BAFN205 Financial Instruments: Analysis of Australian Institutions

VerifiedAdded on 2023/04/06

|13

|1910

|475

Report

AI Summary

This report provides an overview of Australian financial institutions as classified by the Reserve Bank of Australia, analyzing authorized deposit-taking institutions, non-ADI financial institutions, insurers, and fund managers. It examines the performance of Commonwealth Bank using its 2018 annual report, focusing on earnings, revenue, expenses, and asset quality. The report also discusses the term structure of interest rates in Australia and its impact on bond and share valuations, highlighting the importance of accurate interest rate calculation models. Desklib provides access to this and other solved assignments for students.

Running head: FINANCIAL INSTRUMENTS AND INSTITUTIONS

Financial instruments and institutions

Name of the student

Name of the university

Author’s note

Financial instruments and institutions

Name of the student

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Table of Contents

Answer to task 1.........................................................................................................................2

Introduction:...........................................................................................................................2

Discussion:.............................................................................................................................2

Authorized deposit-taking instruments:.............................................................................2

Non-ADI financial institutions:..........................................................................................2

Insurer and fund manager:..................................................................................................2

Conclusion:............................................................................................................................3

Answer to task 2.........................................................................................................................3

Introduction............................................................................................................................3

Discussion..............................................................................................................................3

Conclusion:............................................................................................................................7

Answer to task 3.........................................................................................................................7

Introduction:...........................................................................................................................7

Discussion:.............................................................................................................................7

Conclusion..............................................................................................................................8

References..................................................................................................................................9

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Table of Contents

Answer to task 1.........................................................................................................................2

Introduction:...........................................................................................................................2

Discussion:.............................................................................................................................2

Authorized deposit-taking instruments:.............................................................................2

Non-ADI financial institutions:..........................................................................................2

Insurer and fund manager:..................................................................................................2

Conclusion:............................................................................................................................3

Answer to task 2.........................................................................................................................3

Introduction............................................................................................................................3

Discussion..............................................................................................................................3

Conclusion:............................................................................................................................7

Answer to task 3.........................................................................................................................7

Introduction:...........................................................................................................................7

Discussion:.............................................................................................................................7

Conclusion..............................................................................................................................8

References..................................................................................................................................9

2

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Answer to task 1

Introduction:

The above topic discusses about different types of financial institutions prescribed by

reserve bank of Australia. The topic also depicts about the roles and responsibilities played

by each financial instrument in their own respective fields. RBA have differentiated all the

financial instruments in three parts and discussed the functions of each of them individually.

Discussion:

According to reserve bank of Australia the financial instruments can be divided into

three parts namely-

Authorized deposit-taking instruments:

In this part all the banks, building societies and credit unions are included. The

bank provides wide range of financial services to all the sectors of economy, funds,

management and insurance services. On the other hand, the building societies provide

deposit and home loans to the customers. Similarly, the credit unions also provide

home loans and housing loans.

Non-ADI financial institutions:

Here, the money market corporations, fiancé companies and security market

are included. Money Market Corporation operates into the primary market and

provides borrowing and lending services to the large companies. They also provide

advisory in foreign exchange, capital market. Finance companies provide housing

loans to small and medium business, raise funds by debenture, and share capital issue.

Lastly, securities have been provided by the companies backed by pool of assets

guaranteed by the third parties (Hodge, 2018).

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Answer to task 1

Introduction:

The above topic discusses about different types of financial institutions prescribed by

reserve bank of Australia. The topic also depicts about the roles and responsibilities played

by each financial instrument in their own respective fields. RBA have differentiated all the

financial instruments in three parts and discussed the functions of each of them individually.

Discussion:

According to reserve bank of Australia the financial instruments can be divided into

three parts namely-

Authorized deposit-taking instruments:

In this part all the banks, building societies and credit unions are included. The

bank provides wide range of financial services to all the sectors of economy, funds,

management and insurance services. On the other hand, the building societies provide

deposit and home loans to the customers. Similarly, the credit unions also provide

home loans and housing loans.

Non-ADI financial institutions:

Here, the money market corporations, fiancé companies and security market

are included. Money Market Corporation operates into the primary market and

provides borrowing and lending services to the large companies. They also provide

advisory in foreign exchange, capital market. Finance companies provide housing

loans to small and medium business, raise funds by debenture, and share capital issue.

Lastly, securities have been provided by the companies backed by pool of assets

guaranteed by the third parties (Hodge, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Insurer and fund manager:

All the life insurance, general insurance, health insurance provider companies,

public unit trusts, common funds and friendly societies comes into this part. The life

insurance companies provide accident and disability support to the family of insurer

over the money invested on it. General insurance companies cover insurance of

property, motor vehicles,employer’s assets, government securities and equities.

Health insurance companies provide health insurance. Apart from that the

superannuation funds manage employer’s contribution, provide retirement benefits,

the professional fund managers control these. There are public unit trusts also who

pools investors fund s from assets, equity, property,mortgages. Unit trusts are

managed by subsidiary and merchant banks (Bexley et al., 2013). The cash

management trusts provide trust deed to the public and confine investments. Lastly,

there are common funds that receive money from investor under power of attorney.

These funds are usually invested in specific types of assets. In addition to this,

friendly societies are co-operative financial institutions, which are mutually owned

and provide members a trust liker service. The benefits they provide are insurance and

educational binds, benefits linked with funeral, accident, sickness and other (Kidwell

et al., 2016).

Conclusion:

From the above case study, it can be concluded that all the types of financial

institutions prescribed by reserve bank of Australia are having their responsibility in different

areas and they are performing their roles quite well. Hence, the investors also find it easy to

accept services from them.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Insurer and fund manager:

All the life insurance, general insurance, health insurance provider companies,

public unit trusts, common funds and friendly societies comes into this part. The life

insurance companies provide accident and disability support to the family of insurer

over the money invested on it. General insurance companies cover insurance of

property, motor vehicles,employer’s assets, government securities and equities.

Health insurance companies provide health insurance. Apart from that the

superannuation funds manage employer’s contribution, provide retirement benefits,

the professional fund managers control these. There are public unit trusts also who

pools investors fund s from assets, equity, property,mortgages. Unit trusts are

managed by subsidiary and merchant banks (Bexley et al., 2013). The cash

management trusts provide trust deed to the public and confine investments. Lastly,

there are common funds that receive money from investor under power of attorney.

These funds are usually invested in specific types of assets. In addition to this,

friendly societies are co-operative financial institutions, which are mutually owned

and provide members a trust liker service. The benefits they provide are insurance and

educational binds, benefits linked with funeral, accident, sickness and other (Kidwell

et al., 2016).

Conclusion:

From the above case study, it can be concluded that all the types of financial

institutions prescribed by reserve bank of Australia are having their responsibility in different

areas and they are performing their roles quite well. Hence, the investors also find it easy to

accept services from them.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Answer to task 2

Introduction

The following case study analyses the current performance of commonwealth bank,

which is a major bank of Australia. The case study depicts the overall performance of the

banks by analyzing the annual report for the financial year 2018 through the help of financial

statements provided and supported by some data regarding performance.

Discussion

The following report has analyzed the overall performance of major bank of Australia

like commonwealth bank for the financial year 2018 (Lee et al., 2014). Commonwealth bank

is one of the major banks of Australia. They provide supports like lending and borrowing and

loans services to the other banks. This is one of the leading banks of Australia headquartered

in Sydney, NSW are providing their service since the year 1959. However being one of the

central bank if Australia they have various roles and responsibilities to figure out. These are

as follows-

1. Earnings and returns

2. Revenue generation

3. Expenses

4. Asset quality

5. Balance sheet

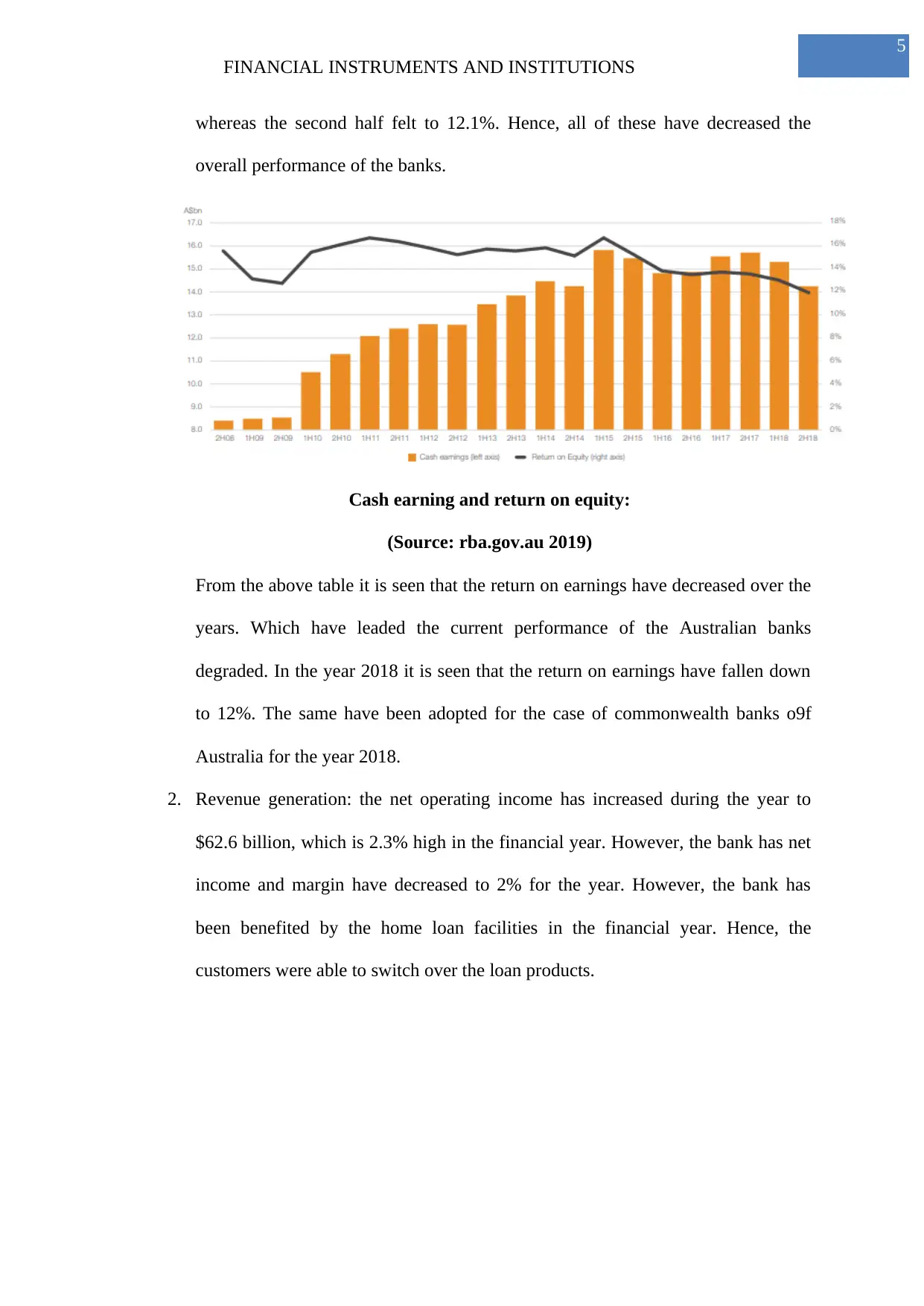

1. Earnings and returns: the earnings have fallen 5.5% to $29.5 billion in the

financial, year 2017 out of $31.2 billion. Since the earnings have fluctuated in the

last four years and the capital has steadily increased over the timeframe, hence

there is a continuous balance sheet growth. However the return on investment

have decreased to 12.5% from 17.5%.The first half have fallen below 13%

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Answer to task 2

Introduction

The following case study analyses the current performance of commonwealth bank,

which is a major bank of Australia. The case study depicts the overall performance of the

banks by analyzing the annual report for the financial year 2018 through the help of financial

statements provided and supported by some data regarding performance.

Discussion

The following report has analyzed the overall performance of major bank of Australia

like commonwealth bank for the financial year 2018 (Lee et al., 2014). Commonwealth bank

is one of the major banks of Australia. They provide supports like lending and borrowing and

loans services to the other banks. This is one of the leading banks of Australia headquartered

in Sydney, NSW are providing their service since the year 1959. However being one of the

central bank if Australia they have various roles and responsibilities to figure out. These are

as follows-

1. Earnings and returns

2. Revenue generation

3. Expenses

4. Asset quality

5. Balance sheet

1. Earnings and returns: the earnings have fallen 5.5% to $29.5 billion in the

financial, year 2017 out of $31.2 billion. Since the earnings have fluctuated in the

last four years and the capital has steadily increased over the timeframe, hence

there is a continuous balance sheet growth. However the return on investment

have decreased to 12.5% from 17.5%.The first half have fallen below 13%

5

FINANCIAL INSTRUMENTS AND INSTITUTIONS

whereas the second half felt to 12.1%. Hence, all of these have decreased the

overall performance of the banks.

Cash earning and return on equity:

(Source: rba.gov.au 2019)

From the above table it is seen that the return on earnings have decreased over the

years. Which have leaded the current performance of the Australian banks

degraded. In the year 2018 it is seen that the return on earnings have fallen down

to 12%. The same have been adopted for the case of commonwealth banks o9f

Australia for the year 2018.

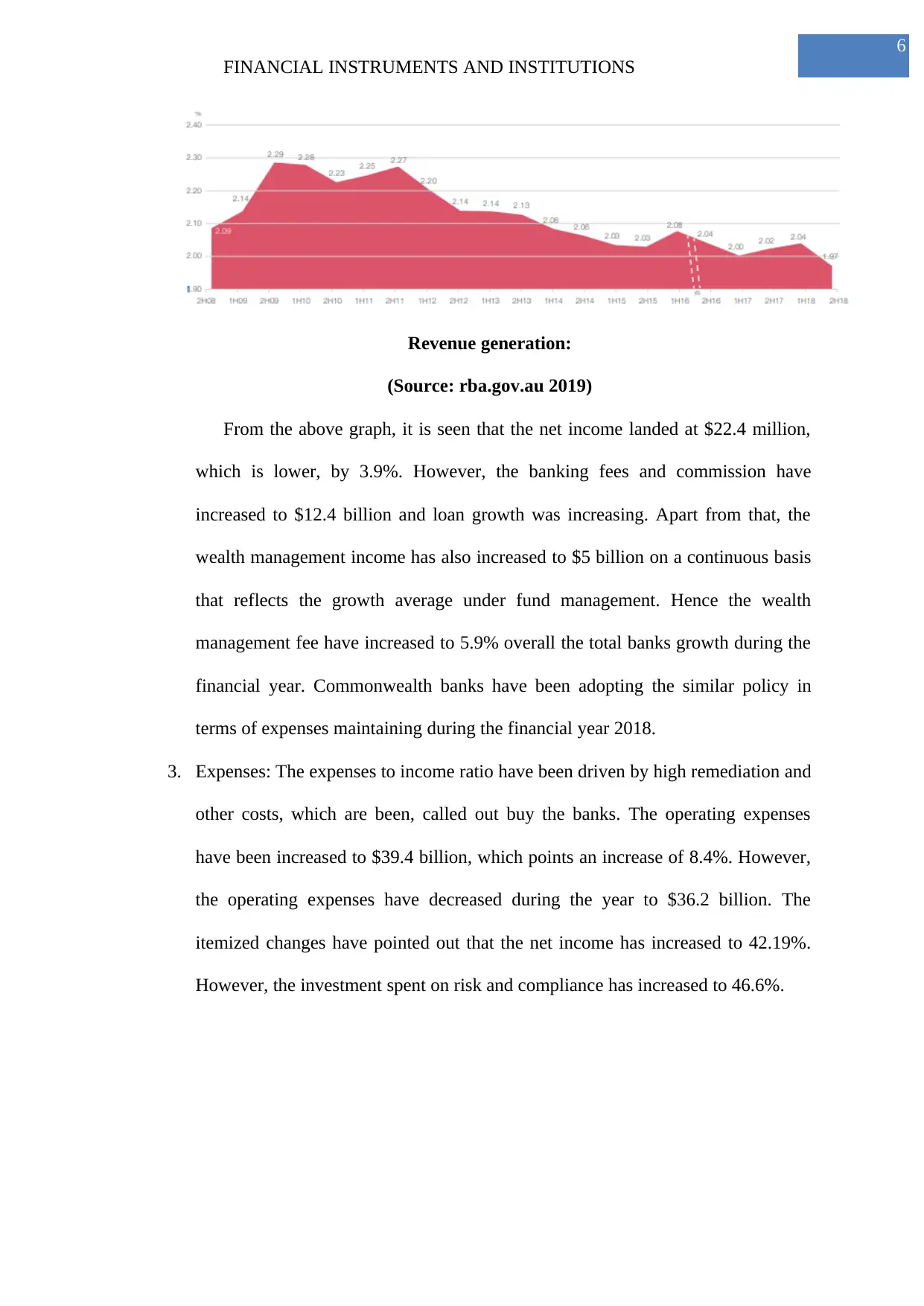

2. Revenue generation: the net operating income has increased during the year to

$62.6 billion, which is 2.3% high in the financial year. However, the bank has net

income and margin have decreased to 2% for the year. However, the bank has

been benefited by the home loan facilities in the financial year. Hence, the

customers were able to switch over the loan products.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

whereas the second half felt to 12.1%. Hence, all of these have decreased the

overall performance of the banks.

Cash earning and return on equity:

(Source: rba.gov.au 2019)

From the above table it is seen that the return on earnings have decreased over the

years. Which have leaded the current performance of the Australian banks

degraded. In the year 2018 it is seen that the return on earnings have fallen down

to 12%. The same have been adopted for the case of commonwealth banks o9f

Australia for the year 2018.

2. Revenue generation: the net operating income has increased during the year to

$62.6 billion, which is 2.3% high in the financial year. However, the bank has net

income and margin have decreased to 2% for the year. However, the bank has

been benefited by the home loan facilities in the financial year. Hence, the

customers were able to switch over the loan products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Revenue generation:

(Source: rba.gov.au 2019)

From the above graph, it is seen that the net income landed at $22.4 million,

which is lower, by 3.9%. However, the banking fees and commission have

increased to $12.4 billion and loan growth was increasing. Apart from that, the

wealth management income has also increased to $5 billion on a continuous basis

that reflects the growth average under fund management. Hence the wealth

management fee have increased to 5.9% overall the total banks growth during the

financial year. Commonwealth banks have been adopting the similar policy in

terms of expenses maintaining during the financial year 2018.

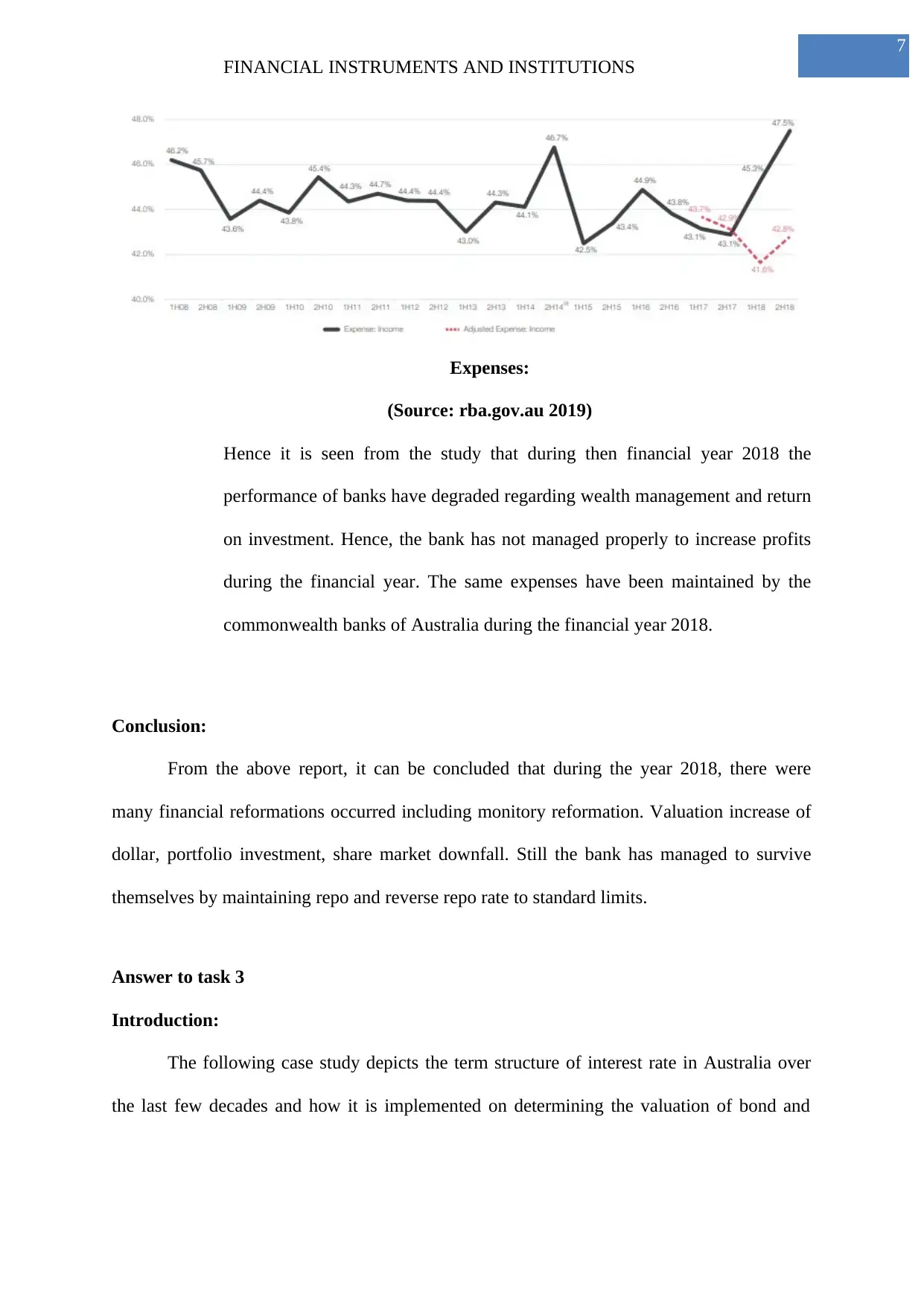

3. Expenses: The expenses to income ratio have been driven by high remediation and

other costs, which are been, called out buy the banks. The operating expenses

have been increased to $39.4 billion, which points an increase of 8.4%. However,

the operating expenses have decreased during the year to $36.2 billion. The

itemized changes have pointed out that the net income has increased to 42.19%.

However, the investment spent on risk and compliance has increased to 46.6%.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Revenue generation:

(Source: rba.gov.au 2019)

From the above graph, it is seen that the net income landed at $22.4 million,

which is lower, by 3.9%. However, the banking fees and commission have

increased to $12.4 billion and loan growth was increasing. Apart from that, the

wealth management income has also increased to $5 billion on a continuous basis

that reflects the growth average under fund management. Hence the wealth

management fee have increased to 5.9% overall the total banks growth during the

financial year. Commonwealth banks have been adopting the similar policy in

terms of expenses maintaining during the financial year 2018.

3. Expenses: The expenses to income ratio have been driven by high remediation and

other costs, which are been, called out buy the banks. The operating expenses

have been increased to $39.4 billion, which points an increase of 8.4%. However,

the operating expenses have decreased during the year to $36.2 billion. The

itemized changes have pointed out that the net income has increased to 42.19%.

However, the investment spent on risk and compliance has increased to 46.6%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Expenses:

(Source: rba.gov.au 2019)

Hence it is seen from the study that during then financial year 2018 the

performance of banks have degraded regarding wealth management and return

on investment. Hence, the bank has not managed properly to increase profits

during the financial year. The same expenses have been maintained by the

commonwealth banks of Australia during the financial year 2018.

Conclusion:

From the above report, it can be concluded that during the year 2018, there were

many financial reformations occurred including monitory reformation. Valuation increase of

dollar, portfolio investment, share market downfall. Still the bank has managed to survive

themselves by maintaining repo and reverse repo rate to standard limits.

Answer to task 3

Introduction:

The following case study depicts the term structure of interest rate in Australia over

the last few decades and how it is implemented on determining the valuation of bond and

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Expenses:

(Source: rba.gov.au 2019)

Hence it is seen from the study that during then financial year 2018 the

performance of banks have degraded regarding wealth management and return

on investment. Hence, the bank has not managed properly to increase profits

during the financial year. The same expenses have been maintained by the

commonwealth banks of Australia during the financial year 2018.

Conclusion:

From the above report, it can be concluded that during the year 2018, there were

many financial reformations occurred including monitory reformation. Valuation increase of

dollar, portfolio investment, share market downfall. Still the bank has managed to survive

themselves by maintaining repo and reverse repo rate to standard limits.

Answer to task 3

Introduction:

The following case study depicts the term structure of interest rate in Australia over

the last few decades and how it is implemented on determining the valuation of bond and

8

FINANCIAL INSTRUMENTS AND INSTITUTIONS

share price in Australia along with the objectives of adding a suitable conclusion in the

report.

Discussion:

Over the last few decades, there has been a rapid increase in trading in derivatives as

the number of products has increased. The interest rate derivatives depend upon the interest

rate models and levels. There are two ways to calculate namely spot rate and term on interest

rate. During the decades, the changes have been shifted to calculate the term interest rate

modeled by reserve bank of Australia (Swanson & Williams, 2014). This rate is used in

calculating the bond value at the end of maturity period. This interest rate bonds plotted

against the maturity curve are called yield value. According to the analysts, this value is

calculated over the interest rate of maturity period. The term structure of interest rate is often

determined by using time and length of the maturity (King & Low, 2014). This process is

used by reserve bank of Australia and commonwealth bank. In this case, the use of interest

rate and interest rate derivatives are used which develops pricing theories and including non-

arbitrage models and modeling of term structure of interest rate. For calculation purpose, the

term structure depends upon forward rates, which are measured by time and maturity. In an

arbitrage, free market the drift coefficient is determined by the volatility of the bond where

the risk lays independent (Viney & Phillips, 2015). The changes of the interest rate are shown

in yield curve. Since the interest rates can be traded in financial market, hence, instruments

like bond, currency and swaps can be traded.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

share price in Australia along with the objectives of adding a suitable conclusion in the

report.

Discussion:

Over the last few decades, there has been a rapid increase in trading in derivatives as

the number of products has increased. The interest rate derivatives depend upon the interest

rate models and levels. There are two ways to calculate namely spot rate and term on interest

rate. During the decades, the changes have been shifted to calculate the term interest rate

modeled by reserve bank of Australia (Swanson & Williams, 2014). This rate is used in

calculating the bond value at the end of maturity period. This interest rate bonds plotted

against the maturity curve are called yield value. According to the analysts, this value is

calculated over the interest rate of maturity period. The term structure of interest rate is often

determined by using time and length of the maturity (King & Low, 2014). This process is

used by reserve bank of Australia and commonwealth bank. In this case, the use of interest

rate and interest rate derivatives are used which develops pricing theories and including non-

arbitrage models and modeling of term structure of interest rate. For calculation purpose, the

term structure depends upon forward rates, which are measured by time and maturity. In an

arbitrage, free market the drift coefficient is determined by the volatility of the bond where

the risk lays independent (Viney & Phillips, 2015). The changes of the interest rate are shown

in yield curve. Since the interest rates can be traded in financial market, hence, instruments

like bond, currency and swaps can be traded.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL INSTRUMENTS AND INSTITUTIONS

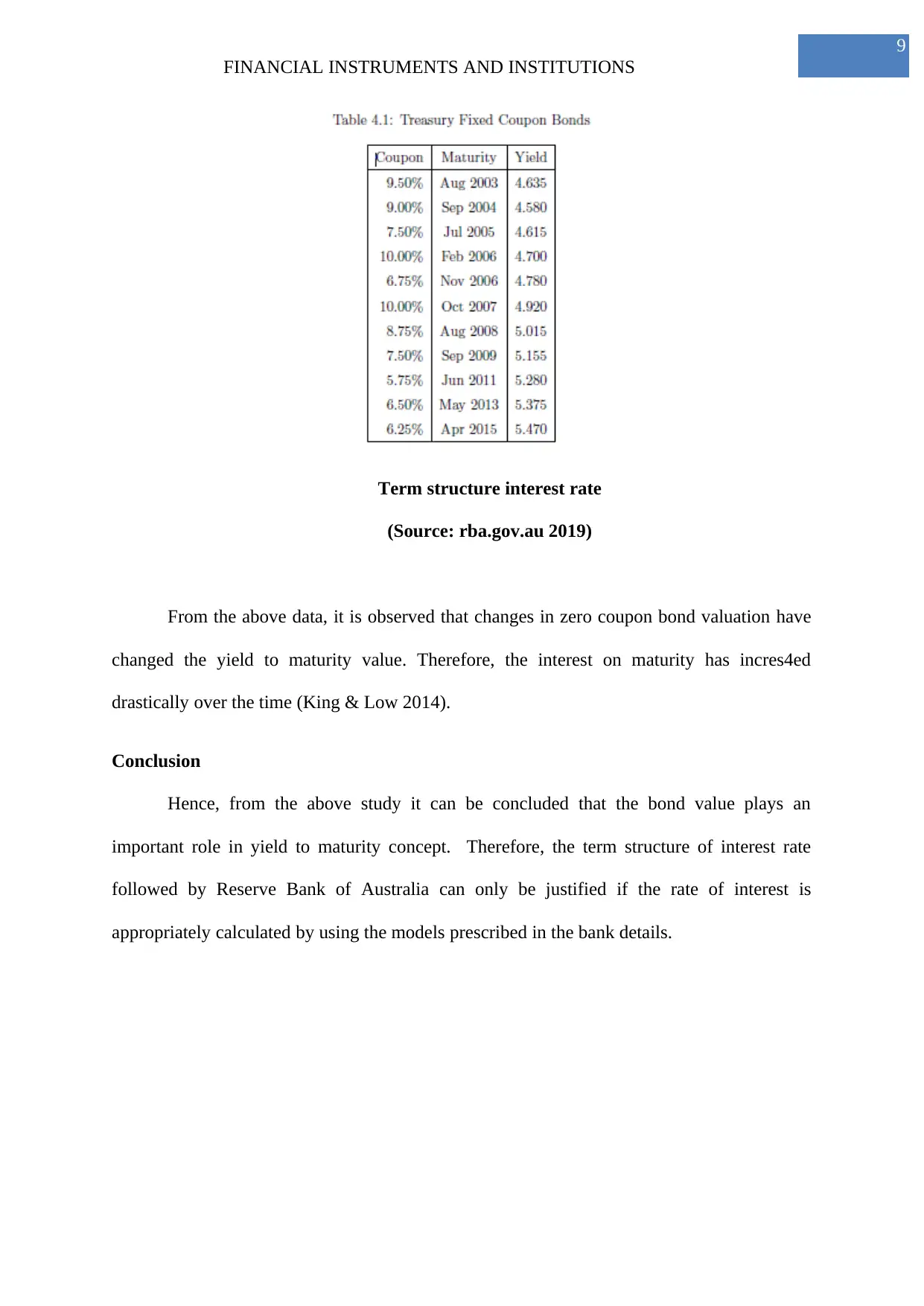

Term structure interest rate

(Source: rba.gov.au 2019)

From the above data, it is observed that changes in zero coupon bond valuation have

changed the yield to maturity value. Therefore, the interest on maturity has incres4ed

drastically over the time (King & Low 2014).

Conclusion

Hence, from the above study it can be concluded that the bond value plays an

important role in yield to maturity concept. Therefore, the term structure of interest rate

followed by Reserve Bank of Australia can only be justified if the rate of interest is

appropriately calculated by using the models prescribed in the bank details.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

Term structure interest rate

(Source: rba.gov.au 2019)

From the above data, it is observed that changes in zero coupon bond valuation have

changed the yield to maturity value. Therefore, the interest on maturity has incres4ed

drastically over the time (King & Low 2014).

Conclusion

Hence, from the above study it can be concluded that the bond value plays an

important role in yield to maturity concept. Therefore, the term structure of interest rate

followed by Reserve Bank of Australia can only be justified if the rate of interest is

appropriately calculated by using the models prescribed in the bank details.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL INSTRUMENTS AND INSTITUTIONS

FINANCIAL INSTRUMENTS AND INSTITUTIONS

11

FINANCIAL INSTRUMENTS AND INSTITUTIONS

References

Badarinza, C., Campbell, J. Y., & Ramadorai, T. (2017). What calls to ARMs? International

evidence on interest rates and the choice of adjustable-rate mortgages. Management

Science, 64(5), 2275-2288.

Bexley, E., Daroesman, S., Arkoudis, S., & James, R. (2013). University Student Finances in

2012: A Study of the Financial Circumstances of Domestic and International Students

in Australia's Universities. Centre for the Study of Higher Education.

Galbreath, J. (2013). ESG in focus: the Australian evidence. Journal of business

ethics, 118(3), 529-541.

Hodge, G. (2018). Privatization: An international review of performance. Routledge.

Kidwell, D. S., Blackwell, D. W., Sias, R. W., & Whidbee, D. A. (2016). Financial

institutions, markets, and money. John Wiley & Sons.

Rogers, M. (2018). Financial Institutions and Markets. In An Economist’s Guide to Economic

History (pp. 87-94). Palgrave Macmillan, Cham.

King, M., & Low, D. (2014). Measuring the''world''real interest rate (No. w19887). National

Bureau of Economic Research.

Lee, C. C., Hsieh, M. F., & Yang, S. J. (2014). The relationship between revenue

diversification and bank performance: Do financial structures and financial reforms

matter?. Japan and the World Economy, 29, 18-35.

Reserve Bank of Australia. (2019). Reserve Bank of Australia. Retrieved 22 March 2019,

from https://www.rba.gov.au/

Swanson, E. T., & Williams, J. C. (2014). Measuring the effect of the zero lower bound on

medium-and longer-term interest rates. American Economic Review, 104(10), 3154-

85.

FINANCIAL INSTRUMENTS AND INSTITUTIONS

References

Badarinza, C., Campbell, J. Y., & Ramadorai, T. (2017). What calls to ARMs? International

evidence on interest rates and the choice of adjustable-rate mortgages. Management

Science, 64(5), 2275-2288.

Bexley, E., Daroesman, S., Arkoudis, S., & James, R. (2013). University Student Finances in

2012: A Study of the Financial Circumstances of Domestic and International Students

in Australia's Universities. Centre for the Study of Higher Education.

Galbreath, J. (2013). ESG in focus: the Australian evidence. Journal of business

ethics, 118(3), 529-541.

Hodge, G. (2018). Privatization: An international review of performance. Routledge.

Kidwell, D. S., Blackwell, D. W., Sias, R. W., & Whidbee, D. A. (2016). Financial

institutions, markets, and money. John Wiley & Sons.

Rogers, M. (2018). Financial Institutions and Markets. In An Economist’s Guide to Economic

History (pp. 87-94). Palgrave Macmillan, Cham.

King, M., & Low, D. (2014). Measuring the''world''real interest rate (No. w19887). National

Bureau of Economic Research.

Lee, C. C., Hsieh, M. F., & Yang, S. J. (2014). The relationship between revenue

diversification and bank performance: Do financial structures and financial reforms

matter?. Japan and the World Economy, 29, 18-35.

Reserve Bank of Australia. (2019). Reserve Bank of Australia. Retrieved 22 March 2019,

from https://www.rba.gov.au/

Swanson, E. T., & Williams, J. C. (2014). Measuring the effect of the zero lower bound on

medium-and longer-term interest rates. American Economic Review, 104(10), 3154-

85.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.