Australian Income Tax Law and Practice: Foreigners in Agriculture

VerifiedAdded on 2020/12/18

|10

|2826

|365

Report

AI Summary

This report delves into the Australian income tax landscape, specifically focusing on the taxation of foreigners involved in agricultural businesses. It begins by defining who is considered a foreigner under Australian tax law, outlining the three statutory tests: the domicile test, the 183-day test, and the superannuation test. The report then details the tax treatments that differ for foreigners, including variations in tax rates, capital gains tax, and Goods and Services Tax (GST). It highlights the implications of these treatments, such as the impact on HECS/HELP debts, investments, and existing corporate structures when ceasing tax residency. The report also addresses specific tax concessions available to primary producers in agriculture. The report concludes with recommendations based on the findings. The report provides a detailed overview of how foreign individuals and businesses are taxed within the Australian agricultural sector, covering the relevant legislation, tax rates, and implications for investment decisions.

AUSTRALIAN INCOME

TAXATION LAW AND

PRACTICE

TAXATION LAW AND

PRACTICE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Defining foreigners in Australian Taxation law (including business)....................................1

2. Determining tax treatments which is different for foreigners.................................................2

3. Implications for identified treatments.....................................................................................3

4. Recommendation ....................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

1. Defining foreigners in Australian Taxation law (including business)....................................1

2. Determining tax treatments which is different for foreigners.................................................2

3. Implications for identified treatments.....................................................................................3

4. Recommendation ....................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

The Australian taxation office is Australian government statutory agency along with

collection of principal revenue body for Australian government. It has responsibility for purpose

of administering taxation system of Australian federal, superannuation legislation and other

linked matters. Usually, it is replicated as act, with outcome of revenue as taxes. The present

report is based on the topic of “tax treatment and implications for foreigners investing in

Agricultural businesses in Australia”. It consists of appropriate defination of foreigners,

determining tax treatments along with implications and recommendations for relevant law forms

as well,

MAIN BODY

1. Defining foreigners in Australian Taxation law (including business)

Foreign business person is elaborated as in Foreign Acquisitions and takeover fees

imposition act 2015 to mean any foreign person, with exception of any individual is not

ordinarily resident of Australia and carries business in Australia or anywhere. The foreigners as

per Australian taxation law are considered who does not belong to that particular origin as

Australia. There are three statutory tests, which are necessary to be passed to consider an

individual as foreigner in Australia according to Australian taxation office. These statutory test

are stated below:

Domicile test: It is first statutory test, as any resident of Australia as domicile which is

referred to place i.e. permanent home is in Australia. Unless satisfaction with permanent

place of abode is not inside Australia. In this aspect, permanent does not signify forever

or everlasting but implied with sense of contrasted to transitory or temporary. The place

of abode is replicated as residence, where you sleep at night and live with family. If one

does not have any fixed or habitual place of overseas abode and move from one country

to other. Furthermore, there is constant movement within single country then domicile

test will be cleared then domicile test will state one as Australian resident not as

foreigners (Edge, 2017).

183-day test: It is about presence in Australia for 183 days or more than half income year

with break or continuous then there is possibility for having constructive residence in

Australia. There is requirement for establishing usual place of abode is not in Australia

and absence of intention for taking residence.

1

The Australian taxation office is Australian government statutory agency along with

collection of principal revenue body for Australian government. It has responsibility for purpose

of administering taxation system of Australian federal, superannuation legislation and other

linked matters. Usually, it is replicated as act, with outcome of revenue as taxes. The present

report is based on the topic of “tax treatment and implications for foreigners investing in

Agricultural businesses in Australia”. It consists of appropriate defination of foreigners,

determining tax treatments along with implications and recommendations for relevant law forms

as well,

MAIN BODY

1. Defining foreigners in Australian Taxation law (including business)

Foreign business person is elaborated as in Foreign Acquisitions and takeover fees

imposition act 2015 to mean any foreign person, with exception of any individual is not

ordinarily resident of Australia and carries business in Australia or anywhere. The foreigners as

per Australian taxation law are considered who does not belong to that particular origin as

Australia. There are three statutory tests, which are necessary to be passed to consider an

individual as foreigner in Australia according to Australian taxation office. These statutory test

are stated below:

Domicile test: It is first statutory test, as any resident of Australia as domicile which is

referred to place i.e. permanent home is in Australia. Unless satisfaction with permanent

place of abode is not inside Australia. In this aspect, permanent does not signify forever

or everlasting but implied with sense of contrasted to transitory or temporary. The place

of abode is replicated as residence, where you sleep at night and live with family. If one

does not have any fixed or habitual place of overseas abode and move from one country

to other. Furthermore, there is constant movement within single country then domicile

test will be cleared then domicile test will state one as Australian resident not as

foreigners (Edge, 2017).

183-day test: It is about presence in Australia for 183 days or more than half income year

with break or continuous then there is possibility for having constructive residence in

Australia. There is requirement for establishing usual place of abode is not in Australia

and absence of intention for taking residence.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation test: It has application to employees of Australian government working

at Australian post overseas with members of PSS and CSS schemes and it does not apply

for members of PSSAP scheme (Residency test, 2018).

Thus, if all three test are not satisfied then one is considered as foreigner for Australian

Taxation law. In nutshell, foreigners are one who visit Australia various times and working and

travelling in multiple locations around Australia. In same series, one is either visiting for less

than 6 months and holidaying in Australia and leaving Australia on permanent aspect is

considered as foreigner in agriculture business.

For instance, In the case of Bronwyn as Australian residents has attained job offer for

working overseas for three years along with option for extending it to another three years. In this

aspect, she, children and her husband has decided for making overseas. They had retained

property in Australia with intend to return one day as in their absence, house will be rented. In

this context, Bronwyn is considered as foreigner as per domicile test, as her permanent place of

abode is not in Australia because of establishing home overseas, length of time committed to

spend and family is accompanying here. As per fact is that, she will not sell home in Australia

which is relevant and not persuasive for overcoming the extraction with context of other factors.

Henceforth, it is arguable about abounding her home in Australia and period of stay by renting it.

The 183 day test does not apply with departure date for overseas where superannuation test does

not apply here (Some examples of Australian residents and foreign residents, 2018).

2. Determining tax treatments which is different for foreigners

According to ATO, application of tax rates to taxable income is dependent that whether

one is Australian resident or foreigner. The high rate of tax is applicable to foreigner's taxable

income and not entitled for tax free threshold. There is presence of rules of special capital gains

taxes for foreigners as it will provide impact during selling of residential property in Australia. In

budget of 2017-18, there is announcement of government that foreigners will be not entitled for

claim in exemption of residence for selling property in Australia. This alteration is not referred as

legislation and subject for process of parliament. In case, this law is passed for foreigner with

CGT event for residential property in Australia this might be not entitled for claiming main

residence exemption with application when exemption will be used as reason for difference to

foreign resident capital gains with rate of holding. During lodge of income tax return, there

should be declaration of capital gain in income and claim is possible for crediting foreign

2

at Australian post overseas with members of PSS and CSS schemes and it does not apply

for members of PSSAP scheme (Residency test, 2018).

Thus, if all three test are not satisfied then one is considered as foreigner for Australian

Taxation law. In nutshell, foreigners are one who visit Australia various times and working and

travelling in multiple locations around Australia. In same series, one is either visiting for less

than 6 months and holidaying in Australia and leaving Australia on permanent aspect is

considered as foreigner in agriculture business.

For instance, In the case of Bronwyn as Australian residents has attained job offer for

working overseas for three years along with option for extending it to another three years. In this

aspect, she, children and her husband has decided for making overseas. They had retained

property in Australia with intend to return one day as in their absence, house will be rented. In

this context, Bronwyn is considered as foreigner as per domicile test, as her permanent place of

abode is not in Australia because of establishing home overseas, length of time committed to

spend and family is accompanying here. As per fact is that, she will not sell home in Australia

which is relevant and not persuasive for overcoming the extraction with context of other factors.

Henceforth, it is arguable about abounding her home in Australia and period of stay by renting it.

The 183 day test does not apply with departure date for overseas where superannuation test does

not apply here (Some examples of Australian residents and foreign residents, 2018).

2. Determining tax treatments which is different for foreigners

According to ATO, application of tax rates to taxable income is dependent that whether

one is Australian resident or foreigner. The high rate of tax is applicable to foreigner's taxable

income and not entitled for tax free threshold. There is presence of rules of special capital gains

taxes for foreigners as it will provide impact during selling of residential property in Australia. In

budget of 2017-18, there is announcement of government that foreigners will be not entitled for

claim in exemption of residence for selling property in Australia. This alteration is not referred as

legislation and subject for process of parliament. In case, this law is passed for foreigner with

CGT event for residential property in Australia this might be not entitled for claiming main

residence exemption with application when exemption will be used as reason for difference to

foreign resident capital gains with rate of holding. During lodge of income tax return, there

should be declaration of capital gain in income and claim is possible for crediting foreign

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

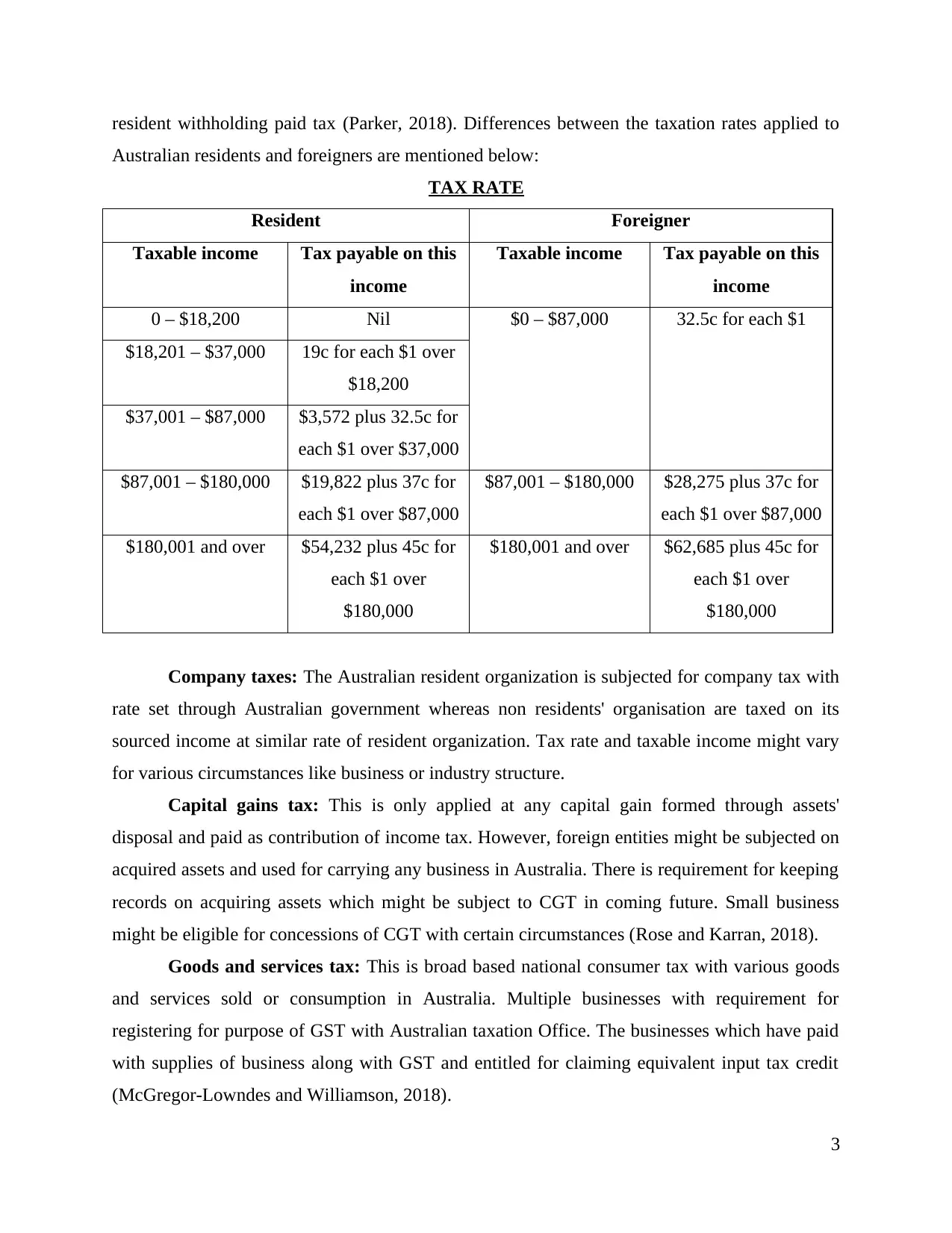

resident withholding paid tax (Parker, 2018). Differences between the taxation rates applied to

Australian residents and foreigners are mentioned below:

TAX RATE

Resident Foreigner

Taxable income Tax payable on this

income

Taxable income Tax payable on this

income

0 – $18,200 Nil $0 – $87,000 32.5c for each $1

$18,201 – $37,000 19c for each $1 over

$18,200

$37,001 – $87,000 $3,572 plus 32.5c for

each $1 over $37,000

$87,001 – $180,000 $19,822 plus 37c for

each $1 over $87,000

$87,001 – $180,000 $28,275 plus 37c for

each $1 over $87,000

$180,001 and over $54,232 plus 45c for

each $1 over

$180,000

$180,001 and over $62,685 plus 45c for

each $1 over

$180,000

Company taxes: The Australian resident organization is subjected for company tax with

rate set through Australian government whereas non residents' organisation are taxed on its

sourced income at similar rate of resident organization. Tax rate and taxable income might vary

for various circumstances like business or industry structure.

Capital gains tax: This is only applied at any capital gain formed through assets'

disposal and paid as contribution of income tax. However, foreign entities might be subjected on

acquired assets and used for carrying any business in Australia. There is requirement for keeping

records on acquiring assets which might be subject to CGT in coming future. Small business

might be eligible for concessions of CGT with certain circumstances (Rose and Karran, 2018).

Goods and services tax: This is broad based national consumer tax with various goods

and services sold or consumption in Australia. Multiple businesses with requirement for

registering for purpose of GST with Australian taxation Office. The businesses which have paid

with supplies of business along with GST and entitled for claiming equivalent input tax credit

(McGregor-Lowndes and Williamson, 2018).

3

Australian residents and foreigners are mentioned below:

TAX RATE

Resident Foreigner

Taxable income Tax payable on this

income

Taxable income Tax payable on this

income

0 – $18,200 Nil $0 – $87,000 32.5c for each $1

$18,201 – $37,000 19c for each $1 over

$18,200

$37,001 – $87,000 $3,572 plus 32.5c for

each $1 over $37,000

$87,001 – $180,000 $19,822 plus 37c for

each $1 over $87,000

$87,001 – $180,000 $28,275 plus 37c for

each $1 over $87,000

$180,001 and over $54,232 plus 45c for

each $1 over

$180,000

$180,001 and over $62,685 plus 45c for

each $1 over

$180,000

Company taxes: The Australian resident organization is subjected for company tax with

rate set through Australian government whereas non residents' organisation are taxed on its

sourced income at similar rate of resident organization. Tax rate and taxable income might vary

for various circumstances like business or industry structure.

Capital gains tax: This is only applied at any capital gain formed through assets'

disposal and paid as contribution of income tax. However, foreign entities might be subjected on

acquired assets and used for carrying any business in Australia. There is requirement for keeping

records on acquiring assets which might be subject to CGT in coming future. Small business

might be eligible for concessions of CGT with certain circumstances (Rose and Karran, 2018).

Goods and services tax: This is broad based national consumer tax with various goods

and services sold or consumption in Australia. Multiple businesses with requirement for

registering for purpose of GST with Australian taxation Office. The businesses which have paid

with supplies of business along with GST and entitled for claiming equivalent input tax credit

(McGregor-Lowndes and Williamson, 2018).

3

There is presence of better tax systems for farmers as averaging income tax if small

businesses with turnover less than $10 million. It comprises primary production for continuing

claim of full deduction for purpose of business assets purchased or installed and helps business

for improving planning and cash flow as well. The ATO helps people affected through drought

and natural disaster through arranging for tax debts must be paid in instalments with absence of

charges of interest. In the same series, allows more time for repaying tax debt with absence of

incurring charges of interest. Furthermore, with special circumstances, commissioner for taxation

might release some individuals for payment through income tax along with fringe benefits and

other taxes is reflected as cause of serious hardship (Taxation measures – Australia, 2019). The

foreigners who invest in agricultural land, will be charged additional charge of 0.5% of its value.

There will be application of additional land tax as rural, agriculture land fees with range of

$5000 to $100000 along with total value of acquisition and thresholds applicable.

3. Implications for identified treatments

The capacity of Australia for tax of non residents might be limited where non-resident is

resident in country where Australia is in Double Taxation Agreements. Usually, it allocates

rights of taxing to country of residence of taxpayer. On the contrary, country of income source

might directly impose withholding taxes on dividends, royalties and interest and also tax in

attributed or actual margin of any commercial enterprise carried by permanent establishment in

country. In this context, Australia has presence of withholding general non-resident tax regime

and taxation of income throughout world is earned through Australian residents might in certain

circumstances provides outcome in issue of double taxation. As Australia has capability for

managing double taxation through tax exemption or foreign tax offset.

There is presence of various tax implications for ceasing tax residency as:

HECS/ HELP and TESL debts: The taxpayers with TSL or HELP debts would be

required for reporting earnings of overseas for making repayments against loans. Furthermore,

assessments would be based on income throughout world for year 2016-17 Australian Income

year and would be directly based on thresholds of current repayment. In the same series,

taxpayers would be required for submitting overseas travel notification to ATO within 7 days of

leaving Australia and appropriate update about contact details while abroad.

Investments: During cease as Australian tax resident, one is deemed for having each

investment which is not Taxable Australian Property. It comprises Australian real property along

4

businesses with turnover less than $10 million. It comprises primary production for continuing

claim of full deduction for purpose of business assets purchased or installed and helps business

for improving planning and cash flow as well. The ATO helps people affected through drought

and natural disaster through arranging for tax debts must be paid in instalments with absence of

charges of interest. In the same series, allows more time for repaying tax debt with absence of

incurring charges of interest. Furthermore, with special circumstances, commissioner for taxation

might release some individuals for payment through income tax along with fringe benefits and

other taxes is reflected as cause of serious hardship (Taxation measures – Australia, 2019). The

foreigners who invest in agricultural land, will be charged additional charge of 0.5% of its value.

There will be application of additional land tax as rural, agriculture land fees with range of

$5000 to $100000 along with total value of acquisition and thresholds applicable.

3. Implications for identified treatments

The capacity of Australia for tax of non residents might be limited where non-resident is

resident in country where Australia is in Double Taxation Agreements. Usually, it allocates

rights of taxing to country of residence of taxpayer. On the contrary, country of income source

might directly impose withholding taxes on dividends, royalties and interest and also tax in

attributed or actual margin of any commercial enterprise carried by permanent establishment in

country. In this context, Australia has presence of withholding general non-resident tax regime

and taxation of income throughout world is earned through Australian residents might in certain

circumstances provides outcome in issue of double taxation. As Australia has capability for

managing double taxation through tax exemption or foreign tax offset.

There is presence of various tax implications for ceasing tax residency as:

HECS/ HELP and TESL debts: The taxpayers with TSL or HELP debts would be

required for reporting earnings of overseas for making repayments against loans. Furthermore,

assessments would be based on income throughout world for year 2016-17 Australian Income

year and would be directly based on thresholds of current repayment. In the same series,

taxpayers would be required for submitting overseas travel notification to ATO within 7 days of

leaving Australia and appropriate update about contact details while abroad.

Investments: During cease as Australian tax resident, one is deemed for having each

investment which is not Taxable Australian Property. It comprises Australian real property along

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with asset for carrying on business via permanent establishment in Australia and indirect interest

in Australian real property with holding of more than 10%. The managed funds, other investment

and shares are not taxable and considered for disposing as of ceased residency date with outcome

of capital gain or loss created on variation among market value of asset at particular time the

taxpayer as foreigner and cost base of asset (Street and et.al., 2017).

This will be outcome in huge unrealised capital gain and in this aspect taxable income is

not necessary with availability for paying tax and no actual sale has taken place. In the same

series, availability of choice where capital gain could be directly disregarded. On the contrary,

choice is made with application of each assets and is disposed as foreigner and gain is not

eligible for discount of CGT along with subject to foreigner tax rates in Australia. Significantly

more tax is payable during election is made for disregarding arisen capital gain for purpose of

ceasing the residency. As the foreigners are not eligible for CGT discount of 50% where this

could be apportioned as per number of working days (A Guide to taxation in Australia, 2019).

Existing corporate structures: In case any taxpayer is trustee or director of trust or

company, there could be multiple implication on status of residency of organization where

individual ceases' residency. Further corporate entity is directly deemed for Australian resident

for purpose of tax as if any central management and resides in Australia has been controlled. If

any trustee if sole director of business unit with consideration of incorporating any aggregate of

resident taxpayer to corporate appropriate register.

Initial place of residence: The foreigners are not exempted through taxes capital gain

during selling of main residence. The function is to subject about existing properties held with

particular date and disposed priory to 30 June 2019. As it signifies timing of crucial sales and

possibilities about some expatriates might be placed better for selling properties with huge

capital gains with little or absence of intention to return.

With context of agriculture business, there are numerous tax concessions with availability

to its primary producers, instead of location or hardship are categorised as tax deductions,

concessional treatment and tax offsets. The tax deductions are related to expenses which are

facilitating earning income and decreases assessable income. It comprises depreciating assets,

horticulture plants, carbon sink forests and forestry managed investment scheme. Concessional

treatment is related to variety of assistance measures for individuals like deferrals of tax liability

5

in Australian real property with holding of more than 10%. The managed funds, other investment

and shares are not taxable and considered for disposing as of ceased residency date with outcome

of capital gain or loss created on variation among market value of asset at particular time the

taxpayer as foreigner and cost base of asset (Street and et.al., 2017).

This will be outcome in huge unrealised capital gain and in this aspect taxable income is

not necessary with availability for paying tax and no actual sale has taken place. In the same

series, availability of choice where capital gain could be directly disregarded. On the contrary,

choice is made with application of each assets and is disposed as foreigner and gain is not

eligible for discount of CGT along with subject to foreigner tax rates in Australia. Significantly

more tax is payable during election is made for disregarding arisen capital gain for purpose of

ceasing the residency. As the foreigners are not eligible for CGT discount of 50% where this

could be apportioned as per number of working days (A Guide to taxation in Australia, 2019).

Existing corporate structures: In case any taxpayer is trustee or director of trust or

company, there could be multiple implication on status of residency of organization where

individual ceases' residency. Further corporate entity is directly deemed for Australian resident

for purpose of tax as if any central management and resides in Australia has been controlled. If

any trustee if sole director of business unit with consideration of incorporating any aggregate of

resident taxpayer to corporate appropriate register.

Initial place of residence: The foreigners are not exempted through taxes capital gain

during selling of main residence. The function is to subject about existing properties held with

particular date and disposed priory to 30 June 2019. As it signifies timing of crucial sales and

possibilities about some expatriates might be placed better for selling properties with huge

capital gains with little or absence of intention to return.

With context of agriculture business, there are numerous tax concessions with availability

to its primary producers, instead of location or hardship are categorised as tax deductions,

concessional treatment and tax offsets. The tax deductions are related to expenses which are

facilitating earning income and decreases assessable income. It comprises depreciating assets,

horticulture plants, carbon sink forests and forestry managed investment scheme. Concessional

treatment is related to variety of assistance measures for individuals like deferrals of tax liability

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps for decreasing assessable income of individual in current financial year. Tax offsets related

to primary producers with application of mechanisms foe decreasing assessable income and to

decrease less tax (Mumford, 2017). As per case Fletcher & Ors v FC or T 91 ATC 4950 has

positive limb with genral deduction provision has need of primary production or professional art

business with income assessable through other sources which is less than $40000 (subtracting

capital gain).

4. Recommendation

The arrangements of capital allowance must be enhanced and streamlined for ensuring

effective rate is higher aspect to match rate of economic depreciation and for decreasing

compliance and administration cost. It comprises allowing assets of low value (<$1000) must be

written off on immediate aspect. Furthermore, impact must be reviewed for special provisions

with application of different investment in statutory effective caps and agriculture along with

other concessional write off provisions. In the same series, for long run, the base of land tax must

be widened to eventually inclusion of all land. With its occurring, the low value land like

agriculture land will not face a land tax liability with below of value per square meter compared

to the lowest rate threshold (Beretta, 2017).

CONCLUSION

From the above study, it had been concluded that taxation differentiated through other

forms of payments like market exchange where taxation does not have need of consent and tied

to rendered service. Legally, it is different as compared to extortion or protection racket due to

imposing institution as government but not private ones. It had shown that Australian taxation is

fully based on self assessment model where all taxpayers are responsible for purpose of lodging

their taxation returns.

6

to primary producers with application of mechanisms foe decreasing assessable income and to

decrease less tax (Mumford, 2017). As per case Fletcher & Ors v FC or T 91 ATC 4950 has

positive limb with genral deduction provision has need of primary production or professional art

business with income assessable through other sources which is less than $40000 (subtracting

capital gain).

4. Recommendation

The arrangements of capital allowance must be enhanced and streamlined for ensuring

effective rate is higher aspect to match rate of economic depreciation and for decreasing

compliance and administration cost. It comprises allowing assets of low value (<$1000) must be

written off on immediate aspect. Furthermore, impact must be reviewed for special provisions

with application of different investment in statutory effective caps and agriculture along with

other concessional write off provisions. In the same series, for long run, the base of land tax must

be widened to eventually inclusion of all land. With its occurring, the low value land like

agriculture land will not face a land tax liability with below of value per square meter compared

to the lowest rate threshold (Beretta, 2017).

CONCLUSION

From the above study, it had been concluded that taxation differentiated through other

forms of payments like market exchange where taxation does not have need of consent and tied

to rendered service. Legally, it is different as compared to extortion or protection racket due to

imposing institution as government but not private ones. It had shown that Australian taxation is

fully based on self assessment model where all taxpayers are responsible for purpose of lodging

their taxation returns.

6

REFERENCES

Books and Journals

Beretta, G. 2017. Taxation of Individuals in the Sharing Economy. Intertax. 45(1). 2-11.

Edge, P. W., 2017. Religion and law: An introduction. Routledge.

McGregor-Lowndes, M., and Williamson, A. 2018. Foundations in Australia: Dimensions for

international comparison.American Behavioral Scientist. 0002764218773495.

Mumford, A. 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Parker, H., 2018. Instead of the Dole: An enquiry into integration of the tax and benefit systems.

Routledge.

Rose, R., and Karran, T. 2018. Taxation by political inertia: Financing the growth of government

in Britain. Routledge.

Street, J. M. and et.al., 2017. Community perspectives on the use of regulation and law for

obesity prevention in children: a citizens’ jury. Health Policy. 121(5). 566-573.

Online

A Guide to taxation in Australia. 2019. [Online]. Available through

<https://hallandwilcox.com.au/a-guide-to-taxation-in-australia/>.

Residency test. 2018. [Online]. Available through

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/Work-out-your-tax-

residency/Residency-tests/>.

Some examples of Australian residents and foreign residents. 2018.

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/Residency/

Examples-of-residents-and-foreign-residents/>.

Taxation measures – Australia. 2019. [Online]. Available through

<http://www.agriculture.gov.au/ag-farm-food/drought/assistance/tax-relief>.

7

Books and Journals

Beretta, G. 2017. Taxation of Individuals in the Sharing Economy. Intertax. 45(1). 2-11.

Edge, P. W., 2017. Religion and law: An introduction. Routledge.

McGregor-Lowndes, M., and Williamson, A. 2018. Foundations in Australia: Dimensions for

international comparison.American Behavioral Scientist. 0002764218773495.

Mumford, A. 2017. Taxing culture: towards a theory of tax collection law. Routledge.

Parker, H., 2018. Instead of the Dole: An enquiry into integration of the tax and benefit systems.

Routledge.

Rose, R., and Karran, T. 2018. Taxation by political inertia: Financing the growth of government

in Britain. Routledge.

Street, J. M. and et.al., 2017. Community perspectives on the use of regulation and law for

obesity prevention in children: a citizens’ jury. Health Policy. 121(5). 566-573.

Online

A Guide to taxation in Australia. 2019. [Online]. Available through

<https://hallandwilcox.com.au/a-guide-to-taxation-in-australia/>.

Residency test. 2018. [Online]. Available through

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/Work-out-your-tax-

residency/Residency-tests/>.

Some examples of Australian residents and foreign residents. 2018.

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/In-detail/Residency/

Examples-of-residents-and-foreign-residents/>.

Taxation measures – Australia. 2019. [Online]. Available through

<http://www.agriculture.gov.au/ag-farm-food/drought/assistance/tax-relief>.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.