Taxation Law: Detailed Examination of Small Business Concessions

VerifiedAdded on 2021/06/18

|14

|719

|18

Report

AI Summary

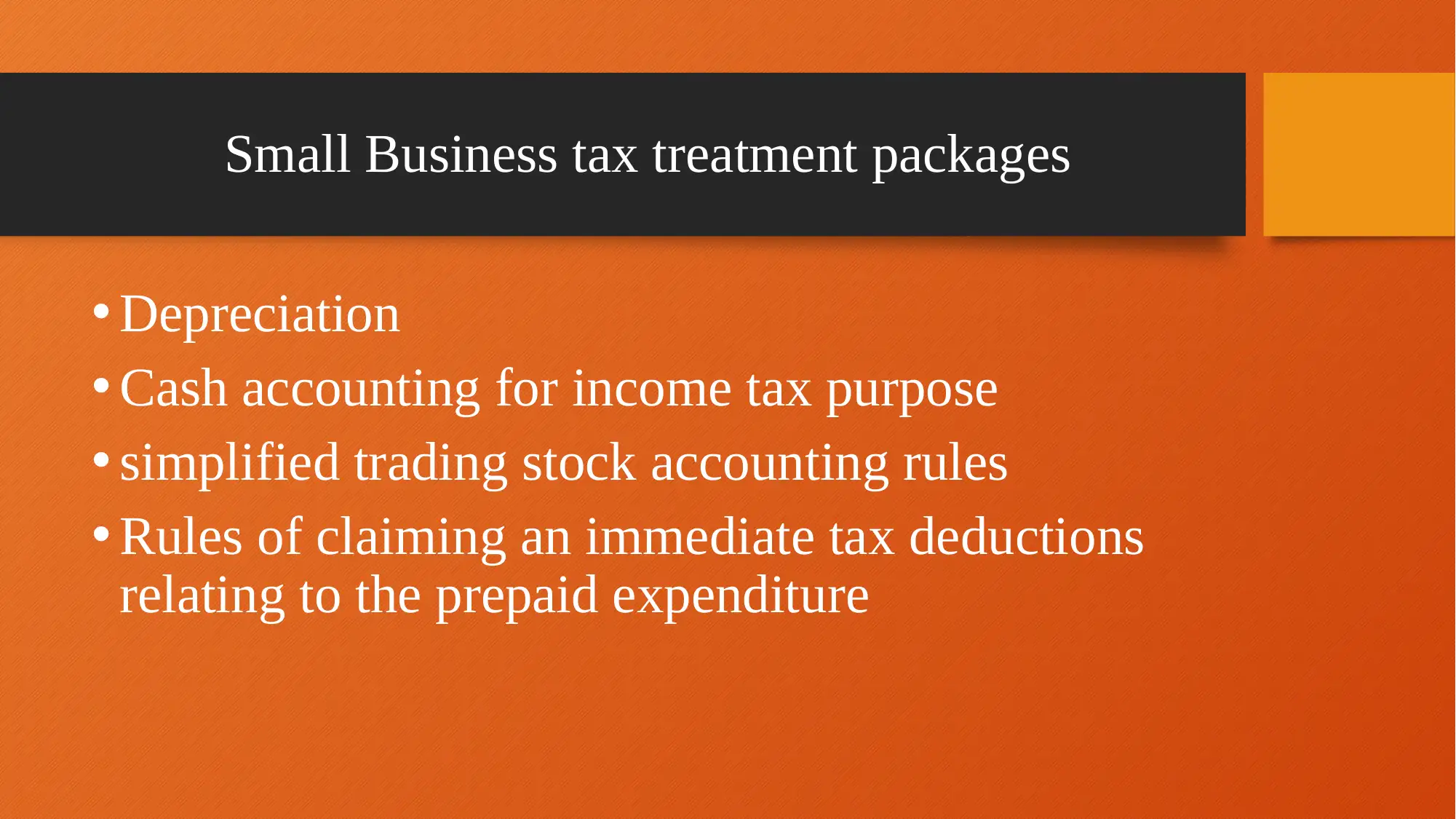

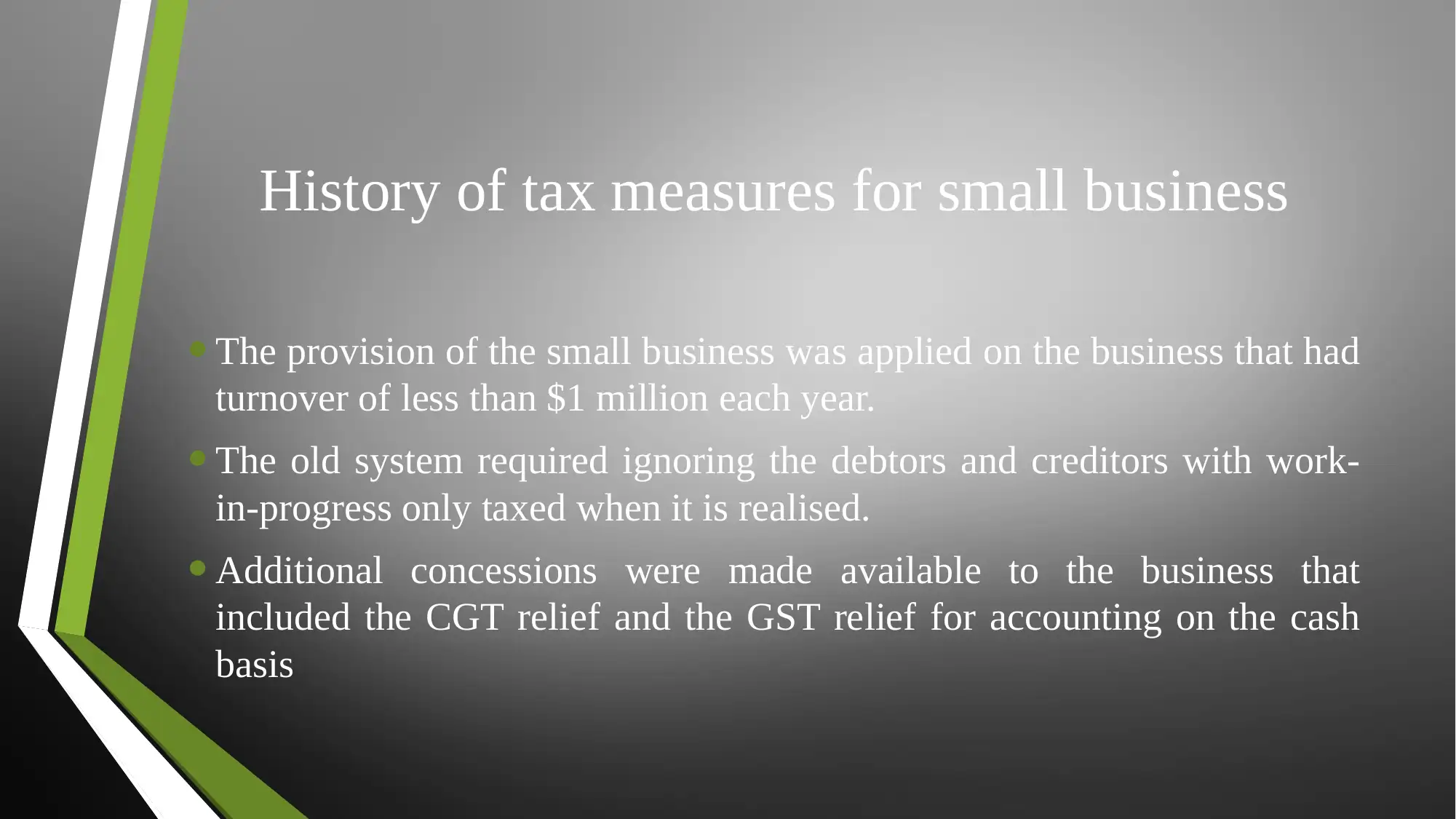

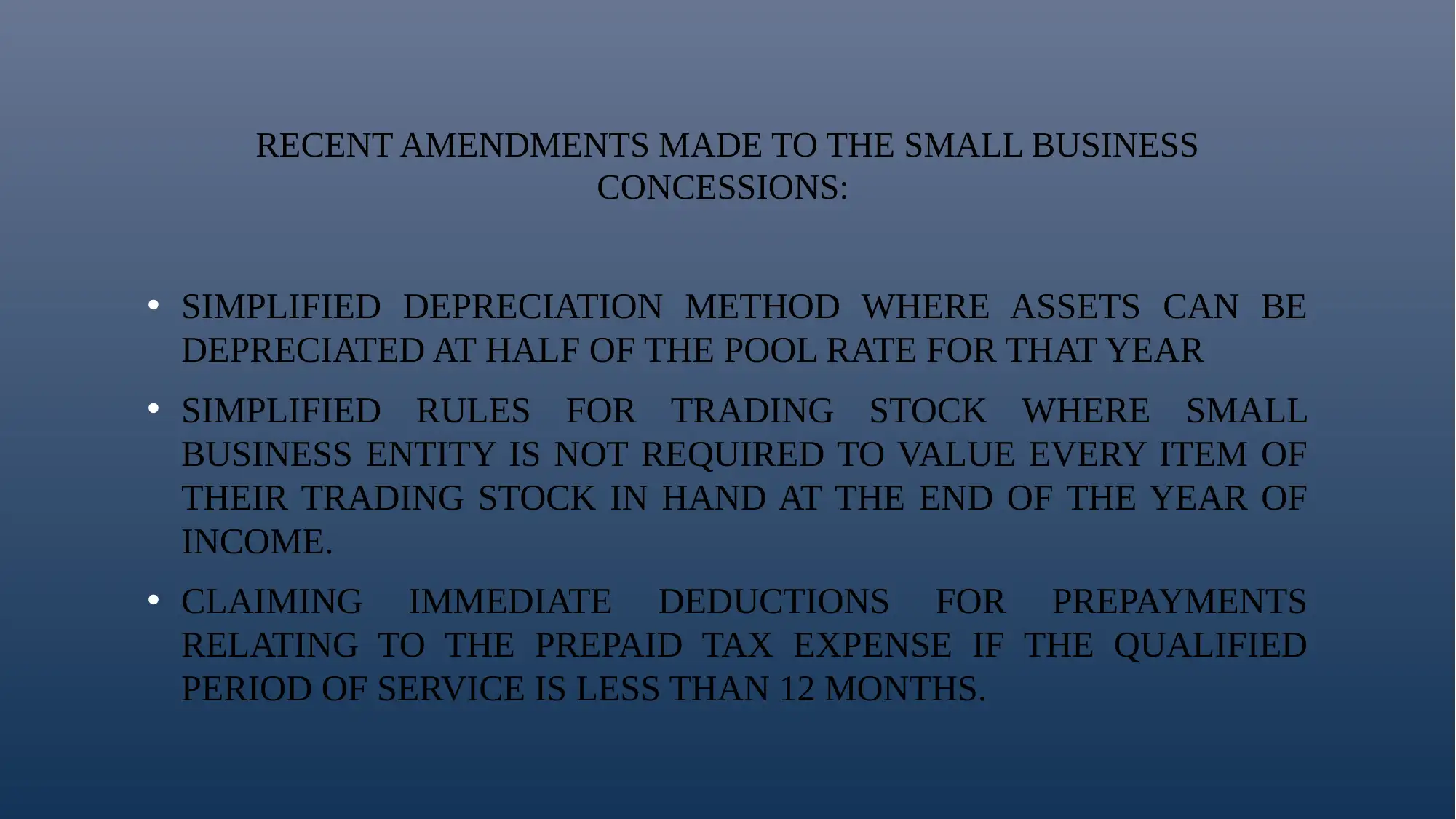

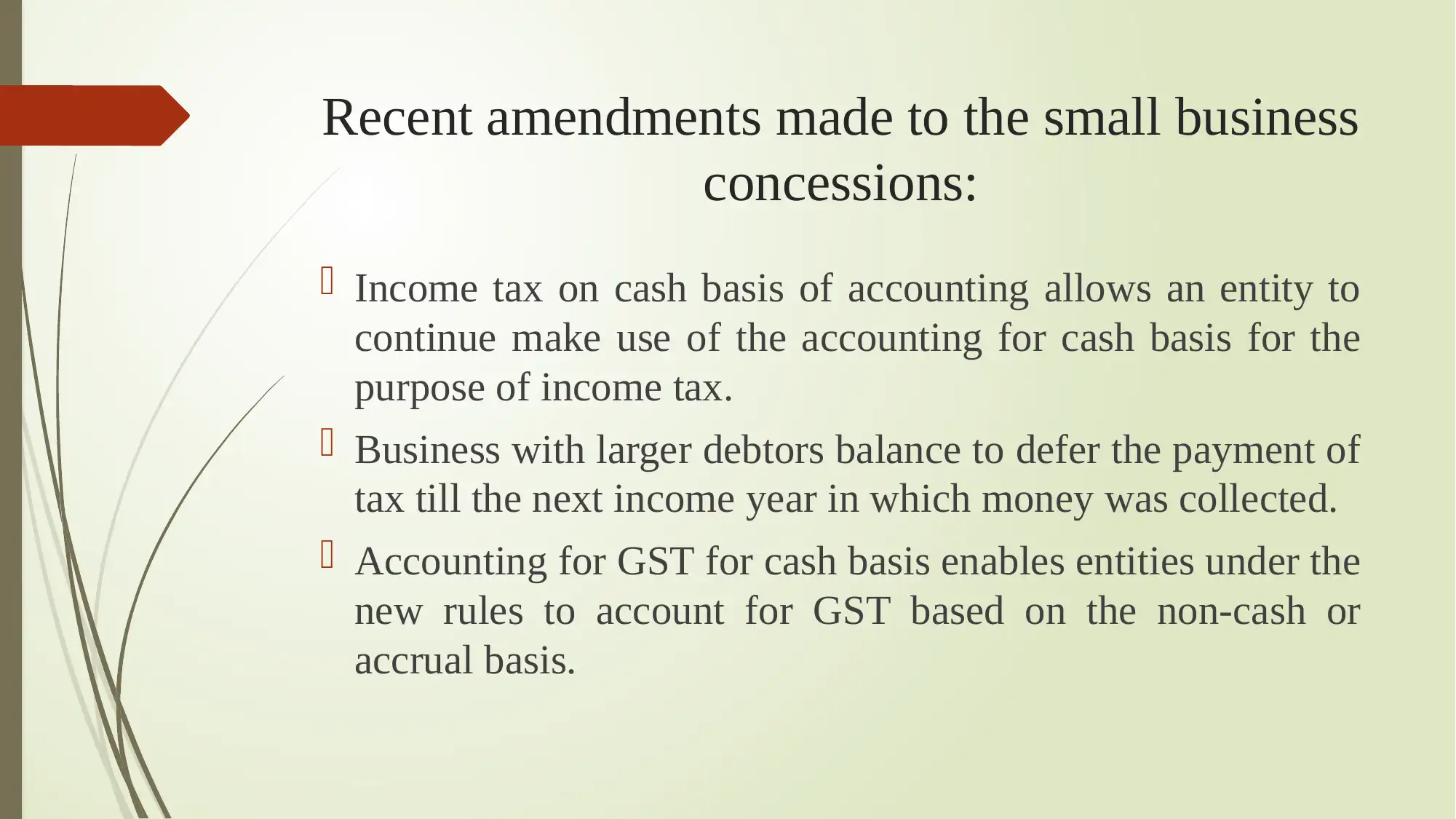

This report provides an overview of taxation law, specifically focusing on small business concessions in Australia. It begins by highlighting the significant contribution of small businesses to the Australian economy and the importance of concessions like the Capital Gains Tax (CGT) relief. The report details various types of concessions, including 15-year exemptions, 50% reductions, retirement exemptions, and rollover exemptions, alongside the eligibility criteria such as the net asset value test and active asset tests. It explores the objectives of these concessions, which aim to simplify tax measures and reduce compliance costs. The report then outlines the history of tax measures for small businesses, including the introduction of simplified tax treatment packages. It also covers recent amendments, such as simplified depreciation methods, trading stock rules, and immediate deductions for prepaid expenses. The effectiveness of these methods is assessed, and recommendations are made, including potential adjustments to the net asset value test. In conclusion, the report underscores the widespread adoption of small business concessions, particularly CGT reliefs and the use of cash basis accounting for GST purposes, emphasizing the efforts to reduce compliance costs for small businesses. The report is a valuable resource for students seeking to understand the intricacies of small business taxation in Australia and is available on Desklib.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.