Australian Superannuation System Essay

VerifiedAdded on 2019/11/25

|11

|2617

|148

Essay

AI Summary

This essay analyzes Australia's superannuation system, examining whether it disproportionately favors the wealthy. It refutes the common misconception that superannuation doesn't reduce government age pension spending, citing data showing significant annual savings. While acknowledging that high-income earners benefit from certain tax concessions, the essay argues that government assistance for retirement is broadly comparable across income brackets, differing mainly in delivery methods (age pension vs. superannuation tax concessions). It highlights that middle-income earners receive the largest share of superannuation tax concessions. The essay concludes with recommendations for improving the system's equity and sustainability, including adjusting policies to better align with its goals, setting a younger preservation age, and applying the superannuation guarantee to income replacement payments. The importance of policy consistency and the principle of adequacy in retirement income are also emphasized.

1

THE AUSTRALIAN SUPERANNUATION SYSTEM

Student’s Name

Professors Name

College

Course

Date

THE AUSTRALIAN SUPERANNUATION SYSTEM

Student’s Name

Professors Name

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

THE AUSTRALIAN SUPERANNUATION SYSTEM

Helping the rich save for retirement”: Does Australia’s superannuation system

favour the rich compared to the poor?

Through the years, there have been constant public debates about the quantum and equity

of tax concessions for superannuation. The primary arguments that surround this have been

embedded on recent government budgets in the face of fiscal challenges as well as the

supernatural and high account balances. Given the nature of this intense debate, it is crucial for

conversations and decision making to take place using an accurate information lens. Currently,

Australia faces an aging population with the characteristics of escalating pension as well as aged

care expenditure. A well-deformed debate on the case study will lay the foundation for

community stakeholders and the government to reach a stable consensus on the potential ways

through which the current superannuation system can be made equitable and sustainable. It is

likely that the government will face challenges in its attempts to set a tax framework policy

aiming at accommodating the expenditure involved in supporting older generations in their

retirement years1. In relation, it is important that the debate is accurate and is not based on myths

that may be credited to inaccurate data or analysis and assertions that lack sufficient evidence.

The role and aim of Australia’s tax concessions for superannuation

One primary argument that research findings suggest is that superannuation saves the

government approximately $7 billion regarding age pension expenditure yearly/annually. Also,

the savings are expected to increase as the system matures. Subsequently, this is contrary to the

widespread myth that superannuation does not help in reducing the government spending with

1 Scott Donald, Hazel Bateman, Ross Buckley, Kevin Liu, and Rob Nicholls. "Too Connected to Fail: The

Regulation of Systemic Risk within Australia's Superannuation System." (Journal of Financial

Regulation 2, no. 1 (2015): 56-78).

THE AUSTRALIAN SUPERANNUATION SYSTEM

Helping the rich save for retirement”: Does Australia’s superannuation system

favour the rich compared to the poor?

Through the years, there have been constant public debates about the quantum and equity

of tax concessions for superannuation. The primary arguments that surround this have been

embedded on recent government budgets in the face of fiscal challenges as well as the

supernatural and high account balances. Given the nature of this intense debate, it is crucial for

conversations and decision making to take place using an accurate information lens. Currently,

Australia faces an aging population with the characteristics of escalating pension as well as aged

care expenditure. A well-deformed debate on the case study will lay the foundation for

community stakeholders and the government to reach a stable consensus on the potential ways

through which the current superannuation system can be made equitable and sustainable. It is

likely that the government will face challenges in its attempts to set a tax framework policy

aiming at accommodating the expenditure involved in supporting older generations in their

retirement years1. In relation, it is important that the debate is accurate and is not based on myths

that may be credited to inaccurate data or analysis and assertions that lack sufficient evidence.

The role and aim of Australia’s tax concessions for superannuation

One primary argument that research findings suggest is that superannuation saves the

government approximately $7 billion regarding age pension expenditure yearly/annually. Also,

the savings are expected to increase as the system matures. Subsequently, this is contrary to the

widespread myth that superannuation does not help in reducing the government spending with

1 Scott Donald, Hazel Bateman, Ross Buckley, Kevin Liu, and Rob Nicholls. "Too Connected to Fail: The

Regulation of Systemic Risk within Australia's Superannuation System." (Journal of Financial

Regulation 2, no. 1 (2015): 56-78).

3

particular regards to the age pension. Superannuation has proved to be a complementary

technique to age pension since it boosts incomes and provides a lifestyle in retirement. Statistics

point out that 32% of individual aged 65 in 2013 were comprehensively fully self-funded in

retirement in retirement up from the 22 per cent in 2000. It is projected that the number will rise

to 43% by the year 2023. According to this year’s report released by an Intergenerational report

(IGR), the reliance of younger retirees on a scale of full age pension is quickly dropping.

However, this statistics is not a reflection of the reliance on the age pension falling. Technically,

this is because the Intergenerational Report examines all retirees and not just those that turn 65.

It is likely that the tightening of the asset test will reduce the percentage of retirees that receive

the age pension2. One particular challenge that is encompassed in the system is ensuring retirees

have sufficient adequate superannuation in retirement. This is in particular regards to the later

years of the retirement of the retirees. Reforms like increasing the superannuation guarantee from

9.2 to 12% as well as the development of longevity products will automatically add the pressure

to the age pension.

As a result of people having superannuation savings, approximately $7 billion

annually is cut from the age pension. The figures, however, are expected to

increase in the future years as more Australians continue to retire with

superannuation balances. Subsequently, this includes:

Approximately $1 billion in savings from 150000 people an inclusive of many

defined benefits schemes.

2 David Ingles, "Does Australia need an annual wealth tax? (And why do we now apply one only to

pensioners)." (Browser Download This Paper 2016).

particular regards to the age pension. Superannuation has proved to be a complementary

technique to age pension since it boosts incomes and provides a lifestyle in retirement. Statistics

point out that 32% of individual aged 65 in 2013 were comprehensively fully self-funded in

retirement in retirement up from the 22 per cent in 2000. It is projected that the number will rise

to 43% by the year 2023. According to this year’s report released by an Intergenerational report

(IGR), the reliance of younger retirees on a scale of full age pension is quickly dropping.

However, this statistics is not a reflection of the reliance on the age pension falling. Technically,

this is because the Intergenerational Report examines all retirees and not just those that turn 65.

It is likely that the tightening of the asset test will reduce the percentage of retirees that receive

the age pension2. One particular challenge that is encompassed in the system is ensuring retirees

have sufficient adequate superannuation in retirement. This is in particular regards to the later

years of the retirement of the retirees. Reforms like increasing the superannuation guarantee from

9.2 to 12% as well as the development of longevity products will automatically add the pressure

to the age pension.

As a result of people having superannuation savings, approximately $7 billion

annually is cut from the age pension. The figures, however, are expected to

increase in the future years as more Australians continue to retire with

superannuation balances. Subsequently, this includes:

Approximately $1 billion in savings from 150000 people an inclusive of many

defined benefits schemes.

2 David Ingles, "Does Australia need an annual wealth tax? (And why do we now apply one only to

pensioners)." (Browser Download This Paper 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Over $3 billion in yearly savings from 160000 people with super balances who

are eligibly fully self-funded.

Around $3 billion in the form of savings from 500000 individuals that receive

$5000 on average

Current tax concessions advantage on high wealth individuals

Although there some counter arguments that argue that its majorly high-income earners

that benefit from government support regarding retirement. On the contrary, it is true to say that

financial assistance for retirement that is provided by the government can be considered broadly

comparable across the personal income tax brackets. The nature on the ground is that all

Australians get access to financial support for their retirement through either tax concessions to

fund their retirement through superannuation or age pension. At times, individuals use a

combination of both. True to say, all Australians receive approximately $300000 across all tax

brackets. Subsequently, this is a direct contribution of the government to their retirement. The

main difference, however, is embedded in the timing and vehicles through which it is delivered.

A relevant example is that the full age pension for a single person is technically at $22,542

annually3.

Tax concessions for superannuation technically are for smaller annual amounts that are

spread over some years. Simply put, all individuals receive the same government assistance

regarding retirement benefits. The only difference is that the timing and vehicle through which

the same is delivered comprehensively differs. To extensively explain this further, a lower

income person will receive the compensation in the form of age pension, low-income

3 Panha Heng, Scott J. Niblock, and Jennifer L. Harrison. "Retirement policy: a review of the role,

characteristics, and contribution of the Australian superannuation system." (Asian

‐Pacific Economic

Literature 29, no. 2 (2015): 1-17).

Over $3 billion in yearly savings from 160000 people with super balances who

are eligibly fully self-funded.

Around $3 billion in the form of savings from 500000 individuals that receive

$5000 on average

Current tax concessions advantage on high wealth individuals

Although there some counter arguments that argue that its majorly high-income earners

that benefit from government support regarding retirement. On the contrary, it is true to say that

financial assistance for retirement that is provided by the government can be considered broadly

comparable across the personal income tax brackets. The nature on the ground is that all

Australians get access to financial support for their retirement through either tax concessions to

fund their retirement through superannuation or age pension. At times, individuals use a

combination of both. True to say, all Australians receive approximately $300000 across all tax

brackets. Subsequently, this is a direct contribution of the government to their retirement. The

main difference, however, is embedded in the timing and vehicles through which it is delivered.

A relevant example is that the full age pension for a single person is technically at $22,542

annually3.

Tax concessions for superannuation technically are for smaller annual amounts that are

spread over some years. Simply put, all individuals receive the same government assistance

regarding retirement benefits. The only difference is that the timing and vehicle through which

the same is delivered comprehensively differs. To extensively explain this further, a lower

income person will receive the compensation in the form of age pension, low-income

3 Panha Heng, Scott J. Niblock, and Jennifer L. Harrison. "Retirement policy: a review of the role,

characteristics, and contribution of the Australian superannuation system." (Asian

‐Pacific Economic

Literature 29, no. 2 (2015): 1-17).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

superannuation contribution and confessional taxed contribution. On the other hand, an

individual in the top income tax bracket receives the compensation as tax concessions for super.

Most of the times, many individuals receive a set combination of all of these. Also, it is

important to point out that government assistance that is set aside for very high-income levels

has been reduced through what has been referred to as lower caps for concessional tax

contributions to super.

Regarding current tax concessions being advantageous for high wealth individuals, in

contrary to the common myth that a bulk of tax concessions for superannuation is directed to

high-income earners, the authentic scenario is that the bulk of tax concessions contributions

benefit middle-income earners most. Usually, the tax concessions in connection to

superannuation concessional contributions are skewed towards the bulk of the community in the

working category to save for their retirement4. According to an analysis by ASFA, approximately

73% of tax concessions was directed to those paying either middle-income marginal tax rates

stretching across 30-38% as well as those who earned between $37000-$180,000 annually in the

years from 2011-2012. Relatively, this is an indication that the contribution gaps have

substantially lowered and is also working to enhance the reduction of concessional contributions

which is comprised of upper-income earners. Subsequently, this continuously will provide

support to many Australians through helping them save for retirement. Another important aspect

to analyse however that is some individuals accumulated high superannuation balances as a

result of contributions and the transfers effected before the contribution caps was legalized 5. In

4 David Ingles,. "Does Australia need an annual wealth tax?(And why do we now apply one only to

pensioners)."( Browser Download This Paper (2016).

5 Alexandra Spicer, Olena Stavrunova, and Susan Thorp. "How portfolios evolve after retirement: Evidence

from Australia." (Economic Record 92, no. 297 (2016): 241-267).

superannuation contribution and confessional taxed contribution. On the other hand, an

individual in the top income tax bracket receives the compensation as tax concessions for super.

Most of the times, many individuals receive a set combination of all of these. Also, it is

important to point out that government assistance that is set aside for very high-income levels

has been reduced through what has been referred to as lower caps for concessional tax

contributions to super.

Regarding current tax concessions being advantageous for high wealth individuals, in

contrary to the common myth that a bulk of tax concessions for superannuation is directed to

high-income earners, the authentic scenario is that the bulk of tax concessions contributions

benefit middle-income earners most. Usually, the tax concessions in connection to

superannuation concessional contributions are skewed towards the bulk of the community in the

working category to save for their retirement4. According to an analysis by ASFA, approximately

73% of tax concessions was directed to those paying either middle-income marginal tax rates

stretching across 30-38% as well as those who earned between $37000-$180,000 annually in the

years from 2011-2012. Relatively, this is an indication that the contribution gaps have

substantially lowered and is also working to enhance the reduction of concessional contributions

which is comprised of upper-income earners. Subsequently, this continuously will provide

support to many Australians through helping them save for retirement. Another important aspect

to analyse however that is some individuals accumulated high superannuation balances as a

result of contributions and the transfers effected before the contribution caps was legalized 5. In

4 David Ingles,. "Does Australia need an annual wealth tax?(And why do we now apply one only to

pensioners)."( Browser Download This Paper (2016).

5 Alexandra Spicer, Olena Stavrunova, and Susan Thorp. "How portfolios evolve after retirement: Evidence

from Australia." (Economic Record 92, no. 297 (2016): 241-267).

6

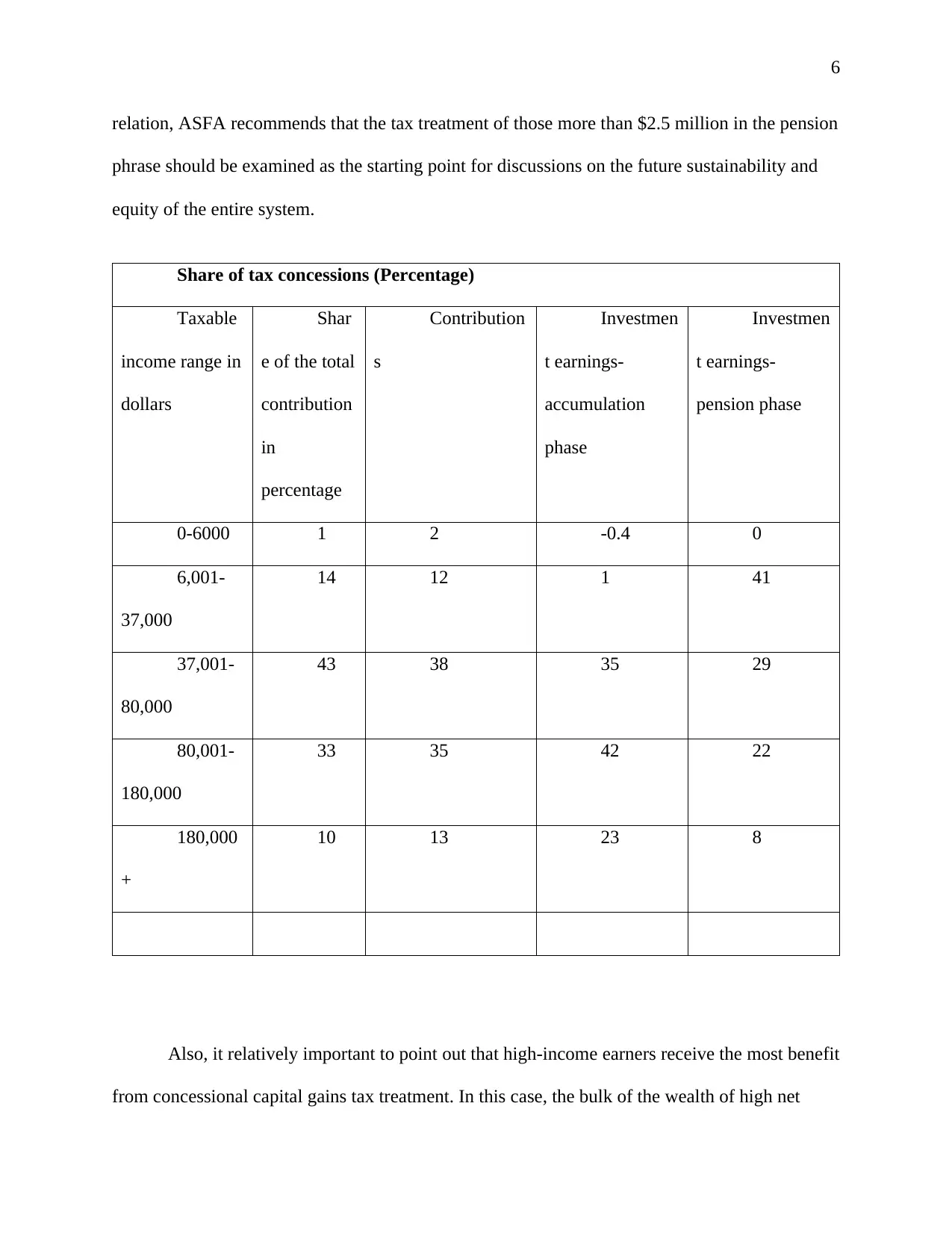

relation, ASFA recommends that the tax treatment of those more than $2.5 million in the pension

phrase should be examined as the starting point for discussions on the future sustainability and

equity of the entire system.

Share of tax concessions (Percentage)

Taxable

income range in

dollars

Shar

e of the total

contribution

in

percentage

Contribution

s

Investmen

t earnings-

accumulation

phase

Investmen

t earnings-

pension phase

0-6000 1 2 -0.4 0

6,001-

37,000

14 12 1 41

37,001-

80,000

43 38 35 29

80,001-

180,000

33 35 42 22

180,000

+

10 13 23 8

Also, it relatively important to point out that high-income earners receive the most benefit

from concessional capital gains tax treatment. In this case, the bulk of the wealth of high net

relation, ASFA recommends that the tax treatment of those more than $2.5 million in the pension

phrase should be examined as the starting point for discussions on the future sustainability and

equity of the entire system.

Share of tax concessions (Percentage)

Taxable

income range in

dollars

Shar

e of the total

contribution

in

percentage

Contribution

s

Investmen

t earnings-

accumulation

phase

Investmen

t earnings-

pension phase

0-6000 1 2 -0.4 0

6,001-

37,000

14 12 1 41

37,001-

80,000

43 38 35 29

80,001-

180,000

33 35 42 22

180,000

+

10 13 23 8

Also, it relatively important to point out that high-income earners receive the most benefit

from concessional capital gains tax treatment. In this case, the bulk of the wealth of high net

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

worth in the form of shareholdings or property, commercial real estate and both residential

investment properties. Also, it is only just a slight over figure of 20% of the total $1.6 trillion

investable assets that are held by technically high net worth individuals. Also, around $300

billion in an approximated total is held by individuals with more than $ 1 million in

superannuation6. Simply put, the highest net worth individuals are likely to have a tremendous

impact on the achievement as well as maintenance of wealth than superannuation tax

concessions through capital gains, family home, and negative gearing.

Recommendations focusing on the tax system about what Australia should do to

provide for its aging population’s retirement

The following section will comprehensively discuss insights and recommendations about

what Australia should adopt to provide for its aging population retirement. Superannuation is a

vital component that will play and will continue to play a fundamental role in providing the

foundations of the economic activities as well as prosperity. One of its primary advantages is that

it lifts household savings by around two points regarding GDP with the increase in compulsory

SG from 9-12%. In relation, this helps the government and Australian business to finance

investment and infrastructure without particularly relying on aspects such as foreign savings and

investment. One of the central suggestion that can be employed by the state to provide for its

aging population is advocating for higher levels of domestic savings which will in return reduce

the cost of capital in the country7. As a result, this will influence and lead to stronger economic

growth for the country as a whole. As people move into retirement, supernatural benefits such as

6 Siobhan Austen, Rhonda Sharp, and Helen Hodgson. "Gender impact analysis and the taxation of

retirement savings in Australia." (2015).

7 , Anne-Marie Brook. Options to narrow New Zealand's saving-investment imbalance.( No. 14/17. New

Zealand Treasury, 2014).

worth in the form of shareholdings or property, commercial real estate and both residential

investment properties. Also, it is only just a slight over figure of 20% of the total $1.6 trillion

investable assets that are held by technically high net worth individuals. Also, around $300

billion in an approximated total is held by individuals with more than $ 1 million in

superannuation6. Simply put, the highest net worth individuals are likely to have a tremendous

impact on the achievement as well as maintenance of wealth than superannuation tax

concessions through capital gains, family home, and negative gearing.

Recommendations focusing on the tax system about what Australia should do to

provide for its aging population’s retirement

The following section will comprehensively discuss insights and recommendations about

what Australia should adopt to provide for its aging population retirement. Superannuation is a

vital component that will play and will continue to play a fundamental role in providing the

foundations of the economic activities as well as prosperity. One of its primary advantages is that

it lifts household savings by around two points regarding GDP with the increase in compulsory

SG from 9-12%. In relation, this helps the government and Australian business to finance

investment and infrastructure without particularly relying on aspects such as foreign savings and

investment. One of the central suggestion that can be employed by the state to provide for its

aging population is advocating for higher levels of domestic savings which will in return reduce

the cost of capital in the country7. As a result, this will influence and lead to stronger economic

growth for the country as a whole. As people move into retirement, supernatural benefits such as

6 Siobhan Austen, Rhonda Sharp, and Helen Hodgson. "Gender impact analysis and the taxation of

retirement savings in Australia." (2015).

7 , Anne-Marie Brook. Options to narrow New Zealand's saving-investment imbalance.( No. 14/17. New

Zealand Treasury, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

insurance payouts and pension payments demand over a total of $50 billion annually; this is

expected to quadruple by the time 2040 approaches. Relatively, the aging population is most

likely to be the cause of a slower rate of GDP growth. Technically this is where the concept of

superannuation joins the conversation. This is because, without the availability of

superannuation, the reduction is likely to be much intense. The primary ideology behind this is

that superannuation provides business with the consumers of the future. As a result, this is

expected to deliver a boost which in return will benefit all Australians.

Another important aspect that Australia needs to work on revolves around improving the

system to better align with its principles and goals ideology. Policies need to be adjusted to

ensure the operational system delivers for the targeted groups of Australians. Although this is a

general recommendation, more specific recommendations include:

Setting superannuation preservation age at five years younger than the normal age

pension age which is at a maximum of 62.

Applying the SG to substantiate income replacement payments.

Building a review mechanism concerning SG rate into the Inter-Generational

Report.

Allowing access to the income stream from ages such as 55-60 specifically to

those who have been unemployed for a specified duration.

Policy principles intervention is also an important aspect that needs to be

comprehensively examined. In the past decades, superannuation systems have been subject to a

degree of policy inconsistency. As a result, this has led to reduced confidence in the reliability of

insurance payouts and pension payments demand over a total of $50 billion annually; this is

expected to quadruple by the time 2040 approaches. Relatively, the aging population is most

likely to be the cause of a slower rate of GDP growth. Technically this is where the concept of

superannuation joins the conversation. This is because, without the availability of

superannuation, the reduction is likely to be much intense. The primary ideology behind this is

that superannuation provides business with the consumers of the future. As a result, this is

expected to deliver a boost which in return will benefit all Australians.

Another important aspect that Australia needs to work on revolves around improving the

system to better align with its principles and goals ideology. Policies need to be adjusted to

ensure the operational system delivers for the targeted groups of Australians. Although this is a

general recommendation, more specific recommendations include:

Setting superannuation preservation age at five years younger than the normal age

pension age which is at a maximum of 62.

Applying the SG to substantiate income replacement payments.

Building a review mechanism concerning SG rate into the Inter-Generational

Report.

Allowing access to the income stream from ages such as 55-60 specifically to

those who have been unemployed for a specified duration.

Policy principles intervention is also an important aspect that needs to be

comprehensively examined. In the past decades, superannuation systems have been subject to a

degree of policy inconsistency. As a result, this has led to reduced confidence in the reliability of

9

the system8. Technically, the position of superannuation as a long term investment, it is critical to

maintaining consumer confidence. To create such an environment, it is vital to have the

underlying policies defined on which the system is expected to be based. One primary argument

by ASFA on the same is that principles such as adequacy should underpin retirement income

policy decisions.

In this case, the primary purpose of having a retirement income policy should be

embedded on ensuring many people have an adequate income in their retirement. Subsequently,

the underlying goal is to minimize the number of retirees that live in relative poverty or poverty

and alternatively maximize the number of the retirees that live in comfort and dignity.

Bibliography

Austen, Siobhan, Rhonda Sharp, and Helen Hodgson. "Gender impact analysis and the taxation of retirement

savings in Australia." (2015).

Brook, Anne-Marie. Options to narrow New Zealand's saving-investment imbalance. No. 14/17. New Zealand

Treasury, 2014.

8 Sue Taylor, Anthony Asher, and Julie Anne Tarr. "Accountability in Regulatory Reform: (Australia's

Superannuation Industry Paradox." Fed. L. Rev. 45 (2017): 257.)

the system8. Technically, the position of superannuation as a long term investment, it is critical to

maintaining consumer confidence. To create such an environment, it is vital to have the

underlying policies defined on which the system is expected to be based. One primary argument

by ASFA on the same is that principles such as adequacy should underpin retirement income

policy decisions.

In this case, the primary purpose of having a retirement income policy should be

embedded on ensuring many people have an adequate income in their retirement. Subsequently,

the underlying goal is to minimize the number of retirees that live in relative poverty or poverty

and alternatively maximize the number of the retirees that live in comfort and dignity.

Bibliography

Austen, Siobhan, Rhonda Sharp, and Helen Hodgson. "Gender impact analysis and the taxation of retirement

savings in Australia." (2015).

Brook, Anne-Marie. Options to narrow New Zealand's saving-investment imbalance. No. 14/17. New Zealand

Treasury, 2014.

8 Sue Taylor, Anthony Asher, and Julie Anne Tarr. "Accountability in Regulatory Reform: (Australia's

Superannuation Industry Paradox." Fed. L. Rev. 45 (2017): 257.)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Donald, Scott, Hazel Bateman, Ross Buckley, Kevin Liu, and Rob Nicholls. "Too Connected to Fail: The

Regulation of Systemic Risk within Australia's Superannuation System." Journal of Financial

Regulation 2, no. 1 (2015): 56-78.

Ghilarducci, Teresa, and Hamilton James. A Comprehensive Plan to Confront the Retirement Savings Crisis. No.

2016-01. Schwartz Center for Economic Policy Analysis (SCEPA), The New School, 2016.

Heng, Panha, Scott J. Niblock, and Jennifer L. Harrison. "Retirement policy: a review of the role, characteristics,

and contribution of the Australian superannuation system." Asian

‐Pacific Economic Literature 29, no. 2

(2015): 1-17.

Hulley, Hardy, Rebecca Mckibbin, Andreas Pedersen, and Susan Thorp. "Means‐Tested Public Pensions, Portfolio

Choice and Decumulation in Retirement." Economic Record 89, no. 284 (2013): 31-51.

Ingles, David, and Miranda Stewart. "Superannuation tax concessions and the age pension: a principled approach to

savings taxation." (2015).

Ingles, David. "Does Australia need an annual wealth tax?(And why do we now apply one only to

pensioners)." Browser Download This Paper (2016).

Ingles, David. "Pensions and superannuation: the need for change." The Australia Institute (2014).

Littlewood, Michael R. "Ageing populations, retirement incomes and public policy: what really matters." Browser

Download This Paper (2014).

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in Australia." St Mark's

Review 235 (2016): 94.

Mathur, Virad. "Time to rethink superannuation." Quadrant 58, no. 7/8 (2014): 95.

Millane, Emily. The Entitlement of Age. Per Capita, 2014.

Nicholls, Rob, M. Scott Donald, and Kevin Liu. "It's a Small World after All: Using Social Network Analysis to

Investigate Systemic Risk in the Australian Superannuation Sector." (2015).

Nisbet, Elise Torunn. "Influence of Board Structure on the Performance and Governance Framework of Australia’s

Superannuation Funds." (2013).

Rayner, Jennifer. Generation less: How Australia is cheating the young. Vol. 9. Black Inc., 2016.

Spicer, Alexandra, Olena Stavrunova, and Susan Thorp. "How portfolios evolve after retirement: Evidence from

Australia." Economic Record 92, no. 297 (2016): 241-267.

Donald, Scott, Hazel Bateman, Ross Buckley, Kevin Liu, and Rob Nicholls. "Too Connected to Fail: The

Regulation of Systemic Risk within Australia's Superannuation System." Journal of Financial

Regulation 2, no. 1 (2015): 56-78.

Ghilarducci, Teresa, and Hamilton James. A Comprehensive Plan to Confront the Retirement Savings Crisis. No.

2016-01. Schwartz Center for Economic Policy Analysis (SCEPA), The New School, 2016.

Heng, Panha, Scott J. Niblock, and Jennifer L. Harrison. "Retirement policy: a review of the role, characteristics,

and contribution of the Australian superannuation system." Asian

‐Pacific Economic Literature 29, no. 2

(2015): 1-17.

Hulley, Hardy, Rebecca Mckibbin, Andreas Pedersen, and Susan Thorp. "Means‐Tested Public Pensions, Portfolio

Choice and Decumulation in Retirement." Economic Record 89, no. 284 (2013): 31-51.

Ingles, David, and Miranda Stewart. "Superannuation tax concessions and the age pension: a principled approach to

savings taxation." (2015).

Ingles, David. "Does Australia need an annual wealth tax?(And why do we now apply one only to

pensioners)." Browser Download This Paper (2016).

Ingles, David. "Pensions and superannuation: the need for change." The Australia Institute (2014).

Littlewood, Michael R. "Ageing populations, retirement incomes and public policy: what really matters." Browser

Download This Paper (2014).

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in Australia." St Mark's

Review 235 (2016): 94.

Mathur, Virad. "Time to rethink superannuation." Quadrant 58, no. 7/8 (2014): 95.

Millane, Emily. The Entitlement of Age. Per Capita, 2014.

Nicholls, Rob, M. Scott Donald, and Kevin Liu. "It's a Small World after All: Using Social Network Analysis to

Investigate Systemic Risk in the Australian Superannuation Sector." (2015).

Nisbet, Elise Torunn. "Influence of Board Structure on the Performance and Governance Framework of Australia’s

Superannuation Funds." (2013).

Rayner, Jennifer. Generation less: How Australia is cheating the young. Vol. 9. Black Inc., 2016.

Spicer, Alexandra, Olena Stavrunova, and Susan Thorp. "How portfolios evolve after retirement: Evidence from

Australia." Economic Record 92, no. 297 (2016): 241-267.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Strano, Christopher, and Dale Pinto. "A comparative analysis of Australian and Hong Kong retirement

systems." eJournal of Tax Research 14, no. 1 (2016): 34.

Taylor, Sue, Anthony Asher, and Julie Anne Tarr. "Accountability in Regulatory Reform: Australia's

Superannuation Industry Paradox." Fed. L. Rev. 45 (2017): 257.

Strano, Christopher, and Dale Pinto. "A comparative analysis of Australian and Hong Kong retirement

systems." eJournal of Tax Research 14, no. 1 (2016): 34.

Taylor, Sue, Anthony Asher, and Julie Anne Tarr. "Accountability in Regulatory Reform: Australia's

Superannuation Industry Paradox." Fed. L. Rev. 45 (2017): 257.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.