Taxation Law Assignment: Examination of Tax Principles and Cases

VerifiedAdded on 2020/04/01

|9

|1475

|37

Homework Assignment

AI Summary

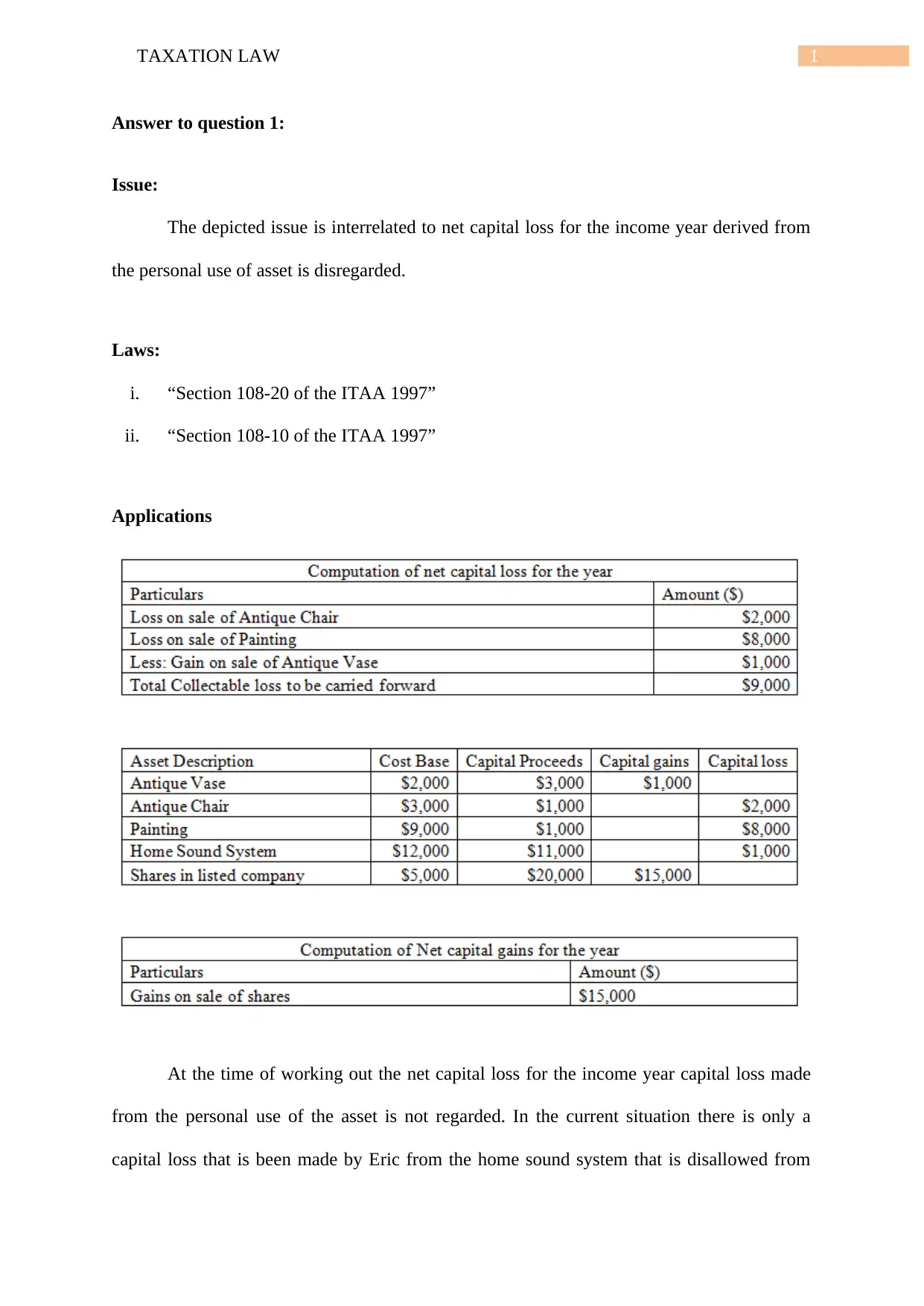

This taxation law assignment provides a comprehensive analysis of various tax-related issues under Australian law. It addresses topics such as net capital loss and its implications, the application of Fringe Benefit Tax (FBT), the division of income and losses in rental property scenarios, the principles of tax avoidance, and the tax treatment of proceeds from the sale of timber. The assignment explores relevant legislation, including the ITAA 1997 and FBTAA 1987, and examines key cases like McDonald v FC of T (1987) and IRC v Duke of Westminster (1936). The solutions offer detailed explanations and conclusions for each question, providing a clear understanding of the tax principles involved. The assignment covers scenarios involving both individual and business contexts, including primary producers and royalty income, offering a broad overview of Australian taxation law.

1 out of 9

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.