Analyzing Tax Implications in Various Australian Case Studies

VerifiedAdded on 2020/04/01

|11

|1766

|68

AI Summary

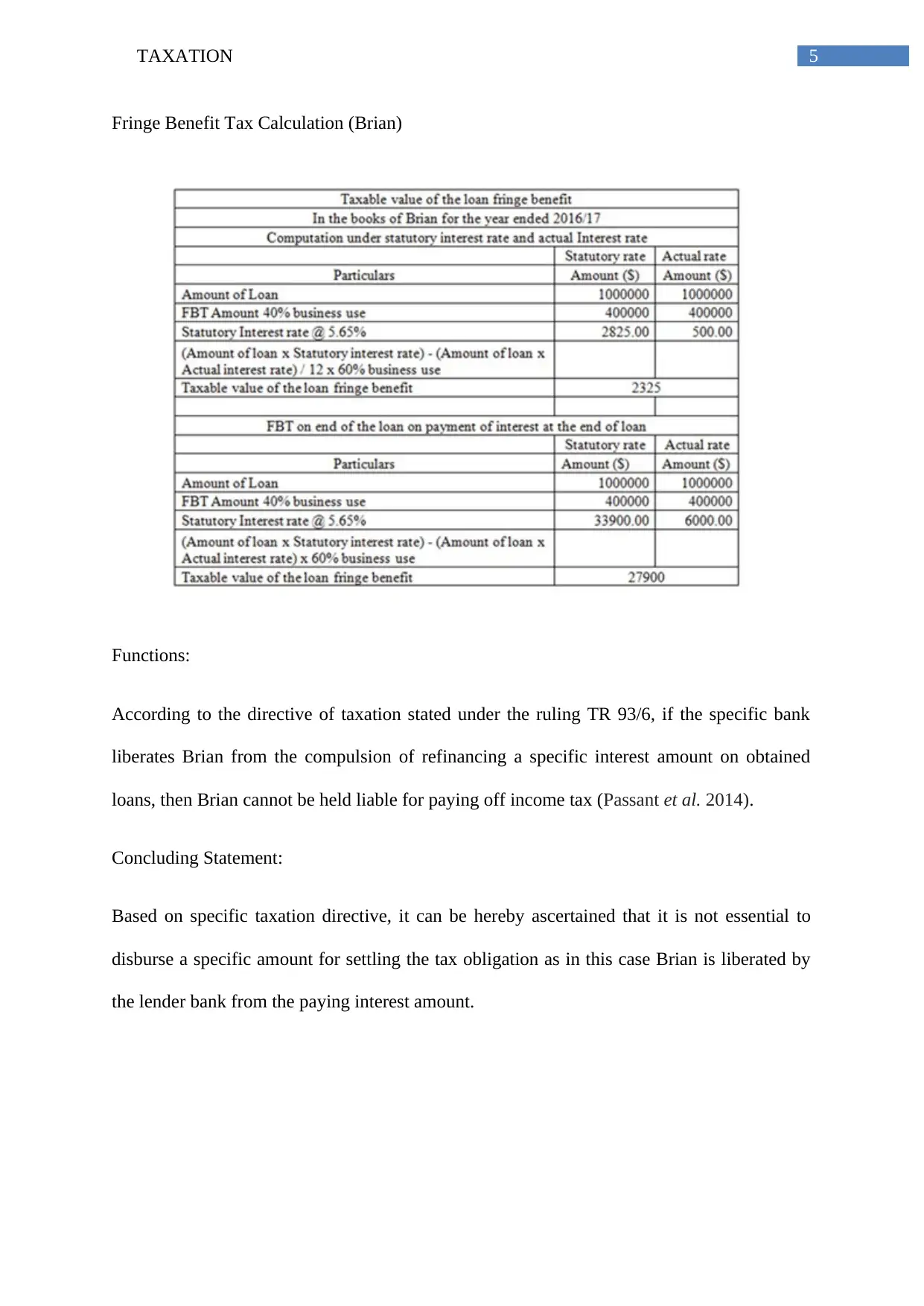

The assignment entails a detailed analysis of several Australian tax cases involving various aspects such as income derived from forestry activities and timber sales. Key areas include examining the implications under specific sections of the Income Tax Assessment Act (ITAA) 1936 and ITAA 1997, notably focusing on how timber sale advances are treated for taxation purposes. The study also looks at royalty payments as outlined in section 26(f) of the ITAA 1936. Furthermore, it explores broader tax issues such as socially responsible firms' tax obligations, emphasizing understanding both specific case facts and overarching legal principles. References to various scholarly articles provide additional insights into related topics like environmental taxation law and economic efficiency linked with Australian taxes.

1 out of 11

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.