King's Own Institute: Australian Superannuation Report, FIN200

VerifiedAdded on 2022/11/23

|11

|2852

|81

Report

AI Summary

This report provides a comprehensive analysis of Australian superannuation, exploring both investment choice and defined benefit plans. It delves into the factors influencing superannuation plan choices, including the time value of money, opportunity cost, and the impact of taxes on contributions. The report examines the amount of contributions, employer and employee roles, and the incentives provided by the Australian government. It further discusses the factors tertiary sector workers must consider when selecting a superannuation plan, such as time value of money, opportunity cost, taxes, and contribution amounts. The report concludes with recommendations for effective superannuation management and highlights the importance of a robust system for financial stability and improved retirement outcomes, while also acknowledging the current focus on accumulation and the potential risks associated with it.

Australian Superannuation 1

AUSTRALIAN SUPERANNUATION

By Students Name

Code + Course

Professor

City, State

Date

Table of Content

AUSTRALIAN SUPERANNUATION

By Students Name

Code + Course

Professor

City, State

Date

Table of Content

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Superannuation 2

s

Superannuation................................................................................................................................3

Introduction......................................................................................................................................3

Superannuation in Australia............................................................................................................3

Investment choice plan....................................................................................................................3

Defined benefit plan........................................................................................................................4

Factors Considered in Superannuation Plan Choice........................................................................4

Time value of money and superannuation...................................................................................4

Taxes and superannuation............................................................................................................5

Opportunity cost and superannuation..........................................................................................5

Amount of Contributions.............................................................................................................6

Conclusion.......................................................................................................................................7

Recommendations............................................................................................................................7

Bibliography....................................................................................................................................9

s

Superannuation................................................................................................................................3

Introduction......................................................................................................................................3

Superannuation in Australia............................................................................................................3

Investment choice plan....................................................................................................................3

Defined benefit plan........................................................................................................................4

Factors Considered in Superannuation Plan Choice........................................................................4

Time value of money and superannuation...................................................................................4

Taxes and superannuation............................................................................................................5

Opportunity cost and superannuation..........................................................................................5

Amount of Contributions.............................................................................................................6

Conclusion.......................................................................................................................................7

Recommendations............................................................................................................................7

Bibliography....................................................................................................................................9

Australian Superannuation 3

Superannuation

Introduction

Globally, governments face a challenge in ensuring retirees live a decent life after their

retirement. In order to overcome this challenge, some governments have imposed compulsory

contribution amongst its citizens to pension funds. The funds are normally managed by super

funds that invest the funds in different investments and in return, the funds earn interest. The

contributions, therefore, grow from the point of deposit to the point they are drawn or at the

retirement of the contributor (Williams, 2018). Different incentives exist for superannuation and

these incentives differ between countries. Some countries reduce the tax liability for the savings;

this results in greater savings and better retirement for its citizen. The growth of superannuation

has seen legislation passed to govern the schemes in countries and provide arbitration channels

for those offended. Superannuation is therefore a great way to secure an individual’s retirement

by saving during the productive years.

Superannuation in Australia

In Australia, the superannuation is a partly compulsory scheme for all the citizens. Employees

have set minimum contributions to make, and the employers must contribute to the

superannuation of its employees on top of the salaries and wages they pay them (Kingston and

Thorp, 2019). The scheme allows extra contributions made by the citizens to complement the

compulsory contributions. The compulsory contribution is referred to concessional while any

contribution above the concessional is non concessional contribution. The Australian

government has created incentives for saving by giving tax benefits on amounts contributed to

superannuation. The contribution by the employer and employee were previously set at 3%, but

there has been a gradual increase in the percentage all through. This growth has been positive

despite great resistance at the introduction stage.

Superannuation

Introduction

Globally, governments face a challenge in ensuring retirees live a decent life after their

retirement. In order to overcome this challenge, some governments have imposed compulsory

contribution amongst its citizens to pension funds. The funds are normally managed by super

funds that invest the funds in different investments and in return, the funds earn interest. The

contributions, therefore, grow from the point of deposit to the point they are drawn or at the

retirement of the contributor (Williams, 2018). Different incentives exist for superannuation and

these incentives differ between countries. Some countries reduce the tax liability for the savings;

this results in greater savings and better retirement for its citizen. The growth of superannuation

has seen legislation passed to govern the schemes in countries and provide arbitration channels

for those offended. Superannuation is therefore a great way to secure an individual’s retirement

by saving during the productive years.

Superannuation in Australia

In Australia, the superannuation is a partly compulsory scheme for all the citizens. Employees

have set minimum contributions to make, and the employers must contribute to the

superannuation of its employees on top of the salaries and wages they pay them (Kingston and

Thorp, 2019). The scheme allows extra contributions made by the citizens to complement the

compulsory contributions. The compulsory contribution is referred to concessional while any

contribution above the concessional is non concessional contribution. The Australian

government has created incentives for saving by giving tax benefits on amounts contributed to

superannuation. The contribution by the employer and employee were previously set at 3%, but

there has been a gradual increase in the percentage all through. This growth has been positive

despite great resistance at the introduction stage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian Superannuation 4

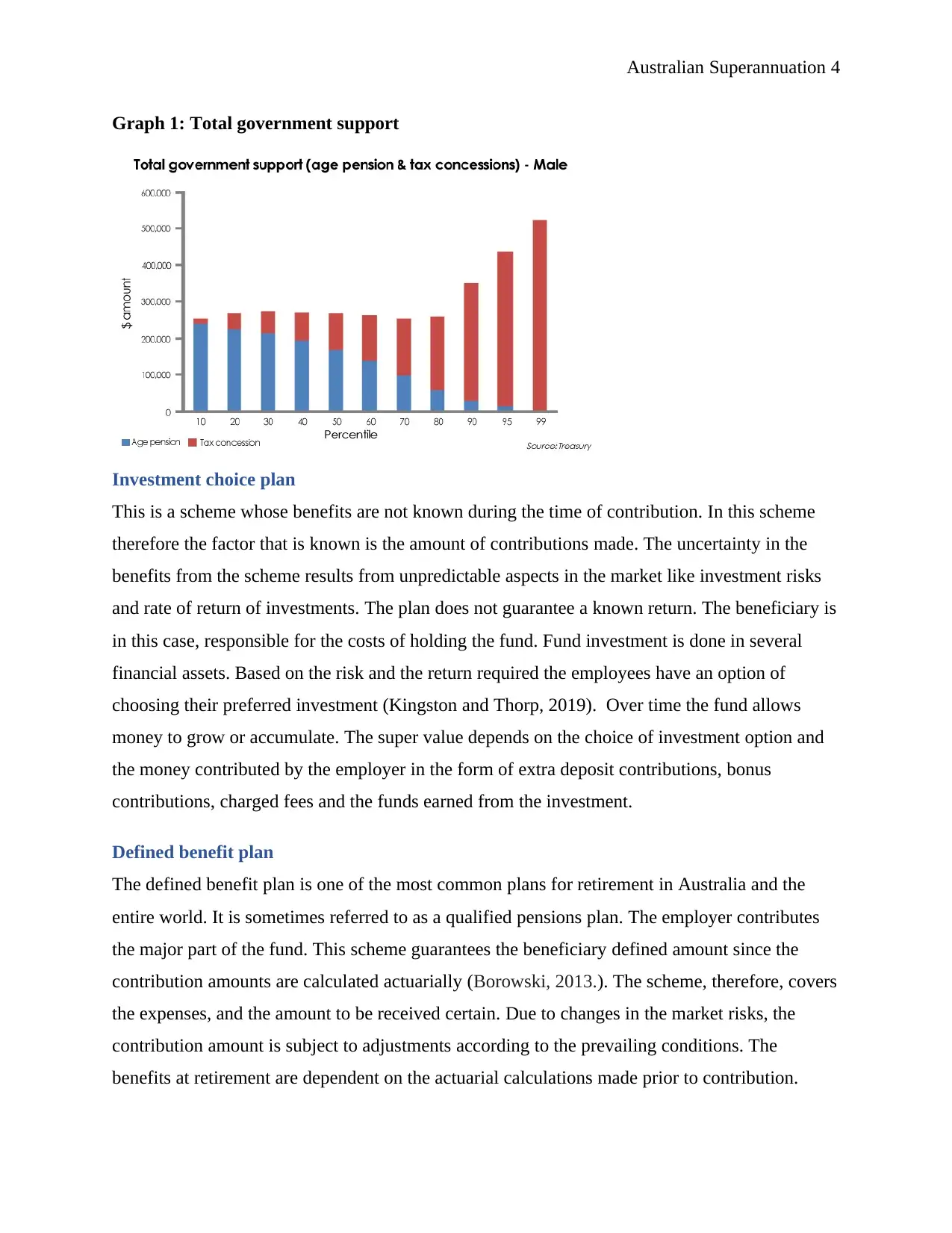

Graph 1: Total government support

Investment choice plan

This is a scheme whose benefits are not known during the time of contribution. In this scheme

therefore the factor that is known is the amount of contributions made. The uncertainty in the

benefits from the scheme results from unpredictable aspects in the market like investment risks

and rate of return of investments. The plan does not guarantee a known return. The beneficiary is

in this case, responsible for the costs of holding the fund. Fund investment is done in several

financial assets. Based on the risk and the return required the employees have an option of

choosing their preferred investment (Kingston and Thorp, 2019). Over time the fund allows

money to grow or accumulate. The super value depends on the choice of investment option and

the money contributed by the employer in the form of extra deposit contributions, bonus

contributions, charged fees and the funds earned from the investment.

Defined benefit plan

The defined benefit plan is one of the most common plans for retirement in Australia and the

entire world. It is sometimes referred to as a qualified pensions plan. The employer contributes

the major part of the fund. This scheme guarantees the beneficiary defined amount since the

contribution amounts are calculated actuarially (Borowski, 2013.). The scheme, therefore, covers

the expenses, and the amount to be received certain. Due to changes in the market risks, the

contribution amount is subject to adjustments according to the prevailing conditions. The

benefits at retirement are dependent on the actuarial calculations made prior to contribution.

Graph 1: Total government support

Investment choice plan

This is a scheme whose benefits are not known during the time of contribution. In this scheme

therefore the factor that is known is the amount of contributions made. The uncertainty in the

benefits from the scheme results from unpredictable aspects in the market like investment risks

and rate of return of investments. The plan does not guarantee a known return. The beneficiary is

in this case, responsible for the costs of holding the fund. Fund investment is done in several

financial assets. Based on the risk and the return required the employees have an option of

choosing their preferred investment (Kingston and Thorp, 2019). Over time the fund allows

money to grow or accumulate. The super value depends on the choice of investment option and

the money contributed by the employer in the form of extra deposit contributions, bonus

contributions, charged fees and the funds earned from the investment.

Defined benefit plan

The defined benefit plan is one of the most common plans for retirement in Australia and the

entire world. It is sometimes referred to as a qualified pensions plan. The employer contributes

the major part of the fund. This scheme guarantees the beneficiary defined amount since the

contribution amounts are calculated actuarially (Borowski, 2013.). The scheme, therefore, covers

the expenses, and the amount to be received certain. Due to changes in the market risks, the

contribution amount is subject to adjustments according to the prevailing conditions. The

benefits at retirement are dependent on the actuarial calculations made prior to contribution.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Superannuation 5

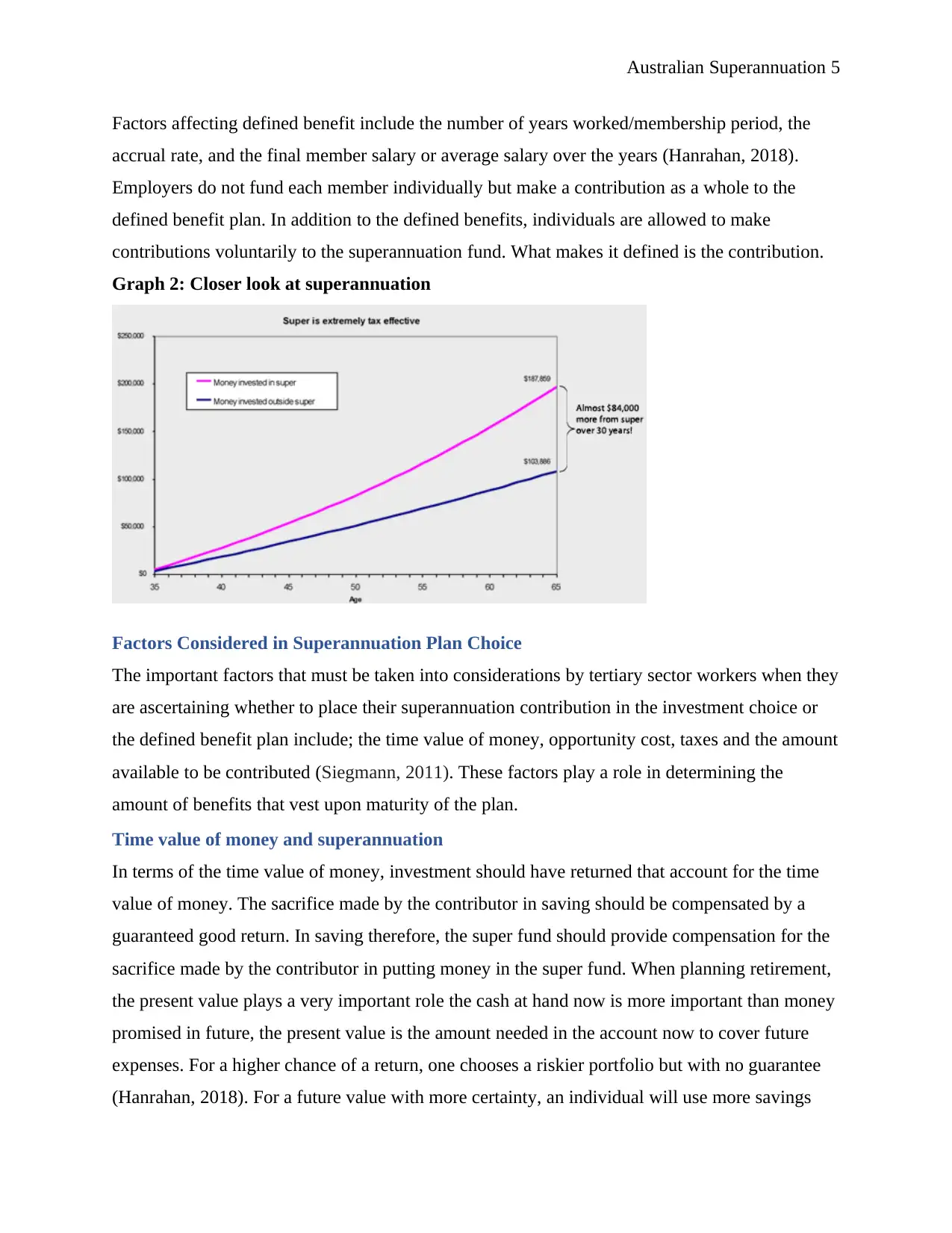

Factors affecting defined benefit include the number of years worked/membership period, the

accrual rate, and the final member salary or average salary over the years (Hanrahan, 2018).

Employers do not fund each member individually but make a contribution as a whole to the

defined benefit plan. In addition to the defined benefits, individuals are allowed to make

contributions voluntarily to the superannuation fund. What makes it defined is the contribution.

Graph 2: Closer look at superannuation

Factors Considered in Superannuation Plan Choice

The important factors that must be taken into considerations by tertiary sector workers when they

are ascertaining whether to place their superannuation contribution in the investment choice or

the defined benefit plan include; the time value of money, opportunity cost, taxes and the amount

available to be contributed (Siegmann, 2011). These factors play a role in determining the

amount of benefits that vest upon maturity of the plan.

Time value of money and superannuation

In terms of the time value of money, investment should have returned that account for the time

value of money. The sacrifice made by the contributor in saving should be compensated by a

guaranteed good return. In saving therefore, the super fund should provide compensation for the

sacrifice made by the contributor in putting money in the super fund. When planning retirement,

the present value plays a very important role the cash at hand now is more important than money

promised in future, the present value is the amount needed in the account now to cover future

expenses. For a higher chance of a return, one chooses a riskier portfolio but with no guarantee

(Hanrahan, 2018). For a future value with more certainty, an individual will use more savings

Factors affecting defined benefit include the number of years worked/membership period, the

accrual rate, and the final member salary or average salary over the years (Hanrahan, 2018).

Employers do not fund each member individually but make a contribution as a whole to the

defined benefit plan. In addition to the defined benefits, individuals are allowed to make

contributions voluntarily to the superannuation fund. What makes it defined is the contribution.

Graph 2: Closer look at superannuation

Factors Considered in Superannuation Plan Choice

The important factors that must be taken into considerations by tertiary sector workers when they

are ascertaining whether to place their superannuation contribution in the investment choice or

the defined benefit plan include; the time value of money, opportunity cost, taxes and the amount

available to be contributed (Siegmann, 2011). These factors play a role in determining the

amount of benefits that vest upon maturity of the plan.

Time value of money and superannuation

In terms of the time value of money, investment should have returned that account for the time

value of money. The sacrifice made by the contributor in saving should be compensated by a

guaranteed good return. In saving therefore, the super fund should provide compensation for the

sacrifice made by the contributor in putting money in the super fund. When planning retirement,

the present value plays a very important role the cash at hand now is more important than money

promised in future, the present value is the amount needed in the account now to cover future

expenses. For a higher chance of a return, one chooses a riskier portfolio but with no guarantee

(Hanrahan, 2018). For a future value with more certainty, an individual will use more savings

Australian Superannuation 6

with a lower return rate. Employee contributions are invested in order to earn returns; this

facilitates growth. The ordinary time earnings determine the employer’s contributions.

Taxes and superannuation

A comprehensive income tax model is adhered to when taxing superannuation as the government

is establishing incentives for saving. Fifteen percent is the flat rate of the superannuation fund tax

income to a maximum of 9.5% of the employer contribution. This amount is tax exempt for the

contributor, but any further additions to the fund attract taxes to a ceiling amount. The

compulsory contribution by the employer is termed as concessional contribution while any

further addition is non concessional (Cummings, 2016). The Australian taxation system taxes

superannuation contributions at three points, when superannuation contribution is received at

retirement, when income from the investment fund is received and on the paid benefits by the

fund.

Contributions can either be concessional or non-concessional. Concessional contributions attract

tax deductions they include superannuation guarantee, employer contributions, and salary

sacrifice contributions. Non- concessional contributions are not taxed Sargent,Lee, Martin and

Zikic, 2013. Funds to superannuation contributions are subject to government caps since 2014

the annual cap has been $ 30,000 and $ 35,000 for employers over 49 years of age. From July

2016 the government reduced the annual before-tax limit to $ 25,000. The fund accessible is

income less allowable deductions are the taxable income of the superannuation fund (Hanrahan,

2018). Payment amounts are taxed at the normal income for social security payment recipients.

Opportunity cost and superannuation

Opportunity cost or alternative cost is the benefits lost when choosing an alternative over

another. It’s the ultimate sacrificed satisfaction from the foregone alternative. A better decision

can be made by carefully understanding the foregone opportunities (Chant, Mohankumar, and

Warren, 2014). An employee choosing a fund over other available super funds in the market is

the opportunity cost. Some contributors go beyond the concessional contribution by contributing

amounts higher than the required. Such contributors should be compensated for the sacrifice in

saving such money. Super funds should, therefore, compensate the employees for the sacrifice

made by investing in that particular fund and leaving out all the rest (Productivity Commission,

with a lower return rate. Employee contributions are invested in order to earn returns; this

facilitates growth. The ordinary time earnings determine the employer’s contributions.

Taxes and superannuation

A comprehensive income tax model is adhered to when taxing superannuation as the government

is establishing incentives for saving. Fifteen percent is the flat rate of the superannuation fund tax

income to a maximum of 9.5% of the employer contribution. This amount is tax exempt for the

contributor, but any further additions to the fund attract taxes to a ceiling amount. The

compulsory contribution by the employer is termed as concessional contribution while any

further addition is non concessional (Cummings, 2016). The Australian taxation system taxes

superannuation contributions at three points, when superannuation contribution is received at

retirement, when income from the investment fund is received and on the paid benefits by the

fund.

Contributions can either be concessional or non-concessional. Concessional contributions attract

tax deductions they include superannuation guarantee, employer contributions, and salary

sacrifice contributions. Non- concessional contributions are not taxed Sargent,Lee, Martin and

Zikic, 2013. Funds to superannuation contributions are subject to government caps since 2014

the annual cap has been $ 30,000 and $ 35,000 for employers over 49 years of age. From July

2016 the government reduced the annual before-tax limit to $ 25,000. The fund accessible is

income less allowable deductions are the taxable income of the superannuation fund (Hanrahan,

2018). Payment amounts are taxed at the normal income for social security payment recipients.

Opportunity cost and superannuation

Opportunity cost or alternative cost is the benefits lost when choosing an alternative over

another. It’s the ultimate sacrificed satisfaction from the foregone alternative. A better decision

can be made by carefully understanding the foregone opportunities (Chant, Mohankumar, and

Warren, 2014). An employee choosing a fund over other available super funds in the market is

the opportunity cost. Some contributors go beyond the concessional contribution by contributing

amounts higher than the required. Such contributors should be compensated for the sacrifice in

saving such money. Super funds should, therefore, compensate the employees for the sacrifice

made by investing in that particular fund and leaving out all the rest (Productivity Commission,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian Superannuation 7

2016). The compensation should be in the form of assurance of the safety of funds by investing

in safe investments as well as guaranteeing a good return at retirement.

Amount of Contributions

Employers make contributions to the fund at 9.5% of the employee earning consisting of salaries,

wages, commissions, and allowances with the exception of overtime. These contributions should

be made on a quarterly basis (Cummings, 2016). They attract a 15% tax deductible to the

employer and not part of the employee taxable income. Contributions can also be made

voluntarily by employees to their superannuation a tax benefit subject to a limit is applicable in

this arrangement.

Salary sacrifice is a situation where an employee requests the employer to deposit their entire

earnings to superannuation instead of paying them for the services rendered. Such contributions

are treated as a superannuation contribution from the employer for tax purposes deducted from

the employer. Since the amount contributed is excluded from the taxable income, it is highly

beneficial to the employee (Bateman, Deetlefs and Dobrescu, 2014). The employee and

employer should have a written agreement before work is commenced for the salary sacrifice

contributions to be valid. In considering the superannuation plan to adopt, the employee should

consider the amount available for saving and the stability of the job. Some plan requires that the

money be deposited to the fund at prescribed times (Stebbing, and Spies-Butcher,.2016). For

none permanently employed individuals, this plan could be disadvantageous.

For prudence purposes, anyone planning to adopt a superannuation fund should go due to due

diligence analysis of the available plans. The findings should lead them to finding the best option

in terms of security of the contribution and the return to be received at retirement or termination

(Odia, and Okoye, 2012). In making the decision on the time value of money, an employee

should consider the plan that gives the best return for the investments made. The fund should

also manage the contributions adequately to ensure their security by choosing investments with

acceptable level of risk. In considering the opportunity cost, the employee should choose a plan

that compensates for the sacrifice made in picking that particular superannuation plan. The

Best plan should also ensure the funds are safe, and the risk level accepted is conservative.

2016). The compensation should be in the form of assurance of the safety of funds by investing

in safe investments as well as guaranteeing a good return at retirement.

Amount of Contributions

Employers make contributions to the fund at 9.5% of the employee earning consisting of salaries,

wages, commissions, and allowances with the exception of overtime. These contributions should

be made on a quarterly basis (Cummings, 2016). They attract a 15% tax deductible to the

employer and not part of the employee taxable income. Contributions can also be made

voluntarily by employees to their superannuation a tax benefit subject to a limit is applicable in

this arrangement.

Salary sacrifice is a situation where an employee requests the employer to deposit their entire

earnings to superannuation instead of paying them for the services rendered. Such contributions

are treated as a superannuation contribution from the employer for tax purposes deducted from

the employer. Since the amount contributed is excluded from the taxable income, it is highly

beneficial to the employee (Bateman, Deetlefs and Dobrescu, 2014). The employee and

employer should have a written agreement before work is commenced for the salary sacrifice

contributions to be valid. In considering the superannuation plan to adopt, the employee should

consider the amount available for saving and the stability of the job. Some plan requires that the

money be deposited to the fund at prescribed times (Stebbing, and Spies-Butcher,.2016). For

none permanently employed individuals, this plan could be disadvantageous.

For prudence purposes, anyone planning to adopt a superannuation fund should go due to due

diligence analysis of the available plans. The findings should lead them to finding the best option

in terms of security of the contribution and the return to be received at retirement or termination

(Odia, and Okoye, 2012). In making the decision on the time value of money, an employee

should consider the plan that gives the best return for the investments made. The fund should

also manage the contributions adequately to ensure their security by choosing investments with

acceptable level of risk. In considering the opportunity cost, the employee should choose a plan

that compensates for the sacrifice made in picking that particular superannuation plan. The

Best plan should also ensure the funds are safe, and the risk level accepted is conservative.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Superannuation 8

When it comes to taxes, the employee should make use of the incentives given and apply for tax

deduction from the fund manager. Superannuation contributed from post-tax earnings are not

taxable, and the retirement benefits are tax exempt. An individual should, however, make

concessional savings and take advantage of the government incentives (Odia, and Okoye, 2012).

In considering amounts available for contribution, an employee should consider the stability of

income. Since defined benefits plan has their contributions determined actuarially, failure to

make contributions on time could affect the scheme. In this case, an individual with an unstable

source of income should consider choosing a more flexible plan to put money (Cummings,

2016). The defined benefits plans are a good investment for those with stable income and more

likely to stay with the current employer until the benefits are passed to them.

Conclusion

Retirement policies highly impact the fiscal position of any state. One of the government’s major

expenditure is retirement payments through superannuation subsidization and pension payments.

The superannuation system might seem entrusted to the private sector, but the government is also

playing a significant role. The compulsory superannuation systems have increased savings

substantially in Austarlia and ensured that citizens are guaranteed of a decent retirement package.

It is however evident that an effective and efficient scheme is essential to manage the funds and

ensure that misappropriation do not occur. By making contributions deductible during taxation

of income and the drawings free from any taxes, the Australian government is giving adequate

incentives to saving.

Financial stability has been enforced through a large pool of stable superannuation assets. Future

wellbeing improvement and great retirement outcomes are the key objective of any pension

scheme; when an employee contributes, they expect enough income flow after retirement that is

sustainable and adequate from an integral system. At the moment the accumulation face seems to

be getting more focus, therefore, posing a risk on whether the scheme will be sustainable in the

future. However, these policies seem to be more beneficial to high-income earners due to tax

expenditures associated with concessional taxation. Taxation should be reduced for the

investment to reach its desired goals.

Recommendations

Based on the analysis and research, Defined Benefit Plan is recommended. This is because for

the pension scheme to be more effective, the superannuation preservation ages should be aligned

When it comes to taxes, the employee should make use of the incentives given and apply for tax

deduction from the fund manager. Superannuation contributed from post-tax earnings are not

taxable, and the retirement benefits are tax exempt. An individual should, however, make

concessional savings and take advantage of the government incentives (Odia, and Okoye, 2012).

In considering amounts available for contribution, an employee should consider the stability of

income. Since defined benefits plan has their contributions determined actuarially, failure to

make contributions on time could affect the scheme. In this case, an individual with an unstable

source of income should consider choosing a more flexible plan to put money (Cummings,

2016). The defined benefits plans are a good investment for those with stable income and more

likely to stay with the current employer until the benefits are passed to them.

Conclusion

Retirement policies highly impact the fiscal position of any state. One of the government’s major

expenditure is retirement payments through superannuation subsidization and pension payments.

The superannuation system might seem entrusted to the private sector, but the government is also

playing a significant role. The compulsory superannuation systems have increased savings

substantially in Austarlia and ensured that citizens are guaranteed of a decent retirement package.

It is however evident that an effective and efficient scheme is essential to manage the funds and

ensure that misappropriation do not occur. By making contributions deductible during taxation

of income and the drawings free from any taxes, the Australian government is giving adequate

incentives to saving.

Financial stability has been enforced through a large pool of stable superannuation assets. Future

wellbeing improvement and great retirement outcomes are the key objective of any pension

scheme; when an employee contributes, they expect enough income flow after retirement that is

sustainable and adequate from an integral system. At the moment the accumulation face seems to

be getting more focus, therefore, posing a risk on whether the scheme will be sustainable in the

future. However, these policies seem to be more beneficial to high-income earners due to tax

expenditures associated with concessional taxation. Taxation should be reduced for the

investment to reach its desired goals.

Recommendations

Based on the analysis and research, Defined Benefit Plan is recommended. This is because for

the pension scheme to be more effective, the superannuation preservation ages should be aligned

Australian Superannuation 9

with the age pension, the age pension eligibility age should also be raised. Some people are using

their retirement savings to offset debt; this can be curbed by limiting lump sum withdrawals from

superannuation accounts. The high inequities should be dealt to ensure the low-income earners

benefit just like the high-income earners.

with the age pension, the age pension eligibility age should also be raised. Some people are using

their retirement savings to offset debt; this can be curbed by limiting lump sum withdrawals from

superannuation accounts. The high inequities should be dealt to ensure the low-income earners

benefit just like the high-income earners.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian Superannuation 10

Bibliography

Bateman, H., Deetlefs, J., Dobrescu, L.I., Newell, B.R., Ortmann, A. and Thorp, S., (2014). Just

interested or getting involved? An analysis of superannuation attitudes and actions. Economic

Record, 90(289), pp.160-178.

Borowski, A., 2013. Risky by Design: The Mandatory Private Pillar of A ustralia's Retirement

Income System. Social Policy & Administration, 47(6), pp.749-764.

Butler, D. and Cheung, J., (2018). Superannuation: Triggering you bring-forward NCCs cap.

Taxation in Australia, 52(8), p.438.

Chant, W., Mohankumar, M. and Warren, G., (2014). MySuper: a new landscape for default

superannuation funds. CIFR Paper, (020).

Cummings, J.R., (2016). Effect of fund size on the performance of Australian superannuation

funds. Accounting & Finance, 56(3), pp.695-725.

De Zwaan, L., Brimble, M. and Stewart, J., (2015). Member perceptions of ESG investing

through superannuation. Sustainability Accounting, Management and Policy Journal, 6(1),

pp.79-102.

Hanrahan, P.A.M.E.L.A., (2018). Legal framework governing aspects of the Australian

superannuation system. Background Paper, 25.

Kendig, H., Wells, Y., O'Loughlin, K. and Heese, K., 2013. Australian baby boomers face

retirement during the global financial crisis. Journal of aging & social policy, 25(3), pp.264-280.

Kingston, G. and Thorp, S., (2019). Superannuation in Australia: A Survey of the Literature.

Economic Record.

Odia, J.O. and Okoye, A.E., 2012. Pensions reform in Nigeria: A comparison between the old

and new scheme. Afro Asian Journal of Social Sciences, 3(3.1), pp.1-17.

Productivity Commission, (2016). Superannuation: alternative default models.

Sargent, L.D., Lee, M.D., Martin, B. and Zikic, J., 2013. Reinventing retirement: New pathways,

new arrangements, new meanings. Human relations, 66(1), pp.3-21.

Siegmann, A., 2011. Minimum funding ratios for defined-benefit pension funds. Journal of

Pension Economics & Finance, 10(3), pp.417-434.

Stebbing, A. and Spies-Butcher, B., 2016. The decline of a homeowning society? Asset-based

welfare, retirement and intergenerational equity in Australia. Housing Studies, 31(2), pp.190-

207.

Bibliography

Bateman, H., Deetlefs, J., Dobrescu, L.I., Newell, B.R., Ortmann, A. and Thorp, S., (2014). Just

interested or getting involved? An analysis of superannuation attitudes and actions. Economic

Record, 90(289), pp.160-178.

Borowski, A., 2013. Risky by Design: The Mandatory Private Pillar of A ustralia's Retirement

Income System. Social Policy & Administration, 47(6), pp.749-764.

Butler, D. and Cheung, J., (2018). Superannuation: Triggering you bring-forward NCCs cap.

Taxation in Australia, 52(8), p.438.

Chant, W., Mohankumar, M. and Warren, G., (2014). MySuper: a new landscape for default

superannuation funds. CIFR Paper, (020).

Cummings, J.R., (2016). Effect of fund size on the performance of Australian superannuation

funds. Accounting & Finance, 56(3), pp.695-725.

De Zwaan, L., Brimble, M. and Stewart, J., (2015). Member perceptions of ESG investing

through superannuation. Sustainability Accounting, Management and Policy Journal, 6(1),

pp.79-102.

Hanrahan, P.A.M.E.L.A., (2018). Legal framework governing aspects of the Australian

superannuation system. Background Paper, 25.

Kendig, H., Wells, Y., O'Loughlin, K. and Heese, K., 2013. Australian baby boomers face

retirement during the global financial crisis. Journal of aging & social policy, 25(3), pp.264-280.

Kingston, G. and Thorp, S., (2019). Superannuation in Australia: A Survey of the Literature.

Economic Record.

Odia, J.O. and Okoye, A.E., 2012. Pensions reform in Nigeria: A comparison between the old

and new scheme. Afro Asian Journal of Social Sciences, 3(3.1), pp.1-17.

Productivity Commission, (2016). Superannuation: alternative default models.

Sargent, L.D., Lee, M.D., Martin, B. and Zikic, J., 2013. Reinventing retirement: New pathways,

new arrangements, new meanings. Human relations, 66(1), pp.3-21.

Siegmann, A., 2011. Minimum funding ratios for defined-benefit pension funds. Journal of

Pension Economics & Finance, 10(3), pp.417-434.

Stebbing, A. and Spies-Butcher, B., 2016. The decline of a homeowning society? Asset-based

welfare, retirement and intergenerational equity in Australia. Housing Studies, 31(2), pp.190-

207.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian Superannuation 11

Williams, R., (2018). Managing superannuation fund investment taxes. Taxation in Australia,

53(2), p.77.

Ntalianis, M. and Wise, V., (2011). The role of financial education in retirement

planning. Australasian Accounting, Business and Finance Journal, 5(2), pp.23-37.

Williams, R., (2018). Managing superannuation fund investment taxes. Taxation in Australia,

53(2), p.77.

Ntalianis, M. and Wise, V., (2011). The role of financial education in retirement

planning. Australasian Accounting, Business and Finance Journal, 5(2), pp.23-37.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.