Cross-Border GST: Analysis of Australian Exported Goods and Services

VerifiedAdded on 2023/05/29

|32

|8910

|159

Report

AI Summary

This report analyzes the Australian Goods and Services Tax (GST) concerning exported goods and services, with a specific focus on services delivered via the internet. It begins with an introduction to the GST system and the concept of exports. The report then delves into specific sections of the GST Act, including Section 38-185, which addresses exports of goods, and Section 38-190, which covers supplies of things (other than goods or real property) for consumption outside the indirect tax zone. The report discusses the application of these sections, providing examples and clarifying the criteria for GST-free status. Furthermore, it examines the treatment of exported services, particularly those delivered via the internet, a critical aspect of modern international trade. The report provides a comparative analysis of the EU-VAT and New Zealand models, exploring the strengths and weaknesses of each approach and highlighting any controversies or conflicts that arise. Finally, the report offers personal opinions on the most effective approach and concludes with recommendations for optimizing the GST framework for exported services. This document is a valuable resource for students studying tax law and international trade, available on Desklib.

Running head: AUSTRALIAN GOODS AND SERVICE TAX

Australian Goods and Service Tax

Name of the Student

Name of the University

Authors Note

Course ID

Australian Goods and Service Tax

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUSTRALIAN GOODS AND SERVICE TAX

Table of Contents

Introduction:...............................................................................................................................2

Section 38-185: Exports of Goods:............................................................................................2

Section 38-190: Supply of things, apart from goods or real property, for consumption out of

the indirect tax zone:..................................................................................................................6

Discussion about the treatment of exported services, particularly services delivered via the

internet:....................................................................................................................................12

Comparative Discussion of EU Model with New Zealand Model:.........................................16

EU-VAT Model:......................................................................................................................16

New Zealand Model:................................................................................................................19

Controversy or cause of Conflicts:...........................................................................................21

Personal opinion on using the AUS/NZ approach or EU Approach:.......................................22

Recommendations:...................................................................................................................23

Conclusion:..............................................................................................................................24

References:...............................................................................................................................25

Table of Contents

Introduction:...............................................................................................................................2

Section 38-185: Exports of Goods:............................................................................................2

Section 38-190: Supply of things, apart from goods or real property, for consumption out of

the indirect tax zone:..................................................................................................................6

Discussion about the treatment of exported services, particularly services delivered via the

internet:....................................................................................................................................12

Comparative Discussion of EU Model with New Zealand Model:.........................................16

EU-VAT Model:......................................................................................................................16

New Zealand Model:................................................................................................................19

Controversy or cause of Conflicts:...........................................................................................21

Personal opinion on using the AUS/NZ approach or EU Approach:.......................................22

Recommendations:...................................................................................................................23

Conclusion:..............................................................................................................................24

References:...............................................................................................................................25

2AUSTRALIAN GOODS AND SERVICE TAX

Introduction:

The exports of goods and services constitutes the value of goods and other services

that are provided in the market to all across the world. These includes the value of

merchandise, freight, insurance, transport and government services. However, it excludes the

compensation that is paid to the employees and investment of income along with transfer

payments. On the other hand, GST is not collected on the cross border services and the

intangibles that are purchased from the offshore suppliers1. When the introduction of GST

was first made in 1986 there were only few customers from New Zealand. The paper would

address the questions relating to the cross border application of GST on the services and

intangibles. A comparative study of the EU-VAT and AUS/NZ Model would be studied to

understand the reliability of the model. A further recommendation would be sought following

the analysis of both the model.

Section 38-185: Exports of Goods:

As stated under “section 38-185 (1)” of the New Tax System in Goods and Service Tax

Act 1999 the supply of goods for the purpose of export are treated as GST-free. However, the

exported goods are only GST-free if the supplier exports the goods from Australia inside 60

days following the day on which the suppler receives the considerations2. Furthermore, the

exported goods are GST-free if on the previous day the supplier provides an invoice relating

to supply which is the day on which an invoice is provided by the supplier. In other words, if

1 Feria, Rita de la, and Max Schofield. "Towards an [Unlawful] Modernized EU VAT Rate

Policy." EC Tax Review 26.2 (2017): 89-95.

2 "Taxpolicy.ird.govt.nz". Taxpolicy.ird.govt.nz, 2018. Online. Internet. 26 Nov. 2018. .

Available: https://taxpolicy.ird.govt.nz/sites/default/files/2015-dd-gst-cross-border.pdf.

Introduction:

The exports of goods and services constitutes the value of goods and other services

that are provided in the market to all across the world. These includes the value of

merchandise, freight, insurance, transport and government services. However, it excludes the

compensation that is paid to the employees and investment of income along with transfer

payments. On the other hand, GST is not collected on the cross border services and the

intangibles that are purchased from the offshore suppliers1. When the introduction of GST

was first made in 1986 there were only few customers from New Zealand. The paper would

address the questions relating to the cross border application of GST on the services and

intangibles. A comparative study of the EU-VAT and AUS/NZ Model would be studied to

understand the reliability of the model. A further recommendation would be sought following

the analysis of both the model.

Section 38-185: Exports of Goods:

As stated under “section 38-185 (1)” of the New Tax System in Goods and Service Tax

Act 1999 the supply of goods for the purpose of export are treated as GST-free. However, the

exported goods are only GST-free if the supplier exports the goods from Australia inside 60

days following the day on which the suppler receives the considerations2. Furthermore, the

exported goods are GST-free if on the previous day the supplier provides an invoice relating

to supply which is the day on which an invoice is provided by the supplier. In other words, if

1 Feria, Rita de la, and Max Schofield. "Towards an [Unlawful] Modernized EU VAT Rate

Policy." EC Tax Review 26.2 (2017): 89-95.

2 "Taxpolicy.ird.govt.nz". Taxpolicy.ird.govt.nz, 2018. Online. Internet. 26 Nov. 2018. .

Available: https://taxpolicy.ird.govt.nz/sites/default/files/2015-dd-gst-cross-border.pdf.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUSTRALIAN GOODS AND SERVICE TAX

a person sells the goods for export then it should be made sure that the export of goods is

done within the time limit that is given under the “section 38-185 (1)” unless the below listed

special rules for export are applicable; The special rules for export are;

a. Export of goods where the payment of consideration is made in portions (section 38-

185 (1) 2).

b. Exporting the aircraft or ships under section 38-185 (1) 3).

c. Exporting the aircraft or ships where the considerations relating to supply is paid in

portions (section 38-185(1)4).

d. Goods which are consumed on the overseas flights or voyages (section 38-185(1)5).

e. Goods that are used for repair, modifying or treating goods which is used for import

for the repairing purpose before making any export (section 38-185(1)6)3.

f. Goods that are exported by travellers based on their accompanied baggage (section

38-185(1)7).

When the goods or any other aircraft of ships is supplied and the considerations

arising is paid in portions then the 60-day period commences from the time when the final

instalment is received by the supplier except an invoice has been previously given for the

final instalment4.

The perfect communication regarding the export sales signifies that the exporter

should assure compliance inside the limits or the risk of losing benefits relating to GST free

3 de la Feria, Rita. "EU VAT principles as interpretative aids to EU VAT rules: the inherent

paradox." (2015).

4 Annacondia, Fabiola, ed. EU VAT Compass 2015/2016. IBFD Publications, 2015.

a person sells the goods for export then it should be made sure that the export of goods is

done within the time limit that is given under the “section 38-185 (1)” unless the below listed

special rules for export are applicable; The special rules for export are;

a. Export of goods where the payment of consideration is made in portions (section 38-

185 (1) 2).

b. Exporting the aircraft or ships under section 38-185 (1) 3).

c. Exporting the aircraft or ships where the considerations relating to supply is paid in

portions (section 38-185(1)4).

d. Goods which are consumed on the overseas flights or voyages (section 38-185(1)5).

e. Goods that are used for repair, modifying or treating goods which is used for import

for the repairing purpose before making any export (section 38-185(1)6)3.

f. Goods that are exported by travellers based on their accompanied baggage (section

38-185(1)7).

When the goods or any other aircraft of ships is supplied and the considerations

arising is paid in portions then the 60-day period commences from the time when the final

instalment is received by the supplier except an invoice has been previously given for the

final instalment4.

The perfect communication regarding the export sales signifies that the exporter

should assure compliance inside the limits or the risk of losing benefits relating to GST free

3 de la Feria, Rita. "EU VAT principles as interpretative aids to EU VAT rules: the inherent

paradox." (2015).

4 Annacondia, Fabiola, ed. EU VAT Compass 2015/2016. IBFD Publications, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUSTRALIAN GOODS AND SERVICE TAX

treatment5. While writing, a modification was issued to change the inside 60-day requirement

to before or inside 60 days so that it can cover the circumstances where the goods exported

prior to making payment and before issuing the invoice6. The GST-Free legislature is also

revised to enable GST-Free status for the goods that is supplied in Australia to the export

purchaser who has not obtained registration under the Australian GST. The law is presently

undertaken only provides GST-Frees supplies where the supplier also forms the exporter of

goods.

The supply of aircraft stores or ship that are for consumption, use or sale on the flight or

voyage or has the destination out of Australia are treated as GST-free7. In spite of the fact that

ineffective and unwanted features of the old wholesale sales tax system particularly claiming

of exemption were thought of being abandoned, it appears that the conditional exemption

system might still be applicable for the GST purpose. Accordingly, section 38-185 (1) 6 gives

GST-free status to supply the goods at the time of repairing, modifying, renovating or treating

other goods from out of Australia but only to the extent that;

a. Goods are attached or turns out to be a part of other goods;

5 "Www5.austlii.edu.au". Www5.austlii.edu.au, 2018. Online. Internet. 26 Nov. 2018. .

Available: http://www5.austlii.edu.au/au/journals/RevenueLawJl/2004/7.pdf.

6 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018.

7 Henkow, Oskar. "Sveda—The increasing obscurity of the direct link test in EU VAT:

Judgment of the Court of Justice of the European Union of 22 October 2015 in Case C-

126/14–Sveda." World Journal of VAT/GST Law 5.1 (2016): 48-54.

treatment5. While writing, a modification was issued to change the inside 60-day requirement

to before or inside 60 days so that it can cover the circumstances where the goods exported

prior to making payment and before issuing the invoice6. The GST-Free legislature is also

revised to enable GST-Free status for the goods that is supplied in Australia to the export

purchaser who has not obtained registration under the Australian GST. The law is presently

undertaken only provides GST-Frees supplies where the supplier also forms the exporter of

goods.

The supply of aircraft stores or ship that are for consumption, use or sale on the flight or

voyage or has the destination out of Australia are treated as GST-free7. In spite of the fact that

ineffective and unwanted features of the old wholesale sales tax system particularly claiming

of exemption were thought of being abandoned, it appears that the conditional exemption

system might still be applicable for the GST purpose. Accordingly, section 38-185 (1) 6 gives

GST-free status to supply the goods at the time of repairing, modifying, renovating or treating

other goods from out of Australia but only to the extent that;

a. Goods are attached or turns out to be a part of other goods;

5 "Www5.austlii.edu.au". Www5.austlii.edu.au, 2018. Online. Internet. 26 Nov. 2018. .

Available: http://www5.austlii.edu.au/au/journals/RevenueLawJl/2004/7.pdf.

6 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018.

7 Henkow, Oskar. "Sveda—The increasing obscurity of the direct link test in EU VAT:

Judgment of the Court of Justice of the European Union of 22 October 2015 in Case C-

126/14–Sveda." World Journal of VAT/GST Law 5.1 (2016): 48-54.

5AUSTRALIAN GOODS AND SERVICE TAX

b. The goods turn out to be unusable or worthless as a result of repair, renovation,

modification or treating other goods.

Section 38-185 intends to help person that import goods in Australia for the purpose

of repair and exporting them subsequently8. The section functions by giving GST-free status

to the goods that is supplied during the course of offering repair services. While it may be

relatively easy to state that the goods which is supplied during the course of their attachment

or incorporation with other goods that might be far difficult to establish that the goods are

covered or supplied during the course of repair work.

Other services that are GST-free on export are the labour services. The manufacturer

relating to the supply of goods during the phase of contract might be treated as GST-free

under section38-185 (1) 19. Finally, the supply of goods to the Australian and overseas

national tourist that are prescribed under the rules of export goods are anticipated to be GST-

free. The prescribed rules are anticipated to bear a resemblance to the current set of rules for

tax-free and sales tax free on sales made to the overseas travellers.

Evidences of GST-Free status:

As per the ATO expectations exporters and other persons that are dependent on the

GST-free treatment under the section 38-185 to generate evidence whenever required10. Proof

8 Ramli, Rosiati, et al. "Compliance costs of Goods and Services Tax (GST) among small and

medium enterprises." Jurnal Pengurusan (UKM Journal of Management) 45 (2015).

9 King, David. Fiscal Tiers (Routledge Revivals): The Economics of Multi-Level Government.

Routledge, 2016.

10 Schenk, Alan, Victor Thuronyi, and Wei Cui. Value added tax. Cambridge University

Press, 2015.

b. The goods turn out to be unusable or worthless as a result of repair, renovation,

modification or treating other goods.

Section 38-185 intends to help person that import goods in Australia for the purpose

of repair and exporting them subsequently8. The section functions by giving GST-free status

to the goods that is supplied during the course of offering repair services. While it may be

relatively easy to state that the goods which is supplied during the course of their attachment

or incorporation with other goods that might be far difficult to establish that the goods are

covered or supplied during the course of repair work.

Other services that are GST-free on export are the labour services. The manufacturer

relating to the supply of goods during the phase of contract might be treated as GST-free

under section38-185 (1) 19. Finally, the supply of goods to the Australian and overseas

national tourist that are prescribed under the rules of export goods are anticipated to be GST-

free. The prescribed rules are anticipated to bear a resemblance to the current set of rules for

tax-free and sales tax free on sales made to the overseas travellers.

Evidences of GST-Free status:

As per the ATO expectations exporters and other persons that are dependent on the

GST-free treatment under the section 38-185 to generate evidence whenever required10. Proof

8 Ramli, Rosiati, et al. "Compliance costs of Goods and Services Tax (GST) among small and

medium enterprises." Jurnal Pengurusan (UKM Journal of Management) 45 (2015).

9 King, David. Fiscal Tiers (Routledge Revivals): The Economics of Multi-Level Government.

Routledge, 2016.

10 Schenk, Alan, Victor Thuronyi, and Wei Cui. Value added tax. Cambridge University

Press, 2015.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUSTRALIAN GOODS AND SERVICE TAX

might comprise of bills of lading, airway bills, proof relating to the export from the

Australian custom services of importation from the state to which the goods are exported.

Nevertheless, the above stated requirement are not likely to be burdensome where the

supplier is also the exporter11. However, in certain situations the suppliers might face the

difficulty to obtain the necessary evidences such as the status of GST-free depending on the

intent or subsequent act of a customer.

Section 38-190: Supply of things, apart from goods or real property, for consumption

out of the indirect tax zone:

Under section 38-190 supply things apart from goods or real property may be treated

as GST-free where the consumption is made out of Australia. However, deciding whether the

supply of goods is consumed out of Australia is not regarded as the easy job12. Under the

section 38-190(1) 1, supplies that are connected directly with the goods or real property

located out of Australia would be treated as GST-free. The example includes the preparation

of designs plans by the Australian architect for the Australian resident where the property is

out of Australia.

Supplies that are made to the non-resident that are not Australian when the supply of good is

done then it is treated as GST-free under the section 38-190 given that;

11 Millar, R. (2013). Tax Base/Tax Rates. Court of Justice of the European Union: Recent

VAT Case Law 2013, Vienna, Austria: Presentation.

12 Lejeune, Ine, and Charlène A. Herbain. "Recent developments on EU VAT: VAT Digital

Single Market package." British Tax Review 1 (2018): 1-5.

might comprise of bills of lading, airway bills, proof relating to the export from the

Australian custom services of importation from the state to which the goods are exported.

Nevertheless, the above stated requirement are not likely to be burdensome where the

supplier is also the exporter11. However, in certain situations the suppliers might face the

difficulty to obtain the necessary evidences such as the status of GST-free depending on the

intent or subsequent act of a customer.

Section 38-190: Supply of things, apart from goods or real property, for consumption

out of the indirect tax zone:

Under section 38-190 supply things apart from goods or real property may be treated

as GST-free where the consumption is made out of Australia. However, deciding whether the

supply of goods is consumed out of Australia is not regarded as the easy job12. Under the

section 38-190(1) 1, supplies that are connected directly with the goods or real property

located out of Australia would be treated as GST-free. The example includes the preparation

of designs plans by the Australian architect for the Australian resident where the property is

out of Australia.

Supplies that are made to the non-resident that are not Australian when the supply of good is

done then it is treated as GST-free under the section 38-190 given that;

11 Millar, R. (2013). Tax Base/Tax Rates. Court of Justice of the European Union: Recent

VAT Case Law 2013, Vienna, Austria: Presentation.

12 Lejeune, Ine, and Charlène A. Herbain. "Recent developments on EU VAT: VAT Digital

Single Market package." British Tax Review 1 (2018): 1-5.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUSTRALIAN GOODS AND SERVICE TAX

a. The supply is not directly related goods that are located outside Australia when the

goods supplied is completed or;

b. There is no direct relation with the supply of real property that are out of Australia.

Thus, the design plans that are made by the Australian architect for the non-resident

would not be treated as GST-free given the property is out of Australia13. Though, legal

instruction provided to the non-resident customers for the operation of Australian GST would

be treated as GST-free given that the customers was not the Australian resident. In another

example, the liability for GST on the domestic delivery of goods could not be avoided by

sending the delivery of invoice to the offshore entity.

According to the scholars it is worth saying that when the supply of goods is done and not

during the time of supply due to the reason of precision14. For example, a right of service may

be supplied on a given day and may be used on a different day. Supplies that is made to the

recipient is regarded as GST-free when;

a. The recipient of goods is not the Australian resident or when the goods supplied is

used or enjoyed.

b. The goods that are supplied is used and enjoyed out of Australia.

13 Millar, R. (2017). Addressing New VAT/GST Challenges and Increasing the Efficiency

and Effectiveness of VAT Administration: Lessons Learned and Future Action. Fourth

Meeting of the OECD Global Forum on VAT 2017, Paris, France: Presentation.

14 Millar, R. (2016). How different is the Australian GST really? The VAT / GST Seminar

2016: The Federal Court of Australia and Melbourne Law School, Melbourne, Vic:

Presentation.

a. The supply is not directly related goods that are located outside Australia when the

goods supplied is completed or;

b. There is no direct relation with the supply of real property that are out of Australia.

Thus, the design plans that are made by the Australian architect for the non-resident

would not be treated as GST-free given the property is out of Australia13. Though, legal

instruction provided to the non-resident customers for the operation of Australian GST would

be treated as GST-free given that the customers was not the Australian resident. In another

example, the liability for GST on the domestic delivery of goods could not be avoided by

sending the delivery of invoice to the offshore entity.

According to the scholars it is worth saying that when the supply of goods is done and not

during the time of supply due to the reason of precision14. For example, a right of service may

be supplied on a given day and may be used on a different day. Supplies that is made to the

recipient is regarded as GST-free when;

a. The recipient of goods is not the Australian resident or when the goods supplied is

used or enjoyed.

b. The goods that are supplied is used and enjoyed out of Australia.

13 Millar, R. (2017). Addressing New VAT/GST Challenges and Increasing the Efficiency

and Effectiveness of VAT Administration: Lessons Learned and Future Action. Fourth

Meeting of the OECD Global Forum on VAT 2017, Paris, France: Presentation.

14 Millar, R. (2016). How different is the Australian GST really? The VAT / GST Seminar

2016: The Federal Court of Australia and Melbourne Law School, Melbourne, Vic:

Presentation.

8AUSTRALIAN GOODS AND SERVICE TAX

c. The goods supplied has no direct connection with the goods that are located in

Australia when the thing that is supplied is carried out with the real property located

in Australia.

Therefore, an Australian resident that purchases the overseas travel insurance from the

local supplier may not be required to pay the GST given that the person was not present in

Australia when the coverage for travel insurance began. Supplies that are made in respect to

the rights of GST-free under the section 38-190 (1) 4, given that;

a. Rights are using it out of Australia

b. The supply is made to the entity which is non-resident of Australia and located out of

Australia when the thing that is done.

Similarly, the sale of Disneyland tickets in Australia must be free from GST since the

tickets are to be used outside Australia15. Sales made by the Australian copyright owner to the

non-resident of the right to distribute the products in the country apart from Australian must

be treated as GST-free supply.

Under section 38-190 (1) 5, GST-free status applies to supplies that comprises of

renovation, repairs, modifications or treatment of the imported goods that are fixed before

making export16. Section 38-190(1) 6, seems to be envisioned to cover the supply of things

apart from goods such as labour services.

15 Millar, R. (2013). Thoughts on the contribution of the late Justice J.G. Hill to Australia's

GST. Australian Tax Forum, 28(1), 137-153.

16 Millar, R. (2015). Comments on Supply of Goods and Services in VAT Law. Court of

Justice of the European Union: Recent VAT Case Law 2015, Vienna, Austria: Presentation.

c. The goods supplied has no direct connection with the goods that are located in

Australia when the thing that is supplied is carried out with the real property located

in Australia.

Therefore, an Australian resident that purchases the overseas travel insurance from the

local supplier may not be required to pay the GST given that the person was not present in

Australia when the coverage for travel insurance began. Supplies that are made in respect to

the rights of GST-free under the section 38-190 (1) 4, given that;

a. Rights are using it out of Australia

b. The supply is made to the entity which is non-resident of Australia and located out of

Australia when the thing that is done.

Similarly, the sale of Disneyland tickets in Australia must be free from GST since the

tickets are to be used outside Australia15. Sales made by the Australian copyright owner to the

non-resident of the right to distribute the products in the country apart from Australian must

be treated as GST-free supply.

Under section 38-190 (1) 5, GST-free status applies to supplies that comprises of

renovation, repairs, modifications or treatment of the imported goods that are fixed before

making export16. Section 38-190(1) 6, seems to be envisioned to cover the supply of things

apart from goods such as labour services.

15 Millar, R. (2013). Thoughts on the contribution of the late Justice J.G. Hill to Australia's

GST. Australian Tax Forum, 28(1), 137-153.

16 Millar, R. (2015). Comments on Supply of Goods and Services in VAT Law. Court of

Justice of the European Union: Recent VAT Case Law 2015, Vienna, Austria: Presentation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUSTRALIAN GOODS AND SERVICE TAX

General exclusion:

A supply of things apart from the goods or real property is not regarded as the free

from GST given the supply of right of options to obtain something where the supply would

be linked to Australia17. The general exclusion under section 38-190 (2) is aimed at catching

the net GST related to supply of rights or options offshore where the exercise of rights or

options is associated with Australia. For example, tickets of grand finale to be held in

Australia were sold the New Zealand Company which later sold the tickets to Australian and

New Zealand residents. Since the supply of grand finale is linked to Australia therefore, the

supply of tickets to the company located in New Zealand would not be regarded as GST-free.

17 Millar, R., Moon, L. (2014). Australia. In Michael Lang, Ine Lejeune (Eds.), Improving

VAT/GST: Designing a Simple and Fraud-Proof Tax System, (pp. 23-110). Amsterdam, The

Netherlands: International Bureau of Fiscal Documentation (IBFD).

General exclusion:

A supply of things apart from the goods or real property is not regarded as the free

from GST given the supply of right of options to obtain something where the supply would

be linked to Australia17. The general exclusion under section 38-190 (2) is aimed at catching

the net GST related to supply of rights or options offshore where the exercise of rights or

options is associated with Australia. For example, tickets of grand finale to be held in

Australia were sold the New Zealand Company which later sold the tickets to Australian and

New Zealand residents. Since the supply of grand finale is linked to Australia therefore, the

supply of tickets to the company located in New Zealand would not be regarded as GST-free.

17 Millar, R., Moon, L. (2014). Australia. In Michael Lang, Ine Lejeune (Eds.), Improving

VAT/GST: Designing a Simple and Fraud-Proof Tax System, (pp. 23-110). Amsterdam, The

Netherlands: International Bureau of Fiscal Documentation (IBFD).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUSTRALIAN GOODS AND SERVICE TAX

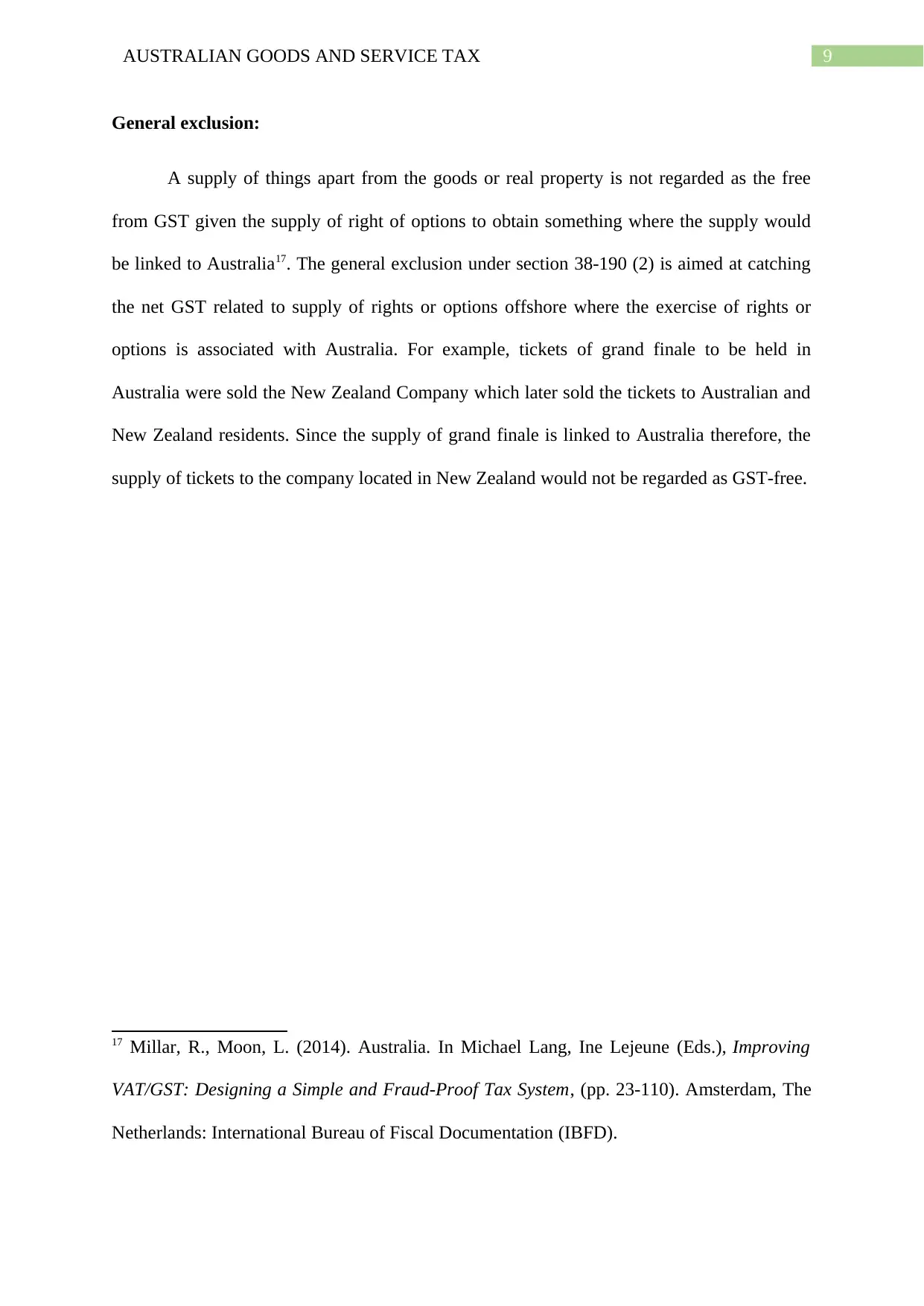

Figure 1: Figure representing Item 2 and 3 and paragraph (b) of item 4

Source: (Austlii.edu.au 2018)

Overview of Item 2 and 3 and paragraph (b) of item 4:

Section 38-190 provides the explanation relating to “supplies of things, other than

goods or real property, for consumption out of Australia”18. The items stated under the

subsection 38-190 lay down the supplies of things, apart from goods and real property for the

consumption that are out of Australian and free from GST given the specific requirements are

18 "Ato.gov.au". Ato.gov.au, 2018. Online. Internet. 26 Nov. 2018. . Available:

https://www.ato.gov.au/misc/downloads/pdf/qc49217.pdf.

Figure 1: Figure representing Item 2 and 3 and paragraph (b) of item 4

Source: (Austlii.edu.au 2018)

Overview of Item 2 and 3 and paragraph (b) of item 4:

Section 38-190 provides the explanation relating to “supplies of things, other than

goods or real property, for consumption out of Australia”18. The items stated under the

subsection 38-190 lay down the supplies of things, apart from goods and real property for the

consumption that are out of Australian and free from GST given the specific requirements are

18 "Ato.gov.au". Ato.gov.au, 2018. Online. Internet. 26 Nov. 2018. . Available:

https://www.ato.gov.au/misc/downloads/pdf/qc49217.pdf.

11AUSTRALIAN GOODS AND SERVICE TAX

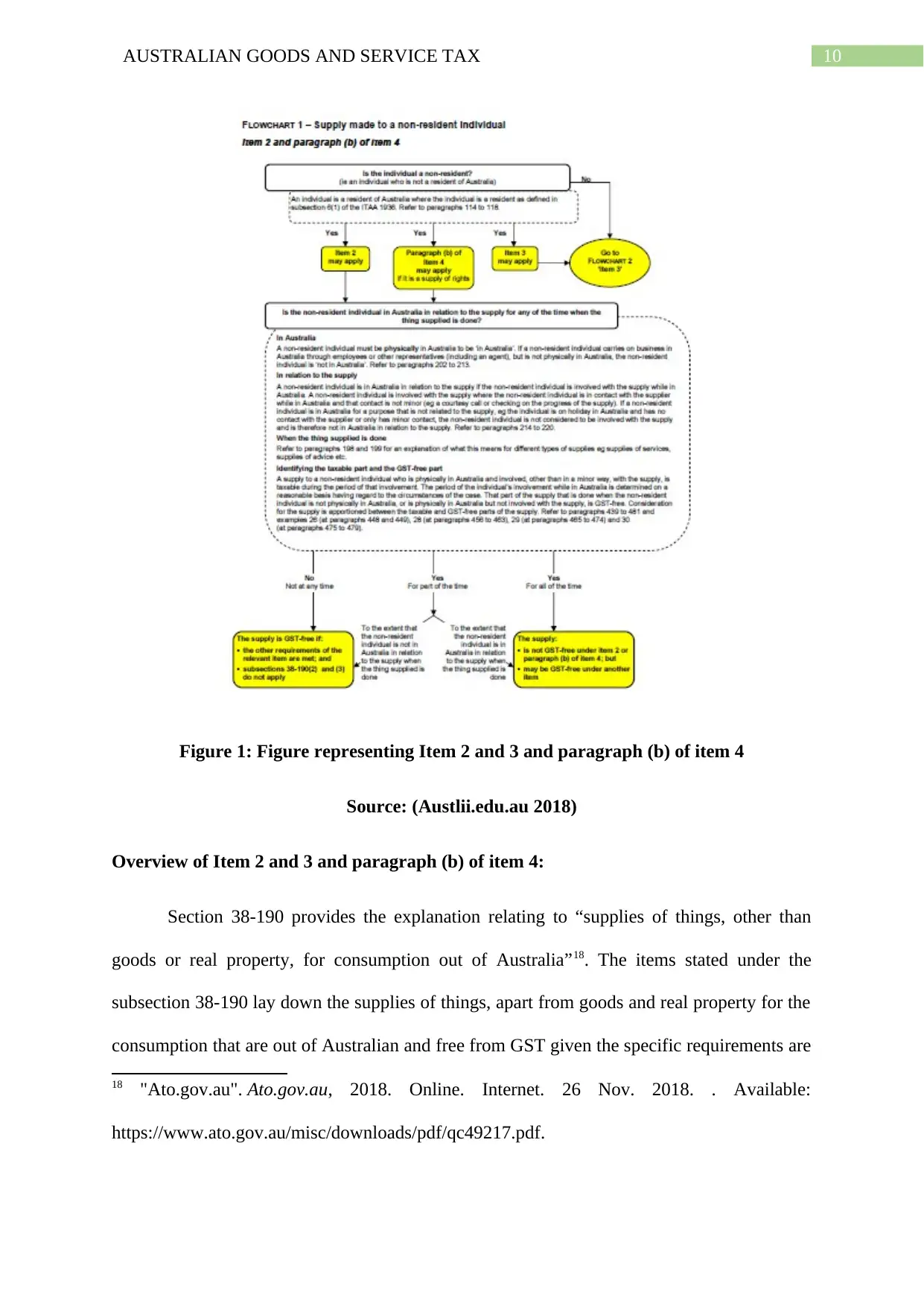

satisfied19. The policy intention as understood by the headings to both the section 38-190 and

the subsection 38-190 (1) by treating the supplies of services or things apart from the goods

or real property as the supplies free from GST given consumption takes place out of

Australia.

Figure 2: Figure representing Item 3 supply made to country together with non-resident

country

19 Millar, R. (2014). Ensuring a consistent and effective VAT treatment of cross-border trade

in B2C Services and intangibles. Second Meeting of the OECD Global Forum on VAT 2014,

Tokyo, Japan: Presentation.

satisfied19. The policy intention as understood by the headings to both the section 38-190 and

the subsection 38-190 (1) by treating the supplies of services or things apart from the goods

or real property as the supplies free from GST given consumption takes place out of

Australia.

Figure 2: Figure representing Item 3 supply made to country together with non-resident

country

19 Millar, R. (2014). Ensuring a consistent and effective VAT treatment of cross-border trade

in B2C Services and intangibles. Second Meeting of the OECD Global Forum on VAT 2014,

Tokyo, Japan: Presentation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 32

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.