Australian Taxation Law Assignment: Detailed Analysis and Solutions

VerifiedAdded on 2020/04/01

|13

|2977

|40

Homework Assignment

AI Summary

This assignment provides a detailed analysis of Australian Taxation Law, addressing various aspects such as the sources of tax law, including constitutional provisions and case laws, and the implications of specific legislation. It explores concepts like Medicare Levy, consumer protection, and the treatment of losses from theft. The assignment further examines deductions, including allowable deductions, stock valuation, and tax calculations based on income levels. Part B focuses on deductions of expenses and losses, while Part C delves into tax residency, and Part D examines assessable income, including employment income, gifts, and fringe benefits. The assignment provides a comprehensive overview of key concepts and their application in Australian tax law.

Running head: Australian Taxation law

Australian Taxation law

Name of Student:

Name of University:

Author’s Note:

Australian Taxation law

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUSTRALIAN TAXATION LAW

Table of Contents

Part A:..............................................................................................................................................2

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................2

Answer to question 3:......................................................................................................................2

Answer to question 4:......................................................................................................................3

Answer to question 5:......................................................................................................................3

Answer to question 6:......................................................................................................................3

Answer to question 7:......................................................................................................................4

Answer to question 8:......................................................................................................................4

Answer to question 9:......................................................................................................................5

Answer to question 10:....................................................................................................................5

Part B:..............................................................................................................................................5

Answer to Part C:.............................................................................................................................7

Answer to Part D:............................................................................................................................8

Answer to Part E:.............................................................................................................................9

References......................................................................................................................................11

AUSTRALIAN TAXATION LAW

Table of Contents

Part A:..............................................................................................................................................2

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................2

Answer to question 3:......................................................................................................................2

Answer to question 4:......................................................................................................................3

Answer to question 5:......................................................................................................................3

Answer to question 6:......................................................................................................................3

Answer to question 7:......................................................................................................................4

Answer to question 8:......................................................................................................................4

Answer to question 9:......................................................................................................................5

Answer to question 10:....................................................................................................................5

Part B:..............................................................................................................................................5

Answer to Part C:.............................................................................................................................7

Answer to Part D:............................................................................................................................8

Answer to Part E:.............................................................................................................................9

References......................................................................................................................................11

2

AUSTRALIAN TAXATION LAW

Part A:

Answer to question 1:

Based on the main source of the information taken from the commonwealth parliament

taxation regulation this has been seen to be derived as per section “51(ii), 53, 55, 90 and 96”. As

mentioned in the context of “Section 51(ii) of Australian Constitution”, the parliament is seen

to be having the power in formulation of laws as per the taxation. In subject to the provisional

laws, it is not seen to discriminate the various portions of the states (Barkoczy, 2016).

Answer to question 2:

The main source of the documentation is seen to set out with the law. The primary source

of the case laws is seen to comprise of the various types of case laws which has been created by

the statutory bodies. These sources have been further observed to be derived with the varied

centre of laws who is responsible for the single authoritative written record for the law. As per

the Australian law, the second source of the tax is seen to be interpreted based on the court

legislation and source of the tribunals. The main rulings have been further seen to be base on the

legislations defined by the commissioner of taxation (Albarea et al., 2015).

Answer to question 3:

The main ruling of the taxation as per “TR 98/17” and the main concern for this has been

further discerned as per the various legislation which seen able to be based on the “subsection 6

(1) of the Income Tax Assessment Act 193”.

The primary rule for this has been seen with the individuals who enter Australia

AUSTRALIAN TAXATION LAW

Part A:

Answer to question 1:

Based on the main source of the information taken from the commonwealth parliament

taxation regulation this has been seen to be derived as per section “51(ii), 53, 55, 90 and 96”. As

mentioned in the context of “Section 51(ii) of Australian Constitution”, the parliament is seen

to be having the power in formulation of laws as per the taxation. In subject to the provisional

laws, it is not seen to discriminate the various portions of the states (Barkoczy, 2016).

Answer to question 2:

The main source of the documentation is seen to set out with the law. The primary source

of the case laws is seen to comprise of the various types of case laws which has been created by

the statutory bodies. These sources have been further observed to be derived with the varied

centre of laws who is responsible for the single authoritative written record for the law. As per

the Australian law, the second source of the tax is seen to be interpreted based on the court

legislation and source of the tribunals. The main rulings have been further seen to be base on the

legislations defined by the commissioner of taxation (Albarea et al., 2015).

Answer to question 3:

The main ruling of the taxation as per “TR 98/17” and the main concern for this has been

further discerned as per the various legislation which seen able to be based on the “subsection 6

(1) of the Income Tax Assessment Act 193”.

The primary rule for this has been seen with the individuals who enter Australia

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUSTRALIAN TAXATION LAW

a. The migrants based in Australia

b. The individuals who went to Australia for studying or academics

c. The visitors on holiday

d. Workers with pre-arranged employment contracts

Answer to question 4:

“Medicare Levy” and “Medicare Levy Surcharge” and the different types of the

reductions have been computed with the inclusion of return on tax. The Medicare levy has been

further seen to be base on the different types of the calculation which has been seen to be taken

from the different types of consideration from the exemption and entitlement. The individual tax

payer has been further seen to levy the Medicare levy 2% partially fund for accessing the

healthcare (Devereux & Feria, 2014).

Answer to question 5:

As per “Schedule 2 of the Competition and Consumer Act 2010”, any sort of the

misconduct and the exclusion in “Section 18 of the Australian Consumer Law “. The preventive

measures associated to deceptive and artificial demeanour has been further defined under the

“Section 12DA of the Australian Securities and Investment Commission Act 2001”. The

primary objective has been further taken for consumer protection for the issues relating to

misleading practice of trade (Taylor & Richardson, 2014).

Answer to question 6:

As per “Section 25-45 of the ITAA 1997”, the loss has been seen to be originated from

the theft and this section has been seen to be based on the various types of the consideration

AUSTRALIAN TAXATION LAW

a. The migrants based in Australia

b. The individuals who went to Australia for studying or academics

c. The visitors on holiday

d. Workers with pre-arranged employment contracts

Answer to question 4:

“Medicare Levy” and “Medicare Levy Surcharge” and the different types of the

reductions have been computed with the inclusion of return on tax. The Medicare levy has been

further seen to be base on the different types of the calculation which has been seen to be taken

from the different types of consideration from the exemption and entitlement. The individual tax

payer has been further seen to levy the Medicare levy 2% partially fund for accessing the

healthcare (Devereux & Feria, 2014).

Answer to question 5:

As per “Schedule 2 of the Competition and Consumer Act 2010”, any sort of the

misconduct and the exclusion in “Section 18 of the Australian Consumer Law “. The preventive

measures associated to deceptive and artificial demeanour has been further defined under the

“Section 12DA of the Australian Securities and Investment Commission Act 2001”. The

primary objective has been further taken for consumer protection for the issues relating to

misleading practice of trade (Taylor & Richardson, 2014).

Answer to question 6:

As per “Section 25-45 of the ITAA 1997”, the loss has been seen to be originated from

the theft and this section has been seen to be based on the various types of the consideration

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUSTRALIAN TAXATION LAW

taken from the loss concerning money. The important treatment for the same has been listed

below as follows:

a. If the loss ascertained by the individual is ascertained in the income year

b. In case the loss has been accounted as per the activities of the theft

c. This particular amount needs to be further seen to be related to the engagement of the

chargeable income and the individual taken from the previous year (Jatrana et al., 2014).

Answer to question 7:

As per the case “W Thomas & Co Pty Ltd v FC of T (1965)”, the various types of

deductions which has been seen to be considered as per the report which has been undertaken by

the tax payers. The case study has been further able to relate to various types of concerns related

to merchant of grain and purchase of building. The taxpayer has undertaken huge sum of repairs

which has been taken based on the roof, walls and floor of the premises. The main interpretations

of the case have included the cost of repairs. This is not taken based on the allowable deductions

as the expenditure as the amount incurred in repairs was not considered with the objective

deriving chargeable income of the taxpayer (Herault & Azpitarte, 2015).

Answer to question 8:

The main value of the stock has been further seen to be based on inclusion of valuing

stock at the end of the income year when it was taken place:

a) The taxpayer will be able to consider this method by alignment of the related stock as per

the present situation and location.

AUSTRALIAN TAXATION LAW

taken from the loss concerning money. The important treatment for the same has been listed

below as follows:

a. If the loss ascertained by the individual is ascertained in the income year

b. In case the loss has been accounted as per the activities of the theft

c. This particular amount needs to be further seen to be related to the engagement of the

chargeable income and the individual taken from the previous year (Jatrana et al., 2014).

Answer to question 7:

As per the case “W Thomas & Co Pty Ltd v FC of T (1965)”, the various types of

deductions which has been seen to be considered as per the report which has been undertaken by

the tax payers. The case study has been further able to relate to various types of concerns related

to merchant of grain and purchase of building. The taxpayer has undertaken huge sum of repairs

which has been taken based on the roof, walls and floor of the premises. The main interpretations

of the case have included the cost of repairs. This is not taken based on the allowable deductions

as the expenditure as the amount incurred in repairs was not considered with the objective

deriving chargeable income of the taxpayer (Herault & Azpitarte, 2015).

Answer to question 8:

The main value of the stock has been further seen to be based on inclusion of valuing

stock at the end of the income year when it was taken place:

a) The taxpayer will be able to consider this method by alignment of the related stock as per

the present situation and location.

5

AUSTRALIAN TAXATION LAW

b) The selling value as per the market has been further considered based on the ordinary

activity of the trading.

c) The procurement of the substitute cost is identical to the purchase price

Answer to question 9:

An individual with a taxable income of $45,000 needs to pay a tax amount of $3572.

Moreover, the taxpayer is obliged to pay 32.5 for every $1 over $37,000.

Answer to question 10:

The employer and the taxpayer has been seen to be referred as PAYG as “Pay As You

Go”, which consists of making the payment at regular interval to the employees. The collection

of the PAYG tax acts as an instalment procedure for the instalment method for the tax collection

done at regular payments towards the expected income of the individual. It has been further

discerned that the individual will under the obligation for returning the file for that particular

year (Rohlin et al., 2014).

Part B:

It has been stated with “Division 8 of the Income Tax Assessment Act 1997”, with the

guidelines which are associated to the deductions of expenses and losses. The division has been

further seen to provide the various types of provisions for the assistance in making the

differentiation of the usual deductions under “section 8-1 of the ITAA 1997”. It has been further

able to provide the guideline for the deductions which needs to be considered as per the “section

8-1 of the ITAA 1997” (Khadem, 2015). An individual as per “section 8-1 of the ITAA 1997”

will be able to claim for the deductions relating to the expenditure and the loss associated to:

AUSTRALIAN TAXATION LAW

b) The selling value as per the market has been further considered based on the ordinary

activity of the trading.

c) The procurement of the substitute cost is identical to the purchase price

Answer to question 9:

An individual with a taxable income of $45,000 needs to pay a tax amount of $3572.

Moreover, the taxpayer is obliged to pay 32.5 for every $1 over $37,000.

Answer to question 10:

The employer and the taxpayer has been seen to be referred as PAYG as “Pay As You

Go”, which consists of making the payment at regular interval to the employees. The collection

of the PAYG tax acts as an instalment procedure for the instalment method for the tax collection

done at regular payments towards the expected income of the individual. It has been further

discerned that the individual will under the obligation for returning the file for that particular

year (Rohlin et al., 2014).

Part B:

It has been stated with “Division 8 of the Income Tax Assessment Act 1997”, with the

guidelines which are associated to the deductions of expenses and losses. The division has been

further seen to provide the various types of provisions for the assistance in making the

differentiation of the usual deductions under “section 8-1 of the ITAA 1997”. It has been further

able to provide the guideline for the deductions which needs to be considered as per the “section

8-1 of the ITAA 1997” (Khadem, 2015). An individual as per “section 8-1 of the ITAA 1997”

will be able to claim for the deductions relating to the expenditure and the loss associated to:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUSTRALIAN TAXATION LAW

a. Derivation of the assessable income

b. Associated expense with the individual taxpayers and the activities of trade

The taxpayers are further seen to be provided with the opportunity for claiming particular

deductions from assessable income as per “section 8-5 of the ITAA 1997”. The main

consideration of Ram has been further incurred with the characteristics and deductions which

have been further seen to be explained based on the various types of the consideration based

on the stated income. An individual taxpayer may be able file for the tax return, and the same

is applicable for Ram for drafting an objection against assessment made.

It has been further seen to be understood that “Para 11 of the Taxation Ruling 2011/5”,

clearly states that individual taxpayer can raise objection for not being satisfied with the tax

assessment stated in section “175A(1) of the Income Tax Assessment Act 1936. The Interpretive

Decision 2002/81” has been further seen to be associated to number of issues for the allowable

expenditure for book-keeping expense and legal disagreement. As per the present situation Ram

will be able to claim for the allowed deductions as per “section 8-1 of the ITAA1997” for

incurring solicitor expense (Meng, Siriwardana, & McNeill, 2013).

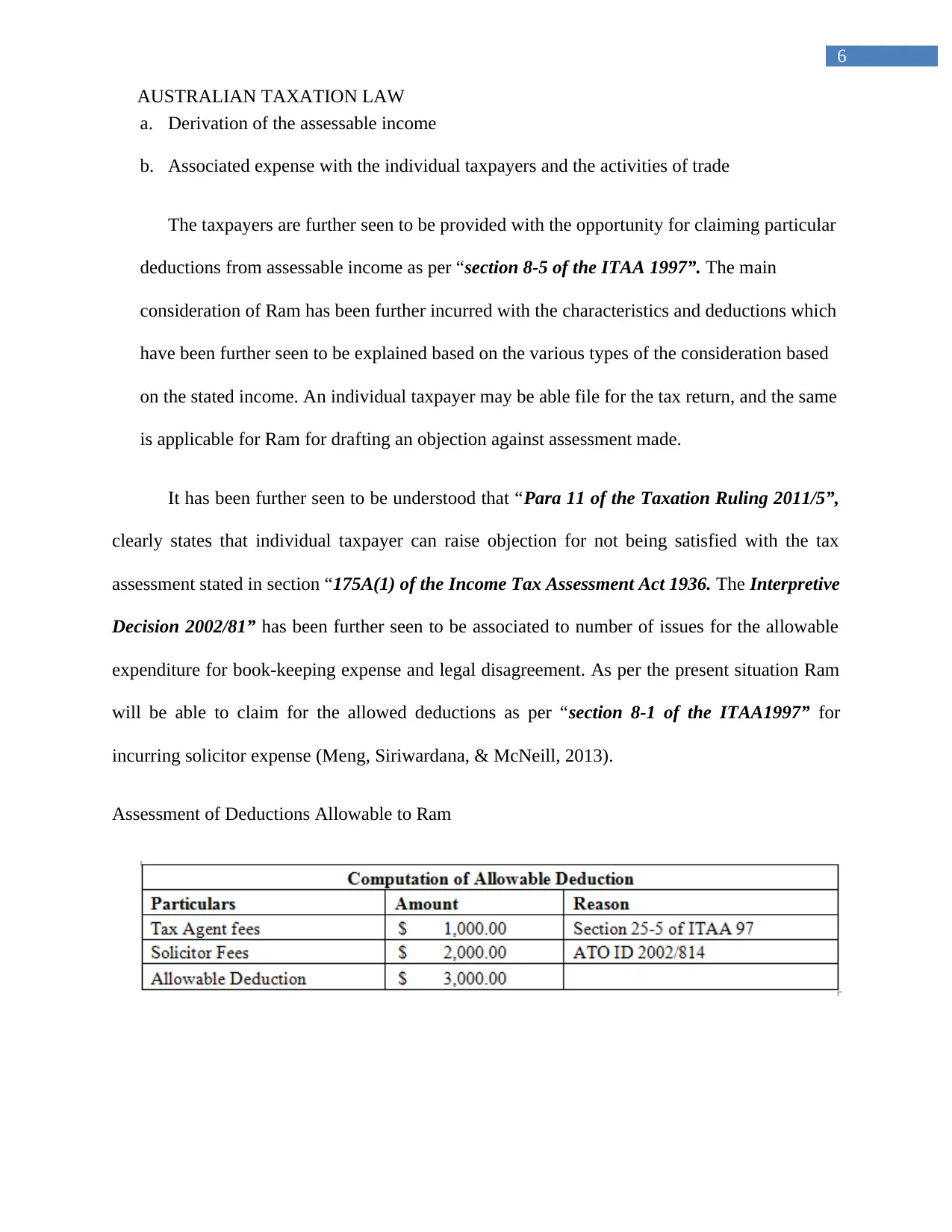

Assessment of Deductions Allowable to Ram

AUSTRALIAN TAXATION LAW

a. Derivation of the assessable income

b. Associated expense with the individual taxpayers and the activities of trade

The taxpayers are further seen to be provided with the opportunity for claiming particular

deductions from assessable income as per “section 8-5 of the ITAA 1997”. The main

consideration of Ram has been further incurred with the characteristics and deductions which

have been further seen to be explained based on the various types of the consideration based

on the stated income. An individual taxpayer may be able file for the tax return, and the same

is applicable for Ram for drafting an objection against assessment made.

It has been further seen to be understood that “Para 11 of the Taxation Ruling 2011/5”,

clearly states that individual taxpayer can raise objection for not being satisfied with the tax

assessment stated in section “175A(1) of the Income Tax Assessment Act 1936. The Interpretive

Decision 2002/81” has been further seen to be associated to number of issues for the allowable

expenditure for book-keeping expense and legal disagreement. As per the present situation Ram

will be able to claim for the allowed deductions as per “section 8-1 of the ITAA1997” for

incurring solicitor expense (Meng, Siriwardana, & McNeill, 2013).

Assessment of Deductions Allowable to Ram

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUSTRALIAN TAXATION LAW

Answer to Part C:

The resident has been defined as per the “section 995-1 of the ITAA 1997”, which has

been further illustrated with the treatment of Australian resident for taxation. This has been

further seen to be defined as per “Section 6-1 of the ITAA 1997”. There have been several

explanations of the residents and the states under the primary residential status determination. As

per “Para 32 of the Taxation Ruling 98/17”, an individual will be treated as a tax resident of

Australia in conformity with the “section 6-1 of the ITAA 1936”. There has been mainly four

residency test observed for determining the residential status as per “Section 6-1 of the Income

tax Assessment Act 1936”. The aforementioned tests are stated as follows:

a. Status of residency as per ordinary concept

b. Test for place of abode

c. 183 days test

d. Test of superannuation

The taxpayer has been seen to be arrived as an international student in Brisbane for the study

and considered as an occupant for tax assessment based on the ordinary concept. In case the

treatment is not done as per Australian inhabitant, the concerning ordinary concept for the

statutory test is applicable for the ascertainment of the status of occupancy and complying with

the primary test.

As per the test of domicile, a person with permanent dwelling in Australia will be

considered as an occupant of Australia for taxation. On the contrary, the occupant of Australia

will be enrolled with more than six month of duration. The present case of Tina has been noticed

with the arrival in Australia for the educational reason and period of residence for more than 183

AUSTRALIAN TAXATION LAW

Answer to Part C:

The resident has been defined as per the “section 995-1 of the ITAA 1997”, which has

been further illustrated with the treatment of Australian resident for taxation. This has been

further seen to be defined as per “Section 6-1 of the ITAA 1997”. There have been several

explanations of the residents and the states under the primary residential status determination. As

per “Para 32 of the Taxation Ruling 98/17”, an individual will be treated as a tax resident of

Australia in conformity with the “section 6-1 of the ITAA 1936”. There has been mainly four

residency test observed for determining the residential status as per “Section 6-1 of the Income

tax Assessment Act 1936”. The aforementioned tests are stated as follows:

a. Status of residency as per ordinary concept

b. Test for place of abode

c. 183 days test

d. Test of superannuation

The taxpayer has been seen to be arrived as an international student in Brisbane for the study

and considered as an occupant for tax assessment based on the ordinary concept. In case the

treatment is not done as per Australian inhabitant, the concerning ordinary concept for the

statutory test is applicable for the ascertainment of the status of occupancy and complying with

the primary test.

As per the test of domicile, a person with permanent dwelling in Australia will be

considered as an occupant of Australia for taxation. On the contrary, the occupant of Australia

will be enrolled with more than six month of duration. The present case of Tina has been noticed

with the arrival in Australia for the educational reason and period of residence for more than 183

8

AUSTRALIAN TAXATION LAW

days. Henceforth, the result has been seen with Tina being regarded as an Australian occupant

for determination of Tax.

Answer to Part D:

Based on the “Section 4-15 of the ITAA 1997”, a resident of Australia is taxed for the

incomes derived from global rulings. Based on the rulings of the section from the taxable

income, the computation is done as per the subtraction of the allowable deductions from the

assessable income. The categorization of the assessable income has been considered as per

“Section 6-5 of the Income tax Assessment Act 1997”. The “section 6-10 of the ITAA 97”

income is not considered as an ordinary income and not considered under the statutory income.

The current scenario of Jimmy and the income has been regarded with the employment in the

restaurant which will be derived as per the ordinary income and various types of the

consideration with “section 6-5 of the ITAA 97”.

The tips received by Jimmy have been considered based on the incentives and have a

direct relation with the employment income which will be a part of the income assessable. The

receipt of the sum has been further seen to be considered as per the purpose of taxation. Based on

the given case Jimmy has received a total amount of $250 included in the assessable income. It

needs to be further noted that the various types of consideration for the assessable income has

been determined based on the exempted income and the income which has been not been

considered as per “section 6-20 of the Income Tax Assessment Act 1997”.

It has been further discerned that gifts are not considered for taxable income and not

received as a portion of the business activity which has been a part of the producing activity of

the taxable income. On the contrary, the gifts are received on part of the parents which are not

AUSTRALIAN TAXATION LAW

days. Henceforth, the result has been seen with Tina being regarded as an Australian occupant

for determination of Tax.

Answer to Part D:

Based on the “Section 4-15 of the ITAA 1997”, a resident of Australia is taxed for the

incomes derived from global rulings. Based on the rulings of the section from the taxable

income, the computation is done as per the subtraction of the allowable deductions from the

assessable income. The categorization of the assessable income has been considered as per

“Section 6-5 of the Income tax Assessment Act 1997”. The “section 6-10 of the ITAA 97”

income is not considered as an ordinary income and not considered under the statutory income.

The current scenario of Jimmy and the income has been regarded with the employment in the

restaurant which will be derived as per the ordinary income and various types of the

consideration with “section 6-5 of the ITAA 97”.

The tips received by Jimmy have been considered based on the incentives and have a

direct relation with the employment income which will be a part of the income assessable. The

receipt of the sum has been further seen to be considered as per the purpose of taxation. Based on

the given case Jimmy has received a total amount of $250 included in the assessable income. It

needs to be further noted that the various types of consideration for the assessable income has

been determined based on the exempted income and the income which has been not been

considered as per “section 6-20 of the Income Tax Assessment Act 1997”.

It has been further discerned that gifts are not considered for taxable income and not

received as a portion of the business activity which has been a part of the producing activity of

the taxable income. On the contrary, the gifts are received on part of the parents which are not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUSTRALIAN TAXATION LAW

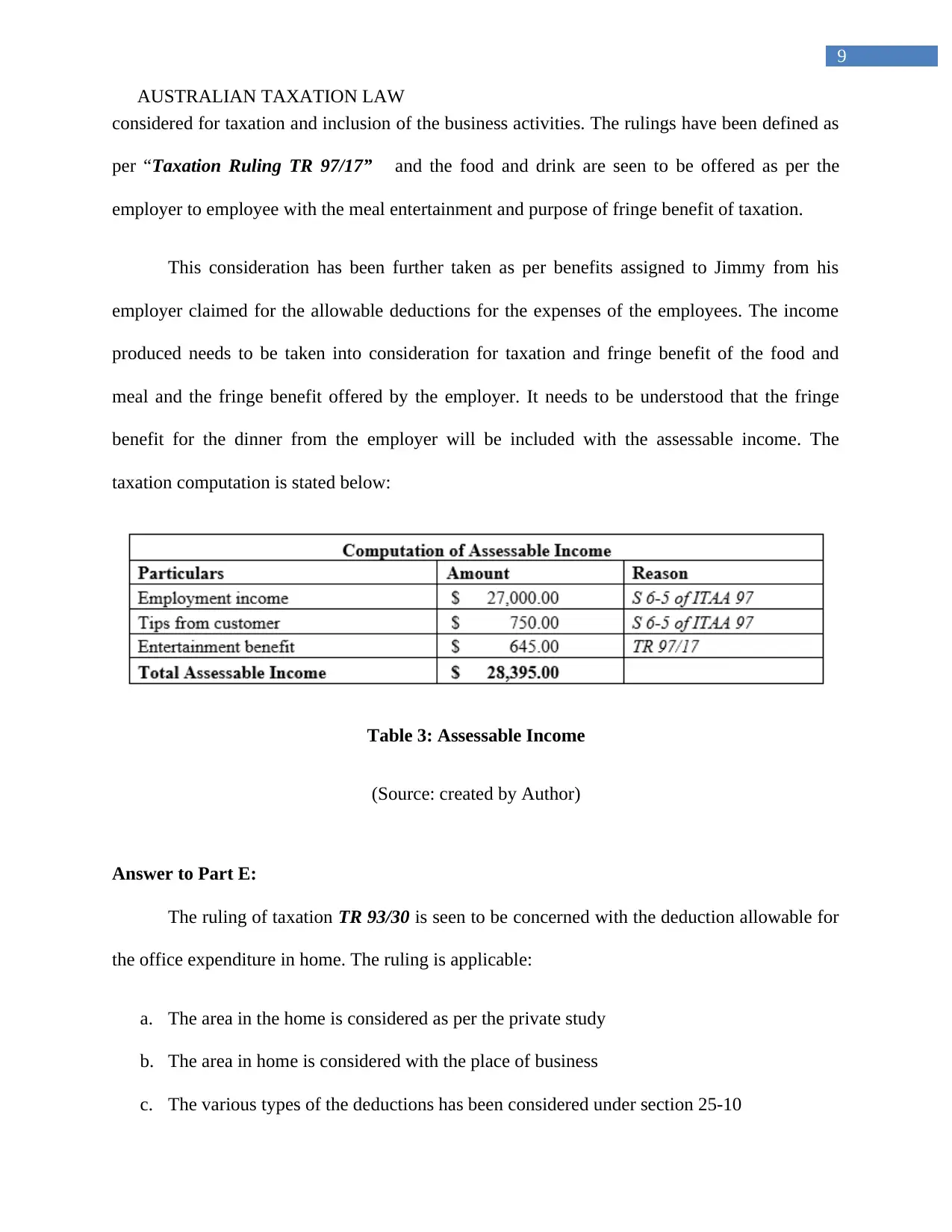

considered for taxation and inclusion of the business activities. The rulings have been defined as

per “Taxation Ruling TR 97/17” and the food and drink are seen to be offered as per the

employer to employee with the meal entertainment and purpose of fringe benefit of taxation.

This consideration has been further taken as per benefits assigned to Jimmy from his

employer claimed for the allowable deductions for the expenses of the employees. The income

produced needs to be taken into consideration for taxation and fringe benefit of the food and

meal and the fringe benefit offered by the employer. It needs to be understood that the fringe

benefit for the dinner from the employer will be included with the assessable income. The

taxation computation is stated below:

Table 3: Assessable Income

(Source: created by Author)

Answer to Part E:

The ruling of taxation TR 93/30 is seen to be concerned with the deduction allowable for

the office expenditure in home. The ruling is applicable:

a. The area in the home is considered as per the private study

b. The area in home is considered with the place of business

c. The various types of the deductions has been considered under section 25-10

AUSTRALIAN TAXATION LAW

considered for taxation and inclusion of the business activities. The rulings have been defined as

per “Taxation Ruling TR 97/17” and the food and drink are seen to be offered as per the

employer to employee with the meal entertainment and purpose of fringe benefit of taxation.

This consideration has been further taken as per benefits assigned to Jimmy from his

employer claimed for the allowable deductions for the expenses of the employees. The income

produced needs to be taken into consideration for taxation and fringe benefit of the food and

meal and the fringe benefit offered by the employer. It needs to be understood that the fringe

benefit for the dinner from the employer will be included with the assessable income. The

taxation computation is stated below:

Table 3: Assessable Income

(Source: created by Author)

Answer to Part E:

The ruling of taxation TR 93/30 is seen to be concerned with the deduction allowable for

the office expenditure in home. The ruling is applicable:

a. The area in the home is considered as per the private study

b. The area in home is considered with the place of business

c. The various types of the deductions has been considered under section 25-10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUSTRALIAN TAXATION LAW

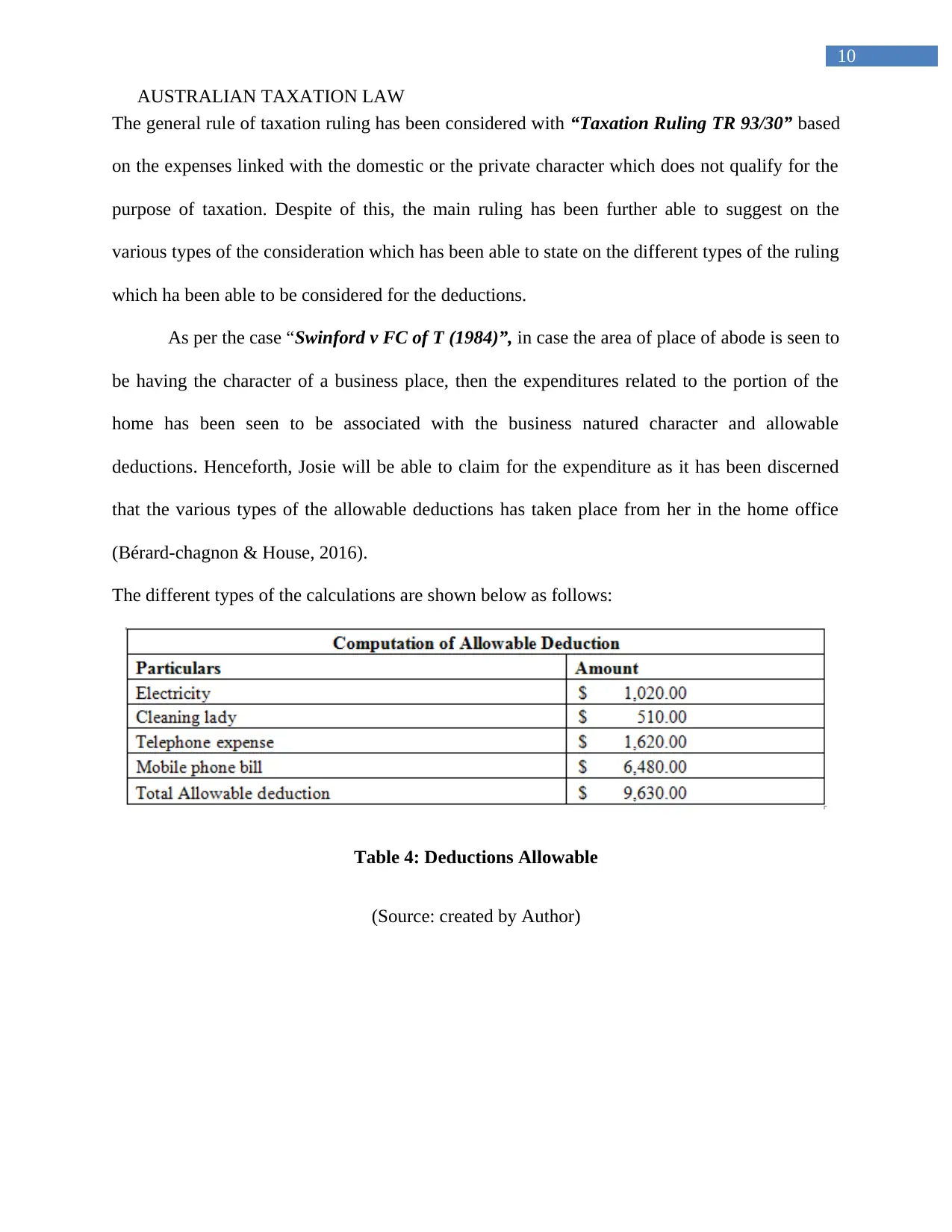

The general rule of taxation ruling has been considered with “Taxation Ruling TR 93/30” based

on the expenses linked with the domestic or the private character which does not qualify for the

purpose of taxation. Despite of this, the main ruling has been further able to suggest on the

various types of the consideration which has been able to state on the different types of the ruling

which ha been able to be considered for the deductions.

As per the case “Swinford v FC of T (1984)”, in case the area of place of abode is seen to

be having the character of a business place, then the expenditures related to the portion of the

home has been seen to be associated with the business natured character and allowable

deductions. Henceforth, Josie will be able to claim for the expenditure as it has been discerned

that the various types of the allowable deductions has taken place from her in the home office

(Bérard-chagnon & House, 2016).

The different types of the calculations are shown below as follows:

Table 4: Deductions Allowable

(Source: created by Author)

AUSTRALIAN TAXATION LAW

The general rule of taxation ruling has been considered with “Taxation Ruling TR 93/30” based

on the expenses linked with the domestic or the private character which does not qualify for the

purpose of taxation. Despite of this, the main ruling has been further able to suggest on the

various types of the consideration which has been able to state on the different types of the ruling

which ha been able to be considered for the deductions.

As per the case “Swinford v FC of T (1984)”, in case the area of place of abode is seen to

be having the character of a business place, then the expenditures related to the portion of the

home has been seen to be associated with the business natured character and allowable

deductions. Henceforth, Josie will be able to claim for the expenditure as it has been discerned

that the various types of the allowable deductions has taken place from her in the home office

(Bérard-chagnon & House, 2016).

The different types of the calculations are shown below as follows:

Table 4: Deductions Allowable

(Source: created by Author)

11

AUSTRALIAN TAXATION LAW

References

Albarea, A., Bernasconi, M., Di Novi, C., Marenzi, A., Rizzi, D., & Zantomio, F. (2015).

Accounting for tax evasion profiles and tax expenditures in microsimulation modelling. the

betamod model for personal income taxes in Italy. International Journal of

Microsimulation, 8(3), 99–136.

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Bérard-chagnon, J., & House, G. (2016). Using data linkage to evaluate the consistency of place

of residence between census data and tax data. In Proceedings of Statistics Canada

Symposium.

Devereux, M., & Feria, R. de la. (2014). Designing and Implementing a Destination-Based

Corporate Tax. Oxford University Centre for Business Taxation, (May), 1.

Herault, N., & Azpitarte, F. (2015). Recent Trends in Income Redistribution in Australia: Can

Changes in the Tax-Benefit System Account for the Decline in Redistribution? Economic

Record, 91(292), 38–53. https://doi.org/10.1111/1475-4932.12154

Jatrana, S., Pasupuleti, S. S. R., & Richardson, K. (2014). Nativity, duration of residence and

chronic health conditions in Australia: Do trends converge towards the native-born

population? Social Science and Medicine, 119, 53–63.

https://doi.org/10.1016/j.socscimed.2014.08.008

Khadem, N. (2015). Tax the rich and save the budget $19.5b a year, The Australia Institute

urges. The Australian Financial Review, p. 2.

AUSTRALIAN TAXATION LAW

References

Albarea, A., Bernasconi, M., Di Novi, C., Marenzi, A., Rizzi, D., & Zantomio, F. (2015).

Accounting for tax evasion profiles and tax expenditures in microsimulation modelling. the

betamod model for personal income taxes in Italy. International Journal of

Microsimulation, 8(3), 99–136.

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Bérard-chagnon, J., & House, G. (2016). Using data linkage to evaluate the consistency of place

of residence between census data and tax data. In Proceedings of Statistics Canada

Symposium.

Devereux, M., & Feria, R. de la. (2014). Designing and Implementing a Destination-Based

Corporate Tax. Oxford University Centre for Business Taxation, (May), 1.

Herault, N., & Azpitarte, F. (2015). Recent Trends in Income Redistribution in Australia: Can

Changes in the Tax-Benefit System Account for the Decline in Redistribution? Economic

Record, 91(292), 38–53. https://doi.org/10.1111/1475-4932.12154

Jatrana, S., Pasupuleti, S. S. R., & Richardson, K. (2014). Nativity, duration of residence and

chronic health conditions in Australia: Do trends converge towards the native-born

population? Social Science and Medicine, 119, 53–63.

https://doi.org/10.1016/j.socscimed.2014.08.008

Khadem, N. (2015). Tax the rich and save the budget $19.5b a year, The Australia Institute

urges. The Australian Financial Review, p. 2.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.