Calculating Taxable Income: Redoubt Pty Ltd & Small Business Rules

VerifiedAdded on 2023/04/20

|12

|2687

|364

Homework Assignment

AI Summary

This assignment provides a detailed analysis of Australian taxation principles, focusing on the calculation of taxable income for entities like Redoubt Pty Ltd. It covers topics such as small business entity simplified trading rules, depreciation methods, and the treatment of prepaid expenses. The document also addresses the offsetting of losses, trust income distribution, and capital gains tax concessions available to small businesses. Furthermore, it discusses the GST implications when selling a business as a going concern, providing a comprehensive overview of key aspects of Australian tax law relevant to businesses and individuals. Desklib offers a range of solved assignments and study resources for students.

Australian tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Question 3........................................................................................................................................6

Question 4........................................................................................................................................7

Question 5........................................................................................................................................8

Question 6........................................................................................................................................8

Question 7........................................................................................................................................9

References......................................................................................................................................10

Question 1........................................................................................................................................3

Question 2........................................................................................................................................5

Question 3........................................................................................................................................6

Question 4........................................................................................................................................7

Question 5........................................................................................................................................8

Question 6........................................................................................................................................8

Question 7........................................................................................................................................9

References......................................................................................................................................10

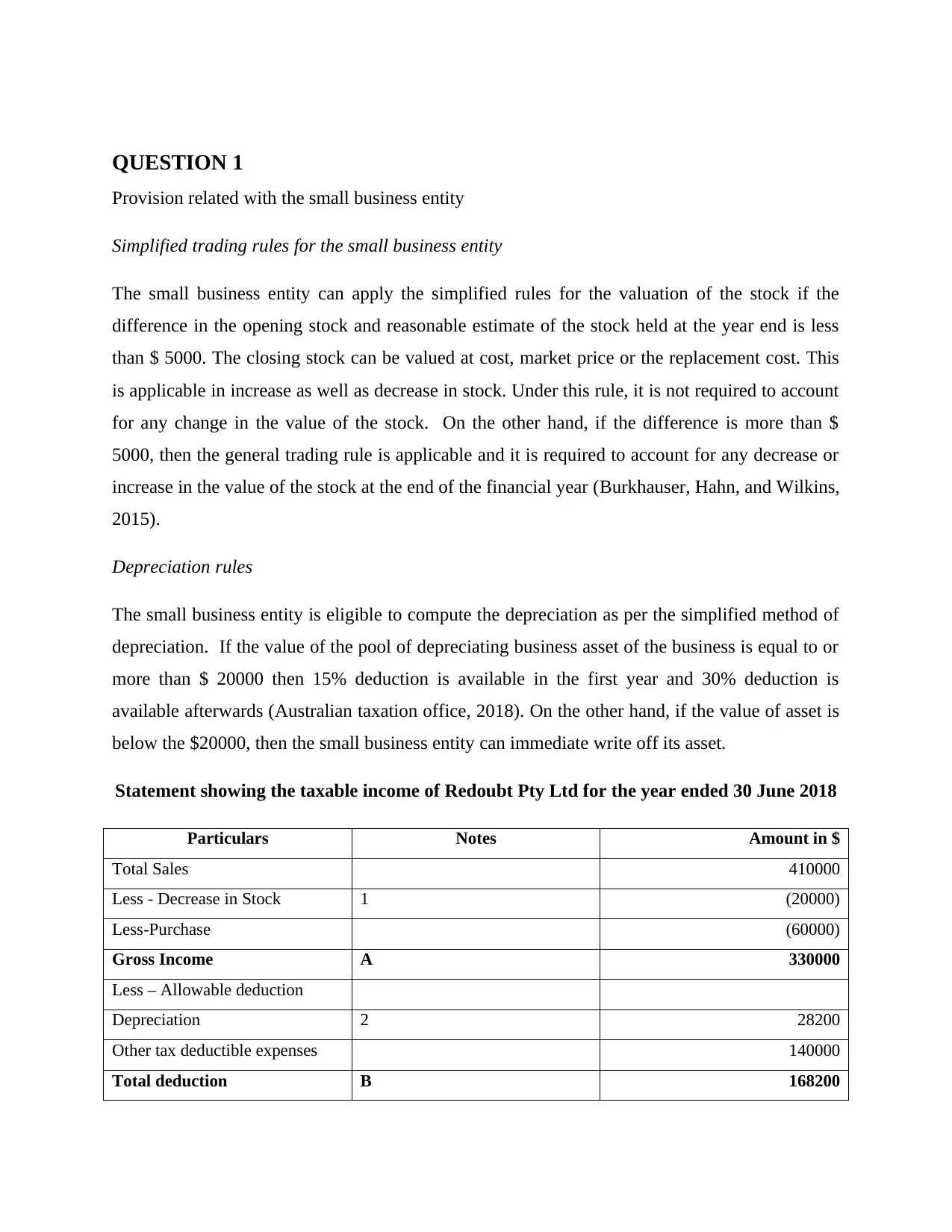

QUESTION 1

Provision related with the small business entity

Simplified trading rules for the small business entity

The small business entity can apply the simplified rules for the valuation of the stock if the

difference in the opening stock and reasonable estimate of the stock held at the year end is less

than $ 5000. The closing stock can be valued at cost, market price or the replacement cost. This

is applicable in increase as well as decrease in stock. Under this rule, it is not required to account

for any change in the value of the stock. On the other hand, if the difference is more than $

5000, then the general trading rule is applicable and it is required to account for any decrease or

increase in the value of the stock at the end of the financial year (Burkhauser, Hahn, and Wilkins,

2015).

Depreciation rules

The small business entity is eligible to compute the depreciation as per the simplified method of

depreciation. If the value of the pool of depreciating business asset of the business is equal to or

more than $ 20000 then 15% deduction is available in the first year and 30% deduction is

available afterwards (Australian taxation office, 2018). On the other hand, if the value of asset is

below the $20000, then the small business entity can immediate write off its asset.

Statement showing the taxable income of Redoubt Pty Ltd for the year ended 30 June 2018

Particulars Notes Amount in $

Total Sales 410000

Less - Decrease in Stock 1 (20000)

Less-Purchase (60000)

Gross Income A 330000

Less – Allowable deduction

Depreciation 2 28200

Other tax deductible expenses 140000

Total deduction B 168200

Provision related with the small business entity

Simplified trading rules for the small business entity

The small business entity can apply the simplified rules for the valuation of the stock if the

difference in the opening stock and reasonable estimate of the stock held at the year end is less

than $ 5000. The closing stock can be valued at cost, market price or the replacement cost. This

is applicable in increase as well as decrease in stock. Under this rule, it is not required to account

for any change in the value of the stock. On the other hand, if the difference is more than $

5000, then the general trading rule is applicable and it is required to account for any decrease or

increase in the value of the stock at the end of the financial year (Burkhauser, Hahn, and Wilkins,

2015).

Depreciation rules

The small business entity is eligible to compute the depreciation as per the simplified method of

depreciation. If the value of the pool of depreciating business asset of the business is equal to or

more than $ 20000 then 15% deduction is available in the first year and 30% deduction is

available afterwards (Australian taxation office, 2018). On the other hand, if the value of asset is

below the $20000, then the small business entity can immediate write off its asset.

Statement showing the taxable income of Redoubt Pty Ltd for the year ended 30 June 2018

Particulars Notes Amount in $

Total Sales 410000

Less - Decrease in Stock 1 (20000)

Less-Purchase (60000)

Gross Income A 330000

Less – Allowable deduction

Depreciation 2 28200

Other tax deductible expenses 140000

Total deduction B 168200

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

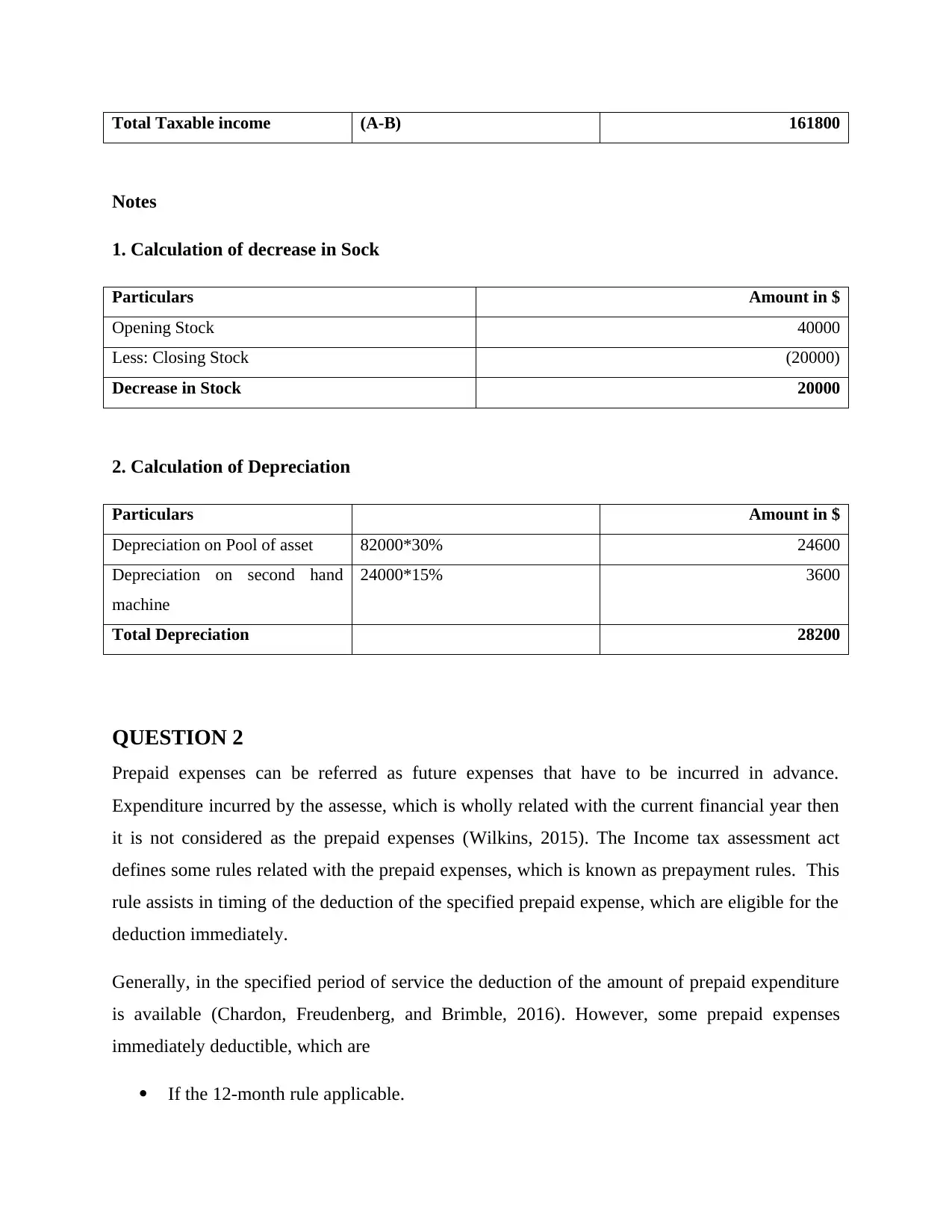

Total Taxable income (A-B) 161800

Notes

1. Calculation of decrease in Sock

Particulars Amount in $

Opening Stock 40000

Less: Closing Stock (20000)

Decrease in Stock 20000

2. Calculation of Depreciation

Particulars Amount in $

Depreciation on Pool of asset 82000*30% 24600

Depreciation on second hand

machine

24000*15% 3600

Total Depreciation 28200

QUESTION 2

Prepaid expenses can be referred as future expenses that have to be incurred in advance.

Expenditure incurred by the assesse, which is wholly related with the current financial year then

it is not considered as the prepaid expenses (Wilkins, 2015). The Income tax assessment act

defines some rules related with the prepaid expenses, which is known as prepayment rules. This

rule assists in timing of the deduction of the specified prepaid expense, which are eligible for the

deduction immediately.

Generally, in the specified period of service the deduction of the amount of prepaid expenditure

is available (Chardon, Freudenberg, and Brimble, 2016). However, some prepaid expenses

immediately deductible, which are

If the 12-month rule applicable.

Notes

1. Calculation of decrease in Sock

Particulars Amount in $

Opening Stock 40000

Less: Closing Stock (20000)

Decrease in Stock 20000

2. Calculation of Depreciation

Particulars Amount in $

Depreciation on Pool of asset 82000*30% 24600

Depreciation on second hand

machine

24000*15% 3600

Total Depreciation 28200

QUESTION 2

Prepaid expenses can be referred as future expenses that have to be incurred in advance.

Expenditure incurred by the assesse, which is wholly related with the current financial year then

it is not considered as the prepaid expenses (Wilkins, 2015). The Income tax assessment act

defines some rules related with the prepaid expenses, which is known as prepayment rules. This

rule assists in timing of the deduction of the specified prepaid expense, which are eligible for the

deduction immediately.

Generally, in the specified period of service the deduction of the amount of prepaid expenditure

is available (Chardon, Freudenberg, and Brimble, 2016). However, some prepaid expenses

immediately deductible, which are

If the 12-month rule applicable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

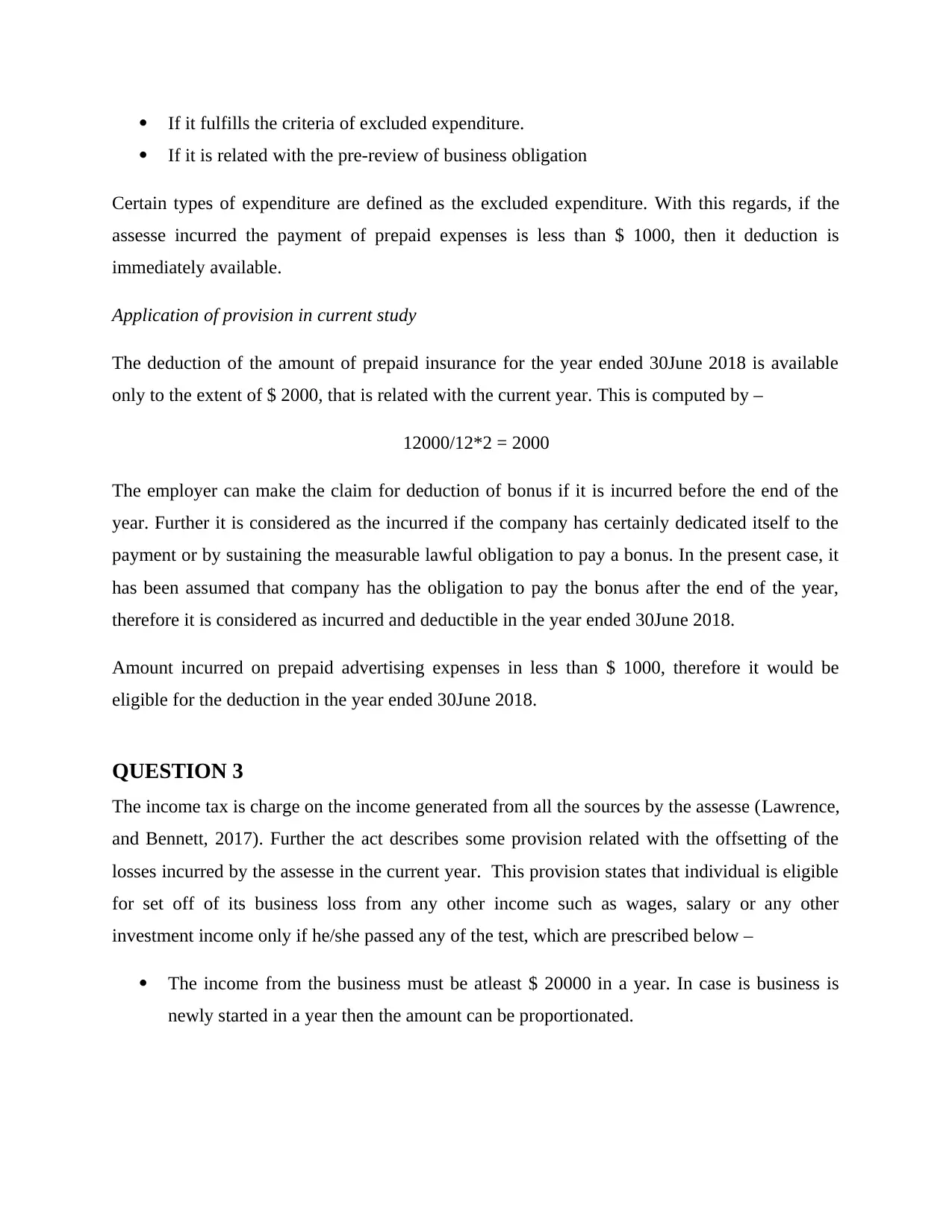

If it fulfills the criteria of excluded expenditure.

If it is related with the pre-review of business obligation

Certain types of expenditure are defined as the excluded expenditure. With this regards, if the

assesse incurred the payment of prepaid expenses is less than $ 1000, then it deduction is

immediately available.

Application of provision in current study

The deduction of the amount of prepaid insurance for the year ended 30June 2018 is available

only to the extent of $ 2000, that is related with the current year. This is computed by –

12000/12*2 = 2000

The employer can make the claim for deduction of bonus if it is incurred before the end of the

year. Further it is considered as the incurred if the company has certainly dedicated itself to the

payment or by sustaining the measurable lawful obligation to pay a bonus. In the present case, it

has been assumed that company has the obligation to pay the bonus after the end of the year,

therefore it is considered as incurred and deductible in the year ended 30June 2018.

Amount incurred on prepaid advertising expenses in less than $ 1000, therefore it would be

eligible for the deduction in the year ended 30June 2018.

QUESTION 3

The income tax is charge on the income generated from all the sources by the assesse (Lawrence,

and Bennett, 2017). Further the act describes some provision related with the offsetting of the

losses incurred by the assesse in the current year. This provision states that individual is eligible

for set off of its business loss from any other income such as wages, salary or any other

investment income only if he/she passed any of the test, which are prescribed below –

The income from the business must be atleast $ 20000 in a year. In case is business is

newly started in a year then the amount can be proportionated.

If it is related with the pre-review of business obligation

Certain types of expenditure are defined as the excluded expenditure. With this regards, if the

assesse incurred the payment of prepaid expenses is less than $ 1000, then it deduction is

immediately available.

Application of provision in current study

The deduction of the amount of prepaid insurance for the year ended 30June 2018 is available

only to the extent of $ 2000, that is related with the current year. This is computed by –

12000/12*2 = 2000

The employer can make the claim for deduction of bonus if it is incurred before the end of the

year. Further it is considered as the incurred if the company has certainly dedicated itself to the

payment or by sustaining the measurable lawful obligation to pay a bonus. In the present case, it

has been assumed that company has the obligation to pay the bonus after the end of the year,

therefore it is considered as incurred and deductible in the year ended 30June 2018.

Amount incurred on prepaid advertising expenses in less than $ 1000, therefore it would be

eligible for the deduction in the year ended 30June 2018.

QUESTION 3

The income tax is charge on the income generated from all the sources by the assesse (Lawrence,

and Bennett, 2017). Further the act describes some provision related with the offsetting of the

losses incurred by the assesse in the current year. This provision states that individual is eligible

for set off of its business loss from any other income such as wages, salary or any other

investment income only if he/she passed any of the test, which are prescribed below –

The income from the business must be atleast $ 20000 in a year. In case is business is

newly started in a year then the amount can be proportionated.

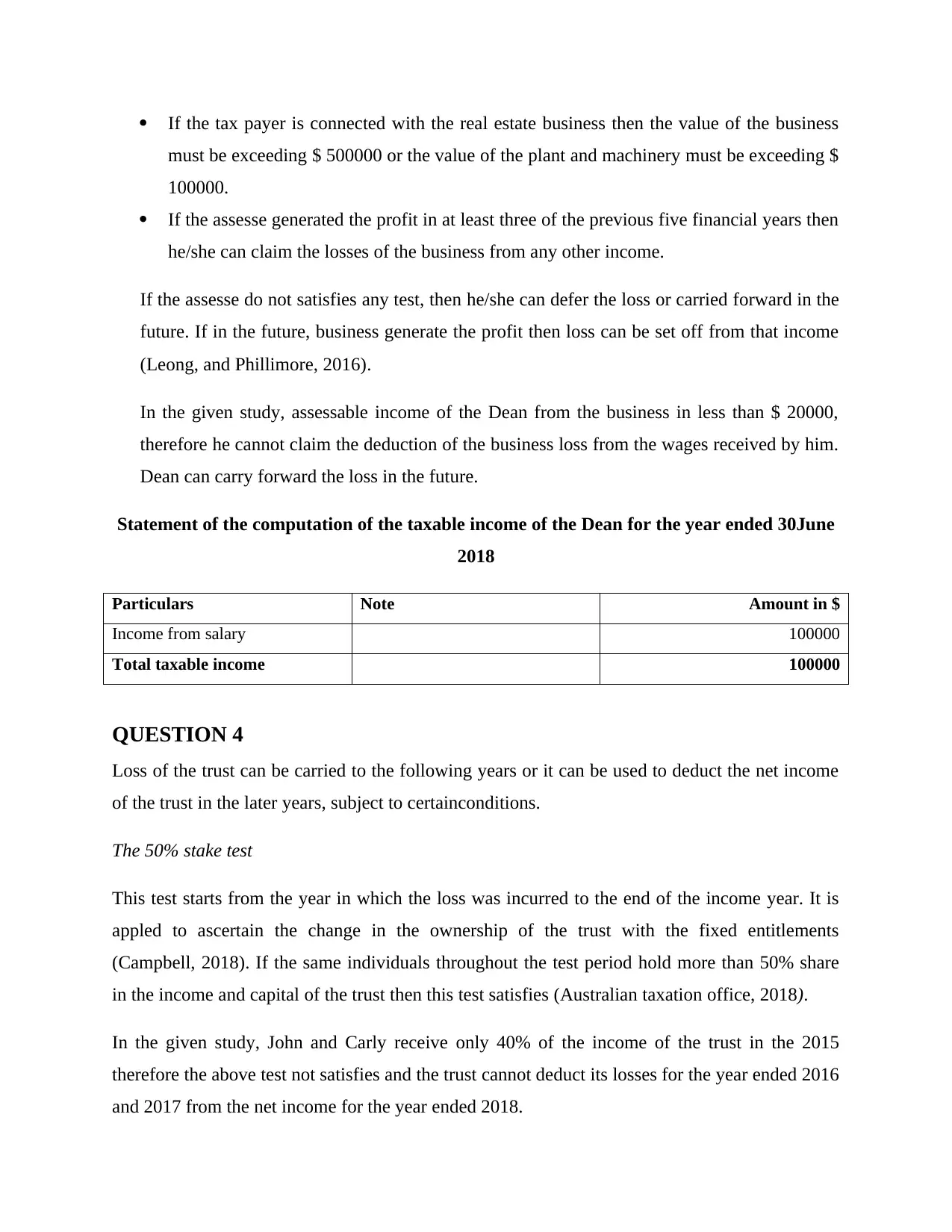

If the tax payer is connected with the real estate business then the value of the business

must be exceeding $ 500000 or the value of the plant and machinery must be exceeding $

100000.

If the assesse generated the profit in at least three of the previous five financial years then

he/she can claim the losses of the business from any other income.

If the assesse do not satisfies any test, then he/she can defer the loss or carried forward in the

future. If in the future, business generate the profit then loss can be set off from that income

(Leong, and Phillimore, 2016).

In the given study, assessable income of the Dean from the business in less than $ 20000,

therefore he cannot claim the deduction of the business loss from the wages received by him.

Dean can carry forward the loss in the future.

Statement of the computation of the taxable income of the Dean for the year ended 30June

2018

Particulars Note Amount in $

Income from salary 100000

Total taxable income 100000

QUESTION 4

Loss of the trust can be carried to the following years or it can be used to deduct the net income

of the trust in the later years, subject to certainconditions.

The 50% stake test

This test starts from the year in which the loss was incurred to the end of the income year. It is

appled to ascertain the change in the ownership of the trust with the fixed entitlements

(Campbell, 2018). If the same individuals throughout the test period hold more than 50% share

in the income and capital of the trust then this test satisfies (Australian taxation office, 2018).

In the given study, John and Carly receive only 40% of the income of the trust in the 2015

therefore the above test not satisfies and the trust cannot deduct its losses for the year ended 2016

and 2017 from the net income for the year ended 2018.

must be exceeding $ 500000 or the value of the plant and machinery must be exceeding $

100000.

If the assesse generated the profit in at least three of the previous five financial years then

he/she can claim the losses of the business from any other income.

If the assesse do not satisfies any test, then he/she can defer the loss or carried forward in the

future. If in the future, business generate the profit then loss can be set off from that income

(Leong, and Phillimore, 2016).

In the given study, assessable income of the Dean from the business in less than $ 20000,

therefore he cannot claim the deduction of the business loss from the wages received by him.

Dean can carry forward the loss in the future.

Statement of the computation of the taxable income of the Dean for the year ended 30June

2018

Particulars Note Amount in $

Income from salary 100000

Total taxable income 100000

QUESTION 4

Loss of the trust can be carried to the following years or it can be used to deduct the net income

of the trust in the later years, subject to certainconditions.

The 50% stake test

This test starts from the year in which the loss was incurred to the end of the income year. It is

appled to ascertain the change in the ownership of the trust with the fixed entitlements

(Campbell, 2018). If the same individuals throughout the test period hold more than 50% share

in the income and capital of the trust then this test satisfies (Australian taxation office, 2018).

In the given study, John and Carly receive only 40% of the income of the trust in the 2015

therefore the above test not satisfies and the trust cannot deduct its losses for the year ended 2016

and 2017 from the net income for the year ended 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 5

In the present study the purchase price is comprised with the three element such as trading stock,

depreciable asset and business goodwill. At the time of computation of the assessable income the

assesse can avail the deduction for the amount paid for purchasing the trading stock. Further on

the depreciable asset the deduction is available with respect to the depreciation. Since the Brian

is small business entity therefore he can claim the depreciation at the rate 30% in the first year

and 15% from the second year onwards. Further there is no deduction available with respect to

the acquisition of the goodwill.

QUESTION 6

If the assesse is the sole trader, conduct a business for the part or whole of the income year and

has an aggregate turnover from the business less than $ 10 Million then it is considered as the

small business entity as per the income tax of the Australia (Wild, 2018). In the given study, it

has been observed that the annual turnover of the Bob is less than $ 10 Million, therefore he can

avail the benefit and concession of the small business entity.

Further, if the net asset value owned by the assesse is less than $ 6 Million just before the capital

gain tax event, then capital gain tax concession is available to the assesse. In ascertaining the net

value of the asset, the assets owned by the assesse and assets owned by any entities related with

assesse is included. Further the capital gain tax asset is not only limited with the business assets.

Moreover if the residence is used for the business purpose, then the market value is included in

the net asset value to the extent it is used for generating the income. Along with this, if there is

any debt which is legally enforceable or any present obligation of the assesse then it is also

considered at the time of determination of the value of net asset. However, the liability must be

related with the asset of the business.

Computation of the net asset value for Bob

Particulars Amount in $

Plant and Machinery 500000

Goodwill 2000000

Building 4000000

In the present study the purchase price is comprised with the three element such as trading stock,

depreciable asset and business goodwill. At the time of computation of the assessable income the

assesse can avail the deduction for the amount paid for purchasing the trading stock. Further on

the depreciable asset the deduction is available with respect to the depreciation. Since the Brian

is small business entity therefore he can claim the depreciation at the rate 30% in the first year

and 15% from the second year onwards. Further there is no deduction available with respect to

the acquisition of the goodwill.

QUESTION 6

If the assesse is the sole trader, conduct a business for the part or whole of the income year and

has an aggregate turnover from the business less than $ 10 Million then it is considered as the

small business entity as per the income tax of the Australia (Wild, 2018). In the given study, it

has been observed that the annual turnover of the Bob is less than $ 10 Million, therefore he can

avail the benefit and concession of the small business entity.

Further, if the net asset value owned by the assesse is less than $ 6 Million just before the capital

gain tax event, then capital gain tax concession is available to the assesse. In ascertaining the net

value of the asset, the assets owned by the assesse and assets owned by any entities related with

assesse is included. Further the capital gain tax asset is not only limited with the business assets.

Moreover if the residence is used for the business purpose, then the market value is included in

the net asset value to the extent it is used for generating the income. Along with this, if there is

any debt which is legally enforceable or any present obligation of the assesse then it is also

considered at the time of determination of the value of net asset. However, the liability must be

related with the asset of the business.

Computation of the net asset value for Bob

Particulars Amount in $

Plant and Machinery 500000

Goodwill 2000000

Building 4000000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

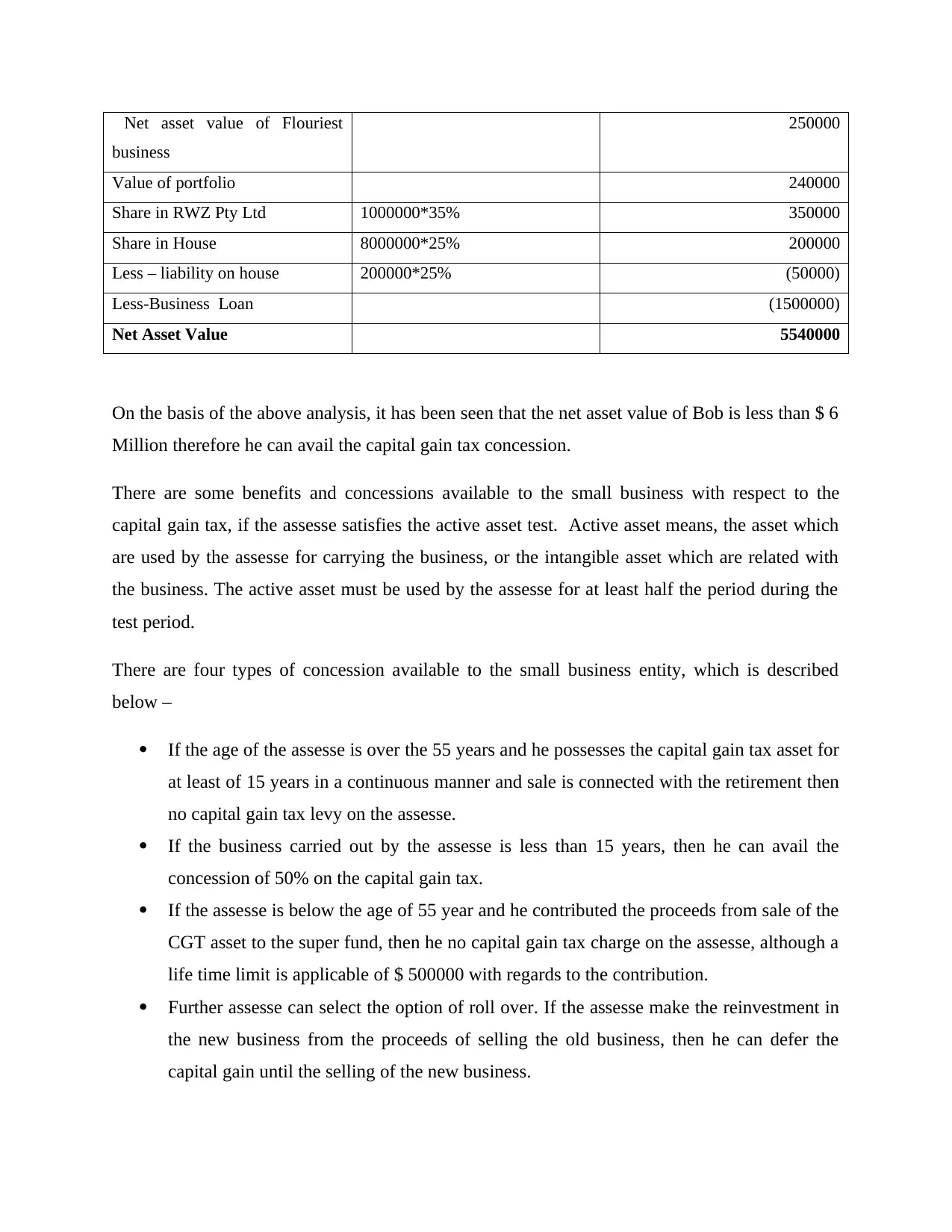

Net asset value of Flouriest

business

250000

Value of portfolio 240000

Share in RWZ Pty Ltd 1000000*35% 350000

Share in House 8000000*25% 200000

Less – liability on house 200000*25% (50000)

Less-Business Loan (1500000)

Net Asset Value 5540000

On the basis of the above analysis, it has been seen that the net asset value of Bob is less than $ 6

Million therefore he can avail the capital gain tax concession.

There are some benefits and concessions available to the small business with respect to the

capital gain tax, if the assesse satisfies the active asset test. Active asset means, the asset which

are used by the assesse for carrying the business, or the intangible asset which are related with

the business. The active asset must be used by the assesse for at least half the period during the

test period.

There are four types of concession available to the small business entity, which is described

below –

If the age of the assesse is over the 55 years and he possesses the capital gain tax asset for

at least of 15 years in a continuous manner and sale is connected with the retirement then

no capital gain tax levy on the assesse.

If the business carried out by the assesse is less than 15 years, then he can avail the

concession of 50% on the capital gain tax.

If the assesse is below the age of 55 year and he contributed the proceeds from sale of the

CGT asset to the super fund, then he no capital gain tax charge on the assesse, although a

life time limit is applicable of $ 500000 with regards to the contribution.

Further assesse can select the option of roll over. If the assesse make the reinvestment in

the new business from the proceeds of selling the old business, then he can defer the

capital gain until the selling of the new business.

business

250000

Value of portfolio 240000

Share in RWZ Pty Ltd 1000000*35% 350000

Share in House 8000000*25% 200000

Less – liability on house 200000*25% (50000)

Less-Business Loan (1500000)

Net Asset Value 5540000

On the basis of the above analysis, it has been seen that the net asset value of Bob is less than $ 6

Million therefore he can avail the capital gain tax concession.

There are some benefits and concessions available to the small business with respect to the

capital gain tax, if the assesse satisfies the active asset test. Active asset means, the asset which

are used by the assesse for carrying the business, or the intangible asset which are related with

the business. The active asset must be used by the assesse for at least half the period during the

test period.

There are four types of concession available to the small business entity, which is described

below –

If the age of the assesse is over the 55 years and he possesses the capital gain tax asset for

at least of 15 years in a continuous manner and sale is connected with the retirement then

no capital gain tax levy on the assesse.

If the business carried out by the assesse is less than 15 years, then he can avail the

concession of 50% on the capital gain tax.

If the assesse is below the age of 55 year and he contributed the proceeds from sale of the

CGT asset to the super fund, then he no capital gain tax charge on the assesse, although a

life time limit is applicable of $ 500000 with regards to the contribution.

Further assesse can select the option of roll over. If the assesse make the reinvestment in

the new business from the proceeds of selling the old business, then he can defer the

capital gain until the selling of the new business.

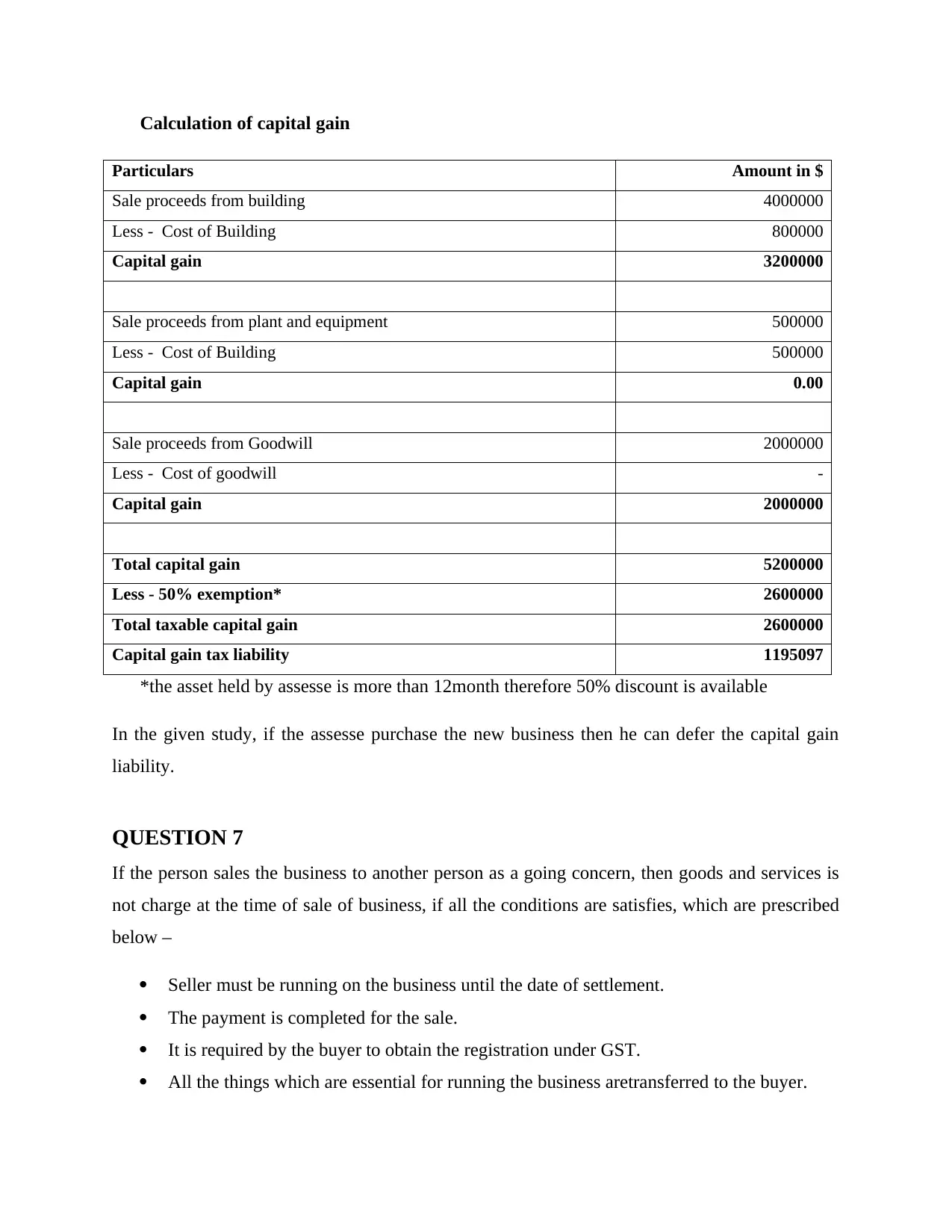

Calculation of capital gain

Particulars Amount in $

Sale proceeds from building 4000000

Less - Cost of Building 800000

Capital gain 3200000

Sale proceeds from plant and equipment 500000

Less - Cost of Building 500000

Capital gain 0.00

Sale proceeds from Goodwill 2000000

Less - Cost of goodwill -

Capital gain 2000000

Total capital gain 5200000

Less - 50% exemption* 2600000

Total taxable capital gain 2600000

Capital gain tax liability 1195097

*the asset held by assesse is more than 12month therefore 50% discount is available

In the given study, if the assesse purchase the new business then he can defer the capital gain

liability.

QUESTION 7

If the person sales the business to another person as a going concern, then goods and services is

not charge at the time of sale of business, if all the conditions are satisfies, which are prescribed

below –

Seller must be running on the business until the date of settlement.

The payment is completed for the sale.

It is required by the buyer to obtain the registration under GST.

All the things which are essential for running the business aretransferred to the buyer.

Particulars Amount in $

Sale proceeds from building 4000000

Less - Cost of Building 800000

Capital gain 3200000

Sale proceeds from plant and equipment 500000

Less - Cost of Building 500000

Capital gain 0.00

Sale proceeds from Goodwill 2000000

Less - Cost of goodwill -

Capital gain 2000000

Total capital gain 5200000

Less - 50% exemption* 2600000

Total taxable capital gain 2600000

Capital gain tax liability 1195097

*the asset held by assesse is more than 12month therefore 50% discount is available

In the given study, if the assesse purchase the new business then he can defer the capital gain

liability.

QUESTION 7

If the person sales the business to another person as a going concern, then goods and services is

not charge at the time of sale of business, if all the conditions are satisfies, which are prescribed

below –

Seller must be running on the business until the date of settlement.

The payment is completed for the sale.

It is required by the buyer to obtain the registration under GST.

All the things which are essential for running the business aretransferred to the buyer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Both, buyer and seller agree in writing that the sale is on the going concern basis. The

agreement must be completed before the sale taken place (Garg,& et.al 2018).

However if the supplier temporary shut dawn business for some of business activities such

as repair, renovation, then it does not lead to violate the above rule (Cassidy, 2017). In the

present study, Val decided to temporary shut dawn the business for the 3 month before the

settlement date for holiday, therefore the GST on the sale of hotel business is levy because it

is essential that business must be carried by the supplier until the date of supply.

agreement must be completed before the sale taken place (Garg,& et.al 2018).

However if the supplier temporary shut dawn business for some of business activities such

as repair, renovation, then it does not lead to violate the above rule (Cassidy, 2017). In the

present study, Val decided to temporary shut dawn the business for the 3 month before the

settlement date for holiday, therefore the GST on the sale of hotel business is levy because it

is essential that business must be carried by the supplier until the date of supply.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 2. Taxation in

Australia, 53(6), p.322.

Cassidy, J., 2017, January. A GST with GRRRRRR: Legislative responses to GST tax avoidance

in Australia and New Zealand. In Australasian Tax Teachers Association Conference 2017.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Garg, K., Chawla, M., Chawla, C. and Taneja, S., 2018. Impact of goods and services tax on

business. International Journal of Education and Management Studies, 8(2), pp.312-314.

Lawrence, S. and Bennett, M., 2017. Image rights in Australia: Fair game or foul ball?. Taxation

in Australia, 51(9), p.487.

Leong, K. and Phillimore, J., 2016. Economic diversification in Australia.In Economic

Diversification Policies in Natural Resource Rich Economies (pp. 164-190).Routledge.

Wild, D., 2018.Time for a tax revolution. Institute of Public Affairs Review: A Quarterly Review

of Politics and Public Affairs, The, 70(1), p.28.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

Online

Australian taxation office, 2018(online).Available Through

<https://www.ato.gov.au/General/Trusts/In-detail/Losses/Trust-loss-provisions>Assessed on [ 7

February 2018]

Books and Journals

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Campbell, S., 2018. Personal liability of a trustee to tax on trust income: Part 2. Taxation in

Australia, 53(6), p.322.

Cassidy, J., 2017, January. A GST with GRRRRRR: Legislative responses to GST tax avoidance

in Australia and New Zealand. In Australasian Tax Teachers Association Conference 2017.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Garg, K., Chawla, M., Chawla, C. and Taneja, S., 2018. Impact of goods and services tax on

business. International Journal of Education and Management Studies, 8(2), pp.312-314.

Lawrence, S. and Bennett, M., 2017. Image rights in Australia: Fair game or foul ball?. Taxation

in Australia, 51(9), p.487.

Leong, K. and Phillimore, J., 2016. Economic diversification in Australia.In Economic

Diversification Policies in Natural Resource Rich Economies (pp. 164-190).Routledge.

Wild, D., 2018.Time for a tax revolution. Institute of Public Affairs Review: A Quarterly Review

of Politics and Public Affairs, The, 70(1), p.28.

Wilkins, R., 2015. Measuring income inequality in Australia. Australian Economic

Review, 48(1), pp.93-102.

Online

Australian taxation office, 2018(online).Available Through

<https://www.ato.gov.au/General/Trusts/In-detail/Losses/Trust-loss-provisions>Assessed on [ 7

February 2018]

Australian taxation office, 2018(online).Available Through

<https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/General-

depreciation-rules---capital-allowances/>Assessed on [ 7 February 2018]

<https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/General-

depreciation-rules---capital-allowances/>Assessed on [ 7 February 2018]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.