Report on Statistical Analysis of Australian Taxation Data

VerifiedAdded on 2020/05/16

|16

|2432

|58

Report

AI Summary

This report analyzes Australian taxation data, focusing on taxpayer lodgement methods. The study examines the proportions of taxpayers using tax agents versus self-preparing, including a comparison of international students. Statistical methods, including confidence intervals and hypothesis testing, are used to compare these proportions. The report investigates the relationship between lodgement methods and age groups using a chi-square test. Furthermore, a descriptive analysis of income and deductions based on lodgement methods is presented, including regression analysis to predict deductions from income. The findings reveal significant differences in lodgement preferences between Australian taxpayers and international students, as well as associations between age, income, and the choice of lodgement method.

Running head: STATISTICS AND DATA ANALYSIS

Statistics and data analysis

Name of the student

Name of the university

Author’s note

Statistics and data analysis

Name of the student

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1STATISTICS AND DATA ANALYSIS

Table of Contents

Section 1..........................................................................................................................................2

Section 2..........................................................................................................................................2

Section 3..........................................................................................................................................3

Section 4..........................................................................................................................................6

Section 5..........................................................................................................................................8

Section 6........................................................................................................................................11

Section 7: Conclusion....................................................................................................................13

References......................................................................................................................................15

Table of Contents

Section 1..........................................................................................................................................2

Section 2..........................................................................................................................................2

Section 3..........................................................................................................................................3

Section 4..........................................................................................................................................6

Section 5..........................................................................................................................................8

Section 6........................................................................................................................................11

Section 7: Conclusion....................................................................................................................13

References......................................................................................................................................15

2STATISTICS AND DATA ANALYSIS

Section 1

The present assignment is a study on the lodgement method of Australian tax payers. Tax

payers in Australia can pay their tax either through tax agents or Self-prepare their returns. The

Australian taxation department from time to time takes initiatives to educate the tax payers

(Chardon, Freudenberg and Brimble 2016). For the analysis a primary data has been taken from

the Australian taxation office. A sample of the data has been selected for the study. In the present

study we have analysed the proportion of tax payers based on lodgement methods. We also have

compared the data with lodgement method of international students. In addition, we have tried to

find relation between lodgement method and age groups. Further, a relation between total

income and deductions based on lodgement methods has also been found.

Table 1: First five cases of dataset 1

Gender age_range Lodgment_method Tot_inc_amt Tot_ded_amt

1 9 S 47838 143

0 10 A 18606 499

1 7 A 99229 3232

1 9 S 49815 2035

0 11 S 17903 0

We have also studied the proportion of lodgement process of international students. Data

of lodgement methods from 60 international students was collected. The proportion of students

using tax agents was compared with the proportion of Australian tax payers.

Section 2

Table 2: Proportion of Australian Tax payers according to Lodgement

Lodgement Method Count Proportion

Tax Agent 754 0.754

Self-Preparer 246 0.246

Total 1000 1

The data on taxation lodgement of 1000 people of Australia shows that 754 people pay

their taxes through tax agents. On the other hand, only 246 people self-prepare their taxes.

Hence, it can be inferred that 75.4% of the population pay taxes by hiring agents who have the

knowledge of paying taxes.

Section 1

The present assignment is a study on the lodgement method of Australian tax payers. Tax

payers in Australia can pay their tax either through tax agents or Self-prepare their returns. The

Australian taxation department from time to time takes initiatives to educate the tax payers

(Chardon, Freudenberg and Brimble 2016). For the analysis a primary data has been taken from

the Australian taxation office. A sample of the data has been selected for the study. In the present

study we have analysed the proportion of tax payers based on lodgement methods. We also have

compared the data with lodgement method of international students. In addition, we have tried to

find relation between lodgement method and age groups. Further, a relation between total

income and deductions based on lodgement methods has also been found.

Table 1: First five cases of dataset 1

Gender age_range Lodgment_method Tot_inc_amt Tot_ded_amt

1 9 S 47838 143

0 10 A 18606 499

1 7 A 99229 3232

1 9 S 49815 2035

0 11 S 17903 0

We have also studied the proportion of lodgement process of international students. Data

of lodgement methods from 60 international students was collected. The proportion of students

using tax agents was compared with the proportion of Australian tax payers.

Section 2

Table 2: Proportion of Australian Tax payers according to Lodgement

Lodgement Method Count Proportion

Tax Agent 754 0.754

Self-Preparer 246 0.246

Total 1000 1

The data on taxation lodgement of 1000 people of Australia shows that 754 people pay

their taxes through tax agents. On the other hand, only 246 people self-prepare their taxes.

Hence, it can be inferred that 75.4% of the population pay taxes by hiring agents who have the

knowledge of paying taxes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3STATISTICS AND DATA ANALYSIS

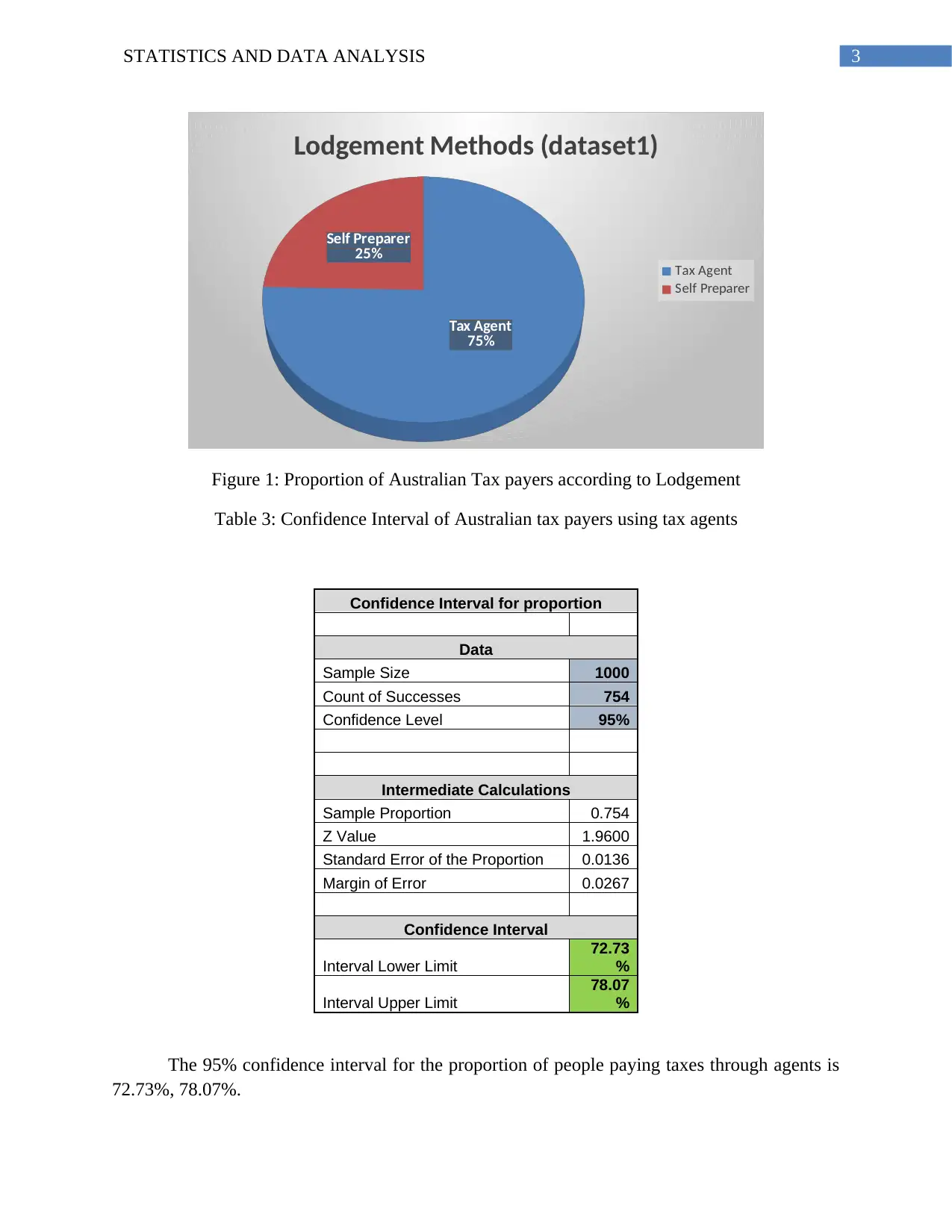

Tax Agent

75%

Self Preparer

25%

Lodgement Methods (dataset1)

Tax Agent

Self Preparer

Figure 1: Proportion of Australian Tax payers according to Lodgement

Table 3: Confidence Interval of Australian tax payers using tax agents

Confidence Interval for proportion

Data

Sample Size 1000

Count of Successes 754

Confidence Level 95%

Intermediate Calculations

Sample Proportion 0.754

Z Value 1.9600

Standard Error of the Proportion 0.0136

Margin of Error 0.0267

Confidence Interval

Interval Lower Limit

72.73

%

Interval Upper Limit

78.07

%

The 95% confidence interval for the proportion of people paying taxes through agents is

72.73%, 78.07%.

Tax Agent

75%

Self Preparer

25%

Lodgement Methods (dataset1)

Tax Agent

Self Preparer

Figure 1: Proportion of Australian Tax payers according to Lodgement

Table 3: Confidence Interval of Australian tax payers using tax agents

Confidence Interval for proportion

Data

Sample Size 1000

Count of Successes 754

Confidence Level 95%

Intermediate Calculations

Sample Proportion 0.754

Z Value 1.9600

Standard Error of the Proportion 0.0136

Margin of Error 0.0267

Confidence Interval

Interval Lower Limit

72.73

%

Interval Upper Limit

78.07

%

The 95% confidence interval for the proportion of people paying taxes through agents is

72.73%, 78.07%.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4STATISTICS AND DATA ANALYSIS

The sample dataset from the Australia taxation office shows that 75.4% of the people pay

their taxes through Tax agents. In addition, if another sample dataset is taken then it can be said

with 95% confidence that the proportion of people paying their taxes through agents would lie

between 72.73% and 78.07%. The above predictions have a 2.67% margin of error.

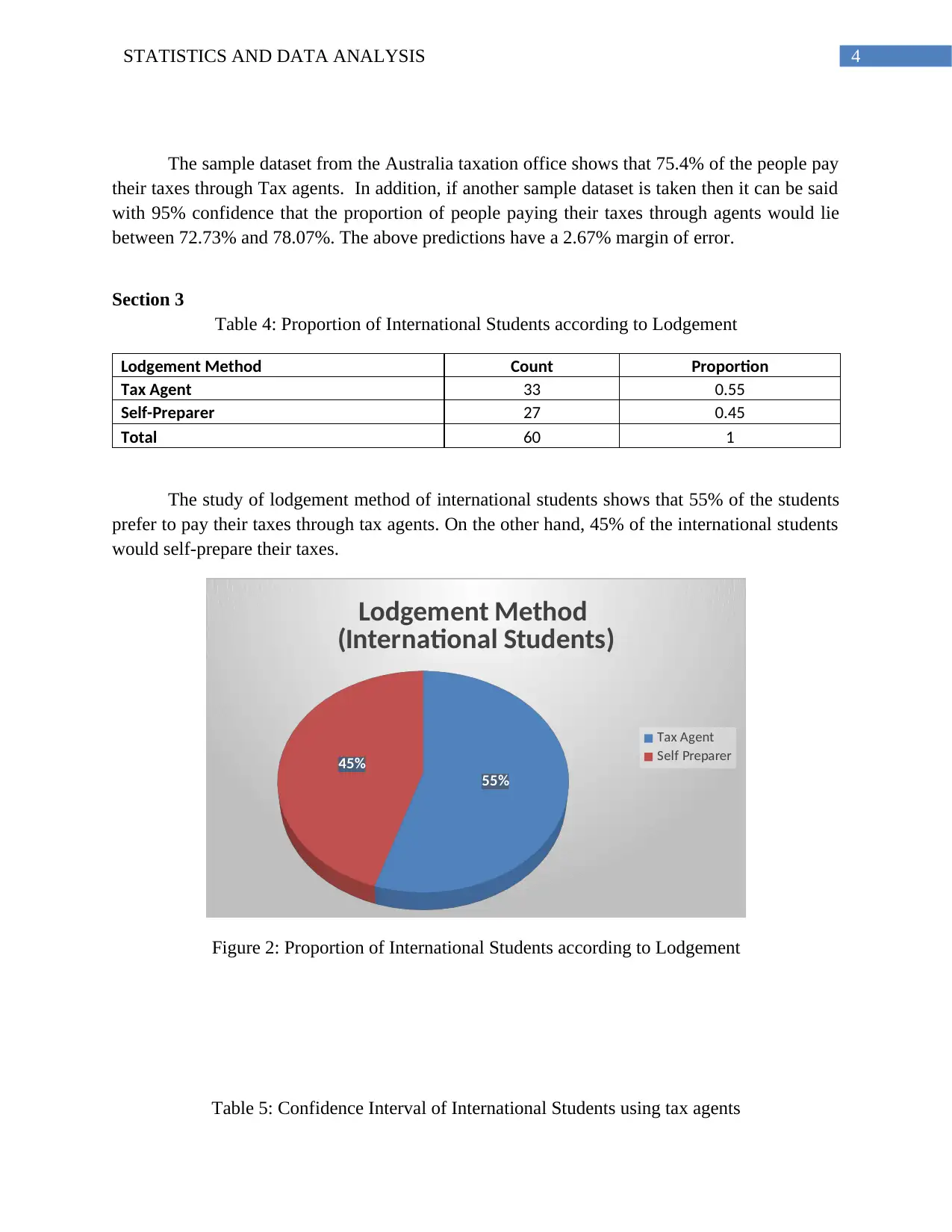

Section 3

Table 4: Proportion of International Students according to Lodgement

Lodgement Method Count Proportion

Tax Agent 33 0.55

Self-Preparer 27 0.45

Total 60 1

The study of lodgement method of international students shows that 55% of the students

prefer to pay their taxes through tax agents. On the other hand, 45% of the international students

would self-prepare their taxes.

55%

45%

Lodgement Method

(International Students)

Tax Agent

Self Preparer

Figure 2: Proportion of International Students according to Lodgement

Table 5: Confidence Interval of International Students using tax agents

The sample dataset from the Australia taxation office shows that 75.4% of the people pay

their taxes through Tax agents. In addition, if another sample dataset is taken then it can be said

with 95% confidence that the proportion of people paying their taxes through agents would lie

between 72.73% and 78.07%. The above predictions have a 2.67% margin of error.

Section 3

Table 4: Proportion of International Students according to Lodgement

Lodgement Method Count Proportion

Tax Agent 33 0.55

Self-Preparer 27 0.45

Total 60 1

The study of lodgement method of international students shows that 55% of the students

prefer to pay their taxes through tax agents. On the other hand, 45% of the international students

would self-prepare their taxes.

55%

45%

Lodgement Method

(International Students)

Tax Agent

Self Preparer

Figure 2: Proportion of International Students according to Lodgement

Table 5: Confidence Interval of International Students using tax agents

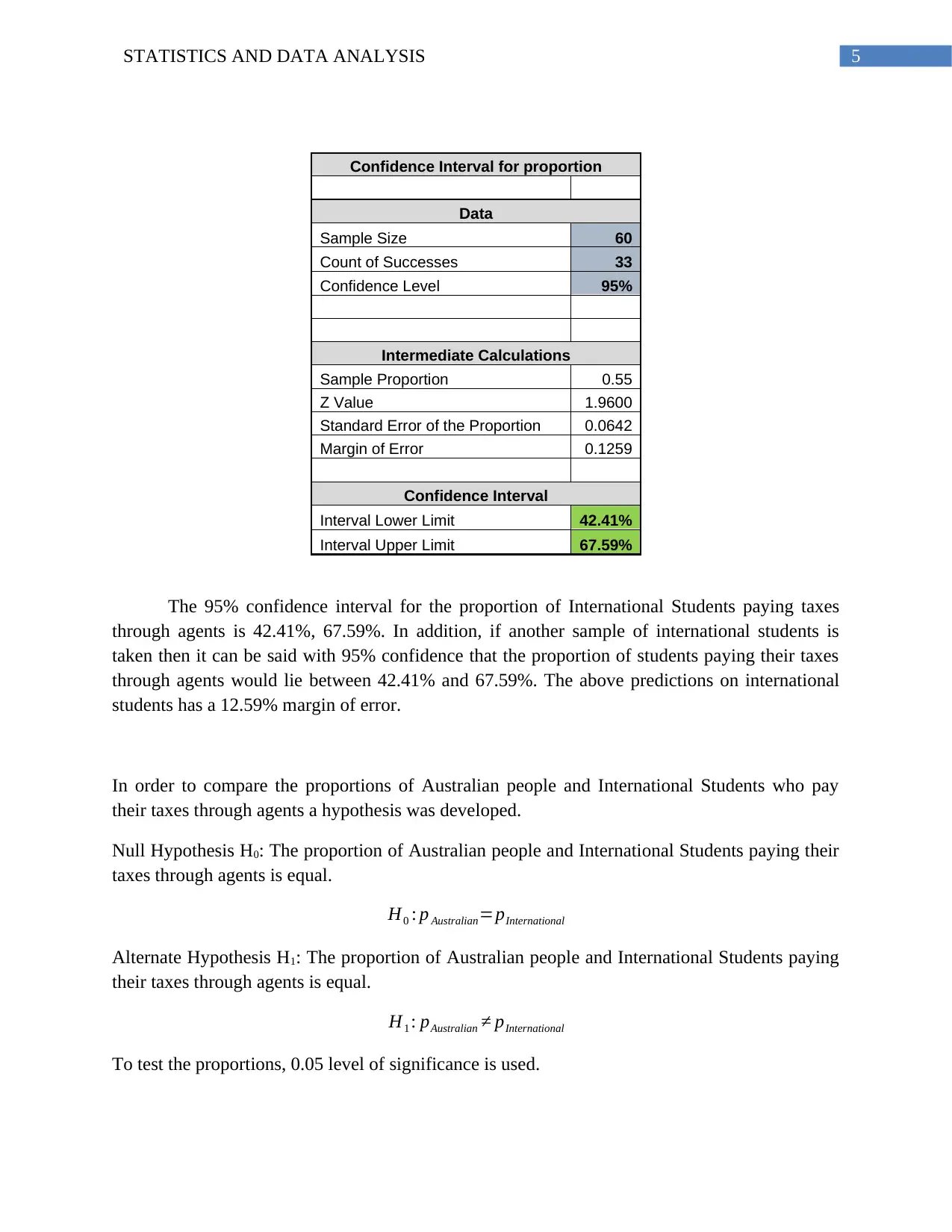

5STATISTICS AND DATA ANALYSIS

Confidence Interval for proportion

Data

Sample Size 60

Count of Successes 33

Confidence Level 95%

Intermediate Calculations

Sample Proportion 0.55

Z Value 1.9600

Standard Error of the Proportion 0.0642

Margin of Error 0.1259

Confidence Interval

Interval Lower Limit 42.41%

Interval Upper Limit 67.59%

The 95% confidence interval for the proportion of International Students paying taxes

through agents is 42.41%, 67.59%. In addition, if another sample of international students is

taken then it can be said with 95% confidence that the proportion of students paying their taxes

through agents would lie between 42.41% and 67.59%. The above predictions on international

students has a 12.59% margin of error.

In order to compare the proportions of Australian people and International Students who pay

their taxes through agents a hypothesis was developed.

Null Hypothesis H0: The proportion of Australian people and International Students paying their

taxes through agents is equal.

H0 : p Australian=pInternational

Alternate Hypothesis H1: The proportion of Australian people and International Students paying

their taxes through agents is equal.

H1 : pAustralian ≠ pInternational

To test the proportions, 0.05 level of significance is used.

Confidence Interval for proportion

Data

Sample Size 60

Count of Successes 33

Confidence Level 95%

Intermediate Calculations

Sample Proportion 0.55

Z Value 1.9600

Standard Error of the Proportion 0.0642

Margin of Error 0.1259

Confidence Interval

Interval Lower Limit 42.41%

Interval Upper Limit 67.59%

The 95% confidence interval for the proportion of International Students paying taxes

through agents is 42.41%, 67.59%. In addition, if another sample of international students is

taken then it can be said with 95% confidence that the proportion of students paying their taxes

through agents would lie between 42.41% and 67.59%. The above predictions on international

students has a 12.59% margin of error.

In order to compare the proportions of Australian people and International Students who pay

their taxes through agents a hypothesis was developed.

Null Hypothesis H0: The proportion of Australian people and International Students paying their

taxes through agents is equal.

H0 : p Australian=pInternational

Alternate Hypothesis H1: The proportion of Australian people and International Students paying

their taxes through agents is equal.

H1 : pAustralian ≠ pInternational

To test the proportions, 0.05 level of significance is used.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6STATISTICS AND DATA ANALYSIS

Thus if the p-value for the test is less than 0.05 then we would reject Null Hypothesis, else accept

it.

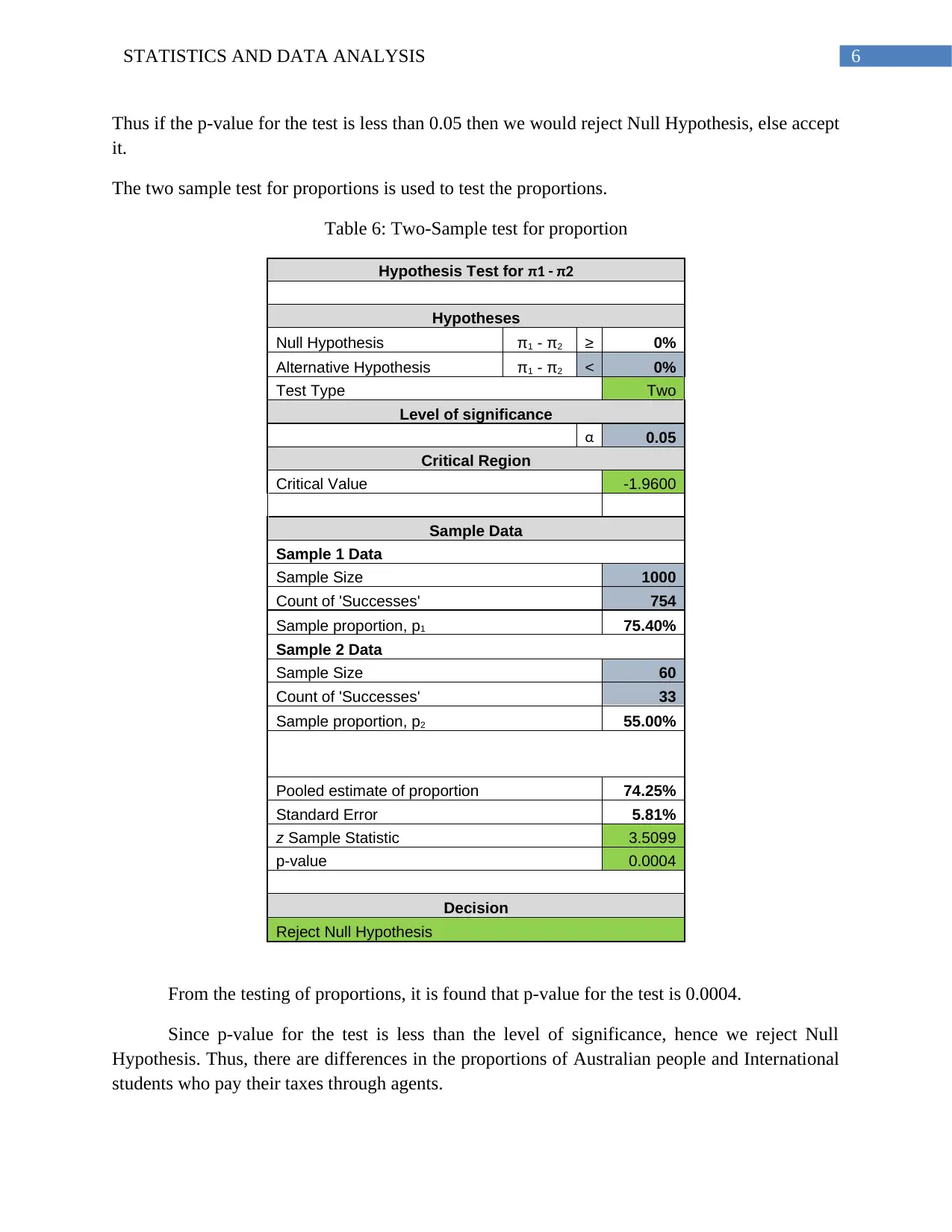

The two sample test for proportions is used to test the proportions.

Table 6: Two-Sample test for proportion

Hypothesis Test for π1 - π2

Hypotheses

Null Hypothesis π1 - π2 ≥ 0%

Alternative Hypothesis π1 - π2 < 0%

Test Type Two

Level of significance

α 0.05

Critical Region

Critical Value -1.9600

Sample Data

Sample 1 Data

Sample Size 1000

Count of 'Successes' 754

Sample proportion, p1 75.40%

Sample 2 Data

Sample Size 60

Count of 'Successes' 33

Sample proportion, p2 55.00%

Pooled estimate of proportion 74.25%

Standard Error 5.81%

z Sample Statistic 3.5099

p-value 0.0004

Decision

Reject Null Hypothesis

From the testing of proportions, it is found that p-value for the test is 0.0004.

Since p-value for the test is less than the level of significance, hence we reject Null

Hypothesis. Thus, there are differences in the proportions of Australian people and International

students who pay their taxes through agents.

Thus if the p-value for the test is less than 0.05 then we would reject Null Hypothesis, else accept

it.

The two sample test for proportions is used to test the proportions.

Table 6: Two-Sample test for proportion

Hypothesis Test for π1 - π2

Hypotheses

Null Hypothesis π1 - π2 ≥ 0%

Alternative Hypothesis π1 - π2 < 0%

Test Type Two

Level of significance

α 0.05

Critical Region

Critical Value -1.9600

Sample Data

Sample 1 Data

Sample Size 1000

Count of 'Successes' 754

Sample proportion, p1 75.40%

Sample 2 Data

Sample Size 60

Count of 'Successes' 33

Sample proportion, p2 55.00%

Pooled estimate of proportion 74.25%

Standard Error 5.81%

z Sample Statistic 3.5099

p-value 0.0004

Decision

Reject Null Hypothesis

From the testing of proportions, it is found that p-value for the test is 0.0004.

Since p-value for the test is less than the level of significance, hence we reject Null

Hypothesis. Thus, there are differences in the proportions of Australian people and International

students who pay their taxes through agents.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7STATISTICS AND DATA ANALYSIS

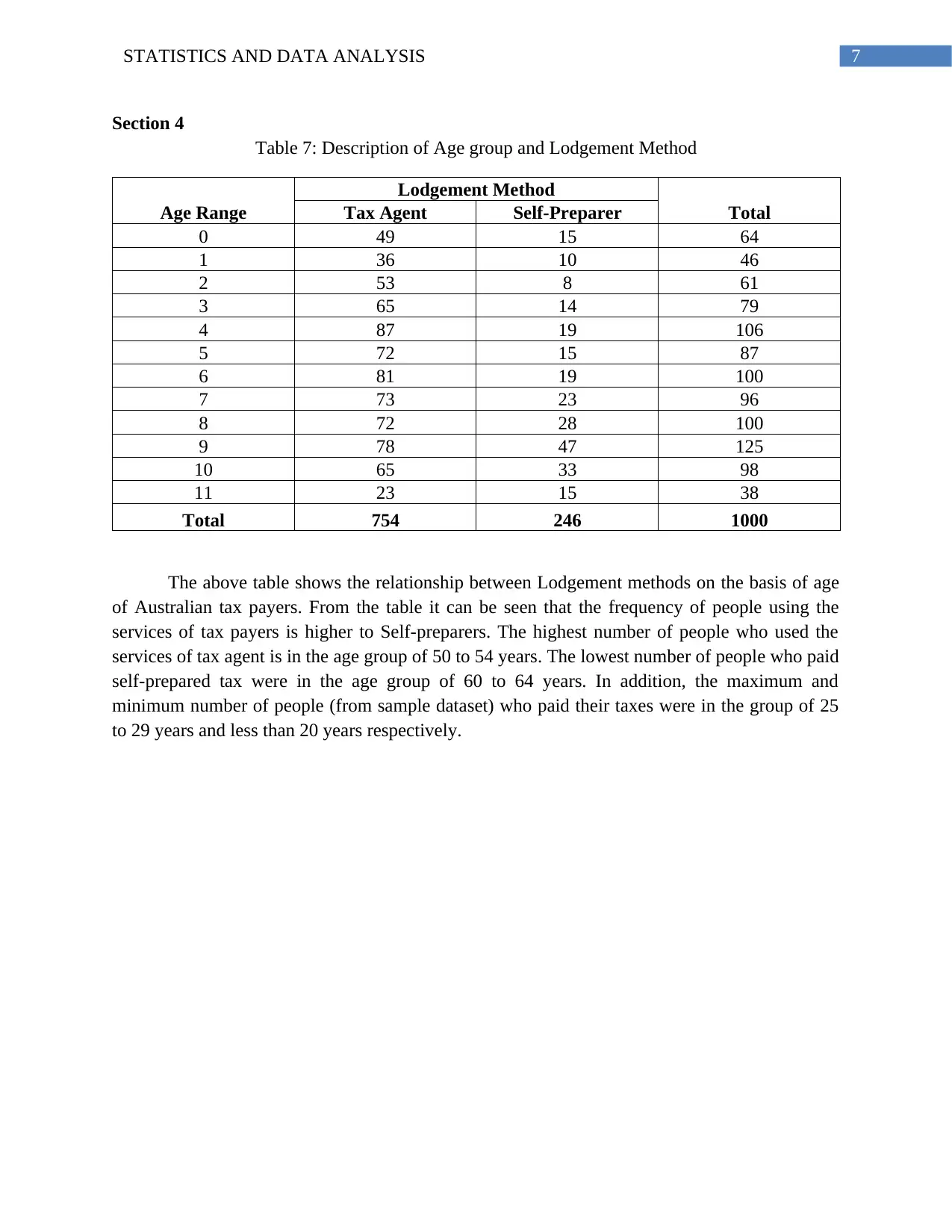

Section 4

Table 7: Description of Age group and Lodgement Method

Age Range

Lodgement Method

TotalTax Agent Self-Preparer

0 49 15 64

1 36 10 46

2 53 8 61

3 65 14 79

4 87 19 106

5 72 15 87

6 81 19 100

7 73 23 96

8 72 28 100

9 78 47 125

10 65 33 98

11 23 15 38

Total 754 246 1000

The above table shows the relationship between Lodgement methods on the basis of age

of Australian tax payers. From the table it can be seen that the frequency of people using the

services of tax payers is higher to Self-preparers. The highest number of people who used the

services of tax agent is in the age group of 50 to 54 years. The lowest number of people who paid

self-prepared tax were in the age group of 60 to 64 years. In addition, the maximum and

minimum number of people (from sample dataset) who paid their taxes were in the group of 25

to 29 years and less than 20 years respectively.

Section 4

Table 7: Description of Age group and Lodgement Method

Age Range

Lodgement Method

TotalTax Agent Self-Preparer

0 49 15 64

1 36 10 46

2 53 8 61

3 65 14 79

4 87 19 106

5 72 15 87

6 81 19 100

7 73 23 96

8 72 28 100

9 78 47 125

10 65 33 98

11 23 15 38

Total 754 246 1000

The above table shows the relationship between Lodgement methods on the basis of age

of Australian tax payers. From the table it can be seen that the frequency of people using the

services of tax payers is higher to Self-preparers. The highest number of people who used the

services of tax agent is in the age group of 50 to 54 years. The lowest number of people who paid

self-prepared tax were in the age group of 60 to 64 years. In addition, the maximum and

minimum number of people (from sample dataset) who paid their taxes were in the group of 25

to 29 years and less than 20 years respectively.

8STATISTICS AND DATA ANALYSIS

0 1 2 3 4 5 6 7 8 9 10 11

0

10

20

30

40

50

60

70

80

90

100

Comparing Lodgement Methods across Age

Groups

Tax Agent Self Preparer

Age Groups

Frequency

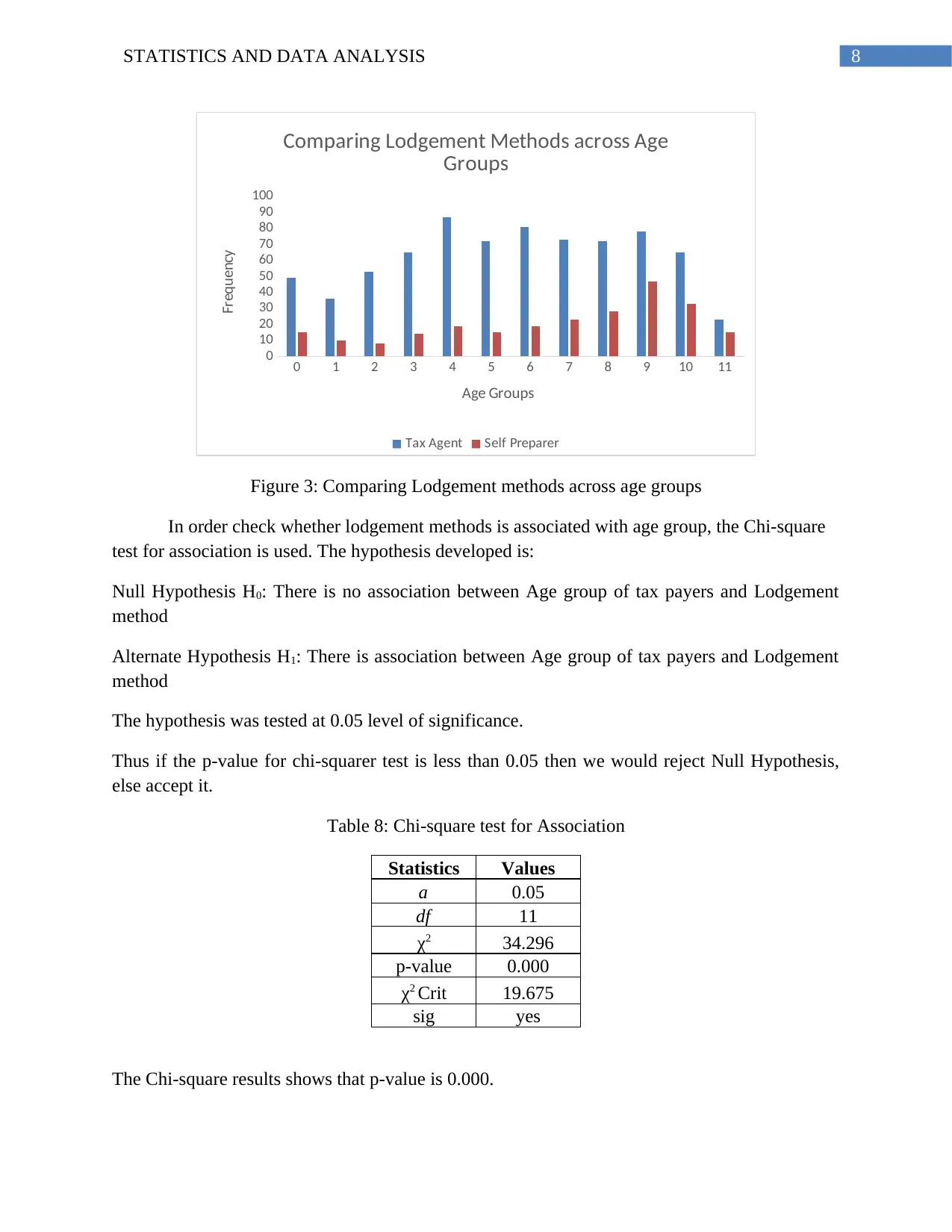

Figure 3: Comparing Lodgement methods across age groups

In order check whether lodgement methods is associated with age group, the Chi-square

test for association is used. The hypothesis developed is:

Null Hypothesis H0: There is no association between Age group of tax payers and Lodgement

method

Alternate Hypothesis H1: There is association between Age group of tax payers and Lodgement

method

The hypothesis was tested at 0.05 level of significance.

Thus if the p-value for chi-squarer test is less than 0.05 then we would reject Null Hypothesis,

else accept it.

Table 8: Chi-square test for Association

Statistics Values

a 0.05

df 11

χ2 34.296

p-value 0.000

χ2 Crit 19.675

sig yes

The Chi-square results shows that p-value is 0.000.

0 1 2 3 4 5 6 7 8 9 10 11

0

10

20

30

40

50

60

70

80

90

100

Comparing Lodgement Methods across Age

Groups

Tax Agent Self Preparer

Age Groups

Frequency

Figure 3: Comparing Lodgement methods across age groups

In order check whether lodgement methods is associated with age group, the Chi-square

test for association is used. The hypothesis developed is:

Null Hypothesis H0: There is no association between Age group of tax payers and Lodgement

method

Alternate Hypothesis H1: There is association between Age group of tax payers and Lodgement

method

The hypothesis was tested at 0.05 level of significance.

Thus if the p-value for chi-squarer test is less than 0.05 then we would reject Null Hypothesis,

else accept it.

Table 8: Chi-square test for Association

Statistics Values

a 0.05

df 11

χ2 34.296

p-value 0.000

χ2 Crit 19.675

sig yes

The Chi-square results shows that p-value is 0.000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9STATISTICS AND DATA ANALYSIS

Since p-value <

-value, hence we reject Null Hypothesis.

Thus, there is an association between Age group of tax payers and Lodgement method.

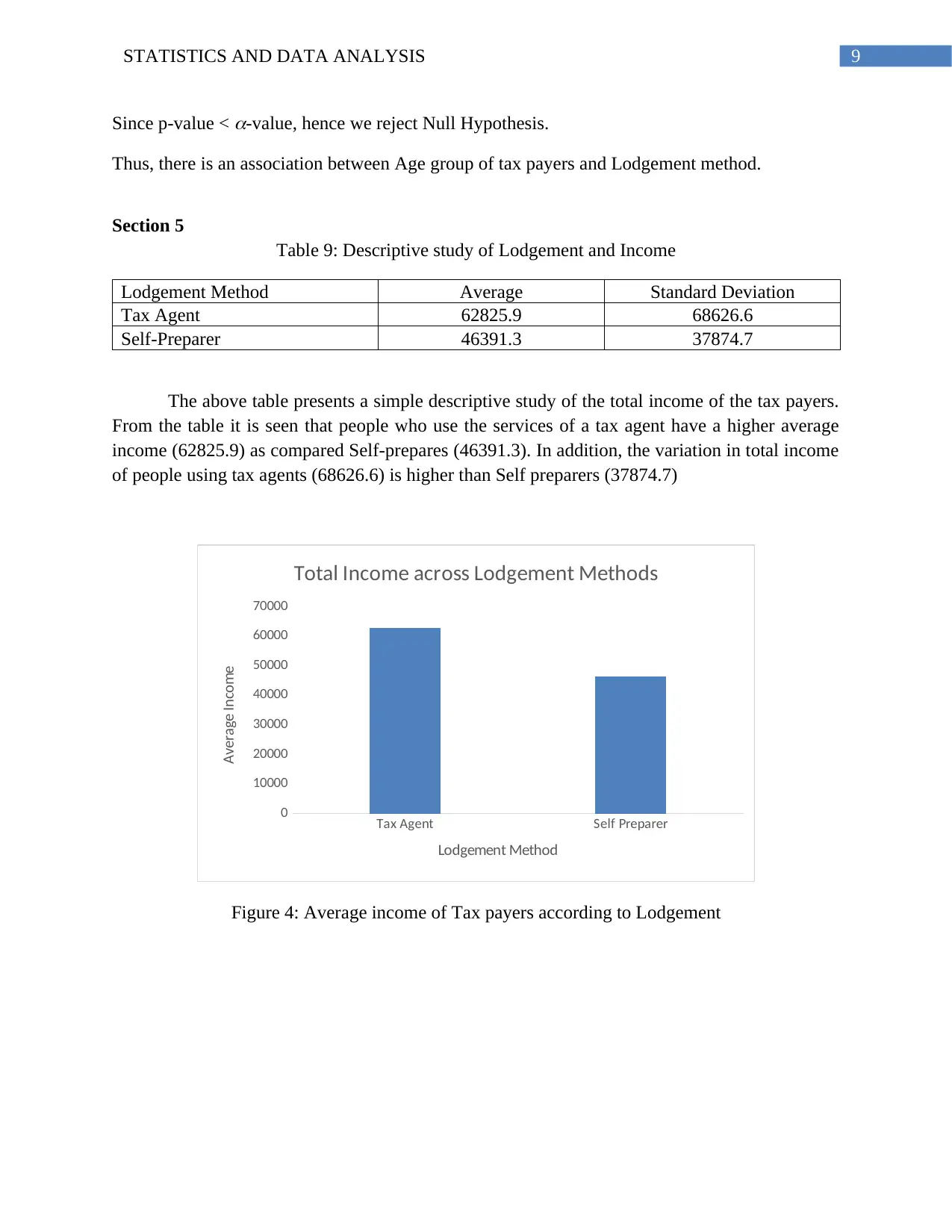

Section 5

Table 9: Descriptive study of Lodgement and Income

Lodgement Method Average Standard Deviation

Tax Agent 62825.9 68626.6

Self-Preparer 46391.3 37874.7

The above table presents a simple descriptive study of the total income of the tax payers.

From the table it is seen that people who use the services of a tax agent have a higher average

income (62825.9) as compared Self-prepares (46391.3). In addition, the variation in total income

of people using tax agents (68626.6) is higher than Self preparers (37874.7)

Tax Agent Self Preparer

0

10000

20000

30000

40000

50000

60000

70000

Total Income across Lodgement Methods

Lodgement Method

Average Income

Figure 4: Average income of Tax payers according to Lodgement

Since p-value <

-value, hence we reject Null Hypothesis.

Thus, there is an association between Age group of tax payers and Lodgement method.

Section 5

Table 9: Descriptive study of Lodgement and Income

Lodgement Method Average Standard Deviation

Tax Agent 62825.9 68626.6

Self-Preparer 46391.3 37874.7

The above table presents a simple descriptive study of the total income of the tax payers.

From the table it is seen that people who use the services of a tax agent have a higher average

income (62825.9) as compared Self-prepares (46391.3). In addition, the variation in total income

of people using tax agents (68626.6) is higher than Self preparers (37874.7)

Tax Agent Self Preparer

0

10000

20000

30000

40000

50000

60000

70000

Total Income across Lodgement Methods

Lodgement Method

Average Income

Figure 4: Average income of Tax payers according to Lodgement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10STATISTICS AND DATA ANALYSIS

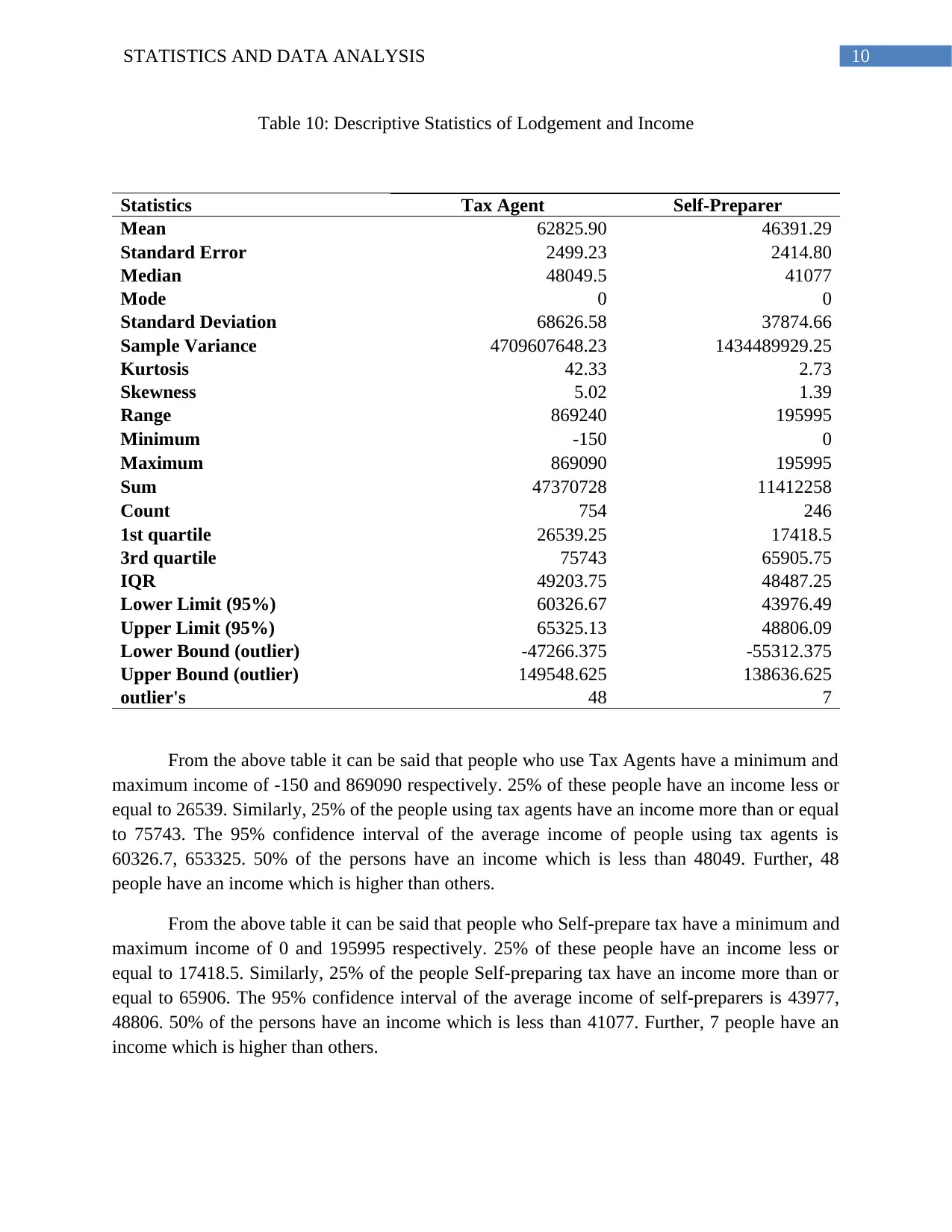

Table 10: Descriptive Statistics of Lodgement and Income

Statistics Tax Agent Self-Preparer

Mean 62825.90 46391.29

Standard Error 2499.23 2414.80

Median 48049.5 41077

Mode 0 0

Standard Deviation 68626.58 37874.66

Sample Variance 4709607648.23 1434489929.25

Kurtosis 42.33 2.73

Skewness 5.02 1.39

Range 869240 195995

Minimum -150 0

Maximum 869090 195995

Sum 47370728 11412258

Count 754 246

1st quartile 26539.25 17418.5

3rd quartile 75743 65905.75

IQR 49203.75 48487.25

Lower Limit (95%) 60326.67 43976.49

Upper Limit (95%) 65325.13 48806.09

Lower Bound (outlier) -47266.375 -55312.375

Upper Bound (outlier) 149548.625 138636.625

outlier's 48 7

From the above table it can be said that people who use Tax Agents have a minimum and

maximum income of -150 and 869090 respectively. 25% of these people have an income less or

equal to 26539. Similarly, 25% of the people using tax agents have an income more than or equal

to 75743. The 95% confidence interval of the average income of people using tax agents is

60326.7, 653325. 50% of the persons have an income which is less than 48049. Further, 48

people have an income which is higher than others.

From the above table it can be said that people who Self-prepare tax have a minimum and

maximum income of 0 and 195995 respectively. 25% of these people have an income less or

equal to 17418.5. Similarly, 25% of the people Self-preparing tax have an income more than or

equal to 65906. The 95% confidence interval of the average income of self-preparers is 43977,

48806. 50% of the persons have an income which is less than 41077. Further, 7 people have an

income which is higher than others.

Table 10: Descriptive Statistics of Lodgement and Income

Statistics Tax Agent Self-Preparer

Mean 62825.90 46391.29

Standard Error 2499.23 2414.80

Median 48049.5 41077

Mode 0 0

Standard Deviation 68626.58 37874.66

Sample Variance 4709607648.23 1434489929.25

Kurtosis 42.33 2.73

Skewness 5.02 1.39

Range 869240 195995

Minimum -150 0

Maximum 869090 195995

Sum 47370728 11412258

Count 754 246

1st quartile 26539.25 17418.5

3rd quartile 75743 65905.75

IQR 49203.75 48487.25

Lower Limit (95%) 60326.67 43976.49

Upper Limit (95%) 65325.13 48806.09

Lower Bound (outlier) -47266.375 -55312.375

Upper Bound (outlier) 149548.625 138636.625

outlier's 48 7

From the above table it can be said that people who use Tax Agents have a minimum and

maximum income of -150 and 869090 respectively. 25% of these people have an income less or

equal to 26539. Similarly, 25% of the people using tax agents have an income more than or equal

to 75743. The 95% confidence interval of the average income of people using tax agents is

60326.7, 653325. 50% of the persons have an income which is less than 48049. Further, 48

people have an income which is higher than others.

From the above table it can be said that people who Self-prepare tax have a minimum and

maximum income of 0 and 195995 respectively. 25% of these people have an income less or

equal to 17418.5. Similarly, 25% of the people Self-preparing tax have an income more than or

equal to 65906. The 95% confidence interval of the average income of self-preparers is 43977,

48806. 50% of the persons have an income which is less than 41077. Further, 7 people have an

income which is higher than others.

11STATISTICS AND DATA ANALYSIS

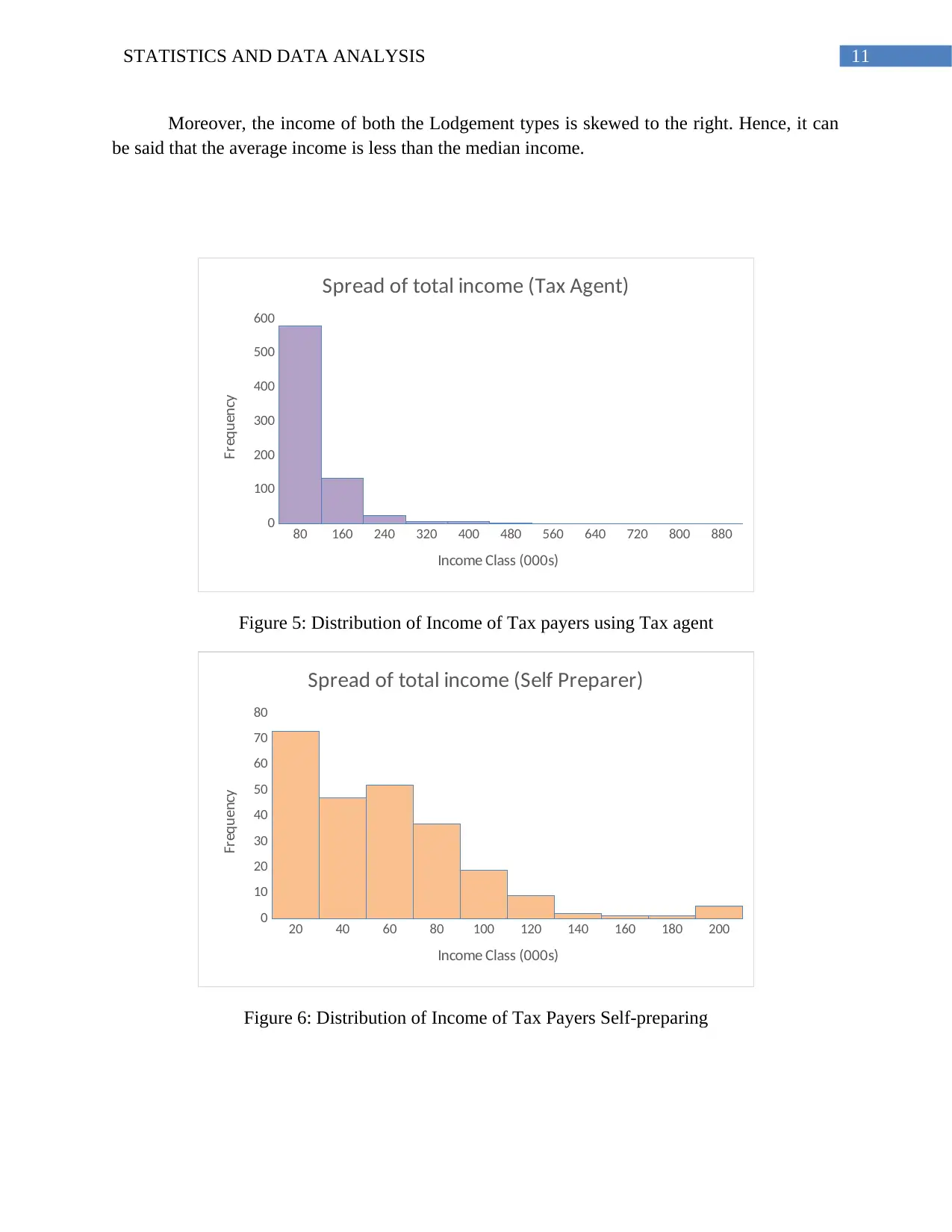

Moreover, the income of both the Lodgement types is skewed to the right. Hence, it can

be said that the average income is less than the median income.

80 160 240 320 400 480 560 640 720 800 880

0

100

200

300

400

500

600

Spread of total income (Tax Agent)

Income Class (000s)

Frequency

Figure 5: Distribution of Income of Tax payers using Tax agent

20 40 60 80 100 120 140 160 180 200

0

10

20

30

40

50

60

70

80

Spread of total income (Self Preparer)

Income Class (000s)

Frequency

Figure 6: Distribution of Income of Tax Payers Self-preparing

Moreover, the income of both the Lodgement types is skewed to the right. Hence, it can

be said that the average income is less than the median income.

80 160 240 320 400 480 560 640 720 800 880

0

100

200

300

400

500

600

Spread of total income (Tax Agent)

Income Class (000s)

Frequency

Figure 5: Distribution of Income of Tax payers using Tax agent

20 40 60 80 100 120 140 160 180 200

0

10

20

30

40

50

60

70

80

Spread of total income (Self Preparer)

Income Class (000s)

Frequency

Figure 6: Distribution of Income of Tax Payers Self-preparing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.