TLAW303 Taxation Law Assignment: Income, Medicare, and Tax Liability

VerifiedAdded on 2023/06/03

|16

|1550

|196

Homework Assignment

AI Summary

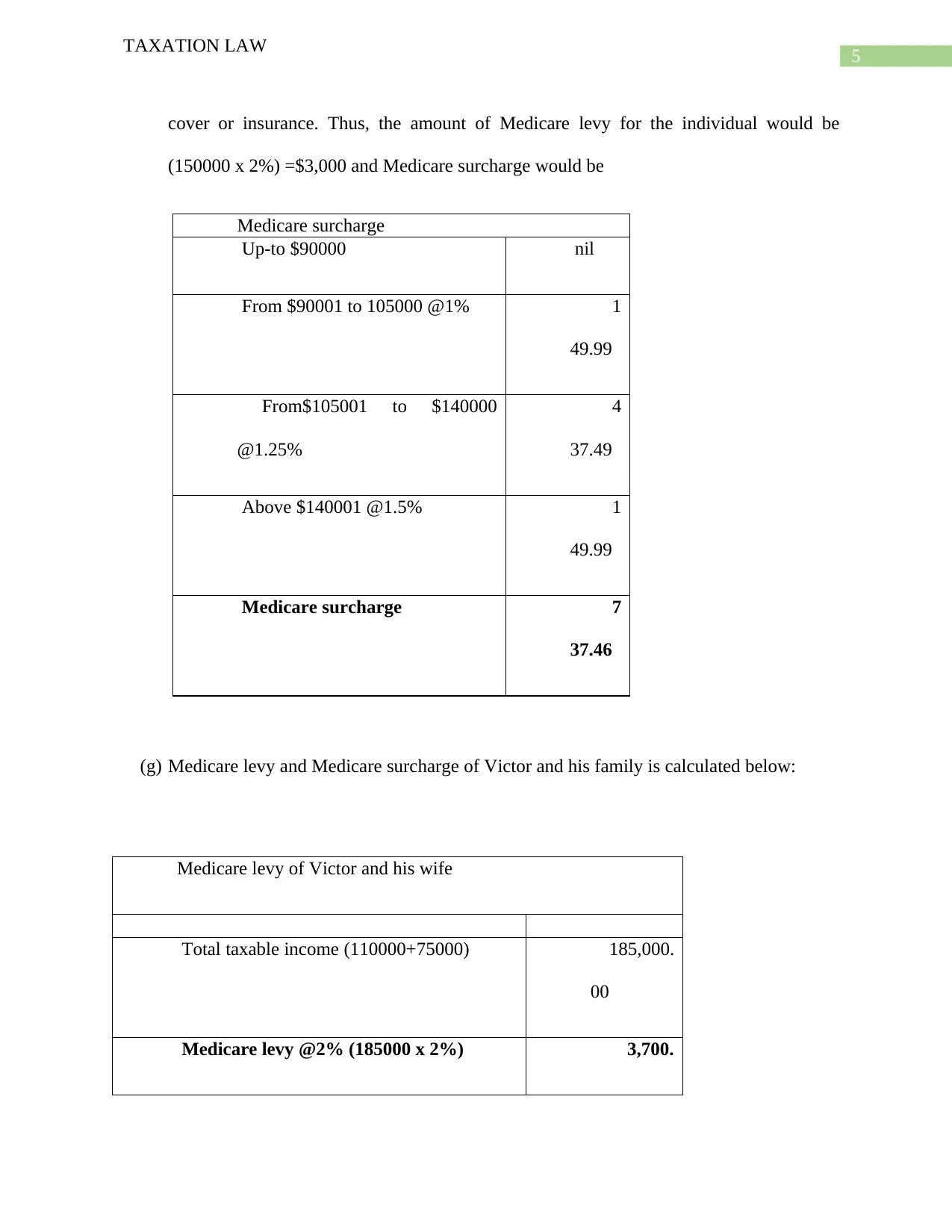

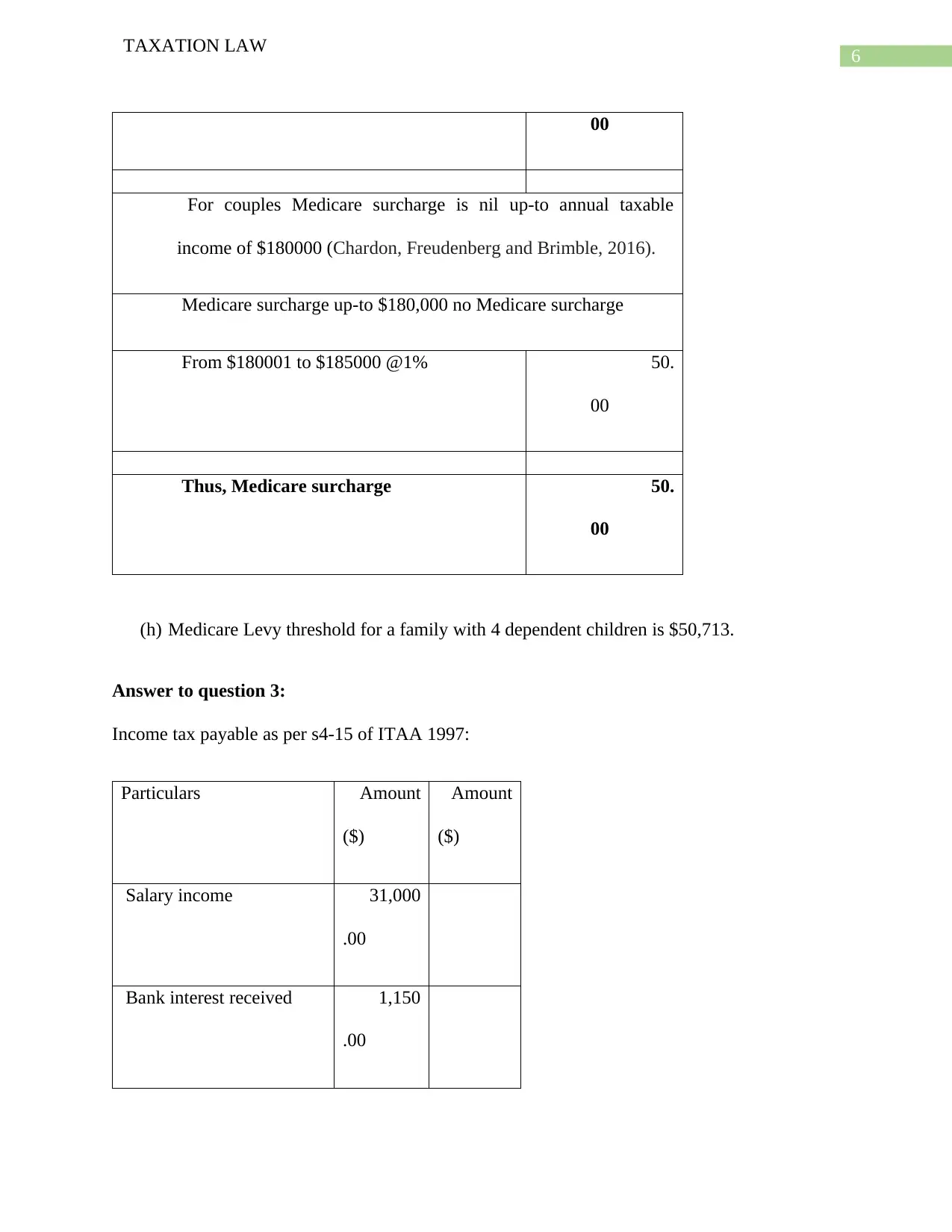

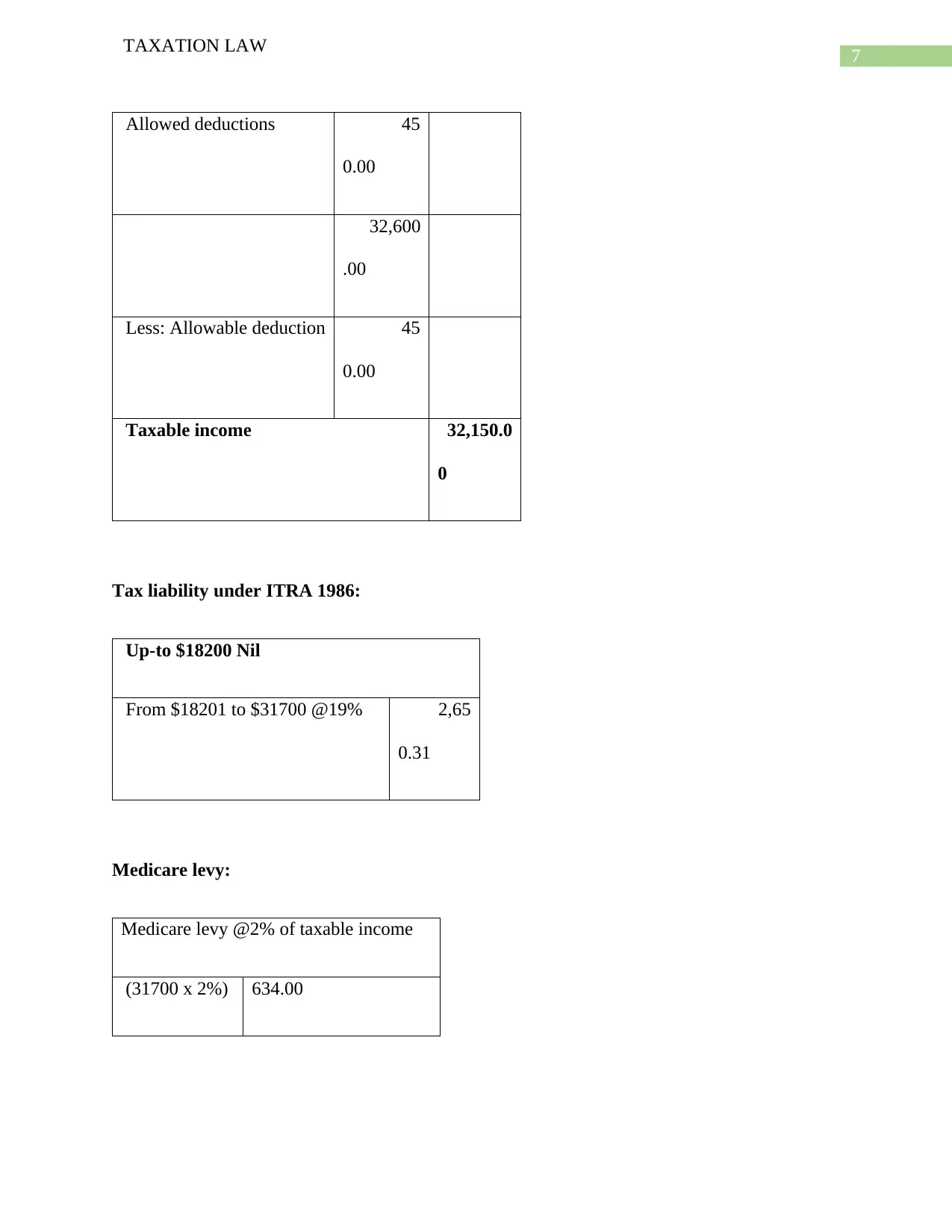

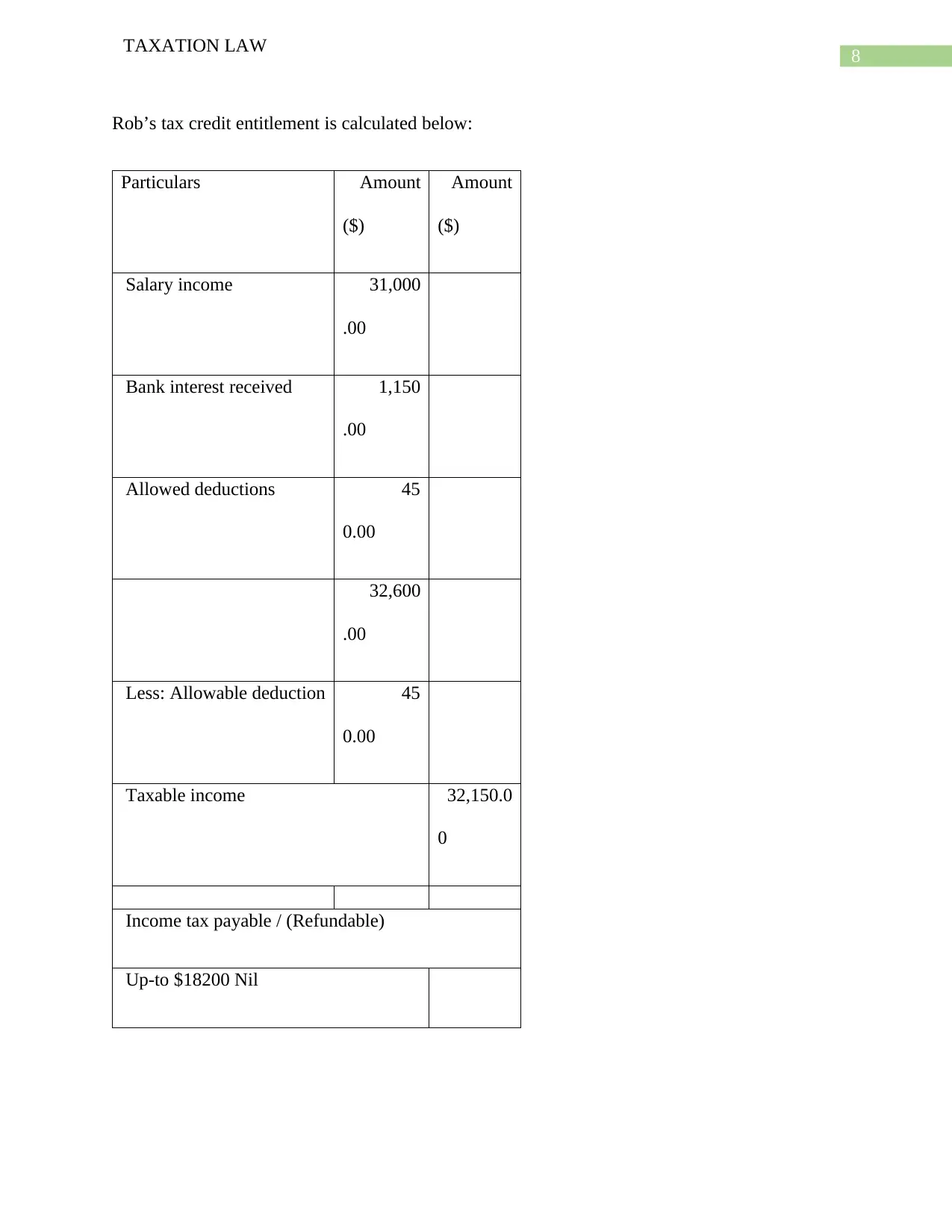

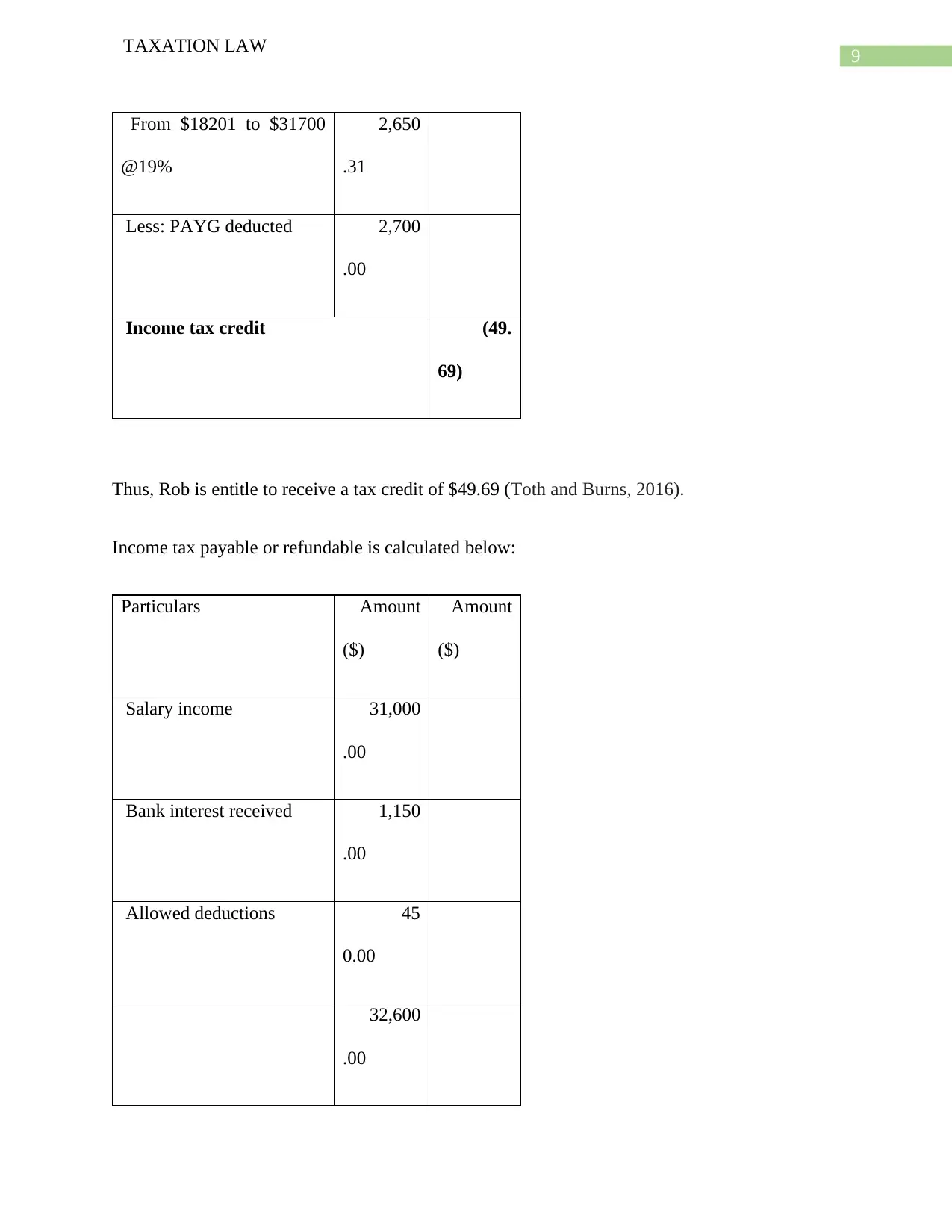

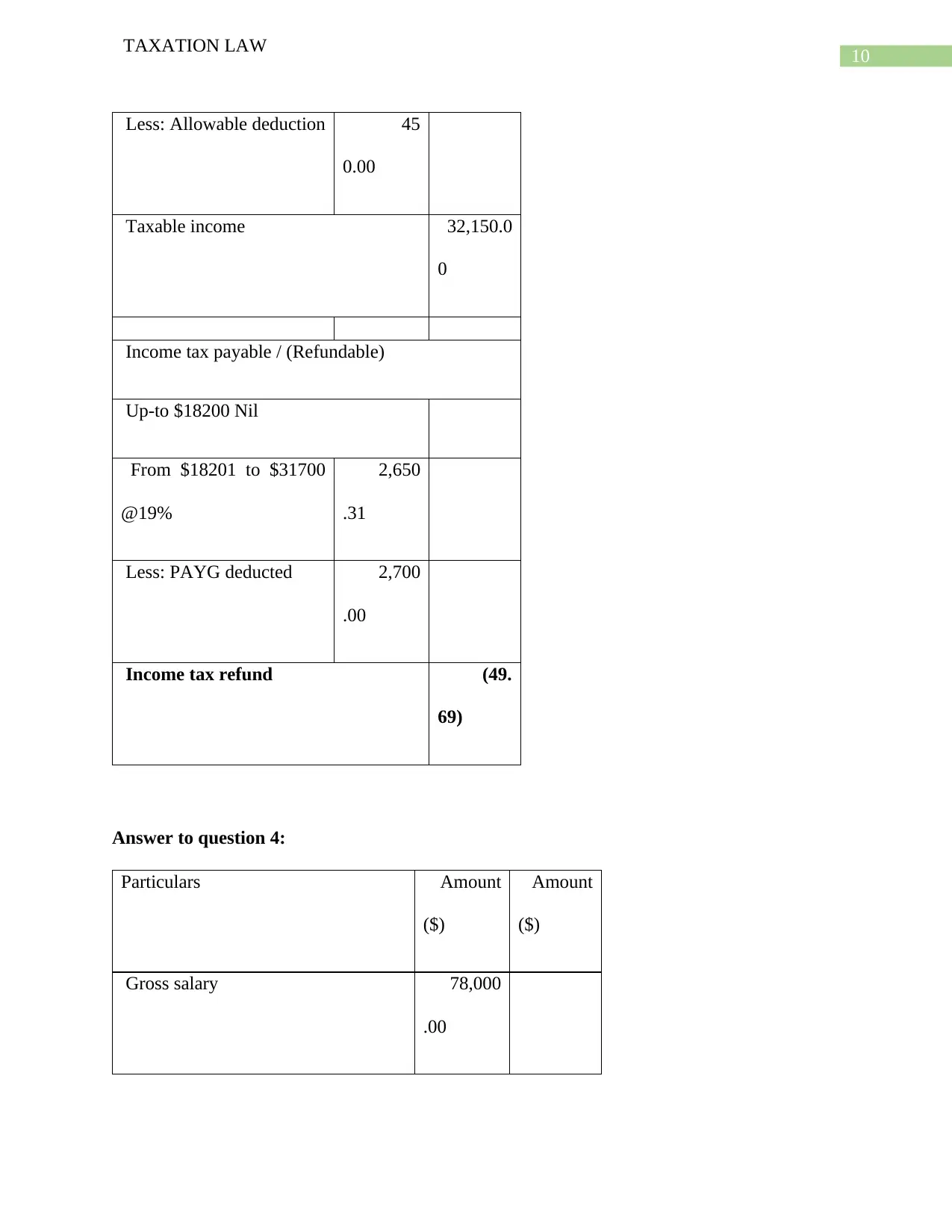

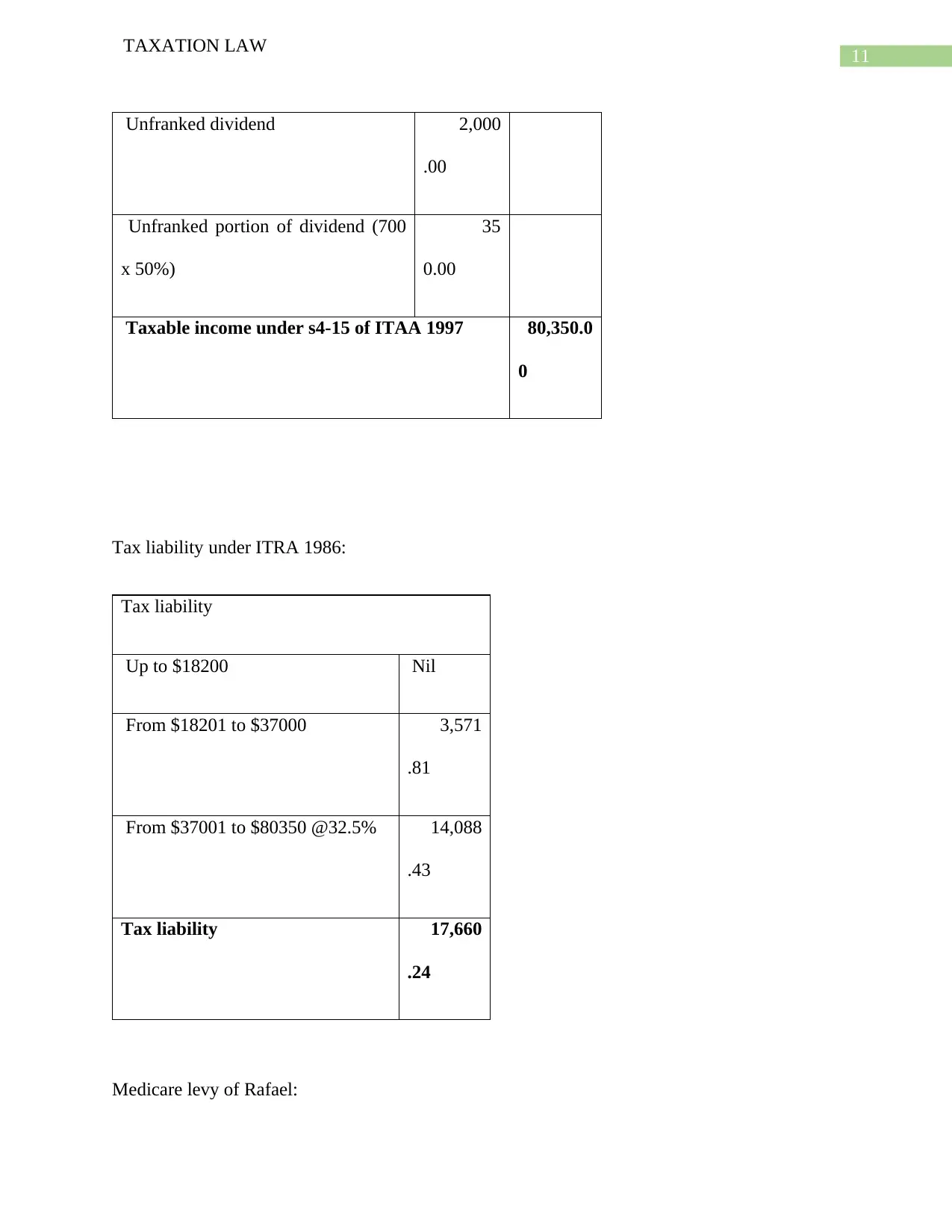

This assignment solution provides detailed calculations for income tax liabilities, Medicare levies, and Medicare surcharges for various scenarios, adhering to Australian tax laws and regulations. The solution addresses four key questions, calculating income tax payable for individuals and companies with different taxable incomes, including non-residents and working holiday visa holders. It also covers the calculation of Medicare levy and surcharge for different taxpayers, including those with private health insurance and families with dependents. Furthermore, the solution determines income tax payable or refundable, considering salary income, bank interest, and allowable deductions, as well as PAYG tax deducted. Finally, the assignment calculates tax liabilities, including Medicare levy, and income tax payable or refundable for individuals with unfranked dividends and PAYG tax withheld. The solution references relevant legislative provisions from the Income Tax Assessment Act 1997 and the Fringe Benefits Tax Assessment Act 1986.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.