Holmes Institute HI6028: Australian Income Tax System Report

VerifiedAdded on 2022/11/17

|13

|2855

|485

Report

AI Summary

This report provides a comprehensive analysis of the Australian income tax system, focusing on income tax, capital gains tax (CGT), and Goods and Services Tax (GST). It examines the Australian taxation system, including self-assessment, withholding taxes, and anti-avoidance provisions. The report delves into relevant legislation and case laws, illustrating the application of taxation principles to real-life scenarios. It explores various forms of deductions, international transactions, and the roles of ATO. The report also includes detailed case studies and the application of taxation principles such as equity, neutrality, efficiency, certainty, and simplicity.

AUSTRALIAN INCOME TAXATION 1

Australian Income Tax System

Institution

Date

Australian Income Tax System

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUSTRALIAN INCOME TAXATION 2

EXECUTIVE SUMMARY

The objective of this report is to enable the learner understand and demonstrate the Australian

income tax system, anti-avoidance provisions and rules applied in Australia. It also aims at

equipping the learners with knowledge and understanding on forms of deductions on income tax

globally and within Australia and provisions on international transactions pertaining Australian

residents and nonresident taxpayers.

The detailed case study on capital gains and Goods and Consumption Taxes is a good example

on how ATO (Australian Tax Office) can approach issues related to capital gains and goods and

services duties. In addition, the report analyzes various legislation laws and fundamental values a

tax system should demonstrate.

EXECUTIVE SUMMARY

The objective of this report is to enable the learner understand and demonstrate the Australian

income tax system, anti-avoidance provisions and rules applied in Australia. It also aims at

equipping the learners with knowledge and understanding on forms of deductions on income tax

globally and within Australia and provisions on international transactions pertaining Australian

residents and nonresident taxpayers.

The detailed case study on capital gains and Goods and Consumption Taxes is a good example

on how ATO (Australian Tax Office) can approach issues related to capital gains and goods and

services duties. In addition, the report analyzes various legislation laws and fundamental values a

tax system should demonstrate.

AUSTRALIAN INCOME TAXATION 3

TABLE OF CONTENT

Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

INCOME TAX................................................................................................................................4

CAPITAL GAIN TAXES (CGT)................................................................................................4

Non Resident individual...........................................................................................................5

GOODS AND SERVICES TAX (GST)......................................................................................5

FRINGE BENEFIT TAX.............................................................................................................5

AUSTRALIA TAXATION SYSTEM............................................................................................6

Self assessment taxation system...............................................................................................6

Withholding taxes.....................................................................................................................6

GST anti - avoidance provisions..............................................................................................6

TAXATION LEGISLATION AND CASE LAWS........................................................................7

PRINCIPLES OF TAXATION.......................................................................................................9

REFERENCES..............................................................................................................................10

TABLE OF CONTENT

Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

INCOME TAX................................................................................................................................4

CAPITAL GAIN TAXES (CGT)................................................................................................4

Non Resident individual...........................................................................................................5

GOODS AND SERVICES TAX (GST)......................................................................................5

FRINGE BENEFIT TAX.............................................................................................................5

AUSTRALIA TAXATION SYSTEM............................................................................................6

Self assessment taxation system...............................................................................................6

Withholding taxes.....................................................................................................................6

GST anti - avoidance provisions..............................................................................................6

TAXATION LEGISLATION AND CASE LAWS........................................................................7

PRINCIPLES OF TAXATION.......................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUSTRALIAN INCOME TAXATION 4

INTRODUCTION

Income tax from Australian residents and non-residents whose income originate from Australia

is imposed by the federal government. For tax purposes, the Australian laws have regulations on

how to determine whether an individual or a company is a resident. It also determines the source

of income whether its Australia or Diaspora. In most cases, tax is imposed from the place or

location of work. The only problem with source and residence rules is that a given income may

be taxed in both countries. To prevent this, Australian government signed double tax consent

with many countries with the aim of ensuring any amount of income is taxed once. Additionally,

it provides foreign tax credits to Australian residents paying foreign taxes on their foreign

income.

INCOME TAX

This is the company’s computable earnings without acceptable deductions. Dividends, salaries,

rent, wages, interest and income from business are some of the taxable income (Evans, 2019,

pg.217). Deductions as well are expenses and costs incurred in gaining income. Deductions on

capital and personal expenses however are not deductible unless certain conditions are reached

(Anesa et al.2019, pg.79).

CAPITAL GAIN TAXES (CGT)

CGT is charged on income earned from sale of a property. Real and intangible assets are subject

to Capital Gain Tax. Assets like motor vehicles, one’s residence and assets meant for personal

use have exemptions. Real property asset among other assets are subject to capital gain for

foreign residents. For assets held more than a year, an Australian resident is allowed a 50%

discount for the purpose of taxation. With the amendment of capital gain tax rule, a non-resident

is not allowed to have the 50 percent discount and instead, loss on capital can only be

compensated by capital earnings.

As per the rules outlined above, one is legally responsible to pay tax on capital gains and

earnings or income and. Australian nonresidents and resident individuals are liable to income tax

and Capital Gain Tax (CGT). When imposing duty to individuals, progressive levy scale system

is used. This means the tax rate is proportional with an increase in taxable income.

INTRODUCTION

Income tax from Australian residents and non-residents whose income originate from Australia

is imposed by the federal government. For tax purposes, the Australian laws have regulations on

how to determine whether an individual or a company is a resident. It also determines the source

of income whether its Australia or Diaspora. In most cases, tax is imposed from the place or

location of work. The only problem with source and residence rules is that a given income may

be taxed in both countries. To prevent this, Australian government signed double tax consent

with many countries with the aim of ensuring any amount of income is taxed once. Additionally,

it provides foreign tax credits to Australian residents paying foreign taxes on their foreign

income.

INCOME TAX

This is the company’s computable earnings without acceptable deductions. Dividends, salaries,

rent, wages, interest and income from business are some of the taxable income (Evans, 2019,

pg.217). Deductions as well are expenses and costs incurred in gaining income. Deductions on

capital and personal expenses however are not deductible unless certain conditions are reached

(Anesa et al.2019, pg.79).

CAPITAL GAIN TAXES (CGT)

CGT is charged on income earned from sale of a property. Real and intangible assets are subject

to Capital Gain Tax. Assets like motor vehicles, one’s residence and assets meant for personal

use have exemptions. Real property asset among other assets are subject to capital gain for

foreign residents. For assets held more than a year, an Australian resident is allowed a 50%

discount for the purpose of taxation. With the amendment of capital gain tax rule, a non-resident

is not allowed to have the 50 percent discount and instead, loss on capital can only be

compensated by capital earnings.

As per the rules outlined above, one is legally responsible to pay tax on capital gains and

earnings or income and. Australian nonresidents and resident individuals are liable to income tax

and Capital Gain Tax (CGT). When imposing duty to individuals, progressive levy scale system

is used. This means the tax rate is proportional with an increase in taxable income.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

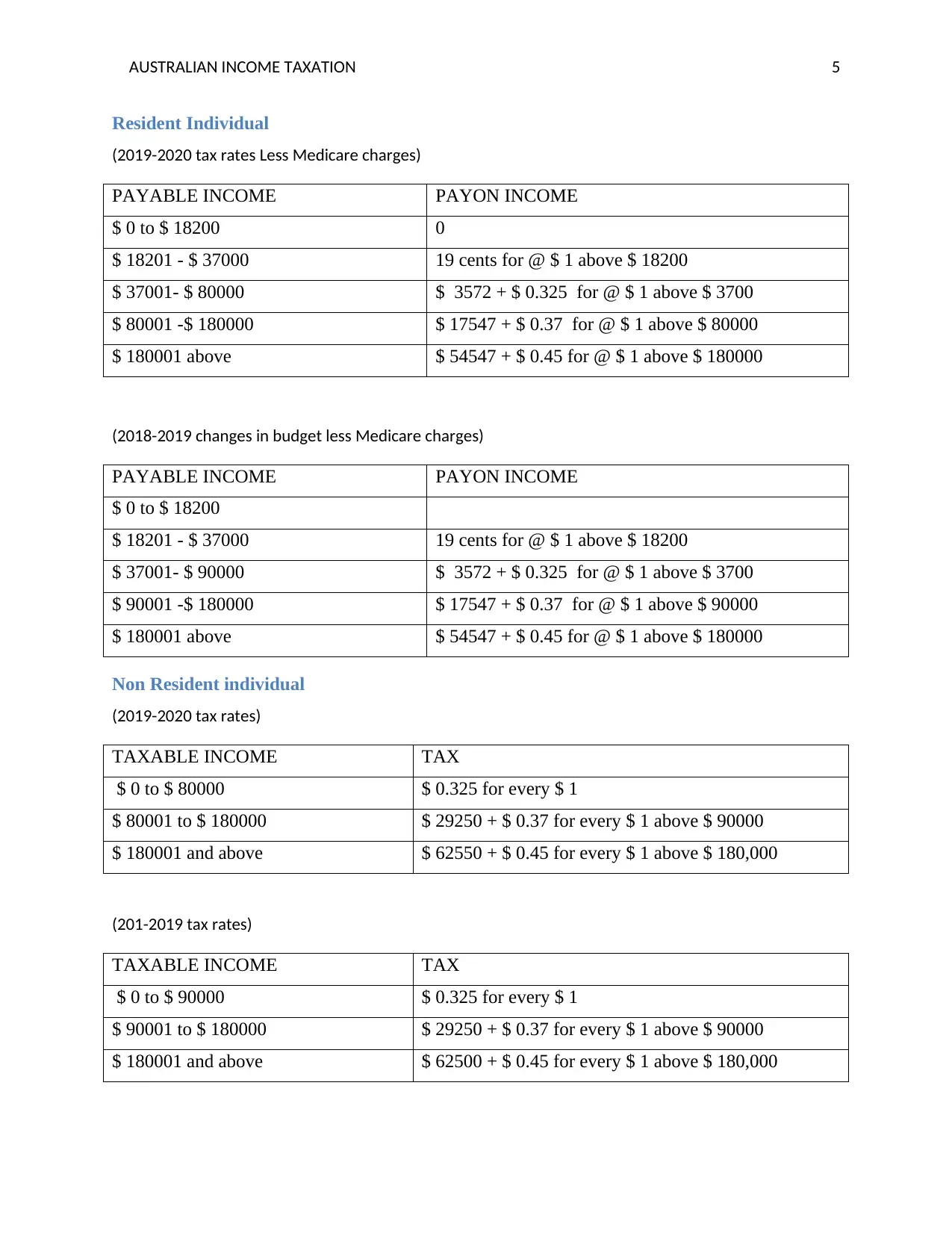

AUSTRALIAN INCOME TAXATION 5

Resident Individual

(2019-2020 tax rates Less Medicare charges)

PAYABLE INCOME PAYON INCOME

$ 0 to $ 18200 0

$ 18201 - $ 37000 19 cents for @ $ 1 above $ 18200

$ 37001- $ 80000 $ 3572 + $ 0.325 for @ $ 1 above $ 3700

$ 80001 -$ 180000 $ 17547 + $ 0.37 for @ $ 1 above $ 80000

$ 180001 above $ 54547 + $ 0.45 for @ $ 1 above $ 180000

(2018-2019 changes in budget less Medicare charges)

PAYABLE INCOME PAYON INCOME

$ 0 to $ 18200

$ 18201 - $ 37000 19 cents for @ $ 1 above $ 18200

$ 37001- $ 90000 $ 3572 + $ 0.325 for @ $ 1 above $ 3700

$ 90001 -$ 180000 $ 17547 + $ 0.37 for @ $ 1 above $ 90000

$ 180001 above $ 54547 + $ 0.45 for @ $ 1 above $ 180000

Non Resident individual

(2019-2020 tax rates)

TAXABLE INCOME TAX

$ 0 to $ 80000 $ 0.325 for every $ 1

$ 80001 to $ 180000 $ 29250 + $ 0.37 for every $ 1 above $ 90000

$ 180001 and above $ 62550 + $ 0.45 for every $ 1 above $ 180,000

(201-2019 tax rates)

TAXABLE INCOME TAX

$ 0 to $ 90000 $ 0.325 for every $ 1

$ 90001 to $ 180000 $ 29250 + $ 0.37 for every $ 1 above $ 90000

$ 180001 and above $ 62500 + $ 0.45 for every $ 1 above $ 180,000

Resident Individual

(2019-2020 tax rates Less Medicare charges)

PAYABLE INCOME PAYON INCOME

$ 0 to $ 18200 0

$ 18201 - $ 37000 19 cents for @ $ 1 above $ 18200

$ 37001- $ 80000 $ 3572 + $ 0.325 for @ $ 1 above $ 3700

$ 80001 -$ 180000 $ 17547 + $ 0.37 for @ $ 1 above $ 80000

$ 180001 above $ 54547 + $ 0.45 for @ $ 1 above $ 180000

(2018-2019 changes in budget less Medicare charges)

PAYABLE INCOME PAYON INCOME

$ 0 to $ 18200

$ 18201 - $ 37000 19 cents for @ $ 1 above $ 18200

$ 37001- $ 90000 $ 3572 + $ 0.325 for @ $ 1 above $ 3700

$ 90001 -$ 180000 $ 17547 + $ 0.37 for @ $ 1 above $ 90000

$ 180001 above $ 54547 + $ 0.45 for @ $ 1 above $ 180000

Non Resident individual

(2019-2020 tax rates)

TAXABLE INCOME TAX

$ 0 to $ 80000 $ 0.325 for every $ 1

$ 80001 to $ 180000 $ 29250 + $ 0.37 for every $ 1 above $ 90000

$ 180001 and above $ 62550 + $ 0.45 for every $ 1 above $ 180,000

(201-2019 tax rates)

TAXABLE INCOME TAX

$ 0 to $ 90000 $ 0.325 for every $ 1

$ 90001 to $ 180000 $ 29250 + $ 0.37 for every $ 1 above $ 90000

$ 180001 and above $ 62500 + $ 0.45 for every $ 1 above $ 180,000

AUSTRALIAN INCOME TAXATION 6

Companies in Australia are subject to taxable income for every income they receive. Similar

rules apply to individuals however profits gained by a company are subject to a flat rate tax of

30% depending on the level of income. From 2015 liberal party fought for a reduction of 1.5%

tax to 28.5%.

For shareholders, chargeable income includes dividends received from the company. The

dividends will therefore be factored in dividend imputation system. The system makes sure that

dividends are eventually paid using the standard income tax rate applicable to each shareholder

(Kirchler &Hoelzl, 2018, pg.255).

GOODS AND SERVICES TAX (GST)

This is a consumption tax levied on trade of goods and services within Australia and those

imported to Australia. It is also referred to as value added tax in other countries. This tax is

imposed at a constant rate of 10 percent however services like education, food, health and

exports are exempted from Goods and Service Tax (GST) (Freebairn, 2018, pg.263).

FRINGE BENEFIT TAX

This is a tax imposed on non-cash benefits given to employees by the employers. Fringe Benefit

tax is imposed at a rate of 45.5 percent on the employer. It can also be deducted from taxable

income earned by an employee (Butler &Alcott, 2018, pg.672).

AUSTRALIA TAXATION SYSTEM

Self-assessment taxation system

In Australian taxation system, the tax payers are responsible for filing their own tax returns also

termed as self-assessmentmodel. ATO does not review every tax in Australia because taxpayer’s

self-assessment is believed to be true. In addition, ATO cannot undertake audit to confirm if self-

taxpayers’ assessment is in line with the actual tax.

Withholding taxes

These taxes are billed on different payment categories and flat rates subject to billing in

question. The main objective of withholding tax is to ensure tax revenue collections are done

within the stipulated time and on continuous basis. The responsibility of withholding depends on

Companies in Australia are subject to taxable income for every income they receive. Similar

rules apply to individuals however profits gained by a company are subject to a flat rate tax of

30% depending on the level of income. From 2015 liberal party fought for a reduction of 1.5%

tax to 28.5%.

For shareholders, chargeable income includes dividends received from the company. The

dividends will therefore be factored in dividend imputation system. The system makes sure that

dividends are eventually paid using the standard income tax rate applicable to each shareholder

(Kirchler &Hoelzl, 2018, pg.255).

GOODS AND SERVICES TAX (GST)

This is a consumption tax levied on trade of goods and services within Australia and those

imported to Australia. It is also referred to as value added tax in other countries. This tax is

imposed at a constant rate of 10 percent however services like education, food, health and

exports are exempted from Goods and Service Tax (GST) (Freebairn, 2018, pg.263).

FRINGE BENEFIT TAX

This is a tax imposed on non-cash benefits given to employees by the employers. Fringe Benefit

tax is imposed at a rate of 45.5 percent on the employer. It can also be deducted from taxable

income earned by an employee (Butler &Alcott, 2018, pg.672).

AUSTRALIA TAXATION SYSTEM

Self-assessment taxation system

In Australian taxation system, the tax payers are responsible for filing their own tax returns also

termed as self-assessmentmodel. ATO does not review every tax in Australia because taxpayer’s

self-assessment is believed to be true. In addition, ATO cannot undertake audit to confirm if self-

taxpayers’ assessment is in line with the actual tax.

Withholding taxes

These taxes are billed on different payment categories and flat rates subject to billing in

question. The main objective of withholding tax is to ensure tax revenue collections are done

within the stipulated time and on continuous basis. The responsibility of withholding depends on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUSTRALIAN INCOME TAXATION 7

the payer and not the receiver of funds. The tax payers are obligated to withhold a given amount

of tax from their payments (Jacob, 2018, pg. 20).

The amount withheld is then paid to ATO in installments over the year. If an Australian

resident individual or firm pays royalties, dividends or interests to a foreign individual or entity,

it will have an obligation to withhold tax. Withholding tax also applies when one fails to indicate

either a TFN-tax file number or the ABN- Australian business umber when required (Mangioni,

2019).

Australia also has PAYG-pay as you go tax withholding. The duty is deducted from

wages or salaries and remitted to ATO by employers. This tax also applies to payment of funds

to businesses if they did not quote their ABN when dealing with your entity (Sandford, 2018).

GST anti - avoidance provisions

GST have similar provisions to those that are available on taxation of income. These

provisions are designed in way that it increases benefits by reducing GST payable and alteration

of GST payment timing. It mainly aims artificial schemes (agreements, promises,

understandings, arrangements and any other deeds whether expressed or implied (Shome, 2019,

pg. 335). Anti-avoidance rules are applicable if the following conditions are met;

a) Availability of scheme

There must be a legally binding agreement and option to restructure or amend an undertaking to

suit the situation if in any way the agreement had not been sealed. Proper timing should also be

considered.

b) GST benefit existence

GST benefit brought by the scheme must exist in either of the following; an entity is not obliged

to pay GST, the entity is entitled to GST refund, ability of the entity to postpone its payments to

later times in future and if the entity has had prior GST refunds.

c) The benefit should also be part of the scheme

It is important to note that that the benefit received by the entity must be attributed to the

scheme.

the payer and not the receiver of funds. The tax payers are obligated to withhold a given amount

of tax from their payments (Jacob, 2018, pg. 20).

The amount withheld is then paid to ATO in installments over the year. If an Australian

resident individual or firm pays royalties, dividends or interests to a foreign individual or entity,

it will have an obligation to withhold tax. Withholding tax also applies when one fails to indicate

either a TFN-tax file number or the ABN- Australian business umber when required (Mangioni,

2019).

Australia also has PAYG-pay as you go tax withholding. The duty is deducted from

wages or salaries and remitted to ATO by employers. This tax also applies to payment of funds

to businesses if they did not quote their ABN when dealing with your entity (Sandford, 2018).

GST anti - avoidance provisions

GST have similar provisions to those that are available on taxation of income. These

provisions are designed in way that it increases benefits by reducing GST payable and alteration

of GST payment timing. It mainly aims artificial schemes (agreements, promises,

understandings, arrangements and any other deeds whether expressed or implied (Shome, 2019,

pg. 335). Anti-avoidance rules are applicable if the following conditions are met;

a) Availability of scheme

There must be a legally binding agreement and option to restructure or amend an undertaking to

suit the situation if in any way the agreement had not been sealed. Proper timing should also be

considered.

b) GST benefit existence

GST benefit brought by the scheme must exist in either of the following; an entity is not obliged

to pay GST, the entity is entitled to GST refund, ability of the entity to postpone its payments to

later times in future and if the entity has had prior GST refunds.

c) The benefit should also be part of the scheme

It is important to note that that the benefit received by the entity must be attributed to the

scheme.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUSTRALIAN INCOME TAXATION 8

d) GST benefit should not be attributed to election or choice

The GST benefit received must be in order of the law or underlying scheme and must not be

attributable to ones’ choice or intentions.

TAXATION LEGISLATION AND CASE LAWS

CASE 1

City Sky Co is eligible to input tax credit because it is a registered company. The

company has a plan of building 15 apartments on its land in Southern part of Brisbane. Land is a

fixed asset and it is neither regarded as a good or service, therefore Goods and Service Tax

(GST) tax cannot be imposed on unoccupied land. In addition, City Sky Co will not be entitled

with input tax credit if it has a plan of building apartments on the land due to black credit

provisions (Fitzpatrick& Kevin, 2019).

Maurice Blackburn, a local lawyer, is offering legal service to City Sky Co at a fee of

$33,000. Services rendered by a lawyer are considered a reverse charge mechanism, hence GST

is charged to the recipient of services. The receiver is entitled to input tax credit only if the

service is purposely for its business. City Sky Co will therefore claim input tax credit of GST

because it is a development company and the advocate’s services is purposely for its business

only. The revenue of Maurice Blackburn has been mentioned but it does not add up for the

business to demand input tax credit for development services (Storm & Coetzee, 2018, pg151).

CASE 2

An assessed is liable to pay duty if his or her income tax surpasses the basic or standard

exemption. this exemption differs from one assessed to another. For example, an assessed whose

age is below 60yrs is entitled to exemption of 250,000. However, which does not include long

term capital earnings. For long-term capital gains, 20% taxes are levied against assesse. Fixed

assets are considered for capital gains if the time of holding the asset exceeds 36 months and 24

months for shares. In the Manjulal J Shaw case law, a gift given to an assessed by a relative or a

friend from the preceding year.

d) GST benefit should not be attributed to election or choice

The GST benefit received must be in order of the law or underlying scheme and must not be

attributable to ones’ choice or intentions.

TAXATION LEGISLATION AND CASE LAWS

CASE 1

City Sky Co is eligible to input tax credit because it is a registered company. The

company has a plan of building 15 apartments on its land in Southern part of Brisbane. Land is a

fixed asset and it is neither regarded as a good or service, therefore Goods and Service Tax

(GST) tax cannot be imposed on unoccupied land. In addition, City Sky Co will not be entitled

with input tax credit if it has a plan of building apartments on the land due to black credit

provisions (Fitzpatrick& Kevin, 2019).

Maurice Blackburn, a local lawyer, is offering legal service to City Sky Co at a fee of

$33,000. Services rendered by a lawyer are considered a reverse charge mechanism, hence GST

is charged to the recipient of services. The receiver is entitled to input tax credit only if the

service is purposely for its business. City Sky Co will therefore claim input tax credit of GST

because it is a development company and the advocate’s services is purposely for its business

only. The revenue of Maurice Blackburn has been mentioned but it does not add up for the

business to demand input tax credit for development services (Storm & Coetzee, 2018, pg151).

CASE 2

An assessed is liable to pay duty if his or her income tax surpasses the basic or standard

exemption. this exemption differs from one assessed to another. For example, an assessed whose

age is below 60yrs is entitled to exemption of 250,000. However, which does not include long

term capital earnings. For long-term capital gains, 20% taxes are levied against assesse. Fixed

assets are considered for capital gains if the time of holding the asset exceeds 36 months and 24

months for shares. In the Manjulal J Shaw case law, a gift given to an assessed by a relative or a

friend from the preceding year.

AUSTRALIAN INCOME TAXATION 9

Computation: Emma’s capital gains for the year 2015.

Land:

Purchase consideration =$ 265,000

Expenses incurred =$ 57,500

. Land sale value = $ 1000,000

Gross Long Term gain = (1000, 000-265,000- 57,500)

= $ 677,500

Shares:

Acquisition cost = (1000*3.5) =$ 3500

Expenses incurred on sale= (50,850*0.02) =1017

Sale value = (1000 shares * $ 50.85) = $ 50,850

Gross Long Term Capital on shares =$ 46,333

Stamp Collection

Sale value =$ 50,000

Expenses incurred =$5000

Purchase value =$60,000

Loss = (50,000 - 60,000 -5,000) = - $ 15,000

Total Loss on stamp sales = $ -15,000

Piano

Purchase value = $80,000

Computation: Emma’s capital gains for the year 2015.

Land:

Purchase consideration =$ 265,000

Expenses incurred =$ 57,500

. Land sale value = $ 1000,000

Gross Long Term gain = (1000, 000-265,000- 57,500)

= $ 677,500

Shares:

Acquisition cost = (1000*3.5) =$ 3500

Expenses incurred on sale= (50,850*0.02) =1017

Sale value = (1000 shares * $ 50.85) = $ 50,850

Gross Long Term Capital on shares =$ 46,333

Stamp Collection

Sale value =$ 50,000

Expenses incurred =$5000

Purchase value =$60,000

Loss = (50,000 - 60,000 -5,000) = - $ 15,000

Total Loss on stamp sales = $ -15,000

Piano

Purchase value = $80,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUSTRALIAN INCOME TAXATION 10

Sale value =$30,000

Loss = (80,000- 30,000) =50,000

Total Loss=$ -50,000

Total long term capital gain

= (677,500 -46,333 – 15,000 -50,000)

= $ 566,167

Tax levied on long term gain for the year 2015

= (566,167 * 20/100)

=$ 113,233.

The assesse is entitled to offset losses subject to long term capital assets and capital gains as long

as the assesse is liable to meet duty charges. Income tax return should be filed latest o n31st July

every assessment year in line with 1961 income tax act.

PRINCIPLES OF TAXATION

This is the fundamental elements or values a tax system should demonstrate. The values include

equity, neutrality, efficiency, certainty, simplicity and equity (Yong et al.2019).

Efficiency Tax system should not twist or alter decisions made on resource allocation in the

economy.

Equity this is the equal allocation of tax responsibility to the population. Distribution of duty

obligation can either horizontal equity where tax payer’s ion same level should be charged a

uniform amount or vertical equity where tax is imposed depending on the level of the payer

(Tran & Zakariyya, 2019, pg.5).

Simplicity is one of the fundamentals of a good tax system. Taxpayers should easily and clearly

comprehend their tax obligation.

Sale value =$30,000

Loss = (80,000- 30,000) =50,000

Total Loss=$ -50,000

Total long term capital gain

= (677,500 -46,333 – 15,000 -50,000)

= $ 566,167

Tax levied on long term gain for the year 2015

= (566,167 * 20/100)

=$ 113,233.

The assesse is entitled to offset losses subject to long term capital assets and capital gains as long

as the assesse is liable to meet duty charges. Income tax return should be filed latest o n31st July

every assessment year in line with 1961 income tax act.

PRINCIPLES OF TAXATION

This is the fundamental elements or values a tax system should demonstrate. The values include

equity, neutrality, efficiency, certainty, simplicity and equity (Yong et al.2019).

Efficiency Tax system should not twist or alter decisions made on resource allocation in the

economy.

Equity this is the equal allocation of tax responsibility to the population. Distribution of duty

obligation can either horizontal equity where tax payer’s ion same level should be charged a

uniform amount or vertical equity where tax is imposed depending on the level of the payer

(Tran & Zakariyya, 2019, pg.5).

Simplicity is one of the fundamentals of a good tax system. Taxpayers should easily and clearly

comprehend their tax obligation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUSTRALIAN INCOME TAXATION 11

Certainty principle the tax payer should be aware of the tax obligation and should have a clear

plan on how to meet the provisions.

Neutrality is where the tax imposed to payers does not have impact on their choices.

Certainty principle the tax payer should be aware of the tax obligation and should have a clear

plan on how to meet the provisions.

Neutrality is where the tax imposed to payers does not have impact on their choices.

AUSTRALIAN INCOME TAXATION 12

REFERENCES

Anesa, M., Gillespie, N., Spee, A.P. and Sadiq, K., 2019. The legitimation of corporate tax

minimization. Accounting, Organizations and Society, 75, pp.17-39.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Fitzpatrick, Kevin. "The Australian Taxation Office's approaches to aggressive tax planning."

In Centre for Tax System Integrity Third International Conference on'Responsive Regulation:

International perspectives on taxation'. Canberra, 24-25 July 2003. Centre for Tax System

Integrity (CTSI), Research School of Social Sciences, The Australian National University, 2019.

Freebairn, J., 2018. Federalism and Tax reform. Australian Economic Review, 51(2), pp.262-

268.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Kirchler, E. and Hoelzl, E., 2018. 16 Tax Behaviour. CENTRE FOR DECISION RESEARCH,

UNIVERSITY OF LEEDS, UK, p.255.

Mangioni, V., 2019. Value capture taxation: alternate sources of revenue for Sub-Central

government in Australia. Journal of Financial Management of Property and Construction.

Sandford, C.T., 2018. Taxing Personal Wealth: An Analysis of Capital Taxation in the United

Kingdom—History, Present Structure and Future Possibilities. Routledge.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

Storm, A. and Coetzee, K., 2018. Towards Improving South Africa's Legislation On Tax

Evasion: A Comparison of Legislation On Tax Evasion of The USA, UK, Australia and South

Africa. Journal of Applied Business Research, 34(1), p.151.

REFERENCES

Anesa, M., Gillespie, N., Spee, A.P. and Sadiq, K., 2019. The legitimation of corporate tax

minimization. Accounting, Organizations and Society, 75, pp.17-39.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Evans, A.C., 2019. Why we use private trusts in Australia: The income tax dimension

explained. Sydney L. Rev., 41, p.217.

Fitzpatrick, Kevin. "The Australian Taxation Office's approaches to aggressive tax planning."

In Centre for Tax System Integrity Third International Conference on'Responsive Regulation:

International perspectives on taxation'. Canberra, 24-25 July 2003. Centre for Tax System

Integrity (CTSI), Research School of Social Sciences, The Australian National University, 2019.

Freebairn, J., 2018. Federalism and Tax reform. Australian Economic Review, 51(2), pp.262-

268.

Jacob, M., 2018. Tax regimes and capital gains realizations. European Accounting

Review, 27(1), pp.1-21.

Kirchler, E. and Hoelzl, E., 2018. 16 Tax Behaviour. CENTRE FOR DECISION RESEARCH,

UNIVERSITY OF LEEDS, UK, p.255.

Mangioni, V., 2019. Value capture taxation: alternate sources of revenue for Sub-Central

government in Australia. Journal of Financial Management of Property and Construction.

Sandford, C.T., 2018. Taxing Personal Wealth: An Analysis of Capital Taxation in the United

Kingdom—History, Present Structure and Future Possibilities. Routledge.

Shome, P., 2019. General Anti-Avoidance Rules (GAAR): A Critical Analysis. Revista de

Direito Internacional Econômico e Tributário, 13(1), pp.331-355.

Storm, A. and Coetzee, K., 2018. Towards Improving South Africa's Legislation On Tax

Evasion: A Comparison of Legislation On Tax Evasion of The USA, UK, Australia and South

Africa. Journal of Applied Business Research, 34(1), p.151.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.