LAWS20060: Taxation Law of Australia Individual Assignment Analysis

VerifiedAdded on 2022/12/26

|16

|3895

|77

Homework Assignment

AI Summary

This document presents a comprehensive solution to an Australian Taxation Law assignment, addressing various aspects of the Australian tax system. The solution includes detailed answers to questions covering topics such as the interpretation of small business entity definitions, deductibility of gifts, the application of capital gains tax (CGT) to personal assets, and the determination of assessable income. It also provides analysis of relevant case law, including Hayes v FCT and FCT v Jenkins, to illustrate key legal principles. Furthermore, the assignment explores the nuances of residency, differentiating between 'usual place of abode' and 'permanent place of abode'. It also examines specific tax deductions, such as those related to self-education expenses, travel, and work-related clothing, providing clear explanations of what is and isn't deductible according to the relevant legislation. The solution utilizes the Australian Guide to Legal Citation (AGLC) referencing method, citing relevant legislation, cases, and tax rulings to support the arguments. The assignment addresses the Medicare Levy and Medicare Levy Surcharge, and their implications. The document serves as a valuable resource for students studying Australian taxation law, offering in-depth analysis and practical application of legal principles.

Running head: TAXATION LAW OF AUSTRALIA

Taxation Law of Australia

Name of the Student

Name of the University

Author Note

Taxation Law of Australia

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1Taxation Law of Australia

Table of Contents

Answer to Question: 1................................................................................................................3

Answer (a)..............................................................................................................................3

Answer (b)..............................................................................................................................3

Answer (c)..............................................................................................................................3

Answer (d)..............................................................................................................................3

Answer (e)..............................................................................................................................3

Answer (f)..............................................................................................................................3

Answer (g)..............................................................................................................................4

Answer (h)..............................................................................................................................4

Answer (i)...............................................................................................................................5

Medicare Levy...........................................................................................................................5

Medicare Levy Surcharge..........................................................................................................5

Answer to Question: 2................................................................................................................5

Answer to Question: 3................................................................................................................7

Answer to Question: 4..............................................................................................................10

Answer (a)............................................................................................................................10

Answer (b)............................................................................................................................11

Answer (c)............................................................................................................................11

Answer (d)............................................................................................................................12

Answer to Question: 5..............................................................................................................12

Answer (a)............................................................................................................................12

Table of Contents

Answer to Question: 1................................................................................................................3

Answer (a)..............................................................................................................................3

Answer (b)..............................................................................................................................3

Answer (c)..............................................................................................................................3

Answer (d)..............................................................................................................................3

Answer (e)..............................................................................................................................3

Answer (f)..............................................................................................................................3

Answer (g)..............................................................................................................................4

Answer (h)..............................................................................................................................4

Answer (i)...............................................................................................................................5

Medicare Levy...........................................................................................................................5

Medicare Levy Surcharge..........................................................................................................5

Answer to Question: 2................................................................................................................5

Answer to Question: 3................................................................................................................7

Answer to Question: 4..............................................................................................................10

Answer (a)............................................................................................................................10

Answer (b)............................................................................................................................11

Answer (c)............................................................................................................................11

Answer (d)............................................................................................................................12

Answer to Question: 5..............................................................................................................12

Answer (a)............................................................................................................................12

2Taxation Law of Australia

Answer (b)............................................................................................................................13

Answer (c)............................................................................................................................13

Answer (d)............................................................................................................................14

Answer (e)............................................................................................................................14

References................................................................................................................................15

Answer (b)............................................................................................................................13

Answer (c)............................................................................................................................13

Answer (d)............................................................................................................................14

Answer (e)............................................................................................................................14

References................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3Taxation Law of Australia

Answer to Question: 1

Answer (a)

The “taxation ruling of TR 2019/1” covers the commissioner view considering an

organization when it perform its business operation under “sec-23, ITRA 1986”- the

definition mentioned in respect of small business entity. It has applicable from the income

year 2015-16 and 2016-17 “sec-328-110, ITAA 1997”1.

Answer (b)

“Division 30 of the ITAA 1997” of the Income Tax Assessment Act, 1997 outlines

the legislation regarding deductibility of gifts or contributions for the taxpayers2.

Answer (c)

The tax rate of 45% is applicable to a resident taxpayer in the current tax year.

Answer (d)

The taxpayers use a car or motorcycle for their personal purpose. Therefore, it

consider as an asset for personal use and comes under “sec-108-20, ITAA 1997”. Hence, not

exempted from capital gains tax.

Answer (e)

“Subsection 104-20 (1), ITAA 1997” includes the CGT event C1, that takes place

when an individual has somehow lost or destroyed the CGT Asset. It commences on the time

when that individual reimbursed for the destruction or that loss or if he/she do not receive any

reimbursement or compensation for the discovered loss.

Answer (f)

The current tax-free threshold for a resident individual of Australia is $18,200.

1 Hopkins, Bruce R. The Law of Tax-Exempt Organizations. 11th ed., 2016.

2 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

Answer to Question: 1

Answer (a)

The “taxation ruling of TR 2019/1” covers the commissioner view considering an

organization when it perform its business operation under “sec-23, ITRA 1986”- the

definition mentioned in respect of small business entity. It has applicable from the income

year 2015-16 and 2016-17 “sec-328-110, ITAA 1997”1.

Answer (b)

“Division 30 of the ITAA 1997” of the Income Tax Assessment Act, 1997 outlines

the legislation regarding deductibility of gifts or contributions for the taxpayers2.

Answer (c)

The tax rate of 45% is applicable to a resident taxpayer in the current tax year.

Answer (d)

The taxpayers use a car or motorcycle for their personal purpose. Therefore, it

consider as an asset for personal use and comes under “sec-108-20, ITAA 1997”. Hence, not

exempted from capital gains tax.

Answer (e)

“Subsection 104-20 (1), ITAA 1997” includes the CGT event C1, that takes place

when an individual has somehow lost or destroyed the CGT Asset. It commences on the time

when that individual reimbursed for the destruction or that loss or if he/she do not receive any

reimbursement or compensation for the discovered loss.

Answer (f)

The current tax-free threshold for a resident individual of Australia is $18,200.

1 Hopkins, Bruce R. The Law of Tax-Exempt Organizations. 11th ed., 2016.

2 Bankman, Joseph, et al. Federal Income Taxation. Aspen Publishers, 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4Taxation Law of Australia

Answer (g)

The High Court decision in the case, Hayes v FCT (1956) 96 CLR 47 states that the

employer who has consider as well founder of the company has given a considerable amount

of gift by allotting shares in a public company3. On the casual basis, the accountant has

provided unpaid services to the employer and some other small-unpaid services has rendered.

The federal court made a judgment by announcing that the gift do not comes under income,

as it is not generating any revenue and the parties has shown its existence of friendship

amongst their families so, it has consider as the occasion of gift. The case is noteworthy as

the intention of the donor is barely decisive.

Answer (h)

Ordinary Income Statutory Income

As the Act does not mentioned any

definition, through the case law it

has found that the Ordinary income

occurs from the decision that is

dependent on the required principles.

Ordinary income is treated as

assessable income for the taxpayer

that comes under “section 6-5,

ITAA 1997”.

Statutory income is reflected as a

computable income as required

activities of certain regulations has

mentioned under the act

Statutory income is reflected prior to

ordinary income’s application. The

amount assessed under the provision

of “section 6-25 (2)”.

3 Leighton-Daly, Mathew. "Wickenby-related tax crime prosecutions." Taxation in Australia 52.7 (2018): 380.

Answer (g)

The High Court decision in the case, Hayes v FCT (1956) 96 CLR 47 states that the

employer who has consider as well founder of the company has given a considerable amount

of gift by allotting shares in a public company3. On the casual basis, the accountant has

provided unpaid services to the employer and some other small-unpaid services has rendered.

The federal court made a judgment by announcing that the gift do not comes under income,

as it is not generating any revenue and the parties has shown its existence of friendship

amongst their families so, it has consider as the occasion of gift. The case is noteworthy as

the intention of the donor is barely decisive.

Answer (h)

Ordinary Income Statutory Income

As the Act does not mentioned any

definition, through the case law it

has found that the Ordinary income

occurs from the decision that is

dependent on the required principles.

Ordinary income is treated as

assessable income for the taxpayer

that comes under “section 6-5,

ITAA 1997”.

Statutory income is reflected as a

computable income as required

activities of certain regulations has

mentioned under the act

Statutory income is reflected prior to

ordinary income’s application. The

amount assessed under the provision

of “section 6-25 (2)”.

3 Leighton-Daly, Mathew. "Wickenby-related tax crime prosecutions." Taxation in Australia 52.7 (2018): 380.

5Taxation Law of Australia

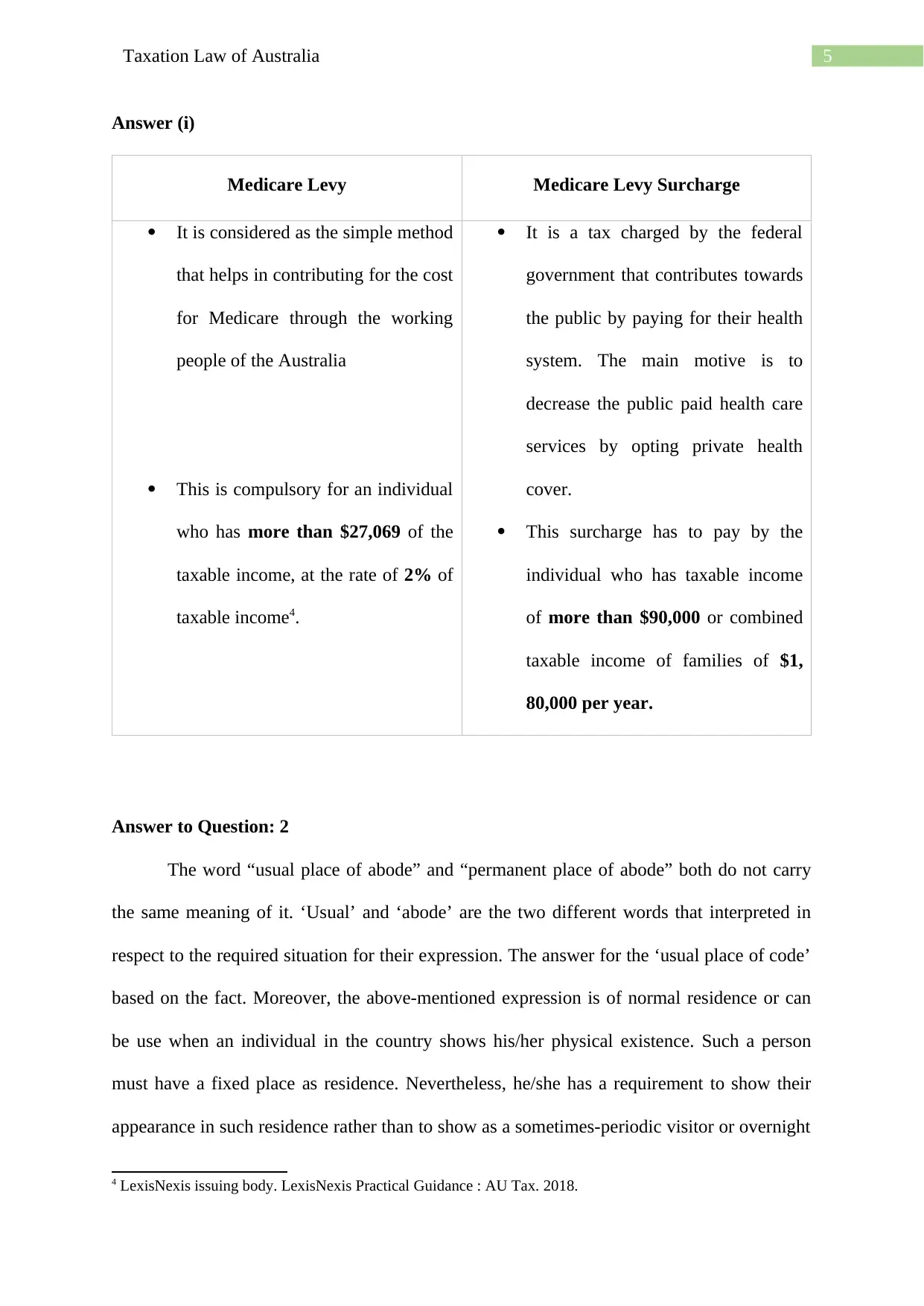

Answer (i)

Medicare Levy Medicare Levy Surcharge

It is considered as the simple method

that helps in contributing for the cost

for Medicare through the working

people of the Australia

This is compulsory for an individual

who has more than $27,069 of the

taxable income, at the rate of 2% of

taxable income4.

It is a tax charged by the federal

government that contributes towards

the public by paying for their health

system. The main motive is to

decrease the public paid health care

services by opting private health

cover.

This surcharge has to pay by the

individual who has taxable income

of more than $90,000 or combined

taxable income of families of $1,

80,000 per year.

Answer to Question: 2

The word “usual place of abode” and “permanent place of abode” both do not carry

the same meaning of it. ‘Usual’ and ‘abode’ are the two different words that interpreted in

respect to the required situation for their expression. The answer for the ‘usual place of code’

based on the fact. Moreover, the above-mentioned expression is of normal residence or can

be use when an individual in the country shows his/her physical existence. Such a person

must have a fixed place as residence. Nevertheless, he/she has a requirement to show their

appearance in such residence rather than to show as a sometimes-periodic visitor or overnight

4 LexisNexis issuing body. LexisNexis Practical Guidance : AU Tax. 2018.

Answer (i)

Medicare Levy Medicare Levy Surcharge

It is considered as the simple method

that helps in contributing for the cost

for Medicare through the working

people of the Australia

This is compulsory for an individual

who has more than $27,069 of the

taxable income, at the rate of 2% of

taxable income4.

It is a tax charged by the federal

government that contributes towards

the public by paying for their health

system. The main motive is to

decrease the public paid health care

services by opting private health

cover.

This surcharge has to pay by the

individual who has taxable income

of more than $90,000 or combined

taxable income of families of $1,

80,000 per year.

Answer to Question: 2

The word “usual place of abode” and “permanent place of abode” both do not carry

the same meaning of it. ‘Usual’ and ‘abode’ are the two different words that interpreted in

respect to the required situation for their expression. The answer for the ‘usual place of code’

based on the fact. Moreover, the above-mentioned expression is of normal residence or can

be use when an individual in the country shows his/her physical existence. Such a person

must have a fixed place as residence. Nevertheless, he/she has a requirement to show their

appearance in such residence rather than to show as a sometimes-periodic visitor or overnight

4 LexisNexis issuing body. LexisNexis Practical Guidance : AU Tax. 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6Taxation Law of Australia

stay or weekly visitor to their accommodation. This states a fixed accommodation in a fixed

place of staying rather than a taxpayer who has been a tenant or the person in Australia,

having their “usual place of abode”.

The place that would considered as short-lived or as temporary in nature- if a person

comes under the sight that he/she has ‘usual place of abode’ and demonstrate that the person

does not have any fixed place or usual place of abode outside the country. However, that

person is moving on a regular basis from one place to another or place themselves from one

state to different state in or within the country and shows any special context of relation to the

place in foreign nation. An individual with his/her own choice considered as accepted some

other place as residence or “permanent place of abode” outside of Australia5.

In the interim, the word “permanent place of abode” indicates that the taxpayer has its

residence in Australia. The meaning of term resident mentioned under “subparagraph (a)

(i)” reflects that the commissioner believes in the ‘permanent place of abode’ of a person is

not outside Australia. The ‘place of abode’ means that the person is staying with their family

in the night. According to the “Levene v IRC (1928)” - “place of abode” refers to the

residence or the surrounding where a person physically exists6.

According to “FCT v Applegate (1979)”- the law court, it has explained that if a

person has gone to New Hebrides in Villa so that he can settle down his office for his

company then also that taxpayer has residence of Australia. In the judgment made by full

Federal court noticed that the taxpayer has ‘permanent place of abode’ out of Australia. The

taxpayer has to consider as a non-resident for that particular income year7.

5 Schurgott, Ken. “Practical Issues with Trusts: Important Updates.” Tax Specialist, vol. 20, no. 1, 2016, pp. 2–

9.

6 Kamdar, Mahomed. "South Africans working abroad: the current dilemma and the tax implications." Tax

Professional2019.34 (2019): 9-11.

7 Idris, Nuhu Musa. "Some comparisons between the Nigerian and South African fiscal regimes regarding an

individual’s tax residence." Obiter 39.1 (2018): 76-84.

stay or weekly visitor to their accommodation. This states a fixed accommodation in a fixed

place of staying rather than a taxpayer who has been a tenant or the person in Australia,

having their “usual place of abode”.

The place that would considered as short-lived or as temporary in nature- if a person

comes under the sight that he/she has ‘usual place of abode’ and demonstrate that the person

does not have any fixed place or usual place of abode outside the country. However, that

person is moving on a regular basis from one place to another or place themselves from one

state to different state in or within the country and shows any special context of relation to the

place in foreign nation. An individual with his/her own choice considered as accepted some

other place as residence or “permanent place of abode” outside of Australia5.

In the interim, the word “permanent place of abode” indicates that the taxpayer has its

residence in Australia. The meaning of term resident mentioned under “subparagraph (a)

(i)” reflects that the commissioner believes in the ‘permanent place of abode’ of a person is

not outside Australia. The ‘place of abode’ means that the person is staying with their family

in the night. According to the “Levene v IRC (1928)” - “place of abode” refers to the

residence or the surrounding where a person physically exists6.

According to “FCT v Applegate (1979)”- the law court, it has explained that if a

person has gone to New Hebrides in Villa so that he can settle down his office for his

company then also that taxpayer has residence of Australia. In the judgment made by full

Federal court noticed that the taxpayer has ‘permanent place of abode’ out of Australia. The

taxpayer has to consider as a non-resident for that particular income year7.

5 Schurgott, Ken. “Practical Issues with Trusts: Important Updates.” Tax Specialist, vol. 20, no. 1, 2016, pp. 2–

9.

6 Kamdar, Mahomed. "South Africans working abroad: the current dilemma and the tax implications." Tax

Professional2019.34 (2019): 9-11.

7 Idris, Nuhu Musa. "Some comparisons between the Nigerian and South African fiscal regimes regarding an

individual’s tax residence." Obiter 39.1 (2018): 76-84.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7Taxation Law of Australia

One of the prominent case of “FCT v Jenkins (1982)” refers- if a taxpayer is

working as an employee as a bank officer and shifted to New Hebrides for three years and in

the due course get returned following stay of 18 months and reflected a poor condition of

health. The Supreme Court of Queensland declare a decision that the taxpayer through the

time span of residing outside of Australia, though in that time span the taxpayer has not

create any material purpose of residing overseas for an unknown period.

“Section 6 (1), ITAA 1936”- to determine an individual’s residency status

Commonwealth public service superannuation funds test is made. According to this, the

member of the commonwealth public service together with their family treated as the tax

resident of Australia. Commonwealth public service superannuation funds test is objective

based test8.

As an evidence from the case laws as well as legislation discussed above, an

individual not to state their ‘usual place of abode’ is outside of Australia. In the time being,

first legislative test that is required to a person to satisfy their ‘permanent place of abode’

outside Australia.

Answer to Question: 3

(a) HECS-HELP- $850:

The question reflects the need of the expenses made for self-education where an

employee working is contributed as a taxpayer to receive an education from a particular

school or college or any other source of study. It is necessary to understand that the course

must be for improving the skills and knowledge supporting to the current work activities. So

in that case get a self-deduction expense. Further, the ATO declared that taxpayer individual

8 Siebert, Horst. Reforming capital income taxation. Routledge, 2019.

One of the prominent case of “FCT v Jenkins (1982)” refers- if a taxpayer is

working as an employee as a bank officer and shifted to New Hebrides for three years and in

the due course get returned following stay of 18 months and reflected a poor condition of

health. The Supreme Court of Queensland declare a decision that the taxpayer through the

time span of residing outside of Australia, though in that time span the taxpayer has not

create any material purpose of residing overseas for an unknown period.

“Section 6 (1), ITAA 1936”- to determine an individual’s residency status

Commonwealth public service superannuation funds test is made. According to this, the

member of the commonwealth public service together with their family treated as the tax

resident of Australia. Commonwealth public service superannuation funds test is objective

based test8.

As an evidence from the case laws as well as legislation discussed above, an

individual not to state their ‘usual place of abode’ is outside of Australia. In the time being,

first legislative test that is required to a person to satisfy their ‘permanent place of abode’

outside Australia.

Answer to Question: 3

(a) HECS-HELP- $850:

The question reflects the need of the expenses made for self-education where an

employee working is contributed as a taxpayer to receive an education from a particular

school or college or any other source of study. It is necessary to understand that the course

must be for improving the skills and knowledge supporting to the current work activities. So

in that case get a self-deduction expense. Further, the ATO declared that taxpayer individual

8 Siebert, Horst. Reforming capital income taxation. Routledge, 2019.

8Taxation Law of Australia

is not permitted to claim the deduction. Because, the contribution is made to the Australian

Government in respect to HECS-HELP.

In the given situation in the question, it has found that the accountant has made an

expense of $850 in the contribution that made to help HECS-HELP. Thus, the trainee

accountant is not permitted to claim the deduction for this contribution to the Australian

Government HECS- HELP.

(b) Travel-work to University- $110:

The ATO has made clear that an individual or a tax payer who is availing self-education

from some other place then he/she is eligible to income tax deduction for the cost incurred

while travelling from the place of study to the taxpayer’s home. It has stated under

legislation “section 8-1, ITAA 1997” a deduction can be claim by an individual who is

travelling to study place to home. In this view, the trainee accountant is eligible for the

deduction as it is related to the expense made in the respect of current work and travelling is

through the University to home.

(c) Books- $200:

Under “Section 8-1, ITAA 1997” it has stated that if an employee during their job made

any self-education expense in terms of increasing their knowledge or enhancing their skills

for the current work doing by them , in that case the person is eligible to get general

deduction. Judgment of the court in “FCT v Highfield (1982)” ATC 4463- The taxpayer got

deduction for the paid fees, travel cost and accommodation for pursuing Master of Science on

Periodontics. The reason is the expenses made in pursuing a course for the degree would

enhance the knowledge and increase the efficiency of the practice of the taxpayer.

is not permitted to claim the deduction. Because, the contribution is made to the Australian

Government in respect to HECS-HELP.

In the given situation in the question, it has found that the accountant has made an

expense of $850 in the contribution that made to help HECS-HELP. Thus, the trainee

accountant is not permitted to claim the deduction for this contribution to the Australian

Government HECS- HELP.

(b) Travel-work to University- $110:

The ATO has made clear that an individual or a tax payer who is availing self-education

from some other place then he/she is eligible to income tax deduction for the cost incurred

while travelling from the place of study to the taxpayer’s home. It has stated under

legislation “section 8-1, ITAA 1997” a deduction can be claim by an individual who is

travelling to study place to home. In this view, the trainee accountant is eligible for the

deduction as it is related to the expense made in the respect of current work and travelling is

through the University to home.

(c) Books- $200:

Under “Section 8-1, ITAA 1997” it has stated that if an employee during their job made

any self-education expense in terms of increasing their knowledge or enhancing their skills

for the current work doing by them , in that case the person is eligible to get general

deduction. Judgment of the court in “FCT v Highfield (1982)” ATC 4463- The taxpayer got

deduction for the paid fees, travel cost and accommodation for pursuing Master of Science on

Periodontics. The reason is the expenses made in pursuing a course for the degree would

enhance the knowledge and increase the efficiency of the practice of the taxpayer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9Taxation Law of Australia

In this view, the deduction would be allowed under “section 8-1, ITAA 1997” for the

expenses made of $200 for books while undertaking a degree that would enhance the

knowledge and the skills of the person.

(d) Childcare during her evening classes- $250:

Any domestic loss and the private type expense made is not eligible for deduction as it

has not met any positive limb and hence this is not deductible under negative limb of “S8-1

(2) (b), ITAA 1997”. In “Lodge v FCT (1972)”. The deductions were not allowed to the

clerk for the child mind during attending her work. The expenses seems not relevant to the

group of taxpayer earning that is taxable9.

The childcare expense of $80 has made to attend an evening class refer to an expense

related to domestic or private type. The “Lodge v FCT (1972)” stated that the sum of $80 is

non-deductible under “S8-1 (2) (b), ITAA 1997” second negative limb, as it is not meeting

positive limbs.

(e) Repair to her fridge at home- $250:

According to “sec25-10, ITAA 1997” the taxpayer is liable to claim deduction for the

expenses made on the premise repairing or to depreciating asset that is for generating income

assessable to it. As the taxpayer has made expenses of $250 on repairing fridge for home. The

amount of $250 will be consider as non-deductible under “sec25-10, ITAA 1997” as it is for

private purpose.

(f) Black trousers and shirt required to be worn at the office- $145:

9 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make compensating adjustments for

income tax and GST in Australia and New Zealand." Australian Tax Forum. Vol. 33. No. 3. 2018.

In this view, the deduction would be allowed under “section 8-1, ITAA 1997” for the

expenses made of $200 for books while undertaking a degree that would enhance the

knowledge and the skills of the person.

(d) Childcare during her evening classes- $250:

Any domestic loss and the private type expense made is not eligible for deduction as it

has not met any positive limb and hence this is not deductible under negative limb of “S8-1

(2) (b), ITAA 1997”. In “Lodge v FCT (1972)”. The deductions were not allowed to the

clerk for the child mind during attending her work. The expenses seems not relevant to the

group of taxpayer earning that is taxable9.

The childcare expense of $80 has made to attend an evening class refer to an expense

related to domestic or private type. The “Lodge v FCT (1972)” stated that the sum of $80 is

non-deductible under “S8-1 (2) (b), ITAA 1997” second negative limb, as it is not meeting

positive limbs.

(e) Repair to her fridge at home- $250:

According to “sec25-10, ITAA 1997” the taxpayer is liable to claim deduction for the

expenses made on the premise repairing or to depreciating asset that is for generating income

assessable to it. As the taxpayer has made expenses of $250 on repairing fridge for home. The

amount of $250 will be consider as non-deductible under “sec25-10, ITAA 1997” as it is for

private purpose.

(f) Black trousers and shirt required to be worn at the office- $145:

9 Datt, Kalmen H., and Mark Keating. "The Commissioner’s obligation to make compensating adjustments for

income tax and GST in Australia and New Zealand." Australian Tax Forum. Vol. 33. No. 3. 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10Taxation Law of Australia

According to “section 8-1, ITAA 1997”, the expenses that has made on the clothing will

not be consider for deduction. In case, “Mansfield v FCT (1996)” expenses made on the

ordinary article related to apparel has not allowed for tax deduction.

The expenses made for shirts and black trousers of $145 is for work at office that is an

ordinary article for apparel. Referring the above case the amount of $145 is non-deductible.

(g) Legal expenses incurred in writing up a new employment contract with a new

employer- $300:

According to “section 8-1, ITAA 1997” the expenses made on the basis to start a

business activity or any work producing to income, that activity will not be considered for

deduction. The court of “Maddalena v FCT (1971)” found that expenses that has made in

travelling to second club and the payment for the activity of negotiating was non-deductible.

The expenses incurred of $300 for a new employment under a new employer refer to a

pre commencement to income generating activities. Referring to the above case the amount

of $300 is basis to begin income producing and hence, not allowed for the tax deduction

under section 8-1, ITAA 1997”.

Answer to Question: 4

Answer (a)

A CGT event takes place when a person allows a lease to someone, they can extend

the period or renew the lease in accordance to the earlier person granted to that lease. On

making the capital gains under CGT event F1, the discount is not applicable.

In the given question, John has owned some land and he has granted the lease to

David for an amount of $7,000. It has resulted in the capital gain from CGT event F1.

Therefore, not any CGT discount on CGT event F1 is applicable.

According to “section 8-1, ITAA 1997”, the expenses that has made on the clothing will

not be consider for deduction. In case, “Mansfield v FCT (1996)” expenses made on the

ordinary article related to apparel has not allowed for tax deduction.

The expenses made for shirts and black trousers of $145 is for work at office that is an

ordinary article for apparel. Referring the above case the amount of $145 is non-deductible.

(g) Legal expenses incurred in writing up a new employment contract with a new

employer- $300:

According to “section 8-1, ITAA 1997” the expenses made on the basis to start a

business activity or any work producing to income, that activity will not be considered for

deduction. The court of “Maddalena v FCT (1971)” found that expenses that has made in

travelling to second club and the payment for the activity of negotiating was non-deductible.

The expenses incurred of $300 for a new employment under a new employer refer to a

pre commencement to income generating activities. Referring to the above case the amount

of $300 is basis to begin income producing and hence, not allowed for the tax deduction

under section 8-1, ITAA 1997”.

Answer to Question: 4

Answer (a)

A CGT event takes place when a person allows a lease to someone, they can extend

the period or renew the lease in accordance to the earlier person granted to that lease. On

making the capital gains under CGT event F1, the discount is not applicable.

In the given question, John has owned some land and he has granted the lease to

David for an amount of $7,000. It has resulted in the capital gain from CGT event F1.

Therefore, not any CGT discount on CGT event F1 is applicable.

11Taxation Law of Australia

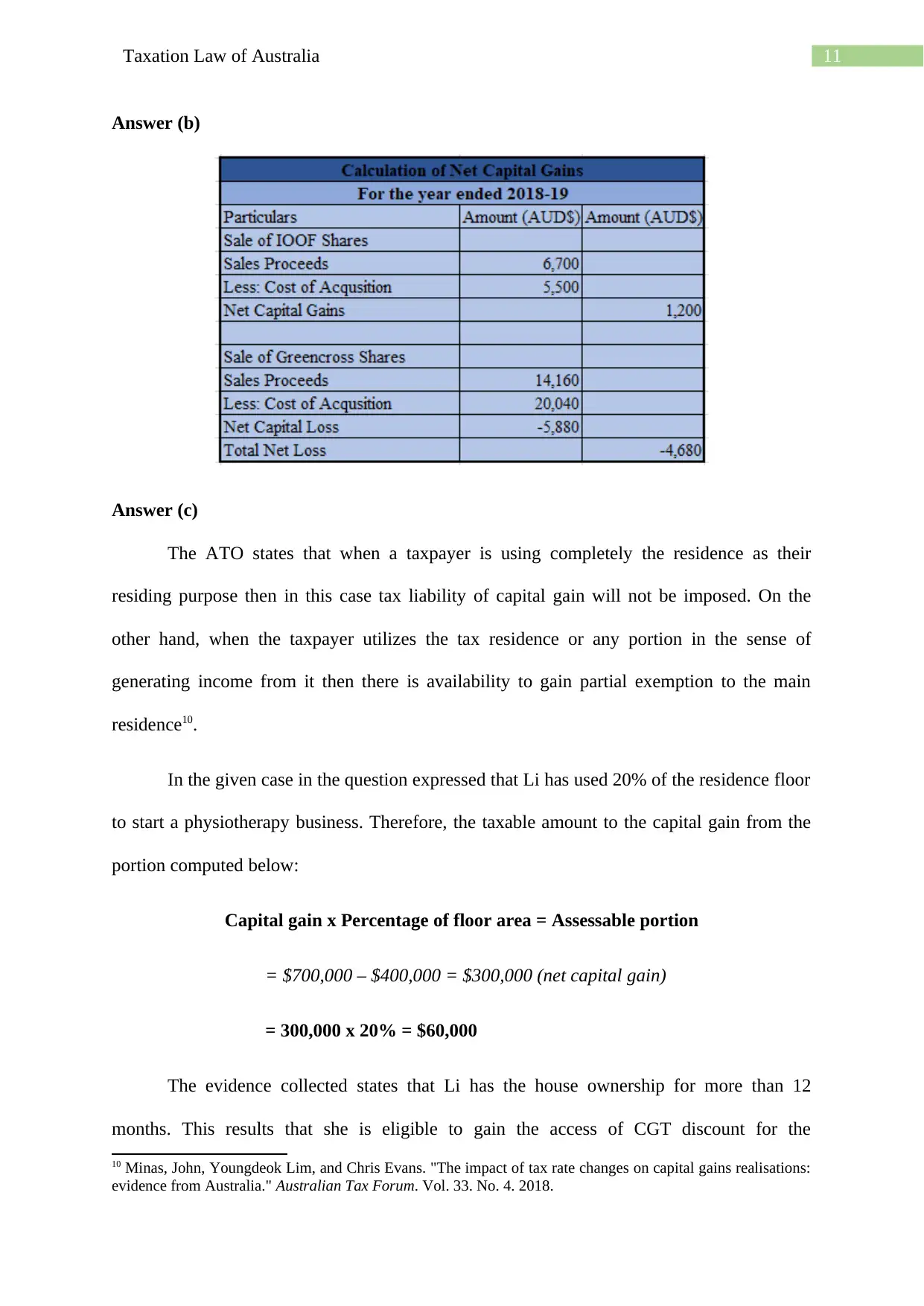

Answer (b)

Answer (c)

The ATO states that when a taxpayer is using completely the residence as their

residing purpose then in this case tax liability of capital gain will not be imposed. On the

other hand, when the taxpayer utilizes the tax residence or any portion in the sense of

generating income from it then there is availability to gain partial exemption to the main

residence10.

In the given case in the question expressed that Li has used 20% of the residence floor

to start a physiotherapy business. Therefore, the taxable amount to the capital gain from the

portion computed below:

Capital gain x Percentage of floor area = Assessable portion

= $700,000 – $400,000 = $300,000 (net capital gain)

= 300,000 x 20% = $60,000

The evidence collected states that Li has the house ownership for more than 12

months. This results that she is eligible to gain the access of CGT discount for the

10 Minas, John, Youngdeok Lim, and Chris Evans. "The impact of tax rate changes on capital gains realisations:

evidence from Australia." Australian Tax Forum. Vol. 33. No. 4. 2018.

Answer (b)

Answer (c)

The ATO states that when a taxpayer is using completely the residence as their

residing purpose then in this case tax liability of capital gain will not be imposed. On the

other hand, when the taxpayer utilizes the tax residence or any portion in the sense of

generating income from it then there is availability to gain partial exemption to the main

residence10.

In the given case in the question expressed that Li has used 20% of the residence floor

to start a physiotherapy business. Therefore, the taxable amount to the capital gain from the

portion computed below:

Capital gain x Percentage of floor area = Assessable portion

= $700,000 – $400,000 = $300,000 (net capital gain)

= 300,000 x 20% = $60,000

The evidence collected states that Li has the house ownership for more than 12

months. This results that she is eligible to gain the access of CGT discount for the

10 Minas, John, Youngdeok Lim, and Chris Evans. "The impact of tax rate changes on capital gains realisations:

evidence from Australia." Australian Tax Forum. Vol. 33. No. 4. 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.