FNSACC502 Diploma of Accounting: Australian Tax Documentation Guide

VerifiedAdded on 2023/06/11

|16

|4348

|472

Homework Assignment

AI Summary

This assignment provides a comprehensive overview of the Australian taxation system, focusing on the preparation of tax documentation for individuals. It covers various aspects of tax legislation, including assessable and exempt income, deductions, tax offsets, capital gains and losses, and specific provisions related to car expenses, gifts, capital allowances, pensions, employment termination payments, and personal service income. The assignment also addresses record-keeping requirements, information related to family trusts, superannuation provisions, and small business entities. Furthermore, it includes practical sections involving Business Activity Statements (BAS), tax agent requirements, audit compliance, and the use of myGov for tax-related activities. The document includes references to relevant sections of the Income Tax Assessment Act 1997 and other legislative instruments, offering a detailed guide to understanding and navigating the Australian tax system for individuals. Desklib provides this document and many more to help students with their studies.

Australia Taxation

An Overview

An Overview

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Australia Taxation..................................................................................................................................1

TABLE OF CONTENTS..........................................................................................................................2

Part 1 Legislation........................................................................................................................................4

Answers:..................................................................................................................................................4

Division 6 - Assessable income and exempt income............................................................................4

Division 8-Deductions..........................................................................................................................5

Division 13-Tax offsets.........................................................................................................................6

Chapter 3-Part3-1................................................................................................................................6

Division 28-Car expenses.....................................................................................................................7

Division 30: Gifts or Contribution........................................................................................................7

Division 40-Capital allowances............................................................................................................7

Division 52-Certain pensions, benefits and allowances are exempt from income tax.........................8

Division 82-Employment termination payments.................................................................................9

Division 84—Introduction to Personal service income........................................................................9

Division 100-A Guide to capital gains and losses.................................................................................9

Division 121-Record keeping...............................................................................................................9

Division 180-Information about family trusts with interests in companies.........................................9

Division 200:......................................................................................................................................10

Division 280-Guide to the superannuation provisions.......................................................................10

Division 328-Small business entities..................................................................................................10

Division 900--Substantiation rules.....................................................................................................10

Division 905--Offences.......................................................................................................................10

Part 2 – Refer Excel Exhibit........................................................................................................................11

Part 3 – Refer Excel Exhibit........................................................................................................................11

Part 4 – Refer Excel Exhibit........................................................................................................................11

Part 5 – Refer Excel Exhibit........................................................................................................................11

Part 7 – Refer Excel Exhibit........................................................................................................................11

Part 8 – Refer Excel Exhibit........................................................................................................................11

Part 9 – Refer Excel Exhibit........................................................................................................................11

Part 10 Business Activity Statements (BAS)...............................................................................................11

Australia Taxation..................................................................................................................................1

TABLE OF CONTENTS..........................................................................................................................2

Part 1 Legislation........................................................................................................................................4

Answers:..................................................................................................................................................4

Division 6 - Assessable income and exempt income............................................................................4

Division 8-Deductions..........................................................................................................................5

Division 13-Tax offsets.........................................................................................................................6

Chapter 3-Part3-1................................................................................................................................6

Division 28-Car expenses.....................................................................................................................7

Division 30: Gifts or Contribution........................................................................................................7

Division 40-Capital allowances............................................................................................................7

Division 52-Certain pensions, benefits and allowances are exempt from income tax.........................8

Division 82-Employment termination payments.................................................................................9

Division 84—Introduction to Personal service income........................................................................9

Division 100-A Guide to capital gains and losses.................................................................................9

Division 121-Record keeping...............................................................................................................9

Division 180-Information about family trusts with interests in companies.........................................9

Division 200:......................................................................................................................................10

Division 280-Guide to the superannuation provisions.......................................................................10

Division 328-Small business entities..................................................................................................10

Division 900--Substantiation rules.....................................................................................................10

Division 905--Offences.......................................................................................................................10

Part 2 – Refer Excel Exhibit........................................................................................................................11

Part 3 – Refer Excel Exhibit........................................................................................................................11

Part 4 – Refer Excel Exhibit........................................................................................................................11

Part 5 – Refer Excel Exhibit........................................................................................................................11

Part 7 – Refer Excel Exhibit........................................................................................................................11

Part 8 – Refer Excel Exhibit........................................................................................................................11

Part 9 – Refer Excel Exhibit........................................................................................................................11

Part 10 Business Activity Statements (BAS)...............................................................................................11

Answer 1:...............................................................................................................................................11

Answer 2:...............................................................................................................................................11

Answer 3:...............................................................................................................................................12

Answer4:................................................................................................................................................12

Part 11 – Refer Excel Exhibit......................................................................................................................12

Part 12 Tax agent requirements...............................................................................................................12

Part 13 Audit compliance.........................................................................................................................13

Answer 1:...............................................................................................................................................13

Answer 2:...............................................................................................................................................13

Part 15 myGov...........................................................................................................................................14

Answer 1:...............................................................................................................................................14

Answer 2:...............................................................................................................................................14

Answer 3:...............................................................................................................................................15

Answer 4:...............................................................................................................................................15

Answer 5:...............................................................................................................................................15

Bibliography...............................................................................................................................................16

Answer 2:...............................................................................................................................................11

Answer 3:...............................................................................................................................................12

Answer4:................................................................................................................................................12

Part 11 – Refer Excel Exhibit......................................................................................................................12

Part 12 Tax agent requirements...............................................................................................................12

Part 13 Audit compliance.........................................................................................................................13

Answer 1:...............................................................................................................................................13

Answer 2:...............................................................................................................................................13

Part 15 myGov...........................................................................................................................................14

Answer 1:...............................................................................................................................................14

Answer 2:...............................................................................................................................................14

Answer 3:...............................................................................................................................................15

Answer 4:...............................................................................................................................................15

Answer 5:...............................................................................................................................................15

Bibliography...............................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 1 Legislation

Answers:

1. The Australian Taxation Office (ATO) is the main revenue collection agency of the

government. The main role of ATO is to shape the tax and superannuation system in

such a way that it acts as a pillar for fund services for the people out there but not

limited to::

collecting income tax revenue for government

monitoring the goods and services tax (GST) on behalf of the Australian states

and territories

to govern the Programs which result in transfer and benefit to the community.

To administer Australia’s superannuation system

Person responsible for the Australian Business Register1

2. The ITAA1936 is an act of Australia. It is under this act Australian Income tax is

calculated. This act is rewritten into the Income Tax Assessment Act 1997, and new

things have been included in the Income Tax Assessment Act 1997.2

3.

Division 6 - Assessable income and exempt income

Income according to ordinary concepts (ordinary income)

(1) According to ordinary concepts assessable income includes income, which is

called ordinary income.

(2) Assessable income means the income derived directly or indirectly from inside or

outside the country during the year..

(3) If you are a non resident,your assessable income includes:

a) the ordinary income you derived directly or indirectly from all sources during the

year; and

b) other ordinary income that a provision includes in your assessable income for

the income year on some basis other than having an Australian source.

1 Australian Government, About us (23 Apr 2018) <https://www.ato.gov.au/About-ATO/About-us/>

2 Wikipedia, Income Tax Assessment Act 1936 (27 May 2018)

<https://en.wikipedia.org/wiki/Income_Tax_Assessment_Act_1936>

Answers:

1. The Australian Taxation Office (ATO) is the main revenue collection agency of the

government. The main role of ATO is to shape the tax and superannuation system in

such a way that it acts as a pillar for fund services for the people out there but not

limited to::

collecting income tax revenue for government

monitoring the goods and services tax (GST) on behalf of the Australian states

and territories

to govern the Programs which result in transfer and benefit to the community.

To administer Australia’s superannuation system

Person responsible for the Australian Business Register1

2. The ITAA1936 is an act of Australia. It is under this act Australian Income tax is

calculated. This act is rewritten into the Income Tax Assessment Act 1997, and new

things have been included in the Income Tax Assessment Act 1997.2

3.

Division 6 - Assessable income and exempt income

Income according to ordinary concepts (ordinary income)

(1) According to ordinary concepts assessable income includes income, which is

called ordinary income.

(2) Assessable income means the income derived directly or indirectly from inside or

outside the country during the year..

(3) If you are a non resident,your assessable income includes:

a) the ordinary income you derived directly or indirectly from all sources during the

year; and

b) other ordinary income that a provision includes in your assessable income for

the income year on some basis other than having an Australian source.

1 Australian Government, About us (23 Apr 2018) <https://www.ato.gov.au/About-ATO/About-us/>

2 Wikipedia, Income Tax Assessment Act 1936 (27 May 2018)

<https://en.wikipedia.org/wiki/Income_Tax_Assessment_Act_1936>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(4) In working out whether you have derived an amount of ordinary income, and (if

so) when you derived it, you are taken to have received the amount as soon as it is

applied or dealt with in any way on your behalf or as you direct. 3

Other assessable income (statutory income)

Amount that are not ordinary income but are included in ordinary income by provisions

are called statutory income.

Although an amount is statutory income because it has been included in assessable

income under a provision of this Act. 4

Division 8-Deductions

General deductions

Any loss can be deducted from your assessable income to the extent::

a) to gain that assessable income it is incurred.

b) to carry out the business in order to gain that assessable income..

However, one cannot deduct loss under this section to the extent:

a) Capital Nature Loss

b) Private or domestic nature.

c) It is incurred in relation to producing non exempt income

d) Prevention of Provision 5

Specific deductions

1. Deduct an amount which the provision of this act allows you to deduct..

2. Some Provision Prohibits to deduct an amount that one could otherwise deduct

3. An amount that can be deducted under this section is called Specific Deduction6

3 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 6.5 Income according to ordinary concepts

(ordinary income), <http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s6.5.html>

4 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 6.10 Other assessable income (statutory

income), < http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s6.10.html>

5 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 8.1 General deductions, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.1.html>

6 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 8.5 Specific deductions, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.5.html>

so) when you derived it, you are taken to have received the amount as soon as it is

applied or dealt with in any way on your behalf or as you direct. 3

Other assessable income (statutory income)

Amount that are not ordinary income but are included in ordinary income by provisions

are called statutory income.

Although an amount is statutory income because it has been included in assessable

income under a provision of this Act. 4

Division 8-Deductions

General deductions

Any loss can be deducted from your assessable income to the extent::

a) to gain that assessable income it is incurred.

b) to carry out the business in order to gain that assessable income..

However, one cannot deduct loss under this section to the extent:

a) Capital Nature Loss

b) Private or domestic nature.

c) It is incurred in relation to producing non exempt income

d) Prevention of Provision 5

Specific deductions

1. Deduct an amount which the provision of this act allows you to deduct..

2. Some Provision Prohibits to deduct an amount that one could otherwise deduct

3. An amount that can be deducted under this section is called Specific Deduction6

3 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 6.5 Income according to ordinary concepts

(ordinary income), <http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s6.5.html>

4 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 6.10 Other assessable income (statutory

income), < http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s6.10.html>

5 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 8.1 General deductions, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.1.html>

6 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 8.5 Specific deductions, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.5.html>

No double deductions

If two or more Provisions of the act allow to deduct the same amount than the amount

will be deducted under the Provisions which is Proper. 7

Division 13-Tax offsets

The Provision sets out in the list allow you for the tax offset some of which are as

follows:8

Social security and other benefit payments

Leave payments

Superannuation

Dividends

Nonresident beneficiary

Life insurance

Primary production

Child

Dividends

Member serving overseas

Venture capital limited partnership

Employment termination payments

Dependants

National rental affordability

Foreign Income tax paid

Franking deficit tax

Bonus receipt of life insurance

Leave payments

Nonresident beneficiary

Social security and other benefit payment

Chapter 3-Part3-1

This Division is a simplified outline of the capital gains and capital losses provisions,

commonly referred to as capital gains tax ( CGT ). It will help you to understand your

current liabilities, and to factor CGT into your on-going financial affairs. 9

7 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 8.10 No double deductions, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.10.html>

8 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 13.1 List of tax offsets, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s13.1.html>

9 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 100.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s100.1.html>

If two or more Provisions of the act allow to deduct the same amount than the amount

will be deducted under the Provisions which is Proper. 7

Division 13-Tax offsets

The Provision sets out in the list allow you for the tax offset some of which are as

follows:8

Social security and other benefit payments

Leave payments

Superannuation

Dividends

Nonresident beneficiary

Life insurance

Primary production

Child

Dividends

Member serving overseas

Venture capital limited partnership

Employment termination payments

Dependants

National rental affordability

Foreign Income tax paid

Franking deficit tax

Bonus receipt of life insurance

Leave payments

Nonresident beneficiary

Social security and other benefit payment

Chapter 3-Part3-1

This Division is a simplified outline of the capital gains and capital losses provisions,

commonly referred to as capital gains tax ( CGT ). It will help you to understand your

current liabilities, and to factor CGT into your on-going financial affairs. 9

7 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 8.10 No double deductions, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s8.10.html>

8 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 13.1 List of tax offsets, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s13.1.html>

9 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 100.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s100.1.html>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Division 28-Car expenses

This Division frames out the rules for deduction of car expenses if you have a lease car

or hire a car under Hire Purchase agreement.10

This division applies to individual; Partnership firm mustincludes at least one individual,

as if the Partnership were an individual. 11

Two methods are there of computing car Expenses:

The Cents Per Kilometer Method - Number of business kilometers travelled by

car multiplied by the rate of cents kilometers determined for the car 12

The Log method -To use the log method you need to multiply the amount of car

expenses by the business use percentage. 13

Division 30: Gifts or Contribution

This division sets out the requirements to meet in order to qualify for deduction of a

gift .It tells who the recipient of gift and the type of gift or contribution made and how

much deduction for gift and any special condition that are applicable.

A testamentary gift is not deductible under this section.14

Division 40-Capital allowances

(1) A depreciating asset is an asset that has a minimum useful life and depreciates in

value over a period of time, except: 1516

a) land; or

b) Trading stock; or

c) An intangible asset, unless it is mentioned below.

(2) Certain intangible assets which are depreciating assets and not trading stock:

10 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 100.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s100.1.html>

11 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 28.10 Application of Division 28, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s28.10.html>

12 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 28.25 How to calculate your deduction, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s28.25.html>

13 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 28.90 How to calculate your deduction, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s28.90.html>

14 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 30.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s30.1.html>

15 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 40.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s40.1.html>

16 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 40.30 What a depreciating asset is, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s40.30.html>

This Division frames out the rules for deduction of car expenses if you have a lease car

or hire a car under Hire Purchase agreement.10

This division applies to individual; Partnership firm mustincludes at least one individual,

as if the Partnership were an individual. 11

Two methods are there of computing car Expenses:

The Cents Per Kilometer Method - Number of business kilometers travelled by

car multiplied by the rate of cents kilometers determined for the car 12

The Log method -To use the log method you need to multiply the amount of car

expenses by the business use percentage. 13

Division 30: Gifts or Contribution

This division sets out the requirements to meet in order to qualify for deduction of a

gift .It tells who the recipient of gift and the type of gift or contribution made and how

much deduction for gift and any special condition that are applicable.

A testamentary gift is not deductible under this section.14

Division 40-Capital allowances

(1) A depreciating asset is an asset that has a minimum useful life and depreciates in

value over a period of time, except: 1516

a) land; or

b) Trading stock; or

c) An intangible asset, unless it is mentioned below.

(2) Certain intangible assets which are depreciating assets and not trading stock:

10 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 100.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s100.1.html>

11 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 28.10 Application of Division 28, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s28.10.html>

12 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 28.25 How to calculate your deduction, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s28.25.html>

13 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 28.90 How to calculate your deduction, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s28.90.html>

14 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 30.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s30.1.html>

15 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 40.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s40.1.html>

16 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 40.30 What a depreciating asset is, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s40.30.html>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a) mining, quarrying or prospecting rights;

b) mining, quarrying or prospecting information;

c) Intellectual property;

d) In-house software;

e) IRUs;

f) spectrum licenses;

g) data casting transmitter licenses;

h) Telecommunications site access rights.

(3) This Division applies to an improvement to land, or a fixture on land, whether the

improvement or fixture is removable or not, as if it were an asset separate from the land.

(4) Whether a particular composite item is itself a depreciating asset or whether its

components are separate depreciating assets is a question of fact and degree which

can only be determined in the light of all the circumstances of the particular case.

(5) This Division applies to a renewal or extension of a depreciating asset that is a right

as if the renewal or extension were a continuation of the original right.

(6) This Division applies to a mining, quarrying or prospecting right (the new right) as if

it were a continuation of another mining, quarrying or prospecting right you held if:

a) the other right ends; and

b) the new right and the other right relate to the same area, or any difference

in area is not significant

Division 52-Certain pensions, benefits and allowances are exempt from income tax

Under this division certain pension, benefits and allowances are exempt from income

tax either wholly or partly.

Subdivisions:

52-A Exempt Payments under the Social Security Act 1991

52-B Exempt Payments under the Veterans Entitlement Act 1986

52-C Exempt Payments made because of Veterans Entitlement Act 1986

52-CA Exempt Payments under the Military Rehabilitation and Compensation

Act 2004

52-D Exempt payments made by the Commonwealth to reimburse certain

expenditure

52-F Exemption of Commonwealth education or training payments

b) mining, quarrying or prospecting information;

c) Intellectual property;

d) In-house software;

e) IRUs;

f) spectrum licenses;

g) data casting transmitter licenses;

h) Telecommunications site access rights.

(3) This Division applies to an improvement to land, or a fixture on land, whether the

improvement or fixture is removable or not, as if it were an asset separate from the land.

(4) Whether a particular composite item is itself a depreciating asset or whether its

components are separate depreciating assets is a question of fact and degree which

can only be determined in the light of all the circumstances of the particular case.

(5) This Division applies to a renewal or extension of a depreciating asset that is a right

as if the renewal or extension were a continuation of the original right.

(6) This Division applies to a mining, quarrying or prospecting right (the new right) as if

it were a continuation of another mining, quarrying or prospecting right you held if:

a) the other right ends; and

b) the new right and the other right relate to the same area, or any difference

in area is not significant

Division 52-Certain pensions, benefits and allowances are exempt from income tax

Under this division certain pension, benefits and allowances are exempt from income

tax either wholly or partly.

Subdivisions:

52-A Exempt Payments under the Social Security Act 1991

52-B Exempt Payments under the Veterans Entitlement Act 1986

52-C Exempt Payments made because of Veterans Entitlement Act 1986

52-CA Exempt Payments under the Military Rehabilitation and Compensation

Act 2004

52-D Exempt payments made by the Commonwealth to reimburse certain

expenditure

52-F Exemption of Commonwealth education or training payments

52-G Exempt payments under the A New Tax System (Family Assistance)

(Administration) Act 1999 17

Division 82-Employment termination payments

It explain how employment termination payments are treated under Income Tax Act.. 18

Division 84—Introduction to Personal service income

This is about two issues relating to Personal services income which mean ordinary

income or statutory income, or the ordinary income or statutory income of any other

entity, is your personal services income if the income is mainly a reward for your

personal efforts or skills (or would mainly be such a reward if it was your income). 19

Only Individuals can have Personal service income. This section applies whether the

income is for doing work or is for producing a result. The fact that the income is payable

under a contract does not stop the income being mainly a reward for your personal

efforts or skills. This Part does not say that individual is an employee.

Division 100-A Guide to capital gains and losses

This section talks about Capital gain Tax and make you understand your current

liabilities and to take into account capital gain tax into your on-going financial

services..20

Division 121-Record keeping

You must keep the record for at least five years and compulsorily for capital gain and

losses you made after the last relevant Capital Gain Tax event..21

Division 180-Information about family trusts with interests in companies

If the company would only avoid the tax consequences of Division 165 or 175 because

of interests held by a foreign resident family trust, the Commissioner may require the

company to give certain information about the family trust. If it is not given, the company

does not avoid the tax consequences of that Division. 22

17 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 52.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s52.1.html>

18 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 82.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s82.1.html>

19 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 84.5 Meaning of personal services income, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s84.5.html>

20 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 100.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s100.1.html>

21 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 121.10 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s121.10.html>

22 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 180.1 What this Division is about, <

http://www5.austlii.edu.au/au//legis/cth/consol_act/itaa1997240/s180.1.html>

(Administration) Act 1999 17

Division 82-Employment termination payments

It explain how employment termination payments are treated under Income Tax Act.. 18

Division 84—Introduction to Personal service income

This is about two issues relating to Personal services income which mean ordinary

income or statutory income, or the ordinary income or statutory income of any other

entity, is your personal services income if the income is mainly a reward for your

personal efforts or skills (or would mainly be such a reward if it was your income). 19

Only Individuals can have Personal service income. This section applies whether the

income is for doing work or is for producing a result. The fact that the income is payable

under a contract does not stop the income being mainly a reward for your personal

efforts or skills. This Part does not say that individual is an employee.

Division 100-A Guide to capital gains and losses

This section talks about Capital gain Tax and make you understand your current

liabilities and to take into account capital gain tax into your on-going financial

services..20

Division 121-Record keeping

You must keep the record for at least five years and compulsorily for capital gain and

losses you made after the last relevant Capital Gain Tax event..21

Division 180-Information about family trusts with interests in companies

If the company would only avoid the tax consequences of Division 165 or 175 because

of interests held by a foreign resident family trust, the Commissioner may require the

company to give certain information about the family trust. If it is not given, the company

does not avoid the tax consequences of that Division. 22

17 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 52.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s52.1.html>

18 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 82.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s82.1.html>

19 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 84.5 Meaning of personal services income, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s84.5.html>

20 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 100.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s100.1.html>

21 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 121.10 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s121.10.html>

22 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT 180.1 What this Division is about, <

http://www5.austlii.edu.au/au//legis/cth/consol_act/itaa1997240/s180.1.html>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Division 200:

This division provides an overview of the imputation system.

Division 280-Guide to the superannuation provisions

Superannuation provisions Provides tax benefit when your investment is in

superannuation .and income derived from superannuation.

Division 328-Small business entities

This division explains the meaning of small business entity, annual turnover and

aggregated turnover and related concepts.

If you are a small business entity,

You can chose to put the asset into pool and treat the pool as single asset.

You can choose not to account for annual changes in trading stock value that not

more than $5000.

These changes will simplify the working of Taxable income and reduce your compliance

costs. 23

Division 900--Substantiation rules

This division sets out the substantiation rules that apply to certain types of losses or

outgoings. 24

Division 905--Offences

This division deals with the criminal code applies to all offences against this act.

Part 2 – Refer Excel Exhibit

Part 3 – Refer Excel Exhibit

23 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT SECT 328.5 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s328.5.html>

24 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT SECT 900.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s900.1.html>

This division provides an overview of the imputation system.

Division 280-Guide to the superannuation provisions

Superannuation provisions Provides tax benefit when your investment is in

superannuation .and income derived from superannuation.

Division 328-Small business entities

This division explains the meaning of small business entity, annual turnover and

aggregated turnover and related concepts.

If you are a small business entity,

You can chose to put the asset into pool and treat the pool as single asset.

You can choose not to account for annual changes in trading stock value that not

more than $5000.

These changes will simplify the working of Taxable income and reduce your compliance

costs. 23

Division 900--Substantiation rules

This division sets out the substantiation rules that apply to certain types of losses or

outgoings. 24

Division 905--Offences

This division deals with the criminal code applies to all offences against this act.

Part 2 – Refer Excel Exhibit

Part 3 – Refer Excel Exhibit

23 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT SECT 328.5 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s328.5.html>

24 Australian Government, INCOME TAX ASSESSMENT ACT 1997 - SECT SECT 900.1 What this Division is about, <

http://www8.austlii.edu.au/cgi-bin/viewdoc/au/legis/cth/consol_act/itaa1997240/s900.1.html>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part 4 – Refer Excel Exhibit

Part 5 – Refer Excel Exhibit

Part 7 – Refer Excel Exhibit

Part 8 – Refer Excel Exhibit

Part 9 – Refer Excel Exhibit

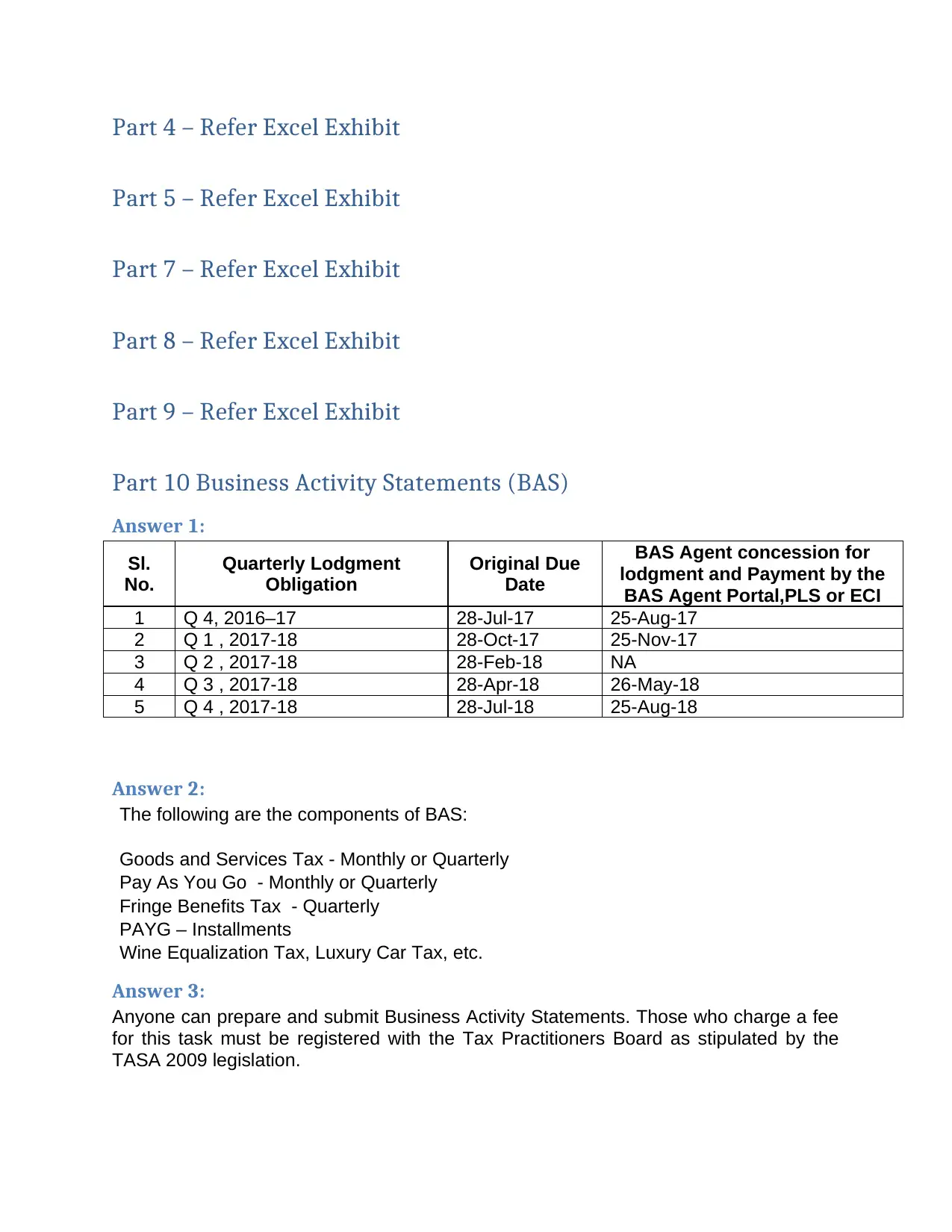

Part 10 Business Activity Statements (BAS)

Answer 1:

Sl.

No.

Quarterly Lodgment

Obligation

Original Due

Date

BAS Agent concession for

lodgment and Payment by the

BAS Agent Portal,PLS or ECI

1 Q 4, 2016–17 28-Jul-17 25-Aug-17

2 Q 1 , 2017-18 28-Oct-17 25-Nov-17

3 Q 2 , 2017-18 28-Feb-18 NA

4 Q 3 , 2017-18 28-Apr-18 26-May-18

5 Q 4 , 2017-18 28-Jul-18 25-Aug-18

Answer 2:

The following are the components of BAS:

Goods and Services Tax - Monthly or Quarterly

Pay As You Go - Monthly or Quarterly

Fringe Benefits Tax - Quarterly

PAYG – Installments

Wine Equalization Tax, Luxury Car Tax, etc.

Answer 3:

Anyone can prepare and submit Business Activity Statements. Those who charge a fee

for this task must be registered with the Tax Practitioners Board as stipulated by the

TASA 2009 legislation.

Part 5 – Refer Excel Exhibit

Part 7 – Refer Excel Exhibit

Part 8 – Refer Excel Exhibit

Part 9 – Refer Excel Exhibit

Part 10 Business Activity Statements (BAS)

Answer 1:

Sl.

No.

Quarterly Lodgment

Obligation

Original Due

Date

BAS Agent concession for

lodgment and Payment by the

BAS Agent Portal,PLS or ECI

1 Q 4, 2016–17 28-Jul-17 25-Aug-17

2 Q 1 , 2017-18 28-Oct-17 25-Nov-17

3 Q 2 , 2017-18 28-Feb-18 NA

4 Q 3 , 2017-18 28-Apr-18 26-May-18

5 Q 4 , 2017-18 28-Jul-18 25-Aug-18

Answer 2:

The following are the components of BAS:

Goods and Services Tax - Monthly or Quarterly

Pay As You Go - Monthly or Quarterly

Fringe Benefits Tax - Quarterly

PAYG – Installments

Wine Equalization Tax, Luxury Car Tax, etc.

Answer 3:

Anyone can prepare and submit Business Activity Statements. Those who charge a fee

for this task must be registered with the Tax Practitioners Board as stipulated by the

TASA 2009 legislation.

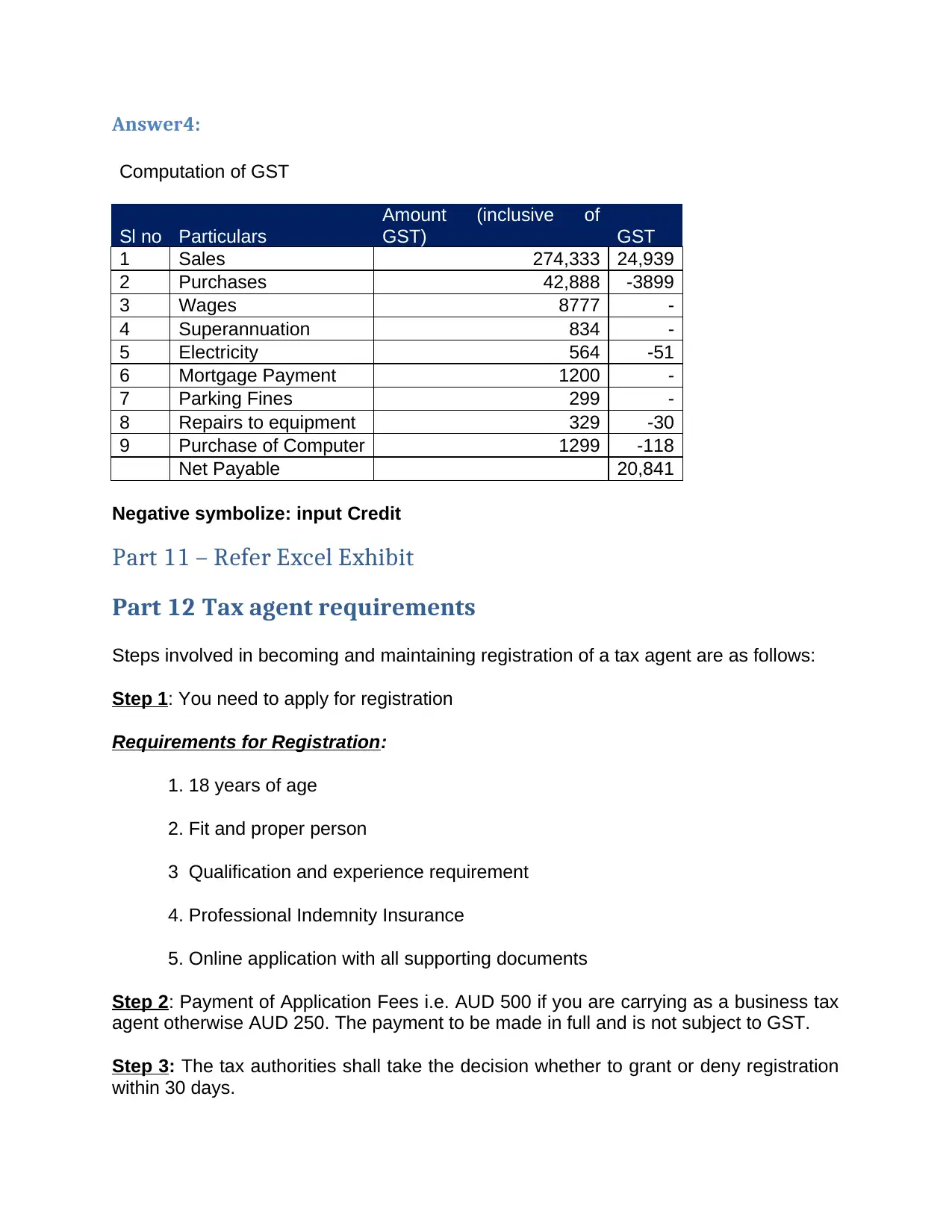

Answer4:

Computation of GST

Sl no Particulars

Amount (inclusive of

GST) GST

1 Sales 274,333 24,939

2 Purchases 42,888 -3899

3 Wages 8777 -

4 Superannuation 834 -

5 Electricity 564 -51

6 Mortgage Payment 1200 -

7 Parking Fines 299 -

8 Repairs to equipment 329 -30

9 Purchase of Computer 1299 -118

Net Payable 20,841

Negative symbolize: input Credit

Part 11 – Refer Excel Exhibit

Part 12 Tax agent requirements

Steps involved in becoming and maintaining registration of a tax agent are as follows:

Step 1: You need to apply for registration

Requirements for Registration:

1. 18 years of age

2. Fit and proper person

3 Qualification and experience requirement

4. Professional Indemnity Insurance

5. Online application with all supporting documents

Step 2: Payment of Application Fees i.e. AUD 500 if you are carrying as a business tax

agent otherwise AUD 250. The payment to be made in full and is not subject to GST.

Step 3: The tax authorities shall take the decision whether to grant or deny registration

within 30 days.

Computation of GST

Sl no Particulars

Amount (inclusive of

GST) GST

1 Sales 274,333 24,939

2 Purchases 42,888 -3899

3 Wages 8777 -

4 Superannuation 834 -

5 Electricity 564 -51

6 Mortgage Payment 1200 -

7 Parking Fines 299 -

8 Repairs to equipment 329 -30

9 Purchase of Computer 1299 -118

Net Payable 20,841

Negative symbolize: input Credit

Part 11 – Refer Excel Exhibit

Part 12 Tax agent requirements

Steps involved in becoming and maintaining registration of a tax agent are as follows:

Step 1: You need to apply for registration

Requirements for Registration:

1. 18 years of age

2. Fit and proper person

3 Qualification and experience requirement

4. Professional Indemnity Insurance

5. Online application with all supporting documents

Step 2: Payment of Application Fees i.e. AUD 500 if you are carrying as a business tax

agent otherwise AUD 250. The payment to be made in full and is not subject to GST.

Step 3: The tax authorities shall take the decision whether to grant or deny registration

within 30 days.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.