Housing Market Dynamics: Renting vs. Buying in Australia Analysis

VerifiedAdded on 2020/02/03

|18

|3391

|44

Report

AI Summary

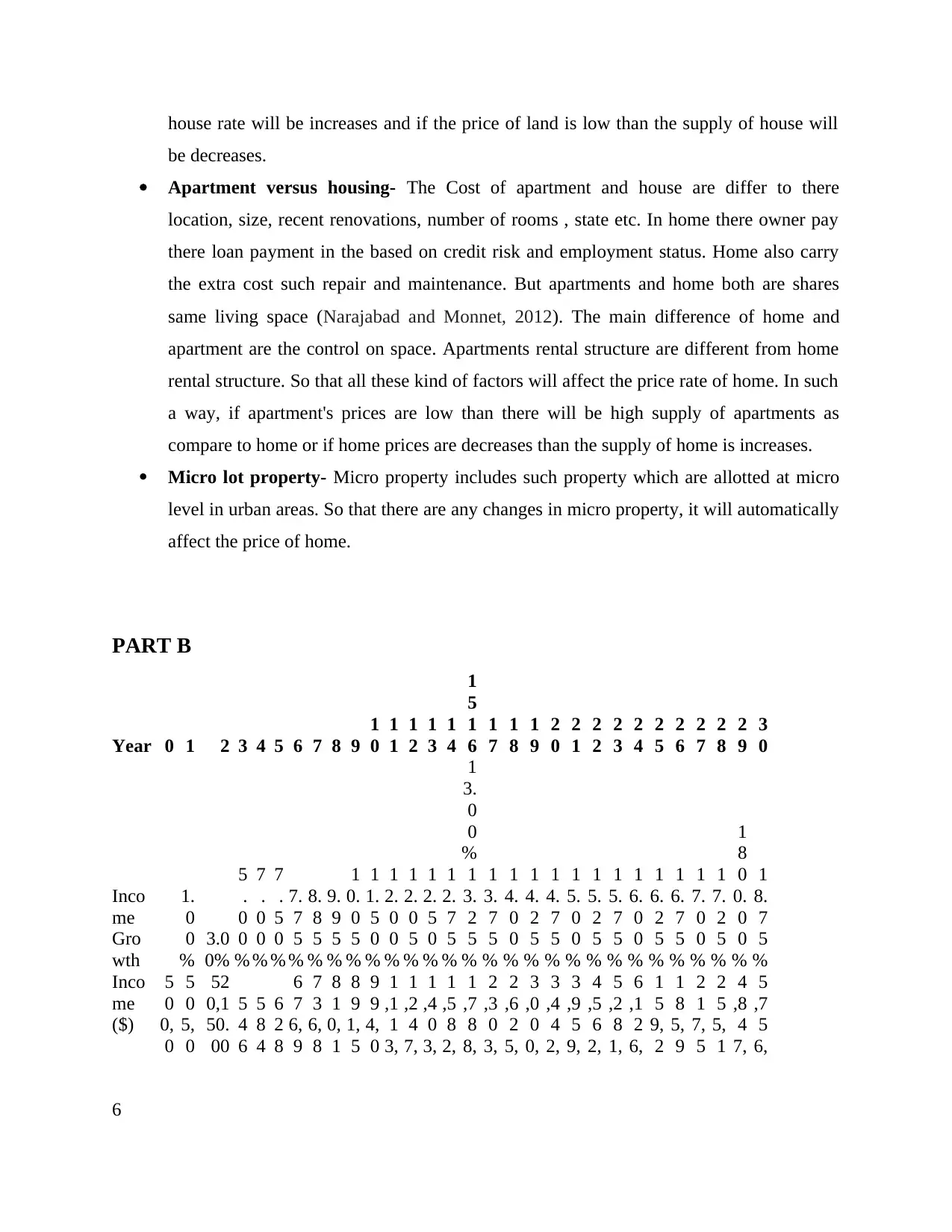

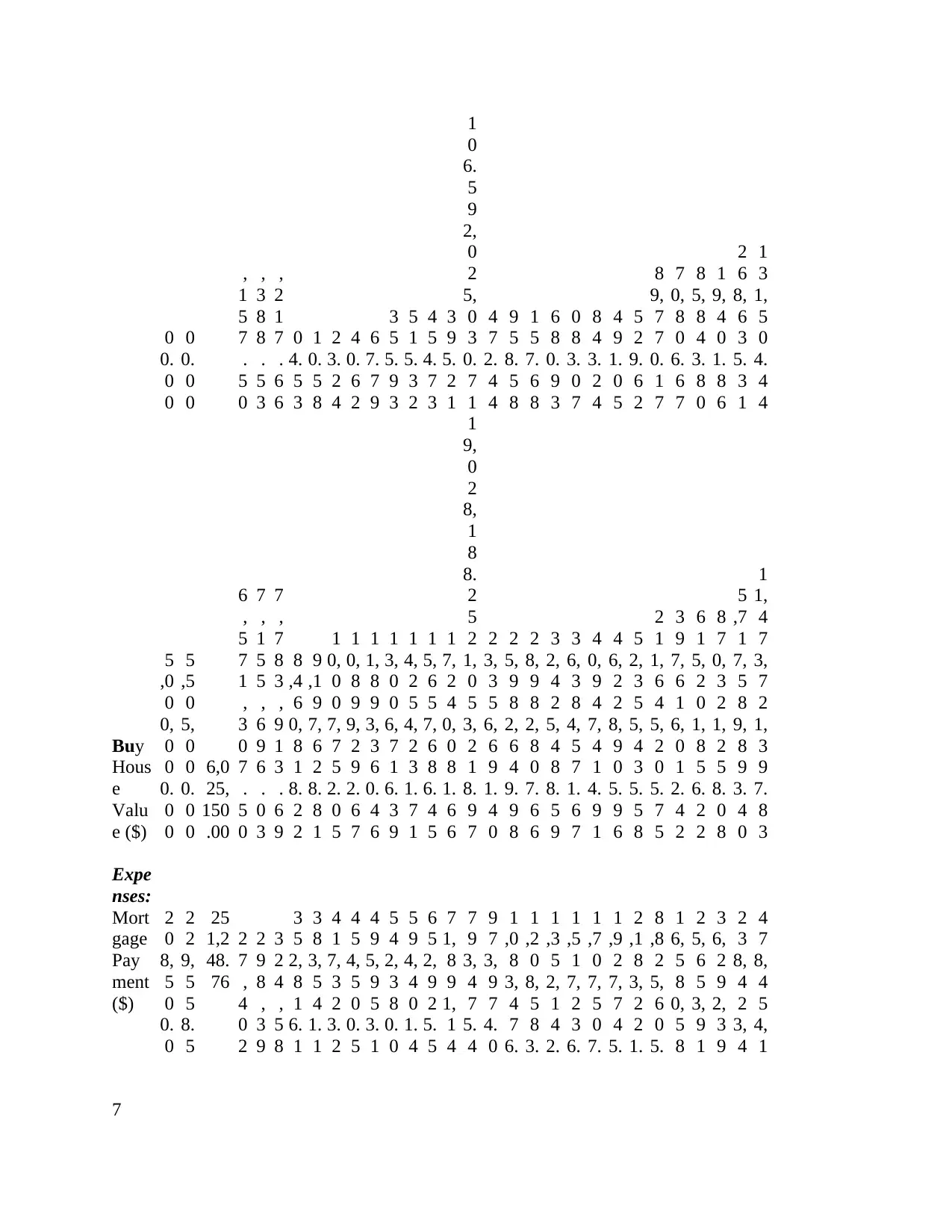

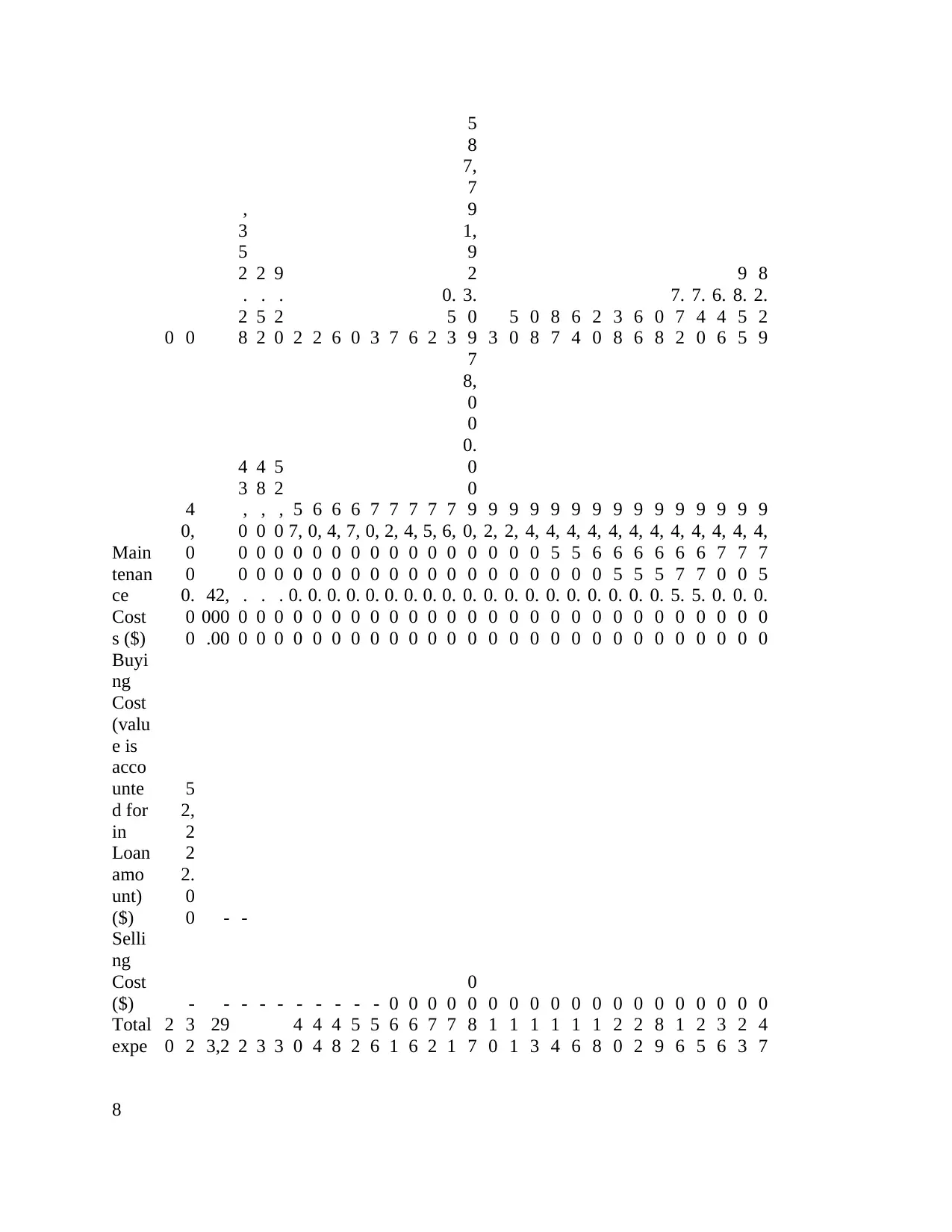

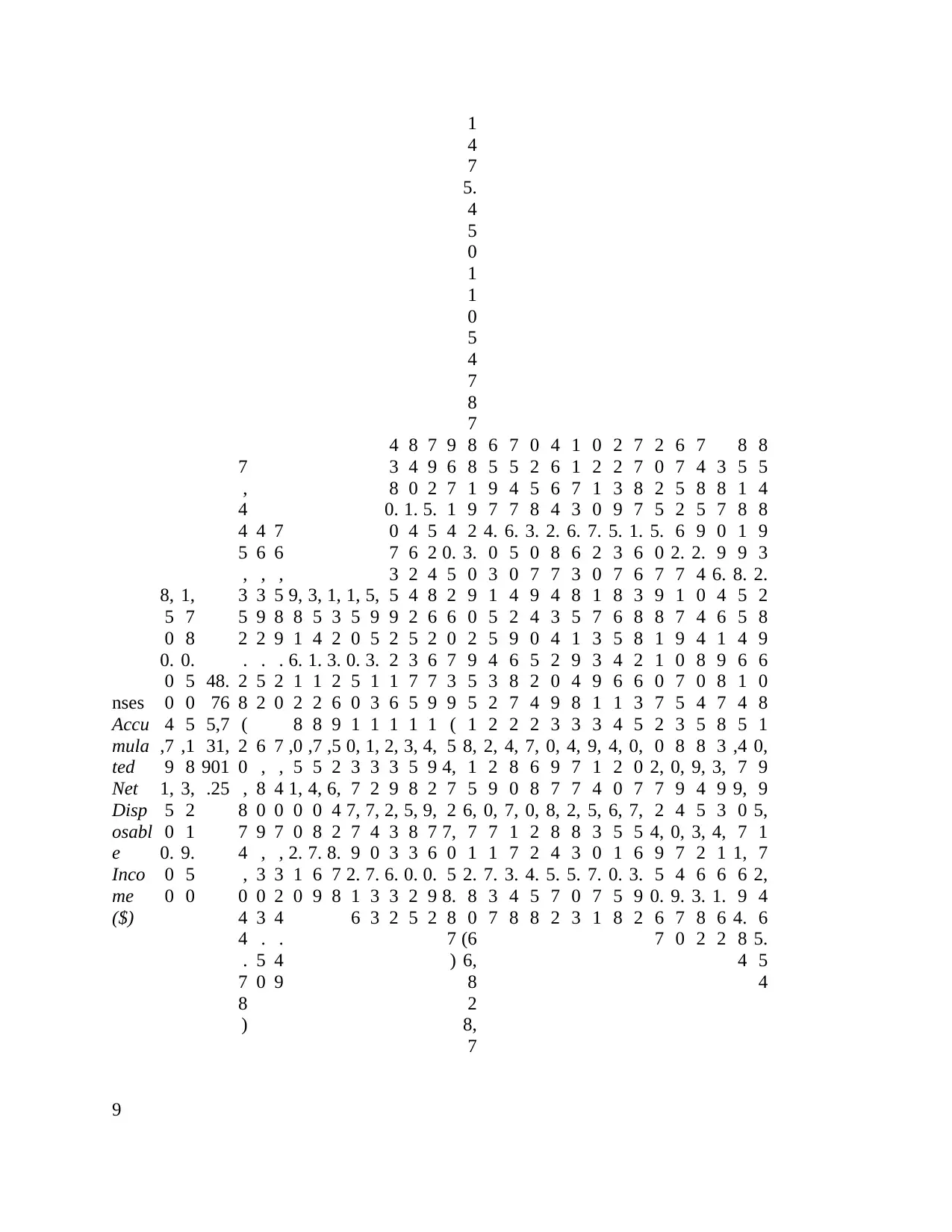

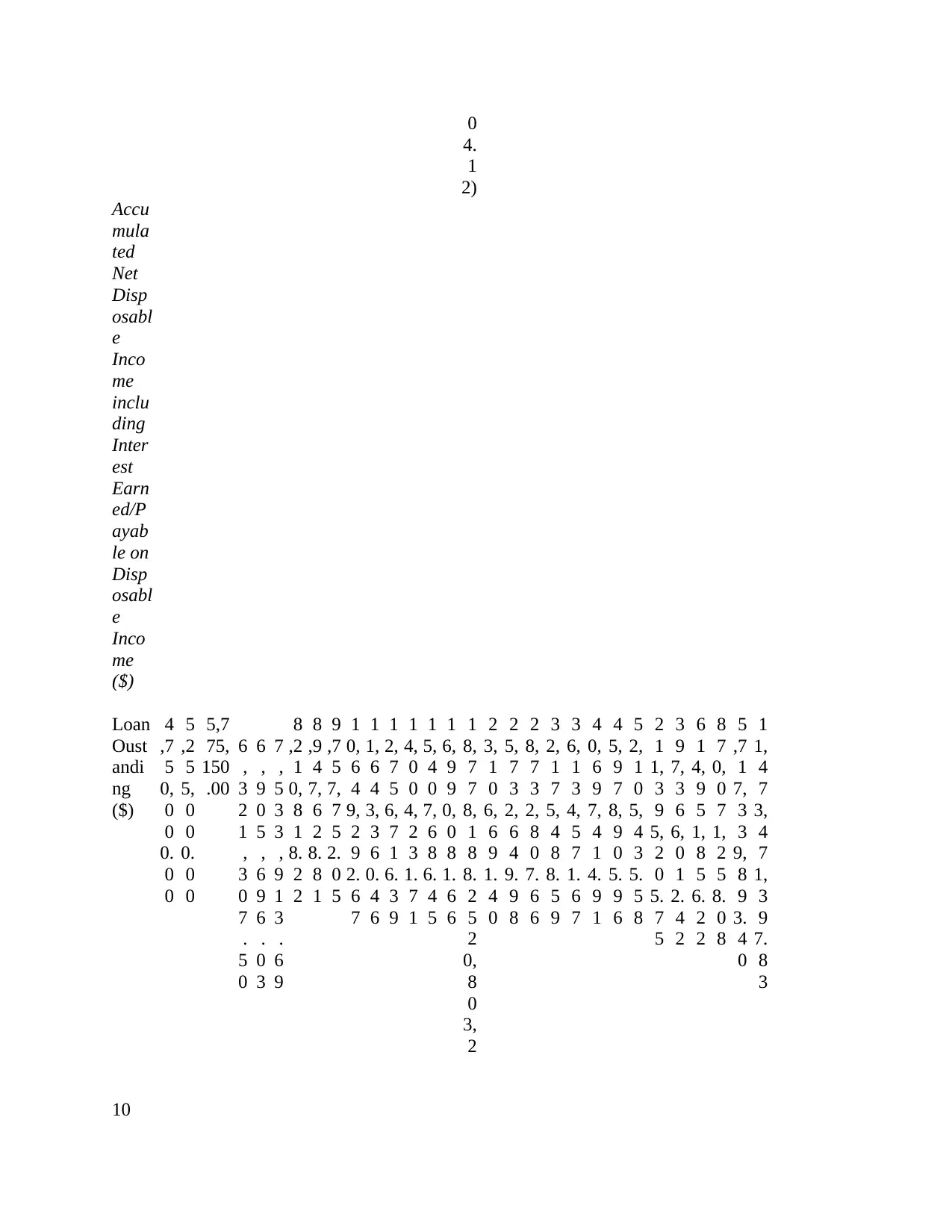

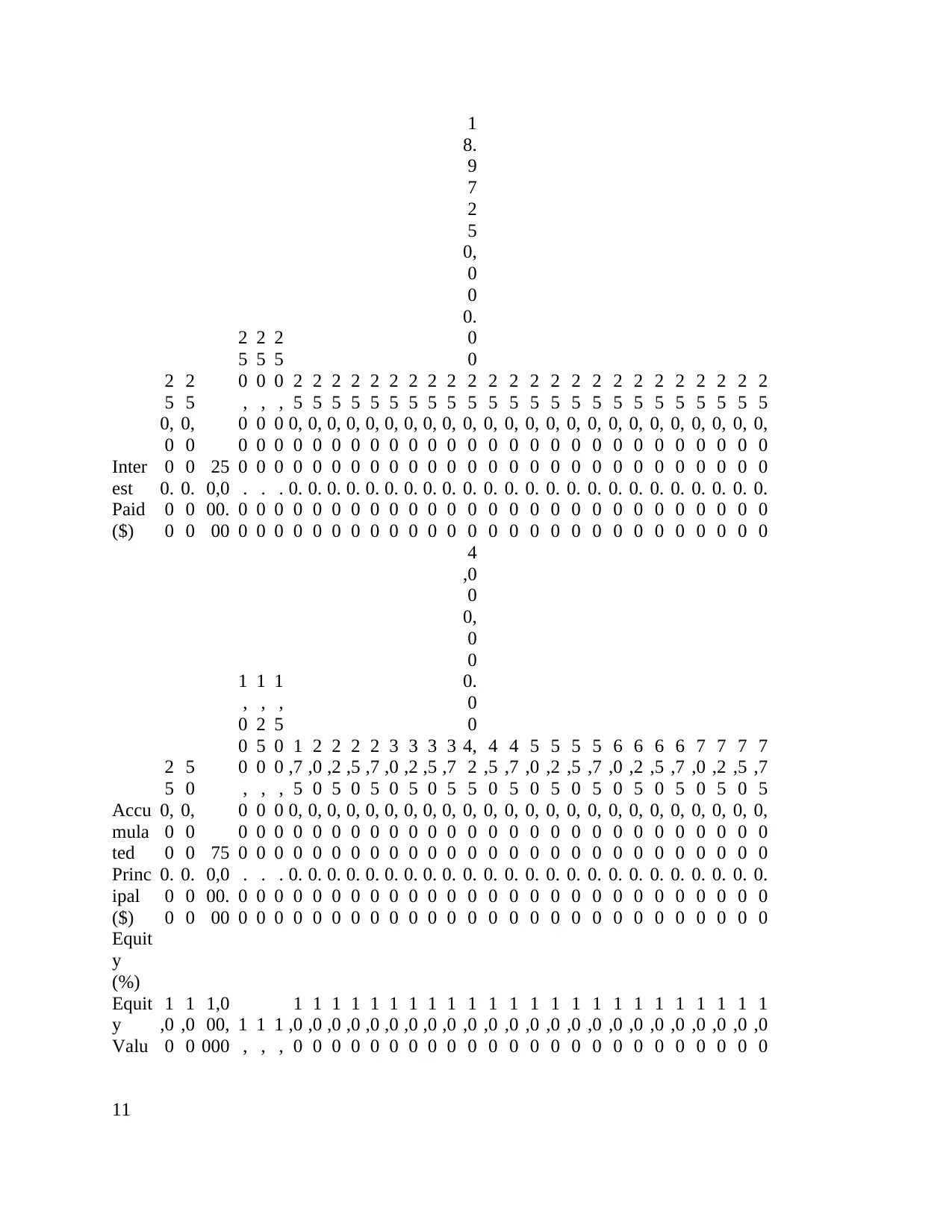

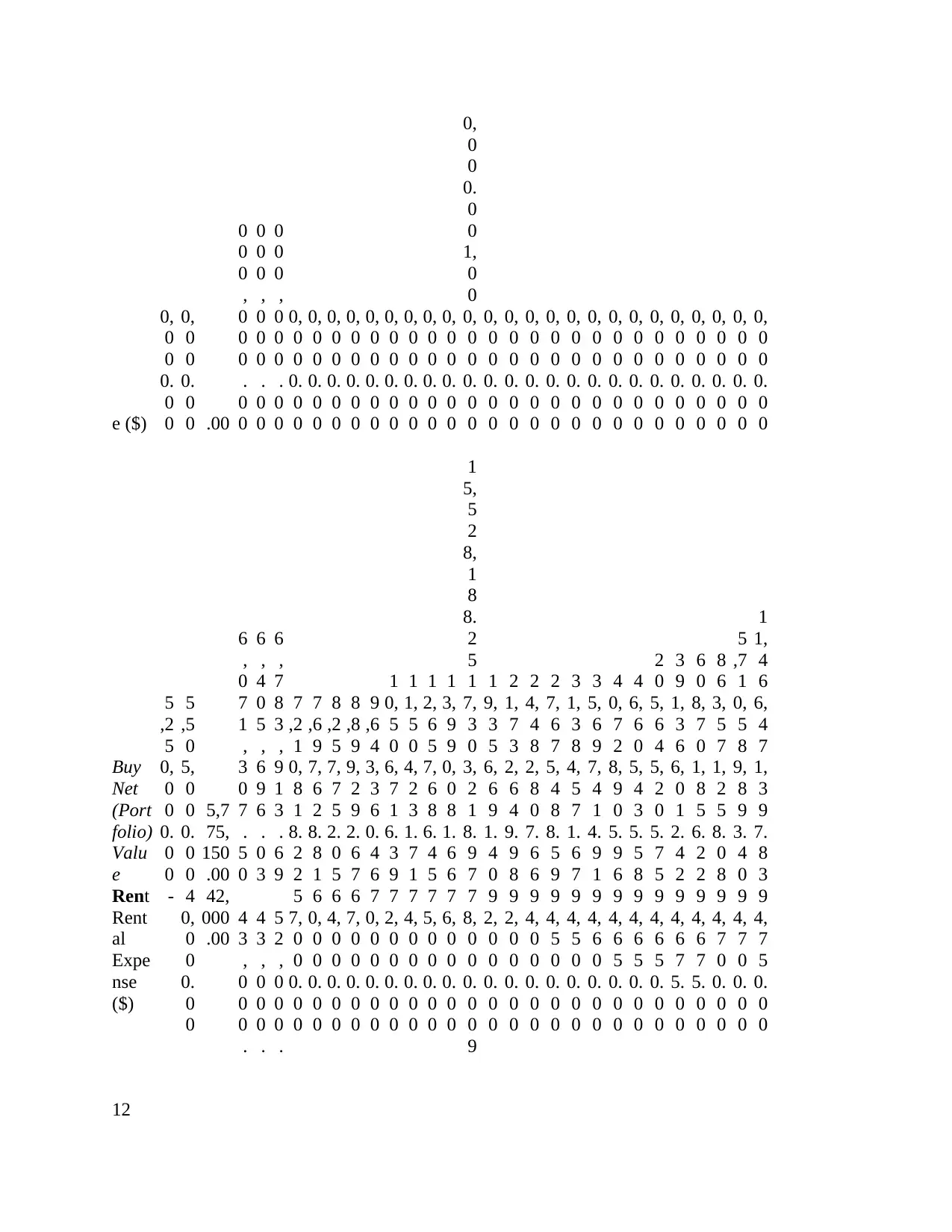

This report delves into the complexities of the Australian housing market, examining the crucial decision of whether to rent or buy a home. It begins with an introduction that highlights the ongoing debate surrounding the valuation of Australian housing, influenced by factors like interest rates and inflation. The report is structured into three parts, with Part A exploring the various demand and supply factors that significantly impact housing prices and rental costs over the next decade. These factors include interest rates, lending conditions, demographics, immigration, government policies, and homeowner grants. Part B presents a detailed financial analysis comparing income growth, house value, expenses, and net disposable income over a 30-year period. The analysis includes tables illustrating the financial implications of buying a house, such as mortgage payments, maintenance costs, and accumulated net disposable income. The report concludes by summarizing the key findings and offering insights into the long-term financial implications of renting versus buying in the Australian context. The report provides a comparative financial analysis, including a table detailing income, expenses, and the value of buying a house over 30 years.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.