BFA714: Australian Tax Law Assignment - Tom Lee Taxable Income

VerifiedAdded on 2023/01/19

|3

|719

|79

Homework Assignment

AI Summary

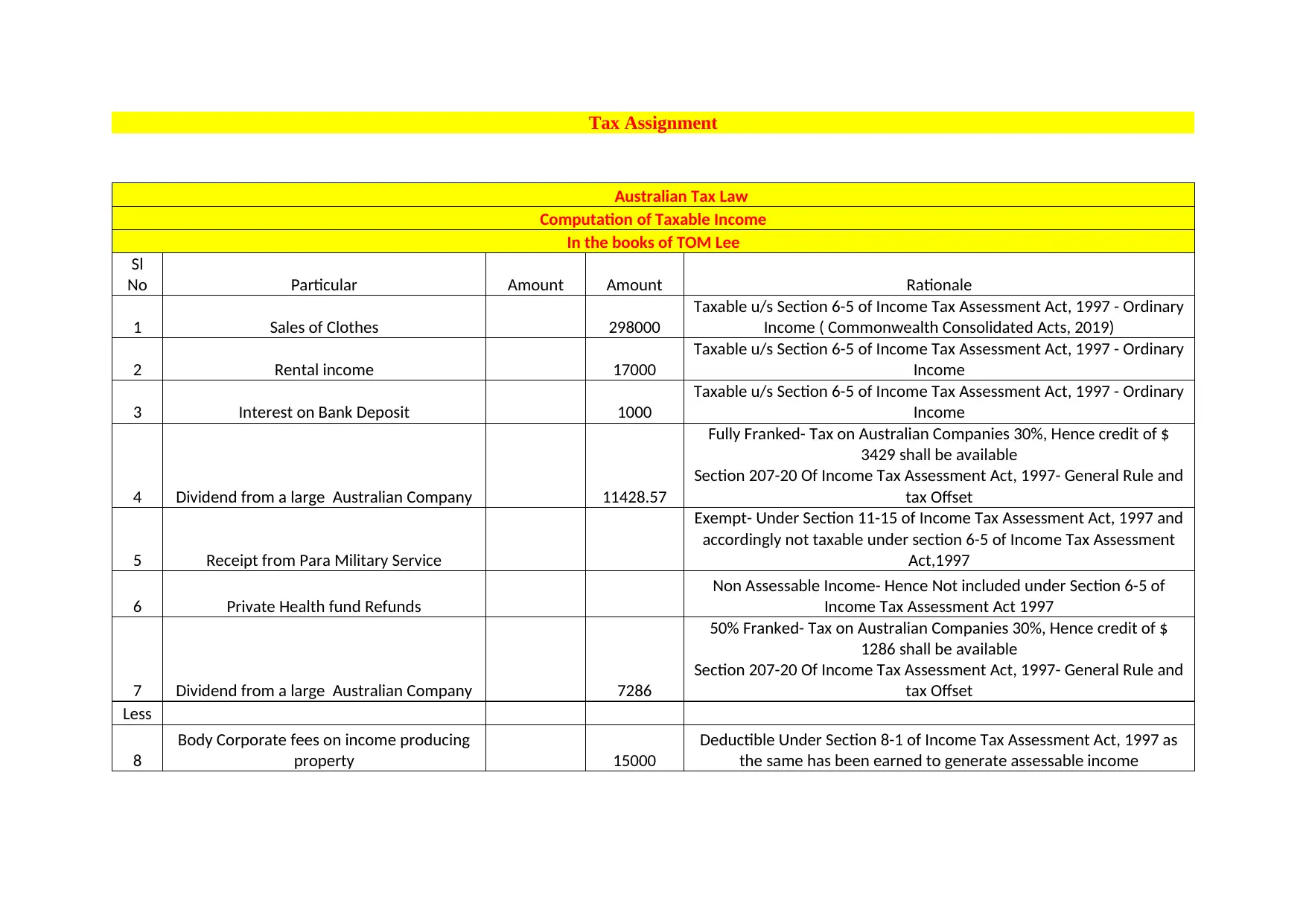

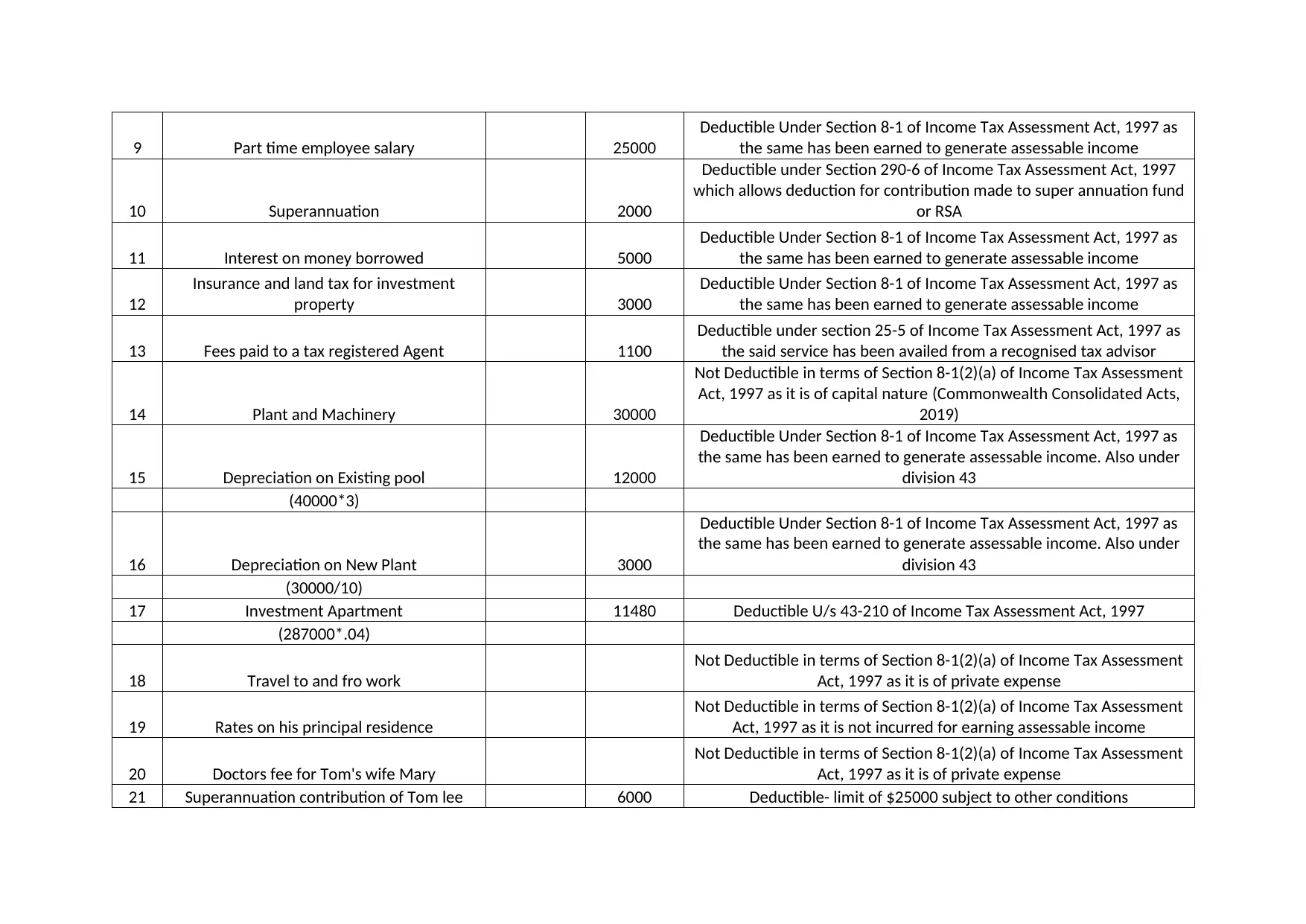

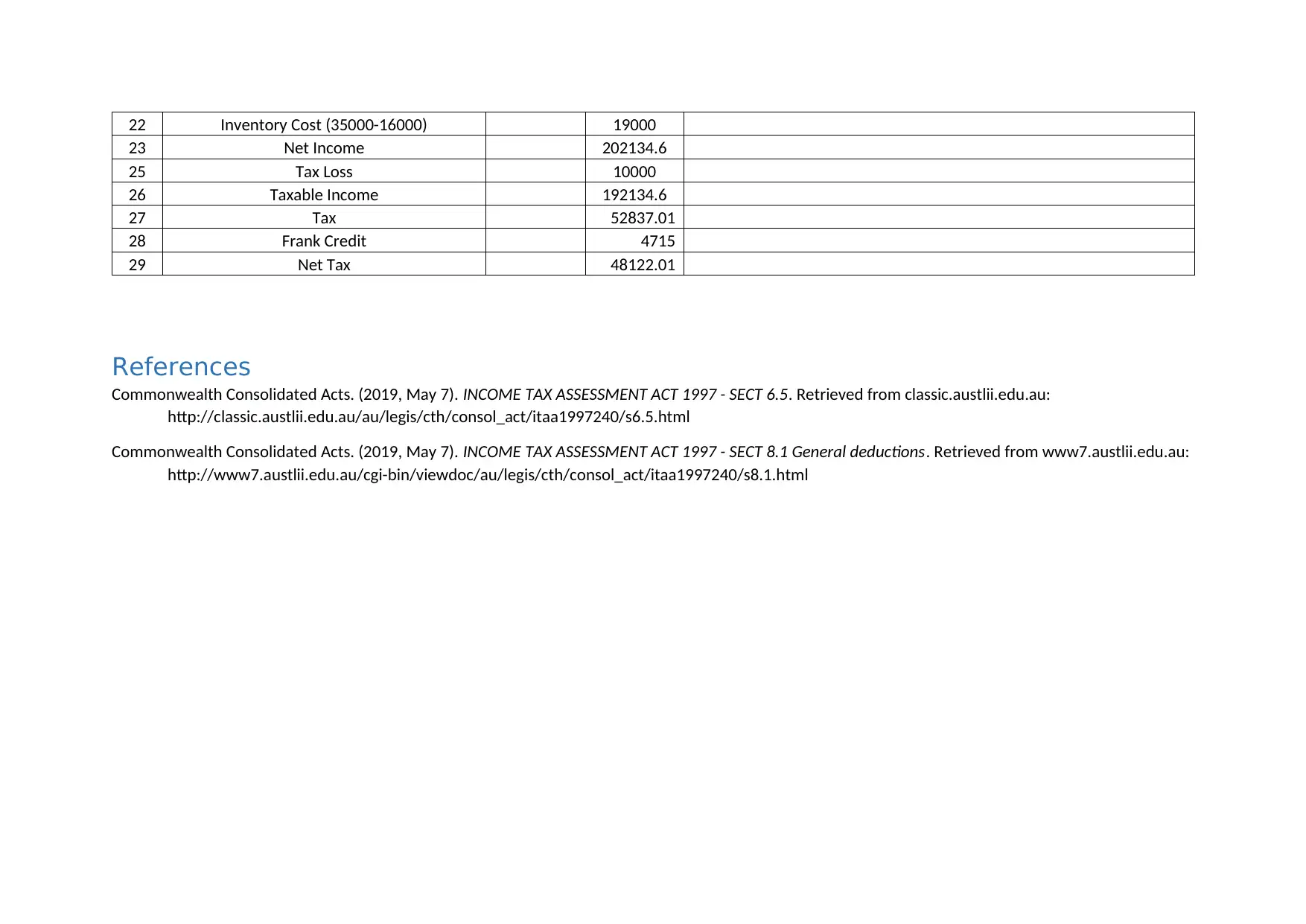

This document presents a detailed solution to an Australian tax law assignment for the BFA714 course, focusing on the computation of taxable income for a sole trader, Tom Lee, who runs a clothing shop. The assignment involves analyzing various income sources, including sales, rental income, interest, and dividends, and determining their taxability under the Income Tax Assessment Act 1997. It also addresses deductible expenses such as body corporate fees, employee salaries, superannuation contributions, interest on borrowed money, insurance, and fees paid to a tax agent. The solution meticulously calculates the taxable income, incorporating relevant tax offsets and depreciation, while referencing specific sections of the Income Tax Assessment Act 1997 to justify each calculation. The assignment covers ordinary income, franked dividends, non-assessable income, and various deductions, providing a comprehensive understanding of Australian taxation principles.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.