Assessment of GST and Capital Gains Tax in Australian Taxation Law

VerifiedAdded on 2022/10/31

|10

|3040

|237

Homework Assignment

AI Summary

This assignment provides a detailed analysis of Australian taxation law, specifically focusing on Goods and Services Tax (GST) and Capital Gains Tax (CGT). The assignment is divided into two parts. The first part examines GST, including the threshold for mandatory registration, eligibility for input tax credits, and the taxability of supplies. The second part delves into capital gains tax, covering the tax treatment of shares, land, collectibles, and personal consumption. The assignment applies relevant sections of the Australian Income Tax Assessment Act, taxation rulings, and Australian Taxation Office (ATO) law to a case study involving a construction company and its legal expenses. It also explores the CGT discount and indexation methods for calculating capital gains. The report provides a clear understanding of GST credits and capital gains calculations, offering valuable insights into Australian tax regulations.

Executive Summary

The whole of the topic has been analyzed in accordance with the Australian income tax

assessment act, taxation ruling and Australian taxation office law. The court decision is

also considered in this report. This assignment includes the brief introduction of goods

and service tax and capital gain and fringe benefit taxation. The question contains two

parts. The first part requires the knowledge of goods and service tax and the second

part requires knowledge of capital gain tax. The task in this assignment has been solved

by applying law, rules, and regulation of the Australian income tax assessment act.

While describing GST, it also discussed the following points:

(a) Thresh hold limit of entity’s business for mandatory registration of goods and

service tax.

(b) Eligibility to claim Input tax credit of goods and service tax paid

(c) Taxability of capital gains taxes in relation to shares, land, collectible and

personal consumption.

The learning outcome of the report helps to determine the correct calculation of capital

gain taxes and claims of credit in respect of payment of goods and service tax in

relation to purchasing of goods and service tax.

Page 1 of 10

The whole of the topic has been analyzed in accordance with the Australian income tax

assessment act, taxation ruling and Australian taxation office law. The court decision is

also considered in this report. This assignment includes the brief introduction of goods

and service tax and capital gain and fringe benefit taxation. The question contains two

parts. The first part requires the knowledge of goods and service tax and the second

part requires knowledge of capital gain tax. The task in this assignment has been solved

by applying law, rules, and regulation of the Australian income tax assessment act.

While describing GST, it also discussed the following points:

(a) Thresh hold limit of entity’s business for mandatory registration of goods and

service tax.

(b) Eligibility to claim Input tax credit of goods and service tax paid

(c) Taxability of capital gains taxes in relation to shares, land, collectible and

personal consumption.

The learning outcome of the report helps to determine the correct calculation of capital

gain taxes and claims of credit in respect of payment of goods and service tax in

relation to purchasing of goods and service tax.

Page 1 of 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction 3

Discussion 3

Solution – 1 3

GST Provision applied on respective case and conclusion: 5

Solution – 2: 6

Tax treatment of capital gain income and also various techniques for calculation of capital

gains: 8

Application of law to the case: 12

Conclusion 14

References 14

Page 2 of 10

Introduction 3

Discussion 3

Solution – 1 3

GST Provision applied on respective case and conclusion: 5

Solution – 2: 6

Tax treatment of capital gain income and also various techniques for calculation of capital

gains: 8

Application of law to the case: 12

Conclusion 14

References 14

Page 2 of 10

Introduction

The report discusses in detail the calculation of capital gain tax. It also describes the

exemption which can be claimed in respect of the sale of a capital asset. It also

discussed that the entity which has gross receipts of more than $75000 during the

financial year.

Eligibility of input tax credit is also discussed. The credit in respect of payment of goods

and services can be claimed only where there is a transaction between two registered

persons. The person making payment of GST can claim credit as input. The input of

GST can be utilized to set off liability or claim as a refund.

It requires the calculation of capital gain in respect of following capital assets such as

land, shares, and collectibles as well as personal assets.

Discussion

Solution – 1

The task discussed organization which is namely the City Sky Co. The given company

is currently involved in the business of making an investment for construction of the

building and also developing several residential properties for sale. The company is

engaged in selling such apartments for the purpose of residential houses. Being a

corporation, City Sky co. is required to take various legal and advisory services. The

City Sky Co. had also taken such service from one of the lawyers whose name is

Maurice Blackburn. It is also given in the question that gross receipts of such lawyer are

$300,000. As already discussed, the mandatory registration of entity, the entity having

more than $75,000 is required to take registration under GST. Accordingly, it is

assumed that Maurice Blackburn is registered under GST provision.

The Issue of this Case:

Whether credit can be claimed by City Sky Co. in respect of GST paid to lawyer Maurice

Blackburn?

In this task, the discussion is based on new legislation of GST Act 1999:

Every person who has gained more than $75000 turnover during the current year is

required to take registration under GST. Further provided in law that cancellation of

such registered will not be done within 12 months from the date on which registration

has been obtained (ATO, QC 22412).

In accordance with ATO Law and Section 11-5 of the Australian income tax assessment

act 1999, where a person provides goods or services in exchange for cash or kind for

providing such services in relation to business then such supplies are called taxable

supplies.

Page 3 of 10

The report discusses in detail the calculation of capital gain tax. It also describes the

exemption which can be claimed in respect of the sale of a capital asset. It also

discussed that the entity which has gross receipts of more than $75000 during the

financial year.

Eligibility of input tax credit is also discussed. The credit in respect of payment of goods

and services can be claimed only where there is a transaction between two registered

persons. The person making payment of GST can claim credit as input. The input of

GST can be utilized to set off liability or claim as a refund.

It requires the calculation of capital gain in respect of following capital assets such as

land, shares, and collectibles as well as personal assets.

Discussion

Solution – 1

The task discussed organization which is namely the City Sky Co. The given company

is currently involved in the business of making an investment for construction of the

building and also developing several residential properties for sale. The company is

engaged in selling such apartments for the purpose of residential houses. Being a

corporation, City Sky co. is required to take various legal and advisory services. The

City Sky Co. had also taken such service from one of the lawyers whose name is

Maurice Blackburn. It is also given in the question that gross receipts of such lawyer are

$300,000. As already discussed, the mandatory registration of entity, the entity having

more than $75,000 is required to take registration under GST. Accordingly, it is

assumed that Maurice Blackburn is registered under GST provision.

The Issue of this Case:

Whether credit can be claimed by City Sky Co. in respect of GST paid to lawyer Maurice

Blackburn?

In this task, the discussion is based on new legislation of GST Act 1999:

Every person who has gained more than $75000 turnover during the current year is

required to take registration under GST. Further provided in law that cancellation of

such registered will not be done within 12 months from the date on which registration

has been obtained (ATO, QC 22412).

In accordance with ATO Law and Section 11-5 of the Australian income tax assessment

act 1999, where a person provides goods or services in exchange for cash or kind for

providing such services in relation to business then such supplies are called taxable

supplies.

Page 3 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxable supplies are such in respect of which tax under GST is required to be paid.

Accordingly, GST would be leviable on taxable supplies only. No GST will be charged

on exempt supplies. Exempt supplies include the export of goods or services or some

type of agricultural and others.

Further stated in section 11-10(2) of the GST act that consultancy services and any

other types of service can be included in supplies.

Section 9-70 of the GST Act (1997) stated that GST will be levied on supplies of taxable

goods and services at a rate of 10%. In accordance with s9-75(1), the GST will be

calculated on the taxable value of supply at a rate of 10% as divided by 110 basis points

in case of inclusive of GST. GST in case of invoice value inclusive of the taxable value

of supply is calculated as follows:

GST = Taxable Value of Supply including GST*10/110.

In accordance with section 7-12 of GST act 1999, the transaction between two

registered parties allows credit of GST paid in respect of goods and service tax. The

GST credit can be utilized to set off the liability or can be claimed as a refund by a

person who had paid. GST act mandates the issue of tax invoice where the amount of

taxable value of service exceeds $75. Input tax credit can be taken in respect of

creditable acquisition only. No credit can be claimed where such acquisition does not

fall under creditable acquisition. (ATO, QC 22430).

GST Provision applied on respective case and conclusion:

Every company which is registered under GST can claim GST paid on any expenses

incurred by them. The person claiming GST credit must fulfill other conditions specified

in the law. The input credit is one of the most advantages for a company that reduces

the cost of products or services.

As stated above, Credit can be claimed only there is a creditable acquisition. It is also

mentioned in the law that selling of land does not fall under GST law and so there is no

requirement to make payment of GST as well as input cannot be claimed in respect of

purchase of GST law.

In this case, The City Sky Co. is involved in the business of construction and

development of residential flats and thereafter selling of such flats. In accordance with

section S 40-65(1) of the GST act, 1999, the residential flat is exempt from payment of

residential flat as such sale is termed as input tax payment of GST.

The creditable acquisition includes the legal service. Accordingly, GST can be claimed

as input in respect of expenses incurred for legal service to Maurice Blackburn.

Hence, input tax credit can be claimed by the City Sky Co. of $ 3000. The calculation of

input tax credit is given below:

= ($33,000*1/11) = $3,000.

Page 4 of 10

Accordingly, GST would be leviable on taxable supplies only. No GST will be charged

on exempt supplies. Exempt supplies include the export of goods or services or some

type of agricultural and others.

Further stated in section 11-10(2) of the GST act that consultancy services and any

other types of service can be included in supplies.

Section 9-70 of the GST Act (1997) stated that GST will be levied on supplies of taxable

goods and services at a rate of 10%. In accordance with s9-75(1), the GST will be

calculated on the taxable value of supply at a rate of 10% as divided by 110 basis points

in case of inclusive of GST. GST in case of invoice value inclusive of the taxable value

of supply is calculated as follows:

GST = Taxable Value of Supply including GST*10/110.

In accordance with section 7-12 of GST act 1999, the transaction between two

registered parties allows credit of GST paid in respect of goods and service tax. The

GST credit can be utilized to set off the liability or can be claimed as a refund by a

person who had paid. GST act mandates the issue of tax invoice where the amount of

taxable value of service exceeds $75. Input tax credit can be taken in respect of

creditable acquisition only. No credit can be claimed where such acquisition does not

fall under creditable acquisition. (ATO, QC 22430).

GST Provision applied on respective case and conclusion:

Every company which is registered under GST can claim GST paid on any expenses

incurred by them. The person claiming GST credit must fulfill other conditions specified

in the law. The input credit is one of the most advantages for a company that reduces

the cost of products or services.

As stated above, Credit can be claimed only there is a creditable acquisition. It is also

mentioned in the law that selling of land does not fall under GST law and so there is no

requirement to make payment of GST as well as input cannot be claimed in respect of

purchase of GST law.

In this case, The City Sky Co. is involved in the business of construction and

development of residential flats and thereafter selling of such flats. In accordance with

section S 40-65(1) of the GST act, 1999, the residential flat is exempt from payment of

residential flat as such sale is termed as input tax payment of GST.

The creditable acquisition includes the legal service. Accordingly, GST can be claimed

as input in respect of expenses incurred for legal service to Maurice Blackburn.

Hence, input tax credit can be claimed by the City Sky Co. of $ 3000. The calculation of

input tax credit is given below:

= ($33,000*1/11) = $3,000.

Page 4 of 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution – 2:

Shareholders are that person who purchases shares or any other securities to earn

income in the form of interest or dividend or capital gains. Generally, there are two types

of investors who held a share for a short period and sold such securities. In case of the

sale of securities, shareholders will earn income in form capital gain. Securities can be

purchased from various modes such as online through stock exchange or through

private equity. While purchasing shares from the public, they had to bid on such an

offer. Any expenditure which will be incurred for the purchase as brokerage shall form

part of the cost of shares and any expenses as brokerage on sale of such shares is

required to reduce from the cost of such shares.

It is worthwhile to consider the following points for the purpose of tax calculation in

respect of shareholders:

● The cost of shares purchase is in the nature of the capital asset and it cannot be

deducted from the current income or deferred income for the purpose of

calculation of assessable income.

● In a case where any income arises on a later period on or after the purchase of

shares. The income may in the form of dividend or interest income. Such income

shall be included in return for the purpose of calculation of taxable income. It is

further provided that any gain that arose on the sale of such shares can be

categories as capital gain. The capital gain tax will attract in respect of such gain.

The capital gain is equal to the sale value of capital assets as reduced by capital

cost base.

● It is also stated that no loss can be set off against income other than capital gain.

Hence, any loss in the nature of capital loss can be set off only against capital

gain. Capital loss can be set off and carry forward for setoff through next year's

capital gain.

● The cost incurred in relation to purchasing of shares includes the brokerage

charges and cost of shares. Hence, such amount is required to be deducted for

the purpose of calculation of capital gain from the full value of consideration of

capital assets.

● No capital gain will be charged on income which is in the nature of dividend

income and interest income from the capital gain. Hence, no capital gain tax will

be levied on such income.

Tax treatment of capital gain income and also various techniques for calculation of

capital gains:

The shareholder’s intention to earn income for a short period on the sale of such share

shall befall in the nature of capital gain and capital gain tax will be levied on such

income. However, where the income is in the nature of dividends, no capital gain tax is

required to pay on such income. Division 100 -104, Part 3-1 prescribes the tax

Page 5 of 10

Shareholders are that person who purchases shares or any other securities to earn

income in the form of interest or dividend or capital gains. Generally, there are two types

of investors who held a share for a short period and sold such securities. In case of the

sale of securities, shareholders will earn income in form capital gain. Securities can be

purchased from various modes such as online through stock exchange or through

private equity. While purchasing shares from the public, they had to bid on such an

offer. Any expenditure which will be incurred for the purchase as brokerage shall form

part of the cost of shares and any expenses as brokerage on sale of such shares is

required to reduce from the cost of such shares.

It is worthwhile to consider the following points for the purpose of tax calculation in

respect of shareholders:

● The cost of shares purchase is in the nature of the capital asset and it cannot be

deducted from the current income or deferred income for the purpose of

calculation of assessable income.

● In a case where any income arises on a later period on or after the purchase of

shares. The income may in the form of dividend or interest income. Such income

shall be included in return for the purpose of calculation of taxable income. It is

further provided that any gain that arose on the sale of such shares can be

categories as capital gain. The capital gain tax will attract in respect of such gain.

The capital gain is equal to the sale value of capital assets as reduced by capital

cost base.

● It is also stated that no loss can be set off against income other than capital gain.

Hence, any loss in the nature of capital loss can be set off only against capital

gain. Capital loss can be set off and carry forward for setoff through next year's

capital gain.

● The cost incurred in relation to purchasing of shares includes the brokerage

charges and cost of shares. Hence, such amount is required to be deducted for

the purpose of calculation of capital gain from the full value of consideration of

capital assets.

● No capital gain will be charged on income which is in the nature of dividend

income and interest income from the capital gain. Hence, no capital gain tax will

be levied on such income.

Tax treatment of capital gain income and also various techniques for calculation of

capital gains:

The shareholder’s intention to earn income for a short period on the sale of such share

shall befall in the nature of capital gain and capital gain tax will be levied on such

income. However, where the income is in the nature of dividends, no capital gain tax is

required to pay on such income. Division 100 -104, Part 3-1 prescribes the tax

Page 5 of 10

treatment concerning the capital gain income. ITAA (1997) prescribes three methods to

determine the capital gain tax. These are as follows:

(a) CGT discount method

(b) Indexation method

(c) Other method:

1) CGT Discount Method: This method is not applicable to the company. Any person

who is not a company can apply the Capital gain discount method for calculation of

capital gain tax. The company applying capital gain tax must fulfill the given

conditions for the calculation of capital income under capital gain tax method:

Assesse should be any person and such a person must not be a

company.

● The event on which capital gain has been occurred on or after September

1999.

● Capital assets must be held for more than 12 months or exact 12 months.

● The person applying capital gain tax discount method must not apply the

indexation methods.

● However certain exception is provided for holding period. Under the following

circumstance, they can apply capital gain discount method eve they hold for a

period of less than 12 months:

○ In the case of divorce, if married persons are separated and they stay

separately due to the breaking of his/her relationship. It shall be treated as

they had fulfilled the condition and they can apply capital discount method

while calculating capital gain.

○ Where an asset has been purchased by the government under the

scheme of compulsory acquisition or case of dismantled, replacement of

loss of such asset. It is treated as a fulfilling condition and they can apply

capital discount methods while calculating the capital gain for both the

persons.

● Inheritance of estate is in the nature of the transfer of capital assets.

Where any asset has been transferred to legal heir or estated on death of

estated. Such asset has been acquired under inheritance due to death of

estate. It is treated as a fulfilling condition and they can apply capital

discount method while calculating capital gain for legal heir only if such

asset has been purchased on or after September 1995.

● There is separate of deduction of capital discount rate for individual trust

or super funds. There is a 50% and 33.33% discount for individuals, trusts

and super funds respectively. It is further stated that no discount can be

claimed in case of loss on sale of capital assets.

Page 6 of 10

determine the capital gain tax. These are as follows:

(a) CGT discount method

(b) Indexation method

(c) Other method:

1) CGT Discount Method: This method is not applicable to the company. Any person

who is not a company can apply the Capital gain discount method for calculation of

capital gain tax. The company applying capital gain tax must fulfill the given

conditions for the calculation of capital income under capital gain tax method:

Assesse should be any person and such a person must not be a

company.

● The event on which capital gain has been occurred on or after September

1999.

● Capital assets must be held for more than 12 months or exact 12 months.

● The person applying capital gain tax discount method must not apply the

indexation methods.

● However certain exception is provided for holding period. Under the following

circumstance, they can apply capital gain discount method eve they hold for a

period of less than 12 months:

○ In the case of divorce, if married persons are separated and they stay

separately due to the breaking of his/her relationship. It shall be treated as

they had fulfilled the condition and they can apply capital discount method

while calculating capital gain.

○ Where an asset has been purchased by the government under the

scheme of compulsory acquisition or case of dismantled, replacement of

loss of such asset. It is treated as a fulfilling condition and they can apply

capital discount methods while calculating the capital gain for both the

persons.

● Inheritance of estate is in the nature of the transfer of capital assets.

Where any asset has been transferred to legal heir or estated on death of

estated. Such asset has been acquired under inheritance due to death of

estate. It is treated as a fulfilling condition and they can apply capital

discount method while calculating capital gain for legal heir only if such

asset has been purchased on or after September 1995.

● There is separate of deduction of capital discount rate for individual trust

or super funds. There is a 50% and 33.33% discount for individuals, trusts

and super funds respectively. It is further stated that no discount can be

claimed in case of loss on sale of capital assets.

Page 6 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2) Indexation Method: the Second method is the indexation method. The company

applying capital gain tax must fulfill the given conditions for the calculation of capital

income under indexation method:

The event on which capital gain has been occurred on or after September

1999.

A capital asset must be held for more than 12 months or exact 12 months.

● It is mandatory for every company to apply a method of indexation for the

purpose of computation of capital gain. The provision excludes the

investment companies listed on the stock exchange. Hence, it should be

kept in mind that the company's other investment company must apply the

indexation method.

● However, a certain exception is provided for the holding period. Under the

following circumstance, they can apply capital gain discount method eve they

hold for a period of less than 12 months:

○ In the case of divorce, if marriage people are separated and they stay

separately due to the breaking of his/her relationship. It shall be treated as

they had fulfilled the condition and they can apply capital discount method

while calculating capital gain.

● Inheritance of estate is in the nature of the transfer of capital assets.

Where any asset has been transferred to legal heir or estated on death of

estated. Such asset has been acquired under inheritance due to death of

estate. It is treated as fulfilling condition and they can apply capital

discount method while calculating capital gain for legal heir only if such

asset has been purchased on or after September 1995.

.

The cost of the index (CPI) can be used to increase the cost base by

multiplication.

3. Other Method: one of the last methods is “Other method”.

● The asset must not be for a period of one or more than one year.

● The capital gain is to be calculated by applying such a convenient method.

The case law prescribes that in the instant question:

There are four types of assets held by Emma which include shares, collection, grand

piano, land, and stamp.

Application of law to the case:

Computation of capital gain is given below:

Calculation of capital gain on the sale of Land

Full value of consideration on sale of land $1,000,000 minus $25,000

which is equal to $975,000

Page 7 of 10

applying capital gain tax must fulfill the given conditions for the calculation of capital

income under indexation method:

The event on which capital gain has been occurred on or after September

1999.

A capital asset must be held for more than 12 months or exact 12 months.

● It is mandatory for every company to apply a method of indexation for the

purpose of computation of capital gain. The provision excludes the

investment companies listed on the stock exchange. Hence, it should be

kept in mind that the company's other investment company must apply the

indexation method.

● However, a certain exception is provided for the holding period. Under the

following circumstance, they can apply capital gain discount method eve they

hold for a period of less than 12 months:

○ In the case of divorce, if marriage people are separated and they stay

separately due to the breaking of his/her relationship. It shall be treated as

they had fulfilled the condition and they can apply capital discount method

while calculating capital gain.

● Inheritance of estate is in the nature of the transfer of capital assets.

Where any asset has been transferred to legal heir or estated on death of

estated. Such asset has been acquired under inheritance due to death of

estate. It is treated as fulfilling condition and they can apply capital

discount method while calculating capital gain for legal heir only if such

asset has been purchased on or after September 1995.

.

The cost of the index (CPI) can be used to increase the cost base by

multiplication.

3. Other Method: one of the last methods is “Other method”.

● The asset must not be for a period of one or more than one year.

● The capital gain is to be calculated by applying such a convenient method.

The case law prescribes that in the instant question:

There are four types of assets held by Emma which include shares, collection, grand

piano, land, and stamp.

Application of law to the case:

Computation of capital gain is given below:

Calculation of capital gain on the sale of Land

Full value of consideration on sale of land $1,000,000 minus $25,000

which is equal to $975,000

Page 7 of 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

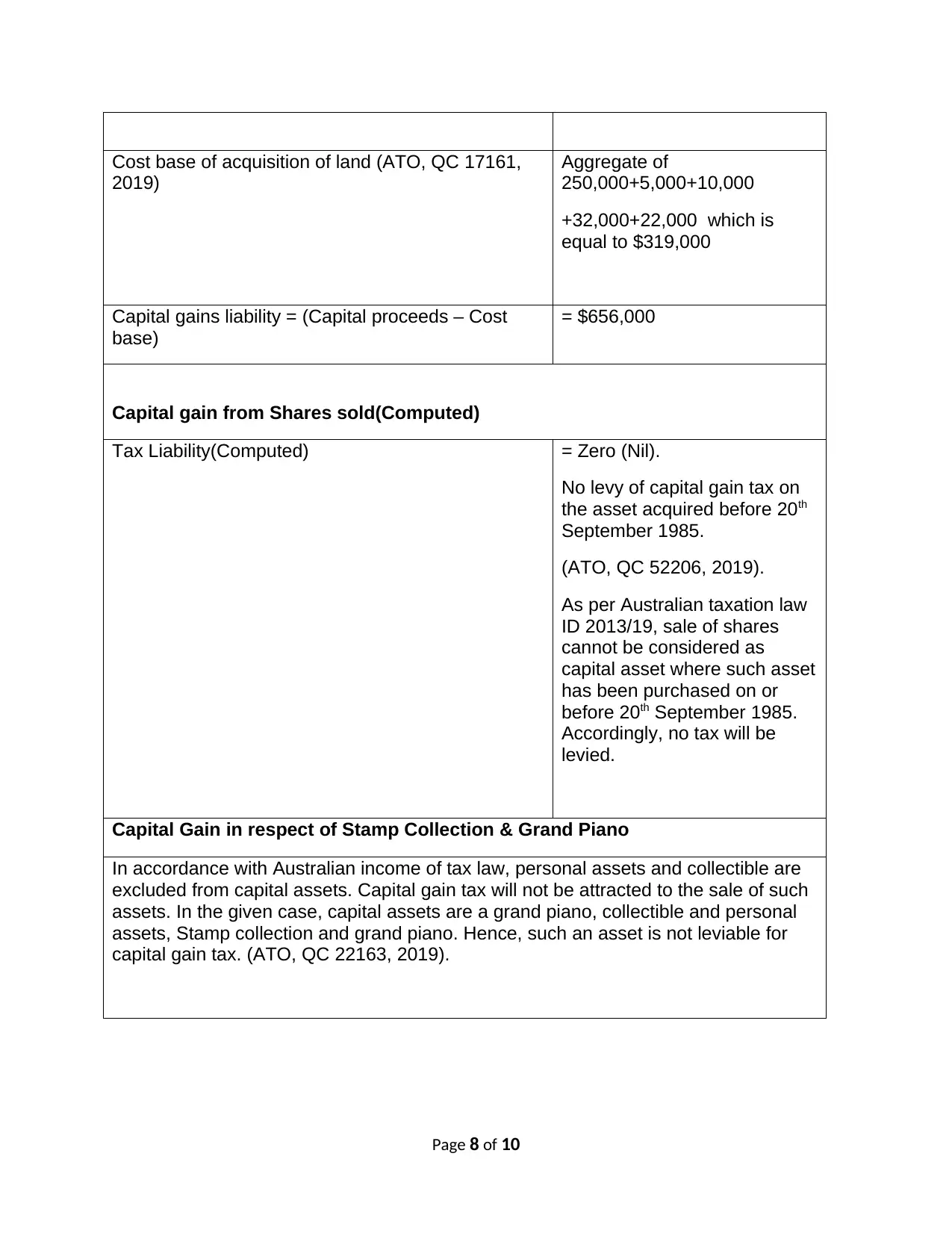

Cost base of acquisition of land (ATO, QC 17161,

2019)

Aggregate of

250,000+5,000+10,000

+32,000+22,000 which is

equal to $319,000

Capital gains liability = (Capital proceeds – Cost

base)

= $656,000

Capital gain from Shares sold(Computed)

Tax Liability(Computed) = Zero (Nil).

No levy of capital gain tax on

the asset acquired before 20th

September 1985.

(ATO, QC 52206, 2019).

As per Australian taxation law

ID 2013/19, sale of shares

cannot be considered as

capital asset where such asset

has been purchased on or

before 20th September 1985.

Accordingly, no tax will be

levied.

Capital Gain in respect of Stamp Collection & Grand Piano

In accordance with Australian income of tax law, personal assets and collectible are

excluded from capital assets. Capital gain tax will not be attracted to the sale of such

assets. In the given case, capital assets are a grand piano, collectible and personal

assets, Stamp collection and grand piano. Hence, such an asset is not leviable for

capital gain tax. (ATO, QC 22163, 2019).

Page 8 of 10

2019)

Aggregate of

250,000+5,000+10,000

+32,000+22,000 which is

equal to $319,000

Capital gains liability = (Capital proceeds – Cost

base)

= $656,000

Capital gain from Shares sold(Computed)

Tax Liability(Computed) = Zero (Nil).

No levy of capital gain tax on

the asset acquired before 20th

September 1985.

(ATO, QC 52206, 2019).

As per Australian taxation law

ID 2013/19, sale of shares

cannot be considered as

capital asset where such asset

has been purchased on or

before 20th September 1985.

Accordingly, no tax will be

levied.

Capital Gain in respect of Stamp Collection & Grand Piano

In accordance with Australian income of tax law, personal assets and collectible are

excluded from capital assets. Capital gain tax will not be attracted to the sale of such

assets. In the given case, capital assets are a grand piano, collectible and personal

assets, Stamp collection and grand piano. Hence, such an asset is not leviable for

capital gain tax. (ATO, QC 22163, 2019).

Page 8 of 10

Conclusion

Accordingly, the calculated capital gain in the given task is $ 65,000. It is also

mentioned in the given question that the asset has been held for a period of more than

12 months accordingly, as mention above we can apply capital gain tax discount

method for calculation of net capital gain.

Calculated, Net capital Gain = $656,000- $656,000*33.33% = $218,667.

Page 9 of 10

Accordingly, the calculated capital gain in the given task is $ 65,000. It is also

mentioned in the given question that the asset has been held for a period of more than

12 months accordingly, as mention above we can apply capital gain tax discount

method for calculation of net capital gain.

Calculated, Net capital Gain = $656,000- $656,000*33.33% = $218,667.

Page 9 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Legislation.gov.au. (2019). A New Tax System (Goods and Services Tax) Act 1999.

[online] Available at: https://www.legislation.gov.au/Details/C2017C00218/Controls/

[Accessed 20 Sep. 2019].

Ato.gov.au. (2019). Choosing the indexation or discount methods. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-

loss/Working-out-your-capital-gain/Choosing-the-indexation-or-discount-methods/

[Accessed 20 Sep. 2019].

Ato.gov.au. (2019). Shares, units and similar investments. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Shares,-units-and-similar-

investments/ [Accessed 20 Sep. 2019].

Ato.gov.au. (2019). Sale of property and other CGT events. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/

Sale-of-property-and-other-CGT-events/ [Accessed 20 Sep. 2019].

Ato.gov.au. (2019). CGT assets and exemptions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/ [Accessed

20 Sep. 2019].

Classic.austlii.edu.au. (2019). INCOME TAX ASSESSMENT ACT 1997. [online]

Available at: http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/ [Accessed

20 Sep. 2019].

Page 10 of 10

Legislation.gov.au. (2019). A New Tax System (Goods and Services Tax) Act 1999.

[online] Available at: https://www.legislation.gov.au/Details/C2017C00218/Controls/

[Accessed 20 Sep. 2019].

Ato.gov.au. (2019). Choosing the indexation or discount methods. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-

loss/Working-out-your-capital-gain/Choosing-the-indexation-or-discount-methods/

[Accessed 20 Sep. 2019].

Ato.gov.au. (2019). Shares, units and similar investments. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Shares,-units-and-similar-

investments/ [Accessed 20 Sep. 2019].

Ato.gov.au. (2019). Sale of property and other CGT events. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/

Sale-of-property-and-other-CGT-events/ [Accessed 20 Sep. 2019].

Ato.gov.au. (2019). CGT assets and exemptions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/ [Accessed

20 Sep. 2019].

Classic.austlii.edu.au. (2019). INCOME TAX ASSESSMENT ACT 1997. [online]

Available at: http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/ [Accessed

20 Sep. 2019].

Page 10 of 10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.