Taxation Law Assignment: Income Tax for Residents and Non-Residents

VerifiedAdded on 2020/03/01

|9

|2395

|64

Homework Assignment

AI Summary

This taxation law assignment addresses the tax implications for Australian residents and non-residents. Part A examines the tax obligations of Robyn Rainer, an Australian resident working abroad, detailing how foreign income is treated, including assessable income, foreign tax offsets, and tax return requirements. It also explains the shift from resident to non-resident status. Part B analyzes the tax situation of Paul, a golf trainer, considering his various income sources (lesson fees, buggy repairs, and a gift) and calculating his total assessable income, including relevant deductions and the nature of professional income versus gifts. The assignment provides detailed calculations and references relevant Australian tax laws and case studies.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Answer- Part A

For the tax year 2016/17:

Robyn Rainer was a resident of Australia and was working as a lecturer at Victoria University.

During the income year 2016/17, Robyn Rainer had to shift to India as she was selected as

coordinator for business courses of Victoria University that were being conducted in Calcutta

University, India. Robyn shall be considered as resident during tax year 2016/17 as she resides in

Australia only and as per the Australian Taxation laws, any person who resides in Australia is

considered as Australian residents for tax purpose and he does not need to apply for any other

residency tests.

In the present case, as Robyn Rainer was not residing in Australia for the full year, hence the

other conditions need to be considered for assessing his residence status such as domicile test,

183-day test. In the given case, no information is given for domicile test hence we shall consider

the 183-day test. Robyn was in Australia for the period 01.07.2016 to 13.01.17 during the tax

year 2016/17 which means that she had resided in Australia for 197 days during tax year

2016/17. Seeing this condition also, Robyn shall be considered a Resident of Australia for tax

year 2016/17 (Saunders et. al, 2015).

As per the relevant provisions of the Australian Tax Laws, the income earned from working

abroad for a person who is a resident in Australia at any time, is taxable in Australia and if any

foreign taxes have been paid by such person on that income, credit shall be allowed for such

taxes (Thorpe, 2012). Hence, Robyn shall have to show her salary earned while in India in the

tax return to be filed in Australia for the tax year 2016/17.

As an Australian resident, Robyn has to –

i. Declare all the income earned by her that shall include the income earned from

abroad also. This will provide a general idea of the income that is earned from

domestic and abroad.

ii. Declare if any taxes were paid by her on the foreign income earned while she served

in India. This will give a description of the income that accrued in India.

2

Answer- Part A

For the tax year 2016/17:

Robyn Rainer was a resident of Australia and was working as a lecturer at Victoria University.

During the income year 2016/17, Robyn Rainer had to shift to India as she was selected as

coordinator for business courses of Victoria University that were being conducted in Calcutta

University, India. Robyn shall be considered as resident during tax year 2016/17 as she resides in

Australia only and as per the Australian Taxation laws, any person who resides in Australia is

considered as Australian residents for tax purpose and he does not need to apply for any other

residency tests.

In the present case, as Robyn Rainer was not residing in Australia for the full year, hence the

other conditions need to be considered for assessing his residence status such as domicile test,

183-day test. In the given case, no information is given for domicile test hence we shall consider

the 183-day test. Robyn was in Australia for the period 01.07.2016 to 13.01.17 during the tax

year 2016/17 which means that she had resided in Australia for 197 days during tax year

2016/17. Seeing this condition also, Robyn shall be considered a Resident of Australia for tax

year 2016/17 (Saunders et. al, 2015).

As per the relevant provisions of the Australian Tax Laws, the income earned from working

abroad for a person who is a resident in Australia at any time, is taxable in Australia and if any

foreign taxes have been paid by such person on that income, credit shall be allowed for such

taxes (Thorpe, 2012). Hence, Robyn shall have to show her salary earned while in India in the

tax return to be filed in Australia for the tax year 2016/17.

As an Australian resident, Robyn has to –

i. Declare all the income earned by her that shall include the income earned from

abroad also. This will provide a general idea of the income that is earned from

domestic and abroad.

ii. Declare if any taxes were paid by her on the foreign income earned while she served

in India. This will give a description of the income that accrued in India.

2

Taxation

iii. Pay taxes on the assessed income in Australia. The income that accrued in Australia

needs to be assessed and hence, the payment needs to be done on that.

The foreign income is exempt in only two cases- if the person is a member of Australian Defense

or member of police force team or member of any organization which is engaged in overseas aid

work. In the given case, Robyn does not have any such designation and hence her income is

supposed to be taxable. In the cases where the assessee has earned any overseas income which

does not form part of the conditions of exempt income and taxes have been paid on such foreign

or overseas income, then such taxes are added back first to the net income in order to calculate

the assessable amount for taxation purpose (Sadiq et.al, 2014). The assessable income should

include all the income that has arisen from various activities done in various part of the world. In

short, due to professionalism whatever activity has been done will form part of the assessable

income.

The foreign income of Robyn will be included on her tax return as Assessable Foreign Income

for the tax year 2016/17. In the given case the information regarding any taxes paid by Robyn in

India is not given. Hence, we can assume that taxes were paid in India also. If this is the case,

then while calculating the taxable income of Robyn, the foreign tax paid shall be added to the

assessable foreign income of Robyn and included in her total income.

Suppose that Total Salary earned by Robyn as coordinator in India from 14.01.2017 to

30.06.2017 was $ 15,000 after tax of $ 3,000 paid by her as a foreign tax. Then while calculating

the assessable income in Australia, the taxes paid will be added back to the income and then the

tax would be calculated at the rates in Australia1. So, the total assessable foreign employment

income from salary will be $ 18,000.

As she had paid foreign tax on employment in India as per our assumption, she may be entitled

to Australian foreign income tax offset. As per the Australian tax laws, a resident of Australia

has to show all the incomes earned by him/ her which shall include both the taxable incomes and

1 Cartwright, M 2013, Death to the Australia Tax?, viewed 24 August 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

3

iii. Pay taxes on the assessed income in Australia. The income that accrued in Australia

needs to be assessed and hence, the payment needs to be done on that.

The foreign income is exempt in only two cases- if the person is a member of Australian Defense

or member of police force team or member of any organization which is engaged in overseas aid

work. In the given case, Robyn does not have any such designation and hence her income is

supposed to be taxable. In the cases where the assessee has earned any overseas income which

does not form part of the conditions of exempt income and taxes have been paid on such foreign

or overseas income, then such taxes are added back first to the net income in order to calculate

the assessable amount for taxation purpose (Sadiq et.al, 2014). The assessable income should

include all the income that has arisen from various activities done in various part of the world. In

short, due to professionalism whatever activity has been done will form part of the assessable

income.

The foreign income of Robyn will be included on her tax return as Assessable Foreign Income

for the tax year 2016/17. In the given case the information regarding any taxes paid by Robyn in

India is not given. Hence, we can assume that taxes were paid in India also. If this is the case,

then while calculating the taxable income of Robyn, the foreign tax paid shall be added to the

assessable foreign income of Robyn and included in her total income.

Suppose that Total Salary earned by Robyn as coordinator in India from 14.01.2017 to

30.06.2017 was $ 15,000 after tax of $ 3,000 paid by her as a foreign tax. Then while calculating

the assessable income in Australia, the taxes paid will be added back to the income and then the

tax would be calculated at the rates in Australia1. So, the total assessable foreign employment

income from salary will be $ 18,000.

As she had paid foreign tax on employment in India as per our assumption, she may be entitled

to Australian foreign income tax offset. As per the Australian tax laws, a resident of Australia

has to show all the incomes earned by him/ her which shall include both the taxable incomes and

1 Cartwright, M 2013, Death to the Australia Tax?, viewed 24 August 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

exempt incomes2. All the incomes have to be shown irrespective of the fact that tax on foreign

income has been paid in the country where the income has been earned. Robyn has earned

foreign employment income which is an income that is earned by Australian residents overseas

and includes salary, commission income, wages, allowances, etc. It may be paid by Australian

employer that is the Victoria University or by the overseas employer that is Calcutta University.

The incomes which shall be included in taxable income of Robyn shall be:

Salary Earned as lecturer in Victoria University

Salary Earned as Coordinator in Calcutta University (tax paid in India shall be adjusted)

Rental Income from flat rented in Melbourne

Once the overseas salary will be included in the income with the taxes added back and the other

incomes are also added, then taxes shall be calculated as per the Australian tax laws and the

foreign tax paid by Robyn shall be given credit while calculating total taxes.

For years ahead tax year 2016/17:

After tax year 2016/17, Robyn shall become a non resident of Australia as per the tax norms as

her residence in Australia shall be less than 183 days provided that she resides in India for the

whole of the tax year. In case of non-residents, the foreign incomes are not taxable at all. The

income earned overseas shall be shown in tax returns as exempt income and the taxes shall be

deducted by the overseas employer on his income earned (Renton, 2005).

Hence, Robyn shall not be taxed in Australia on salary earned in India for the tax years ahead

2016/17.

2 Patterson, D 2009, Cancellation Fees - The ATO Rulings, viewed 24 August 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2009,_Sound_Education_in_GST,_Cancellation_Fees___The_ATO_Rulings.html

4

exempt incomes2. All the incomes have to be shown irrespective of the fact that tax on foreign

income has been paid in the country where the income has been earned. Robyn has earned

foreign employment income which is an income that is earned by Australian residents overseas

and includes salary, commission income, wages, allowances, etc. It may be paid by Australian

employer that is the Victoria University or by the overseas employer that is Calcutta University.

The incomes which shall be included in taxable income of Robyn shall be:

Salary Earned as lecturer in Victoria University

Salary Earned as Coordinator in Calcutta University (tax paid in India shall be adjusted)

Rental Income from flat rented in Melbourne

Once the overseas salary will be included in the income with the taxes added back and the other

incomes are also added, then taxes shall be calculated as per the Australian tax laws and the

foreign tax paid by Robyn shall be given credit while calculating total taxes.

For years ahead tax year 2016/17:

After tax year 2016/17, Robyn shall become a non resident of Australia as per the tax norms as

her residence in Australia shall be less than 183 days provided that she resides in India for the

whole of the tax year. In case of non-residents, the foreign incomes are not taxable at all. The

income earned overseas shall be shown in tax returns as exempt income and the taxes shall be

deducted by the overseas employer on his income earned (Renton, 2005).

Hence, Robyn shall not be taxed in Australia on salary earned in India for the tax years ahead

2016/17.

2 Patterson, D 2009, Cancellation Fees - The ATO Rulings, viewed 24 August 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2009,_Sound_Education_in_GST,_Cancellation_Fees___The_ATO_Rulings.html

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Answer -Part B

Paul runs his business as a golf trainer. He has a source of income in two ways, both by teaching

his clients on how to play golf. He uses to charge as one-time lesson fees or 12 months lessons

fees which were charged in advance that is clients needed to pay entire fees money in one go.

Paul had an arrangement with Eastwood Golf Club to conduct lessons to their club members who

were willing to take occasional classes or they were one time visitors3. Paul had his own clients

also which would pay him occasionally or for 12 weeks advance fees. His financial year used to

start from March to February at a break of every three months that means there shall be total four

batches of three months each. Paul used to refund any sum of money received by his client in

case any of his clients could not attend any of his classes. In case any of students could not attend

any class, Paul uses to refund the fees.

Money received on 30 June 17 by Paul for his professional work:

Particulars Amount

One time lesson: 6000 $

12-week lesson: 28800 $

Total 34800 $

Hence it can be seen that at 30th June 2017, the total earnings made by Paul have been $ 34800

out of which $ 28,800 received on account of 12-week lessons pertains to 4 months which has

been recalculated for 12 months. Private lessons have not been regrouped/ recalculated because it

cannot be ascertained whether private lessons were continued or not. The answer shall be

3 DFRWS 2017, Termination Fees, viewed 24 August 2017,

http://dor.wa.gov/Content/GetAFormOrPublication/PublicationBySubject/TaxTopics/

TerminationFees.aspx

5

Answer -Part B

Paul runs his business as a golf trainer. He has a source of income in two ways, both by teaching

his clients on how to play golf. He uses to charge as one-time lesson fees or 12 months lessons

fees which were charged in advance that is clients needed to pay entire fees money in one go.

Paul had an arrangement with Eastwood Golf Club to conduct lessons to their club members who

were willing to take occasional classes or they were one time visitors3. Paul had his own clients

also which would pay him occasionally or for 12 weeks advance fees. His financial year used to

start from March to February at a break of every three months that means there shall be total four

batches of three months each. Paul used to refund any sum of money received by his client in

case any of his clients could not attend any of his classes. In case any of students could not attend

any class, Paul uses to refund the fees.

Money received on 30 June 17 by Paul for his professional work:

Particulars Amount

One time lesson: 6000 $

12-week lesson: 28800 $

Total 34800 $

Hence it can be seen that at 30th June 2017, the total earnings made by Paul have been $ 34800

out of which $ 28,800 received on account of 12-week lessons pertains to 4 months which has

been recalculated for 12 months. Private lessons have not been regrouped/ recalculated because it

cannot be ascertained whether private lessons were continued or not. The answer shall be

3 DFRWS 2017, Termination Fees, viewed 24 August 2017,

http://dor.wa.gov/Content/GetAFormOrPublication/PublicationBySubject/TaxTopics/

TerminationFees.aspx

5

Taxation

different in case of earnings out of private lessons are to be recalculated4. We have taken the

assumptions that the students in a group were restricted to 20 in number and they were charges $

40 per lesson.

We have taken few assumptions also for calculation purposes. Here in this question, we have

assumed that Paul Income for 12-week lessons is evenly distributed in the entire year that is

where 28800 $ is received for 4 months, i.e. 28800/ 4 = 7200 $ per month. His total 12 months

fees shall be 7200$ * 12 months that is 86400 $. So, the total earnings out of 12-week lessons are

86400 $ for the entire year 2016/17 as per our calculation showed above.

In February 2017, Paul accidentally damaged one of the client’s buggies. Paul agreed to repair

the buggy by using fees money received by 2 clients for repair of the buggy. Paul uses to restrict

the number of students to 20 students for 12-month lessons. This means money equal to 2

student’s fees shall be used by Paul to repair the buggy.

Total Fees received in 12-week lessons: 86400 $

Total Number of students: 20

Two students fees= 86400/ 20* 2

= 8640$

During the year there was another transaction which happened in which Paul received a sum of

money which did not pertain directly to his professional work. However, this transaction could

be indirectly related to his professional work. One of the students of Paul named Doreen had

won a golf tournament (Kobestky, 2005). Doreen gave 10000$ to Paul as a token of appreciation

towards Paul because of Paul teachings only, Doreen could only win the golf tournament. It is to

4 Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 24 August 2017,

www.zdnet.com.au.

6

different in case of earnings out of private lessons are to be recalculated4. We have taken the

assumptions that the students in a group were restricted to 20 in number and they were charges $

40 per lesson.

We have taken few assumptions also for calculation purposes. Here in this question, we have

assumed that Paul Income for 12-week lessons is evenly distributed in the entire year that is

where 28800 $ is received for 4 months, i.e. 28800/ 4 = 7200 $ per month. His total 12 months

fees shall be 7200$ * 12 months that is 86400 $. So, the total earnings out of 12-week lessons are

86400 $ for the entire year 2016/17 as per our calculation showed above.

In February 2017, Paul accidentally damaged one of the client’s buggies. Paul agreed to repair

the buggy by using fees money received by 2 clients for repair of the buggy. Paul uses to restrict

the number of students to 20 students for 12-month lessons. This means money equal to 2

student’s fees shall be used by Paul to repair the buggy.

Total Fees received in 12-week lessons: 86400 $

Total Number of students: 20

Two students fees= 86400/ 20* 2

= 8640$

During the year there was another transaction which happened in which Paul received a sum of

money which did not pertain directly to his professional work. However, this transaction could

be indirectly related to his professional work. One of the students of Paul named Doreen had

won a golf tournament (Kobestky, 2005). Doreen gave 10000$ to Paul as a token of appreciation

towards Paul because of Paul teachings only, Doreen could only win the golf tournament. It is to

4 Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 24 August 2017,

www.zdnet.com.au.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

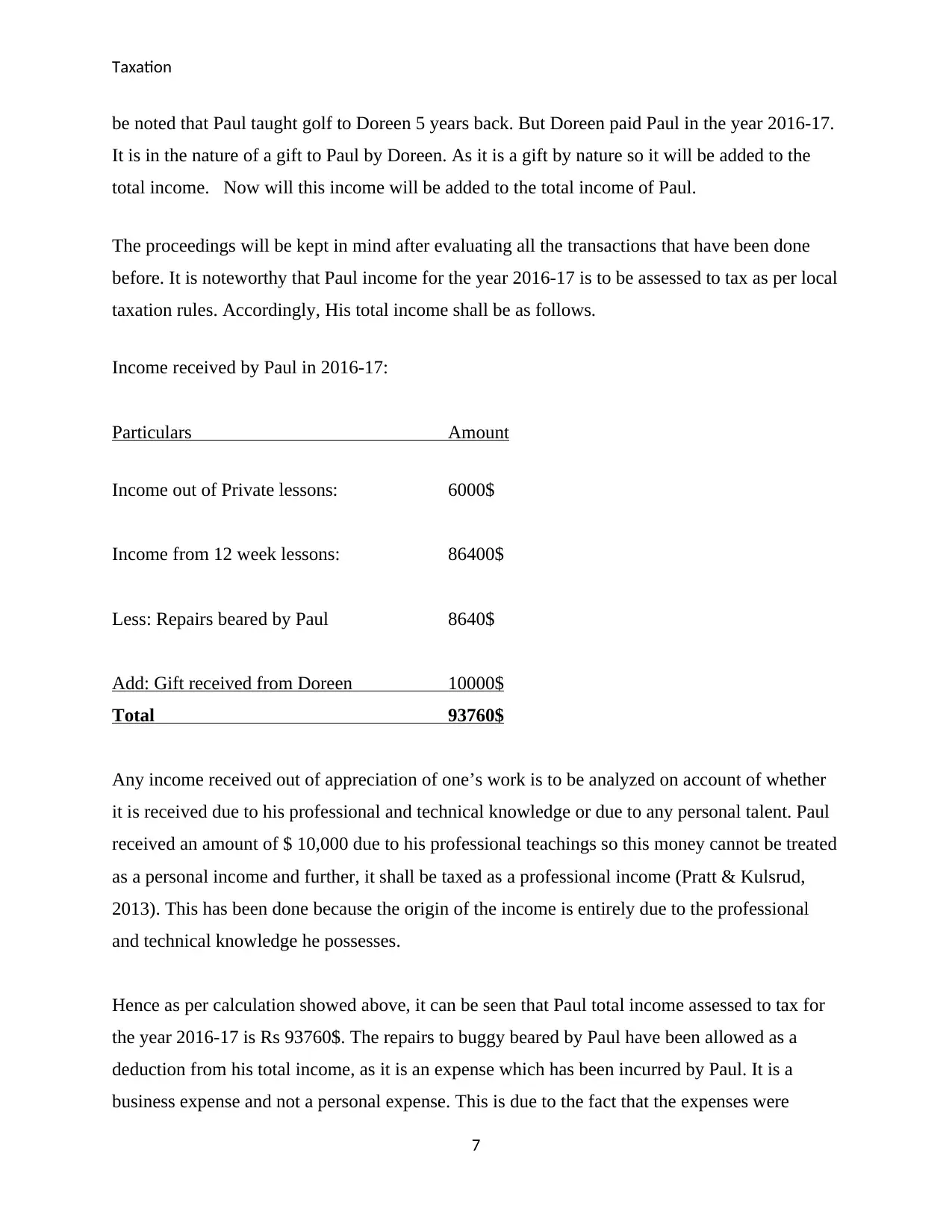

be noted that Paul taught golf to Doreen 5 years back. But Doreen paid Paul in the year 2016-17.

It is in the nature of a gift to Paul by Doreen. As it is a gift by nature so it will be added to the

total income. Now will this income will be added to the total income of Paul.

The proceedings will be kept in mind after evaluating all the transactions that have been done

before. It is noteworthy that Paul income for the year 2016-17 is to be assessed to tax as per local

taxation rules. Accordingly, His total income shall be as follows.

Income received by Paul in 2016-17:

Particulars Amount

Income out of Private lessons: 6000$

Income from 12 week lessons: 86400$

Less: Repairs beared by Paul 8640$

Add: Gift received from Doreen 10000$

Total 93760$

Any income received out of appreciation of one’s work is to be analyzed on account of whether

it is received due to his professional and technical knowledge or due to any personal talent. Paul

received an amount of $ 10,000 due to his professional teachings so this money cannot be treated

as a personal income and further, it shall be taxed as a professional income (Pratt & Kulsrud,

2013). This has been done because the origin of the income is entirely due to the professional

and technical knowledge he possesses.

Hence as per calculation showed above, it can be seen that Paul total income assessed to tax for

the year 2016-17 is Rs 93760$. The repairs to buggy beared by Paul have been allowed as a

deduction from his total income, as it is an expense which has been incurred by Paul. It is a

business expense and not a personal expense. This is due to the fact that the expenses were

7

be noted that Paul taught golf to Doreen 5 years back. But Doreen paid Paul in the year 2016-17.

It is in the nature of a gift to Paul by Doreen. As it is a gift by nature so it will be added to the

total income. Now will this income will be added to the total income of Paul.

The proceedings will be kept in mind after evaluating all the transactions that have been done

before. It is noteworthy that Paul income for the year 2016-17 is to be assessed to tax as per local

taxation rules. Accordingly, His total income shall be as follows.

Income received by Paul in 2016-17:

Particulars Amount

Income out of Private lessons: 6000$

Income from 12 week lessons: 86400$

Less: Repairs beared by Paul 8640$

Add: Gift received from Doreen 10000$

Total 93760$

Any income received out of appreciation of one’s work is to be analyzed on account of whether

it is received due to his professional and technical knowledge or due to any personal talent. Paul

received an amount of $ 10,000 due to his professional teachings so this money cannot be treated

as a personal income and further, it shall be taxed as a professional income (Pratt & Kulsrud,

2013). This has been done because the origin of the income is entirely due to the professional

and technical knowledge he possesses.

Hence as per calculation showed above, it can be seen that Paul total income assessed to tax for

the year 2016-17 is Rs 93760$. The repairs to buggy beared by Paul have been allowed as a

deduction from his total income, as it is an expense which has been incurred by Paul. It is a

business expense and not a personal expense. This is due to the fact that the expenses were

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

incurred during the process of business and not as a personal one. It has been deducted from the

total income earned by Paul (Nethercott et. al, 2013). Secondly, Paul has further received an

amount in nature of gift by one of his student whom he used to teach 5 years back. The amount

of 10000$ has been received as a gift but in fact, it is a receipt due to professional teachings only.

Hence it can’t be argued that it is in purely gift nature.

In absence of any tax rate, tax amount cannot be ascertained however total taxable income for

the year 2016/17 has been calculated above.

8

incurred during the process of business and not as a personal one. It has been deducted from the

total income earned by Paul (Nethercott et. al, 2013). Secondly, Paul has further received an

amount in nature of gift by one of his student whom he used to teach 5 years back. The amount

of 10000$ has been received as a gift but in fact, it is a receipt due to professional teachings only.

Hence it can’t be argued that it is in purely gift nature.

In absence of any tax rate, tax amount cannot be ascertained however total taxable income for

the year 2016/17 has been calculated above.

8

Taxation

Bibliography

Cartwright, M 2013, Death to the Australia Tax?, viewed 24 August 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

DFRWS 2017, Termination Fees, viewed 24 August 2017,

http://dor.wa.gov/Content/GetAFormOrPublication/PublicationBySubject/TaxTopics/

TerminationFees.aspx

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 24 August 2017,

www.zdnet.com.au.

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Patterson, D 2009, Cancellation Fees - The ATO Rulings, viewed 24 August 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2009,_Sound_Education_in_GST,_Cancellation_Fees___The_ATO_Rulings.html

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C, Hanegbi, R., Jogarajan,S, Krever, R.,Obst, W.,& Ting, A 2014,

Principles of Taxation Law, Sydney.

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Thorpe, C 2012, Tax Pack dumped online returns encouraged ABC News, viewed 24 August

2017 http://www.abc.net.au/news/2012-07-09/tax-pack-dumped-online-returns-encouraged/

4117784

9

Bibliography

Cartwright, M 2013, Death to the Australia Tax?, viewed 24 August 2017,

https://www.ato.gov.au/Individuals/Deceased-estates/Being-an-executor/Tax-responsibilities

DFRWS 2017, Termination Fees, viewed 24 August 2017,

http://dor.wa.gov/Content/GetAFormOrPublication/PublicationBySubject/TaxTopics/

TerminationFees.aspx

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 24 August 2017,

www.zdnet.com.au.

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Patterson, D 2009, Cancellation Fees - The ATO Rulings, viewed 24 August 2017

http://www.tved.net.au/index.cfm?SimpleDisplay=PaperDisplay.cfm&PaperDisplay=http://

www.tved.net.au/PublicPapers/

June_2009,_Sound_Education_in_GST,_Cancellation_Fees___The_ATO_Rulings.html

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C, Hanegbi, R., Jogarajan,S, Krever, R.,Obst, W.,& Ting, A 2014,

Principles of Taxation Law, Sydney.

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Thorpe, C 2012, Tax Pack dumped online returns encouraged ABC News, viewed 24 August

2017 http://www.abc.net.au/news/2012-07-09/tax-pack-dumped-online-returns-encouraged/

4117784

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.