Finance Report: Descriptive Analysis of Australian IPO Market

VerifiedAdded on 2021/05/31

|16

|3772

|14

Report

AI Summary

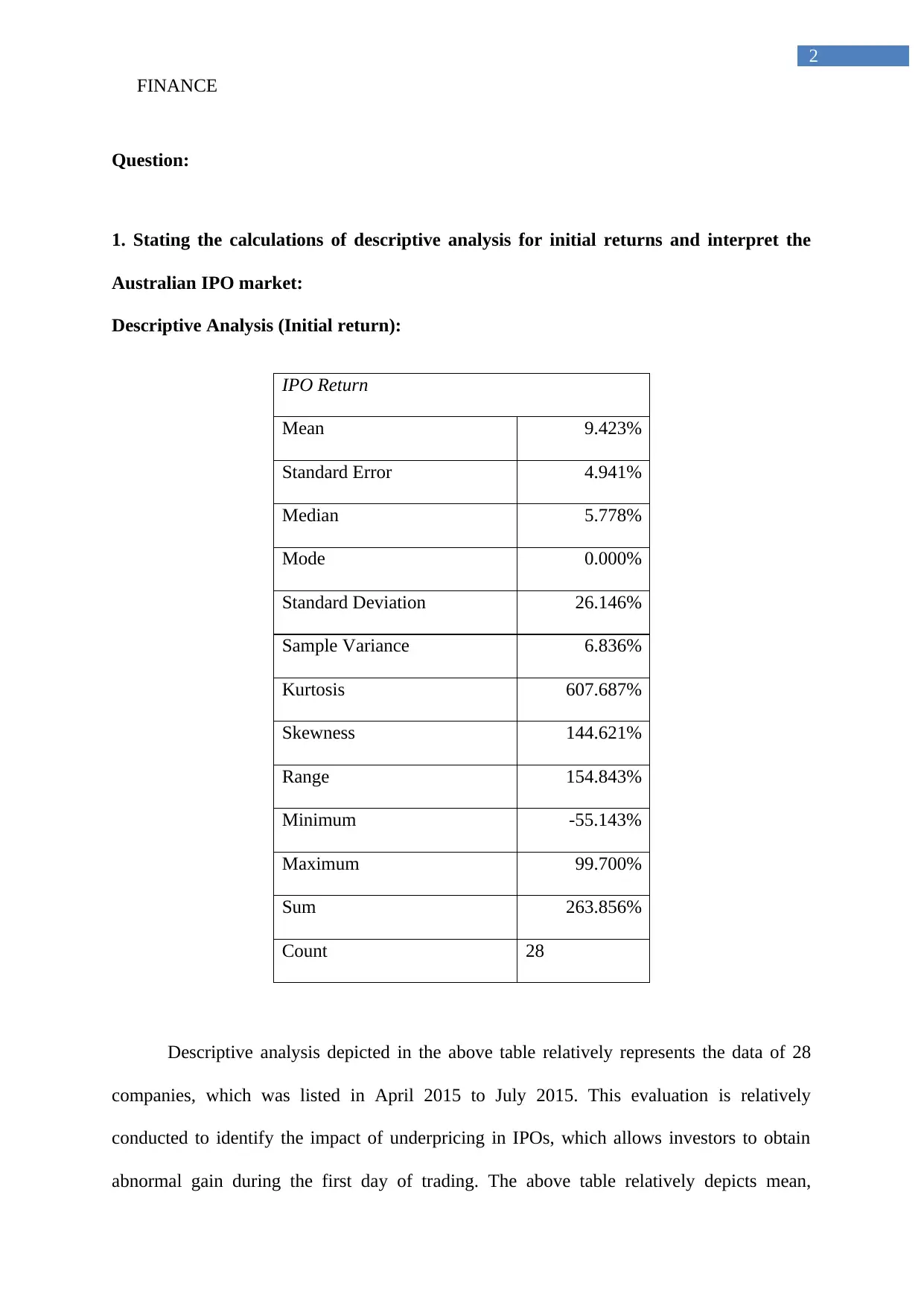

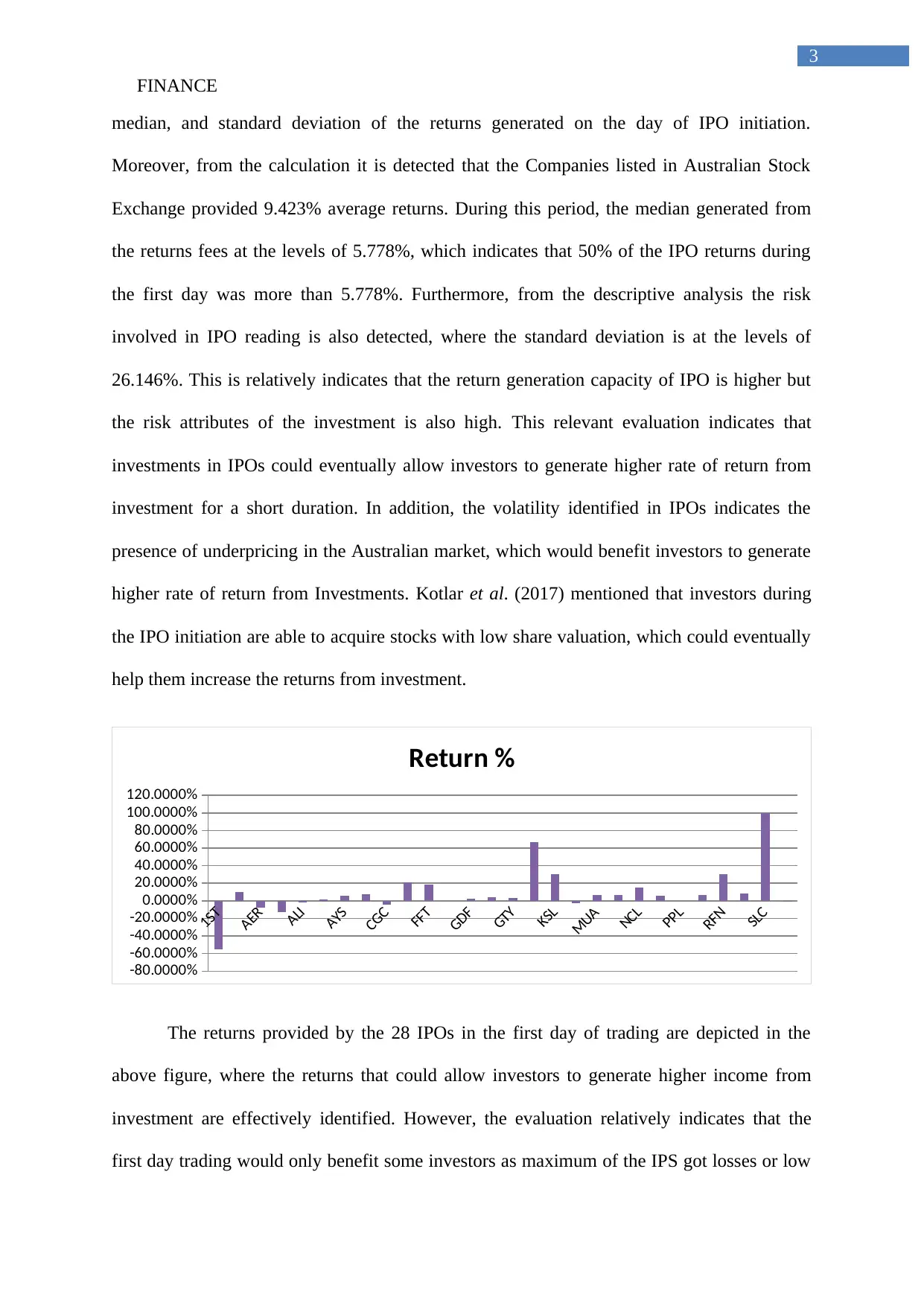

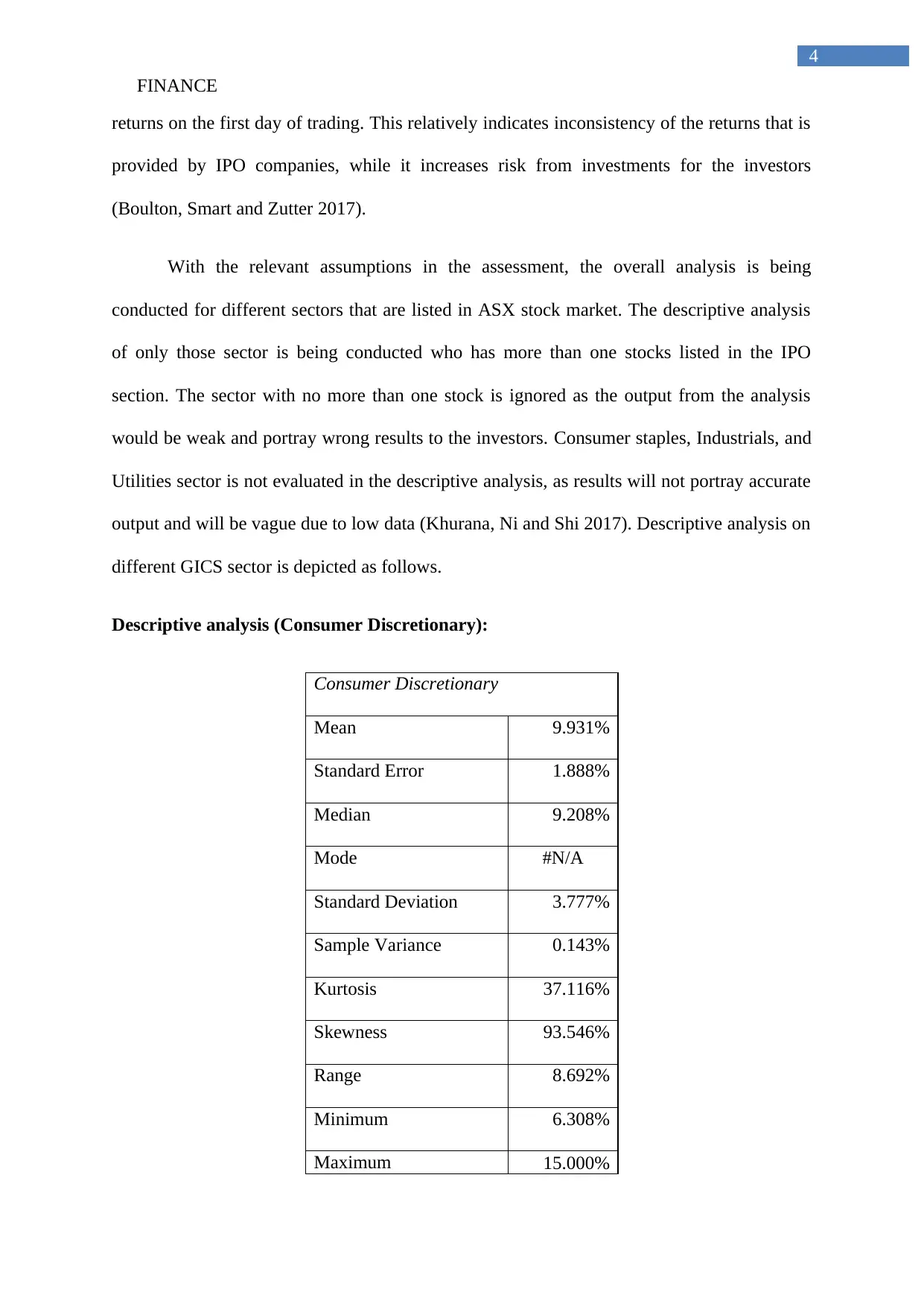

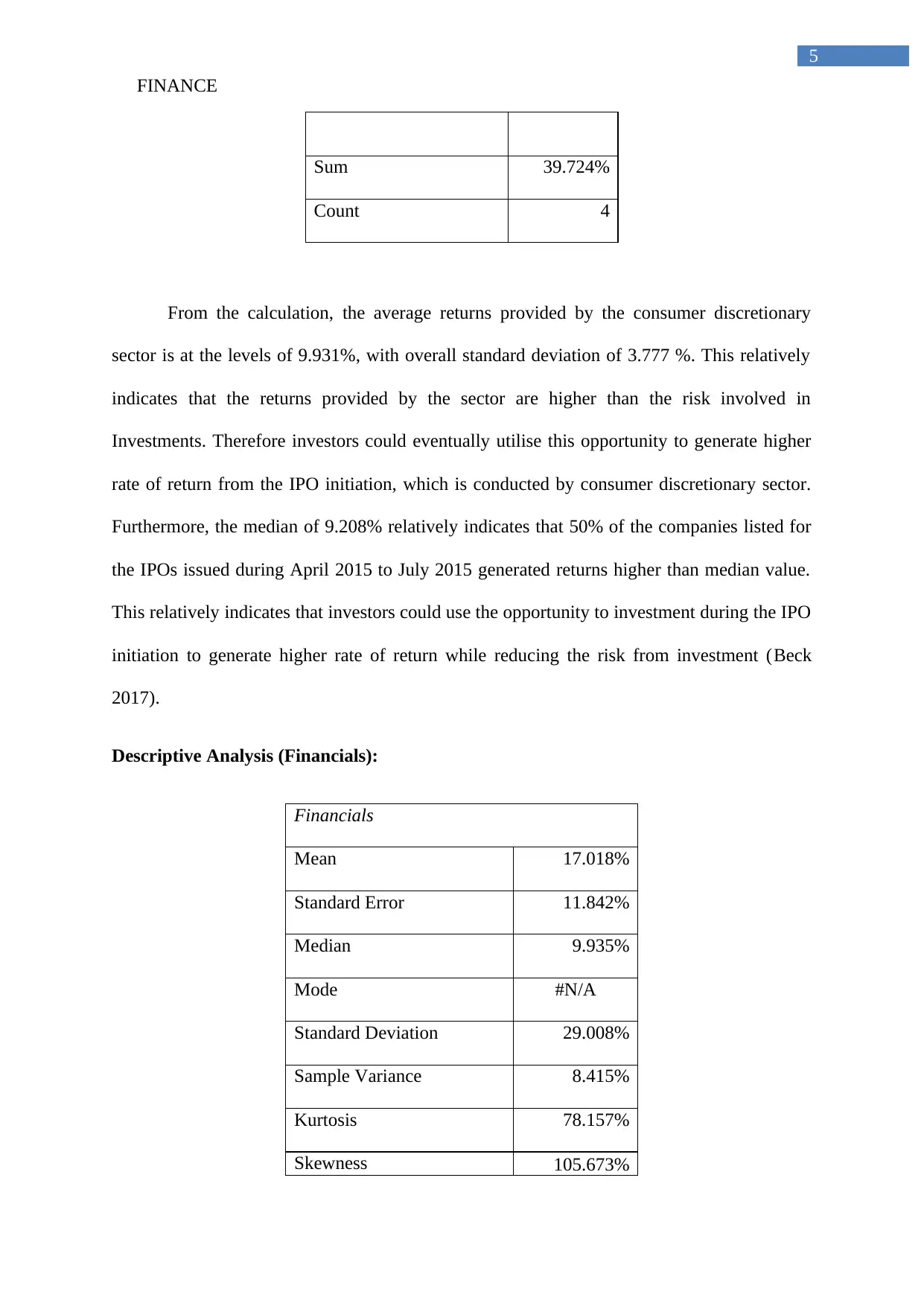

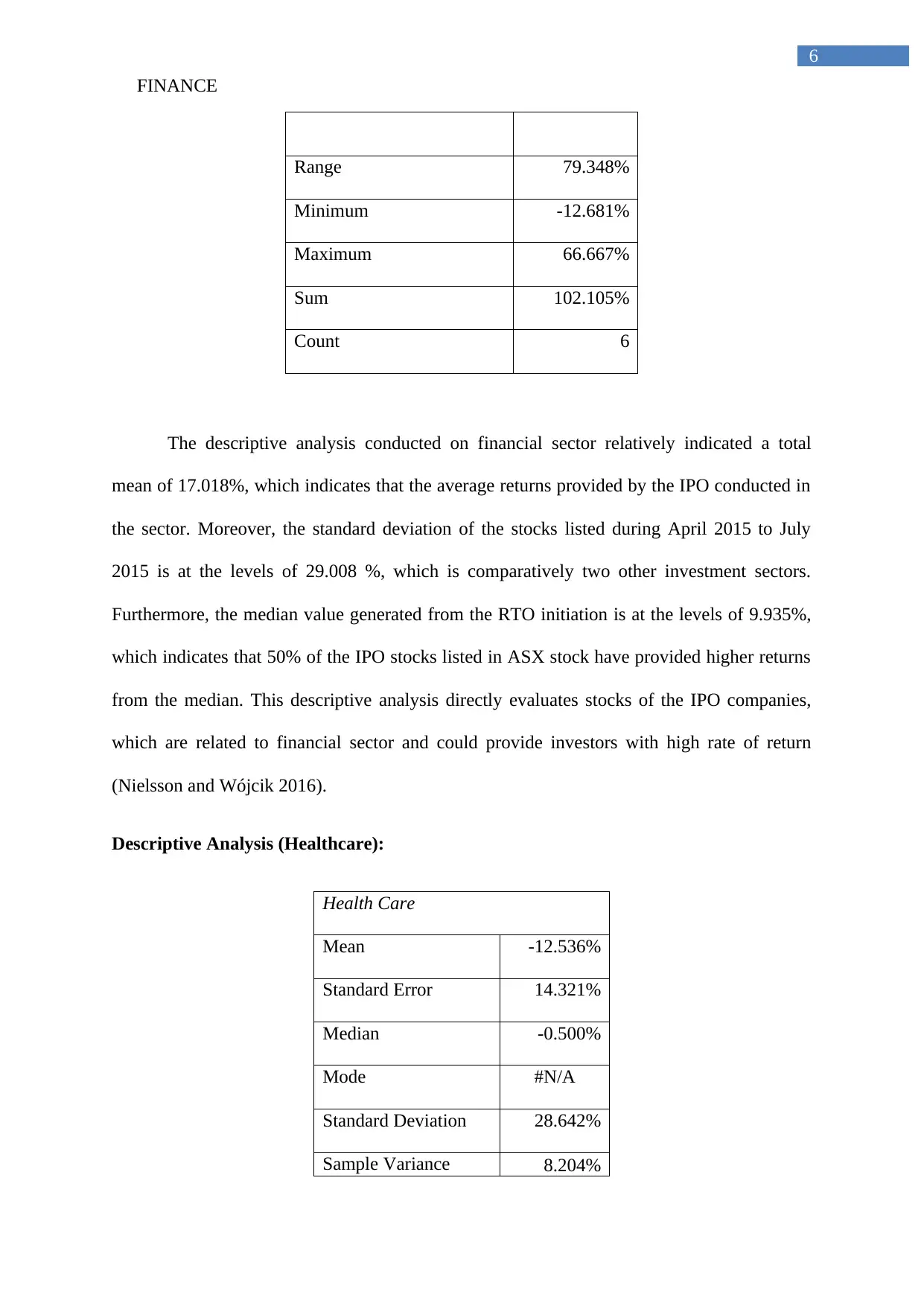

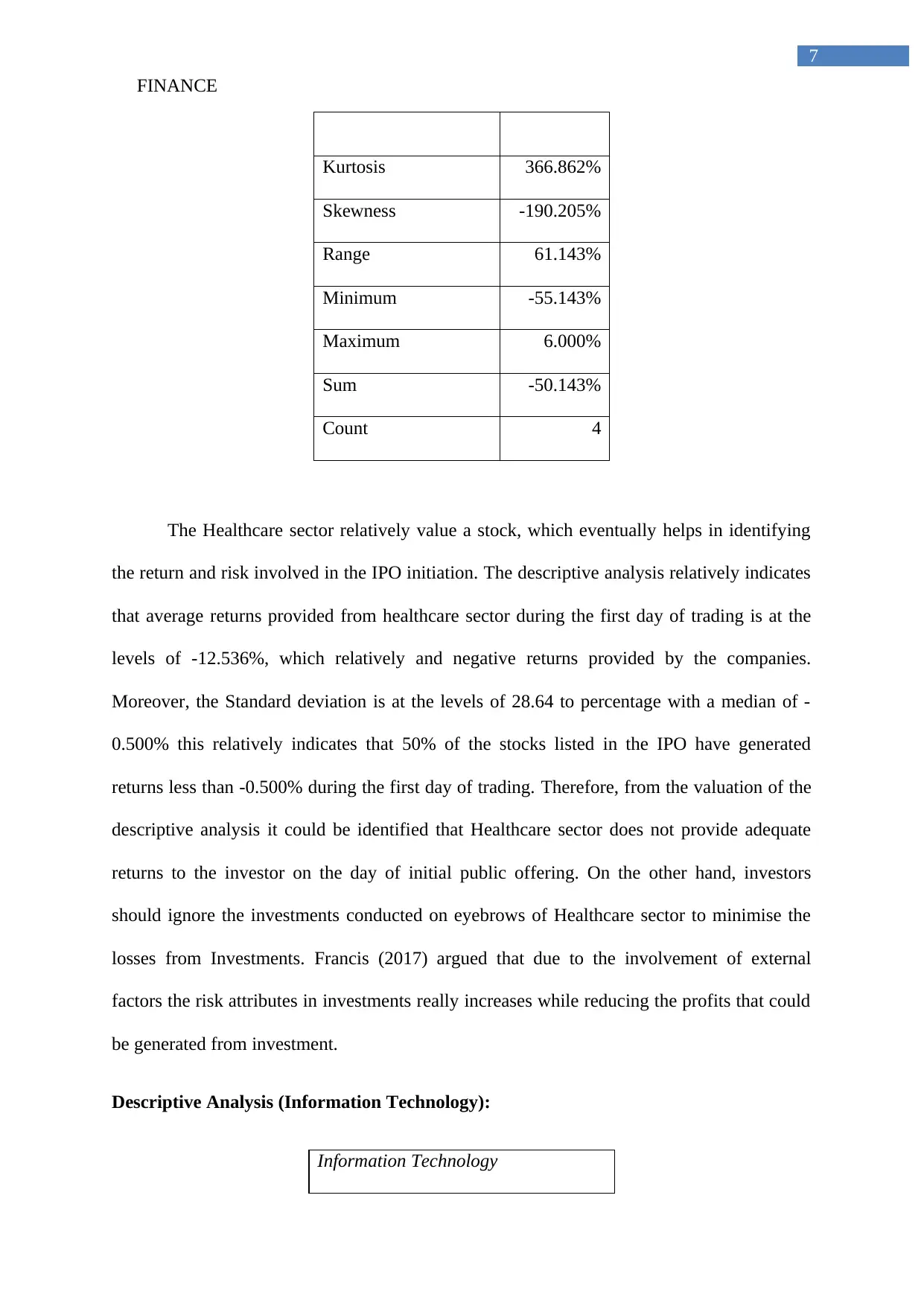

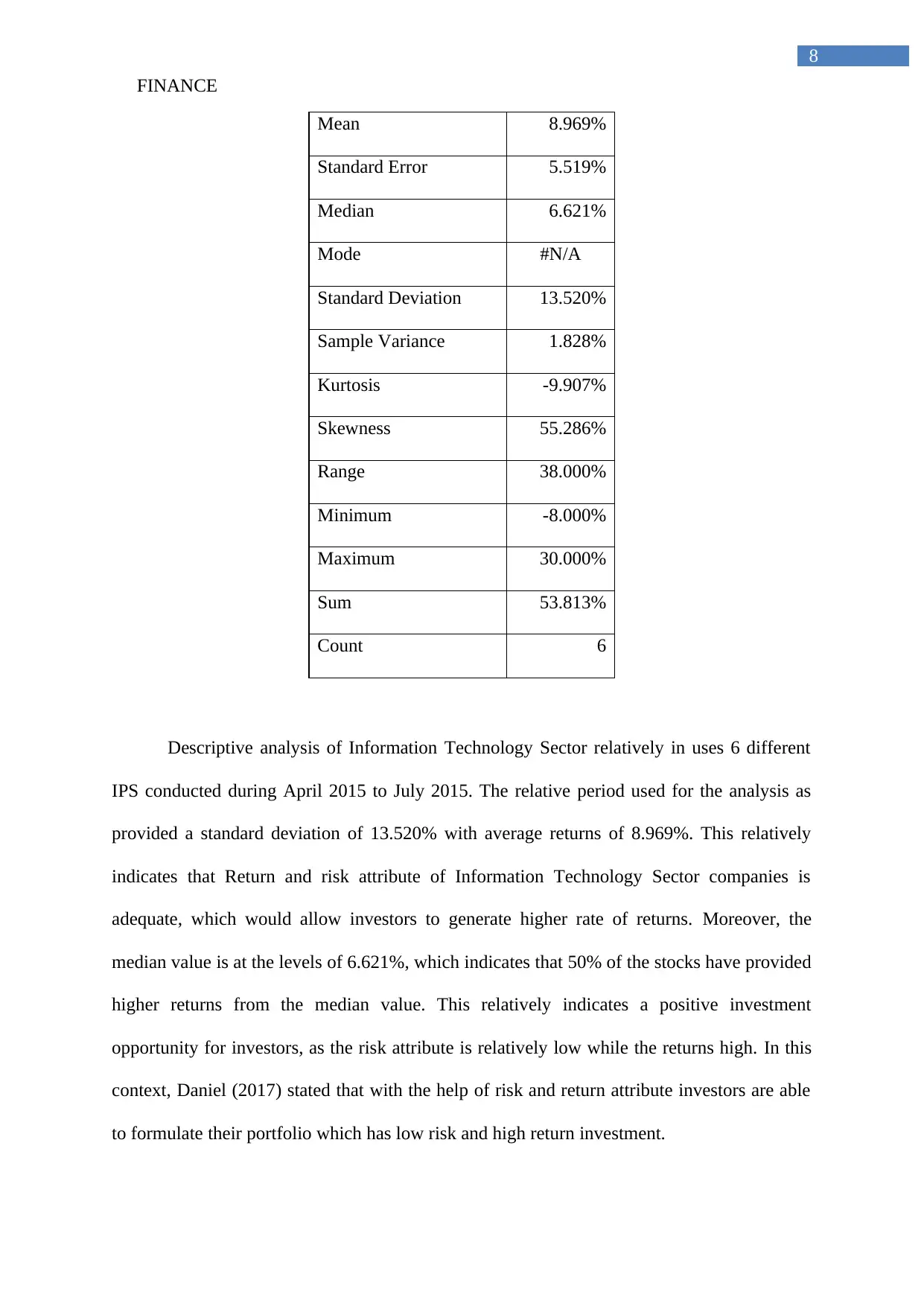

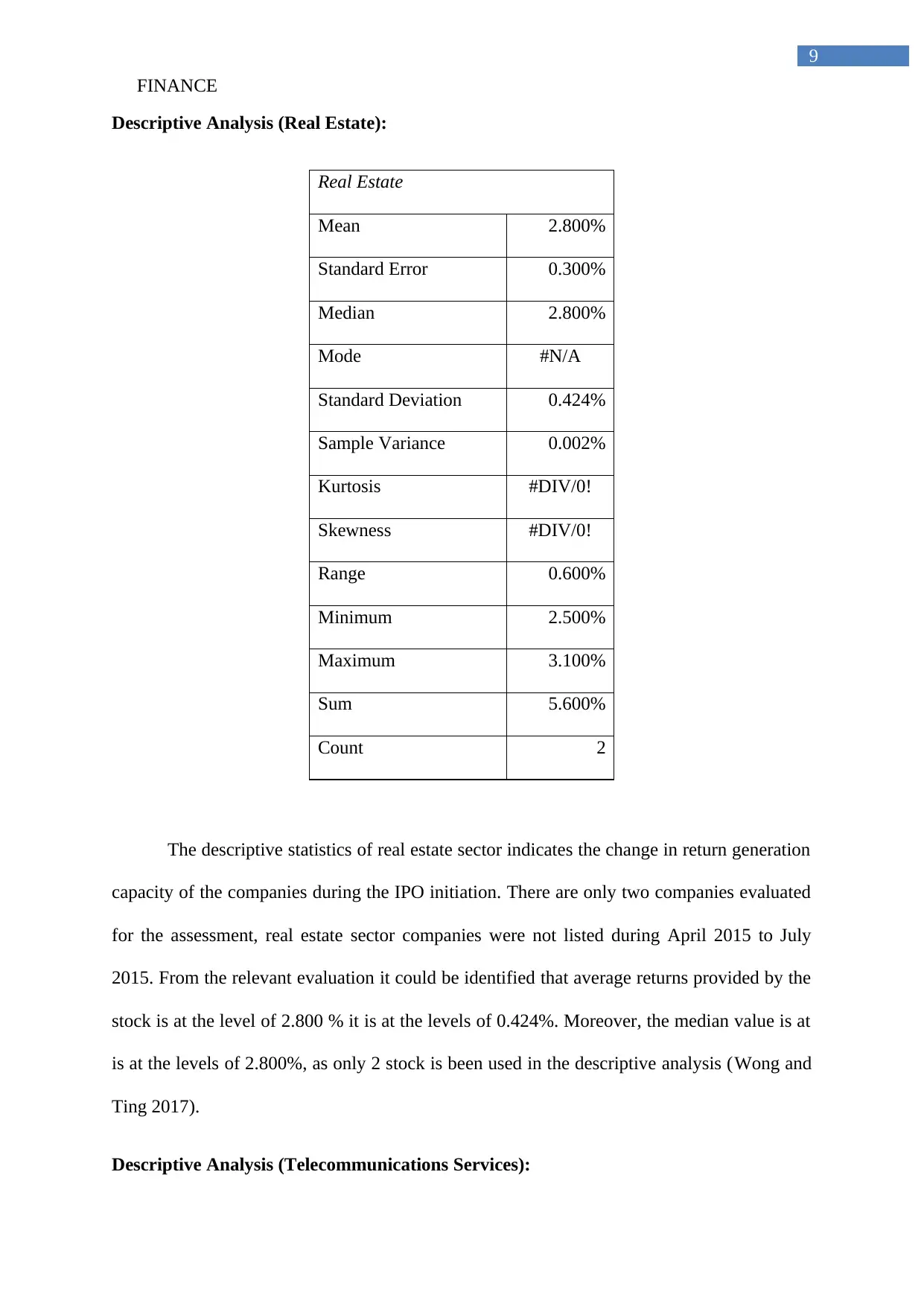

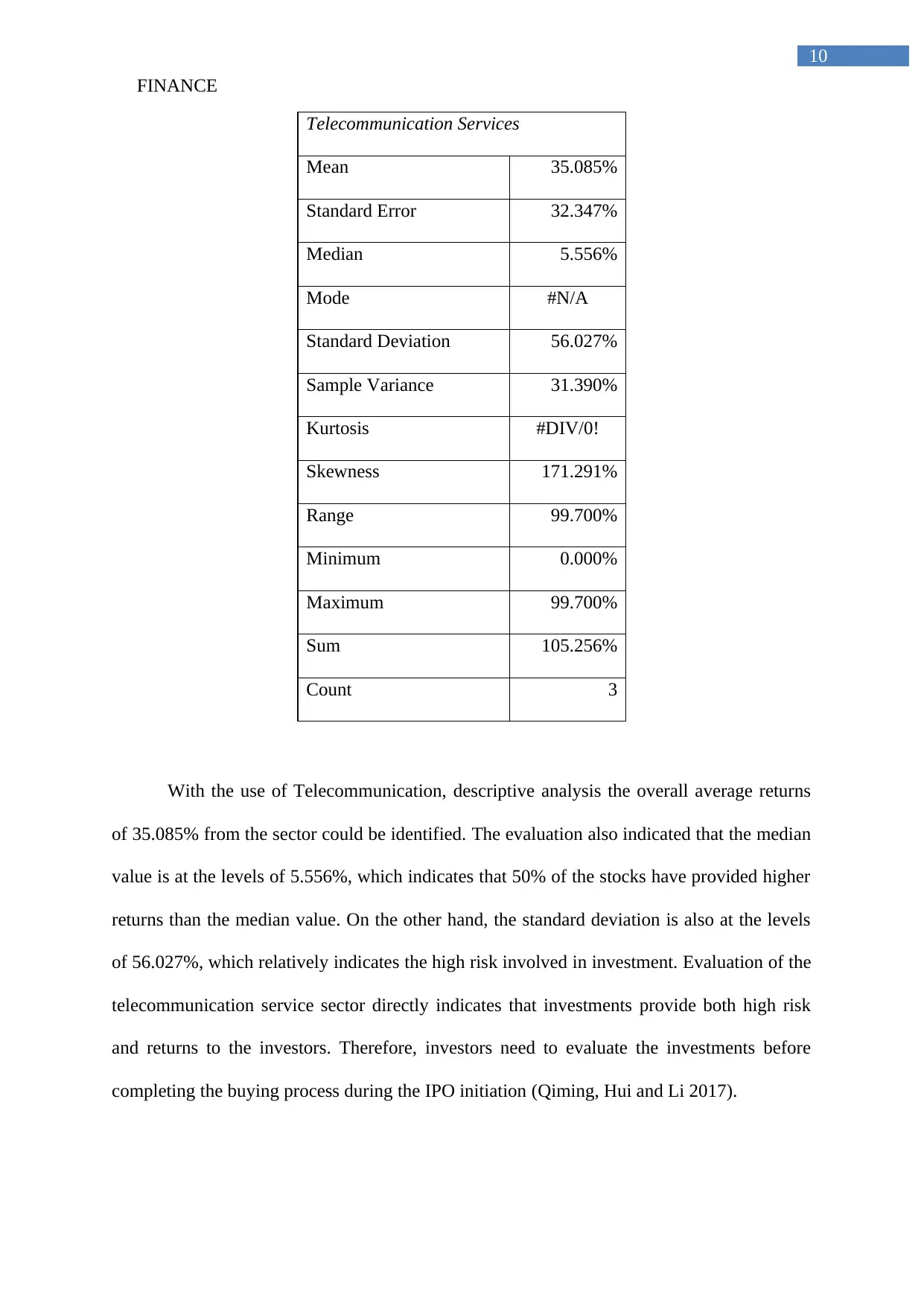

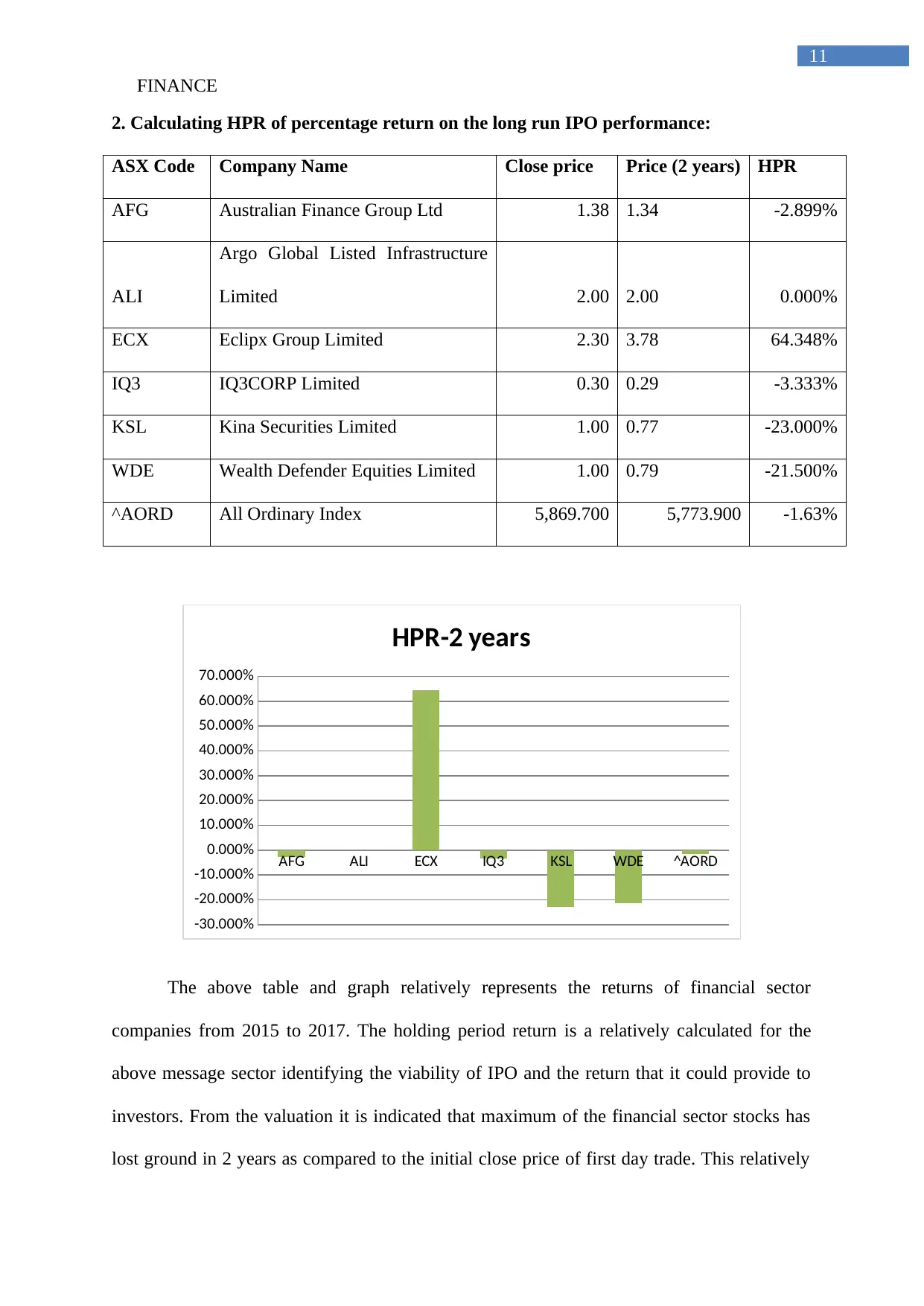

This finance report provides a detailed analysis of the Australian IPO market. It begins with a descriptive analysis of initial returns, examining the performance of companies listed between April and July 2015, and interprets the impact of underpricing on investor gains. The report calculates the Holding Period Return (HPR) to assess the long-run IPO performance and evaluates the returns of financial sector companies from 2015 to 2017. Furthermore, it explores the theories and empirical studies related to short-run IPO underpricing in the US and Australia, focusing on asymmetric information and behavioral theories. The analysis includes sector-specific descriptive statistics and a comparison of returns, volatility, and risk involved in IPO investments, concluding that IPO investments in the Australian market could be risky and may not always provide high returns. The report emphasizes the importance of evaluating investments before participating in IPO initiations.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.