Calculating Partnership and Individual Tax Liabilities in Australia

VerifiedAdded on 2020/05/08

|8

|964

|64

Homework Assignment

AI Summary

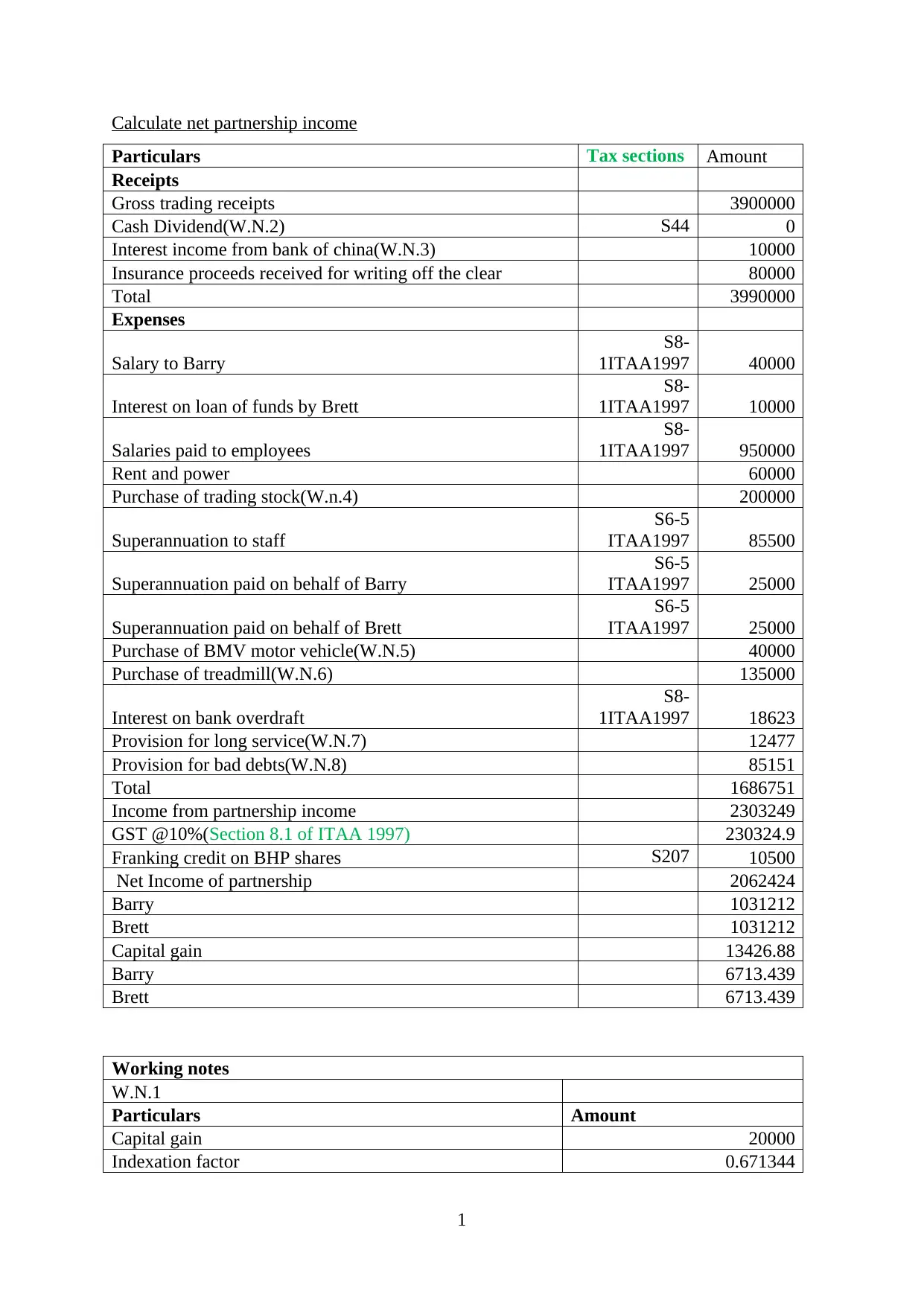

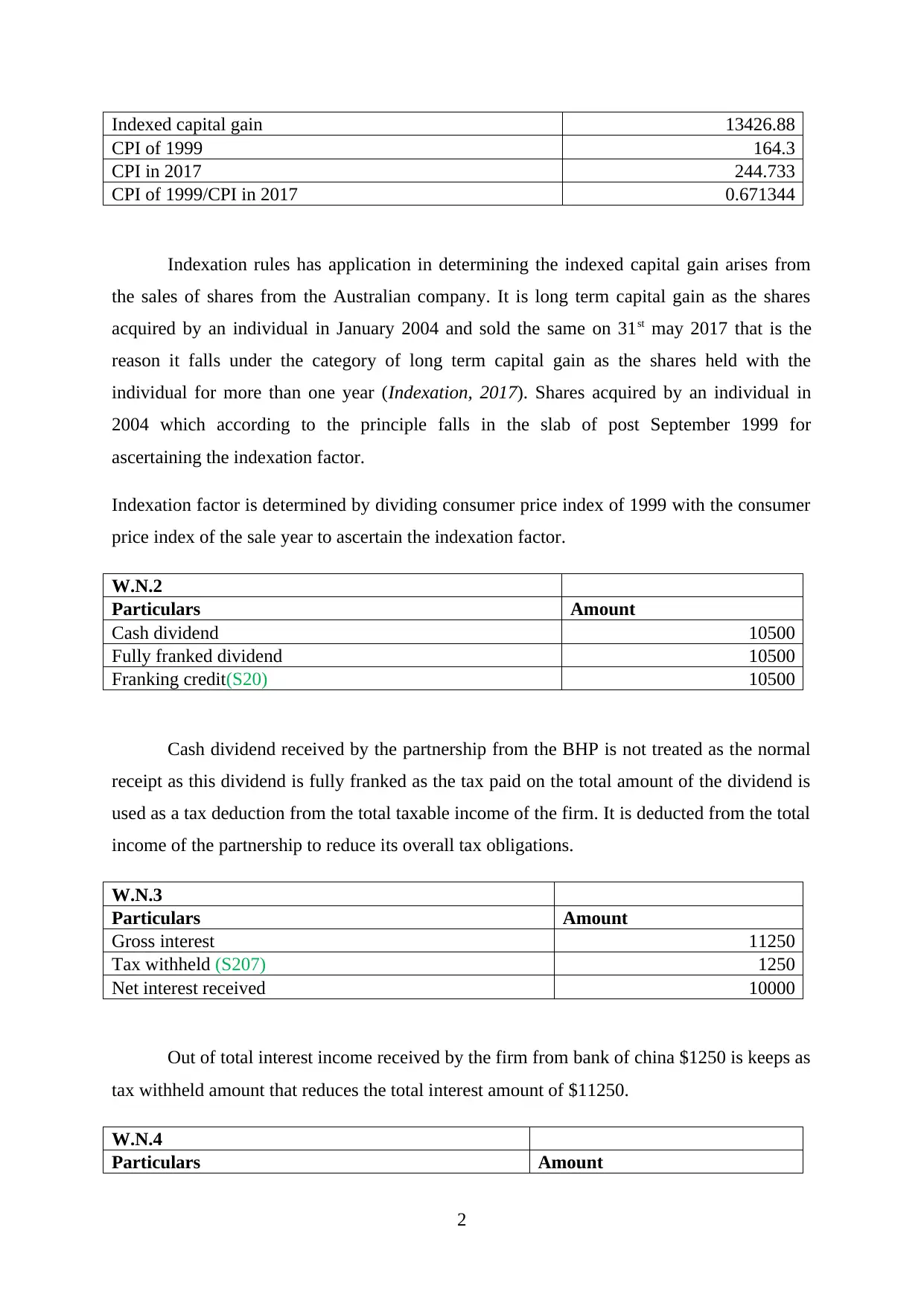

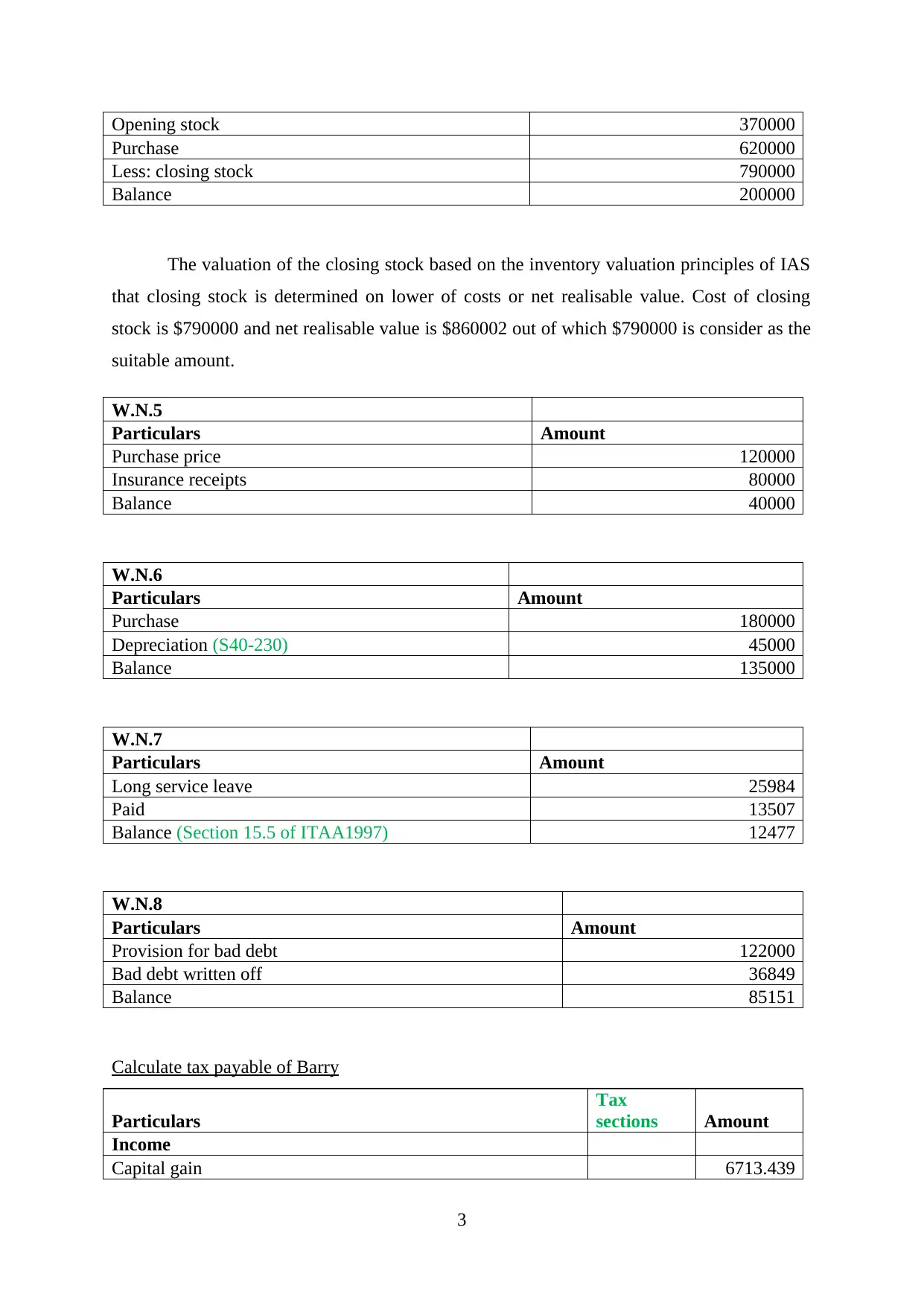

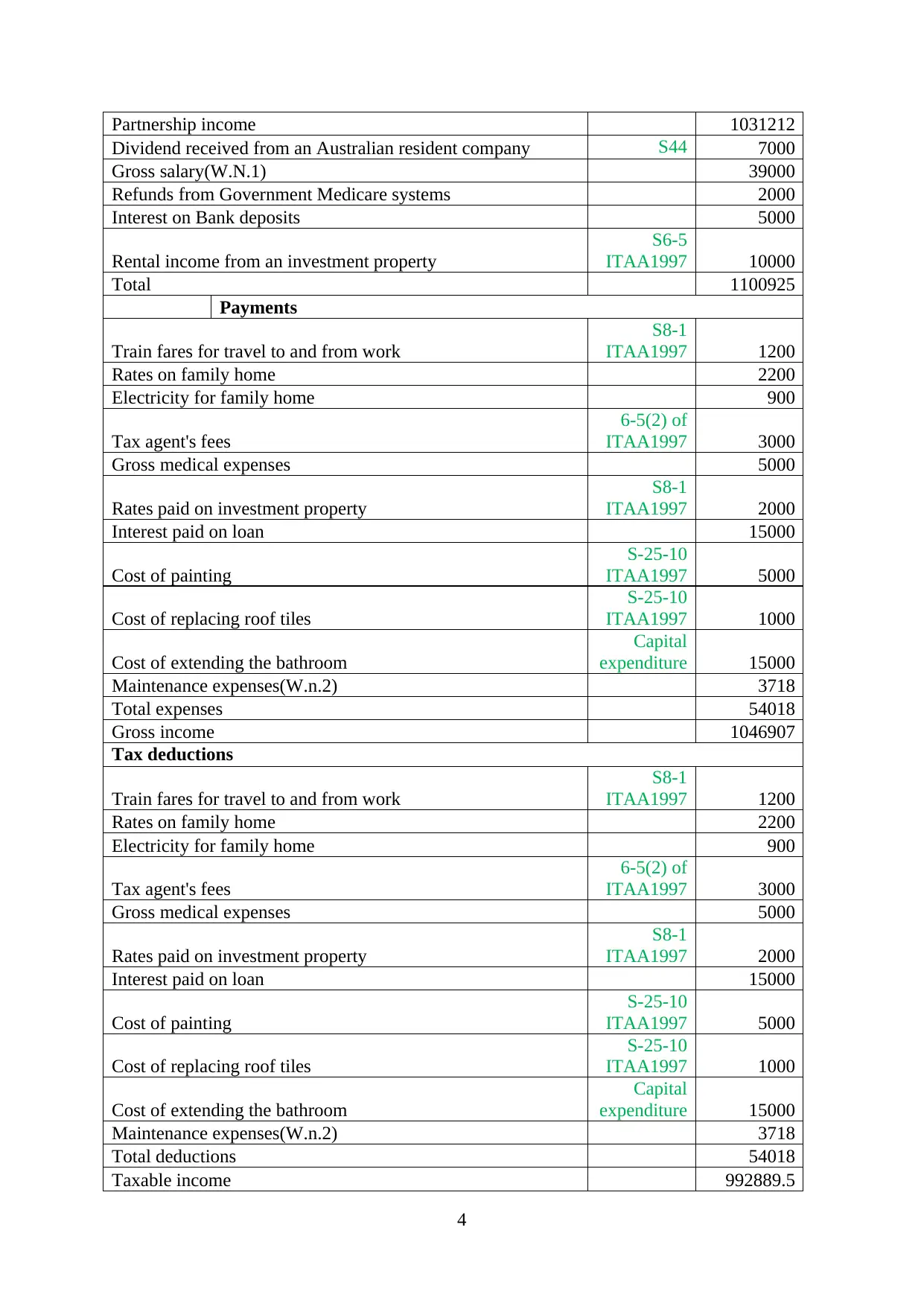

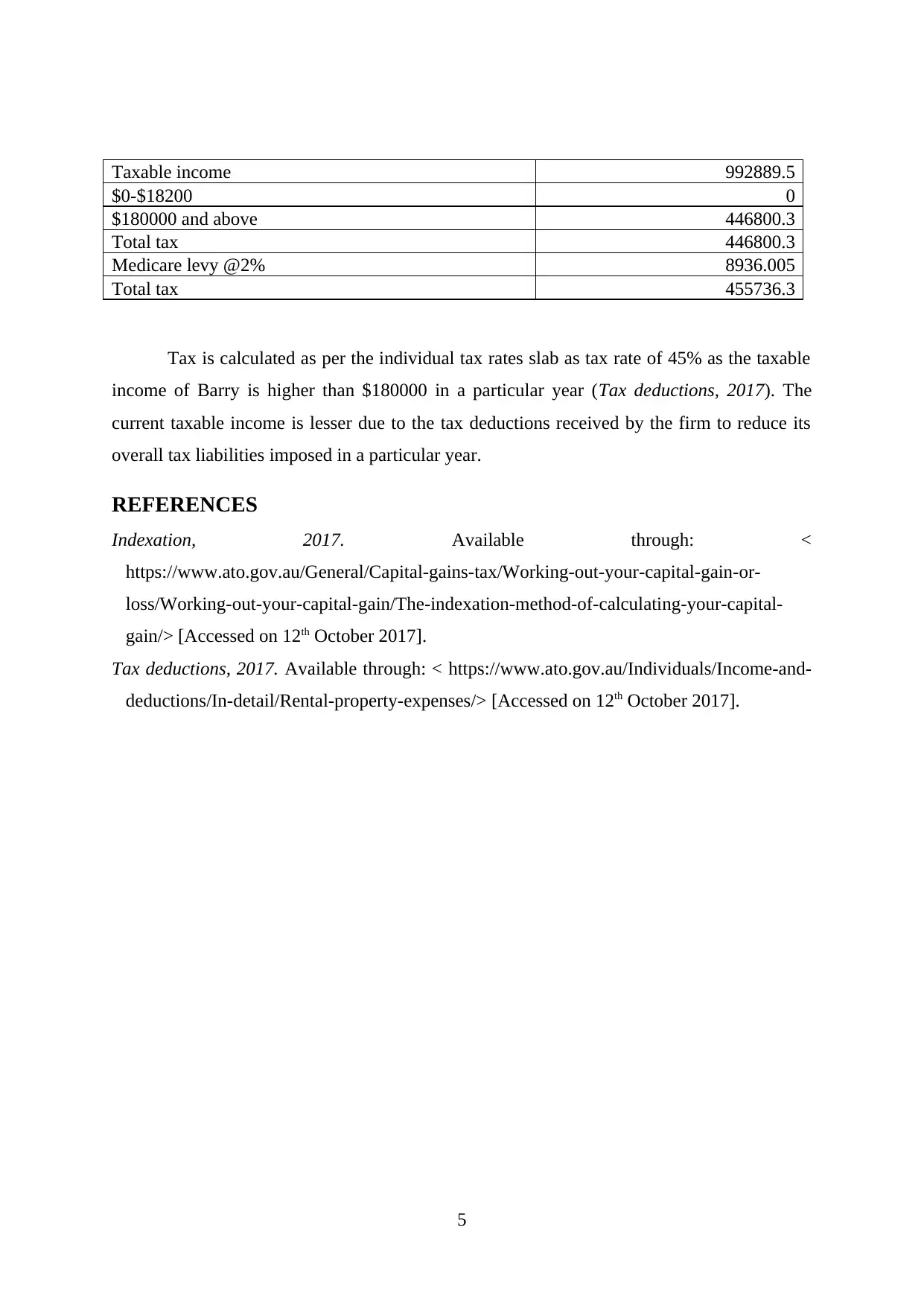

This assignment solution provides a comprehensive analysis of Australian taxation law, focusing on the calculation of net partnership income and the individual tax payable by Barry. The solution begins by calculating the net partnership income, detailing various receipts such as gross trading receipts, cash dividends, and interest income, along with corresponding expenses like salaries, rent, and depreciation. Several working notes are included to explain the calculations for capital gains, dividends, interest, stock valuation, and provisions for bad debts and long service leave. Following the partnership income calculation, the assignment calculates Barry's individual tax liability, outlining his income sources (capital gains, partnership income, salary, dividends, interest, and rental income) and allowable deductions (train fares, rates, electricity, tax agent fees, medical expenses, interest, and maintenance). The final calculation determines Barry's taxable income, total tax, and Medicare levy, adhering to the individual tax rates. The solution references relevant sections of the Income Tax Assessment Act 1997 and provides links to ATO resources for further clarification.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.