Partnership Taxation: 'The Two B's' Income Statement & Tax Payable

VerifiedAdded on 2020/05/01

|9

|1560

|70

Homework Assignment

AI Summary

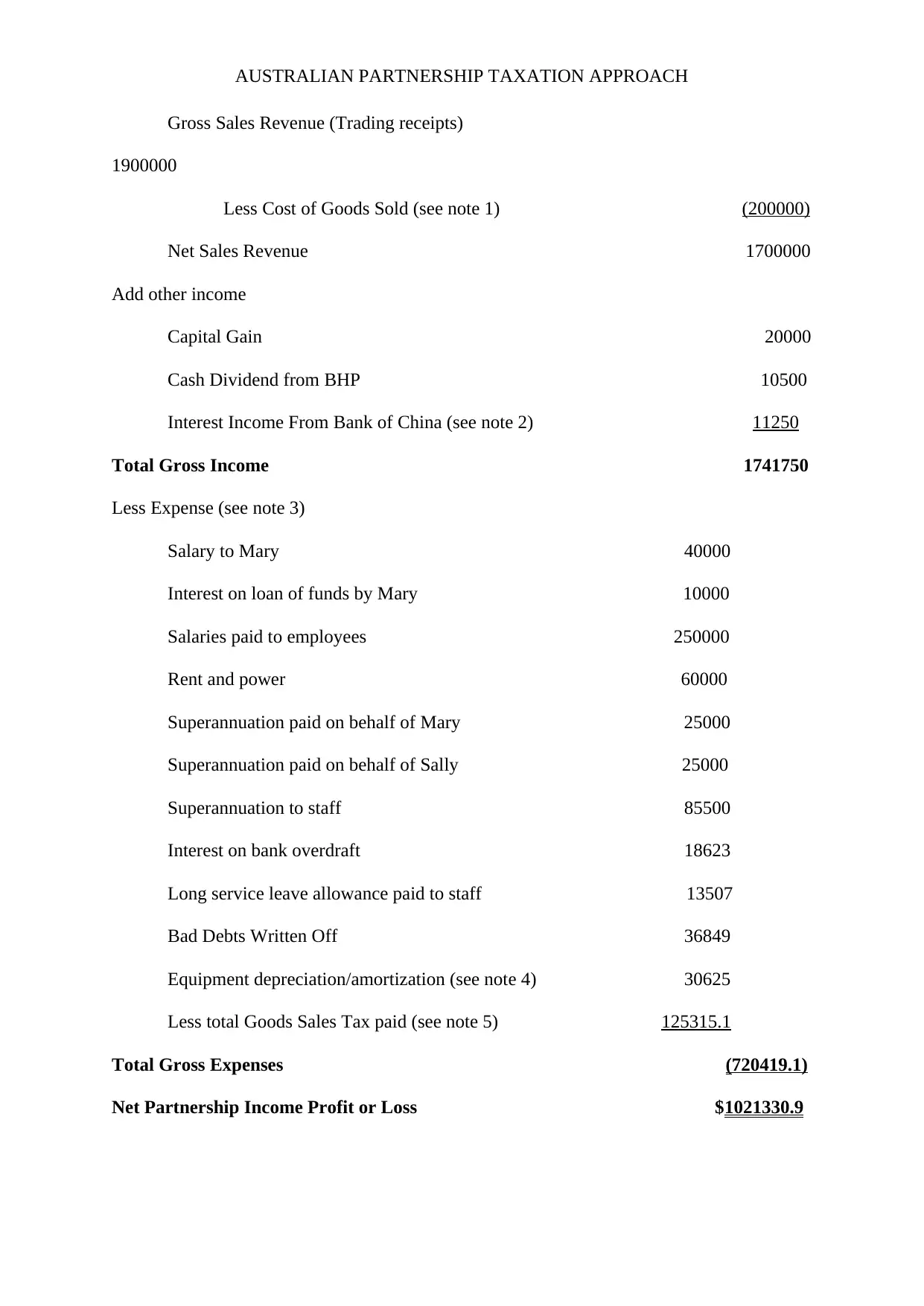

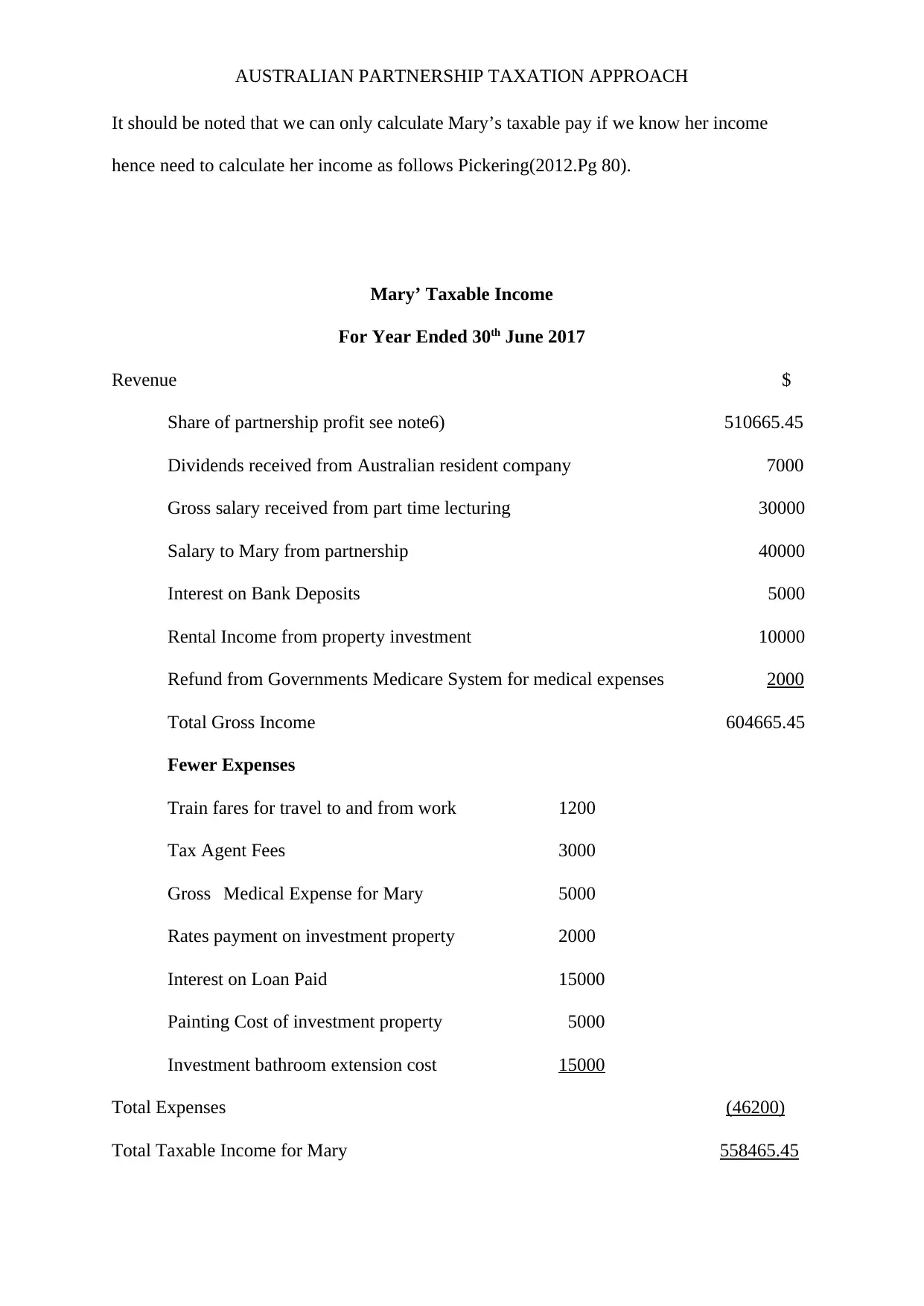

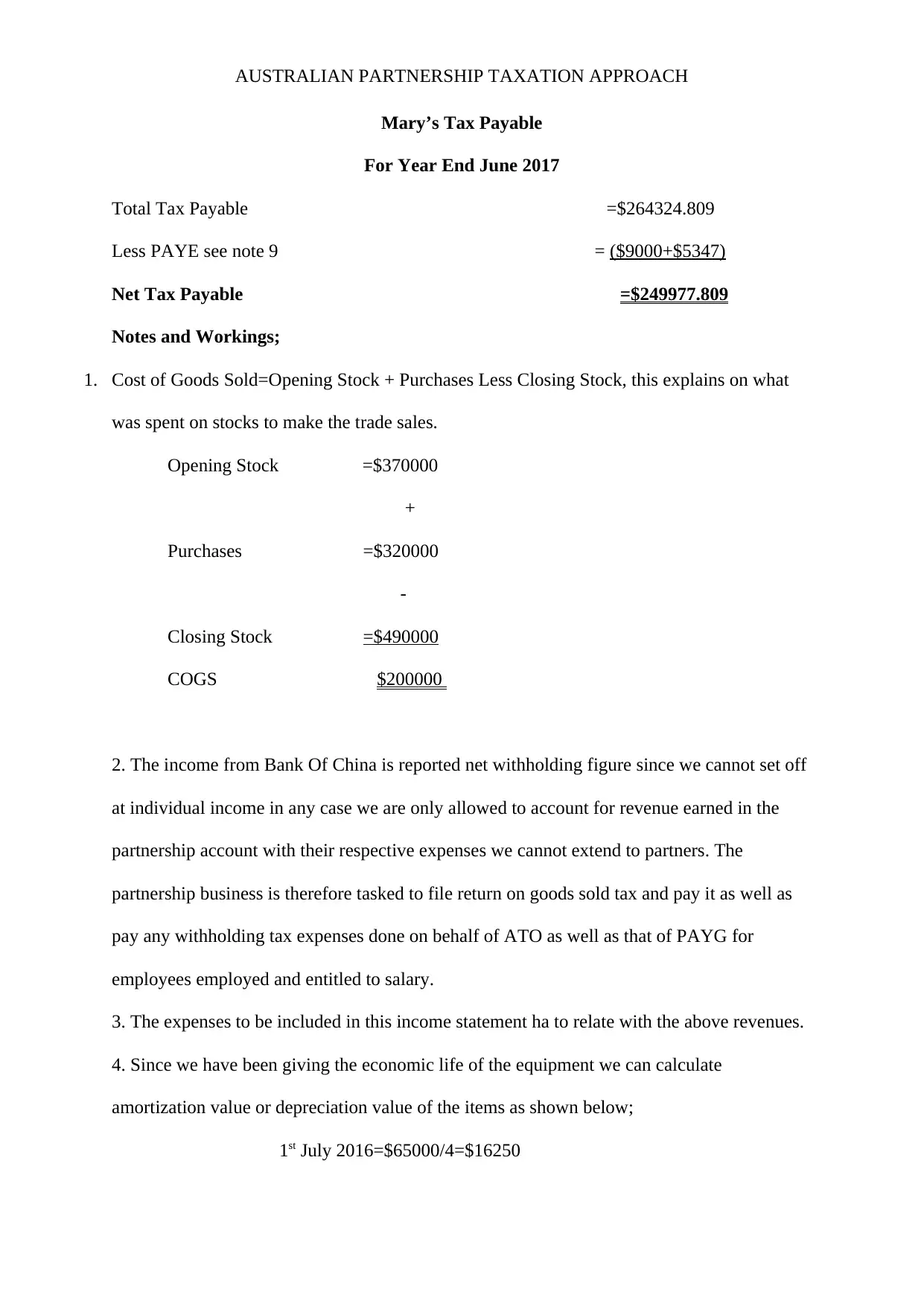

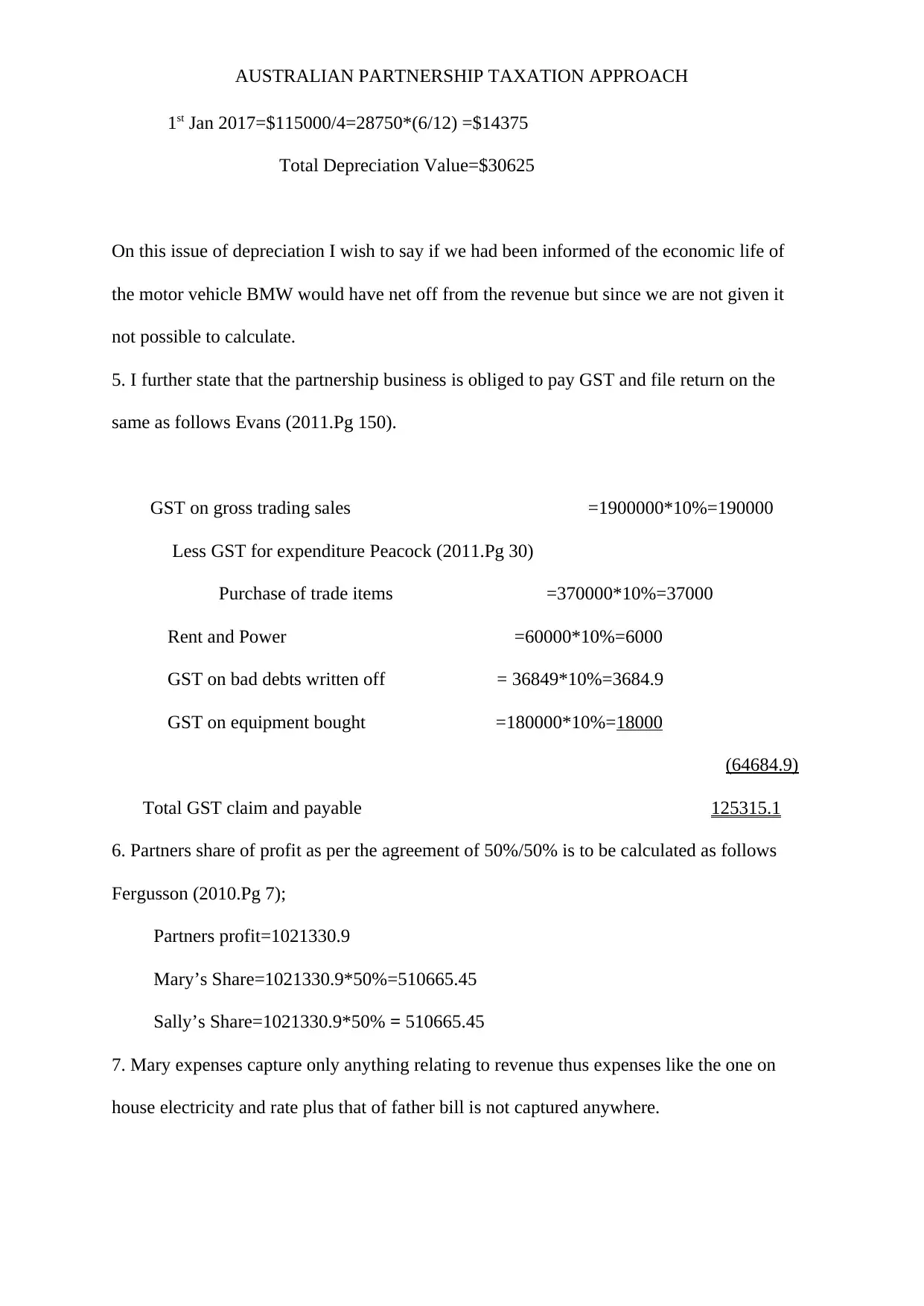

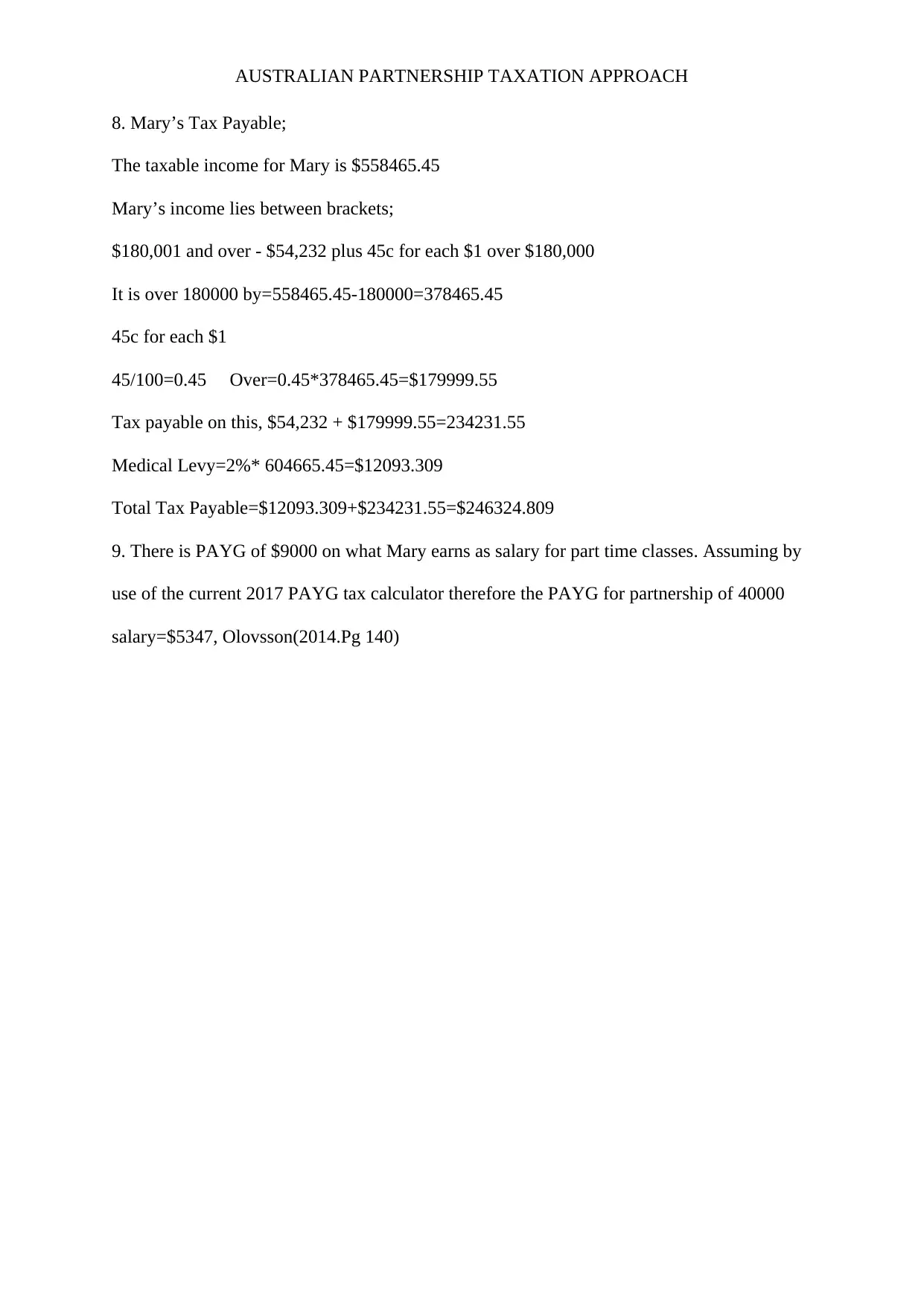

This assignment provides a detailed analysis of Australian partnership taxation, focusing on 'The Two B's' partnership. It includes the preparation of an income statement, calculation of net partnership profit or loss, and a breakdown of Mary's taxable income and tax payable. The document outlines revenue sources such as gross sales, other income (capital gains, dividends, interest), and various expenses including cost of goods sold, salaries, rent, depreciation, and GST. The analysis includes detailed notes and workings for each calculation, such as cost of goods sold, GST calculation, and depreciation. Furthermore, it calculates Mary's share of the partnership profit, her total taxable income, and ultimately, her tax payable, incorporating various income sources and allowable deductions. References to relevant accounting standards and tax regulations are also provided.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.