Comprehensive Analysis of Small Business Taxation Law in Australia

VerifiedAdded on 2020/06/06

|9

|2628

|32

Report

AI Summary

This report provides a detailed overview of taxation law as it pertains to small businesses in Australia. It begins with a definition of small businesses within the context of taxation law, considering factors such as company assets, employee structure, and turnover. The report then explores various tax treatments for business income, including cash and accrual accounting methods, foreign income, personal service income, and crowdfunding. It also examines tax treatments for income from properties, including capital gains. Furthermore, the report delves into tax offsets and deductions available to small businesses, such as the unincorporated small business tax discount and deductions for travel expenses, asset costs, and home-based businesses. The report concludes by outlining other tax concessions, including income tax concessions, CGT concessions, PAYG instalment concessions, FBT concessions, and GST and Excise concessions, providing a comprehensive guide to the tax landscape for small businesses in New South Wales.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1. Definition of small business in taxation law...........................................................................1

2. Tax treatments for income from business for small business.................................................2

4. Tax treatments for offsets and deductions for small businesses.............................................3

5. Other tax concessions for small business................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

1. Definition of small business in taxation law...........................................................................1

2. Tax treatments for income from business for small business.................................................2

4. Tax treatments for offsets and deductions for small businesses.............................................3

5. Other tax concessions for small business................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Taxation laws are mainly identified as legislations development by governing bodies and

parliament that relates to the treatments of tax which needs to be paid the every business

enterprise in countries (Main, 2016). It is also considered as governmental assessment on

property values, estates of the deceased, granting licences or income and import duties from for

overseas nations. It is usally charged by government on earnings of a individual, trust and

organization along with the value of property. In present scenario, taxation laws and act that

prevails under the NSW are studied and analysed in order to determine the meaning small

business enterprise under the taxation law. Further, analysis taxation administration act 1967 is

also done to identified the tax treatments for income earned by small business enterprise along

with the tax treatments for income from property.

1. Definition of small business in taxation law

Small business are generally defined as a structure that are not public companies or a

larger firm but in term of taxation law definition may differ which is based on assets of company,

employees structure, turnover, partnership of the firm etc.

Small business use cash method to make report of income and expenditure. Small business have

gross receipt of less than $10 million in three previous years. Small business accrue the bad debts

being anticipated. Small business can deduct the cost of capital improvement. Big firms has to

pay alternative minimum tax if it is more than their regular tax liability (Main, 2015). But small

businesses do not have to do so. They are being exempted from the same. Small businesses are

those which enjoys the advantage of hybrid retirement plan which is clubbed with pension plan.

Small business are those having five hundred or few employees. In large organisation the cost of

coverage is being included whether paid by the company or an employee while small firms are

exempted from this. They enjoy its advantage and are devoid of it. They are not required to give

welfare coverage to its employees. Some small businesses pay continue wages to the employees

can opt tax credit up-to some set limit.

1

Taxation laws are mainly identified as legislations development by governing bodies and

parliament that relates to the treatments of tax which needs to be paid the every business

enterprise in countries (Main, 2016). It is also considered as governmental assessment on

property values, estates of the deceased, granting licences or income and import duties from for

overseas nations. It is usally charged by government on earnings of a individual, trust and

organization along with the value of property. In present scenario, taxation laws and act that

prevails under the NSW are studied and analysed in order to determine the meaning small

business enterprise under the taxation law. Further, analysis taxation administration act 1967 is

also done to identified the tax treatments for income earned by small business enterprise along

with the tax treatments for income from property.

1. Definition of small business in taxation law

Small business are generally defined as a structure that are not public companies or a

larger firm but in term of taxation law definition may differ which is based on assets of company,

employees structure, turnover, partnership of the firm etc.

Small business use cash method to make report of income and expenditure. Small business have

gross receipt of less than $10 million in three previous years. Small business accrue the bad debts

being anticipated. Small business can deduct the cost of capital improvement. Big firms has to

pay alternative minimum tax if it is more than their regular tax liability (Main, 2015). But small

businesses do not have to do so. They are being exempted from the same. Small businesses are

those which enjoys the advantage of hybrid retirement plan which is clubbed with pension plan.

Small business are those having five hundred or few employees. In large organisation the cost of

coverage is being included whether paid by the company or an employee while small firms are

exempted from this. They enjoy its advantage and are devoid of it. They are not required to give

welfare coverage to its employees. Some small businesses pay continue wages to the employees

can opt tax credit up-to some set limit.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Tax treatments for income from business for small business

There are several accounting methods have been used by small business for treatments of

tax which is to paid on income earned from different sources. These accounting methods have

been taken that needs to be taken in to consideration. The amount which are included will need

to be assess-able income which in any financial year based on whether the account for income of

enterprise on cash basis or accruals basis.

Cash basis: As per taxation act 1967, if the organization is account for actionable income on the

basis of cash that they can include payments which they have earned at the time of financial year

regardless of the time on which they have accomplished the work (Williams, 2017). The

organization can only income which they have actually received from payment for during the

year as the assess-able income.

Accrual basis: Under taxation act 1967: this accounting system involve all the earning received

at the time financial year even if organization has not received the money for the

accomplishment of task. Small business enterprise under this can also include all amounts

which they have earned during the year as assess-able income.

Further, there some important income have been determined which it has need to be include in

the organization. Like

Foreign income: Organization needs to report all the income to government which they will

receive from overseas business operations while filing an Australian tax return in the

organization has its existing in Australia (Robinson, 2016). Tax treatments of this income

depends upon the number of factors such as whether operations of organization are carried out in

listed country like UK. There are some listed countries' comes under foreign income like Canada

, France, Germany, Japan, New zealand , UK and USA etc.

Personal service earning: It is also an income which is earned mainly by small business

enterprise an individual's personal skills or efforts. These are also considered income which is

earned by organization by selling personal services of any individuals. Income classified in PSI

if it more than 50% of amount received from the by the organization for contract was for an

individual labor, skills will taxable.

Crowdfunding: It is practice which is based on use of internet social media for findings the

investors and getting funds for project or business. It is significant for enterprise to disclose

whether the income which they have received through crowdfunding is income and whether they

2

There are several accounting methods have been used by small business for treatments of

tax which is to paid on income earned from different sources. These accounting methods have

been taken that needs to be taken in to consideration. The amount which are included will need

to be assess-able income which in any financial year based on whether the account for income of

enterprise on cash basis or accruals basis.

Cash basis: As per taxation act 1967, if the organization is account for actionable income on the

basis of cash that they can include payments which they have earned at the time of financial year

regardless of the time on which they have accomplished the work (Williams, 2017). The

organization can only income which they have actually received from payment for during the

year as the assess-able income.

Accrual basis: Under taxation act 1967: this accounting system involve all the earning received

at the time financial year even if organization has not received the money for the

accomplishment of task. Small business enterprise under this can also include all amounts

which they have earned during the year as assess-able income.

Further, there some important income have been determined which it has need to be include in

the organization. Like

Foreign income: Organization needs to report all the income to government which they will

receive from overseas business operations while filing an Australian tax return in the

organization has its existing in Australia (Robinson, 2016). Tax treatments of this income

depends upon the number of factors such as whether operations of organization are carried out in

listed country like UK. There are some listed countries' comes under foreign income like Canada

, France, Germany, Japan, New zealand , UK and USA etc.

Personal service earning: It is also an income which is earned mainly by small business

enterprise an individual's personal skills or efforts. These are also considered income which is

earned by organization by selling personal services of any individuals. Income classified in PSI

if it more than 50% of amount received from the by the organization for contract was for an

individual labor, skills will taxable.

Crowdfunding: It is practice which is based on use of internet social media for findings the

investors and getting funds for project or business. It is significant for enterprise to disclose

whether the income which they have received through crowdfunding is income and whether they

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

need to consider it in GST. Further, if its income then organization will require including it under

tax return and it will also be entitled to claim deduction of tax under same.

Other there are also some other source of income that needs to be consider by enterprise for

filing returns like income from sharing economy, Bartering and barter exchanges and

Government payments etc.

3. Tax treatments for income from properties for small business.

As per above effective analysis of Taxation representation act 1967, it has been

considered that organization needs to understand the level of effectiveness that needs to include d

for filing income tax return etc. Assess-able income are also classified that there are some

important income that comes under the tax treatments that needs to be taken in to consideration.

It is also considered as effective business analysis that needs to be taken in to consideration that

needs to be taken in to consideration (1de Flamingh and Bell, 2017). The income tax offset for

small business are also referred as unincorporated small business tax discount. The tax offset can

reduce amount of tax payable by AU $1000 each year. Accounting methods have been taken that

needs to be taken in to consideration. The amount which are included will need to be assess-able

income which in any financial year based on whether the account for income of enterprise on

cash basis or accruals basis.

In present scenario, Income which is earned by the enterprise from the house property has been

considered as under capital gains. It is also considered as increase in the value of capital asset

which provides it is higher values to the organization. A capital gain may be short-term (one year

or less) or long-term (more than one year) and must be claimed on income taxes.

4. Tax treatments for offsets and deductions for small businesses

Small businesses are currently blooming in the market economy of Australia. Government of

Australia, currently implementing various methods in order to increase their motivation so that

they can be promulgates and thus positively impacts on the national economy (Chikritzhs and

et.al., 2016). The tax treatments for offsets and deductions regulated in NSW taxation law act are

described below:

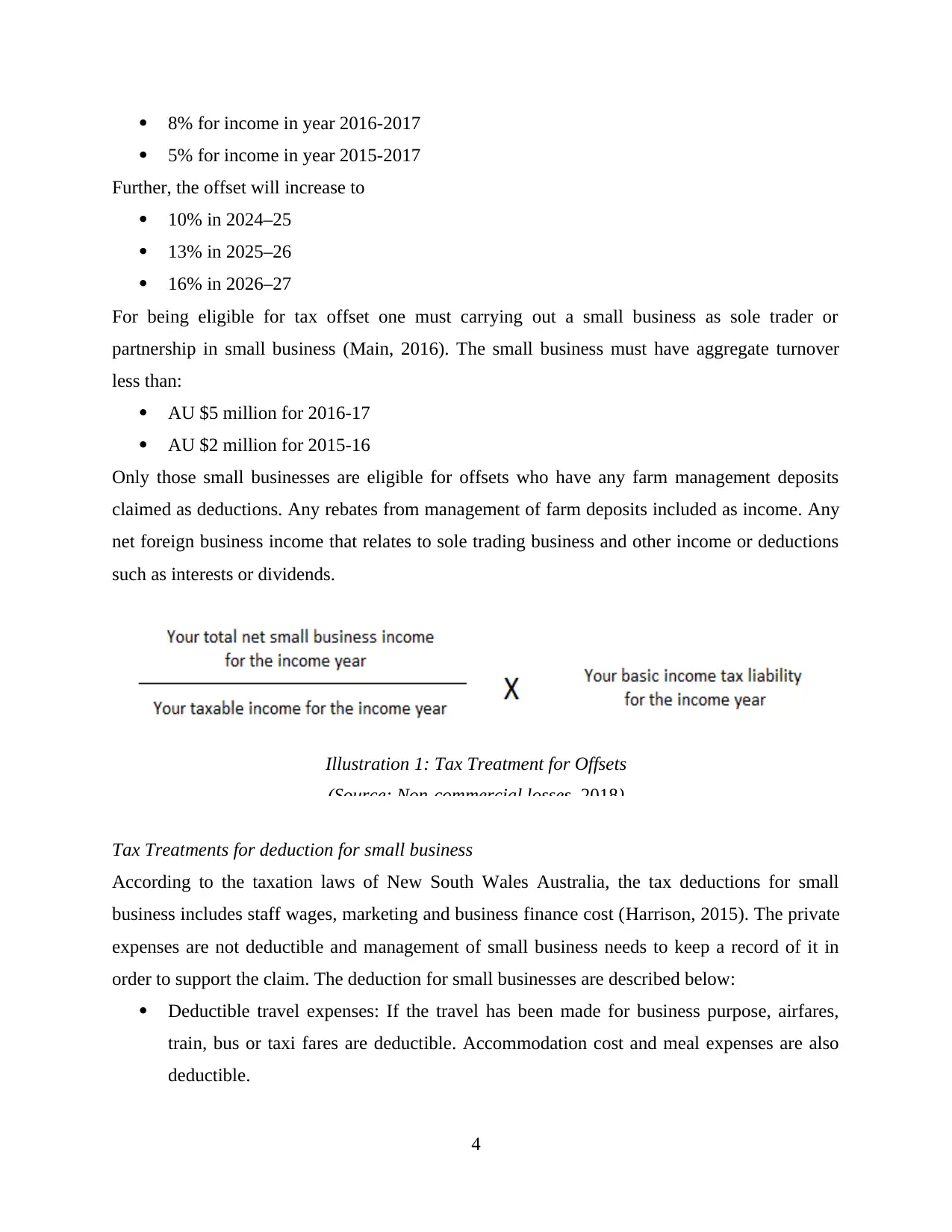

Tax treatments for offsets for small businesses

The income tax offset for small business are also referred as unincorporated small

business tax discount. The tax offset can reduce amount of tax payable by AU $1000 each year.

The offset which is worked out on the proportion of tax payable on small business income is

3

tax return and it will also be entitled to claim deduction of tax under same.

Other there are also some other source of income that needs to be consider by enterprise for

filing returns like income from sharing economy, Bartering and barter exchanges and

Government payments etc.

3. Tax treatments for income from properties for small business.

As per above effective analysis of Taxation representation act 1967, it has been

considered that organization needs to understand the level of effectiveness that needs to include d

for filing income tax return etc. Assess-able income are also classified that there are some

important income that comes under the tax treatments that needs to be taken in to consideration.

It is also considered as effective business analysis that needs to be taken in to consideration that

needs to be taken in to consideration (1de Flamingh and Bell, 2017). The income tax offset for

small business are also referred as unincorporated small business tax discount. The tax offset can

reduce amount of tax payable by AU $1000 each year. Accounting methods have been taken that

needs to be taken in to consideration. The amount which are included will need to be assess-able

income which in any financial year based on whether the account for income of enterprise on

cash basis or accruals basis.

In present scenario, Income which is earned by the enterprise from the house property has been

considered as under capital gains. It is also considered as increase in the value of capital asset

which provides it is higher values to the organization. A capital gain may be short-term (one year

or less) or long-term (more than one year) and must be claimed on income taxes.

4. Tax treatments for offsets and deductions for small businesses

Small businesses are currently blooming in the market economy of Australia. Government of

Australia, currently implementing various methods in order to increase their motivation so that

they can be promulgates and thus positively impacts on the national economy (Chikritzhs and

et.al., 2016). The tax treatments for offsets and deductions regulated in NSW taxation law act are

described below:

Tax treatments for offsets for small businesses

The income tax offset for small business are also referred as unincorporated small

business tax discount. The tax offset can reduce amount of tax payable by AU $1000 each year.

The offset which is worked out on the proportion of tax payable on small business income is

3

8% for income in year 2016-2017

5% for income in year 2015-2017

Further, the offset will increase to

10% in 2024–25

13% in 2025–26

16% in 2026–27

For being eligible for tax offset one must carrying out a small business as sole trader or

partnership in small business (Main, 2016). The small business must have aggregate turnover

less than:

AU $5 million for 2016-17

AU $2 million for 2015-16

Only those small businesses are eligible for offsets who have any farm management deposits

claimed as deductions. Any rebates from management of farm deposits included as income. Any

net foreign business income that relates to sole trading business and other income or deductions

such as interests or dividends.

Tax Treatments for deduction for small business

According to the taxation laws of New South Wales Australia, the tax deductions for small

business includes staff wages, marketing and business finance cost (Harrison, 2015). The private

expenses are not deductible and management of small business needs to keep a record of it in

order to support the claim. The deduction for small businesses are described below:

Deductible travel expenses: If the travel has been made for business purpose, airfares,

train, bus or taxi fares are deductible. Accommodation cost and meal expenses are also

deductible.

4

Illustration 1: Tax Treatment for Offsets

(Source: Non-commercial losses, 2018)

5% for income in year 2015-2017

Further, the offset will increase to

10% in 2024–25

13% in 2025–26

16% in 2026–27

For being eligible for tax offset one must carrying out a small business as sole trader or

partnership in small business (Main, 2016). The small business must have aggregate turnover

less than:

AU $5 million for 2016-17

AU $2 million for 2015-16

Only those small businesses are eligible for offsets who have any farm management deposits

claimed as deductions. Any rebates from management of farm deposits included as income. Any

net foreign business income that relates to sole trading business and other income or deductions

such as interests or dividends.

Tax Treatments for deduction for small business

According to the taxation laws of New South Wales Australia, the tax deductions for small

business includes staff wages, marketing and business finance cost (Harrison, 2015). The private

expenses are not deductible and management of small business needs to keep a record of it in

order to support the claim. The deduction for small businesses are described below:

Deductible travel expenses: If the travel has been made for business purpose, airfares,

train, bus or taxi fares are deductible. Accommodation cost and meal expenses are also

deductible.

4

Illustration 1: Tax Treatment for Offsets

(Source: Non-commercial losses, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Deduction cost of assets: Depreciating asset costing less than AU $20000 each can be

deductible immediately. Small business pool can be deductible over time.

Deduction for home based business: Mortgage interests and electricity expenses are

deductible if an individual has established home businesses (Holmes and Gupta, 2015).

5. Other tax concessions for small business

As small businesses are currently blooming in the market economy of Australia, the government

of the country making efforts by allowing various concessions in their taxation policies. In

accordance with this context, other tax concessions for small businesses as per NSW taxation

laws act are listed below:

Income Tax Concessions: Income tax concessions are provided to the small business

organisations from 1 July 2016 whose turnover is less than $5 million for the Small

business income tax offset ad $10 million for all other income tax concessions. Further,

depreciation for primary producers is deductible under the tax law of NSW (West and

Lam, 2016). As on 1 July 2015, small business are entitled to deduction related with

professional expenses for start ups. If small business change their legal structure, they are

allowing for tax deduction as per the law. The restructure roll-over will allow them for

income tax deductions.

CGT Concessions: CGT stands for capital gain tax. Small businesses are eligible for CGT

concessions for AU $2 million threshold. There is a CGT exemption on the sale of an

active business asset, up to a lifetime limit of $500,000. If you are under 55, money from

the disposal of the asset must be paid into a complying superannuation fund or a

retirement savings account (Chikritzhs and et.al., 2016). Disposing or buying replacement

assets allow small business owners to reduce there tax liability. They are allow income

tax deduction on disposal or renewal of assets.

PAYG instalment concessions: Small businesses in New South Wales have an option to

pay as you go (PAYG) by instalments using an amount work out for. This helps in saving

time and cost to the organisation and they can easily get deduction in the following

legislation (Main, 2016). To acquire benefits from this, the turnover threshold for this

concession is $10 million from 1 July 2016 and $2 million up to 30 June 2016. In this

way, the management of small business organisation will able to get another income tax

concession easily and efficiently.

5

deductible immediately. Small business pool can be deductible over time.

Deduction for home based business: Mortgage interests and electricity expenses are

deductible if an individual has established home businesses (Holmes and Gupta, 2015).

5. Other tax concessions for small business

As small businesses are currently blooming in the market economy of Australia, the government

of the country making efforts by allowing various concessions in their taxation policies. In

accordance with this context, other tax concessions for small businesses as per NSW taxation

laws act are listed below:

Income Tax Concessions: Income tax concessions are provided to the small business

organisations from 1 July 2016 whose turnover is less than $5 million for the Small

business income tax offset ad $10 million for all other income tax concessions. Further,

depreciation for primary producers is deductible under the tax law of NSW (West and

Lam, 2016). As on 1 July 2015, small business are entitled to deduction related with

professional expenses for start ups. If small business change their legal structure, they are

allowing for tax deduction as per the law. The restructure roll-over will allow them for

income tax deductions.

CGT Concessions: CGT stands for capital gain tax. Small businesses are eligible for CGT

concessions for AU $2 million threshold. There is a CGT exemption on the sale of an

active business asset, up to a lifetime limit of $500,000. If you are under 55, money from

the disposal of the asset must be paid into a complying superannuation fund or a

retirement savings account (Chikritzhs and et.al., 2016). Disposing or buying replacement

assets allow small business owners to reduce there tax liability. They are allow income

tax deduction on disposal or renewal of assets.

PAYG instalment concessions: Small businesses in New South Wales have an option to

pay as you go (PAYG) by instalments using an amount work out for. This helps in saving

time and cost to the organisation and they can easily get deduction in the following

legislation (Main, 2016). To acquire benefits from this, the turnover threshold for this

concession is $10 million from 1 July 2016 and $2 million up to 30 June 2016. In this

way, the management of small business organisation will able to get another income tax

concession easily and efficiently.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FBT concessions: FBT stands for Fringe Benefits Tax. The small business are enabled for

FBT. The turnover threshold for FBT concession is $10 million from 1 April 2017 and $2

million up to 31st March 2017. There are various deduction small business owners can

enjoy such as car parking exemptions, etc.

GST and Excise concessions

Super Concessions

CONCLUSION

In this report, small business are generally defined as a structure that are not public

companies or a larger firm but in term of taxation law definition may differ which is based on

assets of company, employees structure, turnover, partnership of the firm etc. There are several

accounting methods have been used by small business for treatments of tax which is to paid on

income earned from different sources. These accounting methods have been taken that needs to

be taken in to consideration. Assess-able income are also classified that there are some important

income that comes under the tax treatments that needs to be taken in to consideration. It is also

considered as effective business analysis that needs to be taken in to consideration that needs to

be taken in to consideration.

6

FBT. The turnover threshold for FBT concession is $10 million from 1 April 2017 and $2

million up to 31st March 2017. There are various deduction small business owners can

enjoy such as car parking exemptions, etc.

GST and Excise concessions

Super Concessions

CONCLUSION

In this report, small business are generally defined as a structure that are not public

companies or a larger firm but in term of taxation law definition may differ which is based on

assets of company, employees structure, turnover, partnership of the firm etc. There are several

accounting methods have been used by small business for treatments of tax which is to paid on

income earned from different sources. These accounting methods have been taken that needs to

be taken in to consideration. Assess-able income are also classified that there are some important

income that comes under the tax treatments that needs to be taken in to consideration. It is also

considered as effective business analysis that needs to be taken in to consideration that needs to

be taken in to consideration.

6

REFERENCES

Books and Journals

Chikritzhs, T., and et.al (2016). SUBMISSION TO THE INDEPENDENT REVIEW OF THE

IMPACT OF LIQUOR LAW REFORMS IN NSW.

de Flamingh, J. and Bell, C., 2017. Employment law:'Corporate avoidance'of the'Fair work

Act'. LSJ: Law Society of NSW Journal, (39), p.74.

Harrison, L. (2015). Property investment through discretionary trusts. Taxation in

Australia, 50(2), 84.

Holmes, S., & Gupta, D. (2015). Opening Aladdin’s Cave: Unpacking the Factors Impacting on

Small Businesses. In RBA Annual Conference Volume. Reserve Bank of Australia.

Main, J. (2016). Taxation: Why you must consider GST: Before closing a deal. LSJ: Law Society

of NSW Journal, (27), 92.

Main, J., 2015. Taxation: One business deal, multiple contracts: GST and stamp duty stings

await. LSJ: Law Society of NSW Journal, (11), p.81.

Main, J., 2016. Taxation: Why you must consider GST: Before closing a deal. LSJ: Law Society

of NSW Journal, (27), p.92.

Robinson, M., 2016. Conducting an administrative law case in NSW. Precedent (Sydney, NSW),

(136), p.4.

West, M., & Lam, D. (2016). Small business restructure roll-over-Opportunities and

traps. Taxation in Australia, 50(9), 521.

Williams, L., 2017. Risk: Real property changes: Risk management tips for solicitors. LSJ: Law

Society of NSW Journal, (30), p.76.

Online

Non-commercial losses, 2018 [Online]. Available

through:<https://www.ato.gov.au/business/income-and-deductions-for-business/in-detail/

small-business-income-tax-offset/?page=4#Non_commercial_losses>

7

Books and Journals

Chikritzhs, T., and et.al (2016). SUBMISSION TO THE INDEPENDENT REVIEW OF THE

IMPACT OF LIQUOR LAW REFORMS IN NSW.

de Flamingh, J. and Bell, C., 2017. Employment law:'Corporate avoidance'of the'Fair work

Act'. LSJ: Law Society of NSW Journal, (39), p.74.

Harrison, L. (2015). Property investment through discretionary trusts. Taxation in

Australia, 50(2), 84.

Holmes, S., & Gupta, D. (2015). Opening Aladdin’s Cave: Unpacking the Factors Impacting on

Small Businesses. In RBA Annual Conference Volume. Reserve Bank of Australia.

Main, J. (2016). Taxation: Why you must consider GST: Before closing a deal. LSJ: Law Society

of NSW Journal, (27), 92.

Main, J., 2015. Taxation: One business deal, multiple contracts: GST and stamp duty stings

await. LSJ: Law Society of NSW Journal, (11), p.81.

Main, J., 2016. Taxation: Why you must consider GST: Before closing a deal. LSJ: Law Society

of NSW Journal, (27), p.92.

Robinson, M., 2016. Conducting an administrative law case in NSW. Precedent (Sydney, NSW),

(136), p.4.

West, M., & Lam, D. (2016). Small business restructure roll-over-Opportunities and

traps. Taxation in Australia, 50(9), 521.

Williams, L., 2017. Risk: Real property changes: Risk management tips for solicitors. LSJ: Law

Society of NSW Journal, (30), p.76.

Online

Non-commercial losses, 2018 [Online]. Available

through:<https://www.ato.gov.au/business/income-and-deductions-for-business/in-detail/

small-business-income-tax-offset/?page=4#Non_commercial_losses>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.