Comparative Study of FHOG and FHP Schemes in Australian Housing Market

VerifiedAdded on 2022/09/12

|14

|3571

|14

Report

AI Summary

This report provides a comparative study of the First Home Owners Grant (FHOG) and First Home Plus (FHP) schemes implemented by the Australian government to support first-time homebuyers. It examines the eligibility criteria, similarities, and differences between the two schemes, concluding that FHOG is more beneficial for both buyers and sellers by lowering effective home prices and increasing demand. The report analyzes the impact of FHOG on demand and supply patterns across Australia's states and territories, using price elasticity of demand to explain its influence on the housing market. Furthermore, it discusses the market structure of the property market and suggests alternative policies to alleviate the financial burden on first-time buyers, particularly regarding stamp duty. The analysis includes an assessment of the schemes' effectiveness in promoting a stable property market and uses diagrams to illustrate demand and supply dynamics.

Running head: COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Comparative Study of FHOG and FHP in Australia

Name of the Student

Name of the University

Student ID

Comparative Study of FHOG and FHP in Australia

Name of the Student

Name of the University

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Executive summary

The report made a comparative study of the FHOG and FHP property market schemes of

the government of Australia that supports first home buyers. Both the schemes have similar

objectives but are different in various sector in implementation part. It has been found from the

report that FHOG is more beneficial for both first home buyers and property market sellers.

FHOG lowers the effective price of the homes thus creates the more demand for properties in the

market. Further study revealed that the market operates in a monopoly market structure. The

discussed about how stamp duty creates hurdle for youth home buyers and suggested alternative

policies that would lower the burden of the youth buyers.

Executive summary

The report made a comparative study of the FHOG and FHP property market schemes of

the government of Australia that supports first home buyers. Both the schemes have similar

objectives but are different in various sector in implementation part. It has been found from the

report that FHOG is more beneficial for both first home buyers and property market sellers.

FHOG lowers the effective price of the homes thus creates the more demand for properties in the

market. Further study revealed that the market operates in a monopoly market structure. The

discussed about how stamp duty creates hurdle for youth home buyers and suggested alternative

policies that would lower the burden of the youth buyers.

2COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Table of Contents

Introduction......................................................................................................................................3

Brief on FHOG and FHP.................................................................................................................3

Comparison between FHOG and FHP............................................................................................6

Impact of FHOG..............................................................................................................................7

Market structure of property market in Australia............................................................................8

Unfair pricing in property market....................................................................................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

Brief on FHOG and FHP.................................................................................................................3

Comparison between FHOG and FHP............................................................................................6

Impact of FHOG..............................................................................................................................7

Market structure of property market in Australia............................................................................8

Unfair pricing in property market....................................................................................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Introduction

The report discusses about the two schemes of the government of Australia that provides

discount or grant to the person who buys their first home. The name of the two schemes are First

Home Plus (FHP) and First Home Owners Grant (FHOG). Even though the schemes are for first

home buyers, they are slightly different in their eligibility criteria. Inn case of FHOG, the

foremost criteria to get the grant is that the first home buyers need to buy a new property

(Budgen et al., 2016). Conversely, to get discount under FHP, first home buyers just need buy a

house be it new or existing. The report thus compares both these schemes regarding the first

home buyers. The report takes eligibility criteria of both the schemes to find the similarities and

dissimilarities between the schemes. Along with that, the discussion focuses on the impact of the

two schemes on the demand and supply of the home property market in the sates of the country it

the schemes exists. Further, with the help of price elasticity of demand analysis the discussion in

the report indicates how FHOG influences the home property market of the country. The report

discusses the market structure of the home property market to understand the applications of the

concerned schemes. The critical assessment of the statement of Ken henry regarding the stamp

duties imposed on the purchase of home in the home property market is a part of discussion of

the report. Hence, the objective of the report is to make a comparative study of FHP and FHOG

schemes and discusses the suitability of the schemes to provide a stable property market.

Brief on FHOG and FHP

First Home Owners Grant

Under the scheme of FHOG, the grant is provided only for one time for new residential

property purchase. The amount of the grant provided in this scheme is a lump sum of $ 10, 000.

Introduction

The report discusses about the two schemes of the government of Australia that provides

discount or grant to the person who buys their first home. The name of the two schemes are First

Home Plus (FHP) and First Home Owners Grant (FHOG). Even though the schemes are for first

home buyers, they are slightly different in their eligibility criteria. Inn case of FHOG, the

foremost criteria to get the grant is that the first home buyers need to buy a new property

(Budgen et al., 2016). Conversely, to get discount under FHP, first home buyers just need buy a

house be it new or existing. The report thus compares both these schemes regarding the first

home buyers. The report takes eligibility criteria of both the schemes to find the similarities and

dissimilarities between the schemes. Along with that, the discussion focuses on the impact of the

two schemes on the demand and supply of the home property market in the sates of the country it

the schemes exists. Further, with the help of price elasticity of demand analysis the discussion in

the report indicates how FHOG influences the home property market of the country. The report

discusses the market structure of the home property market to understand the applications of the

concerned schemes. The critical assessment of the statement of Ken henry regarding the stamp

duties imposed on the purchase of home in the home property market is a part of discussion of

the report. Hence, the objective of the report is to make a comparative study of FHP and FHOG

schemes and discusses the suitability of the schemes to provide a stable property market.

Brief on FHOG and FHP

First Home Owners Grant

Under the scheme of FHOG, the grant is provided only for one time for new residential

property purchase. The amount of the grant provided in this scheme is a lump sum of $ 10, 000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

The aim of the grant is to support the first home buyers such that they get enough encouragement

to buy new homes (First Home Owner Grant., 2020). However, there is a twist to the eligibility

criteria of the scheme and that is the purchased home or property must be new one or else no

grant will be provided even if the home purchased is the first for the buyer (Mangioni, 2017). In

addition to that, the grant is provided based on the number of first home purchase but not on the

individuals who purchase homes. It means that if two persons buy a single property then one

grant will be provided for the purchase of the property but not two. The eligibility criteria of

FHOG are as follows:

The first home buyer must be of the age of 18 years or above during the time of

transaction or making application for availing the grant. Though exceptions can be made

if proper reasons are provided.

The first home that is bought should be the primary residential property, it means that the

buyer need to stay there for minimum six month within one year of purchase of the

property.

The grant is provided to the first home buyers who permanently resides in Australia or a

citizen of the country.

To avail the grant a buyer need to apply for it before completion of one year of

transaction made for the purchase.

More eligibility conditions

Various criteria are there that has to be met to get the facilities under the scheme of

FHOG. A buyers who have made the contract of purchase within the first six months of 2017 are

eligible to get the payment boost facilities (Carrington, Li & Larkin, 2019). FHOG considers a

transaction eligible for the grant if the date of contract or purchase of home is done after July 1,

The aim of the grant is to support the first home buyers such that they get enough encouragement

to buy new homes (First Home Owner Grant., 2020). However, there is a twist to the eligibility

criteria of the scheme and that is the purchased home or property must be new one or else no

grant will be provided even if the home purchased is the first for the buyer (Mangioni, 2017). In

addition to that, the grant is provided based on the number of first home purchase but not on the

individuals who purchase homes. It means that if two persons buy a single property then one

grant will be provided for the purchase of the property but not two. The eligibility criteria of

FHOG are as follows:

The first home buyer must be of the age of 18 years or above during the time of

transaction or making application for availing the grant. Though exceptions can be made

if proper reasons are provided.

The first home that is bought should be the primary residential property, it means that the

buyer need to stay there for minimum six month within one year of purchase of the

property.

The grant is provided to the first home buyers who permanently resides in Australia or a

citizen of the country.

To avail the grant a buyer need to apply for it before completion of one year of

transaction made for the purchase.

More eligibility conditions

Various criteria are there that has to be met to get the facilities under the scheme of

FHOG. A buyers who have made the contract of purchase within the first six months of 2017 are

eligible to get the payment boost facilities (Carrington, Li & Larkin, 2019). FHOG considers a

transaction eligible for the grant if the date of contract or purchase of home is done after July 1,

5COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

2000. However, there is a cap to the amount of eligible transactions. The cap for properties

purchased to the south of the 26th parallel is $7, 50, 000 whereas the cap for properties north of

the 26th parallel is $ 10, 00, 000.

First Home Plus

The scheme of First Home Plus is much newer than the scheme of First Home Owners

Grant. The discount under the scheme is based on transfer duty. Unlike FHOG, there is no

requirement criteria that the homes or properties purchased must be new. The only criteria is that

the home purchased is the first home of the buyer (La Cava, Leal & Zurawski, 2017). It does not

matter if the property purchased is new or old. The eligibility criteria in order to avail FHP

scheme are given below:

To avail the scheme the buyer need to be a permanent resident or citizen of Australia.

At the time of purchase of property, the age of the buyer should be atleast 18 years.

If a buyer purchases an en entire property then only he or she is eligible to avail the

scheme benefits.

To avail the scheme a home or property should be bought individually.

More eligibility conditions

Any property that has been purchased after October 21, 2009 are eligible under the

scheme of FHP. However, a buyer who has served or working in Australian Defense force do not

need to abide the eligibility criteria (First Home Plus., 2020). A buyer who wants to avail FHP

would not get it if he or she owns or co-owns any other property in the country and have availed

the benefit of the scheme earlier. To become eligible for the scheme a buyer should move to the

new home after the completion of purchase of the new home within one year (Thompson, et al.,

2000. However, there is a cap to the amount of eligible transactions. The cap for properties

purchased to the south of the 26th parallel is $7, 50, 000 whereas the cap for properties north of

the 26th parallel is $ 10, 00, 000.

First Home Plus

The scheme of First Home Plus is much newer than the scheme of First Home Owners

Grant. The discount under the scheme is based on transfer duty. Unlike FHOG, there is no

requirement criteria that the homes or properties purchased must be new. The only criteria is that

the home purchased is the first home of the buyer (La Cava, Leal & Zurawski, 2017). It does not

matter if the property purchased is new or old. The eligibility criteria in order to avail FHP

scheme are given below:

To avail the scheme the buyer need to be a permanent resident or citizen of Australia.

At the time of purchase of property, the age of the buyer should be atleast 18 years.

If a buyer purchases an en entire property then only he or she is eligible to avail the

scheme benefits.

To avail the scheme a home or property should be bought individually.

More eligibility conditions

Any property that has been purchased after October 21, 2009 are eligible under the

scheme of FHP. However, a buyer who has served or working in Australian Defense force do not

need to abide the eligibility criteria (First Home Plus., 2020). A buyer who wants to avail FHP

would not get it if he or she owns or co-owns any other property in the country and have availed

the benefit of the scheme earlier. To become eligible for the scheme a buyer should move to the

new home after the completion of purchase of the new home within one year (Thompson, et al.,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

2018). The concession is given based on the transfer duty and this duty is determined based on

the value of the property.

Comparison between FHOG and FHP

The government of Australia came up with the schemes of FHOG and FHP to support

and encourage the first home buyers. The objective of both the schemes are similar but there are

various differences in their eligibility criteria. The only two criteria that are similar for both the

schemes are the criteria of age and citizenship or residential status. Other criteria however are

different. In case of FHOG, there is no such criteria of purchasing the whole property like FHP.

The kind of benefit provided by both the schemes are different from each other (Crowley & Li,

2016). In FHP, the amount of transfer duty is paid whereas in FHOG lump sum up to $10, 000 is

paid. However, benefit under both the schemes are subject to the value of the property

purchased. Another difference is that in FHOG the property bought must be new, which is not

the case with FHP. From the detailed study of the eligibility criteria of both the schemes, it can

be said that FHP is more welfare centric than FHOG. In case of FHP, any first home buyer who

buys his or her first home will get the monetary benefit under the scheme (Pawson, 2019). On

the other hand, under FHOG only the first home buyers purchasing the new properties are gets

the benefit. Hence, it can be said that FHP encourages more person to buy first home whereas

FHOG encourages first home buyers to purchase new homes. Additionally, benefit under FHOG

is clearer than FHP as it states the amount of benefit in prior (Chirstensen, 2017). Therefore,

from business perspective, FHOG is better than FHP in boosting the property market of the

country since to avail FHOG, first home buyers will purchase new homes and thus causes

building of new properties (Raynor, Dosen & Otter, 2017). Therefore, if economic perspective is

considered then FHOG is more suitable scheme.

2018). The concession is given based on the transfer duty and this duty is determined based on

the value of the property.

Comparison between FHOG and FHP

The government of Australia came up with the schemes of FHOG and FHP to support

and encourage the first home buyers. The objective of both the schemes are similar but there are

various differences in their eligibility criteria. The only two criteria that are similar for both the

schemes are the criteria of age and citizenship or residential status. Other criteria however are

different. In case of FHOG, there is no such criteria of purchasing the whole property like FHP.

The kind of benefit provided by both the schemes are different from each other (Crowley & Li,

2016). In FHP, the amount of transfer duty is paid whereas in FHOG lump sum up to $10, 000 is

paid. However, benefit under both the schemes are subject to the value of the property

purchased. Another difference is that in FHOG the property bought must be new, which is not

the case with FHP. From the detailed study of the eligibility criteria of both the schemes, it can

be said that FHP is more welfare centric than FHOG. In case of FHP, any first home buyer who

buys his or her first home will get the monetary benefit under the scheme (Pawson, 2019). On

the other hand, under FHOG only the first home buyers purchasing the new properties are gets

the benefit. Hence, it can be said that FHP encourages more person to buy first home whereas

FHOG encourages first home buyers to purchase new homes. Additionally, benefit under FHOG

is clearer than FHP as it states the amount of benefit in prior (Chirstensen, 2017). Therefore,

from business perspective, FHOG is better than FHP in boosting the property market of the

country since to avail FHOG, first home buyers will purchase new homes and thus causes

building of new properties (Raynor, Dosen & Otter, 2017). Therefore, if economic perspective is

considered then FHOG is more suitable scheme.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Impact of FHOG

The first government scheme in Australia to provide financial support to the first home

buyers is known as the First Home Owners Grant. Under this scheme, the first home buyers are

provided with monetary benefit. The major aim of introducing he scheme is to encourage and

first home buyers to purchase new homes. The scheme has been quite successful in its objective.

Owing to this, the property market in Australia faced rise in demand. As a result, sudden increase

in demand for new homes in the property market the price of properties increased significantly in

the six states and Northern Territory of Australia. It has been found that the grant benefit

provided to the first home buyers in different state is different. Due to this difference in grant,

demand for new homes in different states is different (REIQ, 2016). Actually, the grant decides

the effective price of new homes because the price that the first home buyers required to pay for

new homes are determined by subtraction the amount of grant from the actual market price. The

demand and supply of any product is highly dependent on the price of the product. In the case of

property market, there is no exception (Redden, Phelan & Baker, 2020). The amount of grant

given in South Australia and NSW is $15,000. In Queensland, the amount of grant is higher and

the first home buyers in this state get s benefit of $ 20, 000. In the other states, Victoria, Northern

Territory and Western Australia the amount of the grant is $10,000 (First Home Owner Grant.,

2020). However, the capital territory of Australia has the lowest grant of amount $7, 000.

Therefore, it can be said that the states with highest grant has the lowest effective price for new

homes and thus demand for new homes would be maximum in the sates with lowest effective

price.

It is know from the theory of microeconomics that the price elasticity of demand is

greater than 1 in case of luxury goods (de Rassenfosse, 2020). Here, homes and property are

Impact of FHOG

The first government scheme in Australia to provide financial support to the first home

buyers is known as the First Home Owners Grant. Under this scheme, the first home buyers are

provided with monetary benefit. The major aim of introducing he scheme is to encourage and

first home buyers to purchase new homes. The scheme has been quite successful in its objective.

Owing to this, the property market in Australia faced rise in demand. As a result, sudden increase

in demand for new homes in the property market the price of properties increased significantly in

the six states and Northern Territory of Australia. It has been found that the grant benefit

provided to the first home buyers in different state is different. Due to this difference in grant,

demand for new homes in different states is different (REIQ, 2016). Actually, the grant decides

the effective price of new homes because the price that the first home buyers required to pay for

new homes are determined by subtraction the amount of grant from the actual market price. The

demand and supply of any product is highly dependent on the price of the product. In the case of

property market, there is no exception (Redden, Phelan & Baker, 2020). The amount of grant

given in South Australia and NSW is $15,000. In Queensland, the amount of grant is higher and

the first home buyers in this state get s benefit of $ 20, 000. In the other states, Victoria, Northern

Territory and Western Australia the amount of the grant is $10,000 (First Home Owner Grant.,

2020). However, the capital territory of Australia has the lowest grant of amount $7, 000.

Therefore, it can be said that the states with highest grant has the lowest effective price for new

homes and thus demand for new homes would be maximum in the sates with lowest effective

price.

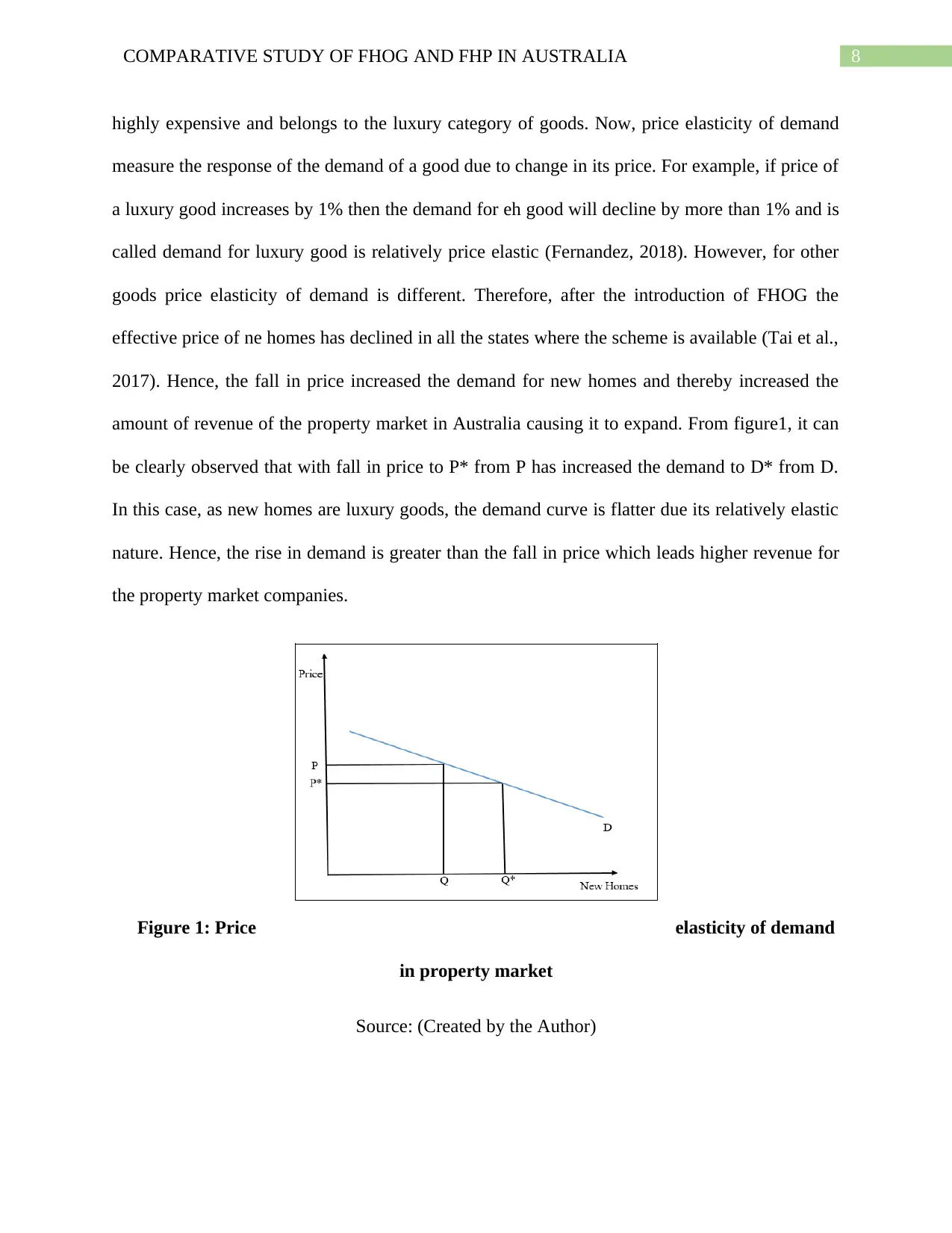

It is know from the theory of microeconomics that the price elasticity of demand is

greater than 1 in case of luxury goods (de Rassenfosse, 2020). Here, homes and property are

8COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

highly expensive and belongs to the luxury category of goods. Now, price elasticity of demand

measure the response of the demand of a good due to change in its price. For example, if price of

a luxury good increases by 1% then the demand for eh good will decline by more than 1% and is

called demand for luxury good is relatively price elastic (Fernandez, 2018). However, for other

goods price elasticity of demand is different. Therefore, after the introduction of FHOG the

effective price of ne homes has declined in all the states where the scheme is available (Tai et al.,

2017). Hence, the fall in price increased the demand for new homes and thereby increased the

amount of revenue of the property market in Australia causing it to expand. From figure1, it can

be clearly observed that with fall in price to P* from P has increased the demand to D* from D.

In this case, as new homes are luxury goods, the demand curve is flatter due its relatively elastic

nature. Hence, the rise in demand is greater than the fall in price which leads higher revenue for

the property market companies.

Figure 1: Price elasticity of demand

in property market

Source: (Created by the Author)

highly expensive and belongs to the luxury category of goods. Now, price elasticity of demand

measure the response of the demand of a good due to change in its price. For example, if price of

a luxury good increases by 1% then the demand for eh good will decline by more than 1% and is

called demand for luxury good is relatively price elastic (Fernandez, 2018). However, for other

goods price elasticity of demand is different. Therefore, after the introduction of FHOG the

effective price of ne homes has declined in all the states where the scheme is available (Tai et al.,

2017). Hence, the fall in price increased the demand for new homes and thereby increased the

amount of revenue of the property market in Australia causing it to expand. From figure1, it can

be clearly observed that with fall in price to P* from P has increased the demand to D* from D.

In this case, as new homes are luxury goods, the demand curve is flatter due its relatively elastic

nature. Hence, the rise in demand is greater than the fall in price which leads higher revenue for

the property market companies.

Figure 1: Price elasticity of demand

in property market

Source: (Created by the Author)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Market structure of property market in Australia

The property market in Australia is dominated by more than one company. Hence, the

amount fixed investment required and number of companies in the market it can be said the

property market in Australia is of oligopoly structure. The product in oligopoly market is

homogenous in nature but in case of property market, each and every product is different from

each other and thus make them heterogonous. Every product is unique due to its different design,

location and accessibility to hospitals, market, office and educational institutes. In addition to

that, climate of different states are different. Uniqueness of each product cannot be replicated. It

should be further noted that a company or real estate developer builds numerous homes over a

large area of land and thus in those specific area only that company is the only one that sells

properties (Baur, 2019). Even though there are many real estate companies operating in the

property market in Australia, each of them enjoys market power over specific region. There exist

high barriers to entry and exit. Hence, property owners can charge high price to earn super

normal profit (Geltner, Kumar & Van de Minne, 2019). However, due to government regulation

there is no such monopoly practice in the market. Therefore, from above discussion it can be said

that the property market in Australia is of monopoly structure.

Unfair pricing in property market

The argument of Ken Henry that stamp duty creates hurdle for youth new home buyers is

strong and convincing. This is because the imposition of stamp duty would increase the effective

price of homes and thus make then less affordable for youths as they have just started their career

and thus they have limited budget. Moreover, stamp duty has to be paid upfront and in full which

is difficult for youth buyers since gathering lump sum is a tough job for them. Hence, it can be

said that stamp duty does creates a hurdle for youths to buy new homes (Scanlon, Whitehead &

Market structure of property market in Australia

The property market in Australia is dominated by more than one company. Hence, the

amount fixed investment required and number of companies in the market it can be said the

property market in Australia is of oligopoly structure. The product in oligopoly market is

homogenous in nature but in case of property market, each and every product is different from

each other and thus make them heterogonous. Every product is unique due to its different design,

location and accessibility to hospitals, market, office and educational institutes. In addition to

that, climate of different states are different. Uniqueness of each product cannot be replicated. It

should be further noted that a company or real estate developer builds numerous homes over a

large area of land and thus in those specific area only that company is the only one that sells

properties (Baur, 2019). Even though there are many real estate companies operating in the

property market in Australia, each of them enjoys market power over specific region. There exist

high barriers to entry and exit. Hence, property owners can charge high price to earn super

normal profit (Geltner, Kumar & Van de Minne, 2019). However, due to government regulation

there is no such monopoly practice in the market. Therefore, from above discussion it can be said

that the property market in Australia is of monopoly structure.

Unfair pricing in property market

The argument of Ken Henry that stamp duty creates hurdle for youth new home buyers is

strong and convincing. This is because the imposition of stamp duty would increase the effective

price of homes and thus make then less affordable for youths as they have just started their career

and thus they have limited budget. Moreover, stamp duty has to be paid upfront and in full which

is difficult for youth buyers since gathering lump sum is a tough job for them. Hence, it can be

said that stamp duty does creates a hurdle for youths to buy new homes (Scanlon, Whitehead &

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Blanc, 2017). Further, stamp duties have adverse effect on the property market as it lowers the

demand since it increases the effective price. Therefore, instead of stamp duty the government

should charge tax that can be paid in quarterly or yearly installments. However, the tax should be

for limited period and not for permanent since it is replacement for stamp duty. Hence, this will

ease the burden of the youth buyers and help them to buy new homes.

Conclusion

It can be inferred from the above discussion reading FHOG and FHP that objective of

both the schemes are same, which is to support the first home buyers. However, both the

schemes have their uniqueness. FHOG is for those first home buyers who purchases new homes

and FHP is for all the first home buyers. The type benefit provided in both the schemes are

different too. In contrary, it has been observed that the FHOG scheme is more effective in

expanding the property market in Australia since it encourages first home buyers to buy new

homes. Hence, it seems that FHOG is a better policy for both property sellers and property

buyers. The rise in demand new homes increases as FHOG successfully decreases the effective

price of the properties or homes. Further, study of the property market helped to find that it is of

monopoly market structure. It has also been found that stamp duty is acting like a hurdle for

youth first home buyers which shall be replaced with other revenue collecting polices that

removes the hurdle for the youths.

Blanc, 2017). Further, stamp duties have adverse effect on the property market as it lowers the

demand since it increases the effective price. Therefore, instead of stamp duty the government

should charge tax that can be paid in quarterly or yearly installments. However, the tax should be

for limited period and not for permanent since it is replacement for stamp duty. Hence, this will

ease the burden of the youth buyers and help them to buy new homes.

Conclusion

It can be inferred from the above discussion reading FHOG and FHP that objective of

both the schemes are same, which is to support the first home buyers. However, both the

schemes have their uniqueness. FHOG is for those first home buyers who purchases new homes

and FHP is for all the first home buyers. The type benefit provided in both the schemes are

different too. In contrary, it has been observed that the FHOG scheme is more effective in

expanding the property market in Australia since it encourages first home buyers to buy new

homes. Hence, it seems that FHOG is a better policy for both property sellers and property

buyers. The rise in demand new homes increases as FHOG successfully decreases the effective

price of the properties or homes. Further, study of the property market helped to find that it is of

monopoly market structure. It has also been found that stamp duty is acting like a hurdle for

youth first home buyers which shall be replaced with other revenue collecting polices that

removes the hurdle for the youths.

11COMPARATIVE STUDY OF FHOG AND FHP IN AUSTRALIA

Reference

Baur, D. G. (2019). Monopoly in Real Life-The Housing Market, Finance and

Inequality. Finance and Inequality (January 28, 2019).

Bugden, J., Waschik, R., Fraser, I., & Racine, J. S. (2016). Parametric and non-parametric

analysis of tax changes. Global Business and Economics Review, 18(5), 533-549.

Carrington, S. J., Li, B., & Larkin, M. P. (2019). The Role of Tax and Subsidy Policy in Driving

Australian House Prices. Economic record, 95(309), 227-247.

Christensen, S. A. (2017). Tax update for property buyers. Australian Property Law

Bulletin, 32(4), 63-65.

Crowley, D., & Li, S. M. (2016). An NPV analysis of buying versus renting for prospective

Australian first home buyers. Economic Record, 92(299), 606-630.

de Rassenfosse, G. (2020). On the price elasticity of demand for trademarks. Industry and

Innovation, 27(1-2), 11-24.

Fernandez, V. (2018). Price and income elasticity of demand for mineral

commodities. Resources Policy, 59, 160-183.

First Home Owner Grant. (2020). Firsthome.gov.au. Retrieved 6 March 2020, from

http://www.firsthome.gov.au/

First Home Owner Grant. (2020). Revenue NSW. Retrieved from

https://www.revenue.nsw.gov.au/grants-schemes/previous-schemes/first-home-owner-

grant

Reference

Baur, D. G. (2019). Monopoly in Real Life-The Housing Market, Finance and

Inequality. Finance and Inequality (January 28, 2019).

Bugden, J., Waschik, R., Fraser, I., & Racine, J. S. (2016). Parametric and non-parametric

analysis of tax changes. Global Business and Economics Review, 18(5), 533-549.

Carrington, S. J., Li, B., & Larkin, M. P. (2019). The Role of Tax and Subsidy Policy in Driving

Australian House Prices. Economic record, 95(309), 227-247.

Christensen, S. A. (2017). Tax update for property buyers. Australian Property Law

Bulletin, 32(4), 63-65.

Crowley, D., & Li, S. M. (2016). An NPV analysis of buying versus renting for prospective

Australian first home buyers. Economic Record, 92(299), 606-630.

de Rassenfosse, G. (2020). On the price elasticity of demand for trademarks. Industry and

Innovation, 27(1-2), 11-24.

Fernandez, V. (2018). Price and income elasticity of demand for mineral

commodities. Resources Policy, 59, 160-183.

First Home Owner Grant. (2020). Firsthome.gov.au. Retrieved 6 March 2020, from

http://www.firsthome.gov.au/

First Home Owner Grant. (2020). Revenue NSW. Retrieved from

https://www.revenue.nsw.gov.au/grants-schemes/previous-schemes/first-home-owner-

grant

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.