Financial Modelling Project: CAPM Analysis of Australian Stocks

VerifiedAdded on 2022/08/18

|12

|2109

|16

Project

AI Summary

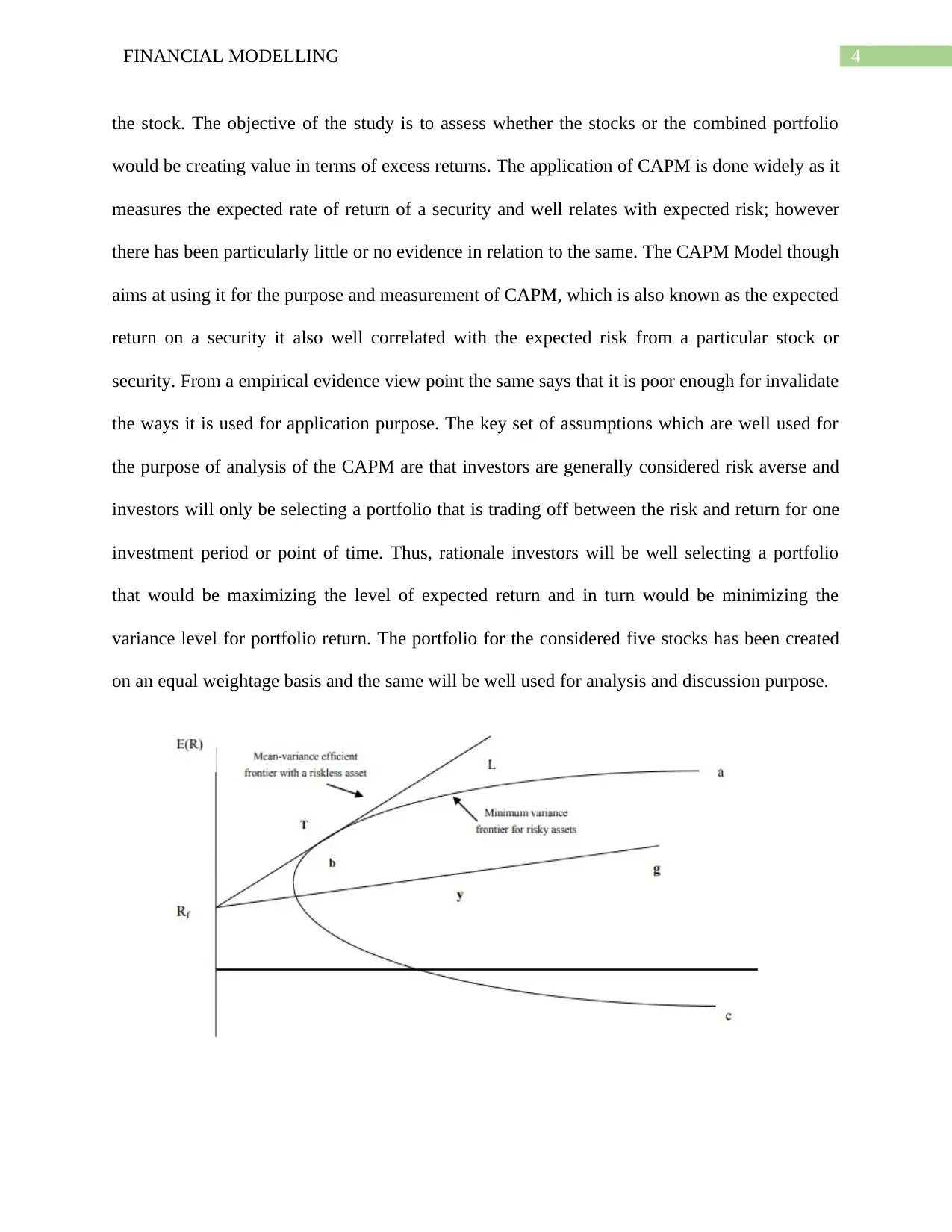

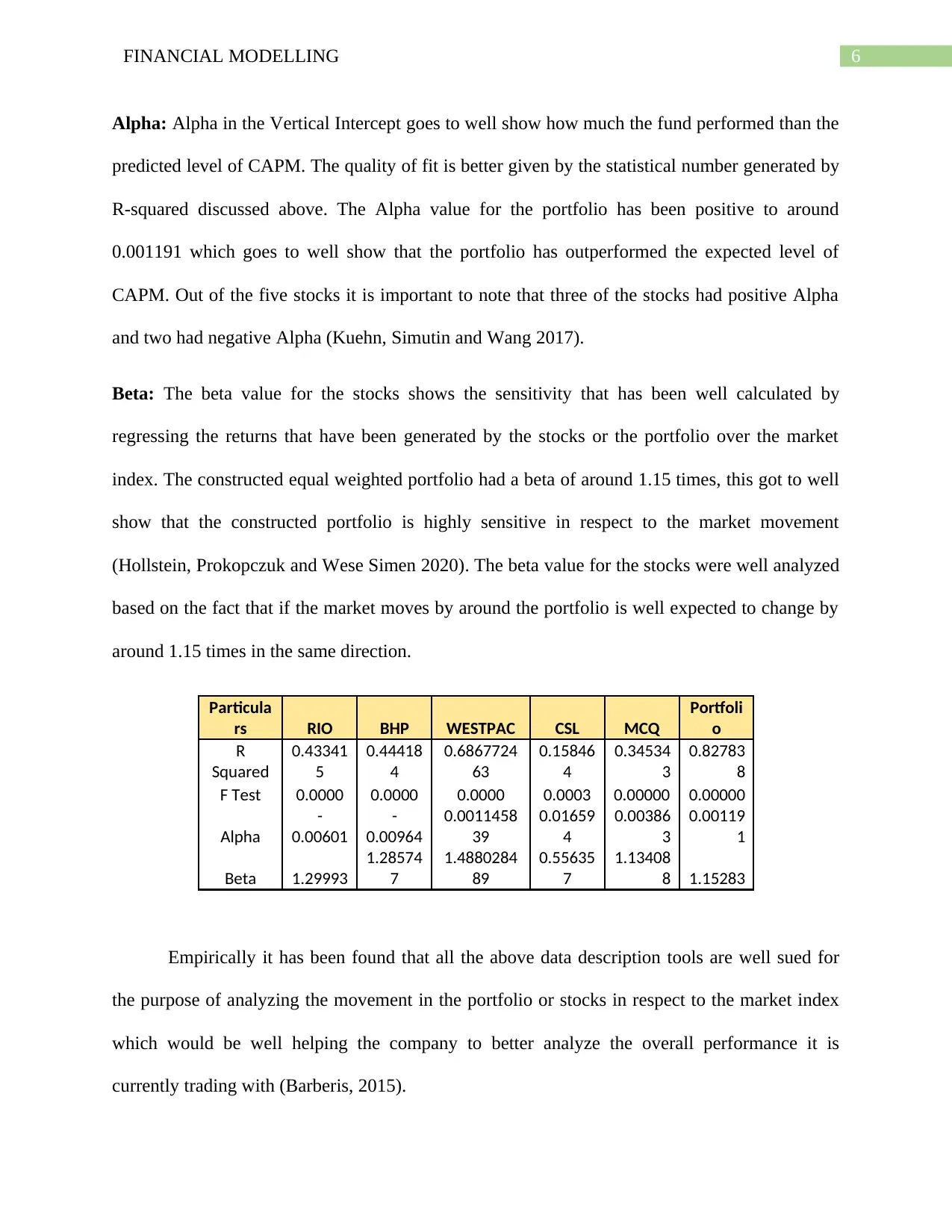

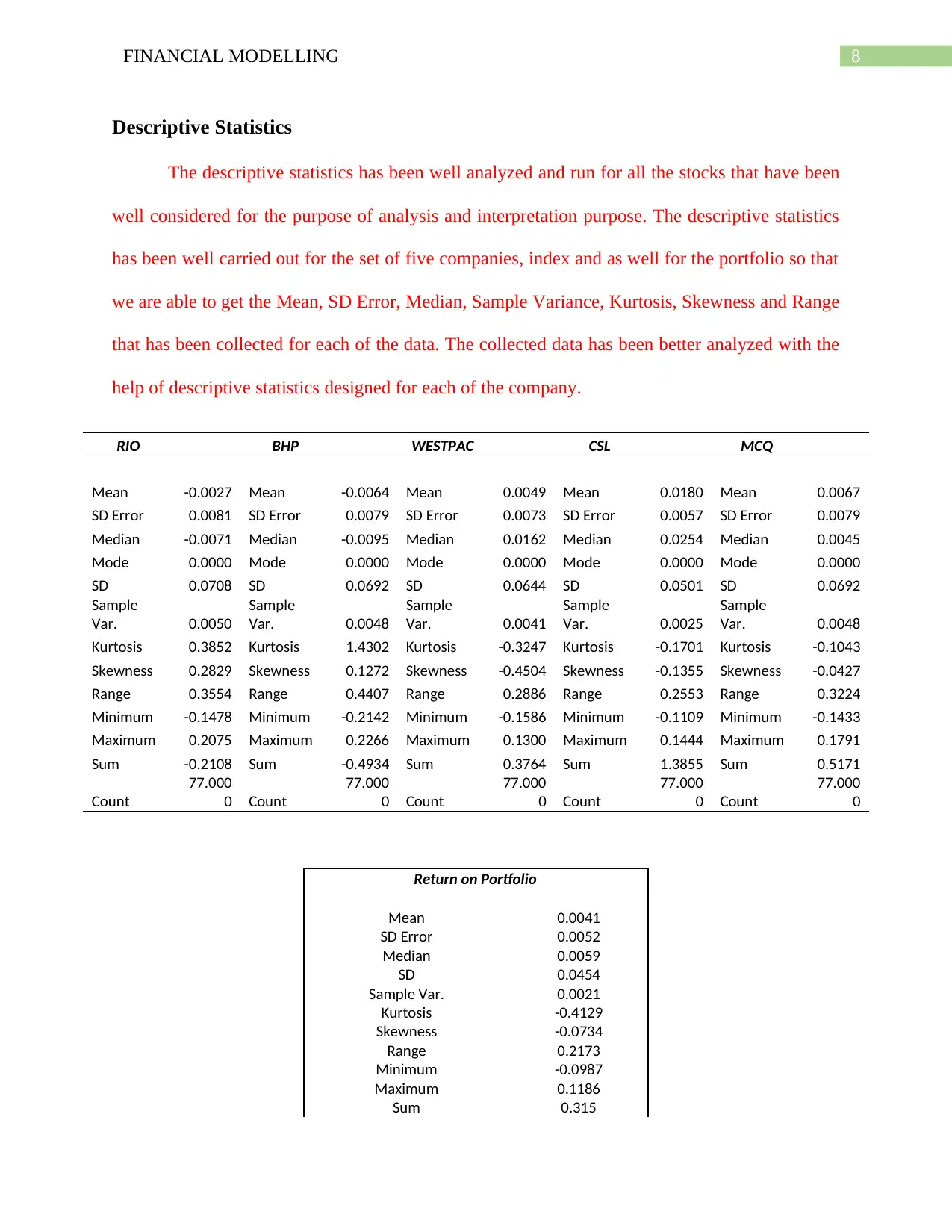

This financial modelling project undertakes a comprehensive analysis of selected large-cap Australian companies actively traded on the Australian market from January 2010 to June 2016, focusing on investment perspectives. The study employs the Capital Asset Pricing Model (CAPM) to determine expected stock returns. Regression analysis, R-squared, F-test, Alpha, and Beta values are calculated to assess the model's validity. Descriptive statistics, including mean, standard deviation, and other relevant metrics, are derived to provide a detailed understanding of the data. The analysis uses Excel and STATA software for statistical calculations and model evaluation, including unit root tests and diagnostic tests. The project constructs and analyzes an equally weighted portfolio of five stocks, examining their sensitivity to market movements and assessing portfolio performance against CAPM predictions. Findings are presented with tables and include a discussion of the results and their implications for the model. The project also provides recommendations based on the analysis.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.