University Financial Statement Analysis of API Ltd: Report

VerifiedAdded on 2023/06/05

|21

|4804

|458

Report

AI Summary

This report provides a comprehensive financial statement analysis of Australian Pharmaceuticals Industries Ltd (API Ltd), examining its performance over a five-year period. The analysis employs trend analysis, various accounting tools, and ratio analysis to assess the company's growth and financial health. It delves into macroeconomic factors, including government regulations and demographic trends, and their impact on API Ltd's operations. Industry and business strategy analyses, along with Porter's Five Forces model, are used to evaluate the company's competitive landscape. The report explores liquidity, solvency, activity, and profitability ratios, such as current ratio, quick ratio, return on equity, and asset turnover, to provide insights into API Ltd's financial risk and cash flow management. The study highlights key findings and implications of each ratio, offering a detailed overview of the company's financial position and performance trends. The report concludes with a discussion of the significant factors affecting profit margins, including selling, general, warehousing, and financial expenses, and suggests strategic recommendations for improvement.

Running head: FINANCIAL STATEMENT ANALYSIS

Financial Statement Analysis

Name of the Student:

Name of the University:

Author’s Note:

Word Count: 2100 words.

Financial Statement Analysis

Name of the Student:

Name of the University:

Author’s Note:

Word Count: 2100 words.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL STATEMENT ANALYSIS

Executive Summary

The aim of the report is to show the changes in the company’s financial statement over the five year

horizon period. The financial review of the company have been performed using trend analysis and

various accounting tools. The ratio analysis and percentage analysis of the company provides an

oversight of the company’s trend in growth and performance of the company. The project also tells

about the various changes in the economy and sector and its influence on company’s operations. The

financial risk analysis along with the cash flow management of the company using ratio analysis.

Executive Summary

The aim of the report is to show the changes in the company’s financial statement over the five year

horizon period. The financial review of the company have been performed using trend analysis and

various accounting tools. The ratio analysis and percentage analysis of the company provides an

oversight of the company’s trend in growth and performance of the company. The project also tells

about the various changes in the economy and sector and its influence on company’s operations. The

financial risk analysis along with the cash flow management of the company using ratio analysis.

2FINANCIAL STATEMENT ANALYSIS

Introduction

The Australian Pharmaceuticals Industries Ltd operates in the pharmaceuticals sector. There

were several oversight given into the company. The study of the report is outlined in our assignment.

Macro-Economic Analysis was carried for determining the conditions and factors under which the

company operates. There are certain government rules and regulations, demographic trend and level

of disposable income factors which are discussed in the macroeconomic section.

Through this detailed study of the macro-economic conditions we get to know that the

company may face hurdles in the upcoming five year of horizon time period due to strict rules and

regulations of the government. The company may be able to deliver superior returns in contrast to its

superiors if the company increase the operational and efficiency level of the operations of the

company. The company’s industry and business strategy analysis was performed to analyse the

operations of the company. As part of the Industry Analysis and Business strategy the position of the

company’s product and portfolio analysis was performed (Cook 2016).

The report also shows the conducted accounting analysis and ratio analysis performed where

the financials and operations of the company shows stable and less volatility.

Discussion

Macro-Economic Policy

Macro-Economic Policy, Industry and Business Factors influence the working conditions of a

company. These factors directly and indirectly impacts the company’s operations, it is essential to

know the factors as these are reflected rough the fundamentals and financials of the company. The

Australian Pharmaceuticals Ltd is having the largest market share in wholesale distribution of

pharmaceuticals and other health care products (Borio 2014). The financial report for the company of

2017 shows the revenue segment analysis where the company has majority of its revenue earning

around 95% from Australia and other from New Zealand. The Australian Government policy changes

could influence significantly company’s operations. Certain regulatory reforms, policy and procedures

Introduction

The Australian Pharmaceuticals Industries Ltd operates in the pharmaceuticals sector. There

were several oversight given into the company. The study of the report is outlined in our assignment.

Macro-Economic Analysis was carried for determining the conditions and factors under which the

company operates. There are certain government rules and regulations, demographic trend and level

of disposable income factors which are discussed in the macroeconomic section.

Through this detailed study of the macro-economic conditions we get to know that the

company may face hurdles in the upcoming five year of horizon time period due to strict rules and

regulations of the government. The company may be able to deliver superior returns in contrast to its

superiors if the company increase the operational and efficiency level of the operations of the

company. The company’s industry and business strategy analysis was performed to analyse the

operations of the company. As part of the Industry Analysis and Business strategy the position of the

company’s product and portfolio analysis was performed (Cook 2016).

The report also shows the conducted accounting analysis and ratio analysis performed where

the financials and operations of the company shows stable and less volatility.

Discussion

Macro-Economic Policy

Macro-Economic Policy, Industry and Business Factors influence the working conditions of a

company. These factors directly and indirectly impacts the company’s operations, it is essential to

know the factors as these are reflected rough the fundamentals and financials of the company. The

Australian Pharmaceuticals Ltd is having the largest market share in wholesale distribution of

pharmaceuticals and other health care products (Borio 2014). The financial report for the company of

2017 shows the revenue segment analysis where the company has majority of its revenue earning

around 95% from Australia and other from New Zealand. The Australian Government policy changes

could influence significantly company’s operations. Certain regulatory reforms, policy and procedures

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL STATEMENT ANALYSIS

have severally impacted the company operation from the year 2015, the demand for branded products

was affected by the introduction of Pharmaceutical Benefit scheme (P.B.S) where customers prefer

switching to generic products. The demographic trend for the company are useful as the elderly

population of Australia is growing. The Australian elderly population is APL biggest market. The

future income growth for the company depend on the disposable income and the consumer spending.

Increase in household disposable income and gross earnings will have a positive impact and influence

on the company (Mankiw 2014).

Business and Industry Analysis

The company has an improved focus on one of the brand which is the Priceline brand for

making it a market leader in the beauty, healthcare and well-being retailer. The company strong

network growth and market share has appositive influence on the operations of the company. The

Industry analysis of the company was performed by using porter’s five force model where we found

that the company was in a cut throat competition with its competitors and its influence on the price or

dominance was quite low. Porter five force analysis gives a brief idea about the industry analysis

(Dobbsv 2014).

Porter’s Five Force Analysis

Rivalry Among

Existing Firms:

High

Threats of New

Entry : Medium

Threats of

Substitute Products:

Low

Bargaining Power

of customers: High

Bargaining Power

of Suppliers:

Medium

have severally impacted the company operation from the year 2015, the demand for branded products

was affected by the introduction of Pharmaceutical Benefit scheme (P.B.S) where customers prefer

switching to generic products. The demographic trend for the company are useful as the elderly

population of Australia is growing. The Australian elderly population is APL biggest market. The

future income growth for the company depend on the disposable income and the consumer spending.

Increase in household disposable income and gross earnings will have a positive impact and influence

on the company (Mankiw 2014).

Business and Industry Analysis

The company has an improved focus on one of the brand which is the Priceline brand for

making it a market leader in the beauty, healthcare and well-being retailer. The company strong

network growth and market share has appositive influence on the operations of the company. The

Industry analysis of the company was performed by using porter’s five force model where we found

that the company was in a cut throat competition with its competitors and its influence on the price or

dominance was quite low. Porter five force analysis gives a brief idea about the industry analysis

(Dobbsv 2014).

Porter’s Five Force Analysis

Rivalry Among

Existing Firms:

High

Threats of New

Entry : Medium

Threats of

Substitute Products:

Low

Bargaining Power

of customers: High

Bargaining Power

of Suppliers:

Medium

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL STATEMENT ANALYSIS

Ratio Analysis

Ratio Analysis provides a trend analysis of the company’s financial operations and it’s also provides

investors with important details of company’s financials. The return on equity is the ratio, which has

been emphasized a lot because it indicates the performance of the company. The ratio is calculated as

a percentage of net income in contrast to the shareholders equity of a company. The ratio analysis was

done on the basis of five year trend analysis and the implications of each ratio on the financials and

workings of the company.

Liquidity Ratio

The ratio measure a company ability for meeting up and paying of the short term obligations of the

company. The liquidity ratio for the company has remained stable this shows that the company is

efficiently utilising the current assets of the company (Law 2018).

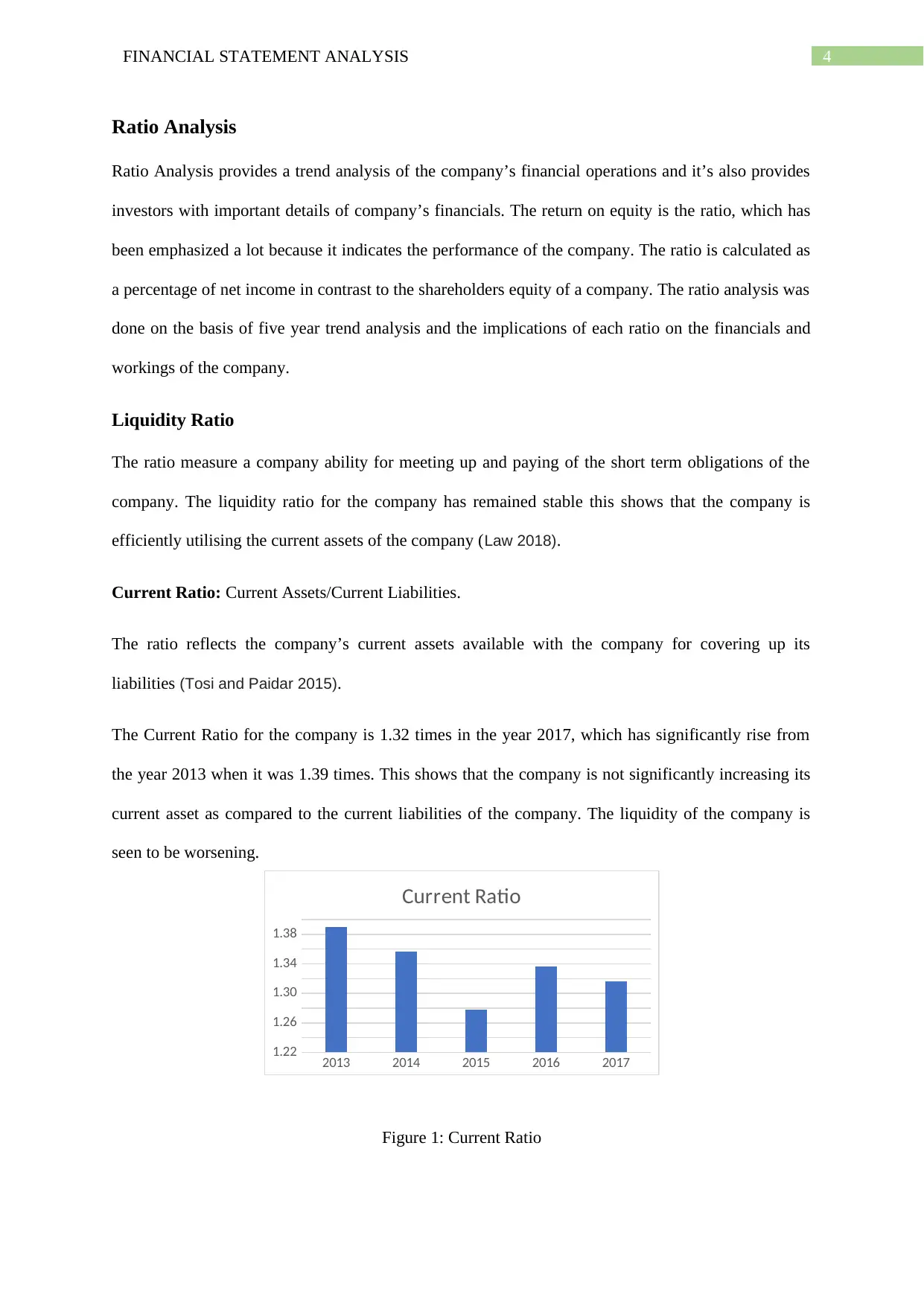

Current Ratio: Current Assets/Current Liabilities.

The ratio reflects the company’s current assets available with the company for covering up its

liabilities (Tosi and Paidar 2015).

The Current Ratio for the company is 1.32 times in the year 2017, which has significantly rise from

the year 2013 when it was 1.39 times. This shows that the company is not significantly increasing its

current asset as compared to the current liabilities of the company. The liquidity of the company is

seen to be worsening.

Figure 1: Current Ratio

2013 2014 2015 2016 2017

1.22

1.26

1.30

1.34

1.38

Current Ratio

Ratio Analysis

Ratio Analysis provides a trend analysis of the company’s financial operations and it’s also provides

investors with important details of company’s financials. The return on equity is the ratio, which has

been emphasized a lot because it indicates the performance of the company. The ratio is calculated as

a percentage of net income in contrast to the shareholders equity of a company. The ratio analysis was

done on the basis of five year trend analysis and the implications of each ratio on the financials and

workings of the company.

Liquidity Ratio

The ratio measure a company ability for meeting up and paying of the short term obligations of the

company. The liquidity ratio for the company has remained stable this shows that the company is

efficiently utilising the current assets of the company (Law 2018).

Current Ratio: Current Assets/Current Liabilities.

The ratio reflects the company’s current assets available with the company for covering up its

liabilities (Tosi and Paidar 2015).

The Current Ratio for the company is 1.32 times in the year 2017, which has significantly rise from

the year 2013 when it was 1.39 times. This shows that the company is not significantly increasing its

current asset as compared to the current liabilities of the company. The liquidity of the company is

seen to be worsening.

Figure 1: Current Ratio

2013 2014 2015 2016 2017

1.22

1.26

1.30

1.34

1.38

Current Ratio

5FINANCIAL STATEMENT ANALYSIS

Source: Appendix 1

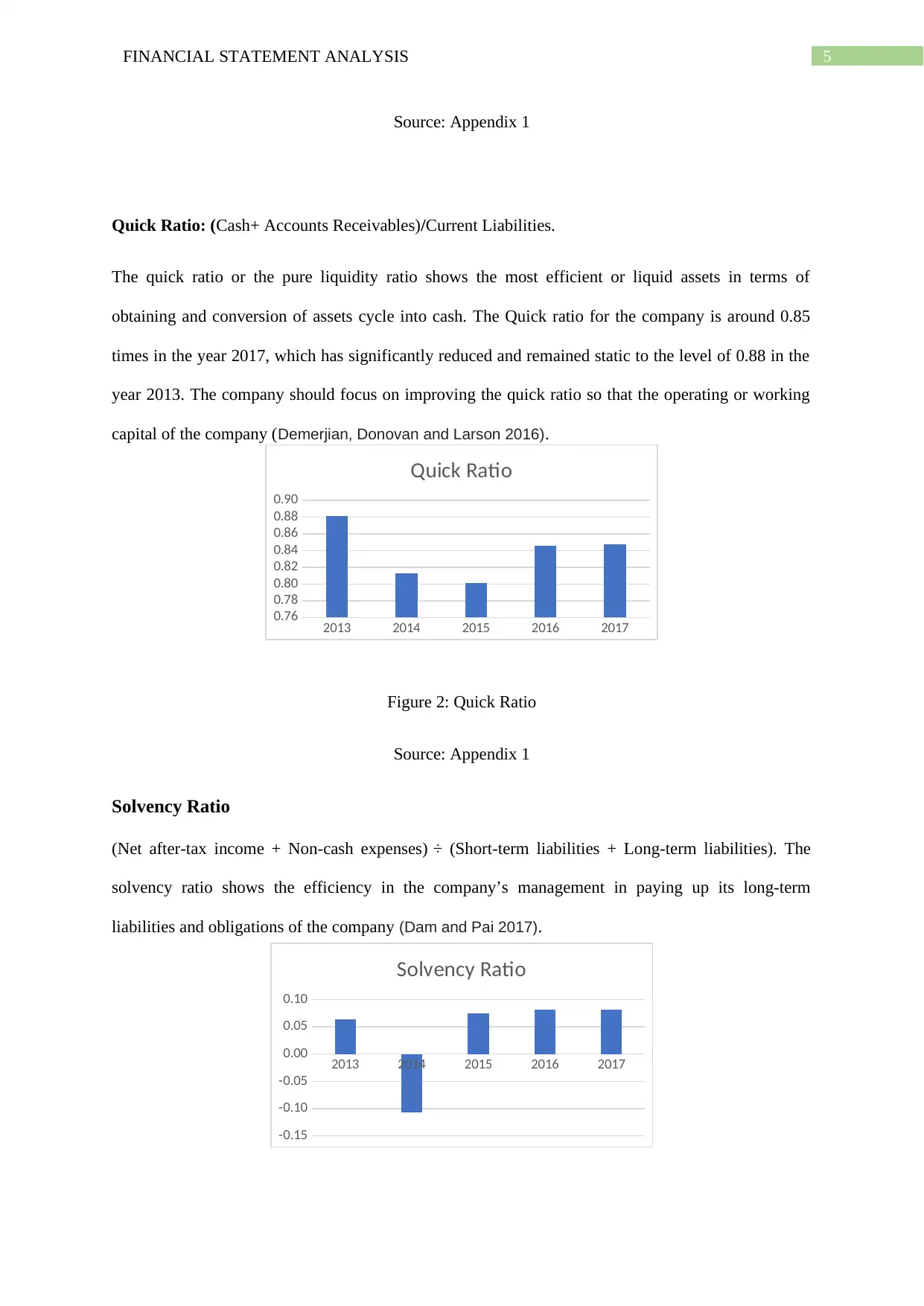

Quick Ratio: (Cash+ Accounts Receivables)/Current Liabilities.

The quick ratio or the pure liquidity ratio shows the most efficient or liquid assets in terms of

obtaining and conversion of assets cycle into cash. The Quick ratio for the company is around 0.85

times in the year 2017, which has significantly reduced and remained static to the level of 0.88 in the

year 2013. The company should focus on improving the quick ratio so that the operating or working

capital of the company (Demerjian, Donovan and Larson 2016).

Figure 2: Quick Ratio

Source: Appendix 1

Solvency Ratio

(Net after-tax income + Non-cash expenses) ÷ (Short-term liabilities + Long-term liabilities). The

solvency ratio shows the efficiency in the company’s management in paying up its long-term

liabilities and obligations of the company (Dam and Pai 2017).

2013 2014 2015 2016 2017

0.76

0.78

0.80

0.82

0.84

0.86

0.88

0.90

Quick Ratio

2013 2014 2015 2016 2017

-0.15

-0.10

-0.05

0.00

0.05

0.10

Solvency Ratio

Source: Appendix 1

Quick Ratio: (Cash+ Accounts Receivables)/Current Liabilities.

The quick ratio or the pure liquidity ratio shows the most efficient or liquid assets in terms of

obtaining and conversion of assets cycle into cash. The Quick ratio for the company is around 0.85

times in the year 2017, which has significantly reduced and remained static to the level of 0.88 in the

year 2013. The company should focus on improving the quick ratio so that the operating or working

capital of the company (Demerjian, Donovan and Larson 2016).

Figure 2: Quick Ratio

Source: Appendix 1

Solvency Ratio

(Net after-tax income + Non-cash expenses) ÷ (Short-term liabilities + Long-term liabilities). The

solvency ratio shows the efficiency in the company’s management in paying up its long-term

liabilities and obligations of the company (Dam and Pai 2017).

2013 2014 2015 2016 2017

0.76

0.78

0.80

0.82

0.84

0.86

0.88

0.90

Quick Ratio

2013 2014 2015 2016 2017

-0.15

-0.10

-0.05

0.00

0.05

0.10

Solvency Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL STATEMENT ANALYSIS

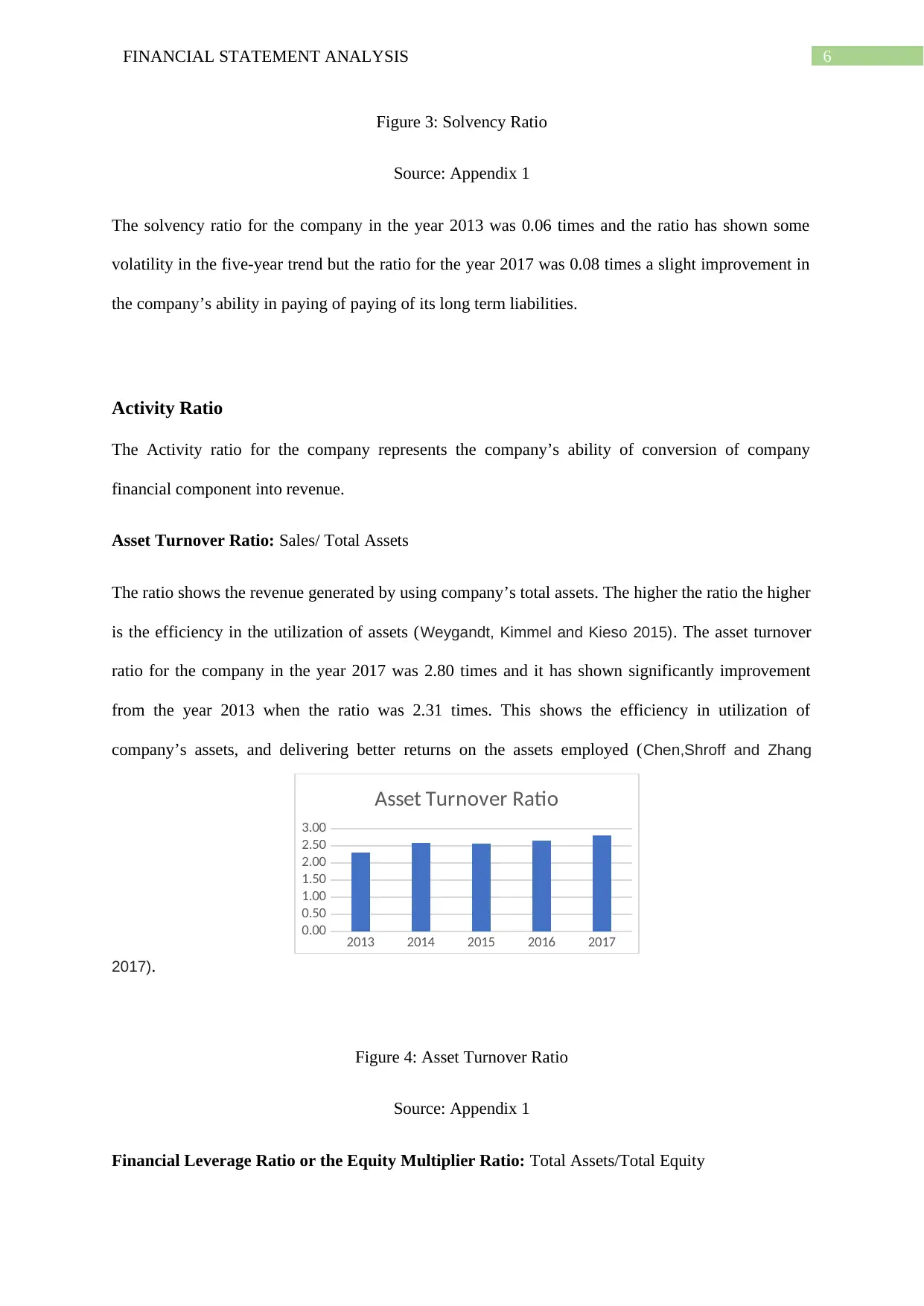

Figure 3: Solvency Ratio

Source: Appendix 1

The solvency ratio for the company in the year 2013 was 0.06 times and the ratio has shown some

volatility in the five-year trend but the ratio for the year 2017 was 0.08 times a slight improvement in

the company’s ability in paying of paying of its long term liabilities.

Activity Ratio

The Activity ratio for the company represents the company’s ability of conversion of company

financial component into revenue.

Asset Turnover Ratio: Sales/ Total Assets

The ratio shows the revenue generated by using company’s total assets. The higher the ratio the higher

is the efficiency in the utilization of assets (Weygandt, Kimmel and Kieso 2015). The asset turnover

ratio for the company in the year 2017 was 2.80 times and it has shown significantly improvement

from the year 2013 when the ratio was 2.31 times. This shows the efficiency in utilization of

company’s assets, and delivering better returns on the assets employed (Chen,Shroff and Zhang

2017).

Figure 4: Asset Turnover Ratio

Source: Appendix 1

Financial Leverage Ratio or the Equity Multiplier Ratio: Total Assets/Total Equity

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Asset Turnover Ratio

Figure 3: Solvency Ratio

Source: Appendix 1

The solvency ratio for the company in the year 2013 was 0.06 times and the ratio has shown some

volatility in the five-year trend but the ratio for the year 2017 was 0.08 times a slight improvement in

the company’s ability in paying of paying of its long term liabilities.

Activity Ratio

The Activity ratio for the company represents the company’s ability of conversion of company

financial component into revenue.

Asset Turnover Ratio: Sales/ Total Assets

The ratio shows the revenue generated by using company’s total assets. The higher the ratio the higher

is the efficiency in the utilization of assets (Weygandt, Kimmel and Kieso 2015). The asset turnover

ratio for the company in the year 2017 was 2.80 times and it has shown significantly improvement

from the year 2013 when the ratio was 2.31 times. This shows the efficiency in utilization of

company’s assets, and delivering better returns on the assets employed (Chen,Shroff and Zhang

2017).

Figure 4: Asset Turnover Ratio

Source: Appendix 1

Financial Leverage Ratio or the Equity Multiplier Ratio: Total Assets/Total Equity

2013 2014 2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Asset Turnover Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STATEMENT ANALYSIS

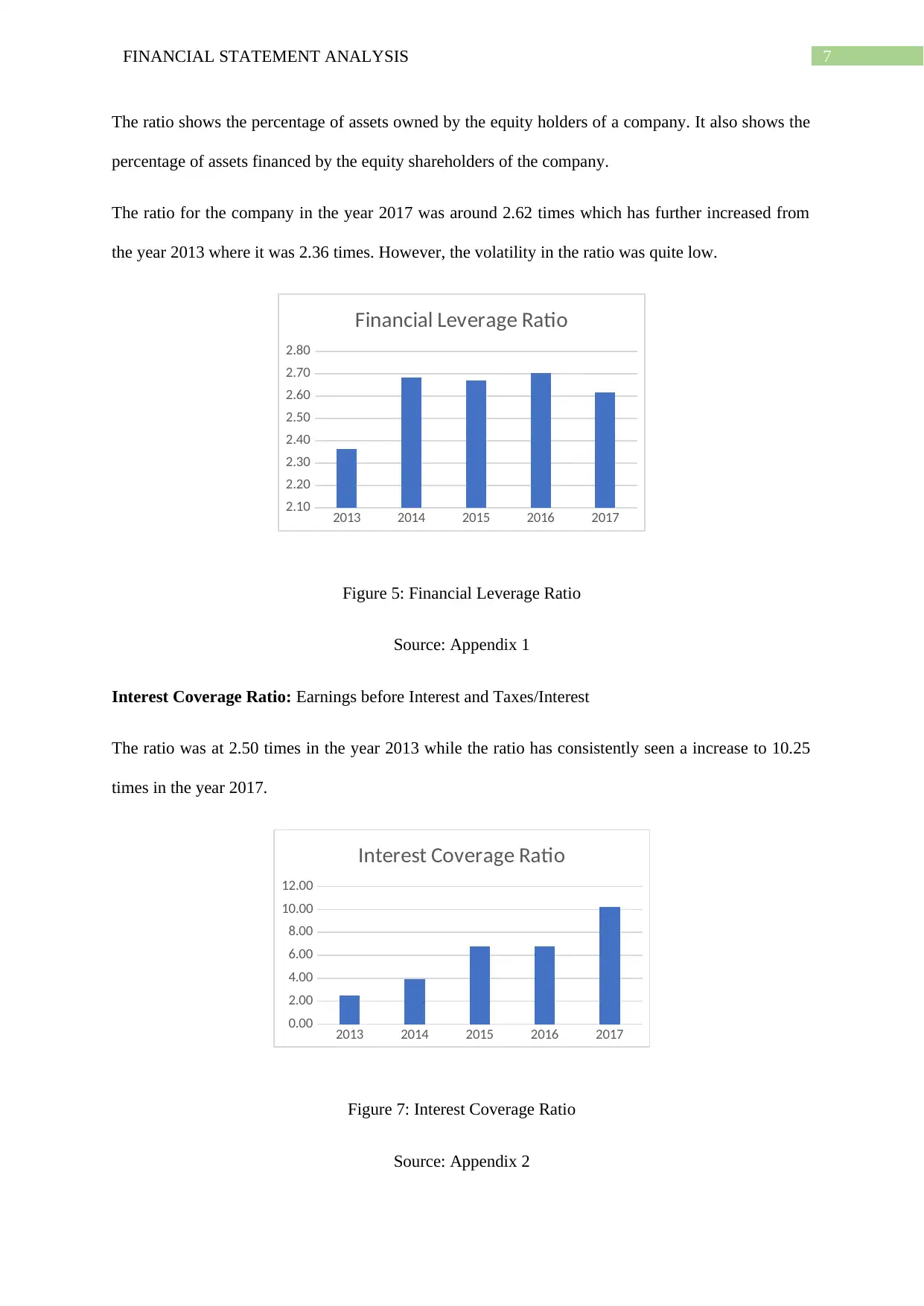

The ratio shows the percentage of assets owned by the equity holders of a company. It also shows the

percentage of assets financed by the equity shareholders of the company.

The ratio for the company in the year 2017 was around 2.62 times which has further increased from

the year 2013 where it was 2.36 times. However, the volatility in the ratio was quite low.

Figure 5: Financial Leverage Ratio

Source: Appendix 1

Interest Coverage Ratio: Earnings before Interest and Taxes/Interest

The ratio was at 2.50 times in the year 2013 while the ratio has consistently seen a increase to 10.25

times in the year 2017.

Figure 7: Interest Coverage Ratio

Source: Appendix 2

2013 2014 2015 2016 2017

2.10

2.20

2.30

2.40

2.50

2.60

2.70

2.80

Financial Leverage Ratio

2013 2014 2015 2016 2017

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Interest Coverage Ratio

The ratio shows the percentage of assets owned by the equity holders of a company. It also shows the

percentage of assets financed by the equity shareholders of the company.

The ratio for the company in the year 2017 was around 2.62 times which has further increased from

the year 2013 where it was 2.36 times. However, the volatility in the ratio was quite low.

Figure 5: Financial Leverage Ratio

Source: Appendix 1

Interest Coverage Ratio: Earnings before Interest and Taxes/Interest

The ratio was at 2.50 times in the year 2013 while the ratio has consistently seen a increase to 10.25

times in the year 2017.

Figure 7: Interest Coverage Ratio

Source: Appendix 2

2013 2014 2015 2016 2017

2.10

2.20

2.30

2.40

2.50

2.60

2.70

2.80

Financial Leverage Ratio

2013 2014 2015 2016 2017

0.00

2.00

4.00

6.00

8.00

10.00

12.00

Interest Coverage Ratio

8FINANCIAL STATEMENT ANALYSIS

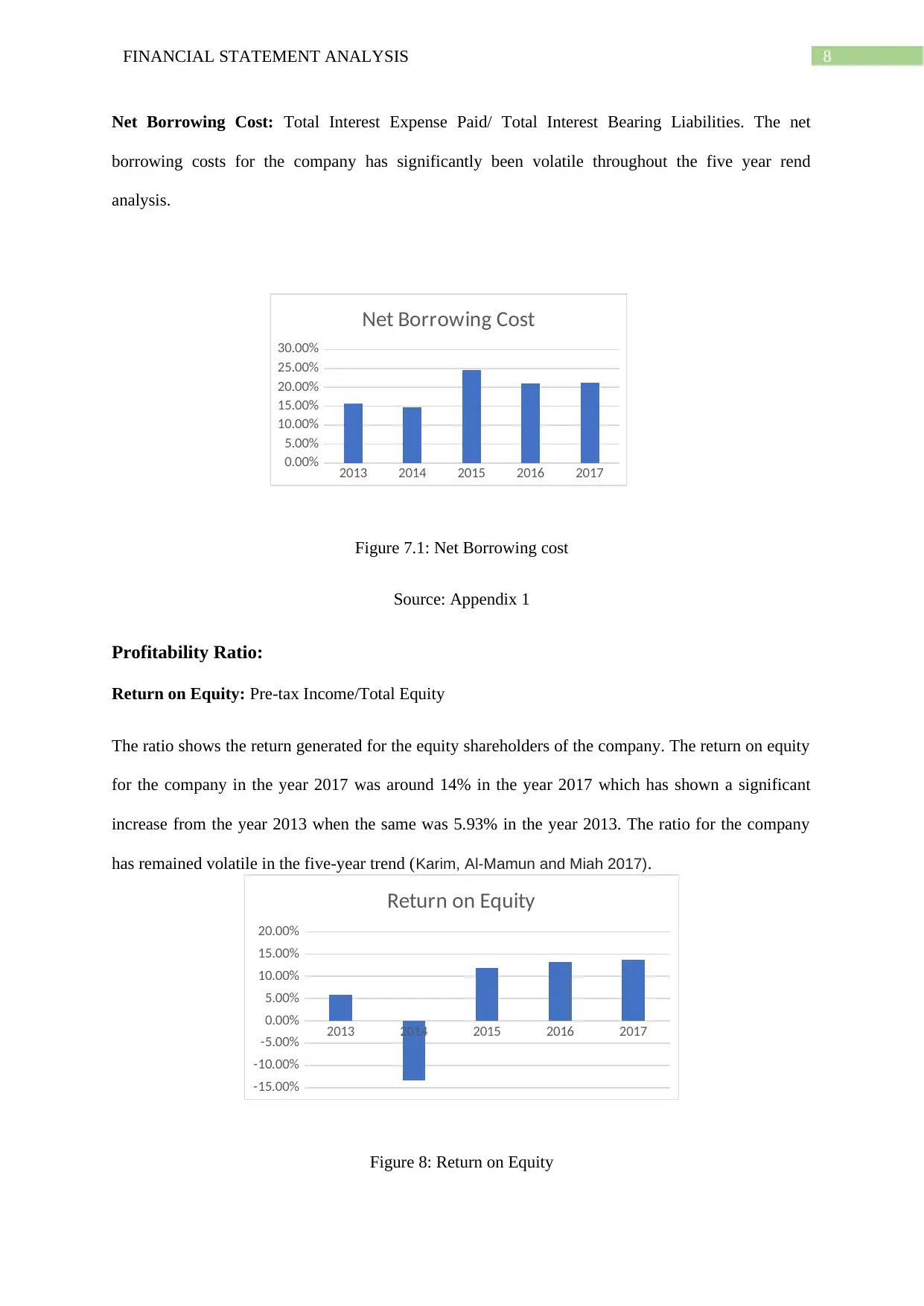

Net Borrowing Cost: Total Interest Expense Paid/ Total Interest Bearing Liabilities. The net

borrowing costs for the company has significantly been volatile throughout the five year rend

analysis.

Figure 7.1: Net Borrowing cost

Source: Appendix 1

Profitability Ratio:

Return on Equity: Pre-tax Income/Total Equity

The ratio shows the return generated for the equity shareholders of the company. The return on equity

for the company in the year 2017 was around 14% in the year 2017 which has shown a significant

increase from the year 2013 when the same was 5.93% in the year 2013. The ratio for the company

has remained volatile in the five-year trend (Karim, Al-Mamun and Miah 2017).

Figure 8: Return on Equity

2013 2014 2015 2016 2017

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Return on Equity

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Net Borrowing Cost

Net Borrowing Cost: Total Interest Expense Paid/ Total Interest Bearing Liabilities. The net

borrowing costs for the company has significantly been volatile throughout the five year rend

analysis.

Figure 7.1: Net Borrowing cost

Source: Appendix 1

Profitability Ratio:

Return on Equity: Pre-tax Income/Total Equity

The ratio shows the return generated for the equity shareholders of the company. The return on equity

for the company in the year 2017 was around 14% in the year 2017 which has shown a significant

increase from the year 2013 when the same was 5.93% in the year 2013. The ratio for the company

has remained volatile in the five-year trend (Karim, Al-Mamun and Miah 2017).

Figure 8: Return on Equity

2013 2014 2015 2016 2017

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Return on Equity

2013 2014 2015 2016 2017

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Net Borrowing Cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL STATEMENT ANALYSIS

Source: Appendix 1

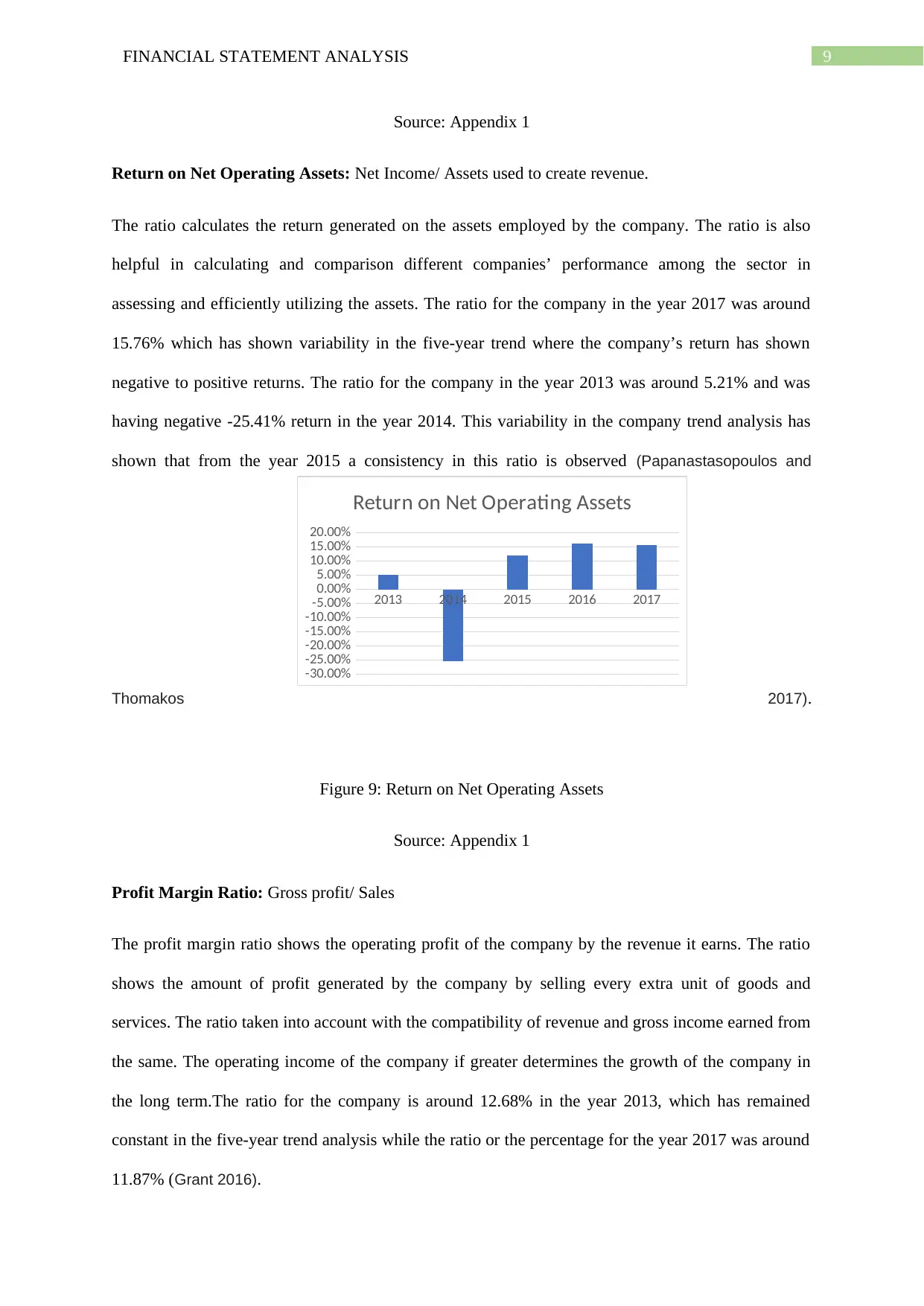

Return on Net Operating Assets: Net Income/ Assets used to create revenue.

The ratio calculates the return generated on the assets employed by the company. The ratio is also

helpful in calculating and comparison different companies’ performance among the sector in

assessing and efficiently utilizing the assets. The ratio for the company in the year 2017 was around

15.76% which has shown variability in the five-year trend where the company’s return has shown

negative to positive returns. The ratio for the company in the year 2013 was around 5.21% and was

having negative -25.41% return in the year 2014. This variability in the company trend analysis has

shown that from the year 2015 a consistency in this ratio is observed (Papanastasopoulos and

Thomakos 2017).

Figure 9: Return on Net Operating Assets

Source: Appendix 1

Profit Margin Ratio: Gross profit/ Sales

The profit margin ratio shows the operating profit of the company by the revenue it earns. The ratio

shows the amount of profit generated by the company by selling every extra unit of goods and

services. The ratio taken into account with the compatibility of revenue and gross income earned from

the same. The operating income of the company if greater determines the growth of the company in

the long term.The ratio for the company is around 12.68% in the year 2013, which has remained

constant in the five-year trend analysis while the ratio or the percentage for the year 2017 was around

11.87% (Grant 2016).

2013 2014 2015 2016 2017

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Return on Net Operating Assets

Source: Appendix 1

Return on Net Operating Assets: Net Income/ Assets used to create revenue.

The ratio calculates the return generated on the assets employed by the company. The ratio is also

helpful in calculating and comparison different companies’ performance among the sector in

assessing and efficiently utilizing the assets. The ratio for the company in the year 2017 was around

15.76% which has shown variability in the five-year trend where the company’s return has shown

negative to positive returns. The ratio for the company in the year 2013 was around 5.21% and was

having negative -25.41% return in the year 2014. This variability in the company trend analysis has

shown that from the year 2015 a consistency in this ratio is observed (Papanastasopoulos and

Thomakos 2017).

Figure 9: Return on Net Operating Assets

Source: Appendix 1

Profit Margin Ratio: Gross profit/ Sales

The profit margin ratio shows the operating profit of the company by the revenue it earns. The ratio

shows the amount of profit generated by the company by selling every extra unit of goods and

services. The ratio taken into account with the compatibility of revenue and gross income earned from

the same. The operating income of the company if greater determines the growth of the company in

the long term.The ratio for the company is around 12.68% in the year 2013, which has remained

constant in the five-year trend analysis while the ratio or the percentage for the year 2017 was around

11.87% (Grant 2016).

2013 2014 2015 2016 2017

-30.00%

-25.00%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Return on Net Operating Assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL STATEMENT ANALYSIS

Figure 10: Profit Margin

Source: Appendix 1

Analysis of Profit Margin

The three significant items which have caused major changes in the profit margin are selling

and general expense are the most important and constituent form of income statement and influences

the profit margin by almost 80%. The company’s net profit gets affected due to expenses warehousing

and distributing expenses, marketing and sales expense and other general expenses. The other is the

financial expenses which the company spends on the debt borrowing it has. The company should try

to reduce these expenses by financing with equity method which will help save interest or borrowing

costs for the company. The income tax expenses for the company depends on the statutory tax rate,

which is not always the same as the effective tax rate. It occurs due to the creation of deferred tax

assets and liabilities created in the books of the companies. The income tax rate and the effective tax

rate for the company has been in the range of approximately 27% with a slight volatility of around 5%

(Appendix 2). The company should focus on tax saving benefits like introduction of debt financing

when the company is in high tax bracket, when the company is having a minimal or no risk in debt

financing (Heikal, Khaddafi and Ummah 2014).

Analysis of Assets and Liabilities

Three major assets and liabilities whose turnover ratio have contributed to the overall change

in the assets efficiency is the fixed assets of the company i.e., plant and machinery which have

reduced by around 5% from 2016-2017 but the increase in the revenue was at the same time observed

2013 2014 2015 2016 2017

11.20%

11.40%

11.60%

11.80%

12.00%

12.20%

12.40%

12.60%

12.80%

13.00%

13.20%

Profit Margin

Figure 10: Profit Margin

Source: Appendix 1

Analysis of Profit Margin

The three significant items which have caused major changes in the profit margin are selling

and general expense are the most important and constituent form of income statement and influences

the profit margin by almost 80%. The company’s net profit gets affected due to expenses warehousing

and distributing expenses, marketing and sales expense and other general expenses. The other is the

financial expenses which the company spends on the debt borrowing it has. The company should try

to reduce these expenses by financing with equity method which will help save interest or borrowing

costs for the company. The income tax expenses for the company depends on the statutory tax rate,

which is not always the same as the effective tax rate. It occurs due to the creation of deferred tax

assets and liabilities created in the books of the companies. The income tax rate and the effective tax

rate for the company has been in the range of approximately 27% with a slight volatility of around 5%

(Appendix 2). The company should focus on tax saving benefits like introduction of debt financing

when the company is in high tax bracket, when the company is having a minimal or no risk in debt

financing (Heikal, Khaddafi and Ummah 2014).

Analysis of Assets and Liabilities

Three major assets and liabilities whose turnover ratio have contributed to the overall change

in the assets efficiency is the fixed assets of the company i.e., plant and machinery which have

reduced by around 5% from 2016-2017 but the increase in the revenue was at the same time observed

2013 2014 2015 2016 2017

11.20%

11.40%

11.60%

11.80%

12.00%

12.20%

12.40%

12.60%

12.80%

13.00%

13.20%

Profit Margin

11FINANCIAL STATEMENT ANALYSIS

to be around 5.26%. This shows that the company has shown efficiency in production and revenue

generation (Appendix 3). The trade and other receivable which has reduced by 1.12% from the year

shows the management has started focusing on the efficiency of this particular asset. While if we see

at the liability side from the year 2013-2017 the company has reduced the loans and borrowing and

long term debt of the company significantly which has let the company reduce financial risks and

reduce interest expense a significant component of income statement (Panigrahi and Sharma 2016).

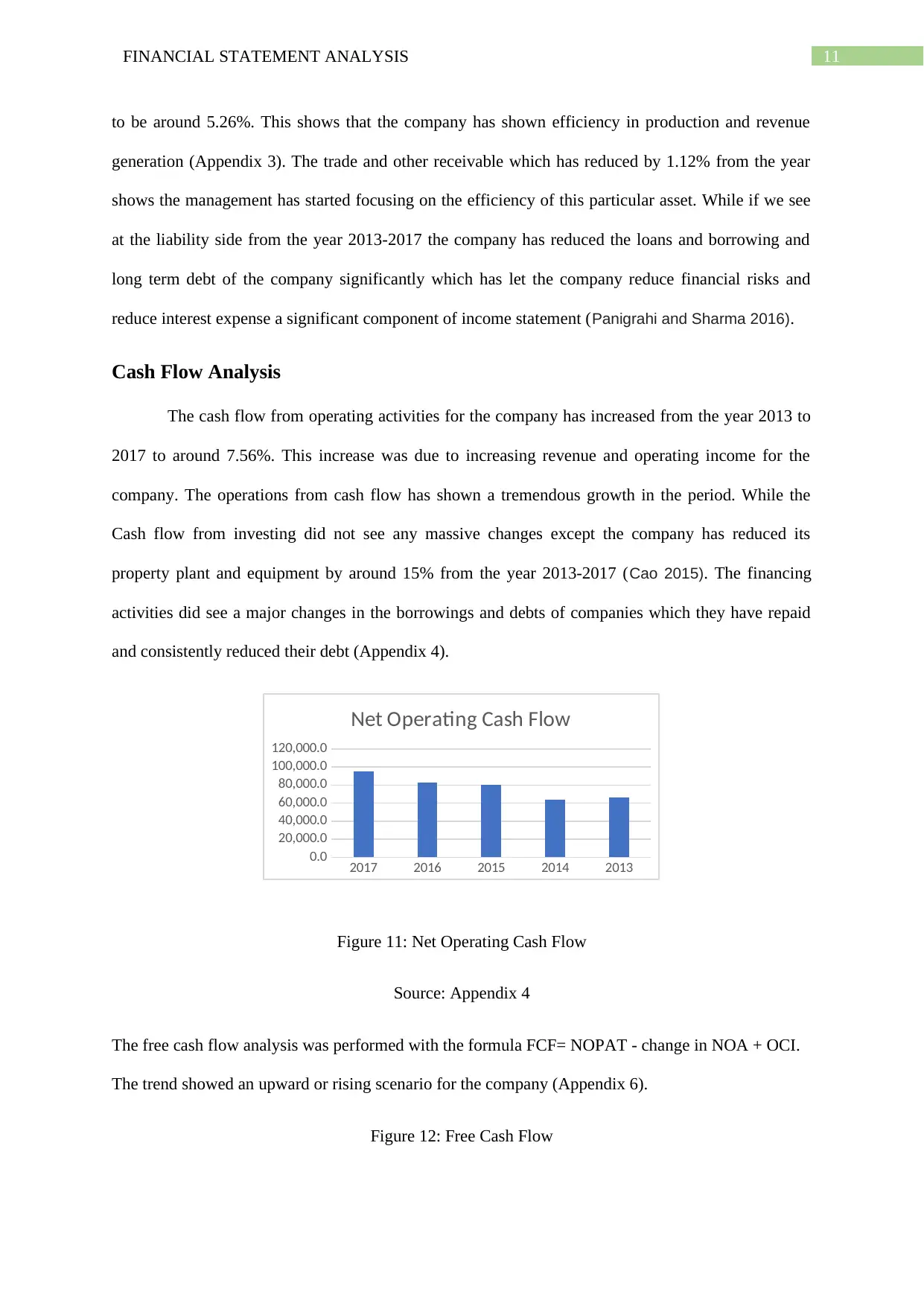

Cash Flow Analysis

The cash flow from operating activities for the company has increased from the year 2013 to

2017 to around 7.56%. This increase was due to increasing revenue and operating income for the

company. The operations from cash flow has shown a tremendous growth in the period. While the

Cash flow from investing did not see any massive changes except the company has reduced its

property plant and equipment by around 15% from the year 2013-2017 (Cao 2015). The financing

activities did see a major changes in the borrowings and debts of companies which they have repaid

and consistently reduced their debt (Appendix 4).

Figure 11: Net Operating Cash Flow

Source: Appendix 4

The free cash flow analysis was performed with the formula FCF= NOPAT - change in NOA + OCI.

The trend showed an upward or rising scenario for the company (Appendix 6).

Figure 12: Free Cash Flow

2017 2016 2015 2014 2013

0.0

20,000.0

40,000.0

60,000.0

80,000.0

100,000.0

120,000.0

Net Operating Cash Flow

to be around 5.26%. This shows that the company has shown efficiency in production and revenue

generation (Appendix 3). The trade and other receivable which has reduced by 1.12% from the year

shows the management has started focusing on the efficiency of this particular asset. While if we see

at the liability side from the year 2013-2017 the company has reduced the loans and borrowing and

long term debt of the company significantly which has let the company reduce financial risks and

reduce interest expense a significant component of income statement (Panigrahi and Sharma 2016).

Cash Flow Analysis

The cash flow from operating activities for the company has increased from the year 2013 to

2017 to around 7.56%. This increase was due to increasing revenue and operating income for the

company. The operations from cash flow has shown a tremendous growth in the period. While the

Cash flow from investing did not see any massive changes except the company has reduced its

property plant and equipment by around 15% from the year 2013-2017 (Cao 2015). The financing

activities did see a major changes in the borrowings and debts of companies which they have repaid

and consistently reduced their debt (Appendix 4).

Figure 11: Net Operating Cash Flow

Source: Appendix 4

The free cash flow analysis was performed with the formula FCF= NOPAT - change in NOA + OCI.

The trend showed an upward or rising scenario for the company (Appendix 6).

Figure 12: Free Cash Flow

2017 2016 2015 2014 2013

0.0

20,000.0

40,000.0

60,000.0

80,000.0

100,000.0

120,000.0

Net Operating Cash Flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.