Analysis of Financial Instruments and Institutions in Australia

VerifiedAdded on 2023/01/13

|14

|2194

|70

Report

AI Summary

This report provides an in-depth analysis of financial instruments and institutions in Australia, addressing three key tasks. Task 1 examines the main types of financial institutions as classified by the Reserve Bank of Australia (RBA), including authorized and non-authorized deposit-taking institutions, and funds and insurance managers, detailing their roles and responsibilities. Task 2 focuses on the performance of major Australian banks, such as ANZ, Commonwealth Bank, Westpac, and NAB, using financial indicators like revenue, net income, profit before tax, and loan impairment, to assess their performance in a transforming industry landscape. Task 3 explores the term structure of interest rates in Australia, illustrating the relationship between bond yields and maturities, and its significance in the fixed income world. The report uses data and charts to support the analysis, providing a comprehensive overview of the Australian financial landscape.

Running head: FINANCIAL INSTRUMENTS AND INSTITUTIONS

Financial instruments and institutions

Name of the Student

Name of the University

Author Note

Financial instruments and institutions

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Table of Contents

Answer to task 1:........................................................................................................................2

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Conclusion:................................................................................................................................4

Answer to task 2:........................................................................................................................4

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................4

Conclusion:................................................................................................................................8

Answer to task 3:........................................................................................................................8

Introduction:...............................................................................................................................8

Discussion:.................................................................................................................................8

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................12

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Table of Contents

Answer to task 1:........................................................................................................................2

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Conclusion:................................................................................................................................4

Answer to task 2:........................................................................................................................4

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................4

Conclusion:................................................................................................................................8

Answer to task 3:........................................................................................................................8

Introduction:...............................................................................................................................8

Discussion:.................................................................................................................................8

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................12

2

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Answer to task 1:

Introduction:

The report is prepared to identify the main types of financial institutions that are

classified by the Reserve Bank of Australia. For this purpose, the performance, roles and

responsibilities played by each financial institution have also been presented. The Reserve

Bank of Australia has divided the financial institutions in into three categories comprising of

non-authorized deposit taking institution, authorized deposit taking institution and funds and

insurance managers.

Discussion:

All the three categories of the financial institutions classified by RBA are explained

below:

Non-authorized deposit taking institute:

Different types of institutions that are classified as non-authorized institutions include

finance companies, money market corporations and securitizes. Finance companies

comprised of pastoral finance companies and general financiers and money market

Corporations include broker dealers. The function of finance companies is to raise funds from

retail investors and wholesale market using unsecured notes and debentures. Money market

Corporation on other hand has its operation primarily in wholesale market and provides

lending facilities to large corporations and bank along with some other services such as

capital market, capital finance, investment management and foreign exchange (rba.gov.au,

2019). Securitisers are the special purpose vehicle that uses pool of assets to issue securities.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Answer to task 1:

Introduction:

The report is prepared to identify the main types of financial institutions that are

classified by the Reserve Bank of Australia. For this purpose, the performance, roles and

responsibilities played by each financial institution have also been presented. The Reserve

Bank of Australia has divided the financial institutions in into three categories comprising of

non-authorized deposit taking institution, authorized deposit taking institution and funds and

insurance managers.

Discussion:

All the three categories of the financial institutions classified by RBA are explained

below:

Non-authorized deposit taking institute:

Different types of institutions that are classified as non-authorized institutions include

finance companies, money market corporations and securitizes. Finance companies

comprised of pastoral finance companies and general financiers and money market

Corporations include broker dealers. The function of finance companies is to raise funds from

retail investors and wholesale market using unsecured notes and debentures. Money market

Corporation on other hand has its operation primarily in wholesale market and provides

lending facilities to large corporations and bank along with some other services such as

capital market, capital finance, investment management and foreign exchange (rba.gov.au,

2019). Securitisers are the special purpose vehicle that uses pool of assets to issue securities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL INSTRUMENTS AND INSTITUTIONS

The credit enhancements of the securities are usually done by way of guarantee from third

parties.

Authorized deposit-taking institute:

Building societies, banks and credit unions are categorized as authorized deposit

taking institute, which are managed by APRA. Banks are the financial institution having the

function of providing wide range of financial services including insurance and fund

management services. Credit unions provide service to economy by way personal loan,

deposit and payment service to members. Building societies shave the same function as that

of credit unions (rba.gov.au, 2019).

Funds and insurance managers:

The type of financial institution that operates as insurance and fund managers include

life insurance companies, health insurance companies, approved deposit and superannuation

funds and general insurance companies all of which are regulated by APRA. The function of

Health Insurance Company is to provide insurance for covering the private cost of health and

investment is mainly done in government securities, loan and equities. Life insurance

companies provide accident, disability and life insurance, investment and superannuation,

annuities. Assets of this financial institution are invested mostly in securities and equities and

are managed on fiduciary basis in statutory funds. General insurance companies on other

hand provide motor vehicle, property and liability to employer by investing in government

securities, loan and deposit and equities. Other institutions operate as fund managers such as

public unit trust, approved and superannuation deposit funds, friendly societies, common

funds and cash management trust which are regulated by ASIC. Cash management trust is the

trust unit that is governed by trust deeds and their investment is generally confined to the

financial securities in the short-term money market (Viney & Phillips, 2012). Public unit trust

FINANCIAL INSTRUMENTS AND INSTITUTIONS

The credit enhancements of the securities are usually done by way of guarantee from third

parties.

Authorized deposit-taking institute:

Building societies, banks and credit unions are categorized as authorized deposit

taking institute, which are managed by APRA. Banks are the financial institution having the

function of providing wide range of financial services including insurance and fund

management services. Credit unions provide service to economy by way personal loan,

deposit and payment service to members. Building societies shave the same function as that

of credit unions (rba.gov.au, 2019).

Funds and insurance managers:

The type of financial institution that operates as insurance and fund managers include

life insurance companies, health insurance companies, approved deposit and superannuation

funds and general insurance companies all of which are regulated by APRA. The function of

Health Insurance Company is to provide insurance for covering the private cost of health and

investment is mainly done in government securities, loan and equities. Life insurance

companies provide accident, disability and life insurance, investment and superannuation,

annuities. Assets of this financial institution are invested mostly in securities and equities and

are managed on fiduciary basis in statutory funds. General insurance companies on other

hand provide motor vehicle, property and liability to employer by investing in government

securities, loan and deposit and equities. Other institutions operate as fund managers such as

public unit trust, approved and superannuation deposit funds, friendly societies, common

funds and cash management trust which are regulated by ASIC. Cash management trust is the

trust unit that is governed by trust deeds and their investment is generally confined to the

financial securities in the short-term money market (Viney & Phillips, 2012). Public unit trust

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL INSTRUMENTS AND INSTITUTIONS

are the trust that pool the funds of investors into certain types of assets such as market

investment, money, equities, cash, overseas securities and mortgage. The insurance

companies, bank subsidiaries and merchant banks do management of unit trust.

Conclusion:

The analysis of the different types of financial institutions classified by RBA depicts

that each of the institutions has different functions and objectives in terms of contribution to

the services to economy. Most of such institutions are regulated and supervised by the

authorized deposit-taking institute in Australia.

Answer to task 2:

Introduction:

The report intends to elucidate the performance of the major banks operating in

Australia by performing the analysis of data. In this study, four major banks operating in the

country has been chosen which comprise of The Australian and New Zealand banking group

limited, Common wealth bank of Australia, Westpac and National Australia bank. The

performance of these banks can be analyzed in terms of several financial indicators such as

revenue, net income earned, and profit before tax, interest, loan impairment and deposits.

Discussion:

The results of the major banks of Australia depicts that in the era of transformation of

industry, the growth seems to be challenging. There has been improvement in the margin and

loan impairment; however, the banks are facing the major change brought by operating and

regulatory environment in terms of rising level of capital, slowing growth revenue, increasing

remediation and legal cost. Different strategic initiatives and investments are pursued by the

FINANCIAL INSTRUMENTS AND INSTITUTIONS

are the trust that pool the funds of investors into certain types of assets such as market

investment, money, equities, cash, overseas securities and mortgage. The insurance

companies, bank subsidiaries and merchant banks do management of unit trust.

Conclusion:

The analysis of the different types of financial institutions classified by RBA depicts

that each of the institutions has different functions and objectives in terms of contribution to

the services to economy. Most of such institutions are regulated and supervised by the

authorized deposit-taking institute in Australia.

Answer to task 2:

Introduction:

The report intends to elucidate the performance of the major banks operating in

Australia by performing the analysis of data. In this study, four major banks operating in the

country has been chosen which comprise of The Australian and New Zealand banking group

limited, Common wealth bank of Australia, Westpac and National Australia bank. The

performance of these banks can be analyzed in terms of several financial indicators such as

revenue, net income earned, and profit before tax, interest, loan impairment and deposits.

Discussion:

The results of the major banks of Australia depicts that in the era of transformation of

industry, the growth seems to be challenging. There has been improvement in the margin and

loan impairment; however, the banks are facing the major change brought by operating and

regulatory environment in terms of rising level of capital, slowing growth revenue, increasing

remediation and legal cost. Different strategic initiatives and investments are pursued by the

5

FINANCIAL INSTRUMENTS AND INSTITUTIONS

major banks as they seek to simplify, reorient and digitize their business model (Valverde et

al., 2016).

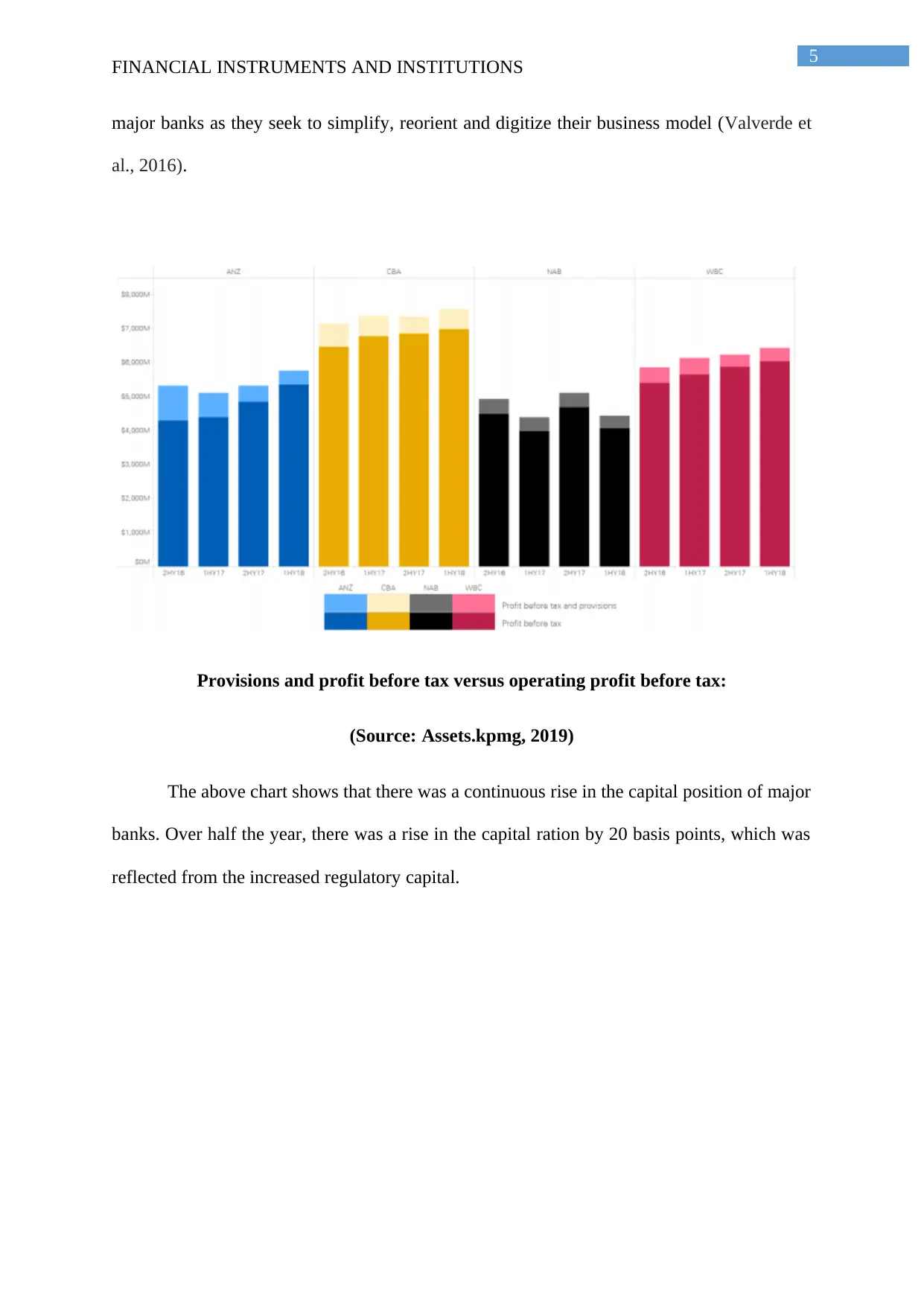

Provisions and profit before tax versus operating profit before tax:

(Source: Assets.kpmg, 2019)

The above chart shows that there was a continuous rise in the capital position of major

banks. Over half the year, there was a rise in the capital ration by 20 basis points, which was

reflected from the increased regulatory capital.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

major banks as they seek to simplify, reorient and digitize their business model (Valverde et

al., 2016).

Provisions and profit before tax versus operating profit before tax:

(Source: Assets.kpmg, 2019)

The above chart shows that there was a continuous rise in the capital position of major

banks. Over half the year, there was a rise in the capital ration by 20 basis points, which was

reflected from the increased regulatory capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL INSTRUMENTS AND INSTITUTIONS

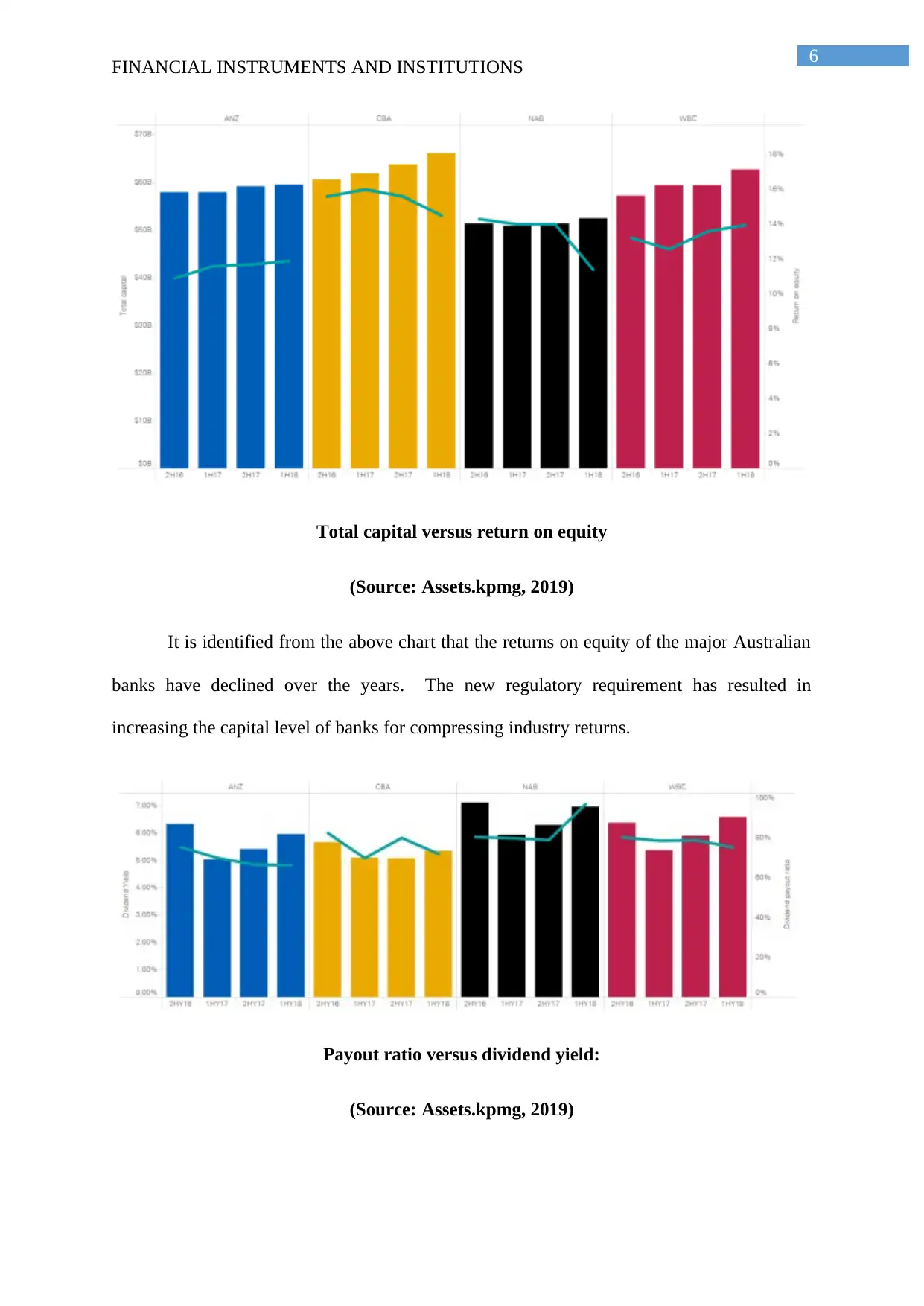

Total capital versus return on equity

(Source: Assets.kpmg, 2019)

It is identified from the above chart that the returns on equity of the major Australian

banks have declined over the years. The new regulatory requirement has resulted in

increasing the capital level of banks for compressing industry returns.

Payout ratio versus dividend yield:

(Source: Assets.kpmg, 2019)

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Total capital versus return on equity

(Source: Assets.kpmg, 2019)

It is identified from the above chart that the returns on equity of the major Australian

banks have declined over the years. The new regulatory requirement has resulted in

increasing the capital level of banks for compressing industry returns.

Payout ratio versus dividend yield:

(Source: Assets.kpmg, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL INSTRUMENTS AND INSTITUTIONS

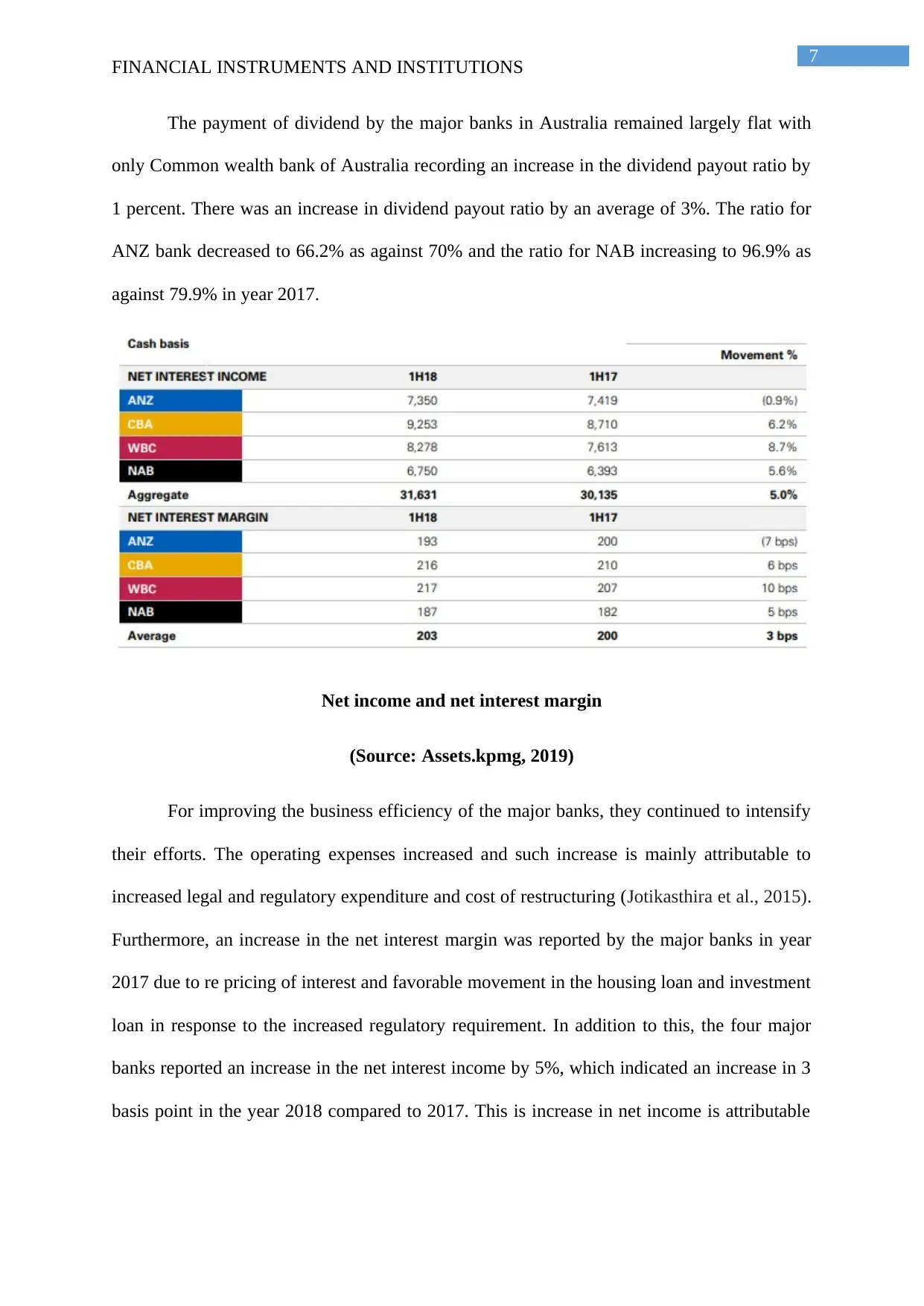

The payment of dividend by the major banks in Australia remained largely flat with

only Common wealth bank of Australia recording an increase in the dividend payout ratio by

1 percent. There was an increase in dividend payout ratio by an average of 3%. The ratio for

ANZ bank decreased to 66.2% as against 70% and the ratio for NAB increasing to 96.9% as

against 79.9% in year 2017.

Net income and net interest margin

(Source: Assets.kpmg, 2019)

For improving the business efficiency of the major banks, they continued to intensify

their efforts. The operating expenses increased and such increase is mainly attributable to

increased legal and regulatory expenditure and cost of restructuring (Jotikasthira et al., 2015).

Furthermore, an increase in the net interest margin was reported by the major banks in year

2017 due to re pricing of interest and favorable movement in the housing loan and investment

loan in response to the increased regulatory requirement. In addition to this, the four major

banks reported an increase in the net interest income by 5%, which indicated an increase in 3

basis point in the year 2018 compared to 2017. This is increase in net income is attributable

FINANCIAL INSTRUMENTS AND INSTITUTIONS

The payment of dividend by the major banks in Australia remained largely flat with

only Common wealth bank of Australia recording an increase in the dividend payout ratio by

1 percent. There was an increase in dividend payout ratio by an average of 3%. The ratio for

ANZ bank decreased to 66.2% as against 70% and the ratio for NAB increasing to 96.9% as

against 79.9% in year 2017.

Net income and net interest margin

(Source: Assets.kpmg, 2019)

For improving the business efficiency of the major banks, they continued to intensify

their efforts. The operating expenses increased and such increase is mainly attributable to

increased legal and regulatory expenditure and cost of restructuring (Jotikasthira et al., 2015).

Furthermore, an increase in the net interest margin was reported by the major banks in year

2017 due to re pricing of interest and favorable movement in the housing loan and investment

loan in response to the increased regulatory requirement. In addition to this, the four major

banks reported an increase in the net interest income by 5%, which indicated an increase in 3

basis point in the year 2018 compared to 2017. This is increase in net income is attributable

8

FINANCIAL INSTRUMENTS AND INSTITUTIONS

to factors such as deposit and mortgage repricing, decrease in cost of wholesale funding and

an increase in interest earning assets (Österholm, 2018).

Conclusion:

From the analysis of the above data pertaining to different performance indicators, it

can be inferred that the performance of banks improved in some aspects as a response to the

stringent legal and regulatory requirement. However, the expenses and costs of these banks

increased due to several factors along with slowing growth of revenue.

Answer to task 3:

Introduction:

In this report, the term structure of interest rates in Australia is demonstrated which

depicts the relationship between bond yield or interest rates and different maturities or term.

In the fixed income world, the term structure of interest rate is the most crucial benchmark

because of its role played in the economy and such interest rate is central to all the debt

securities (Kidwell et al., 2016).

Discussion:

The term structure is presented by the yield curve that helps in plotting the yield to

maturity of bonds with varying term to maturity. The Australian government bonds are used

in the Australia as the yield do not incorporate any risk premium and have essentially zero

probability of making default (Fernández and Tamayo, 2017).

FINANCIAL INSTRUMENTS AND INSTITUTIONS

to factors such as deposit and mortgage repricing, decrease in cost of wholesale funding and

an increase in interest earning assets (Österholm, 2018).

Conclusion:

From the analysis of the above data pertaining to different performance indicators, it

can be inferred that the performance of banks improved in some aspects as a response to the

stringent legal and regulatory requirement. However, the expenses and costs of these banks

increased due to several factors along with slowing growth of revenue.

Answer to task 3:

Introduction:

In this report, the term structure of interest rates in Australia is demonstrated which

depicts the relationship between bond yield or interest rates and different maturities or term.

In the fixed income world, the term structure of interest rate is the most crucial benchmark

because of its role played in the economy and such interest rate is central to all the debt

securities (Kidwell et al., 2016).

Discussion:

The term structure is presented by the yield curve that helps in plotting the yield to

maturity of bonds with varying term to maturity. The Australian government bonds are used

in the Australia as the yield do not incorporate any risk premium and have essentially zero

probability of making default (Fernández and Tamayo, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL INSTRUMENTS AND INSTITUTIONS

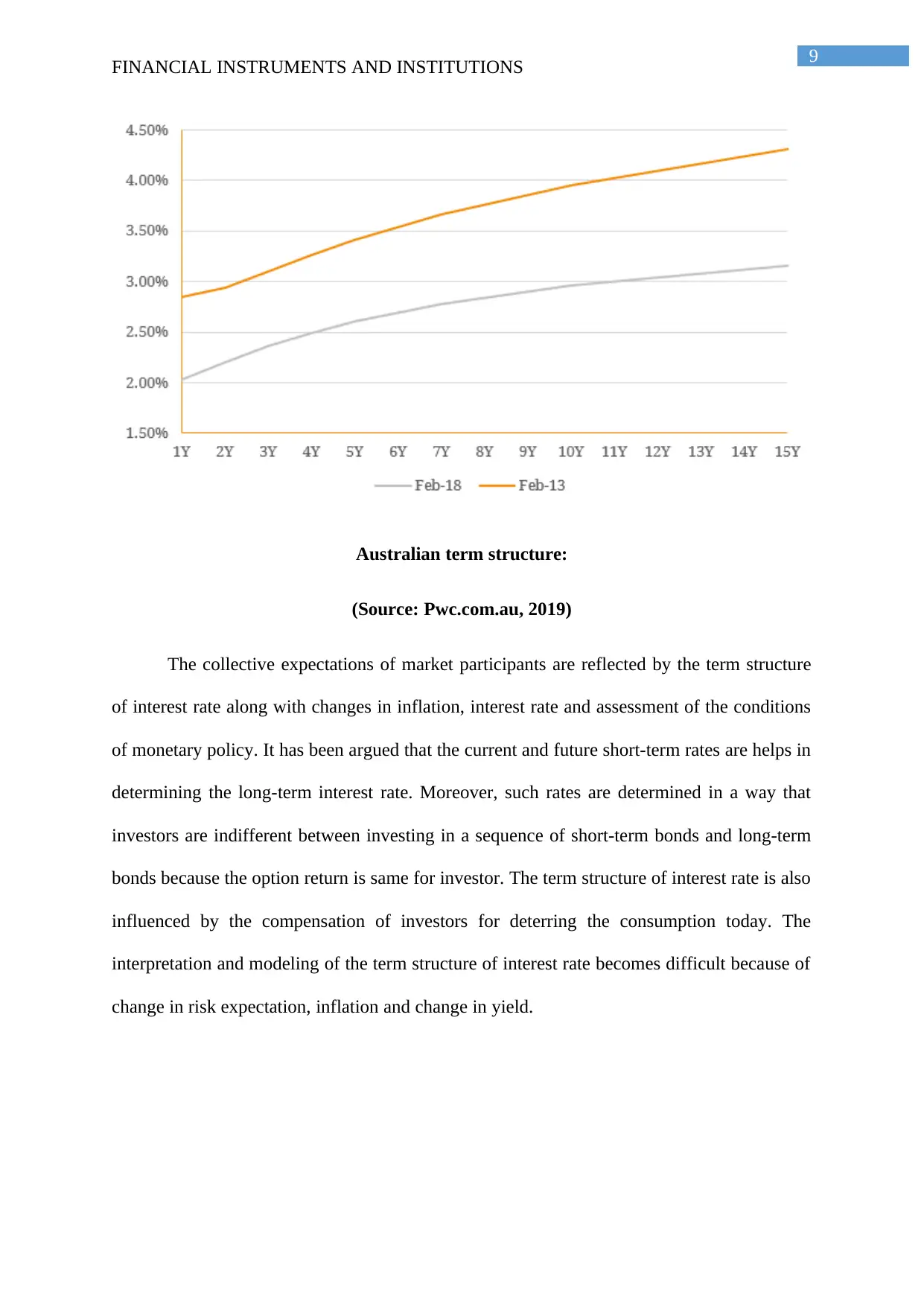

Australian term structure:

(Source: Pwc.com.au, 2019)

The collective expectations of market participants are reflected by the term structure

of interest rate along with changes in inflation, interest rate and assessment of the conditions

of monetary policy. It has been argued that the current and future short-term rates are helps in

determining the long-term interest rate. Moreover, such rates are determined in a way that

investors are indifferent between investing in a sequence of short-term bonds and long-term

bonds because the option return is same for investor. The term structure of interest rate is also

influenced by the compensation of investors for deterring the consumption today. The

interpretation and modeling of the term structure of interest rate becomes difficult because of

change in risk expectation, inflation and change in yield.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Australian term structure:

(Source: Pwc.com.au, 2019)

The collective expectations of market participants are reflected by the term structure

of interest rate along with changes in inflation, interest rate and assessment of the conditions

of monetary policy. It has been argued that the current and future short-term rates are helps in

determining the long-term interest rate. Moreover, such rates are determined in a way that

investors are indifferent between investing in a sequence of short-term bonds and long-term

bonds because the option return is same for investor. The term structure of interest rate is also

influenced by the compensation of investors for deterring the consumption today. The

interpretation and modeling of the term structure of interest rate becomes difficult because of

change in risk expectation, inflation and change in yield.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Term structure interest rate:

(Source: rba.gov.au 2019)

The data presented above in table depicts that the valuation of zero coupon bands

have changed the yield of bonds until maturity value. It has caused reduction in the interest

level until the time of maturity.

A risk is associated with the reaction of the dollar of Australia when the rate of

Australian dollar falls below the US dollar. It assumes that investors are delighted about

making investment as long as they are required to make payment via the interest premium.

The pricing and arbitrage theories are developed by using interest rate derivatives and

modeling of the term structure of interest rate. The computation of term structure of interest

rate is dependent upon the forward rates that are measured by the maturity and time.

Conclusion:

The above report has analyzed the importance of value of bond in determining the

yield and the role played by the term structure of interest rate. The justification about the term

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Term structure interest rate:

(Source: rba.gov.au 2019)

The data presented above in table depicts that the valuation of zero coupon bands

have changed the yield of bonds until maturity value. It has caused reduction in the interest

level until the time of maturity.

A risk is associated with the reaction of the dollar of Australia when the rate of

Australian dollar falls below the US dollar. It assumes that investors are delighted about

making investment as long as they are required to make payment via the interest premium.

The pricing and arbitrage theories are developed by using interest rate derivatives and

modeling of the term structure of interest rate. The computation of term structure of interest

rate is dependent upon the forward rates that are measured by the maturity and time.

Conclusion:

The above report has analyzed the importance of value of bond in determining the

yield and the role played by the term structure of interest rate. The justification about the term

11

FINANCIAL INSTRUMENTS AND INSTITUTIONS

structure of interest rate determined by the Reserve bank of Australia only if the computation

of interest rate is appropriately done using the models.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

structure of interest rate determined by the Reserve bank of Australia only if the computation

of interest rate is appropriately done using the models.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.