TAX LAW 1010: Residential Status and Tax Deductions Analysis

VerifiedAdded on 2022/08/26

|11

|2466

|14

Homework Assignment

AI Summary

This tax law assignment solution analyzes two key scenarios related to Australian taxation. The first scenario focuses on determining an individual's residential status for tax purposes, considering factors like visa status, physical presence, intention to reside, and family connections. It explores the application of the Income Tax Assessment Act 1997, including the resides test, domicile test, and 183-day test. The second scenario examines the tax implications of income earned overseas and the deductibility of various expenses, including work-related travel and business expenses. The solution provides a detailed analysis of relevant legislation and case law, offering clear conclusions regarding tax liabilities and allowable deductions, including travel expenses, office rent, and pet minding fees. The assignment emphasizes the importance of residential status in determining tax obligations and provides practical examples of how tax laws apply in real-life situations.

Running Head: TAX LAW

Tax law

Name of the Student:

Name of the university:

Author Note:

Tax law

Name of the Student:

Name of the university:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAX LAW

Table of Contents

Question 1 (a)......................................................................................................................2

Question 1(b).......................................................................................................................4

Question 2............................................................................................................................6

Reference list.......................................................................................................................8

TAX LAW

Table of Contents

Question 1 (a)......................................................................................................................2

Question 1(b).......................................................................................................................4

Question 2............................................................................................................................6

Reference list.......................................................................................................................8

2

TAX LAW

Question 1 (a)

Residential status is an important factor to determine the tax. The Australian Taxation

Office (ATO) has made different standards and regulation for the immigrants and Australian

residents to determine their tax purpose. This standard ensures that an individual is taxed

according to the ATO if he satisfies the resident conditions.

Issues: Tompson Pondage is holding Germany passport visited Australia in the year of 2007 by

holding a work visa. His visa was permitted to work and live in Australia. In Australia, he

worked in a contract basis as a marine engineer on a sea barge. This company is an Australian

owned company. Soon this company is leased to a Malaysia based company that is Ocean

Development Limited and they were carrying out their work in China. Tompson accepted this

work and left Australia on 8 July 2015 leaving behind his wife and child in Australia. He worked

with the Ocean development limited for nine month and earned AUD $ 90000. After the end of

the contract with the Ocean Development he return back to the Australia and entered into his

wife business as partner.

Law: In accordance to the Residential Tenancies Act 1997 an Australian resident is always

taxable under ATO laws and regulation irrespective of where he or she lives. This is also

applicable to those who is residing in Australia for more than six month until and unless they

have any intention to live in Australia or having a permanent home in overseas (Braithwaite and

Wirth 2019). An individual is also considered as a resident of Australia if he or she moved to

Australia from overseas and shows the intention to stay there and make connection.

For assessing the residential status there are number of process which are as follows:

TAX LAW

Question 1 (a)

Residential status is an important factor to determine the tax. The Australian Taxation

Office (ATO) has made different standards and regulation for the immigrants and Australian

residents to determine their tax purpose. This standard ensures that an individual is taxed

according to the ATO if he satisfies the resident conditions.

Issues: Tompson Pondage is holding Germany passport visited Australia in the year of 2007 by

holding a work visa. His visa was permitted to work and live in Australia. In Australia, he

worked in a contract basis as a marine engineer on a sea barge. This company is an Australian

owned company. Soon this company is leased to a Malaysia based company that is Ocean

Development Limited and they were carrying out their work in China. Tompson accepted this

work and left Australia on 8 July 2015 leaving behind his wife and child in Australia. He worked

with the Ocean development limited for nine month and earned AUD $ 90000. After the end of

the contract with the Ocean Development he return back to the Australia and entered into his

wife business as partner.

Law: In accordance to the Residential Tenancies Act 1997 an Australian resident is always

taxable under ATO laws and regulation irrespective of where he or she lives. This is also

applicable to those who is residing in Australia for more than six month until and unless they

have any intention to live in Australia or having a permanent home in overseas (Braithwaite and

Wirth 2019). An individual is also considered as a resident of Australia if he or she moved to

Australia from overseas and shows the intention to stay there and make connection.

For assessing the residential status there are number of process which are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAX LAW

Resides test – Under the section 6(1) of the Income Tax Assessment Act 1997 this test

determines whether an individual is an Australian resident or not. It is the main test which

ATO uses to determine the resident status for the tax purpose. If the individual resides in

Australia then he or she is considered as an Australian resident for the tax purpose and if

this test satisfies, no other test is required to be applied (Anon 2020). Some of the

factors that are used to determine the residency status include physical presence, intention

or purpose, family, business, employment and living arrangement. If the individual does

not satisfy, reside test than other statutory test are need to be followed.

Domicile test – Under the section 6(1) of the Income Tax Assessment Act 1997 this test

is the first statutory test where an Australian resident domicile is checked. This test

requires showing a permanent house or something that is more than a residence in the

Australia and if it satisfies then the individual is considered as the Australian resident for

the tax purpose (Braithwaite and Reinhart 2019).

183-day test – Under the section 6(1) of the Income Tax Assessment Act 1997 this test

checks the presence of the individual in Australia for more than 183 days in a continuous

or with a break. If the individual satisfies the condition, he or she is considered as an

Australian resident until and unless the individual has a home in overseas or does not

have any intention to reside in Australia.

Superannuation test – Under the section 6(1) of the Income Tax Assessment Act 1997 it

is the third statutory test which covers certain Australian government employees. This

test ensures that individual working at a overseas are treated as an Australian resident.

In accordance of the case Harding v Commissioner of Taxation residential makes a big

difference in the tax situation and an Australian resident is taxed worldwide which includes

TAX LAW

Resides test – Under the section 6(1) of the Income Tax Assessment Act 1997 this test

determines whether an individual is an Australian resident or not. It is the main test which

ATO uses to determine the resident status for the tax purpose. If the individual resides in

Australia then he or she is considered as an Australian resident for the tax purpose and if

this test satisfies, no other test is required to be applied (Anon 2020). Some of the

factors that are used to determine the residency status include physical presence, intention

or purpose, family, business, employment and living arrangement. If the individual does

not satisfy, reside test than other statutory test are need to be followed.

Domicile test – Under the section 6(1) of the Income Tax Assessment Act 1997 this test

is the first statutory test where an Australian resident domicile is checked. This test

requires showing a permanent house or something that is more than a residence in the

Australia and if it satisfies then the individual is considered as the Australian resident for

the tax purpose (Braithwaite and Reinhart 2019).

183-day test – Under the section 6(1) of the Income Tax Assessment Act 1997 this test

checks the presence of the individual in Australia for more than 183 days in a continuous

or with a break. If the individual satisfies the condition, he or she is considered as an

Australian resident until and unless the individual has a home in overseas or does not

have any intention to reside in Australia.

Superannuation test – Under the section 6(1) of the Income Tax Assessment Act 1997 it

is the third statutory test which covers certain Australian government employees. This

test ensures that individual working at a overseas are treated as an Australian resident.

In accordance of the case Harding v Commissioner of Taxation residential makes a big

difference in the tax situation and an Australian resident is taxed worldwide which includes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAX LAW

income from all sources. But if the individual is not a resident of Australia then he or she is taxed

in the Australian sourced income.

If an Australian resident going overseas for the purpose of work then also they remain as

an Australian resident for the tax purpose (Burkhauser, Hahn and Wilkins 2015). Here residential

status is considered as the primary fact which undergoes with reside test and if required then

through three statutory test.

If any individual is working as a contract in Australia for more than six month than also

the individual is considered as the resident of Australia. ATO does not determines the tax

liability according to the citizenship and nationality.

There is also an option of temporary resident who will be exempt from the Australian tax.

A temporary resident for the tax purpose are those individual who holds a temporary visa under

the Migration Act, considered as non-resident under the Social Security Act and the individual

does not have any Australian spouse in accordance with the Social Security Act (Sakurai and

Braithwaite 2019).

Discussion: Tompson came to Australia with a work visa but he is staying there for more than

the nine years without any break which shows his intention of staying in Australia. He also has a

wife and a child in Australia and his wife has a business in Australia. Moreover, it is assumed

that his wife is a permanent resident of Australia. While going to the oversea work with the

Ocean Development limited for nine month does not make him non-resident as he already,

satisfy the residential condition under Australian tax law.

Conclusion: According to the Residential Tenancies Act 1997 Tompson satisfies the reside test

by having a home in Australia. So he does not need to satisfies other three statutory test. He also

TAX LAW

income from all sources. But if the individual is not a resident of Australia then he or she is taxed

in the Australian sourced income.

If an Australian resident going overseas for the purpose of work then also they remain as

an Australian resident for the tax purpose (Burkhauser, Hahn and Wilkins 2015). Here residential

status is considered as the primary fact which undergoes with reside test and if required then

through three statutory test.

If any individual is working as a contract in Australia for more than six month than also

the individual is considered as the resident of Australia. ATO does not determines the tax

liability according to the citizenship and nationality.

There is also an option of temporary resident who will be exempt from the Australian tax.

A temporary resident for the tax purpose are those individual who holds a temporary visa under

the Migration Act, considered as non-resident under the Social Security Act and the individual

does not have any Australian spouse in accordance with the Social Security Act (Sakurai and

Braithwaite 2019).

Discussion: Tompson came to Australia with a work visa but he is staying there for more than

the nine years without any break which shows his intention of staying in Australia. He also has a

wife and a child in Australia and his wife has a business in Australia. Moreover, it is assumed

that his wife is a permanent resident of Australia. While going to the oversea work with the

Ocean Development limited for nine month does not make him non-resident as he already,

satisfy the residential condition under Australian tax law.

Conclusion: According to the Residential Tenancies Act 1997 Tompson satisfies the reside test

by having a home in Australia. So he does not need to satisfies other three statutory test. He also

5

TAX LAW

has spouse who is a permanent resident of Australia. Which makes him the resident of Australia

and his income is taxable in Australia.

Question 1(b)

Issues: Tompson after working with the Ocean Development in China earned AUD $ 90000. In

China his employer provided him quarter and meals as the part of the accommodation. His salary

is received in the bank account of Australia after deducting tax. Tompson has its all assets in

Australia which includes home in Sydney, investment in residential unit, super policy with AMP,

listed share, bank account and also a membership in local golf club.

Law: According to the Income Tax Assessment Act 1997 if an individual is a foreign resident

earning income in Australia which includes employment income, rental income, pension or

annuities and capital gain from an Australian assets need to declare their tax return.

If an individual is, an Australian resident for the tax purpose need to declare all the

income earned in Australia as well as the income which is earned in foreign. There is an option

to offset the taxes paid in foreign to reduce the Australian tax (Hobson 2019).

If an individual is consider as a temporary resident, which could be by having temporary

visa, not having spouse in Australia, or considered as non-resident in according to the Social

Security Act 1991. They need to declare their income that is derived in Australia and all other

incomes that are earned from overseas in the form of employment or any service. While other

foreign incomes and capital gain does not need to be declared (Ato.gov.au 2020).

If an individual came to Australia for working on holiday under subclass 417 or 462 then

they have to pay tax at a fixed rate on the income earned in Australia irrespective to the

residential status (Schenk, Thuronyi and Cui 2015).

TAX LAW

has spouse who is a permanent resident of Australia. Which makes him the resident of Australia

and his income is taxable in Australia.

Question 1(b)

Issues: Tompson after working with the Ocean Development in China earned AUD $ 90000. In

China his employer provided him quarter and meals as the part of the accommodation. His salary

is received in the bank account of Australia after deducting tax. Tompson has its all assets in

Australia which includes home in Sydney, investment in residential unit, super policy with AMP,

listed share, bank account and also a membership in local golf club.

Law: According to the Income Tax Assessment Act 1997 if an individual is a foreign resident

earning income in Australia which includes employment income, rental income, pension or

annuities and capital gain from an Australian assets need to declare their tax return.

If an individual is, an Australian resident for the tax purpose need to declare all the

income earned in Australia as well as the income which is earned in foreign. There is an option

to offset the taxes paid in foreign to reduce the Australian tax (Hobson 2019).

If an individual is consider as a temporary resident, which could be by having temporary

visa, not having spouse in Australia, or considered as non-resident in according to the Social

Security Act 1991. They need to declare their income that is derived in Australia and all other

incomes that are earned from overseas in the form of employment or any service. While other

foreign incomes and capital gain does not need to be declared (Ato.gov.au 2020).

If an individual came to Australia for working on holiday under subclass 417 or 462 then

they have to pay tax at a fixed rate on the income earned in Australia irrespective to the

residential status (Schenk, Thuronyi and Cui 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAX LAW

Conclusion: Being the resident of Australia Tompson while working in the overseas his income

is regarded as the Australian income which is taxable in Australia. And the source of income

which is received by Tompson while working in China is his salary which is received during his

employment and interest from bank of Australia saving account.

Question 2

Issues: Rumpole is a medical doctor and a scientist who works in a local hospital during the

morning time and in a research laboratory in a university at noon. He bears some travelling

expenses like $1200 from home to hospital, $800 from hospital to the local university and $1000

from the university to home. In the current income year, he opens his own practice to serve the

local peoples. For the purpose of the business he took an office on rent at $10000 per month and

he put his pet dog in pet minding for which he has to make expense of $20000 as pet minding

fees for every year.

Law: Income received as a doctor, scientist or any professional in the form of salary or an

allowance which is received from the employer during a financial year need to be shown in the

tax return but excluding the reimbursements while including any bonuses. Under section 8-1 of

Income Tax Assessment Act 1997 states that all work related expenses can be claimed as

deduction (Anon 2020). Deduction which can be claimed for the expenses must have been

spent by the taxpayer himself and it has not been reimbursed or it is directly related to the

earning of the income or all expenses made by the taxpayer must have been recorded as any

receipt to prove the expenses. While if the expenses are made for both the work and private

purpose than the expenses made for the work purpose can only be claimed as deduction (Feld

and Frey 2019).

TAX LAW

Conclusion: Being the resident of Australia Tompson while working in the overseas his income

is regarded as the Australian income which is taxable in Australia. And the source of income

which is received by Tompson while working in China is his salary which is received during his

employment and interest from bank of Australia saving account.

Question 2

Issues: Rumpole is a medical doctor and a scientist who works in a local hospital during the

morning time and in a research laboratory in a university at noon. He bears some travelling

expenses like $1200 from home to hospital, $800 from hospital to the local university and $1000

from the university to home. In the current income year, he opens his own practice to serve the

local peoples. For the purpose of the business he took an office on rent at $10000 per month and

he put his pet dog in pet minding for which he has to make expense of $20000 as pet minding

fees for every year.

Law: Income received as a doctor, scientist or any professional in the form of salary or an

allowance which is received from the employer during a financial year need to be shown in the

tax return but excluding the reimbursements while including any bonuses. Under section 8-1 of

Income Tax Assessment Act 1997 states that all work related expenses can be claimed as

deduction (Anon 2020). Deduction which can be claimed for the expenses must have been

spent by the taxpayer himself and it has not been reimbursed or it is directly related to the

earning of the income or all expenses made by the taxpayer must have been recorded as any

receipt to prove the expenses. While if the expenses are made for both the work and private

purpose than the expenses made for the work purpose can only be claimed as deduction (Feld

and Frey 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAX LAW

In case of business, claiming for deduction is available for most of the expenses which is

related to the business and there must be records of all the expenses paid. But all private related

expenses cannot be claimed for the deduction.

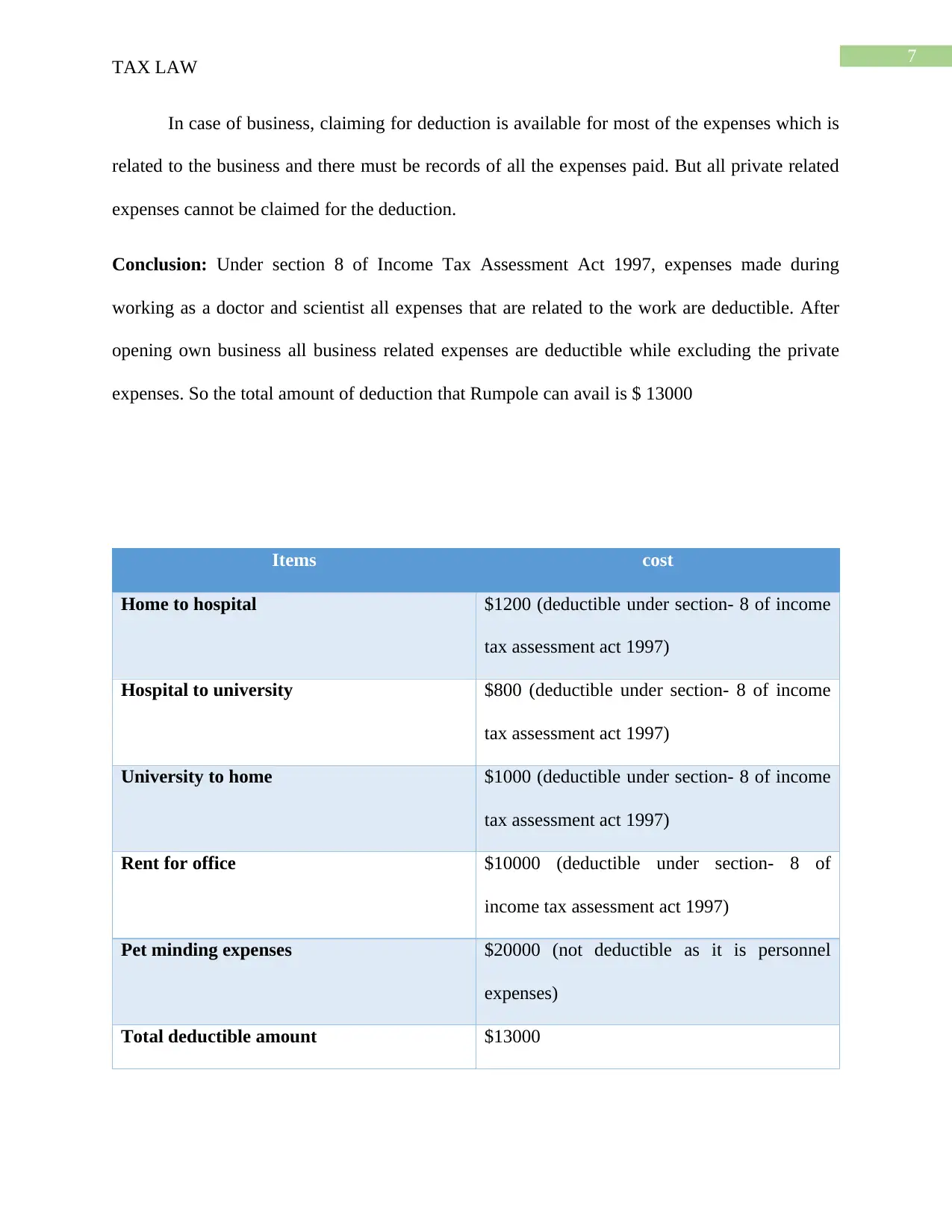

Conclusion: Under section 8 of Income Tax Assessment Act 1997, expenses made during

working as a doctor and scientist all expenses that are related to the work are deductible. After

opening own business all business related expenses are deductible while excluding the private

expenses. So the total amount of deduction that Rumpole can avail is $ 13000

Items cost

Home to hospital $1200 (deductible under section- 8 of income

tax assessment act 1997)

Hospital to university $800 (deductible under section- 8 of income

tax assessment act 1997)

University to home $1000 (deductible under section- 8 of income

tax assessment act 1997)

Rent for office $10000 (deductible under section- 8 of

income tax assessment act 1997)

Pet minding expenses $20000 (not deductible as it is personnel

expenses)

Total deductible amount $13000

TAX LAW

In case of business, claiming for deduction is available for most of the expenses which is

related to the business and there must be records of all the expenses paid. But all private related

expenses cannot be claimed for the deduction.

Conclusion: Under section 8 of Income Tax Assessment Act 1997, expenses made during

working as a doctor and scientist all expenses that are related to the work are deductible. After

opening own business all business related expenses are deductible while excluding the private

expenses. So the total amount of deduction that Rumpole can avail is $ 13000

Items cost

Home to hospital $1200 (deductible under section- 8 of income

tax assessment act 1997)

Hospital to university $800 (deductible under section- 8 of income

tax assessment act 1997)

University to home $1000 (deductible under section- 8 of income

tax assessment act 1997)

Rent for office $10000 (deductible under section- 8 of

income tax assessment act 1997)

Pet minding expenses $20000 (not deductible as it is personnel

expenses)

Total deductible amount $13000

8

TAX LAW

TAX LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAX LAW

Reference list

Ahmed, E., 2019. Tax law: A case of policy eroding compliance?. Centre for Tax System

Integrity (CTSI), Research School of Social Sciences, The Australian National University.

Anon, (2020). [online] Available at: https://www.ato.gov.au/www.ato.gov.au ›

Individuals › Income-and-deductions › Deductions-y... [Accessed 14 Jan. 2020].

Anon, (2020). [online] Available at: https://www.ato.gov.au/www.ato.gov.au ›

Business › Income-and-deductions-for-business [Accessed 14 Jan. 2020].

Ato.gov.au. (2020). Home page. [online] Available at: https://www.ato.gov.au/

[Accessed 14 Jan. 2020].

Braithwaite, J. and Wirth, A., 2019. Towards a framework for large business tax compliance.

Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The Australian

National University.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax Office

comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

TAX LAW

Reference list

Ahmed, E., 2019. Tax law: A case of policy eroding compliance?. Centre for Tax System

Integrity (CTSI), Research School of Social Sciences, The Australian National University.

Anon, (2020). [online] Available at: https://www.ato.gov.au/www.ato.gov.au ›

Individuals › Income-and-deductions › Deductions-y... [Accessed 14 Jan. 2020].

Anon, (2020). [online] Available at: https://www.ato.gov.au/www.ato.gov.au ›

Business › Income-and-deductions-for-business [Accessed 14 Jan. 2020].

Ato.gov.au. (2020). Home page. [online] Available at: https://www.ato.gov.au/

[Accessed 14 Jan. 2020].

Braithwaite, J. and Wirth, A., 2019. Towards a framework for large business tax compliance.

Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The Australian

National University.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax Office

comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAX LAW

Feld, L. and Frey, B., 2019. Tax compliance as the result of a psychological tax contract: The

role of incentives and responsive regulation. Centre for Tax System Integrity (CTSI), Research

School of Social Sciences, The Australian National University.

Harding v Commissioner of Taxation [2018] FCA 837

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian

Tax Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The

Australian National University.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJTR, 13, p.280.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

Sakurai, Y. and Braithwaite, V., 2019. Taxpayers' perceptions of the ideal tax adviser: Playing

safe or saving dollars?. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

Schenk, A., Thuronyi, V. and Cui, W., 2015. Value added tax. Cambridge University Press.

Spiro, P.S., 2018. Tax policy and the underground economy. In Size, causes and consequences

of the underground economy (pp. 179-201). Routledge.

TAX LAW

Feld, L. and Frey, B., 2019. Tax compliance as the result of a psychological tax contract: The

role of incentives and responsive regulation. Centre for Tax System Integrity (CTSI), Research

School of Social Sciences, The Australian National University.

Harding v Commissioner of Taxation [2018] FCA 837

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian

Tax Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The

Australian National University.

James, S., Sawyer, A. and Wallschutzky, I., 2015. Tax simplification: A review of initiatives in

Australia, New Zealand and the United Kingdom. eJTR, 13, p.280.

Mangioni, V., 2015. Land Tax in Australia: Fiscal reform of sub-national government.

Routledge.

Sakurai, Y. and Braithwaite, V., 2019. Taxpayers' perceptions of the ideal tax adviser: Playing

safe or saving dollars?. Centre for Tax System Integrity (CTSI), Research School of Social

Sciences, The Australian National University.

Schenk, A., Thuronyi, V. and Cui, W., 2015. Value added tax. Cambridge University Press.

Spiro, P.S., 2018. Tax policy and the underground economy. In Size, causes and consequences

of the underground economy (pp. 179-201). Routledge.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.