FIN205 Business Finance Project: Australian Market and Stock Analysis

VerifiedAdded on 2023/06/04

|15

|2942

|309

Report

AI Summary

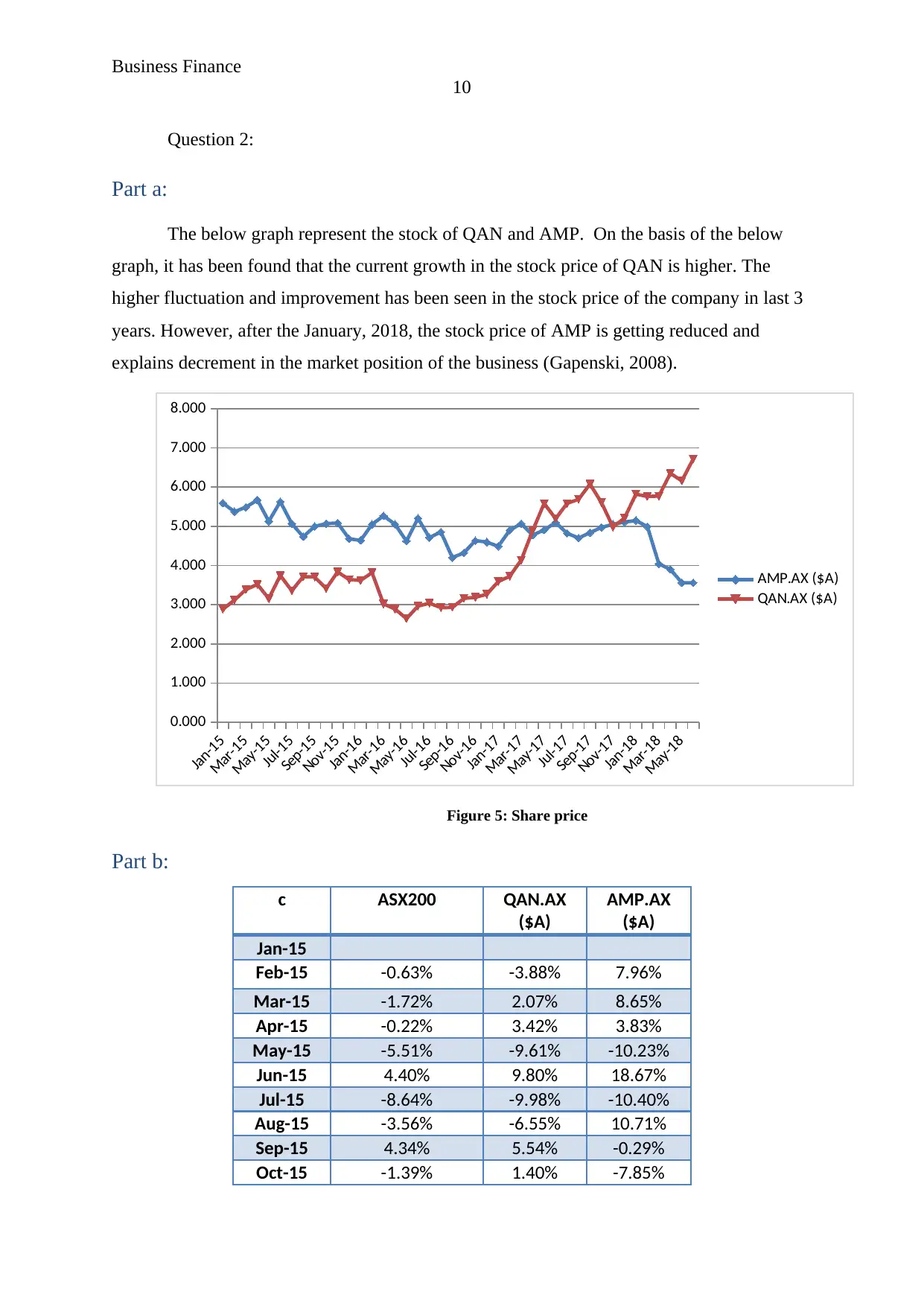

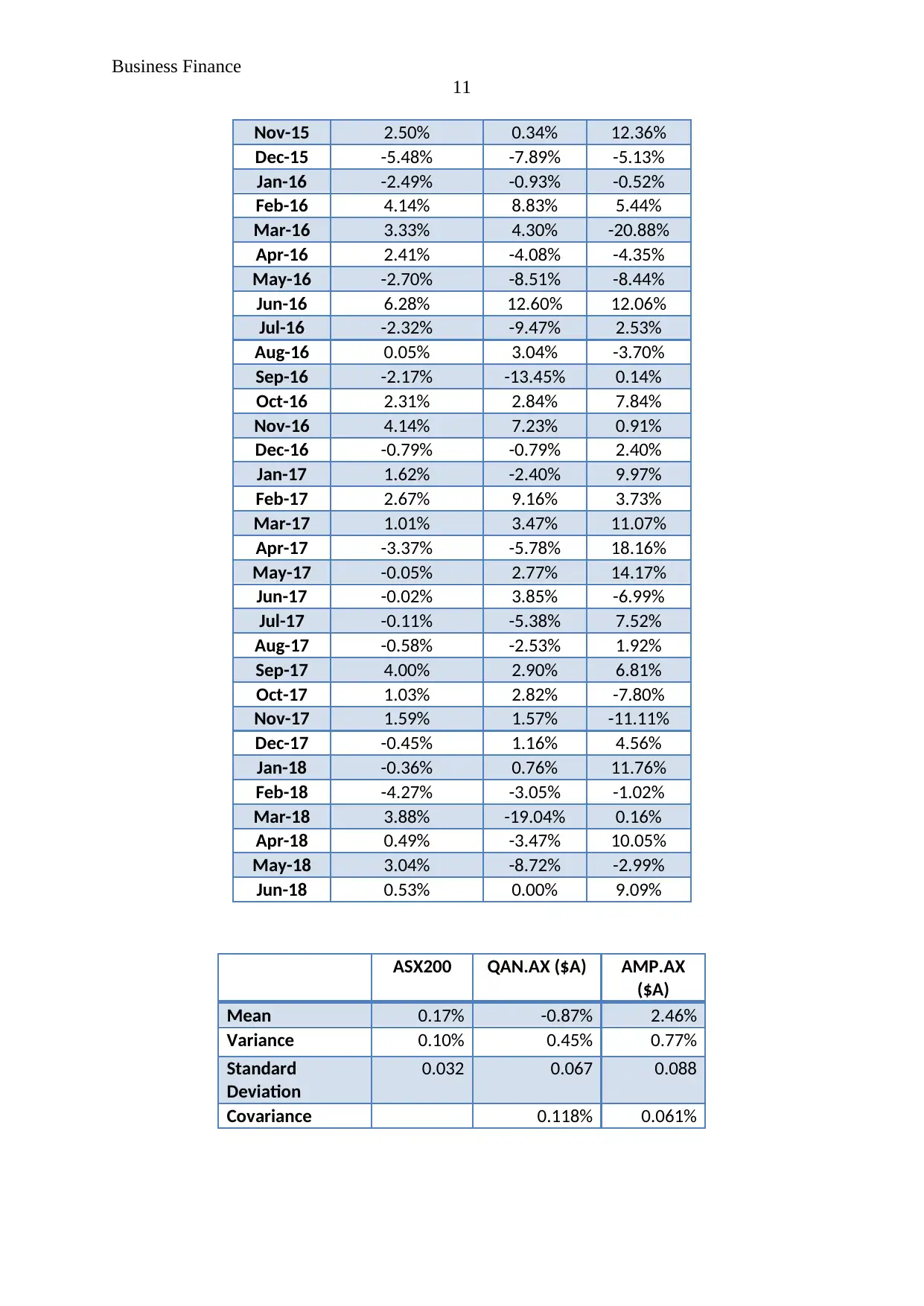

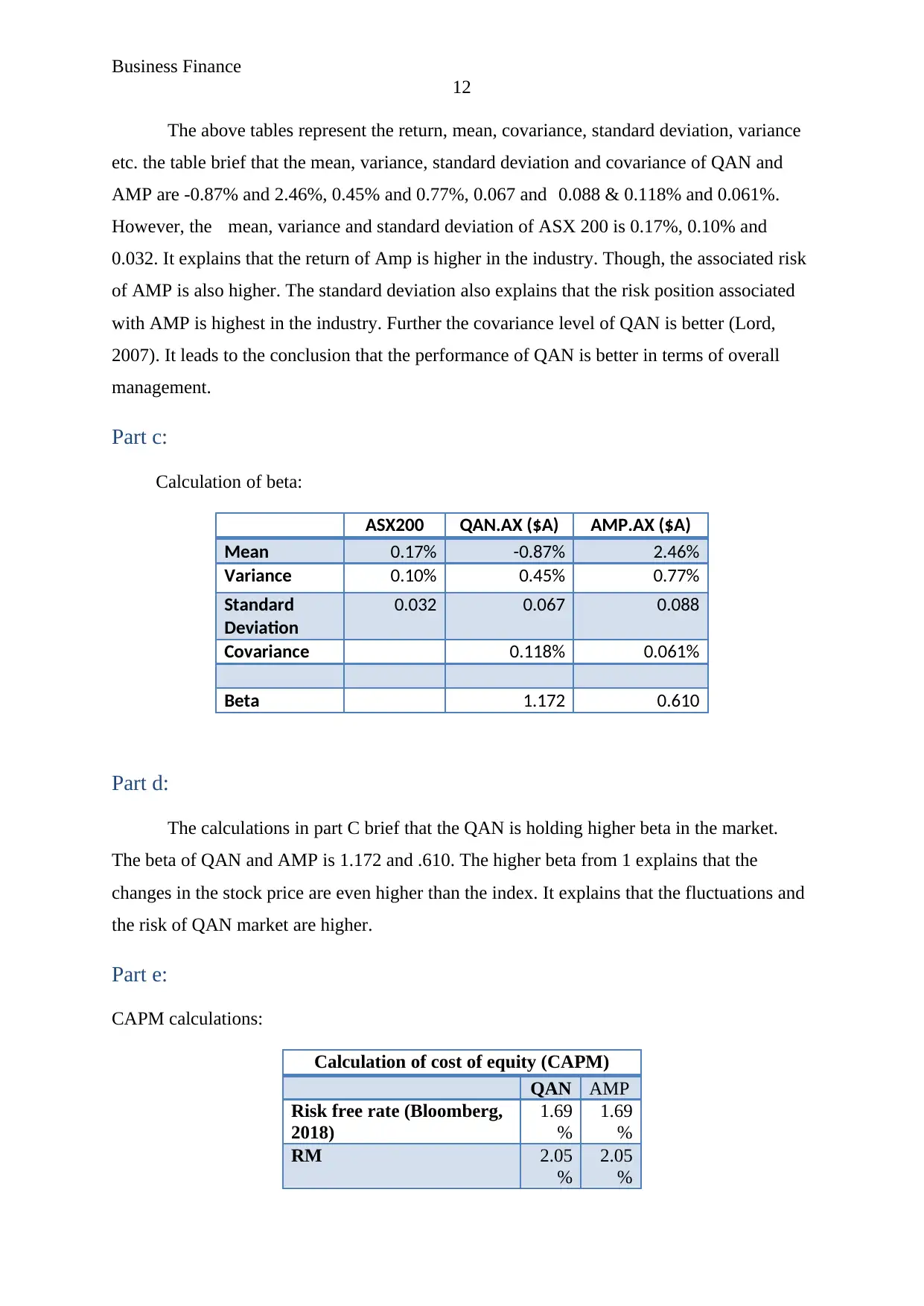

This report provides a comprehensive analysis of business finance concepts, focusing on the Australian market. It begins with an examination of the yield curve, interpreting its shape and relating it to economic conditions and expectation theory. The report then delves into a stock analysis of Qantas (QAN) and AMP, evaluating their stock prices, returns, mean, variance, standard deviation, and covariance. Beta calculations are performed to assess the systematic risk of each stock, and the Capital Asset Pricing Model (CAPM) is used to determine the required rate of return and assess whether the stocks are under or overpriced. The analysis compares the performance of QAN and AMP, considering factors like stock fluctuations, market position, and associated risks, ultimately providing insights into the past performance and future perspectives of both companies.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.