Analysis of Australian Tax System: Problems and Government Plans

VerifiedAdded on 2022/11/01

|15

|3412

|69

Report

AI Summary

This report analyzes the Australian tax system, identifying key issues and challenges. It begins by defining taxation and its significance in Australia, highlighting the country's relatively low tax liability compared to other developed nations. The report then outlines various forms of taxation, including personal income tax, capital gains tax, corporate taxes, and GST, among others. It delves into specific taxation issues, such as those related to superannuation, trusts, general business taxes, and income tax, noting public dissatisfaction and areas of complexity. The report further explores the current tax laws in Australia, covering residency, origin, and dual tax agreements. It also discusses perceived weaknesses in the current law, such as high corporate tax rates and the need for tax reforms. Finally, it examines the government's proposed solutions and potential changes to address these issues, considering lobby efforts and expert opinions. The report concludes with a discussion of the implications of these issues and provides recommendations for improvement.

Contents

“AUSTRALIA IS IN TROUBLE. THE PLAN TO FIX THE TAX SYSTEM”...............................................................1

TAXATION ISSUE OF AUSTRALIA:.............................................................................................................2

“WHAT IS THE CURRENT LAW?”..............................................................................................................3

“PERCEIVED WEAKNESS OF THE CURRENT LAW”....................................................................................4

“HOW THE GOVERNMENT PROPOSES TO ADDRESS THEM?”..................................................................5

“MY VIEWS ON ADDRESSING THE ISSUE”................................................................................................5

REFERENCES-...............................................................................................................................................6

“AUSTRALIA IS IN TROUBLE. THE PLAN TO FIX THE TAX SYSTEM”...............................................................1

TAXATION ISSUE OF AUSTRALIA:.............................................................................................................2

“WHAT IS THE CURRENT LAW?”..............................................................................................................3

“PERCEIVED WEAKNESS OF THE CURRENT LAW”....................................................................................4

“HOW THE GOVERNMENT PROPOSES TO ADDRESS THEM?”..................................................................5

“MY VIEWS ON ADDRESSING THE ISSUE”................................................................................................5

REFERENCES-...............................................................................................................................................6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

“AUSTRALIA IS IN TROUBLE. THE PLAN TO FIX THE TAX SYSTEM”

A tax is a mandatory monetary fee or some form of tariff enforced by a federal agency on a taxpayer to

finance multiple public spending. Refusing to pay, together with evading taxes or objection, is illegal.

Income taxes are Australia's most important type of revenue and are gathered via the Australian

Taxation Department by the state. Australian GST income is gathered by the Administration and then

given by the Commonwealth Grants Commission to the Regions through an allocation scheme.

Compared to other rich, advanced countries, Australia retains a comparatively small tax liability at 27.8%

of GDP in 2018 (Economywatch, 2019).

Forms of taxes collected both by State and National Government:

A tax is a mandatory monetary fee or some form of tariff enforced by a federal agency on a taxpayer to

finance multiple public spending. Refusing to pay, together with evading taxes or objection, is illegal.

Income taxes are Australia's most important type of revenue and are gathered via the Australian

Taxation Department by the state. Australian GST income is gathered by the Administration and then

given by the Commonwealth Grants Commission to the Regions through an allocation scheme.

Compared to other rich, advanced countries, Australia retains a comparatively small tax liability at 27.8%

of GDP in 2018 (Economywatch, 2019).

Forms of taxes collected both by State and National Government:

a. Personal Income Tax- This is the most important source of Revenue for the Central Government

and is imposed on an individual. It is a progressive tax, which means the richer you are the more

you have to pay.

b. Capital Gains Tax (CGT) - Tax imposed on Capital Gain made on disposal of any asset. Family

home is an exemption. In the tax year a property is marketed and/or disposed of, CGT works by

owning net profits regarded as taxable income. If an asset is kept for at least one year than any

profit is first marked down for income earners by 50 percent or for superannuation funds by

33.3 percent (Ato.gov.au, 2019).

c. Corporate Taxes – Whatever profits a company or a corporate makes, it has to pay taxes on it. It

is regressive tax where 30 percent rate is fixed (25 percent for smaller businesses with revenue

less than two million Australian dollars in a year) (Tradingeconomics.com, 2019).

d. Trustee Liability Taxes- In which all or portion of the aggregate trust earnings is allocated to non-

residents or underage kids, to representative of the recipient, the solicitor of that trust is

evaluated on the above portion. In this case, recipients should assert that portion of aggregate

trust earnings on their personal earnings tax yields as well as assert a credit for the amount of

tax compensated on their behalf by the trustee.

e. Good & Services Tax (GST) - A goods and services tax (GST) is a VAT imposed by the

Central government on the distribution of maximum goods and services by tax-registered

corporations at 10 percent (Business.gov.au, 2019).

Apart from these, there are other taxes too like taxes on Property, Departure Tax, Excise taxes, Fuel tax,

Luxury car tax, Customs duties, Payroll taxes ( different in different states), Fringe Benefits Tax,

Inheritance Tax, Superannuation Tax as well as others (Ato.gov.au, 2019).

In this report we will discuss what are the issues in current Tax issues of Australia, Law of Tax policies of

Australia, what government is trying to do to make it friendlier for corporations and public at large and

what more can be done.

and is imposed on an individual. It is a progressive tax, which means the richer you are the more

you have to pay.

b. Capital Gains Tax (CGT) - Tax imposed on Capital Gain made on disposal of any asset. Family

home is an exemption. In the tax year a property is marketed and/or disposed of, CGT works by

owning net profits regarded as taxable income. If an asset is kept for at least one year than any

profit is first marked down for income earners by 50 percent or for superannuation funds by

33.3 percent (Ato.gov.au, 2019).

c. Corporate Taxes – Whatever profits a company or a corporate makes, it has to pay taxes on it. It

is regressive tax where 30 percent rate is fixed (25 percent for smaller businesses with revenue

less than two million Australian dollars in a year) (Tradingeconomics.com, 2019).

d. Trustee Liability Taxes- In which all or portion of the aggregate trust earnings is allocated to non-

residents or underage kids, to representative of the recipient, the solicitor of that trust is

evaluated on the above portion. In this case, recipients should assert that portion of aggregate

trust earnings on their personal earnings tax yields as well as assert a credit for the amount of

tax compensated on their behalf by the trustee.

e. Good & Services Tax (GST) - A goods and services tax (GST) is a VAT imposed by the

Central government on the distribution of maximum goods and services by tax-registered

corporations at 10 percent (Business.gov.au, 2019).

Apart from these, there are other taxes too like taxes on Property, Departure Tax, Excise taxes, Fuel tax,

Luxury car tax, Customs duties, Payroll taxes ( different in different states), Fringe Benefits Tax,

Inheritance Tax, Superannuation Tax as well as others (Ato.gov.au, 2019).

In this report we will discuss what are the issues in current Tax issues of Australia, Law of Tax policies of

Australia, what government is trying to do to make it friendlier for corporations and public at large and

what more can be done.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION ISSUE OF AUSTRALIA:

Australia has more than 125 central and state taxes, but only 10 of them boost 90% of earning. The

present government is under pressure to bring reforms and change the existing tax system which is

becoming headache for public at large (Bagshaw, 2019). There have been reports of dissatisfaction

among people related to certain taxes which are discussed in details below:

Superannuation- Ever-since the authority implemented its tax modification plan in August 1998, the

pension and banking sector has lobbied for an evaluation of the pension scheme. This draft bill did not

take into account overhauling the taxation of payments and advantages for superannuation. Meanwhile,

the special interest groups for retirement and banking were not satisfied with letting the problem being

overlooked. They repeatedly made denunciations of the whole pension scheme by the administration,

not just the pension taxes (Aph.gov.au, 2019). Finally, the administration proposed its unofficial

opinions on the issue. Major issues with the existing system is that there is lack of transparency, tax

incentives are not equitable, most of the advantages go to the high income earner, the existing system is

filled with complexity and treatment of contributions, pensions and annuities in a complex manner.

Tax issue with the Trust- Income tax moves manipulate the distinctions in trust law and tax law

meanings of revenue. Recipients are responsible for tax on quantities they may not accrue resulting in a

split between financial and tax results. It has been noted that in attempt to postpone, decrease or

suppress tax obligations, taxpayers can obtain revenue from trusts in clever methods. ATO statistical

research indicates that various kinds of trusts have distinct lodging trends. However, considering the

absence of accessible info, there is no method to confirm it.

General Business Tax issues- Taxes on Corporates and businesses are very high when compared to other

competing nations. The percent of tax rates on dividends is higher by 13 percent than that of New

Zealand. Corporate Tax rate is 30 percent which form 19 percent of Corporate Tax revenue (percent of

total tax) (Treasury.gov.au, 2019). Our corporate tax rate is higher than the average corporate tax rate

of the entire globe. High taxes cause hindrance for business growth and slow down the economy.

Income Tax- Although it is a trend that developed countries imposes high income tax on its citizens but

there is dissatisfaction among many regarding this.

The biggest problem people currently have with the Australian Taxation Office (ATO) is failure of

software designed to do stuff nicely and automatically. Right now this involves individual income tax

Australia has more than 125 central and state taxes, but only 10 of them boost 90% of earning. The

present government is under pressure to bring reforms and change the existing tax system which is

becoming headache for public at large (Bagshaw, 2019). There have been reports of dissatisfaction

among people related to certain taxes which are discussed in details below:

Superannuation- Ever-since the authority implemented its tax modification plan in August 1998, the

pension and banking sector has lobbied for an evaluation of the pension scheme. This draft bill did not

take into account overhauling the taxation of payments and advantages for superannuation. Meanwhile,

the special interest groups for retirement and banking were not satisfied with letting the problem being

overlooked. They repeatedly made denunciations of the whole pension scheme by the administration,

not just the pension taxes (Aph.gov.au, 2019). Finally, the administration proposed its unofficial

opinions on the issue. Major issues with the existing system is that there is lack of transparency, tax

incentives are not equitable, most of the advantages go to the high income earner, the existing system is

filled with complexity and treatment of contributions, pensions and annuities in a complex manner.

Tax issue with the Trust- Income tax moves manipulate the distinctions in trust law and tax law

meanings of revenue. Recipients are responsible for tax on quantities they may not accrue resulting in a

split between financial and tax results. It has been noted that in attempt to postpone, decrease or

suppress tax obligations, taxpayers can obtain revenue from trusts in clever methods. ATO statistical

research indicates that various kinds of trusts have distinct lodging trends. However, considering the

absence of accessible info, there is no method to confirm it.

General Business Tax issues- Taxes on Corporates and businesses are very high when compared to other

competing nations. The percent of tax rates on dividends is higher by 13 percent than that of New

Zealand. Corporate Tax rate is 30 percent which form 19 percent of Corporate Tax revenue (percent of

total tax) (Treasury.gov.au, 2019). Our corporate tax rate is higher than the average corporate tax rate

of the entire globe. High taxes cause hindrance for business growth and slow down the economy.

Income Tax- Although it is a trend that developed countries imposes high income tax on its citizens but

there is dissatisfaction among many regarding this.

The biggest problem people currently have with the Australian Taxation Office (ATO) is failure of

software designed to do stuff nicely and automatically. Right now this involves individual income tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

returns and single touch payroll, a system requiring all employers to lodge payroll details online. This

should be expected, as no big IT program delivers on time, on budget and in accordance with

requirements.

Otherwise, the ATO is far nicer and more lenient than any foreign taxing authority one deals with. The

ATO only get particularly nasty if they believe you are intentionally noncompliant.

Apart from these there are issues in other taxation systems too.

should be expected, as no big IT program delivers on time, on budget and in accordance with

requirements.

Otherwise, the ATO is far nicer and more lenient than any foreign taxing authority one deals with. The

ATO only get particularly nasty if they believe you are intentionally noncompliant.

Apart from these there are issues in other taxation systems too.

“WHAT IS THE CURRENT LAW?”

Australia's National Gov. has authority to tax Australian citizens only on Aussie revenue from global

outlets and non-residents. Australian law includes particular registration laws to decide if a person or

business is domiciled. Australia also has a scheme to determine if Australia or some other nation is a

revenue generator. In particular, in the location of jobs or the specified location of company, revenue is

generated. Global operations often take place where the appropriate agreement is concluded, although

these wide standards often vary based on the conditions. The danger connected with the laws of

residency and origin is that in two distinct nations one quantity of revenue can be taxed. To prevent this,

Australia has joined into numerous dual tax contracts with other nations that will take precedence over

Australia's National Gov. has authority to tax Australian citizens only on Aussie revenue from global

outlets and non-residents. Australian law includes particular registration laws to decide if a person or

business is domiciled. Australia also has a scheme to determine if Australia or some other nation is a

revenue generator. In particular, in the location of jobs or the specified location of company, revenue is

generated. Global operations often take place where the appropriate agreement is concluded, although

these wide standards often vary based on the conditions. The danger connected with the laws of

residency and origin is that in two distinct nations one quantity of revenue can be taxed. To prevent this,

Australia has joined into numerous dual tax contracts with other nations that will take precedence over

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

national legislation to guarantee that taxation on any specified quantity of revenue is only enforced

once. Moreover, Australia also runs a scheme of overseas tax incentives under which Aussie citizens who

bear overseas tax on overseas revenue are provided tax benefits. Then these benefits are used to

compensate the very same quantity of Aussie taxes paid, once more securing that revenue is taxed only

once. In particular, taxable income is the cumulative assessable earning of an organization minus any

deductions. If a loss is caused, it could be brought forward to subsequent years as long as the loss is

fulfilled in carrying forward trials. Assessable revenue involves products like salaries, wages, company

earnings, stake, lease, and profits. Exemptions usually involve costs involved during revenue profit or

revenue generation, in relation to an amount of particular allowances permitted under laws. Exemptions

are not permitted for private or operating expenditures. If some requirements are fulfilled, however, it is

feasible for businesses and people to offset losses against other revenue kinds. CGT is enforced on sale

proceeds of property, with unique regulations on capital gains assessment. The properties topic to CGT

is quite wide for taxation reasons and involves both physical and intellectual properties. Many assets

such as automobiles, private use resources and one's family home are susceptible to exceptions,

whereas overseas citizens are susceptible to capital gains on only a restricted spectrum of investments,

such as tangible assets. Capital gains are included in the taxable income of taxpayers and are thus taxed

at the relevant income tax rate of each individual. In accordance with the laws stated above, people are

charged on earnings and capital gains. As mentioned, both Aussie residents and non-residents, based on

the basis of the revenue, may be subject to income tax and CGT. Australia utilizes a scheme of graduated

tax measurements to tax people. Under this scheme, as taxable income rises, the level of tax payable

rises. An Australian business is a completely separate entity from its investors. Income earned by a firm

is taxable to the firm after implementing specific laws of residence and basis to those applicable to

people. But, except for people, corporate profits are taxed at a standard price of 30% irrespective of

revenue of the corporation. The then elected Liberal government, though, intended to reduce the

corporate tax rate by 1.5% from 1 July 2015, thus lowering the corporate tax rate to 28.5% (Home.kpmg,

2019). Dividends paid to stakeholders by businesses are shown in the assessable revenue of the

stakeholders and are entitled to a 'scheme of dividend imputation.'

once. Moreover, Australia also runs a scheme of overseas tax incentives under which Aussie citizens who

bear overseas tax on overseas revenue are provided tax benefits. Then these benefits are used to

compensate the very same quantity of Aussie taxes paid, once more securing that revenue is taxed only

once. In particular, taxable income is the cumulative assessable earning of an organization minus any

deductions. If a loss is caused, it could be brought forward to subsequent years as long as the loss is

fulfilled in carrying forward trials. Assessable revenue involves products like salaries, wages, company

earnings, stake, lease, and profits. Exemptions usually involve costs involved during revenue profit or

revenue generation, in relation to an amount of particular allowances permitted under laws. Exemptions

are not permitted for private or operating expenditures. If some requirements are fulfilled, however, it is

feasible for businesses and people to offset losses against other revenue kinds. CGT is enforced on sale

proceeds of property, with unique regulations on capital gains assessment. The properties topic to CGT

is quite wide for taxation reasons and involves both physical and intellectual properties. Many assets

such as automobiles, private use resources and one's family home are susceptible to exceptions,

whereas overseas citizens are susceptible to capital gains on only a restricted spectrum of investments,

such as tangible assets. Capital gains are included in the taxable income of taxpayers and are thus taxed

at the relevant income tax rate of each individual. In accordance with the laws stated above, people are

charged on earnings and capital gains. As mentioned, both Aussie residents and non-residents, based on

the basis of the revenue, may be subject to income tax and CGT. Australia utilizes a scheme of graduated

tax measurements to tax people. Under this scheme, as taxable income rises, the level of tax payable

rises. An Australian business is a completely separate entity from its investors. Income earned by a firm

is taxable to the firm after implementing specific laws of residence and basis to those applicable to

people. But, except for people, corporate profits are taxed at a standard price of 30% irrespective of

revenue of the corporation. The then elected Liberal government, though, intended to reduce the

corporate tax rate by 1.5% from 1 July 2015, thus lowering the corporate tax rate to 28.5% (Home.kpmg,

2019). Dividends paid to stakeholders by businesses are shown in the assessable revenue of the

stakeholders and are entitled to a 'scheme of dividend imputation.'

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

“PERCEIVED WEAKNESS OF THE CURRENT LAW”

Powerful, maintained and integrated economic growth requires a properly-functioning income scheme.

Problem with Australia is that they have taxed individuals and corporates so much that now they have

surplus funds. Surplus is so much that it is now meaningless to keep on taxing at a high rate. Relaxation

or lowering of taxes will lead people to increase their personal expenses and investment which in return

will help in boosting the economy further in the long run. Many scholars and experts have given

proposals for much needed change in tax reforms with their own well documented and researched

reasons. The suggestion was revealed as top economists and large support organizations on each side of

the debate — the Australian Social Services Council and Australia's Business Council — propose a flurry

of change, advising Australia to revisit its previous year’s tax policy or potentially leave behind

employees, welfare recipients and company. For the first occasion in a century, the budget is pushing

towards excess, and legislators are more flexible than ever since the credit crunch. The delay can cause

more severe issues than imagined. According to numbers from the ABS, prosperity for those aged 55

and over rose by 42 percent between 2002 and 2014 contrasted to 7% for individuals aged 25-34. PwC

modeling demonstrates that applying the fixed 30% price will boost the amount of taxpayers by 27%,

assisting to relieve the tax burden stress as the boomers retire. In 40 years' period, the Henry

assessment discovered that there would be only 2.7 employed-age individuals of each individual aged

65 or older, opposed to 5.0 individuals currently and 7.5 individuals 40 years ago (Bagshaw, 2019).

Powerful, maintained and integrated economic growth requires a properly-functioning income scheme.

Problem with Australia is that they have taxed individuals and corporates so much that now they have

surplus funds. Surplus is so much that it is now meaningless to keep on taxing at a high rate. Relaxation

or lowering of taxes will lead people to increase their personal expenses and investment which in return

will help in boosting the economy further in the long run. Many scholars and experts have given

proposals for much needed change in tax reforms with their own well documented and researched

reasons. The suggestion was revealed as top economists and large support organizations on each side of

the debate — the Australian Social Services Council and Australia's Business Council — propose a flurry

of change, advising Australia to revisit its previous year’s tax policy or potentially leave behind

employees, welfare recipients and company. For the first occasion in a century, the budget is pushing

towards excess, and legislators are more flexible than ever since the credit crunch. The delay can cause

more severe issues than imagined. According to numbers from the ABS, prosperity for those aged 55

and over rose by 42 percent between 2002 and 2014 contrasted to 7% for individuals aged 25-34. PwC

modeling demonstrates that applying the fixed 30% price will boost the amount of taxpayers by 27%,

assisting to relieve the tax burden stress as the boomers retire. In 40 years' period, the Henry

assessment discovered that there would be only 2.7 employed-age individuals of each individual aged

65 or older, opposed to 5.0 individuals currently and 7.5 individuals 40 years ago (Bagshaw, 2019).

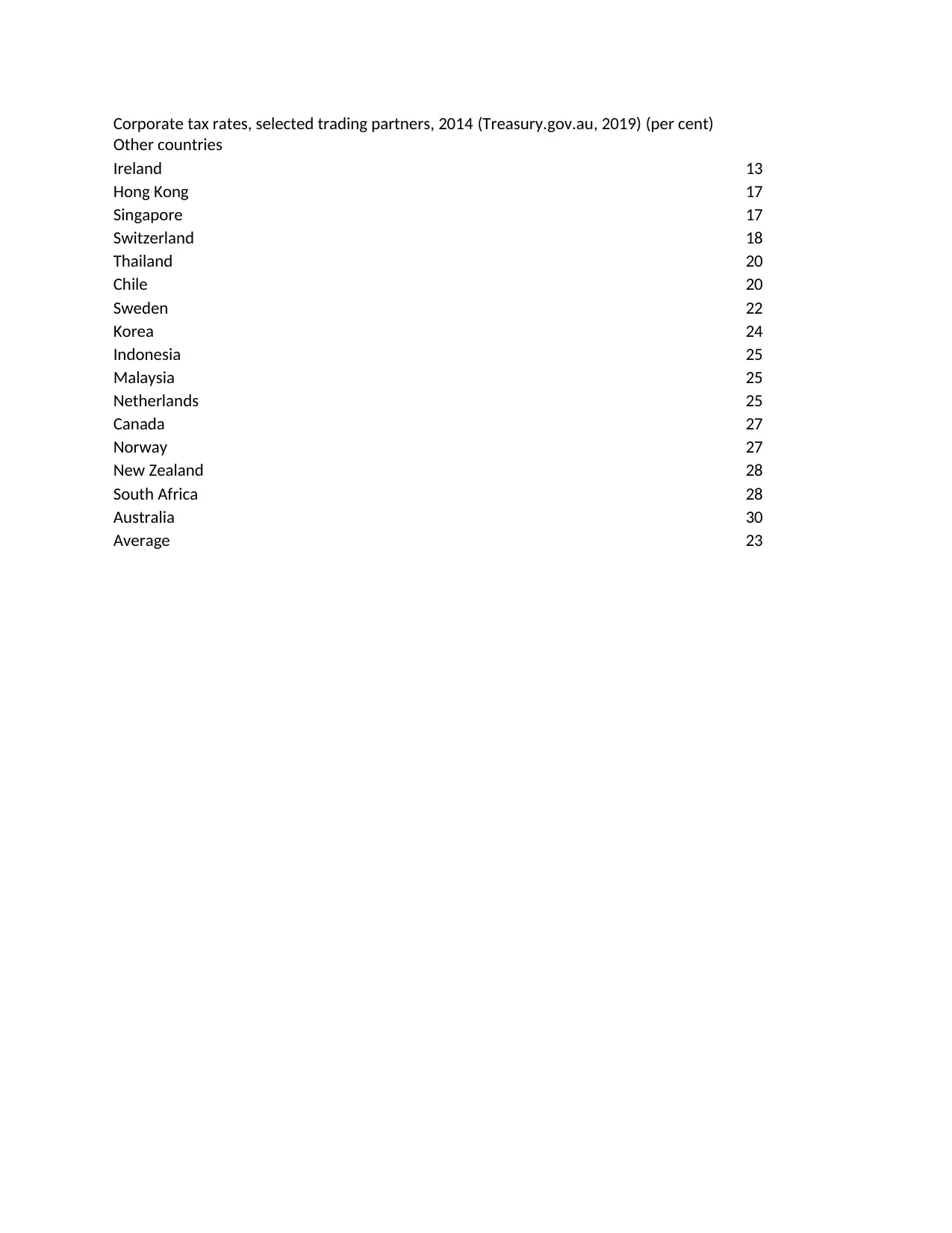

Corporate tax rates, selected trading partners, 2014 (Treasury.gov.au, 2019) (per cent)

Other countries

Ireland 13

Hong Kong 17

Singapore 17

Switzerland 18

Thailand 20

Chile 20

Sweden 22

Korea 24

Indonesia 25

Malaysia 25

Netherlands 25

Canada 27

Norway 27

New Zealand 28

South Africa 28

Australia 30

Average 23

Other countries

Ireland 13

Hong Kong 17

Singapore 17

Switzerland 18

Thailand 20

Chile 20

Sweden 22

Korea 24

Indonesia 25

Malaysia 25

Netherlands 25

Canada 27

Norway 27

New Zealand 28

South Africa 28

Australia 30

Average 23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

“HOW THE GOVERNMENT PROPOSES TO ADDRESS THEM?”

Government feels the heat of the corporations and public at large and is ready to hear out decent

proposals and willing to implement them. There have been many lobbies suggesting many things. Few

are discussed in detail.

Whilst the PwC proposition starts off a debate about the potential of revenue tax, Australia's economic

experts also said that increased GST cap, death taxes, and a change from stamp duty to property tax

should all be on the board after Coalition and Labor governments have put on hold the last two efforts

at significant change.

In a decade since the historic Henry tax assessment, deputy second tax chairman Richard Highfield said

that underlying problems have not been addressed and expenses are increasing, with lost income flying

up to $8 billion annually, as per the Australian Tax Office.

Australia has a poor mix and numerous taxes. To be in line, one has to bear excessive compliance charge

for too little profit. According to Ross Garnaut, the nation needs help. The present scenarios are more

threatening than before and if there is any unpleasant event in upcoming days, we may not be ready.

Different savings are taxed differently. Erstwhile Treasury Secretary and Reserve Bank Governor Bernie

Fraser said the tax policy mismanaging over the previous twenty years provided the basis for a fresh

rejig. He said the Henry assessment had been served "worse than fairness" and called for courageous

thoughts over and above focusing on fragmented regulation by cutting corporate taxes.

"By taxing companies, are we simply supporting the industry or are we attempting to create a stronger,

fair and just nation?" He's been saying. Political intransigence has caused desperation between many

company and social organizations that, while not promoting each of PwC's particular suggestions, have

named for fresh tax concepts to be brought forward. "Australia has become apathetic after 27 years of

Government feels the heat of the corporations and public at large and is ready to hear out decent

proposals and willing to implement them. There have been many lobbies suggesting many things. Few

are discussed in detail.

Whilst the PwC proposition starts off a debate about the potential of revenue tax, Australia's economic

experts also said that increased GST cap, death taxes, and a change from stamp duty to property tax

should all be on the board after Coalition and Labor governments have put on hold the last two efforts

at significant change.

In a decade since the historic Henry tax assessment, deputy second tax chairman Richard Highfield said

that underlying problems have not been addressed and expenses are increasing, with lost income flying

up to $8 billion annually, as per the Australian Tax Office.

Australia has a poor mix and numerous taxes. To be in line, one has to bear excessive compliance charge

for too little profit. According to Ross Garnaut, the nation needs help. The present scenarios are more

threatening than before and if there is any unpleasant event in upcoming days, we may not be ready.

Different savings are taxed differently. Erstwhile Treasury Secretary and Reserve Bank Governor Bernie

Fraser said the tax policy mismanaging over the previous twenty years provided the basis for a fresh

rejig. He said the Henry assessment had been served "worse than fairness" and called for courageous

thoughts over and above focusing on fragmented regulation by cutting corporate taxes.

"By taxing companies, are we simply supporting the industry or are we attempting to create a stronger,

fair and just nation?" He's been saying. Political intransigence has caused desperation between many

company and social organizations that, while not promoting each of PwC's particular suggestions, have

named for fresh tax concepts to be brought forward. "Australia has become apathetic after 27 years of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

continuous economic development," retorted Australia Chief Executive Jennifer Westacott's Business

Committee.

A mixture of worldwide hazards, Australia's elevated private obligation, high political debt,

minimal paying development and low productivity development is not a formula for strength in a

turbulent globe. Cassandra Goldie, Chief Executive of the Australian Social Services Council, said

company group, labour unions, and public industry believe that government needs to enhance the

state's justice and sustainability. "We are broadly agreed that we have a mid to longish-term income

task and that we need to address tax breaks that are not appropriate anymore for intent," she said (The

Conversation, 2019).

Committee.

A mixture of worldwide hazards, Australia's elevated private obligation, high political debt,

minimal paying development and low productivity development is not a formula for strength in a

turbulent globe. Cassandra Goldie, Chief Executive of the Australian Social Services Council, said

company group, labour unions, and public industry believe that government needs to enhance the

state's justice and sustainability. "We are broadly agreed that we have a mid to longish-term income

task and that we need to address tax breaks that are not appropriate anymore for intent," she said (The

Conversation, 2019).

“MY VIEWS ON ADDRESSING THE ISSUE”

Any tax reform's primary aim is always to enable the government to increase greater income. If more

revenue is raised by the Gov., it must imply that people are left with less. Our "open" industry already

has enough manipulations and tensile failures to prevent it operating with the dexterity and

effectiveness it should. Our present tax code is absurdly ineffective, mainly due to leaders (especially

neoconservatives, but all main sides are responsible) who see that every new fiscal relief (i.e. new

legislation, new types, more tax officials, more job for tax officials and attorneys) required votes to meet

their own personal ambitions for a specific electoral demographic purchase. Even changes need to be

supplemented by increased advantages (i.e. see prior parenthetic) so that "nobody is unhappier" or, in

the fresh government treasurers' language, cash that will be "wasted" if new taxes come in as they

would have gained even more under the "ancient" laws.

Any tax reform's primary aim is always to enable the government to increase greater income. If more

revenue is raised by the Gov., it must imply that people are left with less. Our "open" industry already

has enough manipulations and tensile failures to prevent it operating with the dexterity and

effectiveness it should. Our present tax code is absurdly ineffective, mainly due to leaders (especially

neoconservatives, but all main sides are responsible) who see that every new fiscal relief (i.e. new

legislation, new types, more tax officials, more job for tax officials and attorneys) required votes to meet

their own personal ambitions for a specific electoral demographic purchase. Even changes need to be

supplemented by increased advantages (i.e. see prior parenthetic) so that "nobody is unhappier" or, in

the fresh government treasurers' language, cash that will be "wasted" if new taxes come in as they

would have gained even more under the "ancient" laws.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.