERENCES...........................................................................................................................9

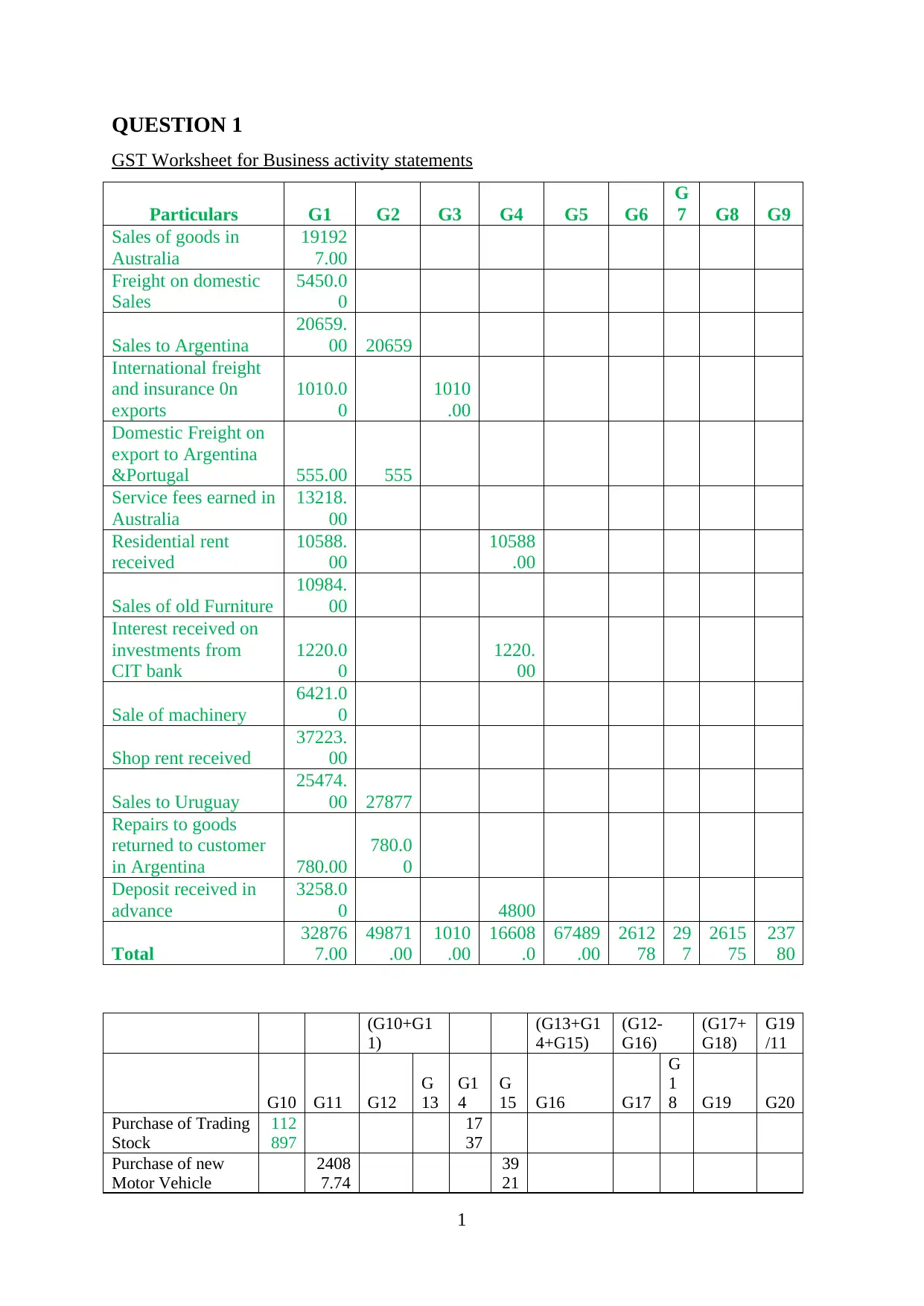

QUESTION 1

GST Worksheet for Business activity statements

Particulars G1 G2 G3 G4 G5 G6

G

7 G8 G9

Sales of goods in

Australia

19192

7.00

Freight on domestic

Sales

5450.0

0

Sales to Argentina

20659.

00 20659

International freight

and insurance 0n

exports

1010.0

0

1010

.00

Domestic Freight on

export to Argentina

&Portugal 555.00 555

Service fees earned in

Australia

13218.

00

Residential rent

received

10588.

00

10588

.00

Sales of old Furniture

10984.

00

Interest received on

investments from

CIT bank

1220.0

0

1220.

00

Sale of machinery

6421.0

0

Shop rent received

37223.

00

Sales to Uruguay

25474.

00 27877

Repairs to goods

returned to customer

in Argentina 780.00

780.0

0

Deposit received in

advance

3258.0

0 4800

Total

32876

7.00

49871

.00

1010

.00

16608

.0

67489

.00

2612

78

29

7

2615

75

237

80

(G10+G1

1)

(G13+G1

4+G15)

(G12-

G16)

(G17+

G18)

G19

/11

G10 G11 G12

G

13

G1

4

G

15 G16 G17

G

1

8 G19 G20

Purchase of Trading

Stock

112

897

17

37

Purchase of new

Motor Vehicle

2408

7.74

39

21

1

GST Worksheet for Business activity statements

Particulars G1 G2 G3 G4 G5 G6

G

7 G8 G9

Sales of goods in

Australia

19192

7.00

Freight on domestic

Sales

5450.0

0

Sales to Argentina

20659.

00 20659

International freight

and insurance 0n

exports

1010.0

0

1010

.00

Domestic Freight on

export to Argentina

&Portugal 555.00 555

Service fees earned in

Australia

13218.

00

Residential rent

received

10588.

00

10588

.00

Sales of old Furniture

10984.

00

Interest received on

investments from

CIT bank

1220.0

0

1220.

00

Sale of machinery

6421.0

0

Shop rent received

37223.

00

Sales to Uruguay

25474.

00 27877

Repairs to goods

returned to customer

in Argentina 780.00

780.0

0

Deposit received in

advance

3258.0

0 4800

Total

32876

7.00

49871

.00

1010

.00

16608

.0

67489

.00

2612

78

29

7

2615

75

237

80

(G10+G1

1)

(G13+G1

4+G15)

(G12-

G16)

(G17+

G18)

G19

/11

G10 G11 G12

G

13

G1

4

G

15 G16 G17

G

1

8 G19 G20

Purchase of Trading

Stock

112

897

17

37

Purchase of new

Motor Vehicle

2408

7.74

39

21

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Residential Rent

(Expense) 9577

95

77

office rental

2986

1

Business Journal

Subscription 239

Interest Paid on

Mortgage

1669

3

16

69

3

Bank Fees 2356

23

56

Purchase of new

office Equipment

221

20

New Motor Vehicle

Insurance 692 55

Electricity Expense

1146

9

Delivery Truck

Repair

221

8

New Motor Vehicle

Repair

135

8 0

Delievery Truck

Insurance 3292

Water Rates 4124

41

24

Land Rates 3554

35

54

Parking Fines 88 88

Telephone

Expenses

1354

0

Building Insurance 3536

Office Stationery

Purchased

331

1

Advertising

expenses

2989

8

Drawings

1000

0

Credit Card

merchant fees 1890

Returned outwards

37

6

Wages and salaries

2309

06

141

904

3958

02.7

5377

06.7

95

77

28

84

0

40

65 42482

495

225

49522

5

450

20

Adjustments Increases Decrease

Sales Return 780

Discount Received 1737

Debtor Bankrupt 2380

2

(Expense) 9577

95

77

office rental

2986

1

Business Journal

Subscription 239

Interest Paid on

Mortgage

1669

3

16

69

3

Bank Fees 2356

23

56

Purchase of new

office Equipment

221

20

New Motor Vehicle

Insurance 692 55

Electricity Expense

1146

9

Delivery Truck

Repair

221

8

New Motor Vehicle

Repair

135

8 0

Delievery Truck

Insurance 3292

Water Rates 4124

41

24

Land Rates 3554

35

54

Parking Fines 88 88

Telephone

Expenses

1354

0

Building Insurance 3536

Office Stationery

Purchased

331

1

Advertising

expenses

2989

8

Drawings

1000

0

Credit Card

merchant fees 1890

Returned outwards

37

6

Wages and salaries

2309

06

141

904

3958

02.7

5377

06.7

95

77

28

84

0

40

65 42482

495

225

49522

5

450

20

Adjustments Increases Decrease

Sales Return 780

Discount Received 1737

Debtor Bankrupt 2380

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

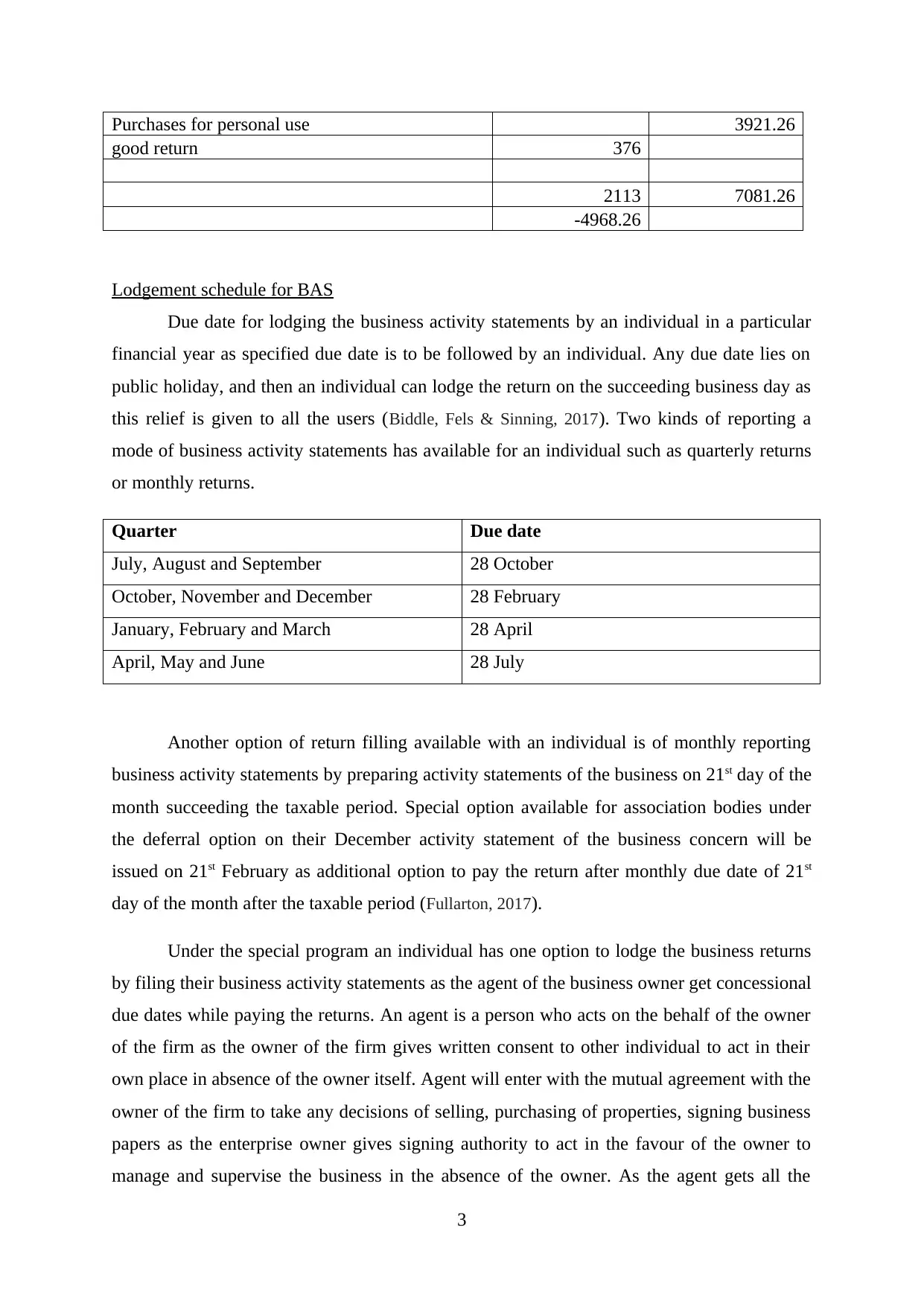

Purchases for personal use 3921.26

good return 376

2113 7081.26

-4968.26

Lodgement schedule for BAS

Due date for lodging the business activity statements by an individual in a particular

financial year as specified due date is to be followed by an individual. Any due date lies on

public holiday, and then an individual can lodge the return on the succeeding business day as

this relief is given to all the users (Biddle, Fels & Sinning, 2017). Two kinds of reporting a

mode of business activity statements has available for an individual such as quarterly returns

or monthly returns.

Quarter Due date

July, August and September 28 October

October, November and December 28 February

January, February and March 28 April

April, May and June 28 July

Another option of return filling available with an individual is of monthly reporting

business activity statements by preparing activity statements of the business on 21st day of the

month succeeding the taxable period. Special option available for association bodies under

the deferral option on their December activity statement of the business concern will be

issued on 21st February as additional option to pay the return after monthly due date of 21st

day of the month after the taxable period (Fullarton, 2017).

Under the special program an individual has one option to lodge the business returns

by filing their business activity statements as the agent of the business owner get concessional

due dates while paying the returns. An agent is a person who acts on the behalf of the owner

of the firm as the owner of the firm gives written consent to other individual to act in their

own place in absence of the owner itself. Agent will enter with the mutual agreement with the

owner of the firm to take any decisions of selling, purchasing of properties, signing business

papers as the enterprise owner gives signing authority to act in the favour of the owner to

manage and supervise the business in the absence of the owner. As the agent gets all the

3

good return 376

2113 7081.26

-4968.26

Lodgement schedule for BAS

Due date for lodging the business activity statements by an individual in a particular

financial year as specified due date is to be followed by an individual. Any due date lies on

public holiday, and then an individual can lodge the return on the succeeding business day as

this relief is given to all the users (Biddle, Fels & Sinning, 2017). Two kinds of reporting a

mode of business activity statements has available for an individual such as quarterly returns

or monthly returns.

Quarter Due date

July, August and September 28 October

October, November and December 28 February

January, February and March 28 April

April, May and June 28 July

Another option of return filling available with an individual is of monthly reporting

business activity statements by preparing activity statements of the business on 21st day of the

month succeeding the taxable period. Special option available for association bodies under

the deferral option on their December activity statement of the business concern will be

issued on 21st February as additional option to pay the return after monthly due date of 21st

day of the month after the taxable period (Fullarton, 2017).

Under the special program an individual has one option to lodge the business returns

by filing their business activity statements as the agent of the business owner get concessional

due dates while paying the returns. An agent is a person who acts on the behalf of the owner

of the firm as the owner of the firm gives written consent to other individual to act in their

own place in absence of the owner itself. Agent will enter with the mutual agreement with the

owner of the firm to take any decisions of selling, purchasing of properties, signing business

papers as the enterprise owner gives signing authority to act in the favour of the owner to

manage and supervise the business in the absence of the owner. As the agent gets all the

3

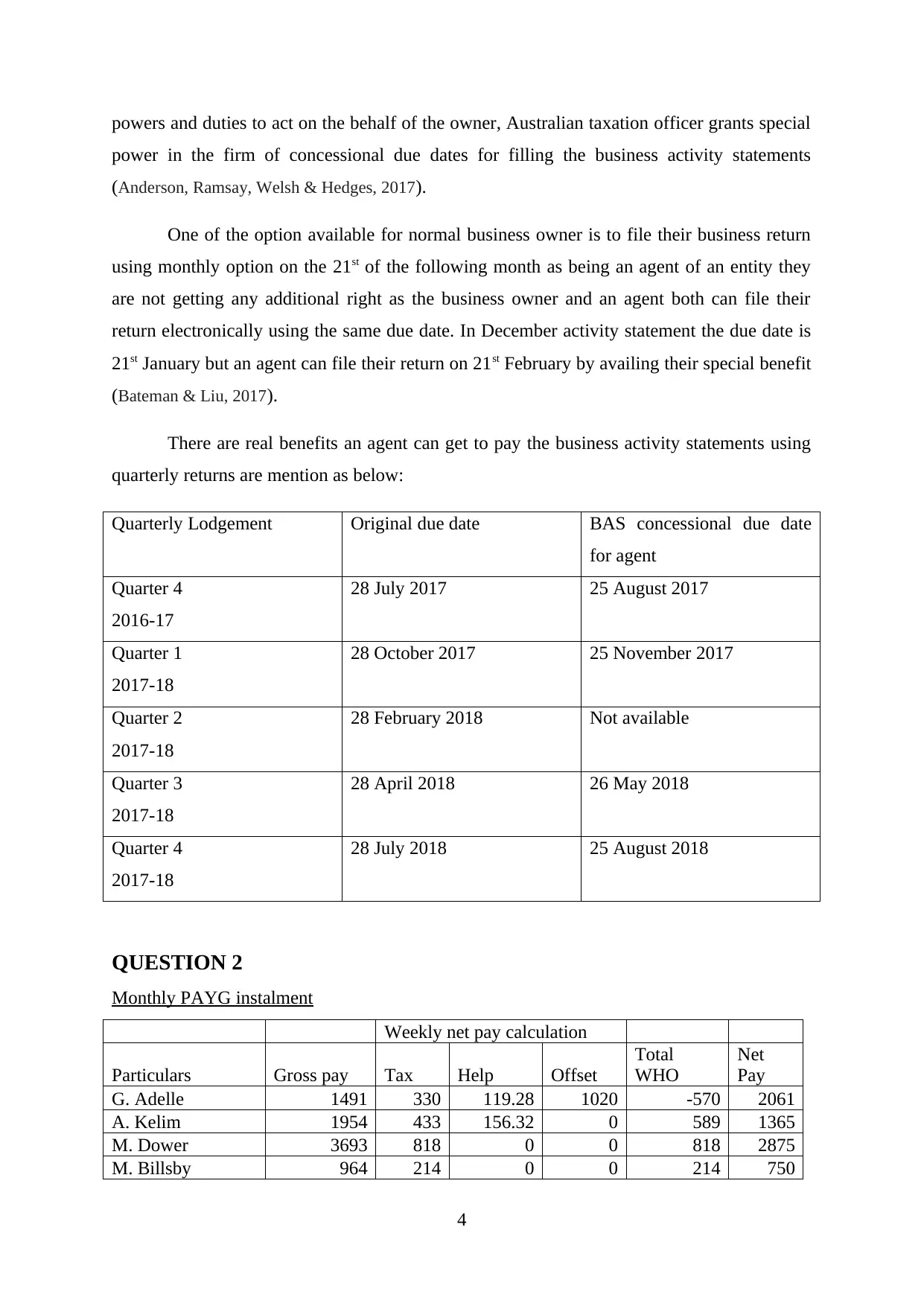

powers and duties to act on the behalf of the owner, Australian taxation officer grants special

power in the firm of concessional due dates for filling the business activity statements

(Anderson, Ramsay, Welsh & Hedges, 2017).

One of the option available for normal business owner is to file their business return

using monthly option on the 21st of the following month as being an agent of an entity they

are not getting any additional right as the business owner and an agent both can file their

return electronically using the same due date. In December activity statement the due date is

21st January but an agent can file their return on 21st February by availing their special benefit

(Bateman & Liu, 2017).

There are real benefits an agent can get to pay the business activity statements using

quarterly returns are mention as below:

Quarterly Lodgement Original due date BAS concessional due date

for agent

Quarter 4

2016-17

28 July 2017 25 August 2017

Quarter 1

2017-18

28 October 2017 25 November 2017

Quarter 2

2017-18

28 February 2018 Not available

Quarter 3

2017-18

28 April 2018 26 May 2018

Quarter 4

2017-18

28 July 2018 25 August 2018

QUESTION 2

Monthly PAYG instalment

Weekly net pay calculation

Particulars Gross pay Tax Help Offset

Total

WHO

Net

Pay

G. Adelle 1491 330 119.28 1020 -570 2061

A. Kelim 1954 433 156.32 0 589 1365

M. Dower 3693 818 0 0 818 2875

M. Billsby 964 214 0 0 214 750

4

power in the firm of concessional due dates for filling the business activity statements

(Anderson, Ramsay, Welsh & Hedges, 2017).

One of the option available for normal business owner is to file their business return

using monthly option on the 21st of the following month as being an agent of an entity they

are not getting any additional right as the business owner and an agent both can file their

return electronically using the same due date. In December activity statement the due date is

21st January but an agent can file their return on 21st February by availing their special benefit

(Bateman & Liu, 2017).

There are real benefits an agent can get to pay the business activity statements using

quarterly returns are mention as below:

Quarterly Lodgement Original due date BAS concessional due date

for agent

Quarter 4

2016-17

28 July 2017 25 August 2017

Quarter 1

2017-18

28 October 2017 25 November 2017

Quarter 2

2017-18

28 February 2018 Not available

Quarter 3

2017-18

28 April 2018 26 May 2018

Quarter 4

2017-18

28 July 2018 25 August 2018

QUESTION 2

Monthly PAYG instalment

Weekly net pay calculation

Particulars Gross pay Tax Help Offset

Total

WHO

Net

Pay

G. Adelle 1491 330 119.28 1020 -570 2061

A. Kelim 1954 433 156.32 0 589 1365

M. Dower 3693 818 0 0 818 2875

M. Billsby 964 214 0 0 214 750

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

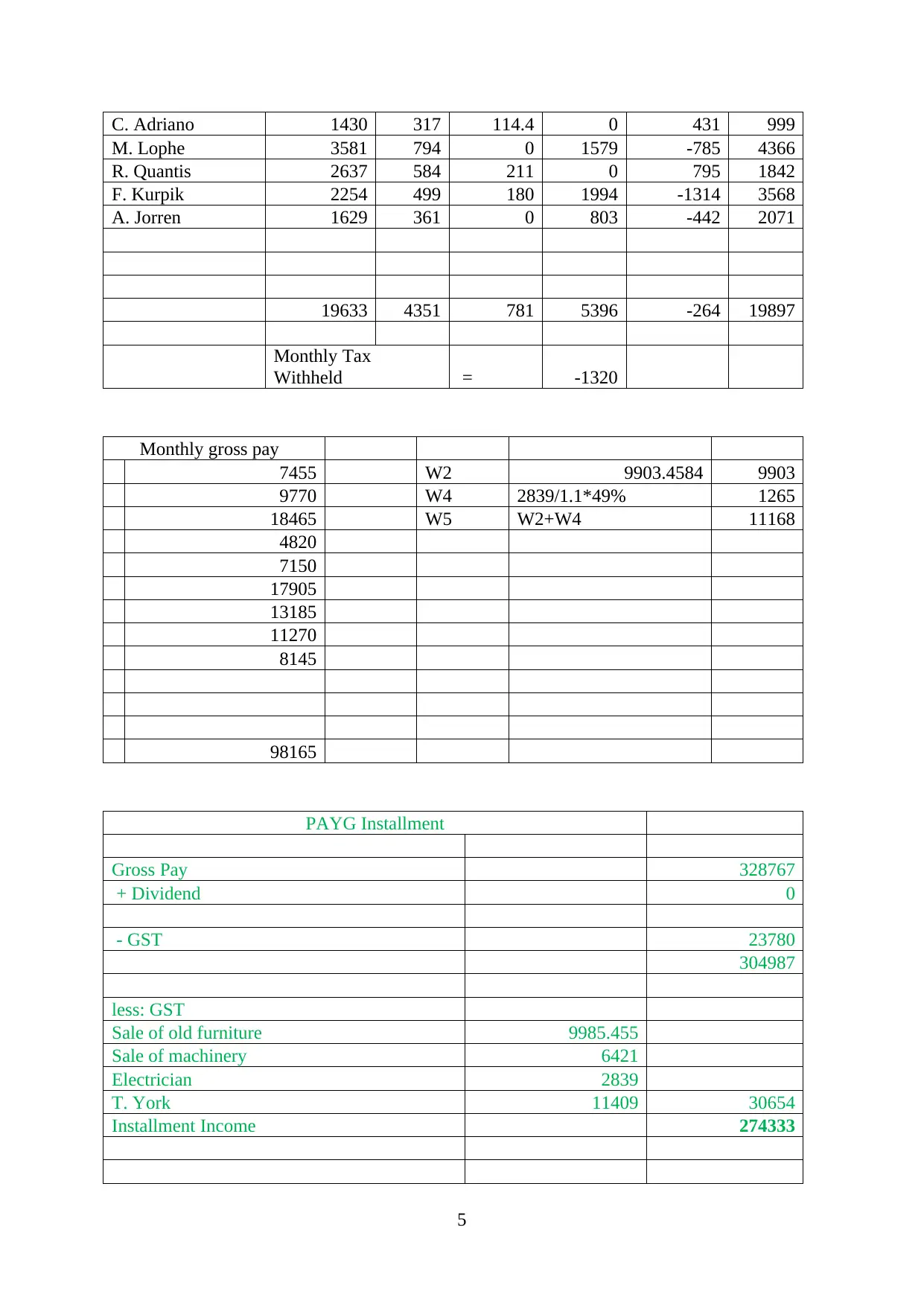

C. Adriano 1430 317 114.4 0 431 999

M. Lophe 3581 794 0 1579 -785 4366

R. Quantis 2637 584 211 0 795 1842

F. Kurpik 2254 499 180 1994 -1314 3568

A. Jorren 1629 361 0 803 -442 2071

19633 4351 781 5396 -264 19897

Monthly Tax

Withheld = -1320

Monthly gross pay

7455 W2 9903.4584 9903

9770 W4 2839/1.1*49% 1265

18465 W5 W2+W4 11168

4820

7150

17905

13185

11270

8145

98165

PAYG Installment

Gross Pay 328767

+ Dividend 0

- GST 23780

304987

less: GST

Sale of old furniture 9985.455

Sale of machinery 6421

Electrician 2839

T. York 11409 30654

Installment Income 274333

5

M. Lophe 3581 794 0 1579 -785 4366

R. Quantis 2637 584 211 0 795 1842

F. Kurpik 2254 499 180 1994 -1314 3568

A. Jorren 1629 361 0 803 -442 2071

19633 4351 781 5396 -264 19897

Monthly Tax

Withheld = -1320

Monthly gross pay

7455 W2 9903.4584 9903

9770 W4 2839/1.1*49% 1265

18465 W5 W2+W4 11168

4820

7150

17905

13185

11270

8145

98165

PAYG Installment

Gross Pay 328767

+ Dividend 0

- GST 23780

304987

less: GST

Sale of old furniture 9985.455

Sale of machinery 6421

Electrician 2839

T. York 11409 30654

Installment Income 274333

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

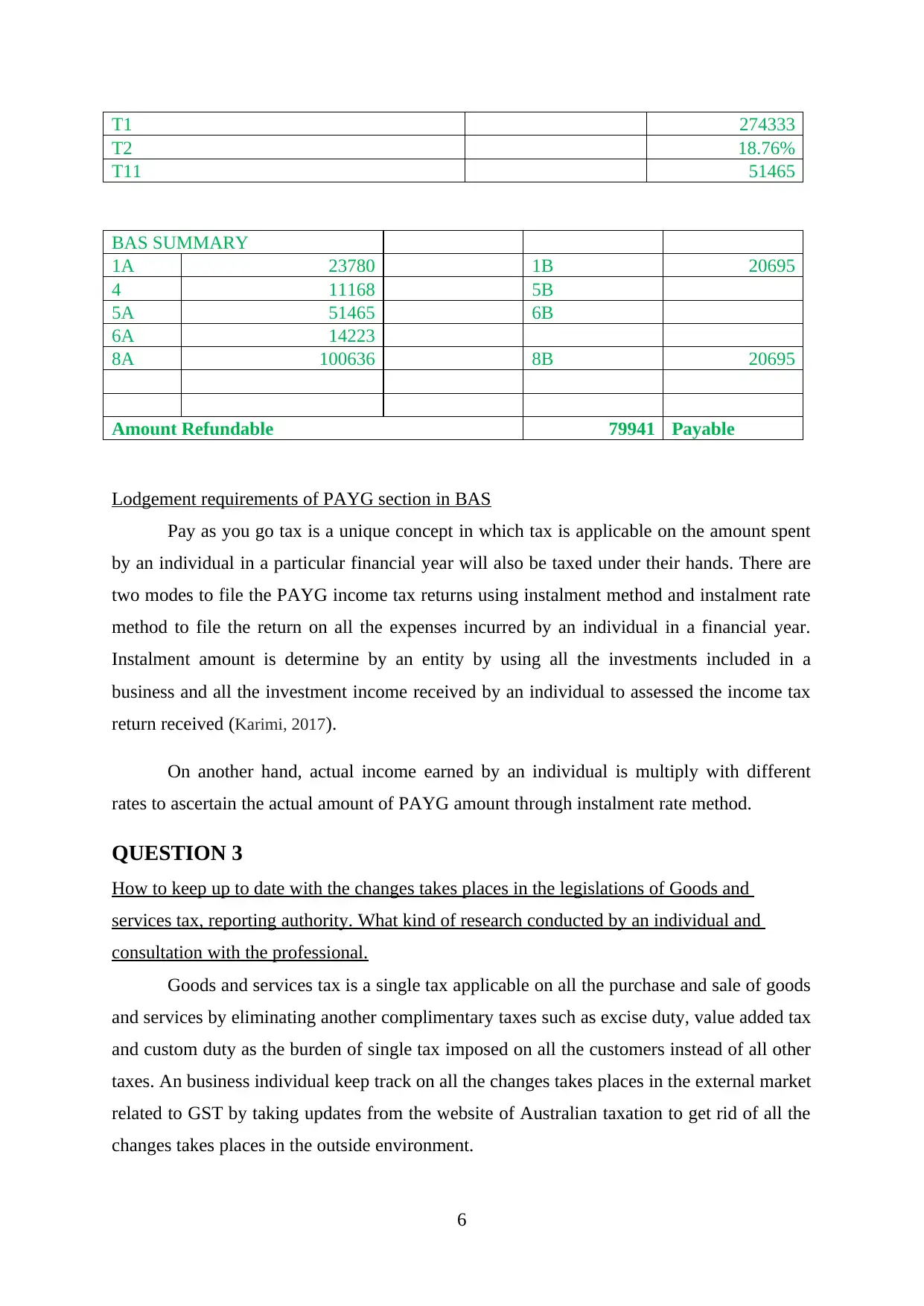

T1 274333

T2 18.76%

T11 51465

BAS SUMMARY

1A 23780 1B 20695

4 11168 5B

5A 51465 6B

6A 14223

8A 100636 8B 20695

Amount Refundable 79941 Payable

Lodgement requirements of PAYG section in BAS

Pay as you go tax is a unique concept in which tax is applicable on the amount spent

by an individual in a particular financial year will also be taxed under their hands. There are

two modes to file the PAYG income tax returns using instalment method and instalment rate

method to file the return on all the expenses incurred by an individual in a financial year.

Instalment amount is determine by an entity by using all the investments included in a

business and all the investment income received by an individual to assessed the income tax

return received (Karimi, 2017).

On another hand, actual income earned by an individual is multiply with different

rates to ascertain the actual amount of PAYG amount through instalment rate method.

QUESTION 3

How to keep up to date with the changes takes places in the legislations of Goods and

services tax, reporting authority. What kind of research conducted by an individual and

consultation with the professional.

Goods and services tax is a single tax applicable on all the purchase and sale of goods

and services by eliminating another complimentary taxes such as excise duty, value added tax

and custom duty as the burden of single tax imposed on all the customers instead of all other

taxes. An business individual keep track on all the changes takes places in the external market

related to GST by taking updates from the website of Australian taxation to get rid of all the

changes takes places in the outside environment.

6

T2 18.76%

T11 51465

BAS SUMMARY

1A 23780 1B 20695

4 11168 5B

5A 51465 6B

6A 14223

8A 100636 8B 20695

Amount Refundable 79941 Payable

Lodgement requirements of PAYG section in BAS

Pay as you go tax is a unique concept in which tax is applicable on the amount spent

by an individual in a particular financial year will also be taxed under their hands. There are

two modes to file the PAYG income tax returns using instalment method and instalment rate

method to file the return on all the expenses incurred by an individual in a financial year.

Instalment amount is determine by an entity by using all the investments included in a

business and all the investment income received by an individual to assessed the income tax

return received (Karimi, 2017).

On another hand, actual income earned by an individual is multiply with different

rates to ascertain the actual amount of PAYG amount through instalment rate method.

QUESTION 3

How to keep up to date with the changes takes places in the legislations of Goods and

services tax, reporting authority. What kind of research conducted by an individual and

consultation with the professional.

Goods and services tax is a single tax applicable on all the purchase and sale of goods

and services by eliminating another complimentary taxes such as excise duty, value added tax

and custom duty as the burden of single tax imposed on all the customers instead of all other

taxes. An business individual keep track on all the changes takes places in the external market

related to GST by taking updates from the website of Australian taxation to get rid of all the

changes takes places in the outside environment.

6

By reviewing the website of www.ato.gov.au, two changes have monitored in the

goods and services tax in the Australia to reduce the overall taxable obligations on an entity.

An enterprise always tries to reduce their tax obligations by paying all the taxes in advance to

secure the overall earnings of the firms after paying all the expenses as the expenses will

helps in decreasing the total tax liability of an entity (Bakhtiari, 2017).

GST tax applicable on imported services and digital products- This change has

applicable in the Australia from 1st July 2017 to apply this rule from new financial

year by winding up the previous rules and regulations. This change shows the

extension of areas of covering up under the goods and services taxes which, in turn,

increasing the tax revenues of the government and also helps in controlling the

importing of goods to safeguard the potential of the domestic business users. It

includes buying of imported services by an individual in the Australia from other

countries and all the digital products. A digital product includes various things such as

movies, music, applications, games, and kindle books, online architectural and legal

services (Somerset, 2017). If an individual and business user meets the threshold limit

of $750000 then they are required to register under the GST law and pay the GST on

the overseas supplies.

GST on low value imported goods- This change come into existence on 1st July

2018 under which sales of lower value goods imported by the customers from outside

the Australia comes under the tax obligation of GST. Total value of goods imported in

the Australia is less than the value of Australian dollar 1000 then these goods will be

exempted from the tax liability.

Secondary research study has used in identifying all the changes takes places in the

eternal environment about the GST legislations. It is essential to gather information

regarding changes takes places in the GST rules and regulations by using internet as one

of the helpful medium. Through internet website of the Australian taxation is used to

update an individual’s knowledge regarding all the changes. Primary research is not

suitable as it is not suitable enough to visits the Association bodies and takes their

interview on the current matter (Cassidy, 2017). Through email and electronically mode,

advanced taxation experts can be contact to know their opinion on the changes in the GST

rules. An entity can reduce their tax obligations by taking experts views of all the taxation

experts in knowing their tax liability.

7

goods and services tax in the Australia to reduce the overall taxable obligations on an entity.

An enterprise always tries to reduce their tax obligations by paying all the taxes in advance to

secure the overall earnings of the firms after paying all the expenses as the expenses will

helps in decreasing the total tax liability of an entity (Bakhtiari, 2017).

GST tax applicable on imported services and digital products- This change has

applicable in the Australia from 1st July 2017 to apply this rule from new financial

year by winding up the previous rules and regulations. This change shows the

extension of areas of covering up under the goods and services taxes which, in turn,

increasing the tax revenues of the government and also helps in controlling the

importing of goods to safeguard the potential of the domestic business users. It

includes buying of imported services by an individual in the Australia from other

countries and all the digital products. A digital product includes various things such as

movies, music, applications, games, and kindle books, online architectural and legal

services (Somerset, 2017). If an individual and business user meets the threshold limit

of $750000 then they are required to register under the GST law and pay the GST on

the overseas supplies.

GST on low value imported goods- This change come into existence on 1st July

2018 under which sales of lower value goods imported by the customers from outside

the Australia comes under the tax obligation of GST. Total value of goods imported in

the Australia is less than the value of Australian dollar 1000 then these goods will be

exempted from the tax liability.

Secondary research study has used in identifying all the changes takes places in the

eternal environment about the GST legislations. It is essential to gather information

regarding changes takes places in the GST rules and regulations by using internet as one

of the helpful medium. Through internet website of the Australian taxation is used to

update an individual’s knowledge regarding all the changes. Primary research is not

suitable as it is not suitable enough to visits the Association bodies and takes their

interview on the current matter (Cassidy, 2017). Through email and electronically mode,

advanced taxation experts can be contact to know their opinion on the changes in the GST

rules. An entity can reduce their tax obligations by taking experts views of all the taxation

experts in knowing their tax liability.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Anderson, H. L., Ramsay, I., Welsh, M. A., & Hedges, J. (2017). Phoenix Activity:

Recommendations on Detection, Disruption and Enforcement.

Bakhtiari, S. (2017). Entrepreneurship Dynamics in Australia: Lessons from Micro-Data.

Bateman, H., & Liu, K. (2017). Pension reform: Australia and China compared. Economic and

Political Studies, 1-19.

Biddle, N., Fels, K., & Sinning, M. (2017). Behavioural Insights and Business Taxation: Evidence

from Two Randomized Controlled Trials.

Cassidy, J. (2017, January). A GST with GRRRRRR: Legislative responses to GST tax avoidance in

Australia and New Zealand. In Australasian Tax Teachers Association Conference 2017.

Fullarton, L. (2017). Artful Aussie Tax Dodger: 100 Years of Tax Reform in Australia. Columbia

University Press.

Karimi, S. (2017). Beyond the Welfare State: Postwar Social Settlement and Public Pension Policy in

Canada and Australia. University of Toronto Press.

Somerset, J. W. (2017). Defining a financially sustainable independent school in Australia (Doctoral

dissertation, Queensland University of Technology).

8

Anderson, H. L., Ramsay, I., Welsh, M. A., & Hedges, J. (2017). Phoenix Activity:

Recommendations on Detection, Disruption and Enforcement.

Bakhtiari, S. (2017). Entrepreneurship Dynamics in Australia: Lessons from Micro-Data.

Bateman, H., & Liu, K. (2017). Pension reform: Australia and China compared. Economic and

Political Studies, 1-19.

Biddle, N., Fels, K., & Sinning, M. (2017). Behavioural Insights and Business Taxation: Evidence

from Two Randomized Controlled Trials.

Cassidy, J. (2017, January). A GST with GRRRRRR: Legislative responses to GST tax avoidance in

Australia and New Zealand. In Australasian Tax Teachers Association Conference 2017.

Fullarton, L. (2017). Artful Aussie Tax Dodger: 100 Years of Tax Reform in Australia. Columbia

University Press.

Karimi, S. (2017). Beyond the Welfare State: Postwar Social Settlement and Public Pension Policy in

Canada and Australia. University of Toronto Press.

Somerset, J. W. (2017). Defining a financially sustainable independent school in Australia (Doctoral

dissertation, Queensland University of Technology).

8

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.